Impairment Analysis of Myer Holdings Ltd.

VerifiedAdded on 2020/02/24

|9

|1884

|133

AI Summary

This assignment requires a detailed analysis of Myer Holdings Ltd.'s impairment testing practices in accordance with Australian Accounting Standard Board (AASB) 136. Students must examine the company's methodology for identifying potential impairments, measuring the value in use and recoverable amount, and ultimately determining the amount of any impairment loss. The analysis should focus on Myer's flexibility and approach to these complex accounting standards.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING STANDARD AND REGULATION

Accounting standards and regulation

Name of the student

Name of the university

Author note

Accounting standards and regulation

Name of the student

Name of the university

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2ACCOUNTING STANDARDS AND REGULATION

Executive summary

The main objective of this report is to provide a clear concept regarding the AASB 136 on

Impairment of asset. The report will mainly focus on the Myer Holdings Ltd, an ASX listed

entity in Australia. The report will take into consideration the procedure f impairment,

evidence for impairment, information valid for successful test of impairment and the

management’s flexibility regarding the impairment test approach for the above mentioned

entity.

Executive summary

The main objective of this report is to provide a clear concept regarding the AASB 136 on

Impairment of asset. The report will mainly focus on the Myer Holdings Ltd, an ASX listed

entity in Australia. The report will take into consideration the procedure f impairment,

evidence for impairment, information valid for successful test of impairment and the

management’s flexibility regarding the impairment test approach for the above mentioned

entity.

3ACCOUNTING STANDARDS AND REGULATION

Table of Contents

ASIC Media release 17 -162......................................................................................................4

a. Evident of impairment with regard to Myer Holdings Ltd.................................................5

b. Process of determining impairment....................................................................................5

c. Information relating to determination of impairment.........................................................6

d. Flexibility Myer Holding Limited management for determining impairment...................7

Reference:..................................................................................................................................9

Table of Contents

ASIC Media release 17 -162......................................................................................................4

a. Evident of impairment with regard to Myer Holdings Ltd.................................................5

b. Process of determining impairment....................................................................................5

c. Information relating to determination of impairment.........................................................6

d. Flexibility Myer Holding Limited management for determining impairment...................7

Reference:..................................................................................................................................9

4ACCOUNTING STANDARDS AND REGULATION

ASIC Media release 17 -162

ASIC through their Media Release 17 – 162, approached that the all the organization

who are listed under the ASX, shall prepare their financial statement with the consideration

that it shall fulfil the purposes of the users. To be more specific, the financial report shall be

prepared with transparency and in accordance with the conceptual framework, so that the

statements can be understood by the external as well as the internal users clearly and it must

be able to fulfil the requirements of the users. It is observed by the ASIC that most of the

companies use improper assumptions while preparing their accounts for various transactions

like recognition if liabilities or revenues. As per the statement of John Price, the

commissioner of ASIC, the auditors shall analyse the accounting strategies with regard to the

statements of previous period (Aasb.gov.au 2017).

As per the AASB 136 on Impairment of assets seeks to assure that the assets in the

balance sheet shall not be carried out in the value which is more than the recoverable value of

the asset. For the purpose of impairment, the recoverable value and fair value of the asset less

the cost of disposal must be measured. The impairment loss is the difference between the

recoverable amount and the fair value of the asset. As per the AASB 136, the organization

shall carry out the impairment test at least once in each year. As per Para 12 – 14 under

AASB 136, some indications are considered for impairment of any asset. However, if any

indication for impairment is found with regard to any if the asset of the company, the

management shall immediately test the asset for impairment (Kabir and Rahman 2016).

Various indications of impairment are as follows –

Internal sources –

It is established that the asset became obsolete or it is damaged physically

The asset or the CGU of the asset is required to be restructured or it is observed that

the asset is kept in idle position for long run

While using the asset, the method of use is significantly changed.

