Activity Based Costing and Traditional Based Costing

VerifiedAdded on 2023/03/23

|15

|2758

|96

AI Summary

This document discusses the differences between Activity Based Costing and Traditional Based Costing methods and their impact on cost allocation. It also explores the reasons behind changes in production costs and how the cost of products can be overstated.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACTIVITY BASED COSTING AND TRADITIONAL

BASED COSTING

BASED COSTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

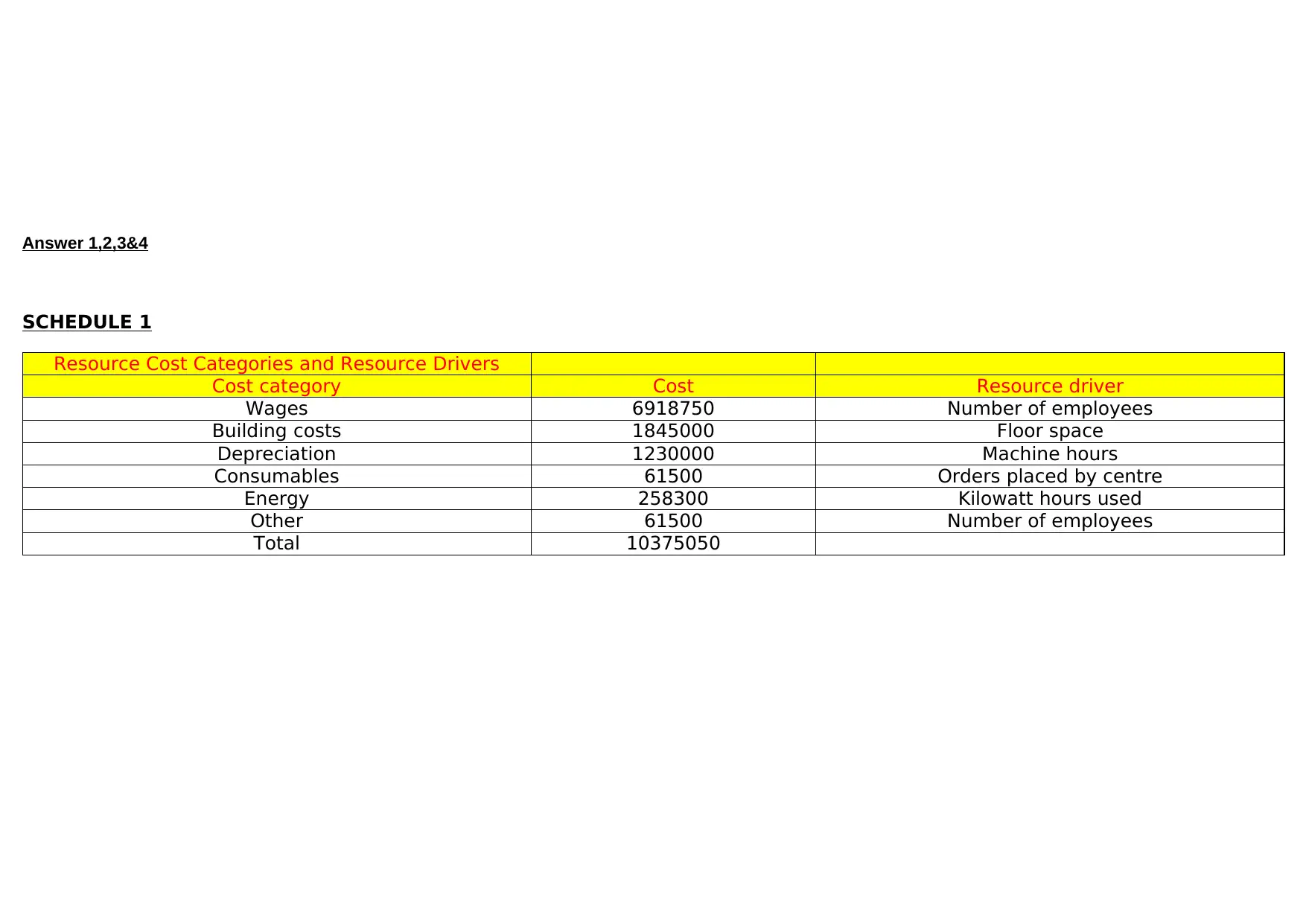

Answer 1,2,3&4

SCHEDULE 1

Resource Cost Categories and Resource Drivers

Cost category Cost Resource driver

Wages 6918750 Number of employees

Building costs 1845000 Floor space

Depreciation 1230000 Machine hours

Consumables 61500 Orders placed by centre

Energy 258300 Kilowatt hours used

Other 61500 Number of employees

Total 10375050

SCHEDULE 1

Resource Cost Categories and Resource Drivers

Cost category Cost Resource driver

Wages 6918750 Number of employees

Building costs 1845000 Floor space

Depreciation 1230000 Machine hours

Consumables 61500 Orders placed by centre

Energy 258300 Kilowatt hours used

Other 61500 Number of employees

Total 10375050

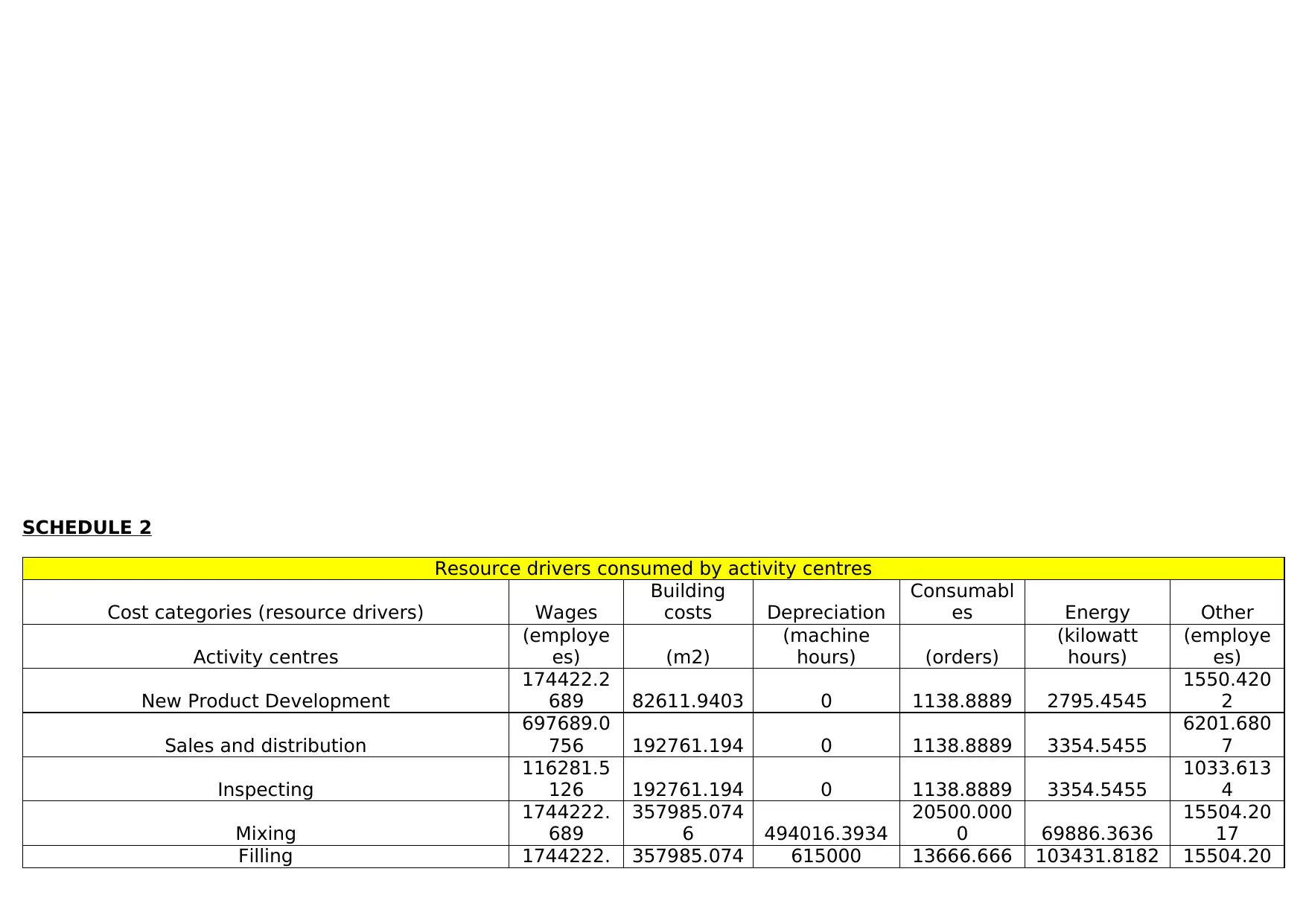

SCHEDULE 2

Resource drivers consumed by activity centres

Cost categories (resource drivers) Wages

Building

costs Depreciation

Consumabl

es Energy Other

Activity centres

(employe

es) (m2)

