University Finance Accounting Assignment: Financial Statement Analysis

VerifiedAdded on 2023/01/07

|13

|2509

|55

Homework Assignment

AI Summary

This finance accounting assignment provides a detailed analysis of financial statements, including the trading account, profit and loss account, and statement of financial position for Bob's Trading. It evaluates the features of financial information for users, emphasizing relevance, faithful representation, comparability, verifiability, understandability, and timeliness. The assignment includes ratio analysis, calculating return on capital employed, gross profit margin, current ratio, trade payable days, and trade receivable days. It also covers bank account balances, sales, rent, advertisements, loan accounts, capital, and drawings. Furthermore, it explores depreciation methods (straight-line and reducing balance) and explains accounting concepts like going concern and materiality. This comprehensive solution is designed to aid students in understanding key financial accounting principles and practices.

Introduction to

Finance Accounting

Finance Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

Question 1a).....................................................................................................................................1

(a) Bob’s Trading Account for the year ending 30th April 2019..................................................1

(b) Bob’s Profit and loss Account for the year ending 30th April 2019.......................................1

(c) Bob’s statement of financial position for the year ending 30th April 2019............................1

Question 1b).....................................................................................................................................2

Evaluation of the features of the financial information for the users of the financial statements

with the importance and benefits to users....................................................................................2

Question 2a).....................................................................................................................................3

Ratio Analysis..............................................................................................................................3

Question 2b).....................................................................................................................................5

(a) Bank account balance at the end of every month...................................................................5

(b) Accounts balances at end of the 2 month periods..................................................................6

(c) Trial balance as at 30 April 2018...........................................................................................8

Question 2c).....................................................................................................................................8

(i) Straight Line method at 12.5%..............................................................................................8

(ii) Reducing Balance Method 15%............................................................................................9

iii) Significance and meaning of accounting concepts................................................................9

REFERENCES..............................................................................................................................11

TABLE OF CONTENTS................................................................................................................2

Question 1a).....................................................................................................................................1

(a) Bob’s Trading Account for the year ending 30th April 2019..................................................1

(b) Bob’s Profit and loss Account for the year ending 30th April 2019.......................................1

(c) Bob’s statement of financial position for the year ending 30th April 2019............................1

Question 1b).....................................................................................................................................2

Evaluation of the features of the financial information for the users of the financial statements

with the importance and benefits to users....................................................................................2

Question 2a).....................................................................................................................................3

Ratio Analysis..............................................................................................................................3

Question 2b).....................................................................................................................................5

(a) Bank account balance at the end of every month...................................................................5

(b) Accounts balances at end of the 2 month periods..................................................................6

(c) Trial balance as at 30 April 2018...........................................................................................8

Question 2c).....................................................................................................................................8

(i) Straight Line method at 12.5%..............................................................................................8

(ii) Reducing Balance Method 15%............................................................................................9

iii) Significance and meaning of accounting concepts................................................................9

REFERENCES..............................................................................................................................11