External source –

The technological, environmental, market and legal circumstances of the operating

environment of the entity has been significantly changed

The asset’s carrying amount exceeds the capitalization of the market

Significant change is there with regard to the market rate of interest or market return

ASIC Media release 17 -162

ASIC through their Media Release 17 – 162, approached that the all the organization

who are listed under the ASX, shall prepare their financial statement with the consideration

that it shall fulfil the purposes of the users. To be more specific, the financial report shall be

prepared with transparency and in accordance with the conceptual framework, so that the

statements can be understood by the external as well as the internal users clearly and it must

be able to fulfil the requirements of the users. It is observed by the ASIC that most of the

companies use improper assumptions while preparing their accounts for various transactions

like recognition if liabilities or revenues. As per the statement of John Price, the

commissioner of ASIC, the auditors shall analyse the accounting strategies with regard to the

statements of previous period (Aasb.gov.au 2017).

As per the AASB 136 on Impairment of assets seeks to assure that the assets in the

balance sheet shall not be carried out in the value which is more than the recoverable value of

the asset. For the purpose of impairment, the recoverable value and fair value of the asset less

the cost of disposal must be measured. The impairment loss is the difference between the

recoverable amount and the fair value of the asset. As per the AASB 136, the organization

shall carry out the impairment test at least once in each year. As per Para 12 – 14 under

AASB 136, some indications are considered for impairment of any asset. However, if any

indication for impairment is found with regard to any if the asset of the company, the

management shall immediately test the asset for impairment (Kabir and Rahman 2016).

Various indications of impairment are as follows –

Internal sources –

It is established that the asset became obsolete or it is damaged physically

The asset or the CGU of the asset is required to be restructured or it is observed that

the asset is kept in idle position for long run

While using the asset, the method of use is significantly changed.

External source –

The technological, environmental, market and legal circumstances of the operating

environment of the entity has been significantly changed

The asset’s carrying amount exceeds the capitalization of the market

Significant change is there with regard to the market rate of interest or market return

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5ACCOUNTING STANDARDS AND REGULATION

Owing to normal wear and tear the value of the asset changed considerably.

a. Evident of impairment with regard to Myer Holdings Ltd

Asset flow – if the impairment test is carried out taking into consideration the asset

flow of various stores of Myer, it can be recognized that that no indication is there

with regard to impairment for any of the stores as there is no significant change

noticed for past few years. Therefore, indication of impairment is not established.

Turnover of asset – taking into consideration the turnover of assets, it is identified

that the turnover is ranged from 1.40 to 1.80. Therefore, significant shift is not there

that can establish the indication of impairment (Investor.myer.com.au 2017).

However, though above tests do not recognize any asset for impairment, it identified

that to compete with the Amazon, Myer planned to change the outlook of the departmental

store at Frankton. Under the planning they want to change the traditional black and white get-

up of the store with the vibrant yellow colour. Further, the uniform of the store staffs will be

changed from the traditional one. Moreover, the storage system will be altered in such way

that will give more space for storage. All these significances will be regarded as partial

restructure as per AASB 136, which is regarded as the internal source of information for the

indication of impairment of the store (Malone, Tarca and Wee 2015). Therefore, the store in

Frankton shall be tested for impairment.