(machine

hours) (orders)

(kilowatt

hours)

(employe

es)

New Product Development

174422.2

689 82611.9403 0 1138.8889 2795.4545

1550.420

2

Sales and distribution

697689.0

756 192761.194 0 1138.8889 3354.5455

6201.680

7

Inspecting

116281.5

126 192761.194 0 1138.8889 3354.5455

1033.613

4

Mixing

1744222.

689

357985.074

6 494016.3934

20500.000

0 69886.3636

15504.20

17

Filling 1744222. 357985.074 615000 13666.666 103431.8182 15504.20

Resource drivers consumed by activity centres

Cost categories (resource drivers) Wages

Building

costs Depreciation

Consumabl

es Energy Other

Activity centres

(employe

es) (m2)

(machine

hours) (orders)

(kilowatt

hours)

(employe

es)

New Product Development

174422.2

689 82611.9403 0 1138.8889 2795.4545

1550.420

2

Sales and distribution

697689.0

756 192761.194 0 1138.8889 3354.5455

6201.680

7

Inspecting

116281.5

126 192761.194 0 1138.8889 3354.5455

1033.613

4

Mixing

1744222.

689

357985.074

6 494016.3934

20500.000

0 69886.3636

15504.20

17

Filling 1744222. 357985.074 615000 13666.666 103431.8182 15504.20

689 6 7 17

Baking and Packing

1395378.

151

357985.074

6 120983.6066

20500.000

0 69886.3636

12403.36

13

Administration

697689.0

756 192761.194 0 2277.7778 2795.4545

6201.680

7

Corporate management

348844.5

378

110149.253

7 0 1138.8889 2795.4545

3100.840

3

Total quantity of resource drivers across all

activity centres 6918750 1845000 1230000

61500.000

0 258300.0000

61500.00

00

Baking and Packing

1395378.