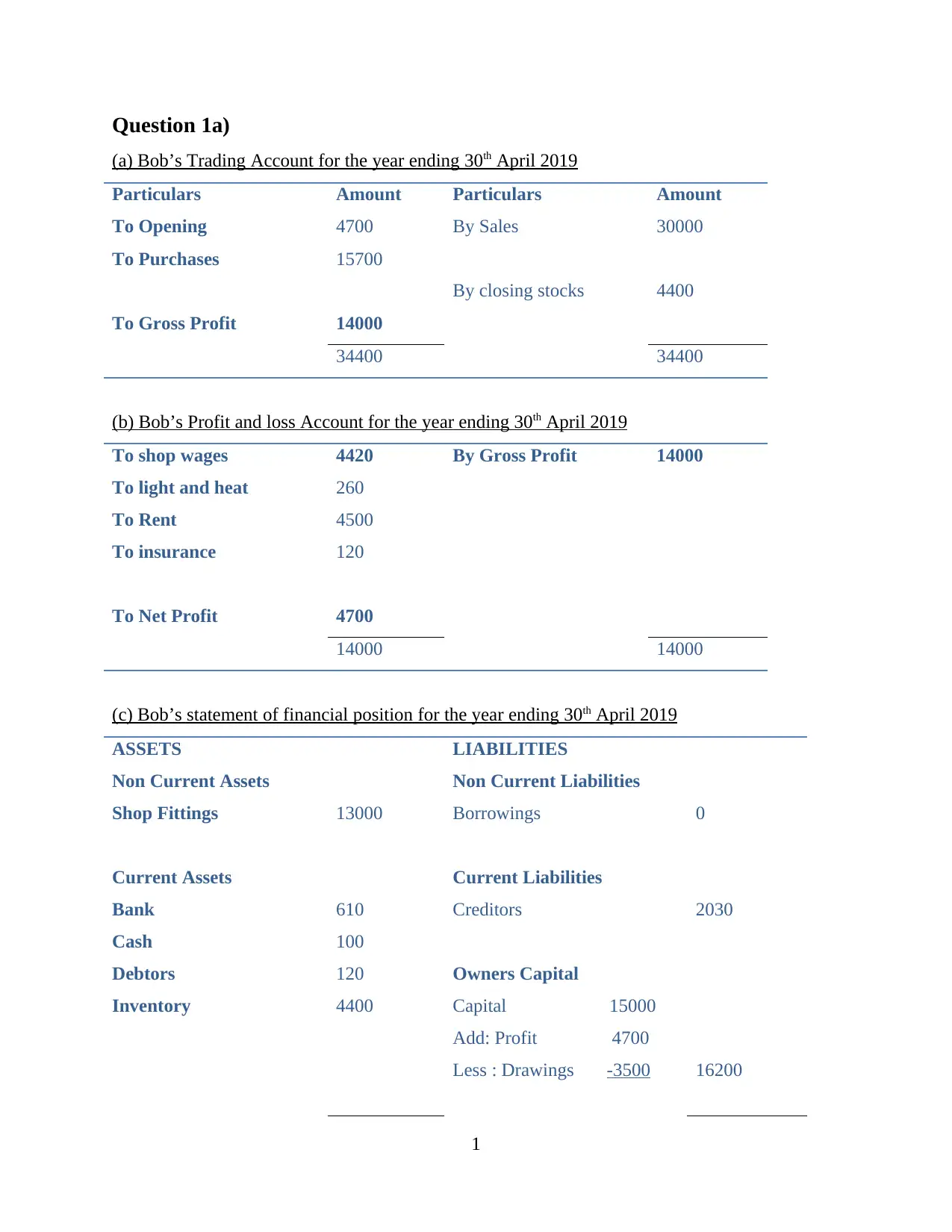

Question 1a)

(a) Bob’s Trading Account for the year ending 30th April 2019

Particulars Amount Particulars Amount

To Opening 4700 By Sales 30000

To Purchases 15700

By closing stocks 4400

To Gross Profit 14000

34400 34400

(b) Bob’s Profit and loss Account for the year ending 30th April 2019

To shop wages 4420 By Gross Profit 14000

To light and heat 260

To Rent 4500

To insurance 120

To Net Profit 4700

14000 14000

(c) Bob’s statement of financial position for the year ending 30th April 2019

ASSETS LIABILITIES

Non Current Assets Non Current Liabilities

Shop Fittings 13000 Borrowings 0

Current Assets Current Liabilities

Bank 610 Creditors 2030

Cash 100

Debtors 120 Owners Capital

Inventory 4400 Capital 15000

Add: Profit 4700

Less : Drawings -3500 16200

1

(a) Bob’s Trading Account for the year ending 30th April 2019

Particulars Amount Particulars Amount

To Opening 4700 By Sales 30000

To Purchases 15700

By closing stocks 4400

To Gross Profit 14000

34400 34400

(b) Bob’s Profit and loss Account for the year ending 30th April 2019

To shop wages 4420 By Gross Profit 14000

To light and heat 260

To Rent 4500

To insurance 120

To Net Profit 4700

14000 14000

(c) Bob’s statement of financial position for the year ending 30th April 2019

ASSETS LIABILITIES

Non Current Assets Non Current Liabilities

Shop Fittings 13000 Borrowings 0

Current Assets Current Liabilities

Bank 610 Creditors 2030

Cash 100

Debtors 120 Owners Capital

Inventory 4400 Capital 15000

Add: Profit 4700

Less : Drawings -3500 16200

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Assets 18230 Total Equity & Liabilities 18230

Question 1b)

Evaluation of the features of the financial information for the users of the financial statements

with the importance and benefits to users

Financial statements could be defined as the summary of all the financial transactions and

events carried out during the year. The information provided by the financial statements is used

by different users as per their interest in the company. it enables the users of financial statements

to make informed business decisions about the company analysing the performance and position

of company over the period. The main six features of financial information to users of the

statements are

Relevance – Information could be stated as relevant if it could influence the decision of users.

Financial statements should provide relevant information about the company for making

economic decisions by the users. If the predictive and contemporary values are not provided by

the financial statements the information is not considered to be relevant for decision making.

Financial information should be relevant as different parties are associated with the business who

wants to evaluate internal functioning of company and the performance targets achieved during

the year.

Faithful Representation – Financial information revealed by the statements should represent

actual performance and position of organisation. The concept requires that information provided

gives a true and fair of financial position as well as performance of the organisations. The

information provided should be free from errors and misstatements and should not be falsely

prepared for representing good performance of the company (Weygandt, Kimmel and Kieso,

2019). The feature of completeness requires that every information that is stated in the financial

statements is true and free from errors and mistakes. All the material transactions or events that

are capable of influencing the behaviour of users should be stated in the statements of company.

Comparability – Financial statements are also prepared so that users can make comparisons

between different firms of the industry for analysing the performance and growth of the

organisation. Keeping this thing in mind the feature accounting bodies required the companies to

prepare financial statements on uniform basis. Financial statements are now prepared by the

2

Question 1b)

Evaluation of the features of the financial information for the users of the financial statements

with the importance and benefits to users

Financial statements could be defined as the summary of all the financial transactions and

events carried out during the year. The information provided by the financial statements is used

by different users as per their interest in the company. it enables the users of financial statements

to make informed business decisions about the company analysing the performance and position

of company over the period. The main six features of financial information to users of the

statements are

Relevance – Information could be stated as relevant if it could influence the decision of users.

Financial statements should provide relevant information about the company for making

economic decisions by the users. If the predictive and contemporary values are not provided by

the financial statements the information is not considered to be relevant for decision making.

Financial information should be relevant as different parties are associated with the business who

wants to evaluate internal functioning of company and the performance targets achieved during

the year.

Faithful Representation – Financial information revealed by the statements should represent

actual performance and position of organisation. The concept requires that information provided

gives a true and fair of financial position as well as performance of the organisations. The

information provided should be free from errors and misstatements and should not be falsely

prepared for representing good performance of the company (Weygandt, Kimmel and Kieso,

2019). The feature of completeness requires that every information that is stated in the financial

statements is true and free from errors and mistakes. All the material transactions or events that

are capable of influencing the behaviour of users should be stated in the statements of company.

Comparability – Financial statements are also prepared so that users can make comparisons

between different firms of the industry for analysing the performance and growth of the

organisation. Keeping this thing in mind the feature accounting bodies required the companies to

prepare financial statements on uniform basis. Financial statements are now prepared by the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

companies following defined accounting standards and presented in accordance with the

reporting frameworks. The accounting standards and reporting frameworks make the financial

standards comparable with the other firms. It allows the investors to make comparisons between

the growth, performance and position of the different companies.

