Accounting: Financial Statements, Ratio Analysis, Bank Account

VerifiedAdded on 2023/01/09

|15

|3321

|78

AI Summary

This document provides an introduction to accounting and discusses the financial statements of Bob's account. It also explains the three main features of information for users of financial statements. The document includes a calculation of ratios and their interpretation. It also provides a step-by-step guide to writing up the bank account and balancing other accounts.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION.......................................................................................................................................3

QUESTION 1..............................................................................................................................................3

(A) Financial statement of Bob’s account................................................................................................3

(b) Three main features of information for users of financial statements.................................................5

QUESTION 2..............................................................................................................................................6

(2a) Calculation of ratio and interpretation..............................................................................................6

QUESTION 2B...........................................................................................................................................8

A. Writing up the bank account, balancing at the end of each month......................................................8

B. Writing up all the other accounts and balance the accounts at the end of two month period...............8

C. Extracting a trial balance as at 30th April 2018..................................................................................10

QUESTION 2C.........................................................................................................................................10

A. Applying dep with straight line method............................................................................................10

B. Applying dep with reducing balance method....................................................................................11

C. Explanation of meaning and significance of different accounting concepts......................................12

CONCLUSION.........................................................................................................................................13

REFERENCES..........................................................................................................................................14

INTRODUCTION.......................................................................................................................................3

QUESTION 1..............................................................................................................................................3

(A) Financial statement of Bob’s account................................................................................................3

(b) Three main features of information for users of financial statements.................................................5

QUESTION 2..............................................................................................................................................6

(2a) Calculation of ratio and interpretation..............................................................................................6

QUESTION 2B...........................................................................................................................................8

A. Writing up the bank account, balancing at the end of each month......................................................8

B. Writing up all the other accounts and balance the accounts at the end of two month period...............8

C. Extracting a trial balance as at 30th April 2018..................................................................................10

QUESTION 2C.........................................................................................................................................10

A. Applying dep with straight line method............................................................................................10

B. Applying dep with reducing balance method....................................................................................11

C. Explanation of meaning and significance of different accounting concepts......................................12

CONCLUSION.........................................................................................................................................13

REFERENCES..........................................................................................................................................14

INTRODUCTION

Accounting is the mechanism for documenting cash activities related to a business. The

financial accounting involves the review, examination and disclosure of these purchases to state

authorities, supervisors and national tax bodies. Financial analysis income accounts are a detailed

description of cash activities across an income statement, restating the activities, financial status

and working capital of a business. Bookkeeping is amongst the most important roles of almost

any company. It can be done by either a housekeeper or administrator in a small company, or

through wide divisions of accounting with hundreds of staff in bigger business. The main goal is

to provide the shareholders with such reports because their money was put in the company. In

this report, the main features of information that are convenient for users are month-end

payments. In addition to this, determine and evaluate information on financial ratio to analyze

the financial performance of the corporation and write up checking account across each couple of

weeks. In addition, implement different methods of devaluation, and understand exactly different

interpretations of financial reporting.

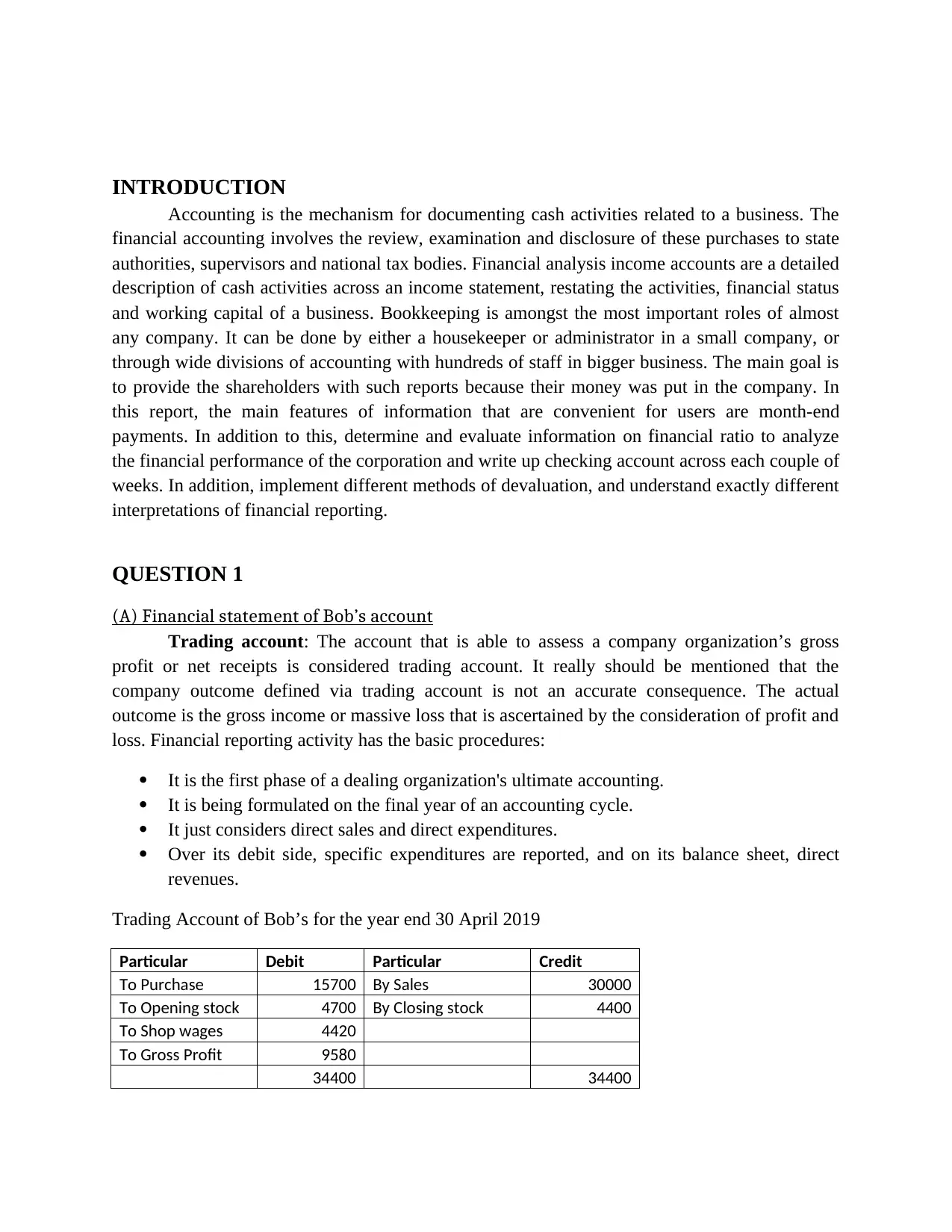

QUESTION 1

(A) Financial statement of Bob’s account

Trading account: The account that is able to assess a company organization’s gross

profit or net receipts is considered trading account. It really should be mentioned that the

company outcome defined via trading account is not an accurate consequence. The actual

outcome is the gross income or massive loss that is ascertained by the consideration of profit and

loss. Financial reporting activity has the basic procedures:

It is the first phase of a dealing organization's ultimate accounting.

It is being formulated on the final year of an accounting cycle.

It just considers direct sales and direct expenditures.

Over its debit side, specific expenditures are reported, and on its balance sheet, direct

revenues.