151

357985.074

6 120983.6066

20500.000

0 69886.3636

12403.36

13

Administration

697689.0

756 192761.194 0 2277.7778 2795.4545

6201.680

7

Corporate management

348844.5

378

110149.253

7 0 1138.8889 2795.4545

3100.840

3

Total quantity of resource drivers across all

activity centres 6918750 1845000 1230000

61500.000

0 258300.0000

61500.00

00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

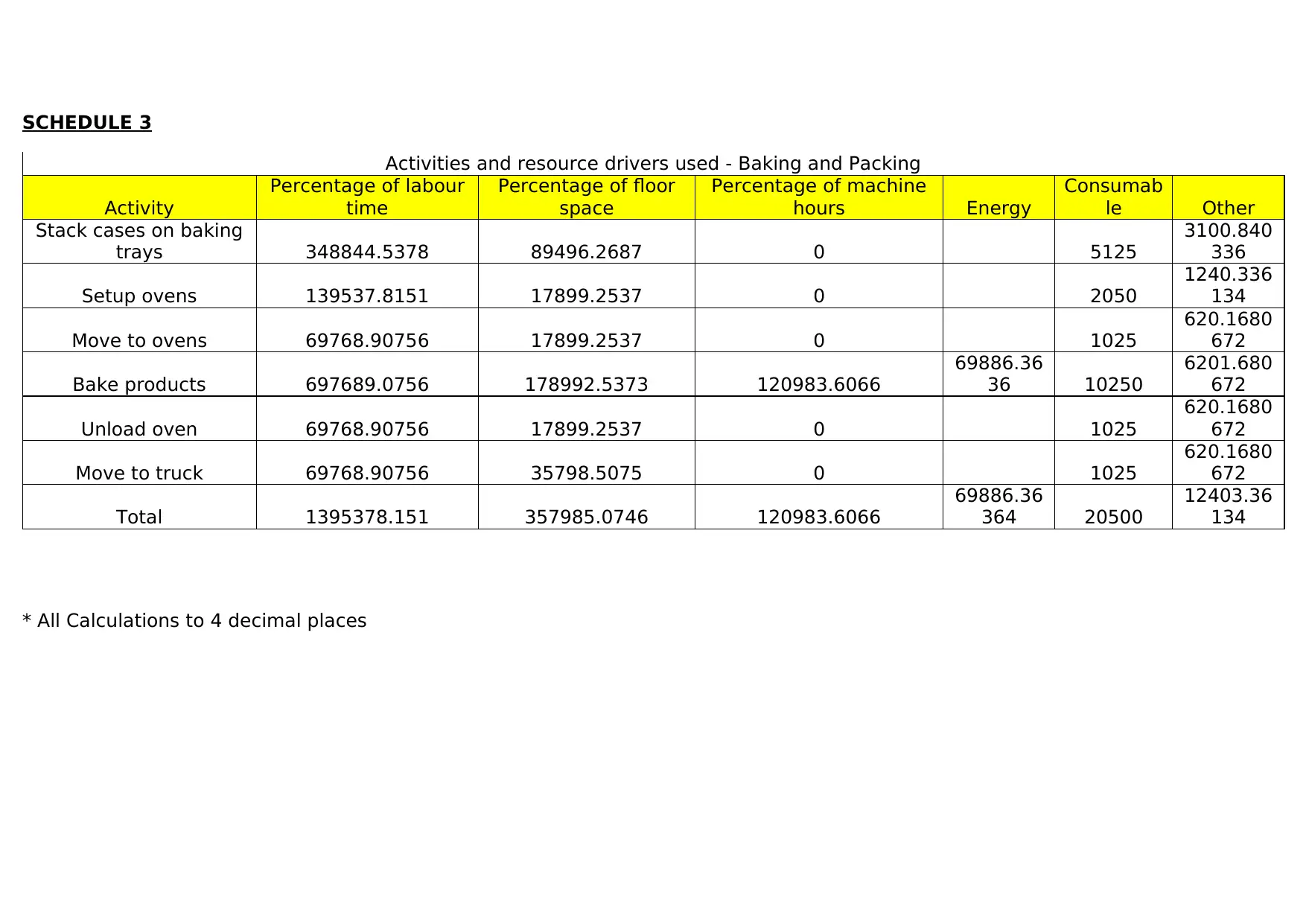

SCHEDULE 3

Activities and resource drivers used - Baking and Packing

Activity

Percentage of labour

time

Percentage of floor

space

Percentage of machine

hours Energy

Consumab

le Other

Stack cases on baking

trays 348844.5378 89496.2687 0 5125

3100.840

336

Setup ovens 139537.8151 17899.2537 0 2050

1240.336

134

Move to ovens 69768.90756 17899.2537 0 1025

620.1680

672

Bake products 697689.0756 178992.5373 120983.6066

69886.36

36 10250

6201.680

672

Unload oven 69768.90756 17899.2537 0 1025

620.1680

672

Move to truck 69768.90756 35798.5075 0 1025

620.1680

672

Total 1395378.151 357985.0746 120983.6066

69886.36

364 20500

12403.36

134

* All Calculations to 4 decimal places

Activities and resource drivers used - Baking and Packing

Activity

Percentage of labour

time

Percentage of floor

space

Percentage of machine

hours Energy

Consumab

le Other

Stack cases on baking

trays 348844.5378 89496.2687 0 5125

3100.840

336

Setup ovens 139537.8151 17899.2537 0 2050

1240.336

134

Move to ovens 69768.90756 17899.2537 0 1025

620.1680

672

Bake products 697689.0756 178992.5373 120983.6066

69886.36

36 10250

6201.680

672

Unload oven 69768.90756 17899.2537 0 1025

620.1680

672

Move to truck 69768.90756 35798.5075 0 1025

620.1680

672

Total 1395378.151 357985.0746 120983.6066

69886.36

364 20500

12403.36

134

* All Calculations to 4 decimal places

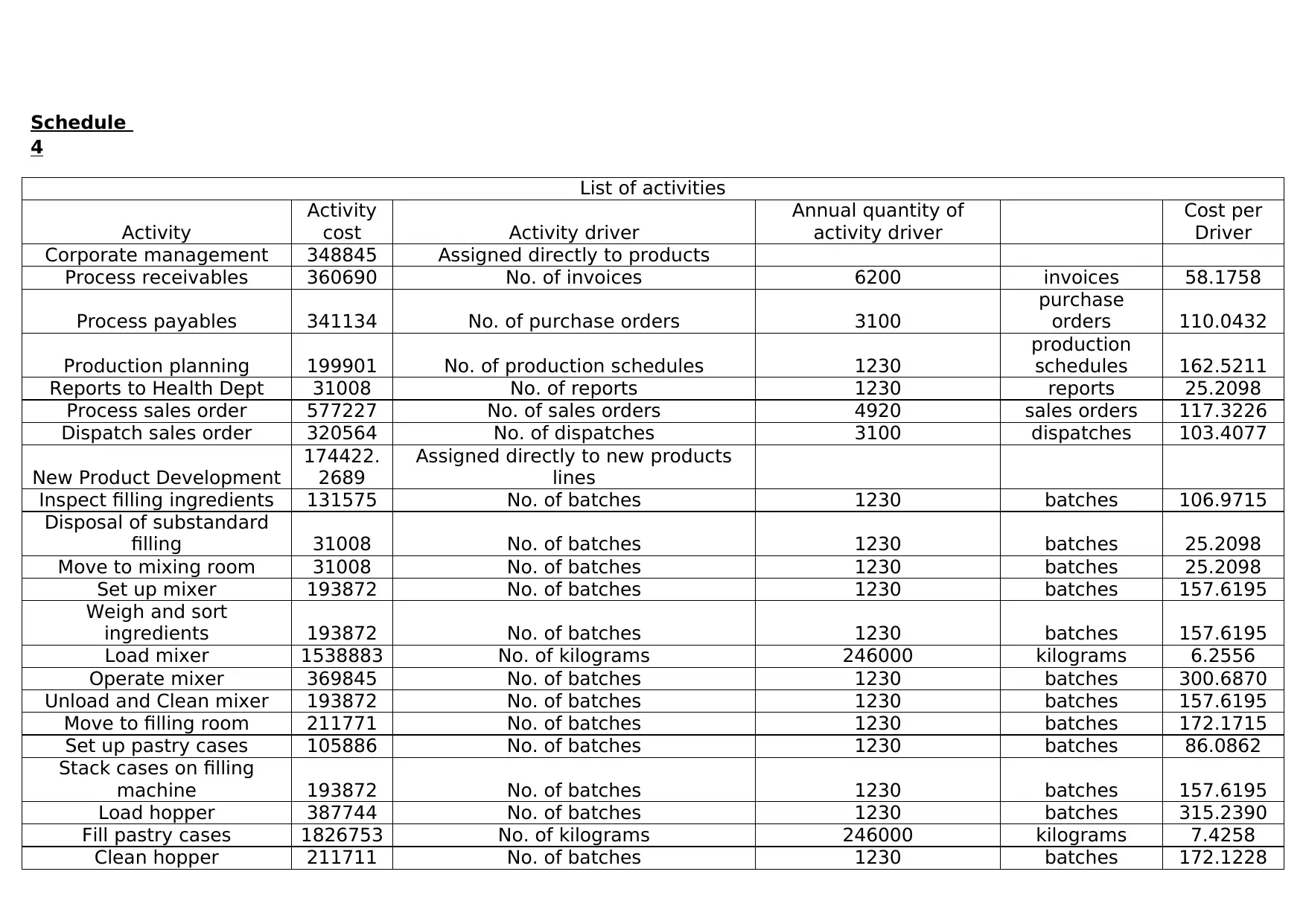

Schedule

4

List of activities

Activity

Activity

cost Activity driver

Annual quantity of

activity driver

Cost per

Driver

Corporate management 348845 Assigned directly to products

Process receivables 360690 No. of invoices 6200 invoices 58.1758

Process payables 341134 No. of purchase orders 3100

purchase

orders 110.0432

Production planning 199901 No. of production schedules 1230

production

schedules 162.5211

Reports to Health Dept 31008 No. of reports 1230 reports 25.2098

Process sales order 577227 No. of sales orders 4920 sales orders 117.3226

Dispatch sales order 320564 No. of dispatches 3100 dispatches 103.4077

New Product Development

174422.

2689

Assigned directly to new products

lines

Inspect filling ingredients 131575 No. of batches 1230 batches 106.9715

Disposal of substandard

filling 31008 No. of batches 1230 batches 25.2098

Move to mixing room 31008 No. of batches 1230 batches 25.2098

Set up mixer 193872 No. of batches 1230 batches 157.6195

Weigh and sort

ingredients 193872 No. of batches 1230 batches 157.6195

Load mixer 1538883 No. of kilograms 246000 kilograms 6.2556

Operate mixer 369845 No. of batches 1230 batches 300.6870

Unload and Clean mixer 193872 No. of batches 1230 batches 157.6195

Move to filling room 211771 No. of batches 1230 batches 172.1715

Set up pastry cases 105886 No. of batches 1230 batches 86.0862

Stack cases on filling

machine 193872 No. of batches 1230 batches 157.6195

Load hopper 387744 No. of batches 1230 batches 315.2390

Fill pastry cases 1826753 No. of kilograms 246000 kilograms 7.4258

Clean hopper 211711 No. of batches 1230 batches 172.1228

4

List of activities

Activity

Activity

cost Activity driver

Annual quantity of

activity driver

Cost per

Driver

Corporate management 348845 Assigned directly to products

Process receivables 360690 No. of invoices 6200 invoices 58.1758

Process payables 341134 No. of purchase orders 3100

purchase

orders 110.0432

Production planning 199901 No. of production schedules 1230

production

schedules 162.5211

Reports to Health Dept 31008 No. of reports 1230 reports 25.2098

Process sales order 577227 No. of sales orders 4920 sales orders 117.3226

Dispatch sales order 320564 No. of dispatches 3100 dispatches 103.4077

New Product Development

174422.