Verifiability – The information of entity should be verifiable so that the assurance could be

framed regarding the authenticity of the transactions. all the material information in financial

statements should be supported with evidence. Users of financial information should be capable

of identifying information that is presented fairly in the statements. Information presented in the

statements is audited by the recognised auditing firms and ensuring that all the transaction are

recorded and carried out in accordance with law and standards. It also ensures that any mistakes

or frauds are not carried out within company.

Understandability – It is an important feature which is focused over by companies while

preparing financial statements for the companies. Information given in the statements by the

companies should be understandable by the common people. Information in the statements

should be represented by the companies concisely and in a manner which is clear to common

user. Important information and polices are not excluded from the report for making them

understandable and simple (Dutta and Patatoukas, 2017). Use of highly technical language that

makes it hard for the users to get information in right context will affect the reliability of

decisions that are taken on the basis of this information. Many decisions are taken on the basis of

financial information that requires the information to be clear and accurate for making sound

decisions.

Timeliness – It is the last feature but of relevant importance. It requires that information

regarding the performance and position should be provided timely to users of financial

statements for making accurate and informed decisions. If financial information containing

material events and transactions capable of influencing the decisions are not provided on time it

could cause serious consequences to users.

Question 2a)

Ratio Analysis

Year 1 Year 2

Employed Capital 3810 4760

3

reporting frameworks. The accounting standards and reporting frameworks make the financial

standards comparable with the other firms. It allows the investors to make comparisons between

the growth, performance and position of the different companies.

Verifiability – The information of entity should be verifiable so that the assurance could be

framed regarding the authenticity of the transactions. all the material information in financial

statements should be supported with evidence. Users of financial information should be capable

of identifying information that is presented fairly in the statements. Information presented in the

statements is audited by the recognised auditing firms and ensuring that all the transaction are

recorded and carried out in accordance with law and standards. It also ensures that any mistakes

or frauds are not carried out within company.

Understandability – It is an important feature which is focused over by companies while

preparing financial statements for the companies. Information given in the statements by the

companies should be understandable by the common people. Information in the statements

should be represented by the companies concisely and in a manner which is clear to common

user. Important information and polices are not excluded from the report for making them

understandable and simple (Dutta and Patatoukas, 2017). Use of highly technical language that

makes it hard for the users to get information in right context will affect the reliability of

decisions that are taken on the basis of this information. Many decisions are taken on the basis of

financial information that requires the information to be clear and accurate for making sound

decisions.

Timeliness – It is the last feature but of relevant importance. It requires that information

regarding the performance and position should be provided timely to users of financial

statements for making accurate and informed decisions. If financial information containing

material events and transactions capable of influencing the decisions are not provided on time it

could cause serious consequences to users.

Question 2a)

