ACCT1059: Auditing Question 2022

Added on 2022-10-17

7 Pages4498 Words8 Views

ACCT1059: Auditing 1

Name

Institution

Course

Tutor

Date

Name

Institution

Course

Tutor

Date

Questions:

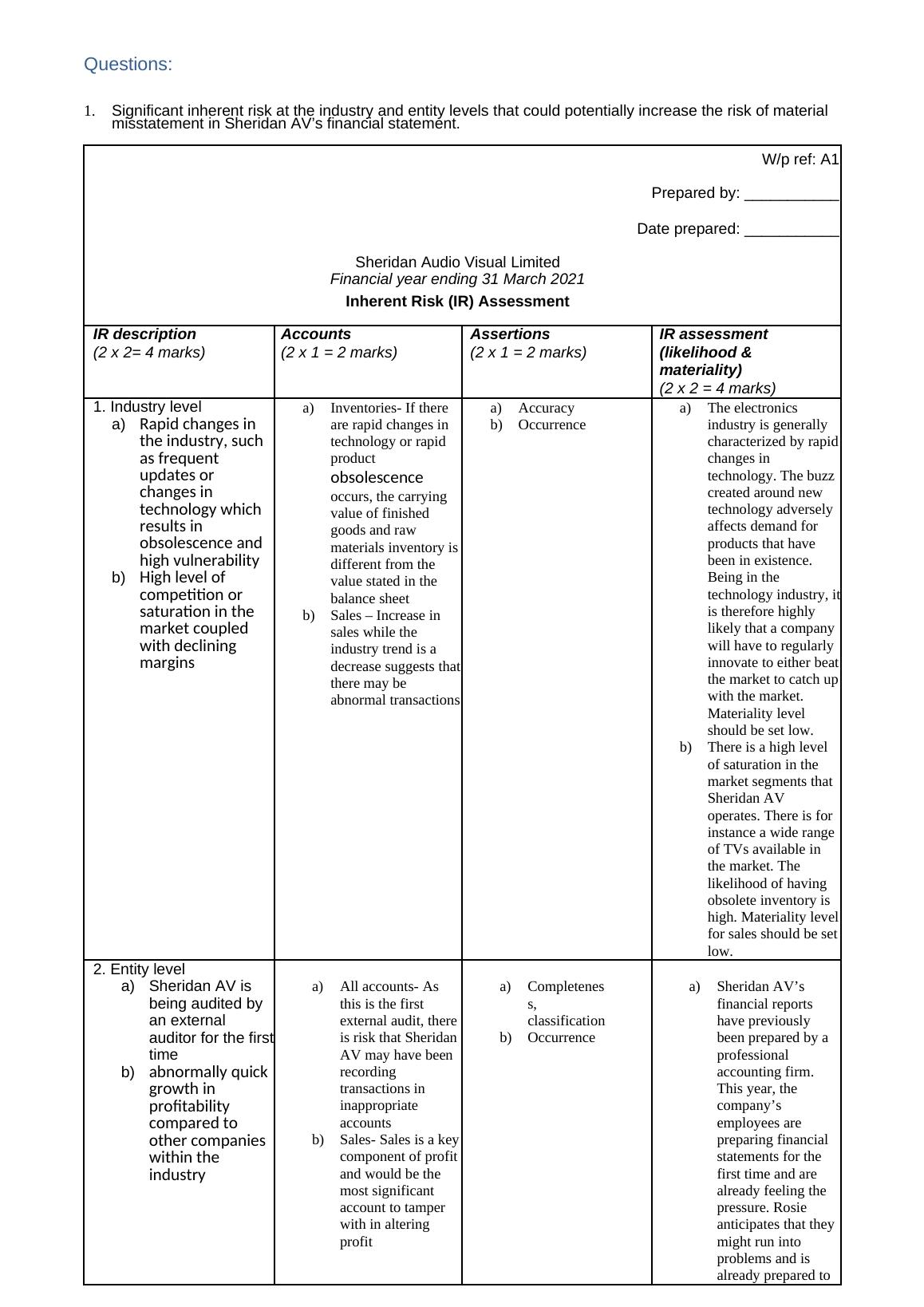

1. Significant inherent risk at the industry and entity levels that could potentially increase the risk of material

misstatement in Sheridan AV’s financial statement.