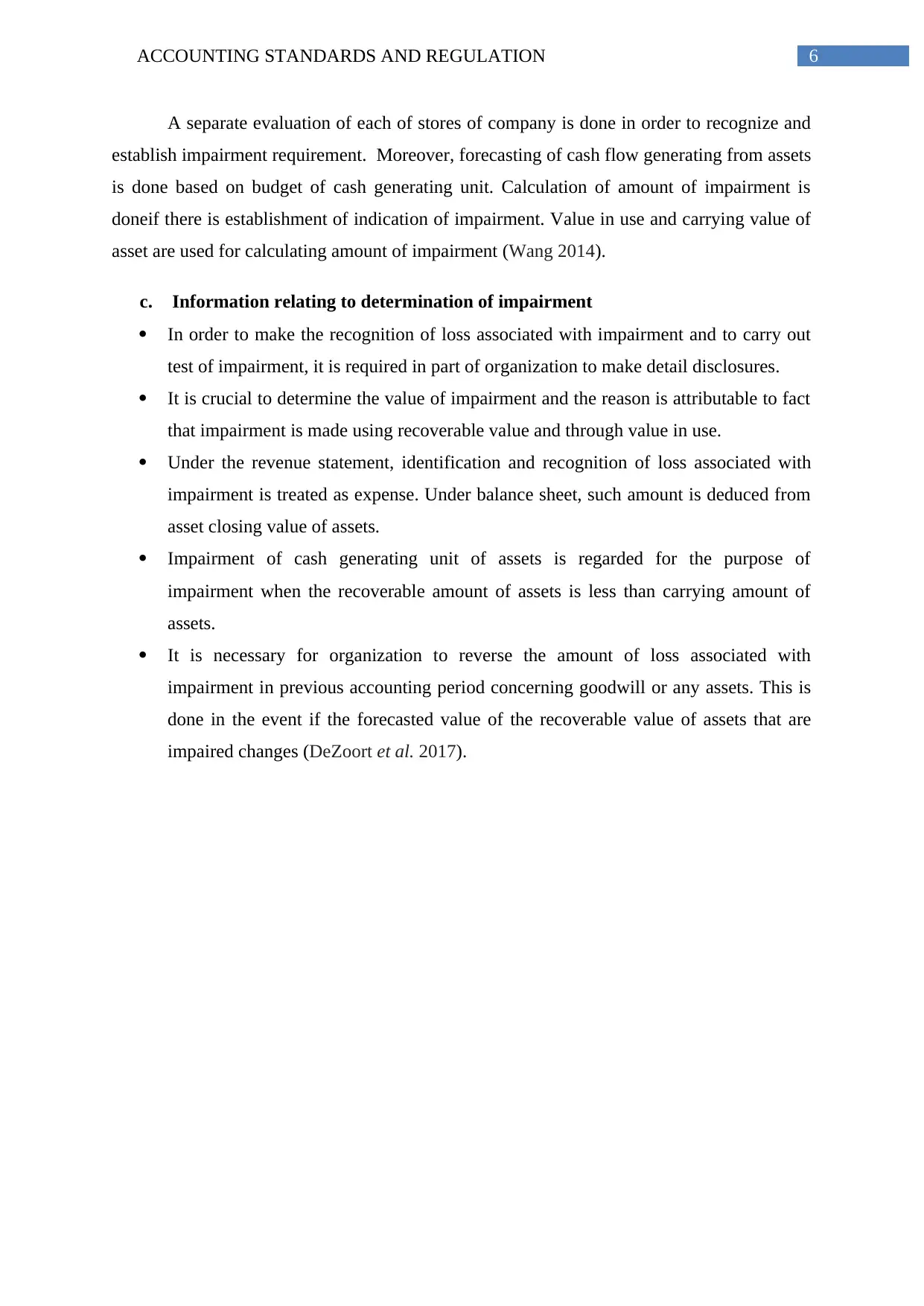

b. Process of determining impairment

For calculating value or amount of impairment of assets when there is any indication

of impairment of any assets of organization, in such event, it is essential to measure the

carrying value of assets and value in use. The approval of assets by the management of

company regarding assets forms the basis of forecasting the cash flow generated by assets.

Forecast of cash flow is generally for long-tem. Management make use of terminal rate of

growth for calculation of cash flow for long time that is five years (Christensen et al. 2015).

Following assumptions have been made for the calculation of cash flow generated by assets

and they are as follows:

Pre discount rate has been assumed to be at 14.4%

Terminal growth rate is assumed to be at 2.5%

Rate of operating margin concerning goods profit are assumed to be at 39.5%.

Owing to normal wear and tear the value of the asset changed considerably.

a. Evident of impairment with regard to Myer Holdings Ltd

Asset flow – if the impairment test is carried out taking into consideration the asset

flow of various stores of Myer, it can be recognized that that no indication is there

with regard to impairment for any of the stores as there is no significant change

noticed for past few years. Therefore, indication of impairment is not established.

Turnover of asset – taking into consideration the turnover of assets, it is identified

that the turnover is ranged from 1.40 to 1.80. Therefore, significant shift is not there

that can establish the indication of impairment (Investor.myer.com.au 2017).

