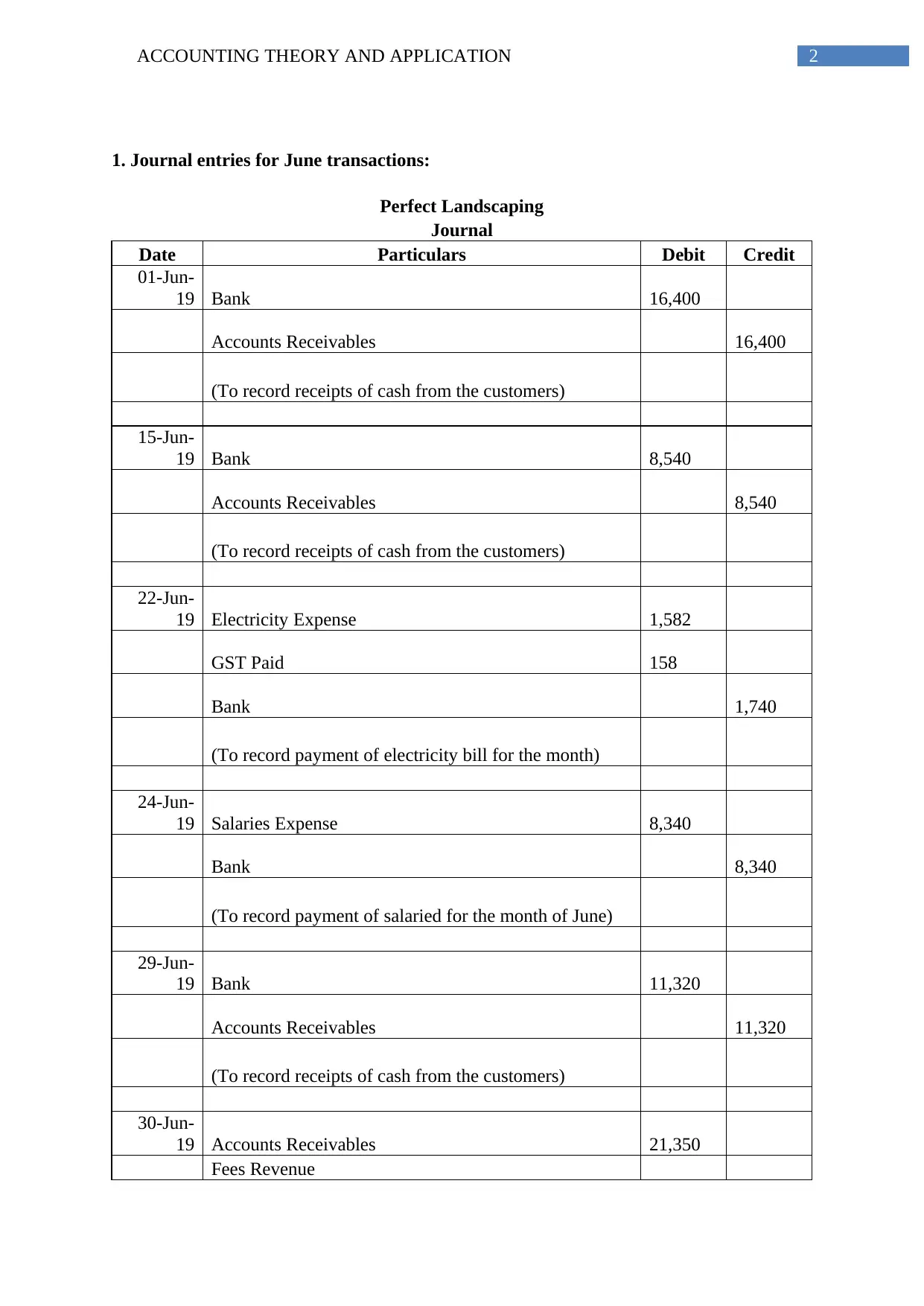

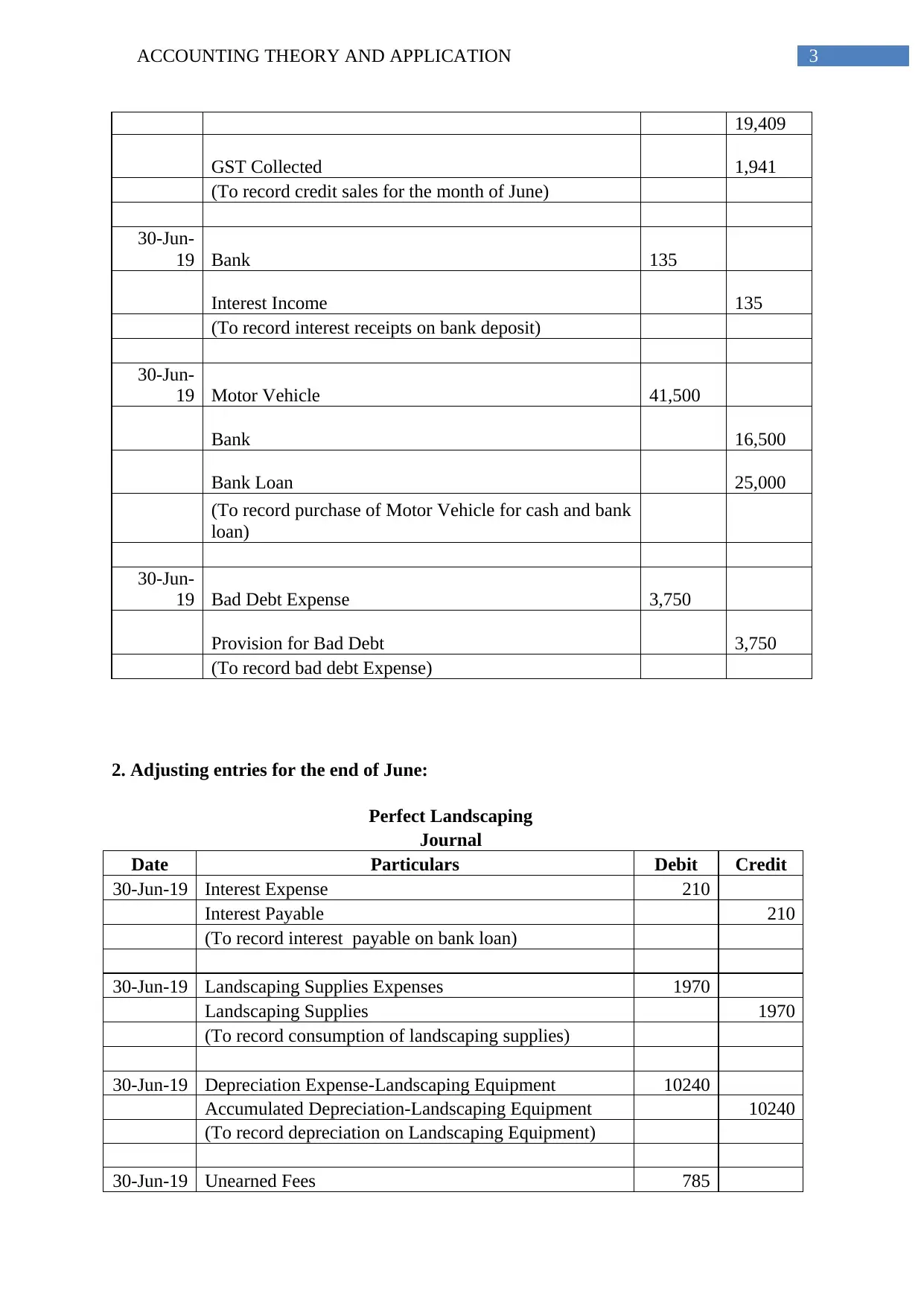

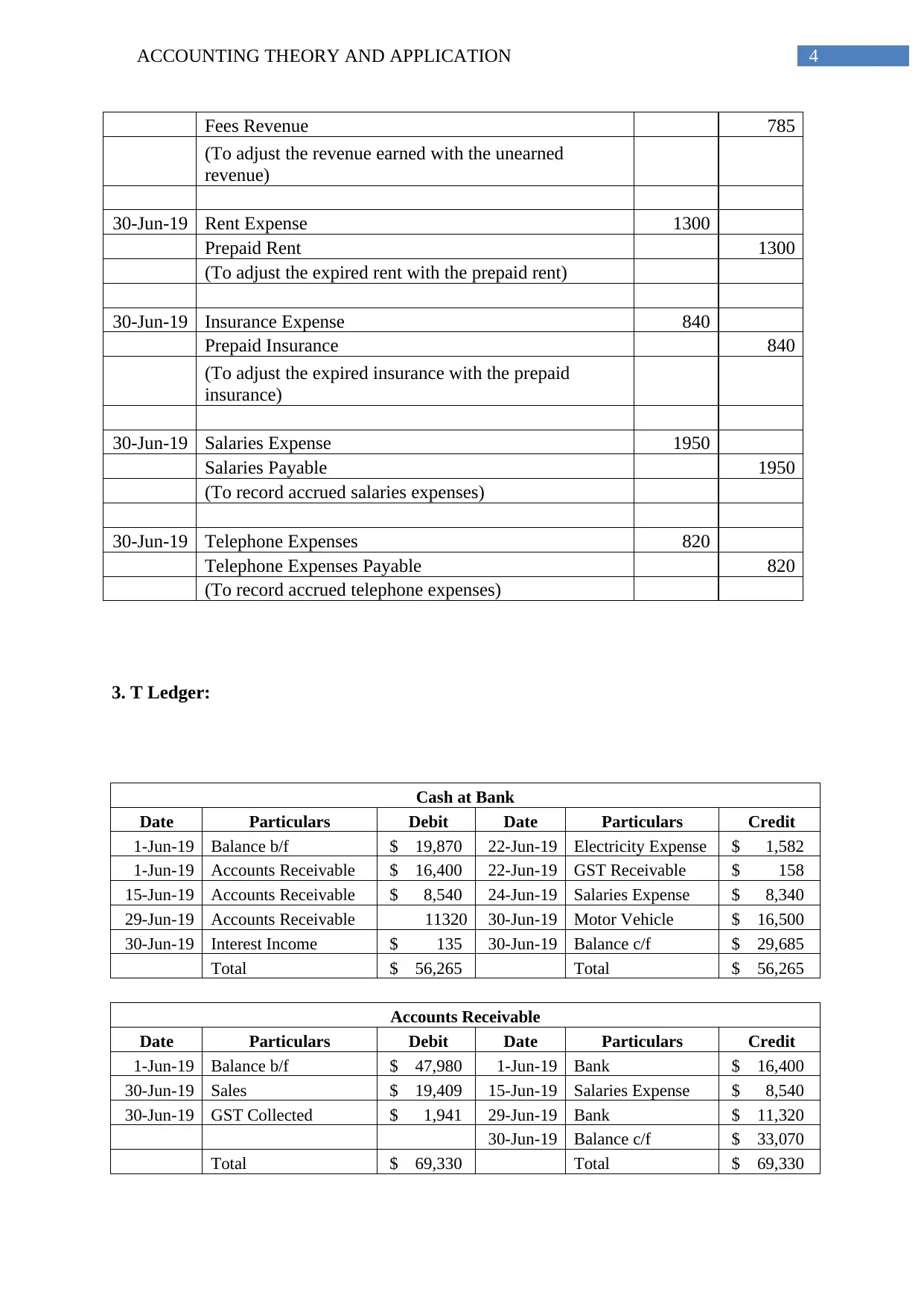

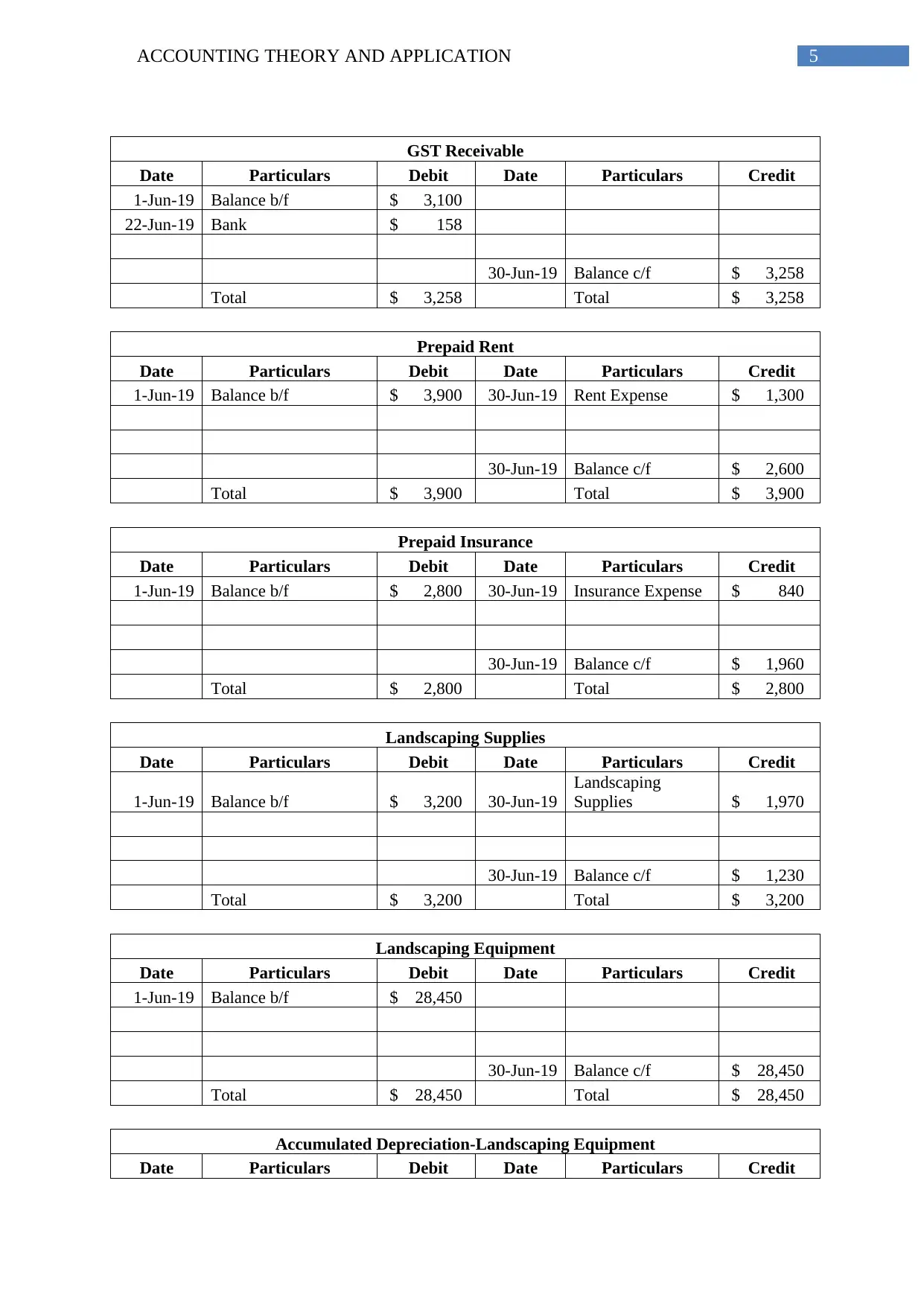