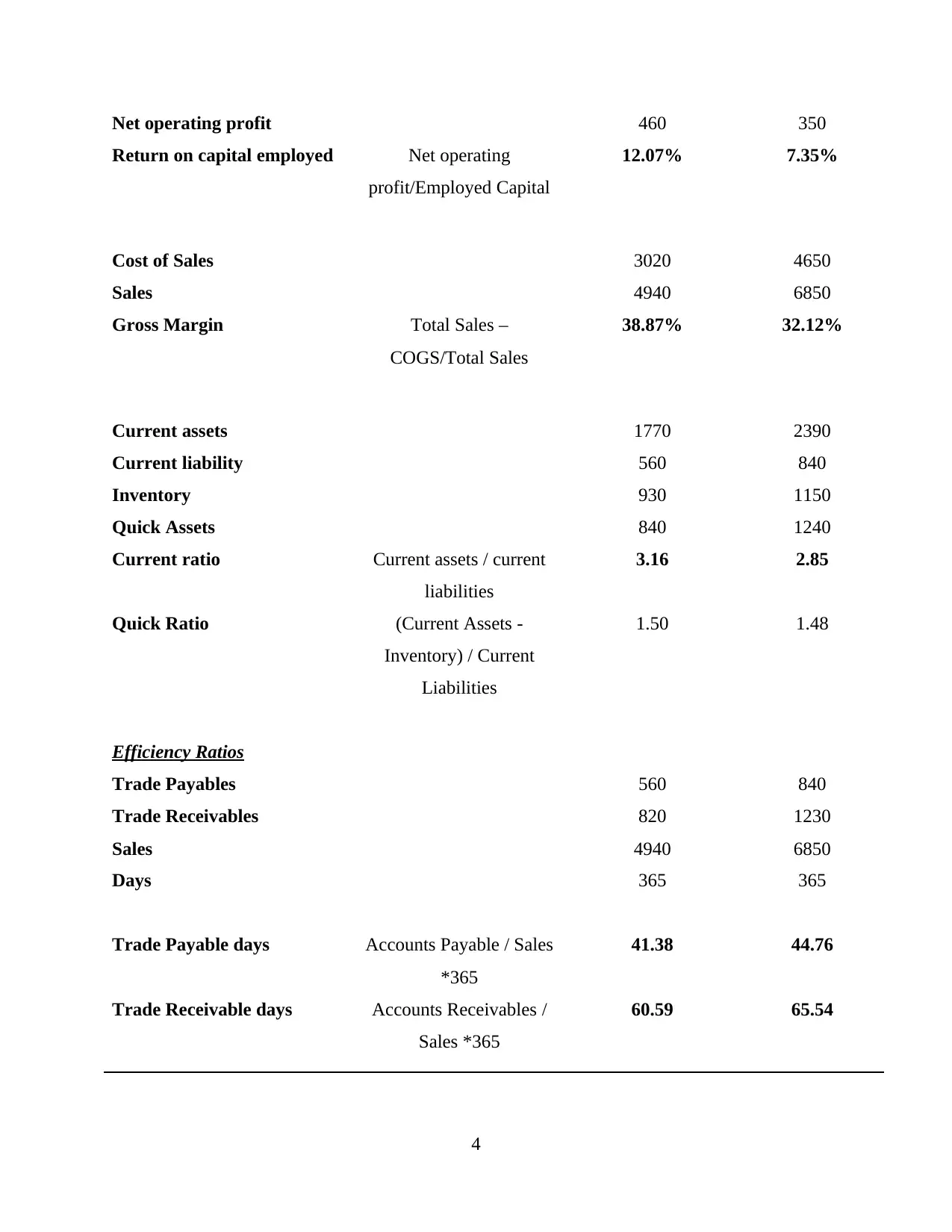

Ratio Analysis

Year 1 Year 2

Employed Capital 3810 4760

3

Net operating profit 460 350

Return on capital employed Net operating

profit/Employed Capital

12.07% 7.35%

Cost of Sales 3020 4650

Sales 4940 6850

Gross Margin Total Sales –

COGS/Total Sales

38.87% 32.12%

Current assets 1770 2390

Current liability 560 840

Inventory 930 1150

Quick Assets 840 1240

Current ratio Current assets / current

liabilities

3.16 2.85

Quick Ratio (Current Assets -

Inventory) / Current

Liabilities

1.50 1.48

Efficiency Ratios

Trade Payables 560 840

Trade Receivables 820 1230

Sales 4940 6850

Days 365 365

Trade Payable days Accounts Payable / Sales

*365

41.38 44.76

Trade Receivable days Accounts Receivables /

Sales *365

60.59 65.54

4

Return on capital employed Net operating

profit/Employed Capital

12.07% 7.35%

Cost of Sales 3020 4650

Sales 4940 6850

Gross Margin Total Sales –

COGS/Total Sales

38.87% 32.12%

Current assets 1770 2390

Current liability 560 840

Inventory 930 1150

Quick Assets 840 1240

Current ratio Current assets / current

liabilities

3.16 2.85

Quick Ratio (Current Assets -

Inventory) / Current

Liabilities

1.50 1.48

Efficiency Ratios

Trade Payables 560 840

Trade Receivables 820 1230

Sales 4940 6850

Days 365 365

Trade Payable days Accounts Payable / Sales

*365

41.38 44.76

Trade Receivable days Accounts Receivables /

Sales *365

60.59 65.54

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

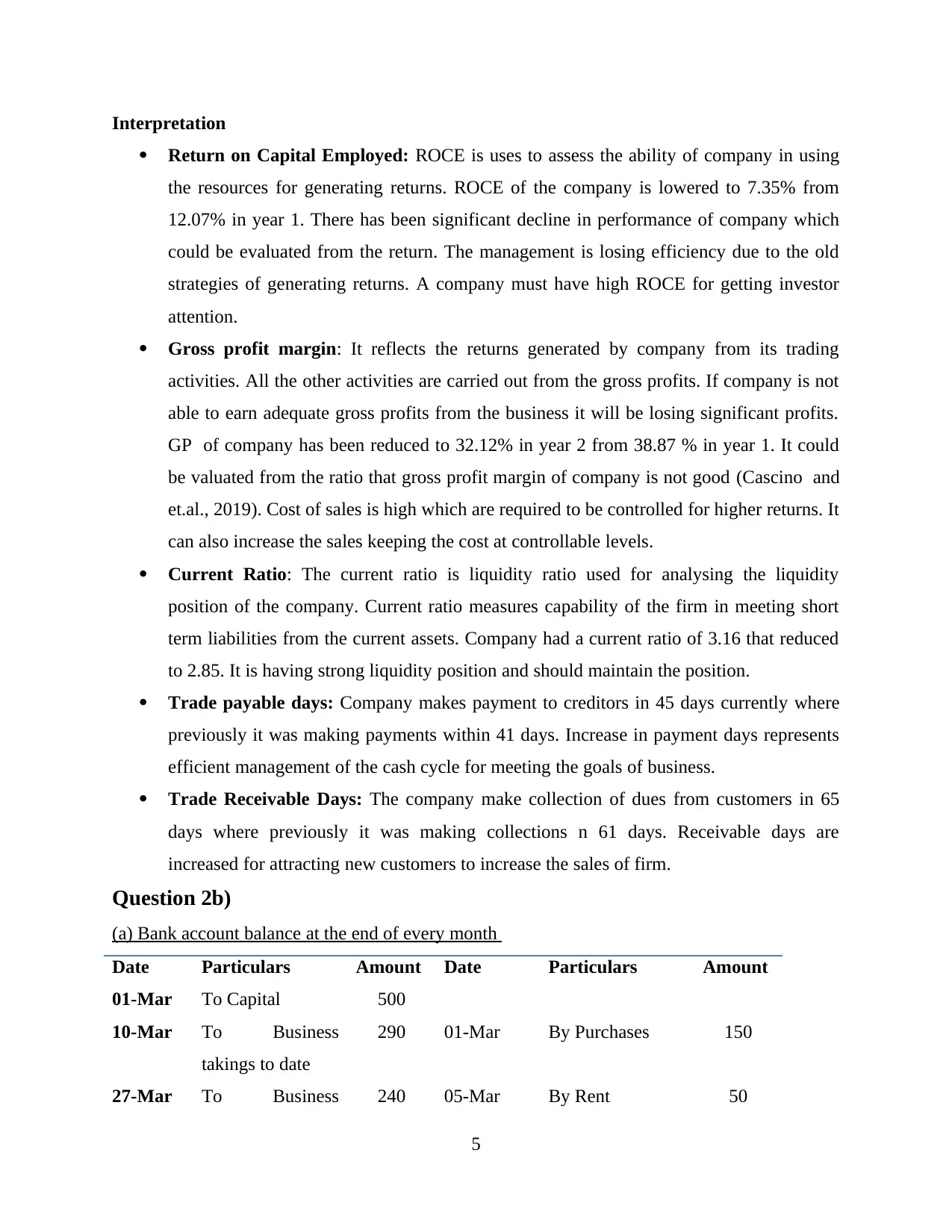

Interpretation

Return on Capital Employed: ROCE is uses to assess the ability of company in using

the resources for generating returns. ROCE of the company is lowered to 7.35% from

12.07% in year 1. There has been significant decline in performance of company which

could be evaluated from the return. The management is losing efficiency due to the old

strategies of generating returns. A company must have high ROCE for getting investor

attention.