However, though above tests do not recognize any asset for impairment, it identified

that to compete with the Amazon, Myer planned to change the outlook of the departmental

store at Frankton. Under the planning they want to change the traditional black and white get-

up of the store with the vibrant yellow colour. Further, the uniform of the store staffs will be

changed from the traditional one. Moreover, the storage system will be altered in such way

that will give more space for storage. All these significances will be regarded as partial

restructure as per AASB 136, which is regarded as the internal source of information for the

indication of impairment of the store (Malone, Tarca and Wee 2015). Therefore, the store in

Frankton shall be tested for impairment.

b. Process of determining impairment

For calculating value or amount of impairment of assets when there is any indication

of impairment of any assets of organization, in such event, it is essential to measure the

carrying value of assets and value in use. The approval of assets by the management of

company regarding assets forms the basis of forecasting the cash flow generated by assets.

Forecast of cash flow is generally for long-tem. Management make use of terminal rate of

growth for calculation of cash flow for long time that is five years (Christensen et al. 2015).

Following assumptions have been made for the calculation of cash flow generated by assets

and they are as follows:

Pre discount rate has been assumed to be at 14.4%

Terminal growth rate is assumed to be at 2.5%

Rate of operating margin concerning goods profit are assumed to be at 39.5%.

6ACCOUNTING STANDARDS AND REGULATION

A separate evaluation of each of stores of company is done in order to recognize and

establish impairment requirement. Moreover, forecasting of cash flow generating from assets

is done based on budget of cash generating unit. Calculation of amount of impairment is

doneif there is establishment of indication of impairment. Value in use and carrying value of

asset are used for calculating amount of impairment (Wang 2014).

c. Information relating to determination of impairment

In order to make the recognition of loss associated with impairment and to carry out

test of impairment, it is required in part of organization to make detail disclosures.

It is crucial to determine the value of impairment and the reason is attributable to fact

that impairment is made using recoverable value and through value in use.

Under the revenue statement, identification and recognition of loss associated with

impairment is treated as expense. Under balance sheet, such amount is deduced from

asset closing value of assets.

Impairment of cash generating unit of assets is regarded for the purpose of

impairment when the recoverable amount of assets is less than carrying amount of

assets.

It is necessary for organization to reverse the amount of loss associated with

impairment in previous accounting period concerning goodwill or any assets. This is

done in the event if the forecasted value of the recoverable value of assets that are

impaired changes (DeZoort et al. 2017).

A separate evaluation of each of stores of company is done in order to recognize and

establish impairment requirement. Moreover, forecasting of cash flow generating from assets

is done based on budget of cash generating unit. Calculation of amount of impairment is

doneif there is establishment of indication of impairment. Value in use and carrying value of

asset are used for calculating amount of impairment (Wang 2014).

c. Information relating to determination of impairment

In order to make the recognition of loss associated with impairment and to carry out

test of impairment, it is required in part of organization to make detail disclosures.

It is crucial to determine the value of impairment and the reason is attributable to fact

that impairment is made using recoverable value and through value in use.

Under the revenue statement, identification and recognition of loss associated with

impairment is treated as expense. Under balance sheet, such amount is deduced from

asset closing value of assets.

Impairment of cash generating unit of assets is regarded for the purpose of

impairment when the recoverable amount of assets is less than carrying amount of

assets.

It is necessary for organization to reverse the amount of loss associated with

impairment in previous accounting period concerning goodwill or any assets. This is

done in the event if the forecasted value of the recoverable value of assets that are

impaired changes (DeZoort et al. 2017).

7ACCOUNTING STANDARDS AND REGULATION

d. Flexibility Myer Holding Limited management for determining impairment

It is not essential for management of company to be expert in accounting as per

Australian securities and investment commission. In such cases, management of organisation

can seek help from accounting firms or by hiring accounting experts. When the forecasted or

projected value relating to accounting does not tally with the required or actual outcome, it is

required by them to discuss matters with accounts by conducting in depth analysis. Data in

financial statements can be presented with more clarity when such analysis is conducted

(Pacter 2014).

As per the requirement of Australian accounting standard board 136, the facts

ascertained in the given case of Myer Holdings Ltd. In such case, it becomes essential for

management to carry out test of impairments at least once in a year. Furthermore, for

measuring the amount of loss related to impairment in the event of any indication of

d. Flexibility Myer Holding Limited management for determining impairment

It is not essential for management of company to be expert in accounting as per

Australian securities and investment commission. In such cases, management of organisation

can seek help from accounting firms or by hiring accounting experts. When the forecasted or

projected value relating to accounting does not tally with the required or actual outcome, it is

required by them to discuss matters with accounts by conducting in depth analysis. Data in

financial statements can be presented with more clarity when such analysis is conducted

(Pacter 2014).