Trading Account of Bob’s for the year end 30 April 2019

Particular Debit Particular Credit

To Purchase 15700 By Sales 30000

To Opening stock 4700 By Closing stock 4400

To Shop wages 4420

To Gross Profit 9580

34400 34400

Accounting is the mechanism for documenting cash activities related to a business. The

financial accounting involves the review, examination and disclosure of these purchases to state

authorities, supervisors and national tax bodies. Financial analysis income accounts are a detailed

description of cash activities across an income statement, restating the activities, financial status

and working capital of a business. Bookkeeping is amongst the most important roles of almost

any company. It can be done by either a housekeeper or administrator in a small company, or

through wide divisions of accounting with hundreds of staff in bigger business. The main goal is

to provide the shareholders with such reports because their money was put in the company. In

this report, the main features of information that are convenient for users are month-end

payments. In addition to this, determine and evaluate information on financial ratio to analyze

the financial performance of the corporation and write up checking account across each couple of

weeks. In addition, implement different methods of devaluation, and understand exactly different

interpretations of financial reporting.

QUESTION 1

(A) Financial statement of Bob’s account

Trading account: The account that is able to assess a company organization’s gross

profit or net receipts is considered trading account. It really should be mentioned that the

company outcome defined via trading account is not an accurate consequence. The actual

outcome is the gross income or massive loss that is ascertained by the consideration of profit and

loss. Financial reporting activity has the basic procedures:

It is the first phase of a dealing organization's ultimate accounting.

It is being formulated on the final year of an accounting cycle.

It just considers direct sales and direct expenditures.

Over its debit side, specific expenditures are reported, and on its balance sheet, direct

revenues.

Trading Account of Bob’s for the year end 30 April 2019

Particular Debit Particular Credit

To Purchase 15700 By Sales 30000

To Opening stock 4700 By Closing stock 4400

To Shop wages 4420

To Gross Profit 9580

34400 34400

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Interpretation: As per the above calculation it has been analyzing that the trading

account prepares by the Bob’s to know the gross profit of business. For this contains opening and

closing stock, purchase and sales. At the end get the amount of 9580 of gross profit in the

company. In this account also include shop wages which is 4420 to calculate gross profit.

Profit & loss account: Profit and loss account shows the firm's net profit and net loss for

the income statement. This payment is provided for the purpose of determining the net profit or

net deterioration that takes place to a business organization while on an income statement.

Benefit and loss balance is triggered by inputting the debit sides gross loss or credited hand net

margin. This information is calculated from the equilibrium taken down from the Trading

account. In contrast to the abovementioned expenditures, an industry will inflict several other

expenditures. These expenditures will be reimbursed from the revenue, or introduced to the total

failure, as well as the expected value will be gross income or massive decrease.

Bob’s profit & loss account for the year end of 30 April 2019

Particular Amount Particular Amount

To Shop fittings 13000 By Gross Profit 9580

To Light and heat 260 By Net Loss 8300

To Rent 4500

To Insurance 120

17880 17880

Interpretation: To calculate the amount of net profit/loss of the company prepare profit

and loss account in which contains all the income in credit side and expenditure in debit side.

There are expenditure include shop fittings, light & heat, insurant and rent. On the other side of

income side does not include any item. At the end get amount of 8300 net loss of Bob’s account.

Financial position statement: The financial status statement is really just another term

for the financial statements. It is amongst the most significant financial statements. The financial

review paper estimates on the resources, liabilities of an organization and the variation in their

total as of the exact act of an accounting cycle. The framework of the economic position paper is

closely related to that of the rudimentary financial statements. The formula for a company would

be: Assets = Liabilities + Equity of shareholders. The structure of a charity cause would be:

Assets = Liabilities + Net Assets. Appropriately, the financial status statement becomes more

accurate when it is structured similar to the accrual accounting process.

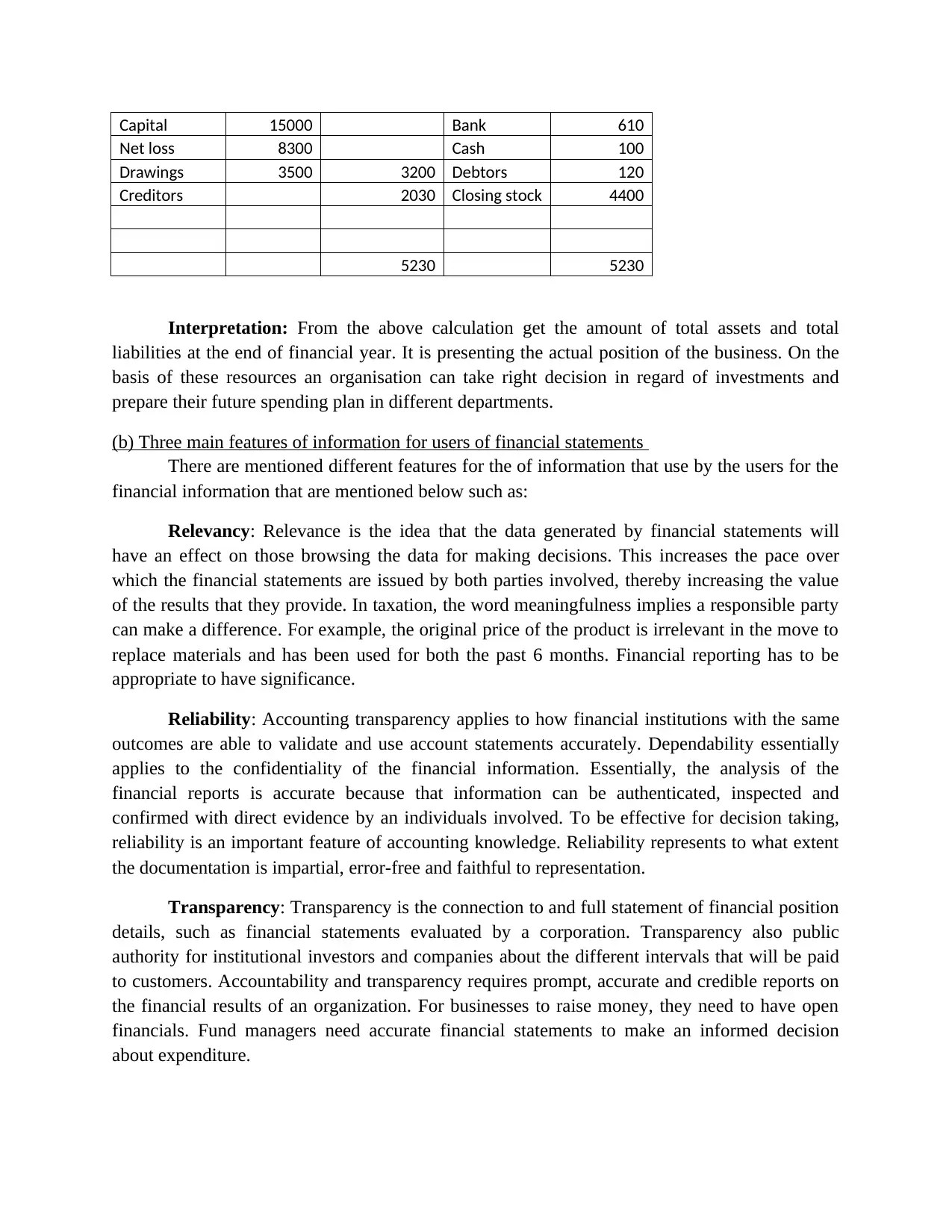

Bob’s financial position statement for the year end of 30 April 2019

Liabilities Amount Assets Amount

account prepares by the Bob’s to know the gross profit of business. For this contains opening and

closing stock, purchase and sales. At the end get the amount of 9580 of gross profit in the

company. In this account also include shop wages which is 4420 to calculate gross profit.