Gross profit margin: It reflects the returns generated by company from its trading

activities. All the other activities are carried out from the gross profits. If company is not

able to earn adequate gross profits from the business it will be losing significant profits.

GP of company has been reduced to 32.12% in year 2 from 38.87 % in year 1. It could

be valuated from the ratio that gross profit margin of company is not good (Cascino and

et.al., 2019). Cost of sales is high which are required to be controlled for higher returns. It

can also increase the sales keeping the cost at controllable levels.

Current Ratio: The current ratio is liquidity ratio used for analysing the liquidity

position of the company. Current ratio measures capability of the firm in meeting short

term liabilities from the current assets. Company had a current ratio of 3.16 that reduced

to 2.85. It is having strong liquidity position and should maintain the position.

Trade payable days: Company makes payment to creditors in 45 days currently where

previously it was making payments within 41 days. Increase in payment days represents

efficient management of the cash cycle for meeting the goals of business.

Trade Receivable Days: The company make collection of dues from customers in 65

days where previously it was making collections n 61 days. Receivable days are

increased for attracting new customers to increase the sales of firm.

Question 2b)

(a) Bank account balance at the end of every month

Date Particulars Amount Date Particulars Amount

01-Mar To Capital 500

10-Mar To Business

takings to date

290 01-Mar By Purchases 150

27-Mar To Business 240 05-Mar By Rent 50

5

Return on Capital Employed: ROCE is uses to assess the ability of company in using

the resources for generating returns. ROCE of the company is lowered to 7.35% from

12.07% in year 1. There has been significant decline in performance of company which

could be evaluated from the return. The management is losing efficiency due to the old

strategies of generating returns. A company must have high ROCE for getting investor

attention.

Gross profit margin: It reflects the returns generated by company from its trading

activities. All the other activities are carried out from the gross profits. If company is not

able to earn adequate gross profits from the business it will be losing significant profits.

GP of company has been reduced to 32.12% in year 2 from 38.87 % in year 1. It could

be valuated from the ratio that gross profit margin of company is not good (Cascino and

et.al., 2019). Cost of sales is high which are required to be controlled for higher returns. It

can also increase the sales keeping the cost at controllable levels.

Current Ratio: The current ratio is liquidity ratio used for analysing the liquidity

position of the company. Current ratio measures capability of the firm in meeting short

term liabilities from the current assets. Company had a current ratio of 3.16 that reduced

to 2.85. It is having strong liquidity position and should maintain the position.

Trade payable days: Company makes payment to creditors in 45 days currently where

previously it was making payments within 41 days. Increase in payment days represents

efficient management of the cash cycle for meeting the goals of business.

Trade Receivable Days: The company make collection of dues from customers in 65

days where previously it was making collections n 61 days. Receivable days are

increased for attracting new customers to increase the sales of firm.