2689

Assigned directly to new products

lines

Inspect filling ingredients 131575 No. of batches 1230 batches 106.9715

Disposal of substandard

filling 31008 No. of batches 1230 batches 25.2098

Move to mixing room 31008 No. of batches 1230 batches 25.2098

Set up mixer 193872 No. of batches 1230 batches 157.6195

Weigh and sort

ingredients 193872 No. of batches 1230 batches 157.6195

Load mixer 1538883 No. of kilograms 246000 kilograms 6.2556

Operate mixer 369845 No. of batches 1230 batches 300.6870

Unload and Clean mixer 193872 No. of batches 1230 batches 157.6195

Move to filling room 211771 No. of batches 1230 batches 172.1715

Set up pastry cases 105886 No. of batches 1230 batches 86.0862

Stack cases on filling

machine 193872 No. of batches 1230 batches 157.6195

Load hopper 387744 No. of batches 1230 batches 315.2390

Fill pastry cases 1826753 No. of kilograms 246000 kilograms 7.4258

Clean hopper 211711 No. of batches 1230 batches 172.1228

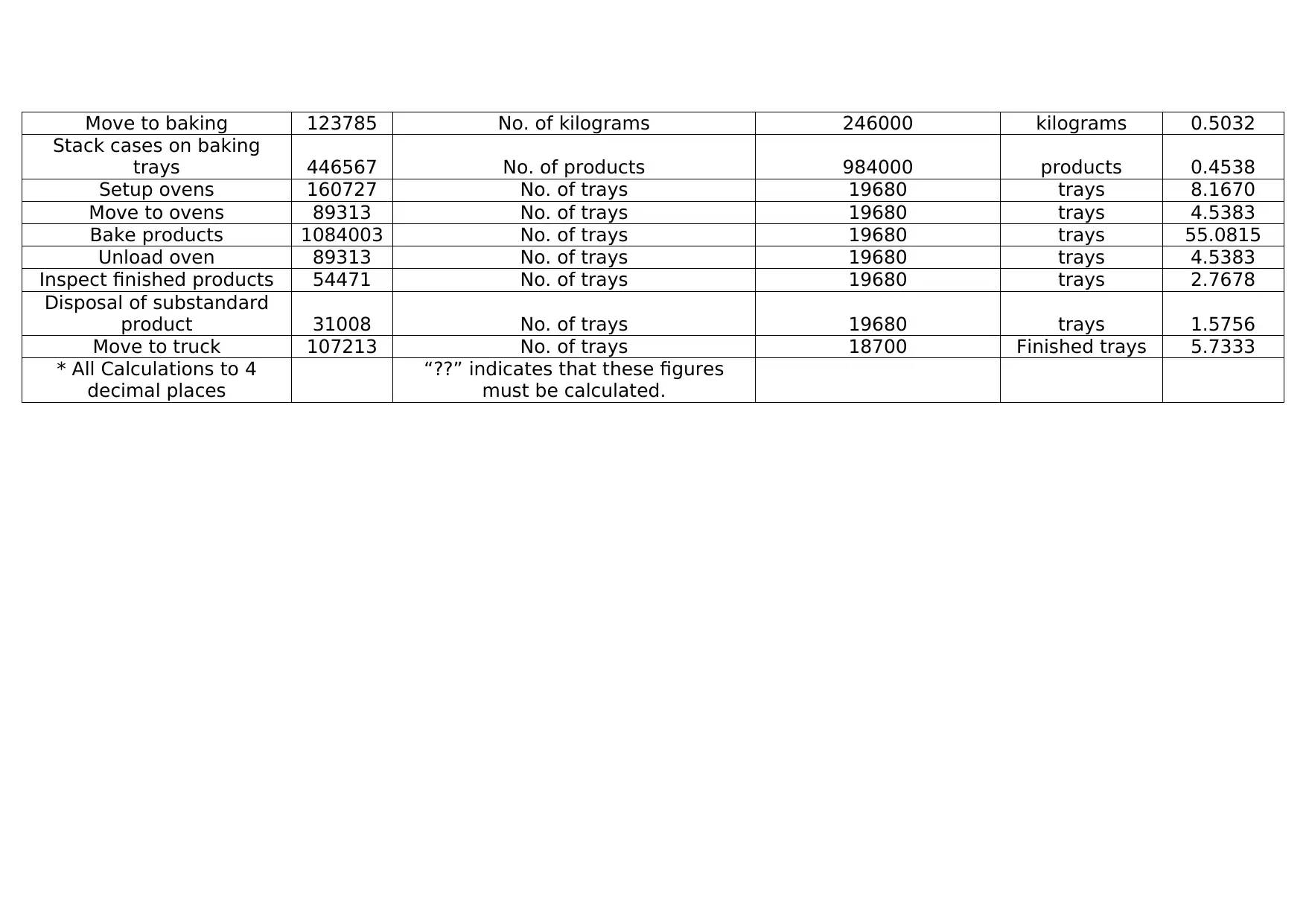

Move to baking 123785 No. of kilograms 246000 kilograms 0.5032

Stack cases on baking

trays 446567 No. of products 984000 products 0.4538

Setup ovens 160727 No. of trays 19680 trays 8.1670

Move to ovens 89313 No. of trays 19680 trays 4.5383

Bake products 1084003 No. of trays 19680 trays 55.0815

Unload oven 89313 No. of trays 19680 trays 4.5383

Inspect finished products 54471 No. of trays 19680 trays 2.7678

Disposal of substandard

product 31008 No. of trays 19680 trays 1.5756

Move to truck 107213 No. of trays 18700 Finished trays 5.7333

* All Calculations to 4

decimal places

“??” indicates that these figures

must be calculated.