Profit & loss account: Profit and loss account shows the firm's net profit and net loss for

the income statement. This payment is provided for the purpose of determining the net profit or

net deterioration that takes place to a business organization while on an income statement.

Benefit and loss balance is triggered by inputting the debit sides gross loss or credited hand net

margin. This information is calculated from the equilibrium taken down from the Trading

account. In contrast to the abovementioned expenditures, an industry will inflict several other

expenditures. These expenditures will be reimbursed from the revenue, or introduced to the total

failure, as well as the expected value will be gross income or massive decrease.

Bob’s profit & loss account for the year end of 30 April 2019

Particular Amount Particular Amount

To Shop fittings 13000 By Gross Profit 9580

To Light and heat 260 By Net Loss 8300

To Rent 4500

To Insurance 120

17880 17880

Interpretation: To calculate the amount of net profit/loss of the company prepare profit

and loss account in which contains all the income in credit side and expenditure in debit side.

There are expenditure include shop fittings, light & heat, insurant and rent. On the other side of

income side does not include any item. At the end get amount of 8300 net loss of Bob’s account.

Financial position statement: The financial status statement is really just another term

for the financial statements. It is amongst the most significant financial statements. The financial

review paper estimates on the resources, liabilities of an organization and the variation in their

total as of the exact act of an accounting cycle. The framework of the economic position paper is

closely related to that of the rudimentary financial statements. The formula for a company would

be: Assets = Liabilities + Equity of shareholders. The structure of a charity cause would be:

Assets = Liabilities + Net Assets. Appropriately, the financial status statement becomes more

accurate when it is structured similar to the accrual accounting process.

Bob’s financial position statement for the year end of 30 April 2019

Liabilities Amount Assets Amount

Capital 15000 Bank 610

Net loss 8300 Cash 100

Drawings 3500 3200 Debtors 120

Creditors 2030 Closing stock 4400

5230 5230

Interpretation: From the above calculation get the amount of total assets and total

liabilities at the end of financial year. It is presenting the actual position of the business. On the

basis of these resources an organisation can take right decision in regard of investments and

prepare their future spending plan in different departments.

(b) Three main features of information for users of financial statements

There are mentioned different features for the of information that use by the users for the

financial information that are mentioned below such as:

Relevancy: Relevance is the idea that the data generated by financial statements will

have an effect on those browsing the data for making decisions. This increases the pace over

which the financial statements are issued by both parties involved, thereby increasing the value

of the results that they provide. In taxation, the word meaningfulness implies a responsible party

can make a difference. For example, the original price of the product is irrelevant in the move to

replace materials and has been used for both the past 6 months. Financial reporting has to be

appropriate to have significance.

Reliability: Accounting transparency applies to how financial institutions with the same

outcomes are able to validate and use account statements accurately. Dependability essentially

applies to the confidentiality of the financial information. Essentially, the analysis of the

financial reports is accurate because that information can be authenticated, inspected and

confirmed with direct evidence by an individuals involved. To be effective for decision taking,

reliability is an important feature of accounting knowledge. Reliability represents to what extent

the documentation is impartial, error-free and faithful to representation.

Transparency: Transparency is the connection to and full statement of financial position

details, such as financial statements evaluated by a corporation. Transparency also public

authority for institutional investors and companies about the different intervals that will be paid

to customers. Accountability and transparency requires prompt, accurate and credible reports on

the financial results of an organization. For businesses to raise money, they need to have open

financials. Fund managers need accurate financial statements to make an informed decision

about expenditure.

Net loss 8300 Cash 100

Drawings 3500 3200 Debtors 120

Creditors 2030 Closing stock 4400

5230 5230

Interpretation: From the above calculation get the amount of total assets and total

liabilities at the end of financial year. It is presenting the actual position of the business. On the

basis of these resources an organisation can take right decision in regard of investments and

prepare their future spending plan in different departments.

(b) Three main features of information for users of financial statements

There are mentioned different features for the of information that use by the users for the

financial information that are mentioned below such as:

Relevancy: Relevance is the idea that the data generated by financial statements will

have an effect on those browsing the data for making decisions. This increases the pace over

which the financial statements are issued by both parties involved, thereby increasing the value

of the results that they provide. In taxation, the word meaningfulness implies a responsible party

can make a difference. For example, the original price of the product is irrelevant in the move to

replace materials and has been used for both the past 6 months. Financial reporting has to be

appropriate to have significance.

Reliability: Accounting transparency applies to how financial institutions with the same

outcomes are able to validate and use account statements accurately. Dependability essentially

applies to the confidentiality of the financial information. Essentially, the analysis of the

financial reports is accurate because that information can be authenticated, inspected and

confirmed with direct evidence by an individuals involved. To be effective for decision taking,

reliability is an important feature of accounting knowledge. Reliability represents to what extent

the documentation is impartial, error-free and faithful to representation.

Transparency: Transparency is the connection to and full statement of financial position

details, such as financial statements evaluated by a corporation. Transparency also public

authority for institutional investors and companies about the different intervals that will be paid

to customers. Accountability and transparency requires prompt, accurate and credible reports on

the financial results of an organization. For businesses to raise money, they need to have open

financials. Fund managers need accurate financial statements to make an informed decision

about expenditure.