W/p ref: A1

Prepared by: ___________

Date prepared: ___________

Sheridan Audio Visual Limited

Financial year ending 31 March 2021

Inherent Risk (IR) Assessment

IR description Accounts Assertions IR assessment

(2 x 2= 4 marks) (2 x 1 = 2 marks) (2 x 1 = 2 marks) (likelihood &

materiality)

(2 x 2 = 4 marks)

1. Industry level

a) Rapid changes

in the industry,

such as

frequent

updates or

changes in

technology

which results in

obsolescence

and high

vulnerability

b) High level of

competition or

saturation in

the market

coupled with

declining

margins

a) Inventories- If there

are rapid changes in

technology or rapid

product

obsolescence

occurs, the carrying

value of finished

goods and raw

materials inventory is

different from the

value stated in the

balance sheet

b) Sales – Increase in

sales while the

industry trend is a

decrease suggests that

there may be

abnormal transactions

a) Accuracy

b) Occurrence

a) The electronics

industry is generally

characterized by rapid

changes in

technology. The buzz

created around new

technology adversely

affects demand for

products that have

been in existence.

Being in the

technology industry, it

is therefore highly

likely that a company

will have to regularly

innovate to either beat

the market to catch up

with the market.

Materiality level

should be set low.

b) There is a high level

of saturation in the

market segments that

Sheridan AV

operates. There is for

instance a wide range

of TVs available in

the market. The

likelihood of having

obsolete inventory is

high. Materiality level

for sales should be set

low.

2. Entity level

a) Sheridan AV is

being audited by

an external

auditor for the first

time

b) abnormally

quick growth

in profitability

compared to

other

companies

within the

industry

a) All accounts- As

this is the first

external audit, there

is risk that Sheridan

AV may have been

recording

transactions in

inappropriate

accounts

b) Sales- Sales is a key

component of profit

and would be the

most significant

account to tamper

with in altering

profit

a) Completenes

s,

classification

b) Occurrence

a) Sheridan AV’s

financial reports

have previously

been prepared by a

professional

accounting firm.

This year, the

company’s

employees are

preparing financial

statements for the

first time and are

already feeling the

pressure. Rosie

anticipates that they

might run into

problems and is

already prepared to

1. Significant inherent risk at the industry and entity levels that could potentially increase the risk of material

misstatement in Sheridan AV’s financial statement.

W/p ref: A1

Prepared by: ___________

Date prepared: ___________

Sheridan Audio Visual Limited

Financial year ending 31 March 2021

Inherent Risk (IR) Assessment

IR description Accounts Assertions IR assessment

(2 x 2= 4 marks) (2 x 1 = 2 marks) (2 x 1 = 2 marks) (likelihood &

materiality)

(2 x 2 = 4 marks)

1. Industry level

a) Rapid changes

in the industry,

such as

frequent

updates or

changes in

technology

which results in

obsolescence

and high

vulnerability

b) High level of

competition or

saturation in

the market

coupled with

declining

margins

a) Inventories- If there

are rapid changes in

technology or rapid

product

obsolescence

occurs, the carrying

value of finished

goods and raw

materials inventory is

different from the

value stated in the

balance sheet

b) Sales – Increase in

sales while the

industry trend is a

decrease suggests that

there may be

abnormal transactions

a) Accuracy

b) Occurrence

a) The electronics

industry is generally

characterized by rapid

changes in

technology. The buzz

created around new

technology adversely

affects demand for

products that have

been in existence.

Being in the

technology industry, it

is therefore highly

likely that a company

will have to regularly

innovate to either beat

the market to catch up

with the market.

Materiality level

should be set low.

b) There is a high level

of saturation in the

market segments that

Sheridan AV

operates. There is for

instance a wide range

of TVs available in

the market. The

likelihood of having

obsolete inventory is

high. Materiality level

for sales should be set

low.

2. Entity level

a) Sheridan AV is

being audited by

an external

auditor for the first

time

b) abnormally

quick growth

in profitability

compared to

other

companies

within the

industry

a) All accounts- As

this is the first

external audit, there

is risk that Sheridan

AV may have been

recording

transactions in

inappropriate

accounts

b) Sales- Sales is a key

component of profit

and would be the

most significant

account to tamper

with in altering

profit

a) Completenes

s,

classification

b) Occurrence

a) Sheridan AV’s

financial reports

have previously

been prepared by a

professional

accounting firm.