Stack cases on baking

trays 446567 No. of products 984000 products 0.4538

Setup ovens 160727 No. of trays 19680 trays 8.1670

Move to ovens 89313 No. of trays 19680 trays 4.5383

Bake products 1084003 No. of trays 19680 trays 55.0815

Unload oven 89313 No. of trays 19680 trays 4.5383

Inspect finished products 54471 No. of trays 19680 trays 2.7678

Disposal of substandard

product 31008 No. of trays 19680 trays 1.5756

Move to truck 107213 No. of trays 18700 Finished trays 5.7333

* All Calculations to 4

decimal places

“??” indicates that these figures

must be calculated.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

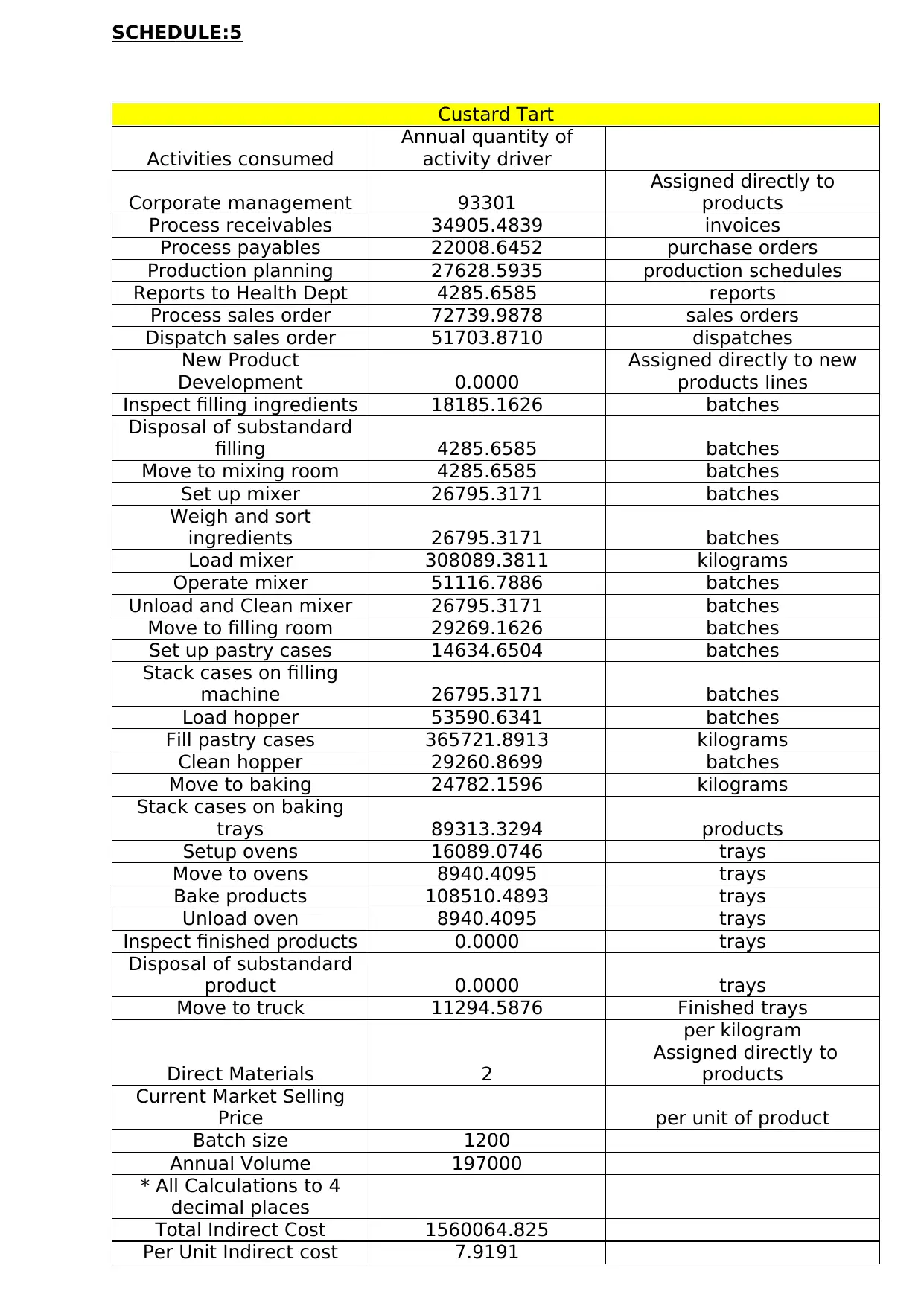

SCHEDULE:5

Custard Tart

Activities consumed

Annual quantity of

activity driver

Corporate management 93301

Assigned directly to

products

Process receivables 34905.4839 invoices

Process payables 22008.6452 purchase orders

Production planning 27628.5935 production schedules

Reports to Health Dept 4285.6585 reports

Process sales order 72739.9878 sales orders

Dispatch sales order 51703.8710 dispatches

New Product

Development 0.0000

Assigned directly to new

products lines

Inspect filling ingredients 18185.1626 batches

Disposal of substandard

filling 4285.6585 batches

Move to mixing room 4285.6585 batches

Set up mixer 26795.3171 batches

Weigh and sort

ingredients 26795.3171 batches

Load mixer 308089.3811 kilograms

Operate mixer 51116.7886 batches

Unload and Clean mixer 26795.3171 batches

Move to filling room 29269.1626 batches

Set up pastry cases 14634.6504 batches

Stack cases on filling

machine 26795.3171 batches

Load hopper 53590.6341 batches

Fill pastry cases 365721.8913 kilograms

Clean hopper 29260.8699 batches

Move to baking 24782.1596 kilograms

Stack cases on baking

trays 89313.3294 products

Setup ovens 16089.0746 trays

Move to ovens 8940.4095 trays

Bake products 108510.4893 trays

Unload oven 8940.4095 trays

Inspect finished products 0.0000 trays

Disposal of substandard

product 0.0000 trays

Move to truck 11294.5876 Finished trays

Direct Materials 2

per kilogram

Assigned directly to

products

Current Market Selling

Price per unit of product

Batch size 1200

Annual Volume 197000

* All Calculations to 4

decimal places

Total Indirect Cost 1560064.825

Per Unit Indirect cost 7.9191

Custard Tart

Activities consumed

Annual quantity of

activity driver

Corporate management 93301

Assigned directly to

products

Process receivables 34905.4839 invoices

Process payables 22008.6452 purchase orders

Production planning 27628.5935 production schedules

Reports to Health Dept 4285.6585 reports

Process sales order 72739.9878 sales orders

Dispatch sales order 51703.8710 dispatches

New Product

Development 0.0000

Assigned directly to new

products lines

Inspect filling ingredients 18185.1626 batches

Disposal of substandard

filling 4285.6585 batches

Move to mixing room 4285.6585 batches

Set up mixer 26795.3171 batches

Weigh and sort

ingredients 26795.3171 batches

Load mixer 308089.3811 kilograms

Operate mixer 51116.7886 batches

Unload and Clean mixer 26795.3171 batches

Move to filling room 29269.1626 batches

Set up pastry cases 14634.6504 batches

Stack cases on filling

machine 26795.3171 batches

Load hopper 53590.6341 batches

Fill pastry cases 365721.8913 kilograms

Clean hopper 29260.8699 batches

Move to baking 24782.1596 kilograms

Stack cases on baking

trays 89313.3294 products

Setup ovens 16089.0746 trays

Move to ovens 8940.4095 trays

Bake products 108510.4893 trays

Unload oven 8940.4095 trays

Inspect finished products 0.0000 trays

Disposal of substandard

product 0.0000 trays

Move to truck 11294.5876 Finished trays

Direct Materials 2

per kilogram

Assigned directly to

products

Current Market Selling

Price per unit of product

Batch size 1200

Annual Volume 197000

* All Calculations to 4

decimal places

Total Indirect Cost 1560064.825

Per Unit Indirect cost 7.9191

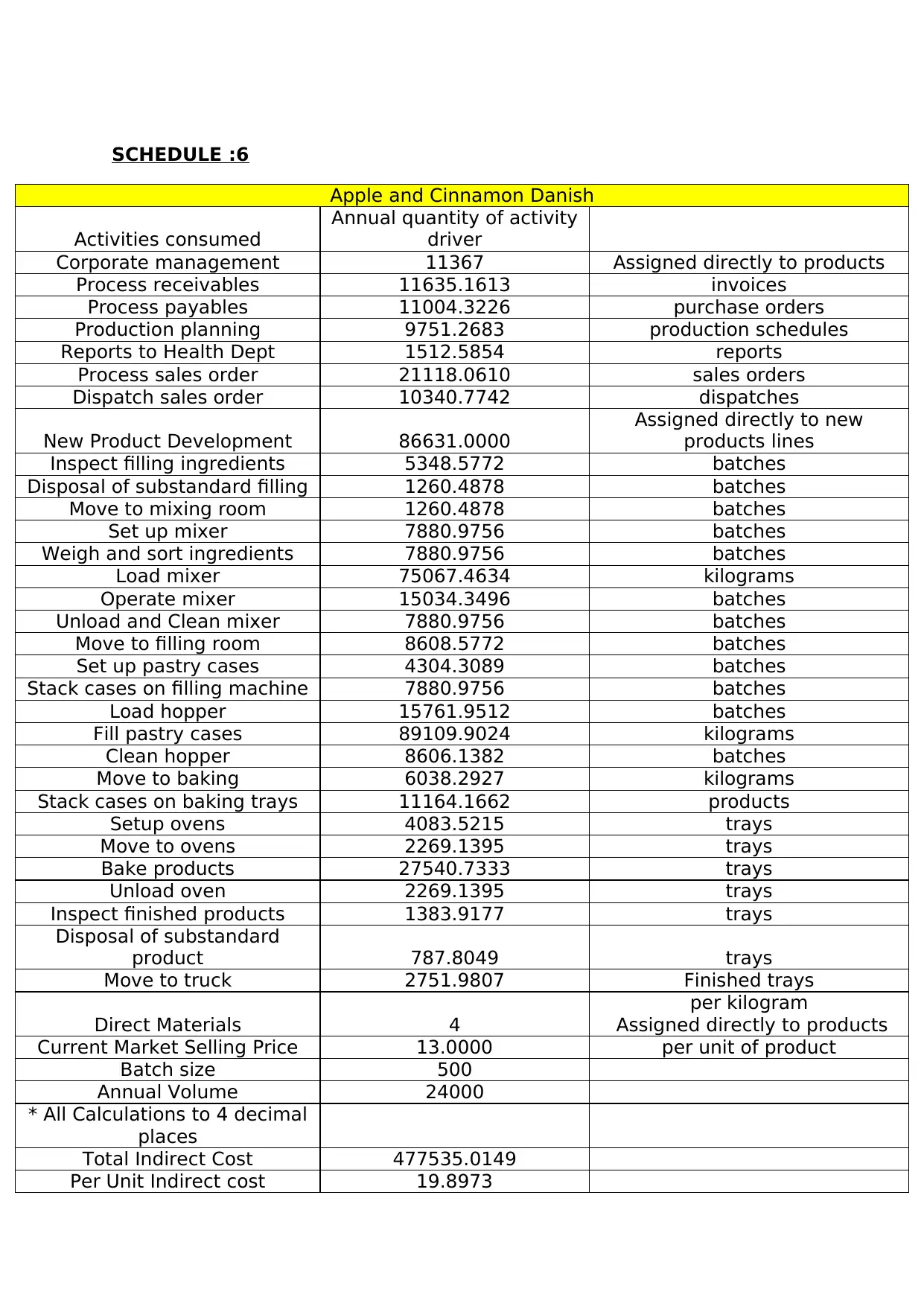

SCHEDULE :6

Apple and Cinnamon Danish

Activities consumed

Annual quantity of activity

driver