QUESTION 2

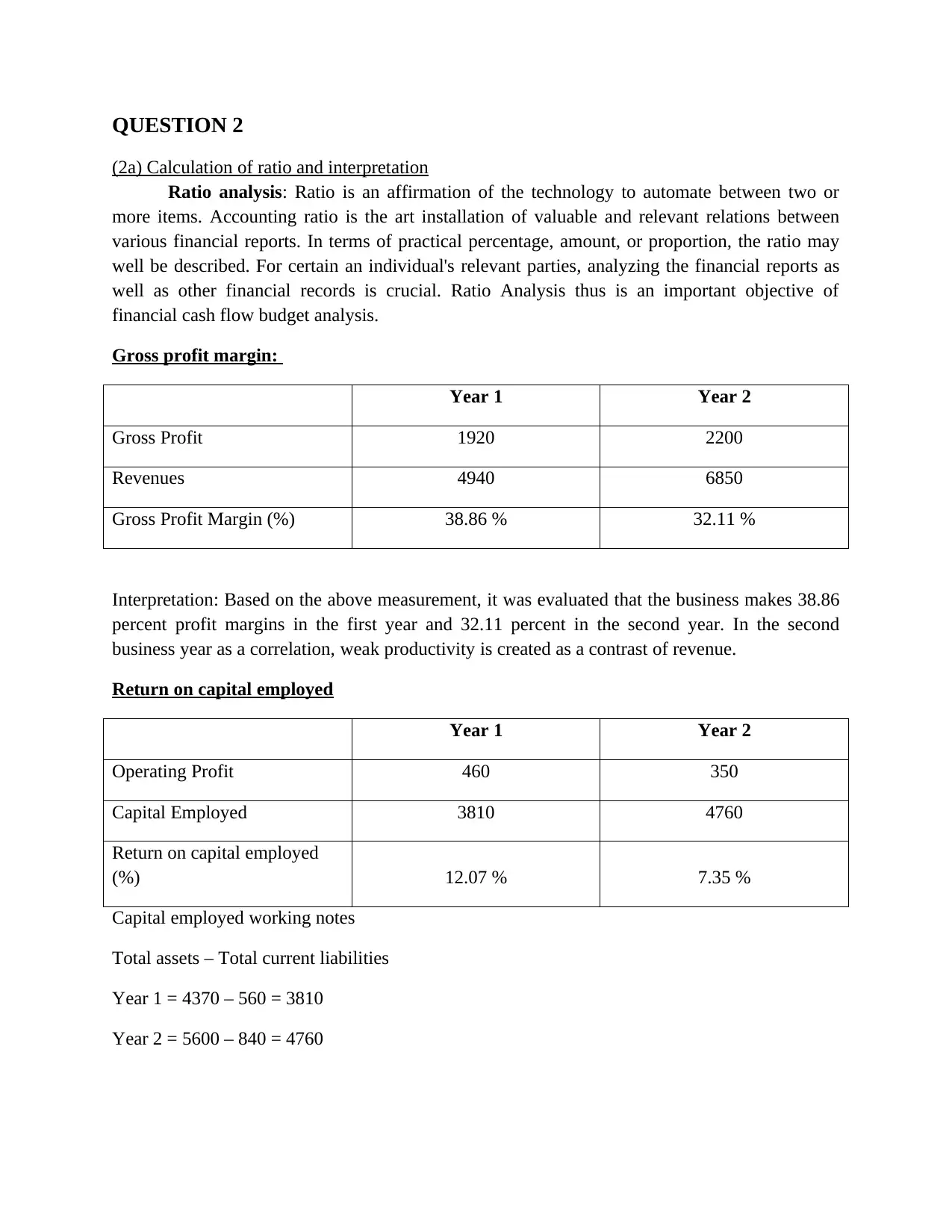

(2a) Calculation of ratio and interpretation

Ratio analysis: Ratio is an affirmation of the technology to automate between two or

more items. Accounting ratio is the art installation of valuable and relevant relations between

various financial reports. In terms of practical percentage, amount, or proportion, the ratio may

well be described. For certain an individual's relevant parties, analyzing the financial reports as

well as other financial records is crucial. Ratio Analysis thus is an important objective of

financial cash flow budget analysis.

Gross profit margin:

Year 1 Year 2

Gross Profit 1920 2200

Revenues 4940 6850

Gross Profit Margin (%) 38.86 % 32.11 %

Interpretation: Based on the above measurement, it was evaluated that the business makes 38.86

percent profit margins in the first year and 32.11 percent in the second year. In the second

business year as a correlation, weak productivity is created as a contrast of revenue.

Return on capital employed

Year 1 Year 2

Operating Profit 460 350

Capital Employed 3810 4760

Return on capital employed

(%) 12.07 % 7.35 %

Capital employed working notes

Total assets – Total current liabilities

Year 1 = 4370 – 560 = 3810

Year 2 = 5600 – 840 = 4760

(2a) Calculation of ratio and interpretation

Ratio analysis: Ratio is an affirmation of the technology to automate between two or

more items. Accounting ratio is the art installation of valuable and relevant relations between

various financial reports. In terms of practical percentage, amount, or proportion, the ratio may

well be described. For certain an individual's relevant parties, analyzing the financial reports as

well as other financial records is crucial. Ratio Analysis thus is an important objective of

financial cash flow budget analysis.

Gross profit margin:

Year 1 Year 2

Gross Profit 1920 2200

Revenues 4940 6850

Gross Profit Margin (%) 38.86 % 32.11 %

Interpretation: Based on the above measurement, it was evaluated that the business makes 38.86

percent profit margins in the first year and 32.11 percent in the second year. In the second

business year as a correlation, weak productivity is created as a contrast of revenue.

Return on capital employed

Year 1 Year 2

Operating Profit 460 350

Capital Employed 3810 4760

Return on capital employed

(%) 12.07 % 7.35 %

Capital employed working notes

Total assets – Total current liabilities

Year 1 = 4370 – 560 = 3810

Year 2 = 5600 – 840 = 4760

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: the Company’s use of this proportion to analyze operational efficiencies and

create revenue from wealth. In second year, the capital employed decreased in contrast with year

yet another. It's not beneficial for the industry as it has detrimental effects.

Current ratio:

Year 1 Year 2

Current Assets 1770 2390

Current Liabilities 560 840

Current ratio 3.16 2.84

Interpretation: Due to the above estimate, the first company achieves the ideal ratio of 2:1 as

well as the break second in the year. Produce 3.16 in first year and 2.84 in second year.

Trade payable period in days:

Year 1 Year 2

Trade Payable 560 840

Cost of sales 3020 4650

Trade payable period in days 67.68 days 65.93 days

Interpretation: According to the chart above, it recognizes that in the first year the organization

can specify the money in the 67.78 days, but in the second year it decreases and reaches on 65.93

days, which is not favorable for the organization.

Trade receivable period

Year 1 Year 2

Trade receivable 820 1230

Total sales 4940 6850

Trade receivable period 60.59 days 65.54 days

Interpretation: From the above estimate, it is calculated that the company gets build from the

debtors in 60.59 days during the first year, but in the next year it rises and reaches 65.54 times

that is not favorable for the organization and affects the liquidity situation.

create revenue from wealth. In second year, the capital employed decreased in contrast with year

yet another. It's not beneficial for the industry as it has detrimental effects.

Current ratio:

Year 1 Year 2

Current Assets 1770 2390

Current Liabilities 560 840

Current ratio 3.16 2.84

Interpretation: Due to the above estimate, the first company achieves the ideal ratio of 2:1 as

well as the break second in the year. Produce 3.16 in first year and 2.84 in second year.

Trade payable period in days:

Year 1 Year 2

Trade Payable 560 840

Cost of sales 3020 4650

Trade payable period in days 67.68 days 65.93 days

Interpretation: According to the chart above, it recognizes that in the first year the organization

can specify the money in the 67.78 days, but in the second year it decreases and reaches on 65.93

days, which is not favorable for the organization.

Trade receivable period

Year 1 Year 2

Trade receivable 820 1230

Total sales 4940 6850

Trade receivable period 60.59 days 65.54 days

Interpretation: From the above estimate, it is calculated that the company gets build from the

debtors in 60.59 days during the first year, but in the next year it rises and reaches 65.54 times

that is not favorable for the organization and affects the liquidity situation.