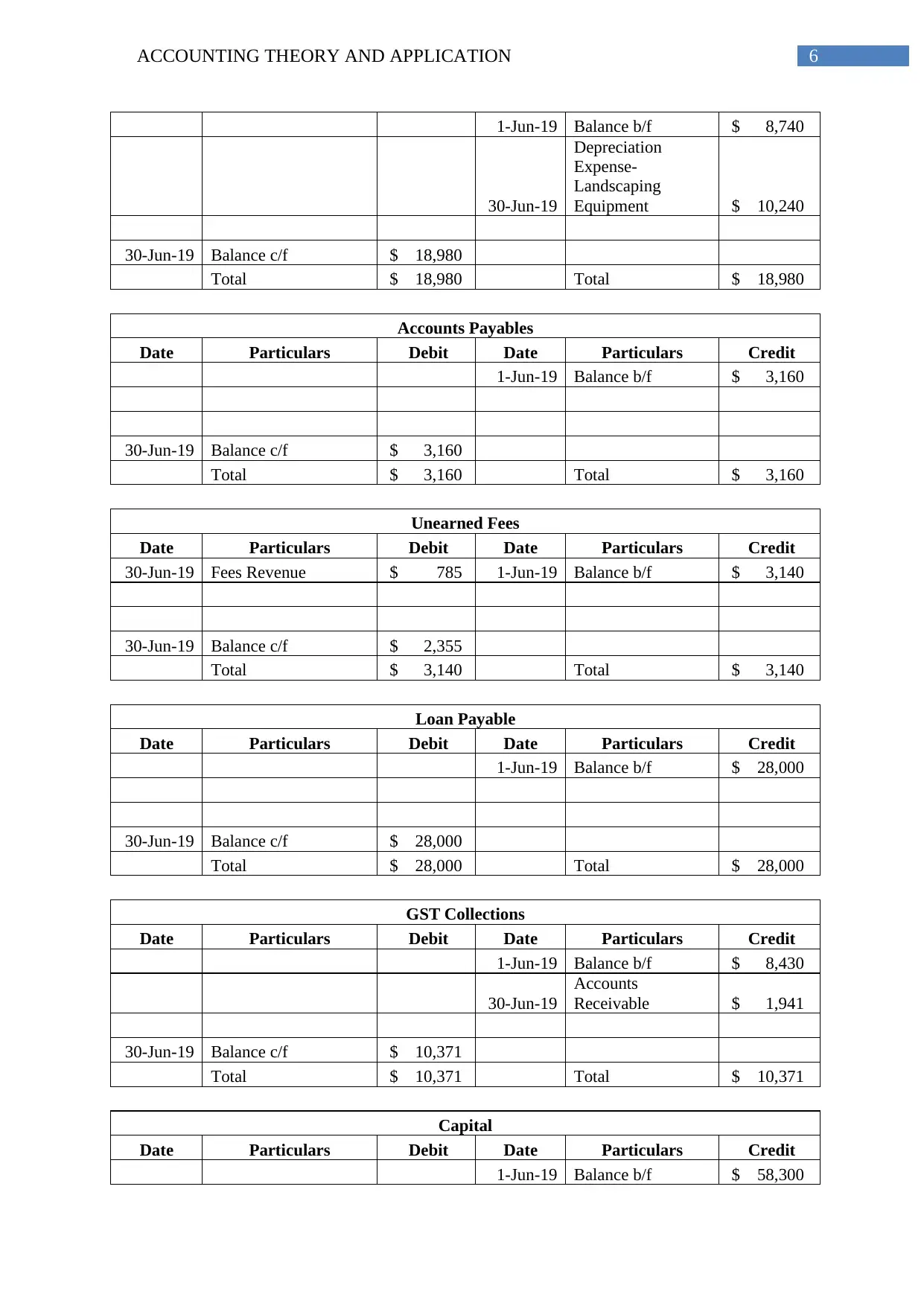

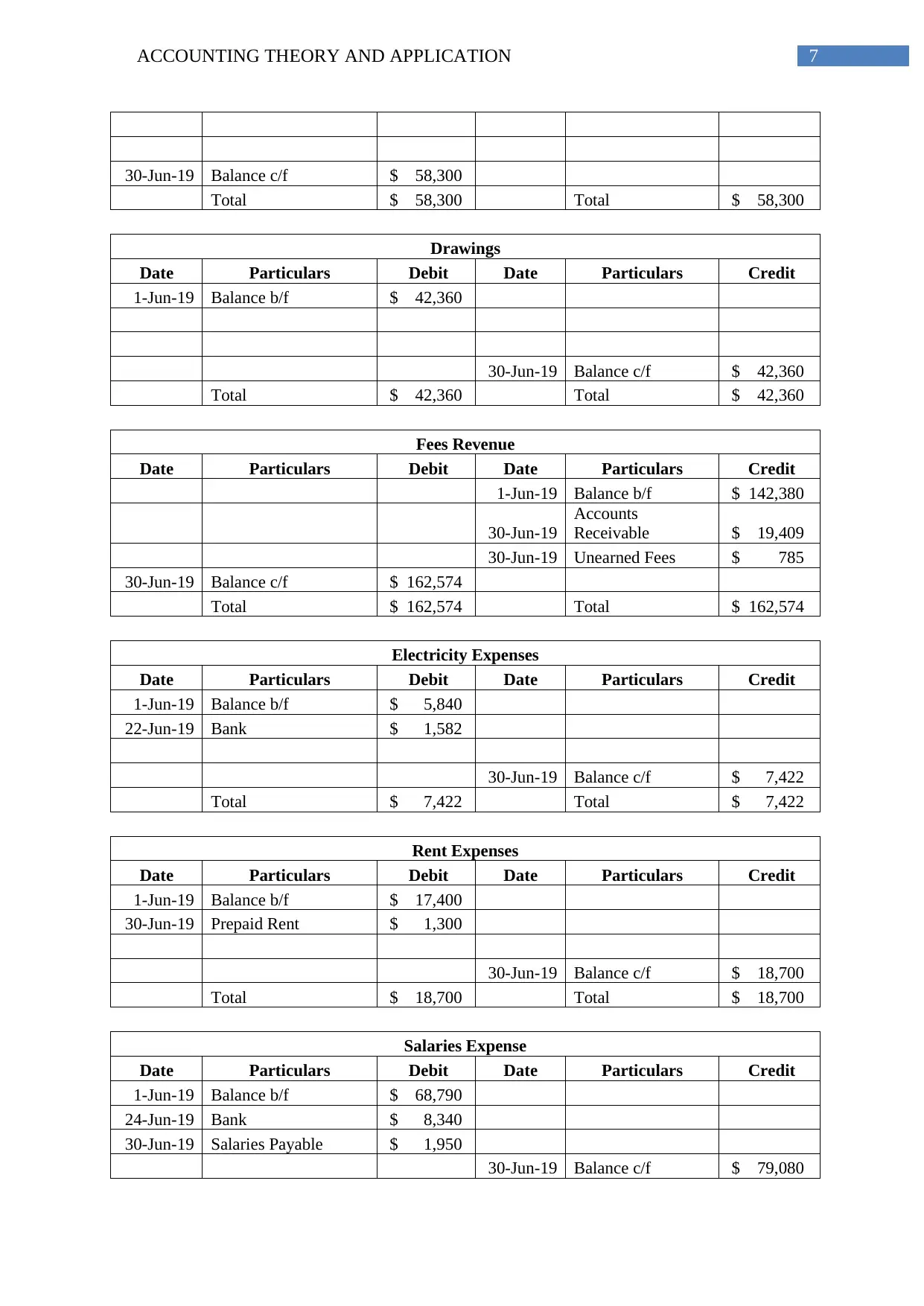

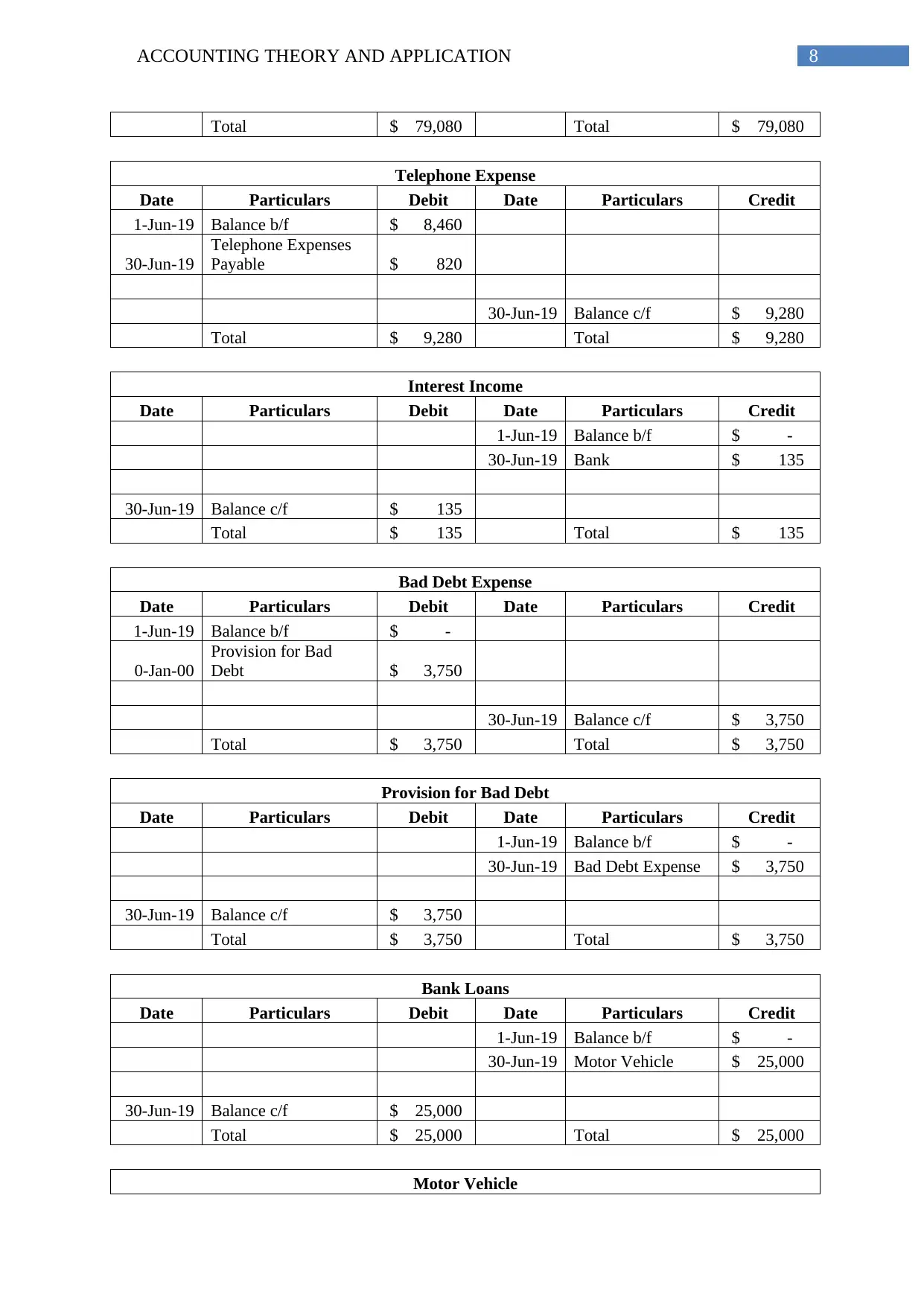

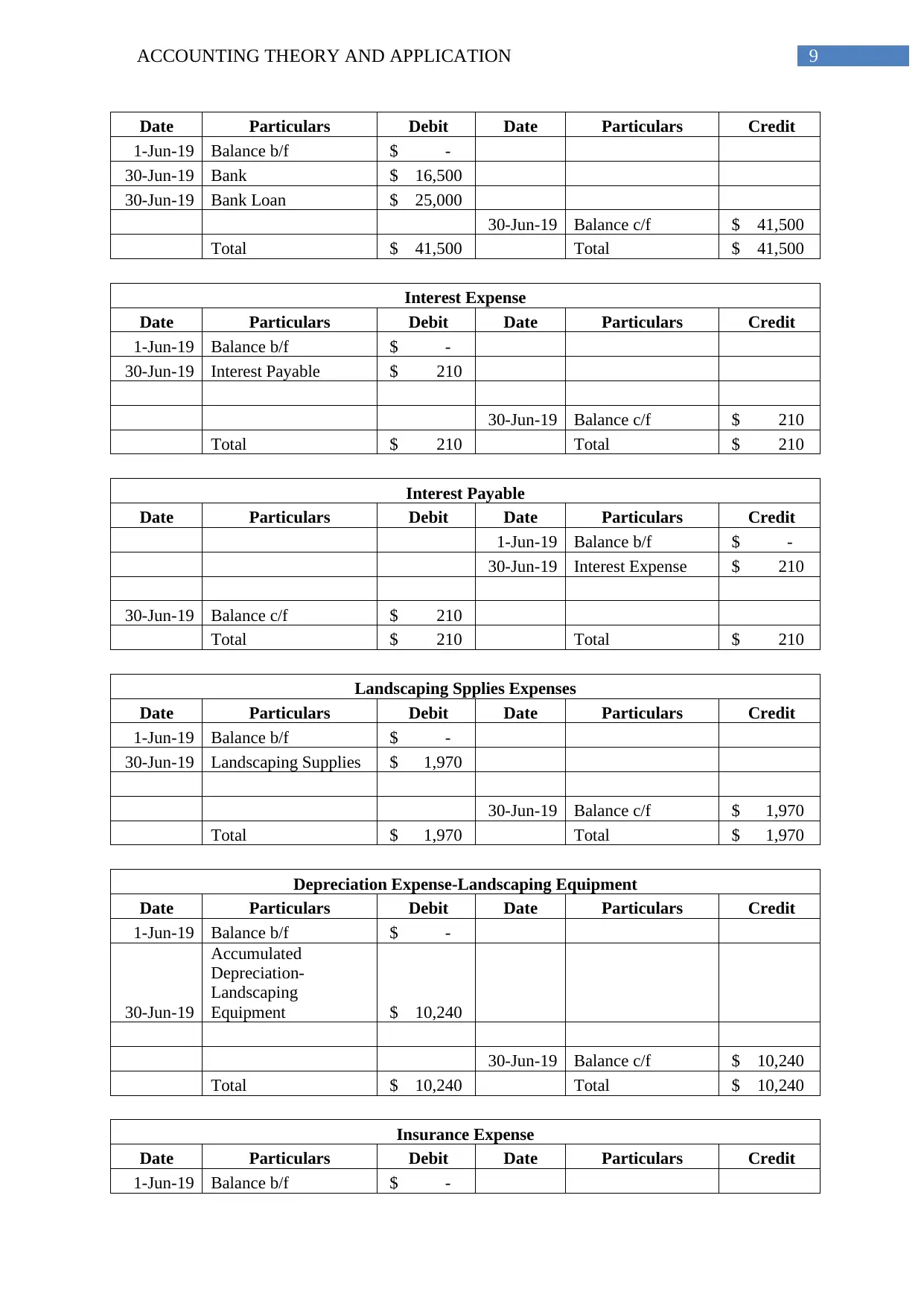