Corporate management 11367 Assigned directly to products

Process receivables 11635.1613 invoices

Process payables 11004.3226 purchase orders

Production planning 9751.2683 production schedules

Reports to Health Dept 1512.5854 reports

Process sales order 21118.0610 sales orders

Dispatch sales order 10340.7742 dispatches

New Product Development 86631.0000

Assigned directly to new

products lines

Inspect filling ingredients 5348.5772 batches

Disposal of substandard filling 1260.4878 batches

Move to mixing room 1260.4878 batches

Set up mixer 7880.9756 batches

Weigh and sort ingredients 7880.9756 batches

Load mixer 75067.4634 kilograms

Operate mixer 15034.3496 batches

Unload and Clean mixer 7880.9756 batches

Move to filling room 8608.5772 batches

Set up pastry cases 4304.3089 batches

Stack cases on filling machine 7880.9756 batches

Load hopper 15761.9512 batches

Fill pastry cases 89109.9024 kilograms

Clean hopper 8606.1382 batches

Move to baking 6038.2927 kilograms

Stack cases on baking trays 11164.1662 products

Setup ovens 4083.5215 trays

Move to ovens 2269.1395 trays

Bake products 27540.7333 trays

Unload oven 2269.1395 trays

Inspect finished products 1383.9177 trays

Disposal of substandard

product 787.8049 trays

Move to truck 2751.9807 Finished trays

Direct Materials 4

per kilogram

Assigned directly to products

Current Market Selling Price 13.0000 per unit of product

Batch size 500

Annual Volume 24000

* All Calculations to 4 decimal

places

Total Indirect Cost 477535.0149

Per Unit Indirect cost 19.8973

Apple and Cinnamon Danish

Activities consumed

Annual quantity of activity

driver

Corporate management 11367 Assigned directly to products

Process receivables 11635.1613 invoices

Process payables 11004.3226 purchase orders

Production planning 9751.2683 production schedules

Reports to Health Dept 1512.5854 reports

Process sales order 21118.0610 sales orders

Dispatch sales order 10340.7742 dispatches

New Product Development 86631.0000

Assigned directly to new

products lines

Inspect filling ingredients 5348.5772 batches

Disposal of substandard filling 1260.4878 batches

Move to mixing room 1260.4878 batches

Set up mixer 7880.9756 batches

Weigh and sort ingredients 7880.9756 batches

Load mixer 75067.4634 kilograms

Operate mixer 15034.3496 batches

Unload and Clean mixer 7880.9756 batches

Move to filling room 8608.5772 batches

Set up pastry cases 4304.3089 batches

Stack cases on filling machine 7880.9756 batches

Load hopper 15761.9512 batches

Fill pastry cases 89109.9024 kilograms

Clean hopper 8606.1382 batches

Move to baking 6038.2927 kilograms

Stack cases on baking trays 11164.1662 products

Setup ovens 4083.5215 trays

Move to ovens 2269.1395 trays

Bake products 27540.7333 trays

Unload oven 2269.1395 trays

Inspect finished products 1383.9177 trays

Disposal of substandard

product 787.8049 trays

Move to truck 2751.9807 Finished trays

Direct Materials 4

per kilogram

Assigned directly to products

Current Market Selling Price 13.0000 per unit of product

Batch size 500

Annual Volume 24000

* All Calculations to 4 decimal

places

Total Indirect Cost 477535.0149

Per Unit Indirect cost 19.8973

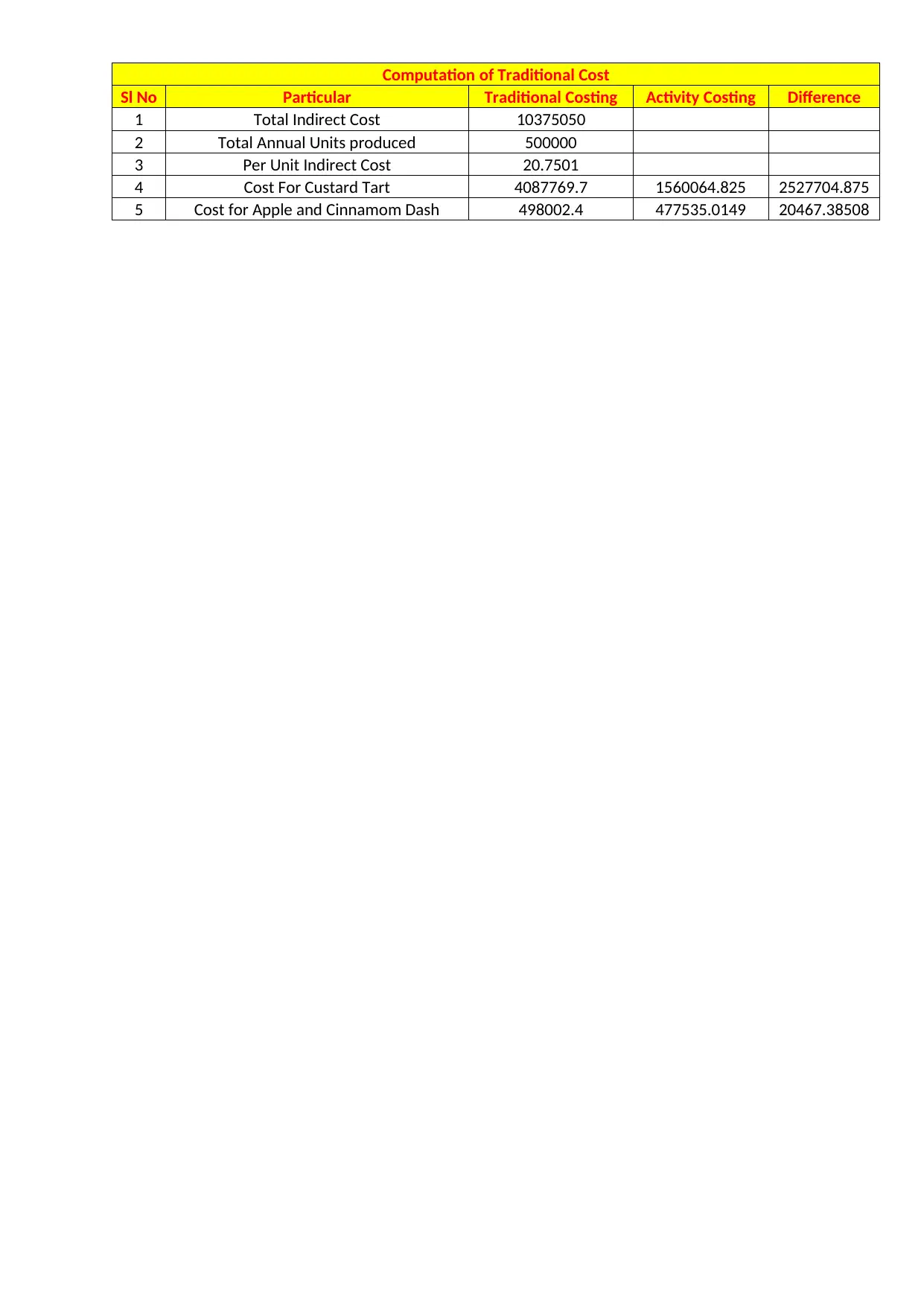

Computation of Traditional Cost

Sl No Particular Traditional Costing Activity Costing Difference

1 Total Indirect Cost 10375050

2 Total Annual Units produced 500000

3 Per Unit Indirect Cost 20.7501

4 Cost For Custard Tart 4087769.7 1560064.825 2527704.875

5 Cost for Apple and Cinnamom Dash 498002.4 477535.0149 20467.38508

Sl No Particular Traditional Costing Activity Costing Difference

1 Total Indirect Cost 10375050

2 Total Annual Units produced 500000

3 Per Unit Indirect Cost 20.7501

4 Cost For Custard Tart 4087769.7 1560064.825 2527704.875

5 Cost for Apple and Cinnamom Dash 498002.4 477535.0149 20467.38508

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Answer5

On the basis of the above analysis it is found that under both methods i.e.

absorption costing and ABC costing method there has been vast difference in the

allocation of overhead under both the methods.