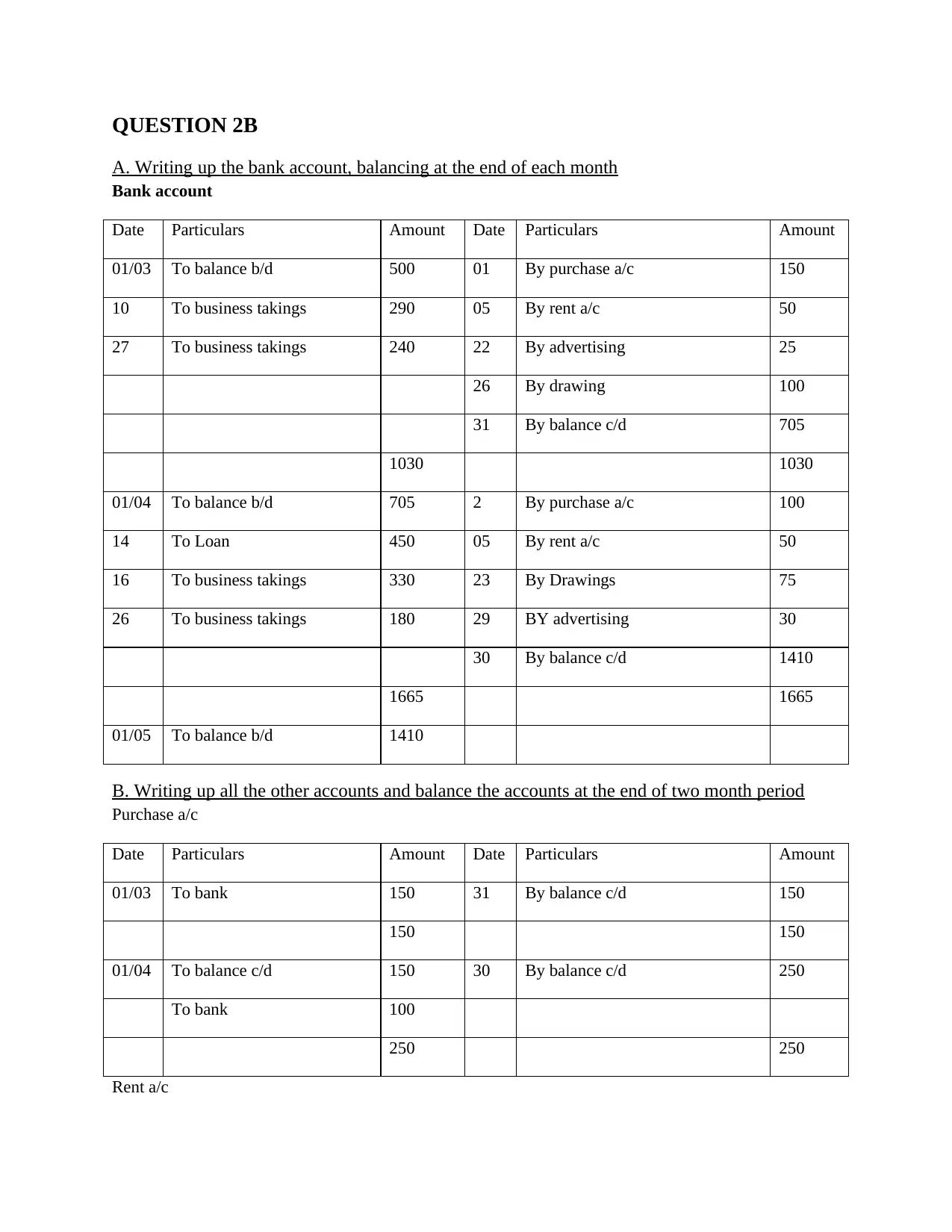

QUESTION 2B

A. Writing up the bank account, balancing at the end of each month

Bank account

Date Particulars Amount Date Particulars Amount

01/03 To balance b/d 500 01 By purchase a/c 150

10 To business takings 290 05 By rent a/c 50

27 To business takings 240 22 By advertising 25

26 By drawing 100

31 By balance c/d 705

1030 1030

01/04 To balance b/d 705 2 By purchase a/c 100

14 To Loan 450 05 By rent a/c 50

16 To business takings 330 23 By Drawings 75

26 To business takings 180 29 BY advertising 30

30 By balance c/d 1410

1665 1665

01/05 To balance b/d 1410

B. Writing up all the other accounts and balance the accounts at the end of two month period

Purchase a/c

Date Particulars Amount Date Particulars Amount

01/03 To bank 150 31 By balance c/d 150

150 150

01/04 To balance c/d 150 30 By balance c/d 250

To bank 100

250 250

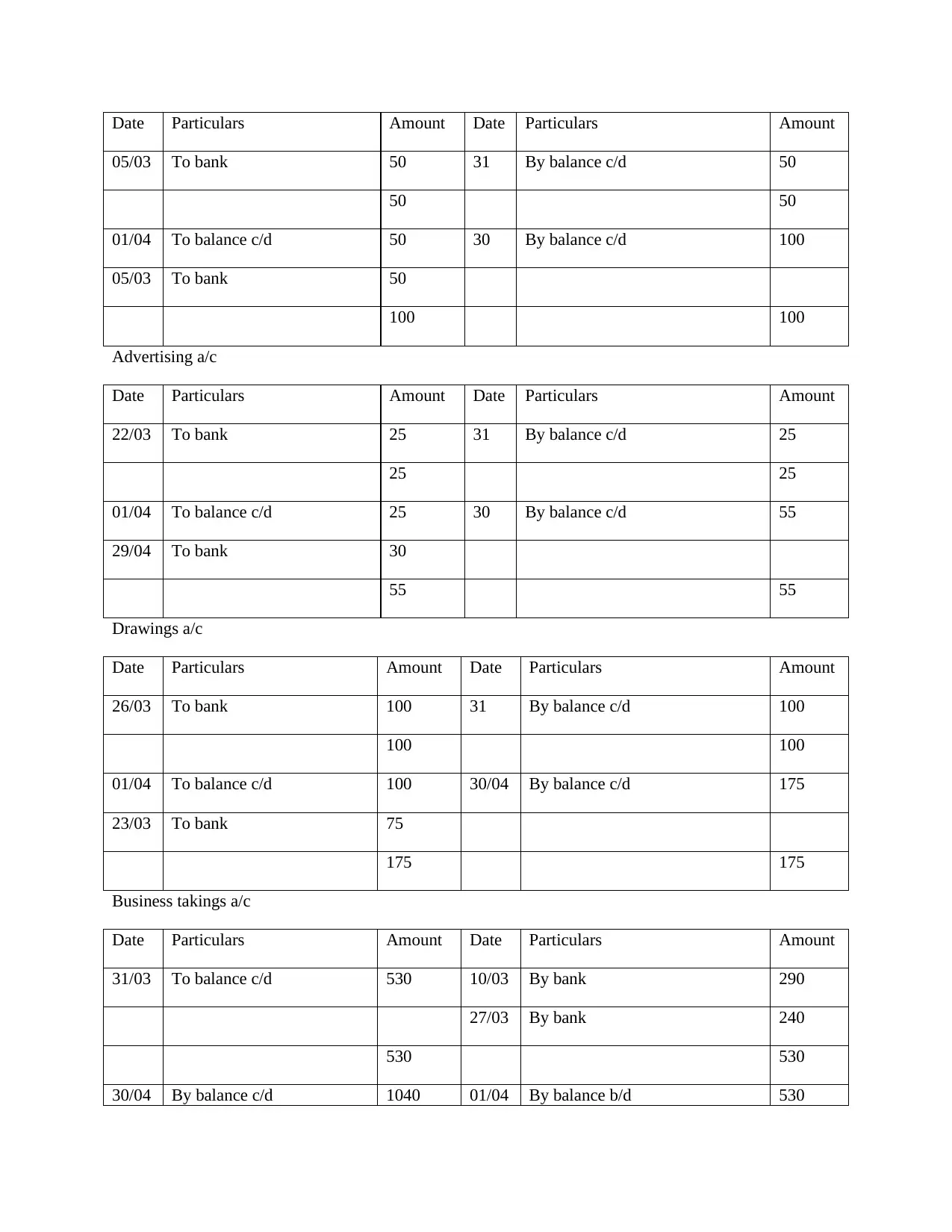

Rent a/c

A. Writing up the bank account, balancing at the end of each month

Bank account

Date Particulars Amount Date Particulars Amount

01/03 To balance b/d 500 01 By purchase a/c 150

10 To business takings 290 05 By rent a/c 50

27 To business takings 240 22 By advertising 25

26 By drawing 100

31 By balance c/d 705

1030 1030

01/04 To balance b/d 705 2 By purchase a/c 100

14 To Loan 450 05 By rent a/c 50

16 To business takings 330 23 By Drawings 75

26 To business takings 180 29 BY advertising 30

30 By balance c/d 1410

1665 1665

01/05 To balance b/d 1410

B. Writing up all the other accounts and balance the accounts at the end of two month period

Purchase a/c

Date Particulars Amount Date Particulars Amount

01/03 To bank 150 31 By balance c/d 150

150 150

01/04 To balance c/d 150 30 By balance c/d 250

To bank 100