This year, the

company’s

employees are

preparing financial

statements for the

first time and are

already feeling the

pressure. Rosie

anticipates that they

might run into

problems and is

already prepared to

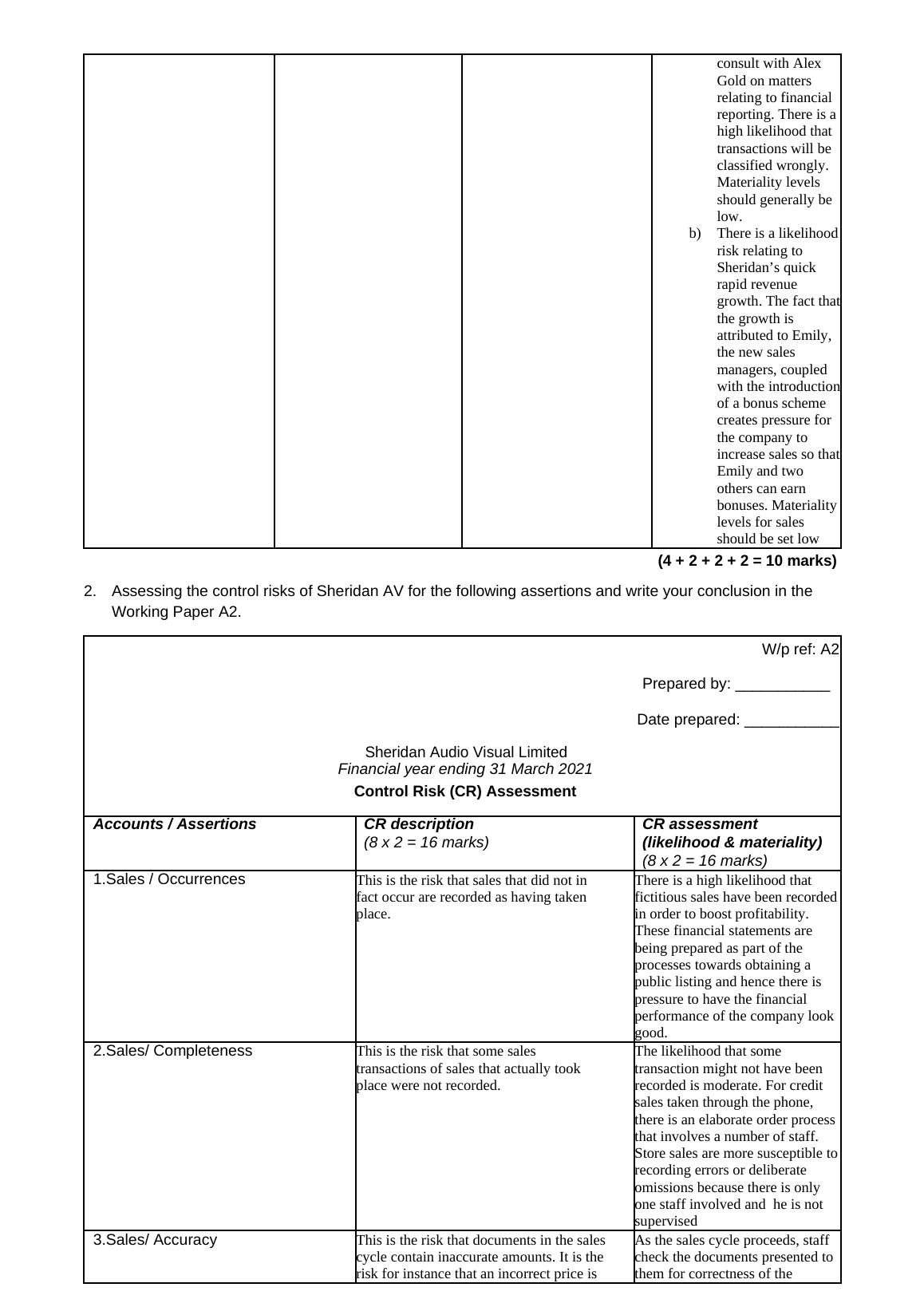

consult with Alex

Gold on matters

relating to financial

reporting. There is a

high likelihood that

transactions will be

classified wrongly.