Answer6

Based on the analysis cost of both the products are overstated.

Answer7

The changes that have occurred in the cost of product may be due to the

following reasons:

1) Increases in the wages of the existing worker and hire of new employee for

the increase of production which lead to increase in overall wages of the

company.

2) Increase in the cost of production i.e. the direct cost involved in the

production of units.

3) Increase in freight and other carriage cost must have increased leading to

increase in the cost of production.

4) Due to increase in the production of goods, the company consumption of

electricity must have been increased leading to increase in the electricity

cost.

5) Others Direct cost involved in the production of goods,

Answer 8 &9

Activity costing

Definition

Activity based costing is a technique of cost accounting which allocates the cost

of different overheads on the basis of benefits received from those overhead

activities. Thus, it recognizes the relationships between costs incurred, the

related overhead activities and the products or services produced. Using this

relationship, it allocates the indirect costs of production to different activities. So,

basically it involves the use of a cost driver which is derived by identifying the

factors involved behind the incurrence of an indirect cost. The determination of

the appropriate driver for a particular activity is the most significant part of this

technique in order to identify the true cost of that activity.

( MyAccountingCourse.com, 2019)

Evolution of activity costing

Activity costing basically emerged in the 1980s in the United States and

developed throughout the 1990s. In the initial stages, it was perceived to be a

mechanism to determine product and services costs more accurately, however, it

subsequently developed into a ‘management philosophy’. Robert Kaplan is

On the basis of the above analysis it is found that under both methods i.e.

absorption costing and ABC costing method there has been vast difference in the

allocation of overhead under both the methods.

Answer6

Based on the analysis cost of both the products are overstated.

Answer7

The changes that have occurred in the cost of product may be due to the

following reasons:

1) Increases in the wages of the existing worker and hire of new employee for

the increase of production which lead to increase in overall wages of the

company.

2) Increase in the cost of production i.e. the direct cost involved in the

production of units.

3) Increase in freight and other carriage cost must have increased leading to

increase in the cost of production.

4) Due to increase in the production of goods, the company consumption of

electricity must have been increased leading to increase in the electricity

cost.

5) Others Direct cost involved in the production of goods,

Answer 8 &9

Activity costing

Definition

Activity based costing is a technique of cost accounting which allocates the cost

of different overheads on the basis of benefits received from those overhead

activities. Thus, it recognizes the relationships between costs incurred, the

related overhead activities and the products or services produced. Using this

relationship, it allocates the indirect costs of production to different activities. So,

basically it involves the use of a cost driver which is derived by identifying the

factors involved behind the incurrence of an indirect cost. The determination of

the appropriate driver for a particular activity is the most significant part of this

technique in order to identify the true cost of that activity.

( MyAccountingCourse.com, 2019)

Evolution of activity costing

Activity costing basically emerged in the 1980s in the United States and

developed throughout the 1990s. In the initial stages, it was perceived to be a

mechanism to determine product and services costs more accurately, however, it

subsequently developed into a ‘management philosophy’. Robert Kaplan is

basically regarded as the father of activity-based costing. Then the period from

1980 to 1985 saw the ad-hoc implementation of activity costing. After this period,

it was recognised that this type of costing provides strategic insights and can be

used as a decision-making tool. With the emergence of database technology, it

became more practical. Research work continued in order to make the technique

more refined to identify the cost accurately. Recently, the Time-driven costing

introduced by Anderson and Kaplan provided a simplification of the costing

model. (Gosselin, 2013)

Advantages

1. Improves the understanding of the overheads and their drivers, thus, bringing the

expensive and non- value adding activities to the management’s focus.

(Association of International Certified Professional Accountants, 2019)

2. Activity based costing (ABC) provides a support base for performance

management techniques like continuous improvement and scorecards.

3. By identifying that activities are responsible for the incurrence of indirect costs

rather than the product or service itself, it helps to understand the cost behaviour

and implement effective cost control.

4. It helps in identifying the unutilised production and estimate the future resource

requirements through its pooling of activity costs and related comparison.

(Association of International Certified Professional Accountants, 2019)

Disadvantages

1. It is much more complex than absorption costing as it involves analysis of

numerous activities to identify the cost drivers. (Association of International

Certified Professional Accountants, 2019)

2. The selection of the appropriate is the most vital and the most challenging part of

this costing technique due to the involvement of multiple factors each selection.

3. It is not suitable for firms depending on the market prices for setting the prices of

their products because in their case cost plus pricing carries no significance.

4. The implementation of ABC system requires a lot of complex calculations which is

both costly as well as time consuming.

Absorption Costing

Definition

Absorption costing is a technique of cost and management accounting which

allocates each and every cost incurred on the products manufactured, whether or

not they are sold. The direct costs are recognised as a base for allocation of

indirect costs. Thus, it is also called full costing. It is a recognised method for

external reporting. It provides a mechanism for accumulating the costs incurred

in the production process and allocating them to individual products. Basically,

Direct Materials, Direct labour are used for deriving the rates for apportionment.

1980 to 1985 saw the ad-hoc implementation of activity costing. After this period,

it was recognised that this type of costing provides strategic insights and can be

used as a decision-making tool. With the emergence of database technology, it

became more practical. Research work continued in order to make the technique

more refined to identify the cost accurately. Recently, the Time-driven costing

introduced by Anderson and Kaplan provided a simplification of the costing

model. (Gosselin, 2013)

Advantages

1. Improves the understanding of the overheads and their drivers, thus, bringing the

expensive and non- value adding activities to the management’s focus.

(Association of International Certified Professional Accountants, 2019)

2. Activity based costing (ABC) provides a support base for performance

management techniques like continuous improvement and scorecards.

3. By identifying that activities are responsible for the incurrence of indirect costs

rather than the product or service itself, it helps to understand the cost behaviour

and implement effective cost control.

4. It helps in identifying the unutilised production and estimate the future resource

requirements through its pooling of activity costs and related comparison.

(Association of International Certified Professional Accountants, 2019)

Disadvantages

1. It is much more complex than absorption costing as it involves analysis of

numerous activities to identify the cost drivers. (Association of International

Certified Professional Accountants, 2019)

2. The selection of the appropriate is the most vital and the most challenging part of

this costing technique due to the involvement of multiple factors each selection.

3. It is not suitable for firms depending on the market prices for setting the prices of

their products because in their case cost plus pricing carries no significance.

4. The implementation of ABC system requires a lot of complex calculations which is

both costly as well as time consuming.

Absorption Costing

Definition

Absorption costing is a technique of cost and management accounting which

allocates each and every cost incurred on the products manufactured, whether or

not they are sold. The direct costs are recognised as a base for allocation of

indirect costs. Thus, it is also called full costing. It is a recognised method for

external reporting. It provides a mechanism for accumulating the costs incurred

in the production process and allocating them to individual products. Basically,

Direct Materials, Direct labour are used for deriving the rates for apportionment.