250 250

Rent a/c

Date Particulars Amount Date Particulars Amount

05/03 To bank 50 31 By balance c/d 50

50 50

01/04 To balance c/d 50 30 By balance c/d 100

05/03 To bank 50

100 100

Advertising a/c

Date Particulars Amount Date Particulars Amount

22/03 To bank 25 31 By balance c/d 25

25 25

01/04 To balance c/d 25 30 By balance c/d 55

29/04 To bank 30

55 55

Drawings a/c

Date Particulars Amount Date Particulars Amount

26/03 To bank 100 31 By balance c/d 100

100 100

01/04 To balance c/d 100 30/04 By balance c/d 175

23/03 To bank 75

175 175

Business takings a/c

Date Particulars Amount Date Particulars Amount

31/03 To balance c/d 530 10/03 By bank 290

27/03 By bank 240

530 530

30/04 By balance c/d 1040 01/04 By balance b/d 530

05/03 To bank 50 31 By balance c/d 50

50 50

01/04 To balance c/d 50 30 By balance c/d 100

05/03 To bank 50

100 100

Advertising a/c

Date Particulars Amount Date Particulars Amount

22/03 To bank 25 31 By balance c/d 25

25 25

01/04 To balance c/d 25 30 By balance c/d 55

29/04 To bank 30

55 55

Drawings a/c

Date Particulars Amount Date Particulars Amount

26/03 To bank 100 31 By balance c/d 100

100 100

01/04 To balance c/d 100 30/04 By balance c/d 175

23/03 To bank 75

175 175

Business takings a/c

Date Particulars Amount Date Particulars Amount

31/03 To balance c/d 530 10/03 By bank 290

27/03 By bank 240

530 530

30/04 By balance c/d 1040 01/04 By balance b/d 530

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16/04 By bank 330

26/04 By bank 180

1040 1040

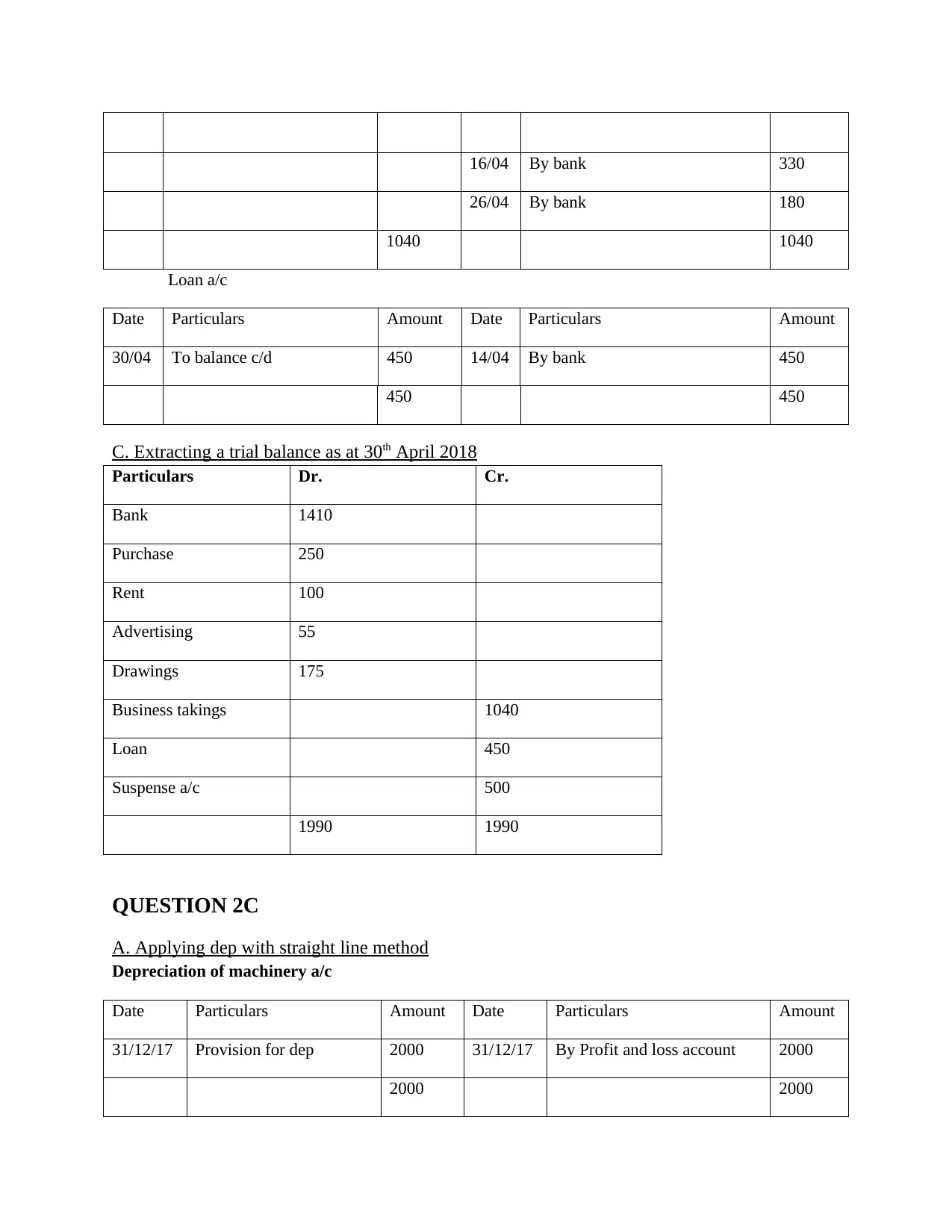

Loan a/c

Date Particulars Amount Date Particulars Amount

30/04 To balance c/d 450 14/04 By bank 450

450 450

C. Extracting a trial balance as at 30th April 2018

Particulars Dr. Cr.