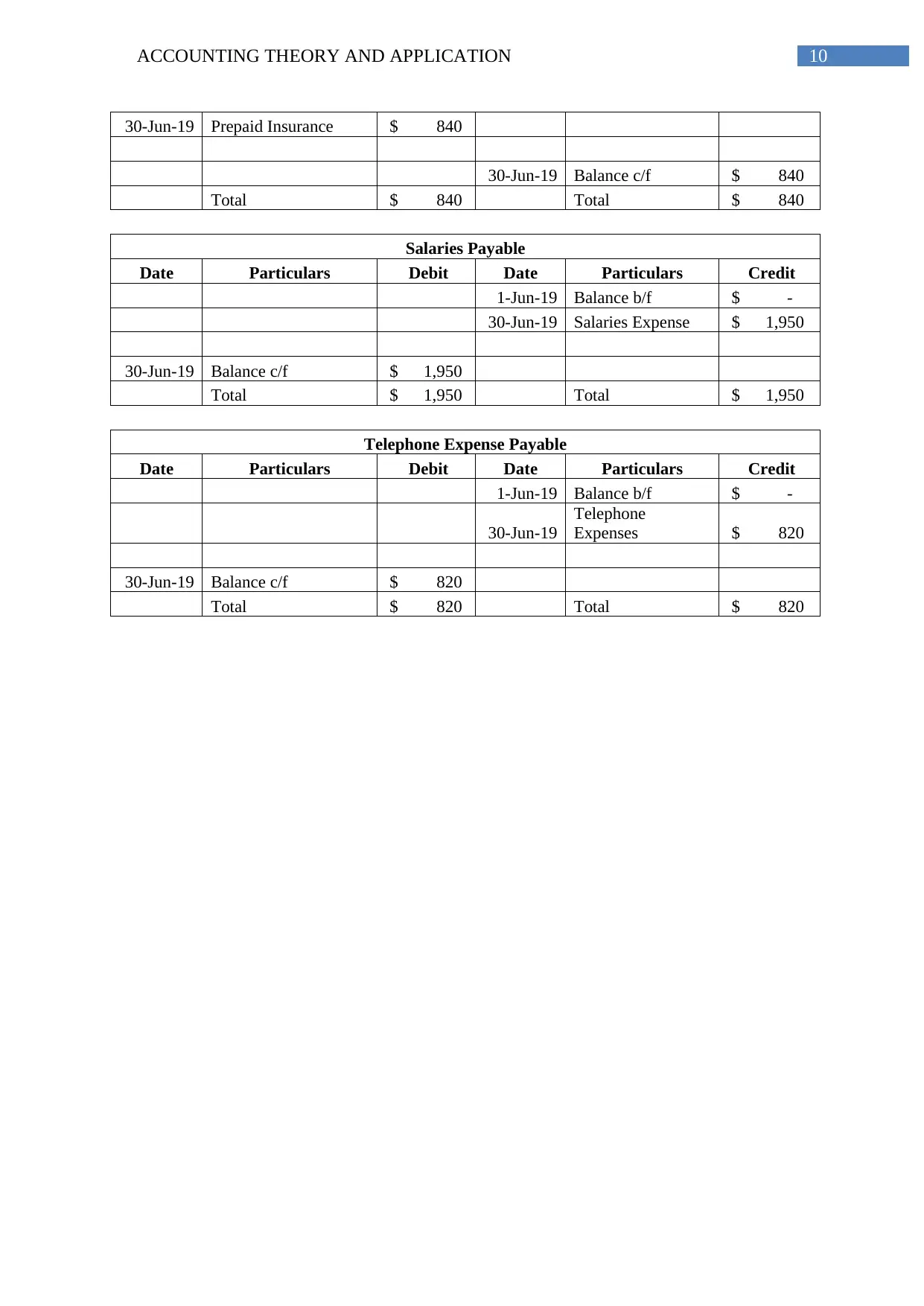

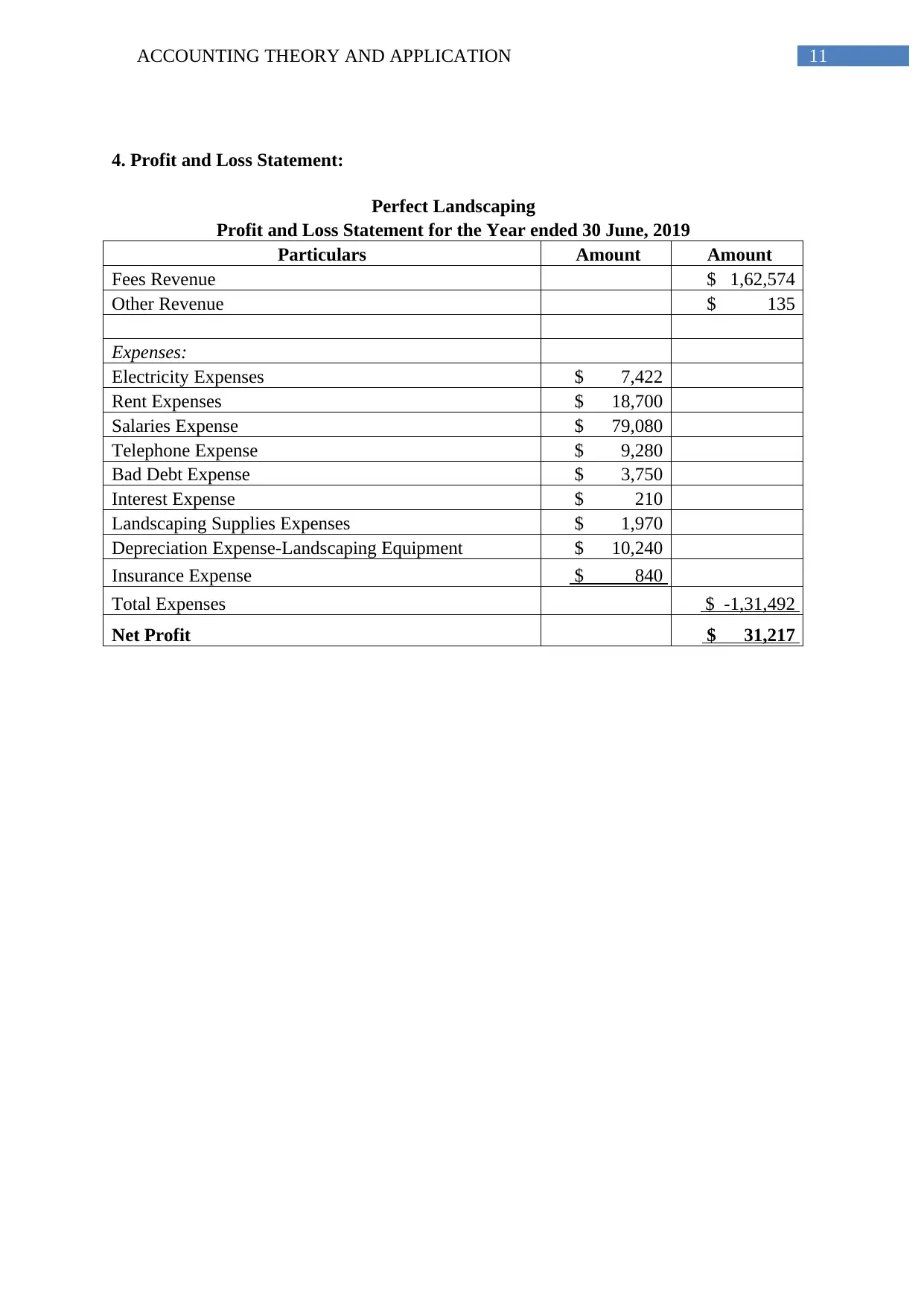

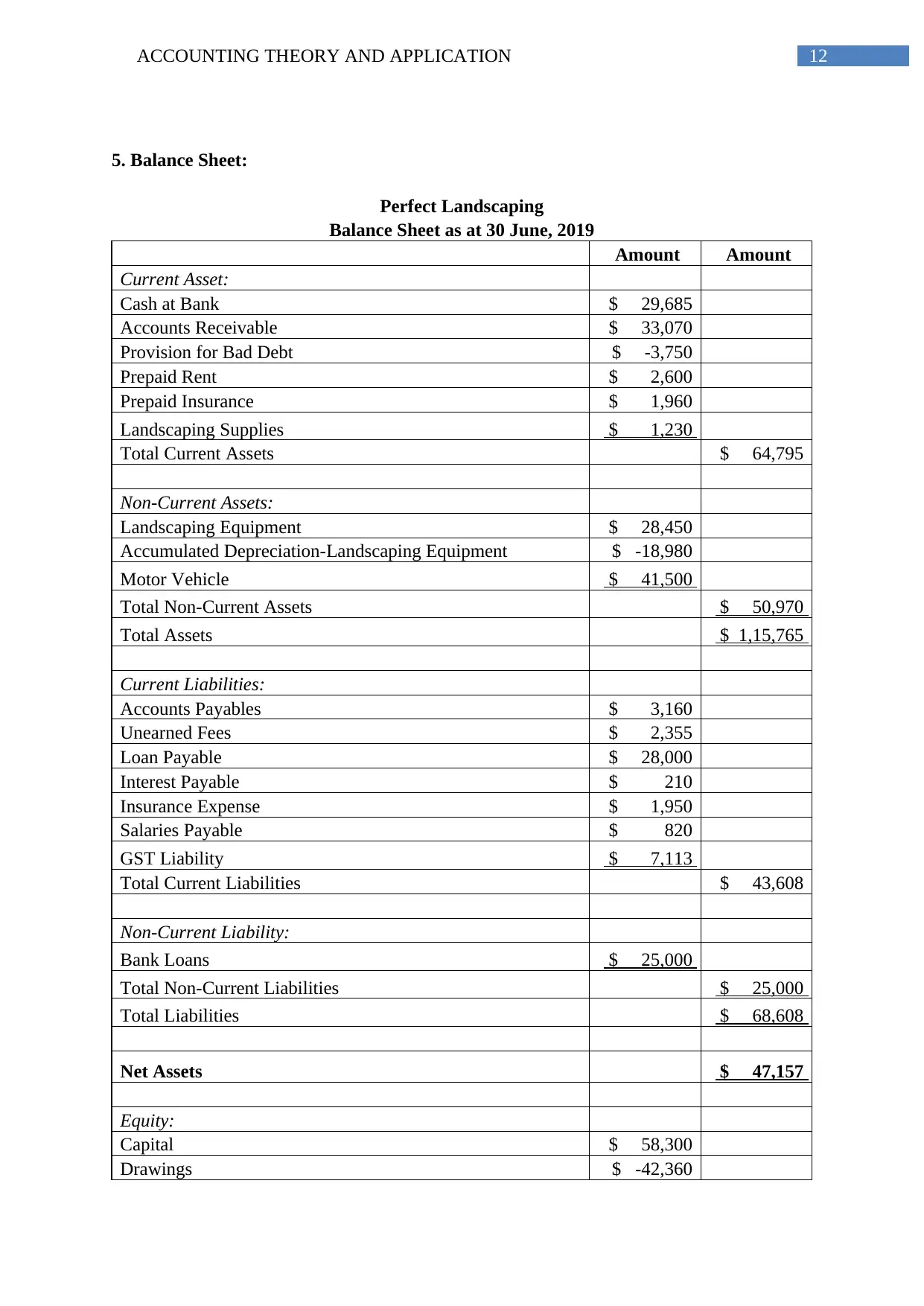

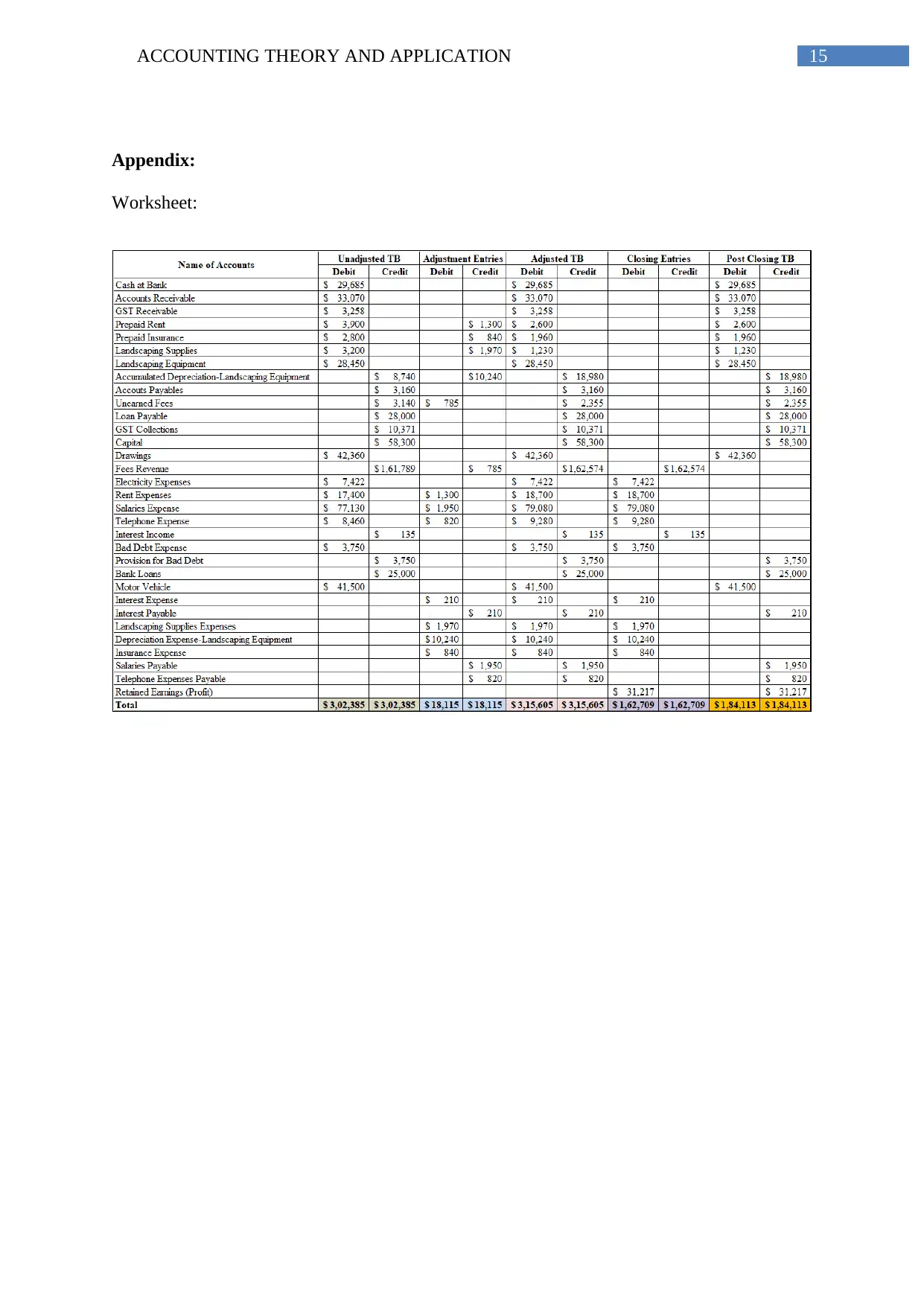

This document contains journal entries, adjusting entries, and T Ledger for Perfect Landscaping. It also includes a Profit and Loss Statement and a Balance Sheet. The document covers topics such as Bank, Accounts Receivable, Electricity Expense, GST Paid, Salaries Expense, Fees Revenue, GST Collected, Interest Income, Motor Vehicle, Bad Debt Expense, Provision for Bad Debt, Interest Expense, Interest Payable, Landscaping Supplies Expenses, Landscaping Supplies, Depreciation Expense-Landscaping Equipment, Accumulated Depreciation-Landscaping Equipment, Unearned Fees, Rent Expense, Prepaid Rent, Insurance Expense, Prepaid Insurance, Salaries Payable, Telephone Expenses, Accounts Payables, Loan Payable, GST Collections, Capital, Drawings, and Fees Revenue.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)