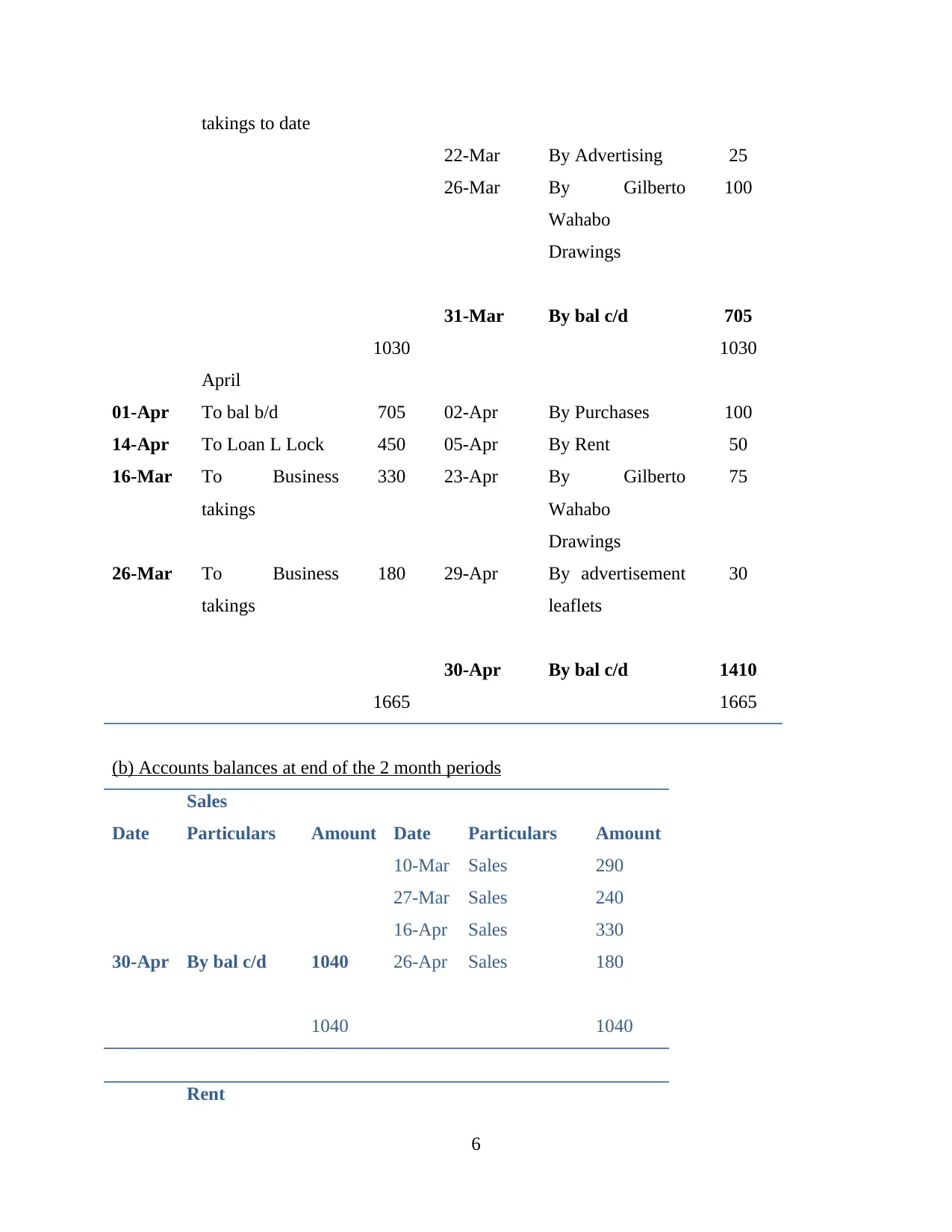

Question 2b)