Bank 1410

Purchase 250

Rent 100

Advertising 55

Drawings 175

Business takings 1040

Loan 450

Suspense a/c 500

1990 1990

QUESTION 2C

A. Applying dep with straight line method

Depreciation of machinery a/c

Date Particulars Amount Date Particulars Amount

31/12/17 Provision for dep 2000 31/12/17 By Profit and loss account 2000

2000 2000

26/04 By bank 180

1040 1040

Loan a/c

Date Particulars Amount Date Particulars Amount

30/04 To balance c/d 450 14/04 By bank 450

450 450

C. Extracting a trial balance as at 30th April 2018

Particulars Dr. Cr.

Bank 1410

Purchase 250

Rent 100

Advertising 55

Drawings 175

Business takings 1040

Loan 450

Suspense a/c 500

1990 1990

QUESTION 2C

A. Applying dep with straight line method

Depreciation of machinery a/c

Date Particulars Amount Date Particulars Amount

31/12/17 Provision for dep 2000 31/12/17 By Profit and loss account 2000

2000 2000

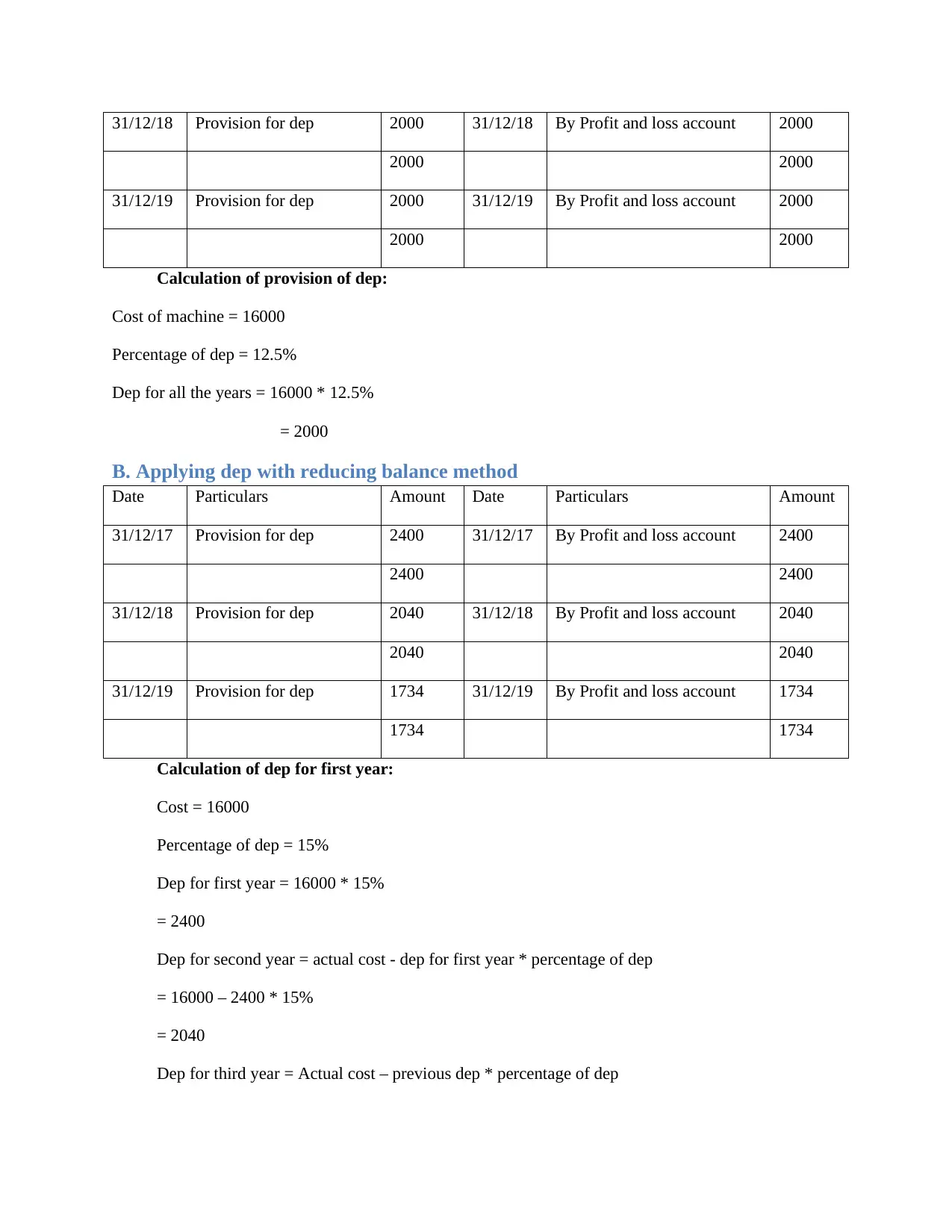

31/12/18 Provision for dep 2000 31/12/18 By Profit and loss account 2000

2000 2000

31/12/19 Provision for dep 2000 31/12/19 By Profit and loss account 2000

2000 2000

Calculation of provision of dep:

Cost of machine = 16000

Percentage of dep = 12.5%

Dep for all the years = 16000 * 12.5%

= 2000

B. Applying dep with reducing balance method

Date Particulars Amount Date Particulars Amount

31/12/17 Provision for dep 2400 31/12/17 By Profit and loss account 2400

2400 2400

31/12/18 Provision for dep 2040 31/12/18 By Profit and loss account 2040

2040 2040

31/12/19 Provision for dep 1734 31/12/19 By Profit and loss account 1734

1734 1734

Calculation of dep for first year:

Cost = 16000

Percentage of dep = 15%

Dep for first year = 16000 * 15%

= 2400

Dep for second year = actual cost - dep for first year * percentage of dep

= 16000 – 2400 * 15%

= 2040

Dep for third year = Actual cost – previous dep * percentage of dep

2000 2000

31/12/19 Provision for dep 2000 31/12/19 By Profit and loss account 2000

2000 2000

Calculation of provision of dep:

Cost of machine = 16000

Percentage of dep = 12.5%

Dep for all the years = 16000 * 12.5%

= 2000

B. Applying dep with reducing balance method

Date Particulars Amount Date Particulars Amount

31/12/17 Provision for dep 2400 31/12/17 By Profit and loss account 2400

2400 2400

31/12/18 Provision for dep 2040 31/12/18 By Profit and loss account 2040

2040 2040

31/12/19 Provision for dep 1734 31/12/19 By Profit and loss account 1734

1734 1734

Calculation of dep for first year:

Cost = 16000

Percentage of dep = 15%

Dep for first year = 16000 * 15%

= 2400

Dep for second year = actual cost - dep for first year * percentage of dep

= 16000 – 2400 * 15%

= 2040

Dep for third year = Actual cost – previous dep * percentage of dep

= 16000 – 2400 – 2040 * 15%

= 1734

C. Explanation of meaning and significance of different accounting concepts

Going concern: It is an accounting concept which is required to be followed by all the

organisations so that the business could be executed in systematic manner. It guides all the

entities to make sure that all the resources are used continuously for operations so that the ability

of the company to make money in future could be determined. It is one of the fundamental

principles of accounting which assumes that beyond and during the net financial year an

enterprise will complete all the current plans and achieve all the goals. All the existing assets and

other resources will be used to meet all the financial goals in upcoming years (Jollands and

Quinn, 2017).