Materiality levels

should generally be

low.

b) There is a likelihood

risk relating to

Sheridan’s quick

rapid revenue

growth. The fact that

the growth is

attributed to Emily,

the new sales

managers, coupled

with the introduction

of a bonus scheme

creates pressure for

the company to

increase sales so that

Emily and two

others can earn

bonuses. Materiality

levels for sales

should be set low

(4 + 2 + 2 + 2 = 10 marks)

2. Assessing the control risks of Sheridan AV for the following assertions and write your conclusion in the

Working Paper A2.

W/p ref: A2

Prepared by: ___________

Date prepared: ___________

Sheridan Audio Visual Limited

Financial year ending 31 March 2021

Control Risk (CR) Assessment

Accounts / Assertions CR description CR assessment

(8 x 2 = 16 marks) (likelihood & materiality)

(8 x 2 = 16 marks)

1.Sales / Occurrences This is the risk that sales that did not in

fact occur are recorded as having taken

place.

There is a high likelihood that

fictitious sales have been recorded

in order to boost profitability.

These financial statements are

being prepared as part of the

processes towards obtaining a

public listing and hence there is

pressure to have the financial

performance of the company look

good.

2.Sales/ Completeness This is the risk that some sales

transactions of sales that actually took

place were not recorded.

The likelihood that some

transaction might not have been

recorded is moderate. For credit

sales taken through the phone,

there is an elaborate order process

that involves a number of staff.

Store sales are more susceptible to

recording errors or deliberate

omissions because there is only

one staff involved and he is not

supervised

3.Sales/ Accuracy This is the risk that documents in the sales

cycle contain inaccurate amounts. It is the

risk for instance that an incorrect price is

As the sales cycle proceeds, staff

check the documents presented to

them for correctness of the

Gold on matters

relating to financial

reporting. There is a

high likelihood that

transactions will be

classified wrongly.

Materiality levels

should generally be

low.

b) There is a likelihood

risk relating to

Sheridan’s quick

rapid revenue

growth. The fact that

the growth is

attributed to Emily,

the new sales

managers, coupled

with the introduction

of a bonus scheme

creates pressure for

the company to

increase sales so that

Emily and two

others can earn

bonuses. Materiality

levels for sales

should be set low

(4 + 2 + 2 + 2 = 10 marks)

2. Assessing the control risks of Sheridan AV for the following assertions and write your conclusion in the

Working Paper A2.

W/p ref: A2

Prepared by: ___________

Date prepared: ___________

Sheridan Audio Visual Limited

Financial year ending 31 March 2021

Control Risk (CR) Assessment

Accounts / Assertions CR description CR assessment

(8 x 2 = 16 marks) (likelihood & materiality)

(8 x 2 = 16 marks)

1.Sales / Occurrences This is the risk that sales that did not in

fact occur are recorded as having taken

place.

There is a high likelihood that

fictitious sales have been recorded

in order to boost profitability.

These financial statements are

being prepared as part of the

processes towards obtaining a

public listing and hence there is

pressure to have the financial

performance of the company look

good.

2.Sales/ Completeness This is the risk that some sales

transactions of sales that actually took

place were not recorded.

The likelihood that some

transaction might not have been

recorded is moderate. For credit

sales taken through the phone,

there is an elaborate order process

that involves a number of staff.

Store sales are more susceptible to

recording errors or deliberate

omissions because there is only

one staff involved and he is not

supervised

3.Sales/ Accuracy This is the risk that documents in the sales

cycle contain inaccurate amounts. It is the

risk for instance that an incorrect price is

As the sales cycle proceeds, staff

check the documents presented to

them for correctness of the

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Sheridan AV Case Study 13lg...

|14

|3570

|212

Inherent Risk in Auditing & Assurancelg...

|6

|1195

|379

Management Accounting: Client Acceptance Decision, Audit Planning, Preliminary Risk Assessment, Inherent Risks, Control Risklg...

|15

|3661

|58

Auditing Theory and Practicelg...

|9

|2047

|80

Auditing Theory and Practicelg...

|11

|2147

|57

Developing an Audit Program for Chalmers Limitedlg...

|10

|680

|33