(a) Bank account balance at the end of every month

Date Particulars Amount Date Particulars Amount

01-Mar To Capital 500

10-Mar To Business

takings to date

290 01-Mar By Purchases 150

27-Mar To Business 240 05-Mar By Rent 50

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

takings to date

22-Mar By Advertising 25

26-Mar By Gilberto

Wahabo

Drawings

100

31-Mar By bal c/d 705

1030 1030

April

01-Apr To bal b/d 705 02-Apr By Purchases 100

14-Apr To Loan L Lock 450 05-Apr By Rent 50

16-Mar To Business

takings

330 23-Apr By Gilberto

Wahabo

Drawings

75

26-Mar To Business

takings

180 29-Apr By advertisement

leaflets

30

30-Apr By bal c/d 1410

1665 1665

(b) Accounts balances at end of the 2 month periods

Sales

Date Particulars Amount Date Particulars Amount

10-Mar Sales 290

27-Mar Sales 240

16-Apr Sales 330

30-Apr By bal c/d 1040 26-Apr Sales 180

1040 1040

Rent

6

22-Mar By Advertising 25

26-Mar By Gilberto

Wahabo

Drawings

100

31-Mar By bal c/d 705

1030 1030

April

01-Apr To bal b/d 705 02-Apr By Purchases 100

14-Apr To Loan L Lock 450 05-Apr By Rent 50

16-Mar To Business

takings

330 23-Apr By Gilberto

Wahabo

Drawings

75

26-Mar To Business

takings

180 29-Apr By advertisement

leaflets

30

30-Apr By bal c/d 1410

1665 1665

(b) Accounts balances at end of the 2 month periods

Sales

Date Particulars Amount Date Particulars Amount

10-Mar Sales 290

27-Mar Sales 240

16-Apr Sales 330

30-Apr By bal c/d 1040 26-Apr Sales 180

1040 1040

Rent

6

Date Particulars Amount Date Particulars Amount

05-

Mar

To Bank 50

05-Apr To Bank 50 30-Apr bal c/d 100

100 100

Advertisements

Date Particulars Amount Date Particulars Amount

22-

Mar

To Bank 25

29-Apr To Bank 30 30-Apr bal c/d 55

55 55

Loan L. lock

Date Particulars Amount Date Particulars Amount

14-Apr By Bank 450

30-Apr Bal c/d 450

450 450

Capital A/c

Date Particulars Amount Date Particulars Amount

01-Mar By bank 500

30-Apr By bal c/d 500

500 500

Drawings

Date Particulars Amount Date Particulars Amount

7

05-

Mar

To Bank 50

05-Apr To Bank 50 30-Apr bal c/d 100

100 100

Advertisements

Date Particulars Amount Date Particulars Amount

22-

Mar

To Bank 25

29-Apr To Bank 30 30-Apr bal c/d 55

55 55

Loan L. lock

Date Particulars Amount Date Particulars Amount

14-Apr By Bank 450

30-Apr Bal c/d 450

450 450

Capital A/c

Date Particulars Amount Date Particulars Amount

01-Mar By bank 500

30-Apr By bal c/d 500

500 500

Drawings

Date Particulars Amount Date Particulars Amount

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

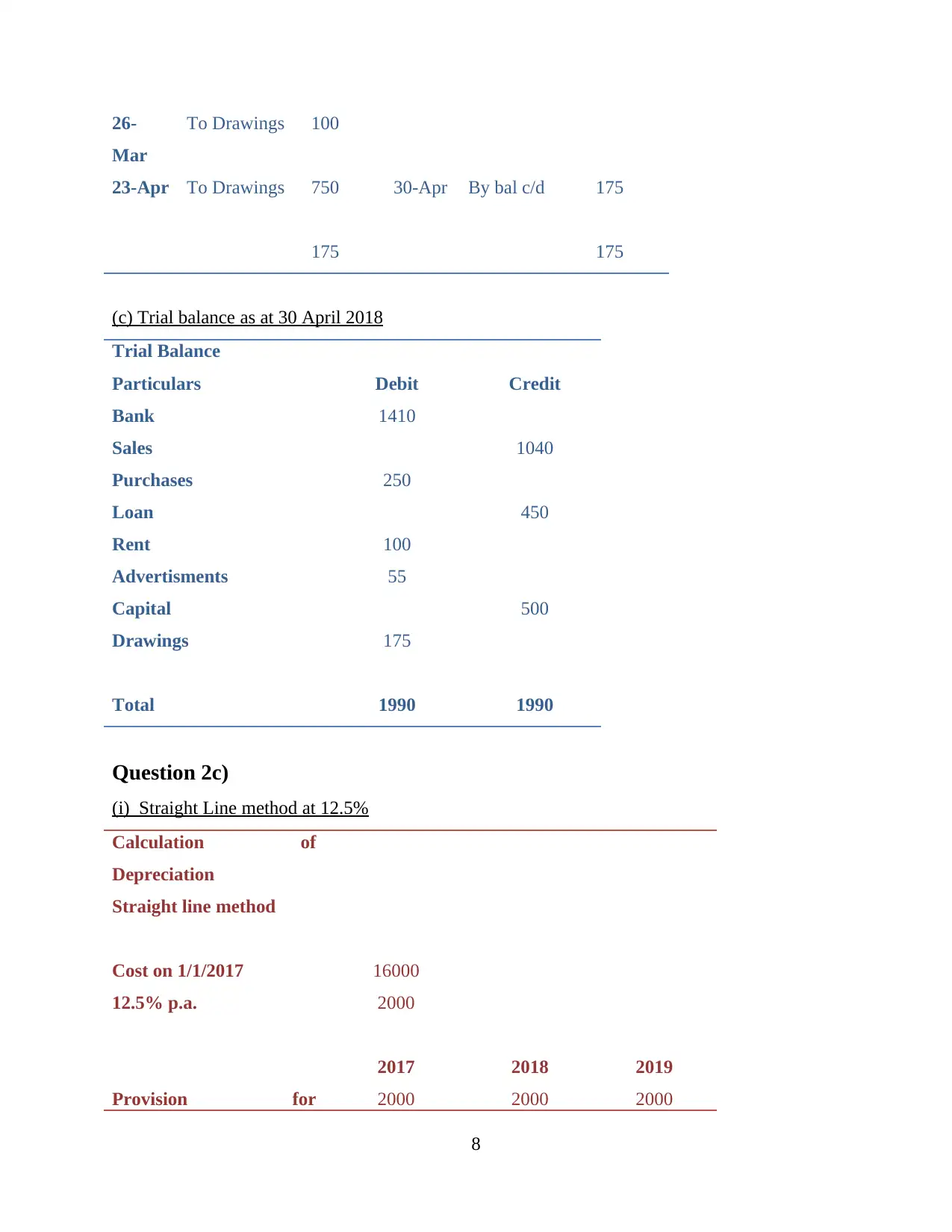

26-

Mar

To Drawings 100

23-Apr To Drawings 750 30-Apr By bal c/d 175

175 175

(c) Trial balance as at 30 April 2018

Trial Balance

Particulars Debit Credit

Bank 1410

Sales 1040

Purchases 250

Loan 450

Rent 100

Advertisments 55

Capital 500

Drawings 175

Total 1990 1990

Question 2c)

(i) Straight Line method at 12.5%

Calculation of

Depreciation

Straight line method

Cost on 1/1/2017 16000

12.5% p.a. 2000

2017 2018 2019

Provision for 2000 2000 2000

8

Mar

To Drawings 100

23-Apr To Drawings 750 30-Apr By bal c/d 175

175 175

(c) Trial balance as at 30 April 2018

Trial Balance

Particulars Debit Credit

Bank 1410

Sales 1040

Purchases 250

Loan 450

Rent 100

Advertisments 55

Capital 500

Drawings 175

Total 1990 1990

Question 2c)

(i) Straight Line method at 12.5%

Calculation of

Depreciation

Straight line method

Cost on 1/1/2017 16000

12.5% p.a. 2000

2017 2018 2019

Provision for 2000 2000 2000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