As per the requirement of Australian accounting standard board 136, the facts

ascertained in the given case of Myer Holdings Ltd. In such case, it becomes essential for

management to carry out test of impairments at least once in a year. Furthermore, for

measuring the amount of loss related to impairment in the event of any indication of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8ACCOUNTING STANDARDS AND REGULATION

impairment, it I required by company to instantly measure the value in use and recoverable

value. From the analysis of case, it is regarded that for carrying out impairment tests, Myer

Holdings Ltd is very adjustable. Survey regarding carrying value of assets is conducted by

organization for each of store and existing signs of impairment is distinguished (Albu et al.

2014). Test of impedance is guaranteed by organization as per AASB 136 fundamentals.

Moreover, various levels of certainties such as estimation of impairment is decided by

organization. Therefore, it can be concluded that company’s management is flexible when it

comes to determine the loss of impairment and carrying out impairment tests.

impairment, it I required by company to instantly measure the value in use and recoverable

value. From the analysis of case, it is regarded that for carrying out impairment tests, Myer

Holdings Ltd is very adjustable. Survey regarding carrying value of assets is conducted by

organization for each of store and existing signs of impairment is distinguished (Albu et al.

2014). Test of impedance is guaranteed by organization as per AASB 136 fundamentals.

Moreover, various levels of certainties such as estimation of impairment is decided by

organization. Therefore, it can be concluded that company’s management is flexible when it

comes to determine the loss of impairment and carrying out impairment tests.

9ACCOUNTING STANDARDS AND REGULATION

Reference:

Aasb.gov.au. 2017. Australian Accounting Standards Board (AASB) - Home. [online]

Available at: http://www.aasb.gov.au/ [Accessed 26 Aug. 2017].

Albu, C.N., Albu, N. and Alexander, D., 2014. When global accounting standards meet the

local context—Insights from an emerging economy. Critical Perspectives on

Accounting, 25(6), pp.489-510.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting

Review, 24(1), pp.31-61.

DeZoort, F.T., Wilkins, A. and Justice, S.E., 2017. Call for papers: The limits of accounting

regulation. Journal of Accounting and Public Policy, 45, p.30Z.

Investor.myer.com.au. 2017. Myer Investor Relations. [online] Available at:

http://investor.myer.com.au/Investor-Centre/ [Accessed 26 Aug. 2017].

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

Malone, L., Tarca, A. and Wee, M., 2015. Non-GAAP earnings disclosures and

IFRS. Accounting and Finance.

Pacter, P., 2014. Global accounting standards-from vision to reality. The CPA Journal, 84(1),

p.6.Page, M., 2014. Business models as a basis for regulation of financial reporting. Journal

of Management & Governance, 18(3), pp.683-695.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

Reference:

Aasb.gov.au. 2017. Australian Accounting Standards Board (AASB) - Home. [online]

Available at: http://www.aasb.gov.au/ [Accessed 26 Aug. 2017].

Albu, C.N., Albu, N. and Alexander, D., 2014. When global accounting standards meet the

local context—Insights from an emerging economy. Critical Perspectives on

Accounting, 25(6), pp.489-510.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting

Review, 24(1), pp.31-61.

DeZoort, F.T., Wilkins, A. and Justice, S.E., 2017. Call for papers: The limits of accounting

regulation. Journal of Accounting and Public Policy, 45, p.30Z.

Investor.myer.com.au. 2017. Myer Investor Relations. [online] Available at:

http://investor.myer.com.au/Investor-Centre/ [Accessed 26 Aug. 2017].

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

Malone, L., Tarca, A. and Wee, M., 2015. Non-GAAP earnings disclosures and

IFRS. Accounting and Finance.

Pacter, P., 2014. Global accounting standards-from vision to reality. The CPA Journal, 84(1),

p.6.Page, M., 2014. Business models as a basis for regulation of financial reporting. Journal

of Management & Governance, 18(3), pp.683-695.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.