Materiality: According to this concept all the finance related details of an enterprise are

considered to be material from the point of view of preparation of the final accounts. It is vital

for all the enterprises to make sure that they are not recording biased information in the books so

that the possibility of materiality in the accounting reports could be ignored. This concept states

that an accounting standard could be ignored by an organisation while formulating the reports if

the impact of doing this is very small of the final accounts. Apart from this, it is allowed if it is

not misleading any user. If it is leaving very huge impact upon the financial statements and

misleading the users then the entities should not ignore any accounting standard. It also

demonstrates that if the mistake in final accounts is made by omission then it could be ignored

for legal actions. On the other hand, if the error is made willingly for misleading the users then it

may result in struct action against the enterprise (Bujaki, Lento and Sayed, 2019).

Business entity concept: This concept states that business man and the business both are

separate. The owners cannot record the personal expenses in the books of business. All the

transactions that are associated with a business should be recorded separately from the owners. If

the personal transactions of the owner will be recorded in the books then it will eb very difficult

to analyse actual profitability of business. It demonstrates that the owner should not extend to

business without recording it as loan or stock purchased. If the owner is recording own expenses

in the books of business then it is not allowed according to the rules and regulations of

accounting. This type of mistakes may result in negative comments of auditor which will leave

negative impact upon the functionality of business (Tekathen, 2019).

CONCLUSION

As per the above study it was concluded that the various types of companies use financial

accounting to assess the financial position of the company. In this accounting firm, new varieties

of documents are prepared which present actual financial results and allow company

management to make good decisions. Trading, profit, and loss statements are made to analyze

= 1734

C. Explanation of meaning and significance of different accounting concepts

Going concern: It is an accounting concept which is required to be followed by all the

organisations so that the business could be executed in systematic manner. It guides all the

entities to make sure that all the resources are used continuously for operations so that the ability

of the company to make money in future could be determined. It is one of the fundamental

principles of accounting which assumes that beyond and during the net financial year an

enterprise will complete all the current plans and achieve all the goals. All the existing assets and

other resources will be used to meet all the financial goals in upcoming years (Jollands and

Quinn, 2017).

Materiality: According to this concept all the finance related details of an enterprise are

considered to be material from the point of view of preparation of the final accounts. It is vital

for all the enterprises to make sure that they are not recording biased information in the books so

that the possibility of materiality in the accounting reports could be ignored. This concept states

that an accounting standard could be ignored by an organisation while formulating the reports if

the impact of doing this is very small of the final accounts. Apart from this, it is allowed if it is

not misleading any user. If it is leaving very huge impact upon the financial statements and

misleading the users then the entities should not ignore any accounting standard. It also

demonstrates that if the mistake in final accounts is made by omission then it could be ignored

for legal actions. On the other hand, if the error is made willingly for misleading the users then it

may result in struct action against the enterprise (Bujaki, Lento and Sayed, 2019).

Business entity concept: This concept states that business man and the business both are

separate. The owners cannot record the personal expenses in the books of business. All the

transactions that are associated with a business should be recorded separately from the owners. If

the personal transactions of the owner will be recorded in the books then it will eb very difficult

to analyse actual profitability of business. It demonstrates that the owner should not extend to

business without recording it as loan or stock purchased. If the owner is recording own expenses

in the books of business then it is not allowed according to the rules and regulations of

accounting. This type of mistakes may result in negative comments of auditor which will leave

negative impact upon the functionality of business (Tekathen, 2019).

CONCLUSION

As per the above study it was concluded that the various types of companies use financial

accounting to assess the financial position of the company. In this accounting firm, new varieties

of documents are prepared which present actual financial results and allow company

management to make good decisions. Trading, profit, and loss statements are made to analyze

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the economic health. In this reason also measure with the advantages the research ratio and user

knowledge functionality.

knowledge functionality.

REFERENCES

Books and Journal

Caballero, R.J., Farhi, E. and Gourinchas, P.O., 2017. Rents, technical change, and risk premia

accounting for secular trends in interest rates, returns on capital, earning yields, and

factor shares. American Economic Review, 107(5), pp.614-20.

Kaur, A. and Lodhia, S., 2018. Stakeholder engagement in sustainability accounting and

reporting. Accounting, Auditing & Accountability Journal.

Modell, S., 2017. Critical realist accounting research: In search of its emancipatory

potential. Critical Perspectives on Accounting, 42, pp.20-35.

Gao, P. and Zhang, G., 2019. Accounting manipulation, peer pressure, and internal control. The

Accounting Review. 94(1). pp.127-151.

Mancini, M. S. and et.al, 2018. Exploring ecosystem services assessment through Ecological

Footprint accounting. Ecosystem Services. 30. pp.228-235.

Apostolou, B., Dorminey, J. W., Hassell, J. M. and Rebele, J. E., 2018. Accounting education

literature review (2017). Journal of accounting education. 43. pp.1-23.

Jollands, S. and Quinn, M., 2017. Politicising the sustaining of water supply in Ireland–the role

of accounting concepts. Accounting, Auditing & Accountability Journal.

Bujaki, M., Lento, C. and Sayed, N., 2019. Utilizing professional accounting concepts to

understand and respond to academic dishonesty in accounting programs. Journal of

Accounting Education. 47. pp.28-47.

Tekathen, M., 2019. Unpacking the Fluidity of Management Accounting Concepts: An

Ethnographic Social Site Analysis of Enterprise Risk Management. European Accounting

Review. 28(5). pp.977-1010.

Books and Journal

Caballero, R.J., Farhi, E. and Gourinchas, P.O., 2017. Rents, technical change, and risk premia

accounting for secular trends in interest rates, returns on capital, earning yields, and

factor shares. American Economic Review, 107(5), pp.614-20.

Kaur, A. and Lodhia, S., 2018. Stakeholder engagement in sustainability accounting and

reporting. Accounting, Auditing & Accountability Journal.

Modell, S., 2017. Critical realist accounting research: In search of its emancipatory

potential. Critical Perspectives on Accounting, 42, pp.20-35.

Gao, P. and Zhang, G., 2019. Accounting manipulation, peer pressure, and internal control. The

Accounting Review. 94(1). pp.127-151.

Mancini, M. S. and et.al, 2018. Exploring ecosystem services assessment through Ecological

Footprint accounting. Ecosystem Services. 30. pp.228-235.

Apostolou, B., Dorminey, J. W., Hassell, J. M. and Rebele, J. E., 2018. Accounting education

literature review (2017). Journal of accounting education. 43. pp.1-23.

Jollands, S. and Quinn, M., 2017. Politicising the sustaining of water supply in Ireland–the role

of accounting concepts. Accounting, Auditing & Accountability Journal.

Bujaki, M., Lento, C. and Sayed, N., 2019. Utilizing professional accounting concepts to

understand and respond to academic dishonesty in accounting programs. Journal of

Accounting Education. 47. pp.28-47.

Tekathen, M., 2019. Unpacking the Fluidity of Management Accounting Concepts: An

Ethnographic Social Site Analysis of Enterprise Risk Management. European Accounting

Review. 28(5). pp.977-1010.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.