depreciation

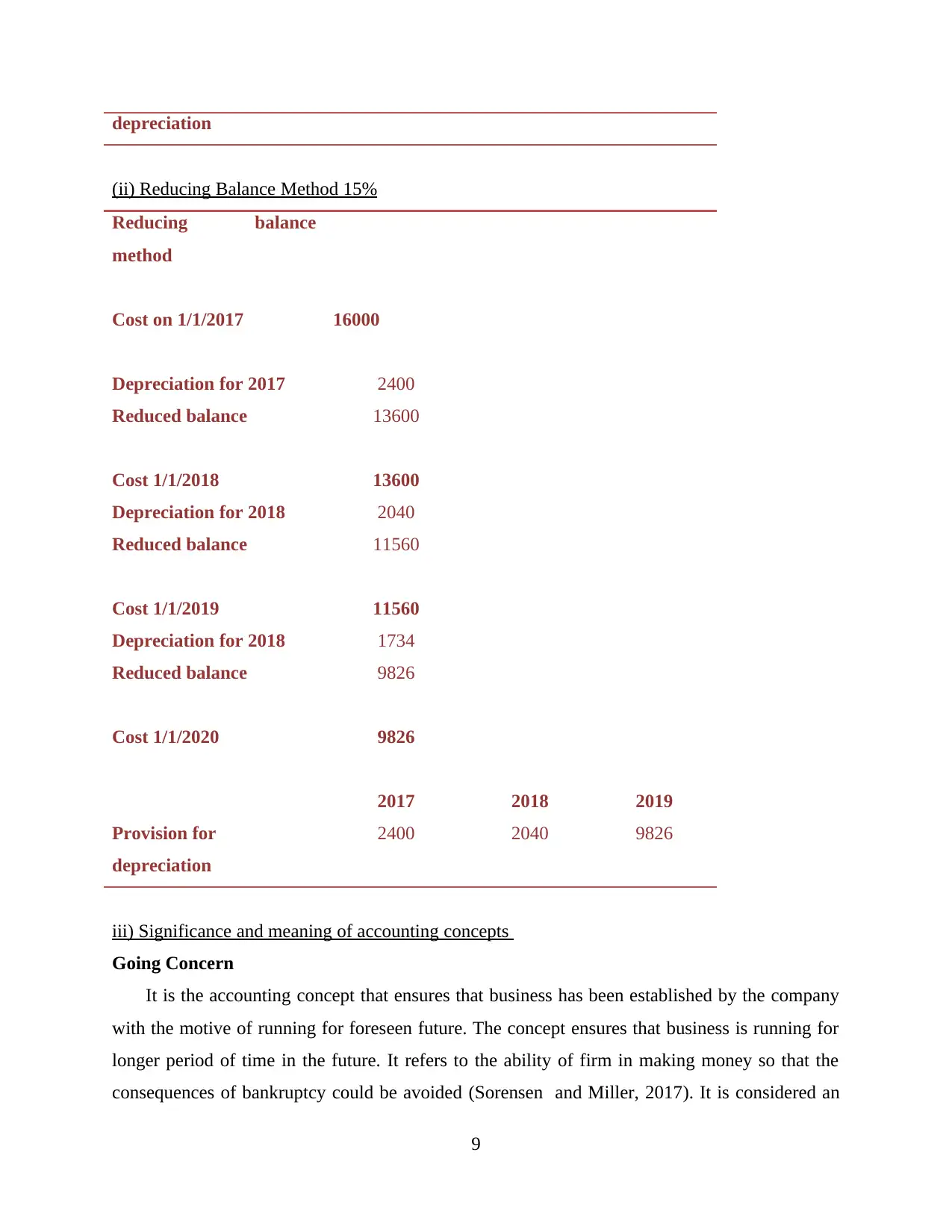

(ii) Reducing Balance Method 15%

Reducing balance

method

Cost on 1/1/2017 16000

Depreciation for 2017 2400

Reduced balance 13600

Cost 1/1/2018 13600

Depreciation for 2018 2040

Reduced balance 11560

Cost 1/1/2019 11560

Depreciation for 2018 1734

Reduced balance 9826

Cost 1/1/2020 9826

2017 2018 2019

Provision for

depreciation

2400 2040 9826

iii) Significance and meaning of accounting concepts

Going Concern

It is the accounting concept that ensures that business has been established by the company

with the motive of running for foreseen future. The concept ensures that business is running for

longer period of time in the future. It refers to the ability of firm in making money so that the

consequences of bankruptcy could be avoided (Sorensen and Miller, 2017). It is considered an

9

(ii) Reducing Balance Method 15%

Reducing balance

method

Cost on 1/1/2017 16000

Depreciation for 2017 2400

Reduced balance 13600

Cost 1/1/2018 13600

Depreciation for 2018 2040

Reduced balance 11560

Cost 1/1/2019 11560

Depreciation for 2018 1734

Reduced balance 9826

Cost 1/1/2020 9826

2017 2018 2019

Provision for

depreciation

2400 2040 9826

iii) Significance and meaning of accounting concepts

Going Concern

It is the accounting concept that ensures that business has been established by the company

with the motive of running for foreseen future. The concept ensures that business is running for

longer period of time in the future. It refers to the ability of firm in making money so that the

consequences of bankruptcy could be avoided (Sorensen and Miller, 2017). It is considered an

9

essential and important accounting concept which allows the business in deferring expenses of

the business for the future accounting period instead of recognising them in one year. It also

protects the third parties by ensuring that business will be carried out in future in which it will be

meeting the financial obligations. There are various expenses and cost that are deferred by the

business under going concept. It motivates the employees to work hard for achieving growth and

promotions in coming years.

Materiality Concept

Materiality in accounting refers to information and transactions that are of significant

value and cause considerable impact over the business. It also refers to impact of errors or

omission in the financial statements over the users of financial information. The concept requires

that all the material information should be presented by the management in the financial

statement. For example a contingent liability of 1 million is material and can influence the

decisions of buyers and therefore should be included in the financial statements. The accounting

concept enables the management to analyse that statements prepared are not misleading and

represent the position of company accurately disclosing all the relevant information. It is a

fundamental accounting principle which is followed by all the organisations preparing financial

records.

Business entity Concept

The accounting concept state business is separate from the owners running it. In the

language of law company is a separate legal entity from its owners and promoters forming it.

The focus of accounting concept is that the business should be considered different from the

owners. From this concept it could be evaluated that business has the separate standing from the

owners and should be considered as a separate unit (Persson, 2019). It is essential for ensuring

that the personal and financial transactions are not treated as single business transactions and

added in business records. It enables the company to recognise business and personal

transactions separately.

10

the business for the future accounting period instead of recognising them in one year. It also

protects the third parties by ensuring that business will be carried out in future in which it will be

meeting the financial obligations. There are various expenses and cost that are deferred by the

business under going concept. It motivates the employees to work hard for achieving growth and

promotions in coming years.

Materiality Concept

Materiality in accounting refers to information and transactions that are of significant

value and cause considerable impact over the business. It also refers to impact of errors or

omission in the financial statements over the users of financial information. The concept requires

that all the material information should be presented by the management in the financial

statement. For example a contingent liability of 1 million is material and can influence the

decisions of buyers and therefore should be included in the financial statements. The accounting

concept enables the management to analyse that statements prepared are not misleading and

represent the position of company accurately disclosing all the relevant information. It is a

fundamental accounting principle which is followed by all the organisations preparing financial

records.

Business entity Concept

The accounting concept state business is separate from the owners running it. In the

language of law company is a separate legal entity from its owners and promoters forming it.

The focus of accounting concept is that the business should be considered different from the

owners. From this concept it could be evaluated that business has the separate standing from the

owners and should be considered as a separate unit (Persson, 2019). It is essential for ensuring

that the personal and financial transactions are not treated as single business transactions and

added in business records. It enables the company to recognise business and personal

transactions separately.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.