Evolution

Absorption costing (also known as traditional costing) owes its origins to the era

when companies dealt in a relatively narrower range of products. The indirect

costs were allocated on the basis of direct labour costs as it was the single

largest contributor to the total costs. Babbage (1835) calculated the first

absorption cost by the aggregating the cost of every process. Managers used to

shun other costing techniques due to the costs involved, especially data

processing costs. But, with the passage of time the businesses became more

diversified and the number of products and services increased, thus, rendering

the decline of absorption costing inevitable. The introduction of activity costing

led to a paradigm shift from the absorption costing model where the principles of

matching costs with the proportionate benefits was adhered to. (essays.pw,

2015)

Advantages

1. It is an accepted costing method as per the Generally Accepted Accounting

Principles (GAAP)

2. It shows less fluctuation in net profits on the back of constant production.

(Accounting For Management, 2019)

3. It eliminates the probabilities of undervaluation of stock and thus often used for

preparation of financial accounts.

4. It is less costly and time consuming than activity-based costing.

Disadvantages

1. It does not provide for any distinction between variable and fixed costs, so, at

times it is not useful for decision making and planning. (Accounting For

Management, 2019)

2. The cost- volume relationship is ignored due to too much emphasis on the total

cost of production.

3. In case of irregular production schedule, it may give an impression that fixed

overheads also fluctuate with sales. (Singh, 2018)

4. It leads to manipulation of accounts by concealing the costs incurred in inventory

until the units are sold. (Singh, 2018)

Absorption costing (also known as traditional costing) owes its origins to the era

when companies dealt in a relatively narrower range of products. The indirect

costs were allocated on the basis of direct labour costs as it was the single

largest contributor to the total costs. Babbage (1835) calculated the first

absorption cost by the aggregating the cost of every process. Managers used to

shun other costing techniques due to the costs involved, especially data

processing costs. But, with the passage of time the businesses became more

diversified and the number of products and services increased, thus, rendering

the decline of absorption costing inevitable. The introduction of activity costing

led to a paradigm shift from the absorption costing model where the principles of

matching costs with the proportionate benefits was adhered to. (essays.pw,

2015)

Advantages

1. It is an accepted costing method as per the Generally Accepted Accounting

Principles (GAAP)

2. It shows less fluctuation in net profits on the back of constant production.

(Accounting For Management, 2019)

3. It eliminates the probabilities of undervaluation of stock and thus often used for

preparation of financial accounts.

4. It is less costly and time consuming than activity-based costing.

Disadvantages

1. It does not provide for any distinction between variable and fixed costs, so, at

times it is not useful for decision making and planning. (Accounting For

Management, 2019)

2. The cost- volume relationship is ignored due to too much emphasis on the total

cost of production.

3. In case of irregular production schedule, it may give an impression that fixed

overheads also fluctuate with sales. (Singh, 2018)

4. It leads to manipulation of accounts by concealing the costs incurred in inventory

until the units are sold. (Singh, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

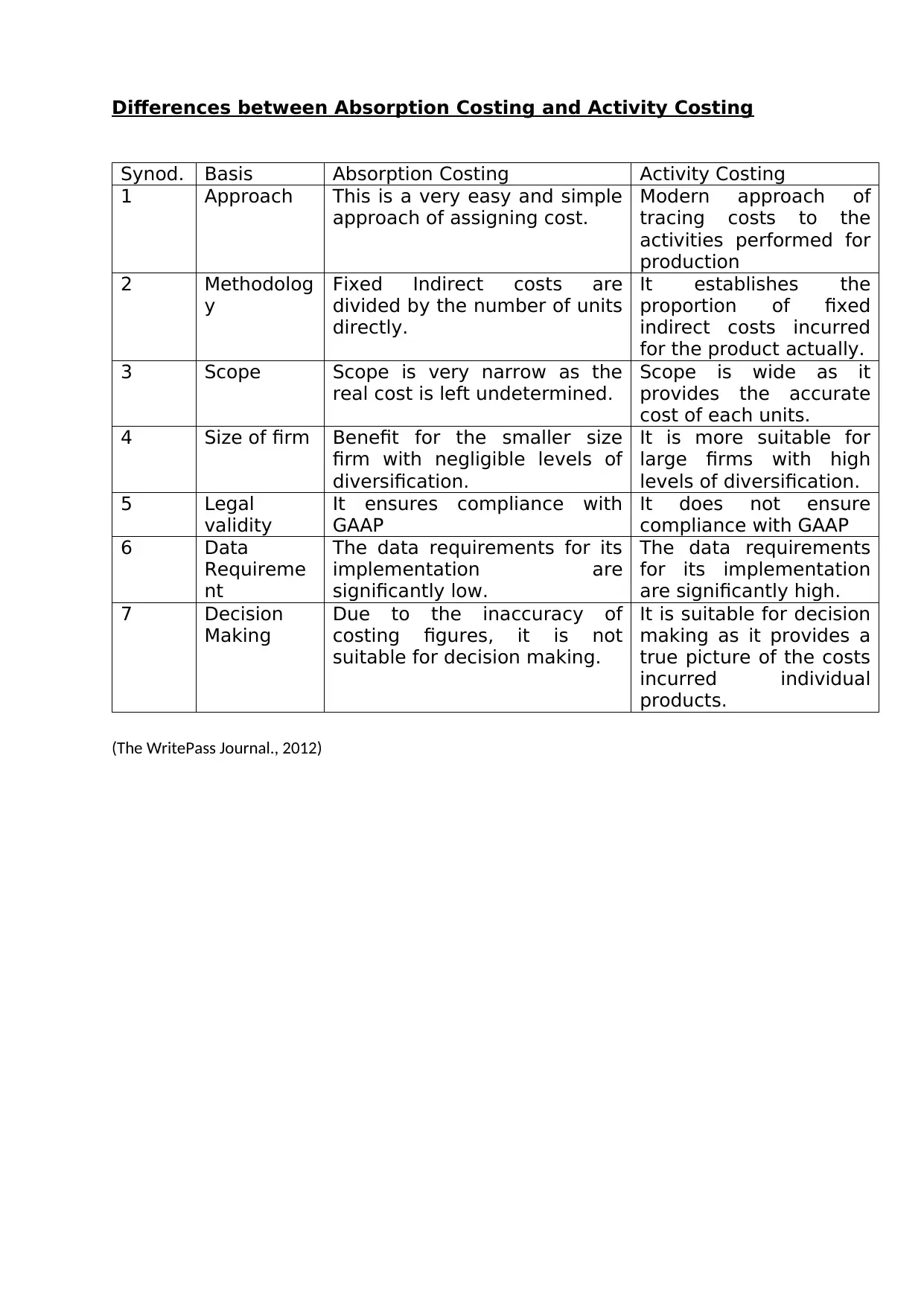

Differences between Absorption Costing and Activity Costing

Synod. Basis Absorption Costing Activity Costing

1 Approach This is a very easy and simple

approach of assigning cost.

Modern approach of

tracing costs to the

activities performed for

production

2 Methodolog

y

Fixed Indirect costs are

divided by the number of units

directly.

It establishes the

proportion of fixed

indirect costs incurred

for the product actually.

3 Scope Scope is very narrow as the

real cost is left undetermined.

Scope is wide as it

provides the accurate

cost of each units.

4 Size of firm Benefit for the smaller size

firm with negligible levels of

diversification.

It is more suitable for

large firms with high

levels of diversification.

5 Legal

validity

It ensures compliance with

GAAP

It does not ensure

compliance with GAAP

6 Data

Requireme

nt

The data requirements for its

implementation are

significantly low.

The data requirements

for its implementation

are significantly high.

7 Decision

Making

Due to the inaccuracy of

costing figures, it is not

suitable for decision making.

It is suitable for decision

making as it provides a

true picture of the costs

incurred individual

products.

(The WritePass Journal., 2012)

Synod. Basis Absorption Costing Activity Costing

1 Approach This is a very easy and simple

approach of assigning cost.

Modern approach of

tracing costs to the

activities performed for

production

2 Methodolog

y

Fixed Indirect costs are

divided by the number of units

directly.

It establishes the

proportion of fixed

indirect costs incurred

for the product actually.

3 Scope Scope is very narrow as the

real cost is left undetermined.

Scope is wide as it

provides the accurate

cost of each units.

4 Size of firm Benefit for the smaller size

firm with negligible levels of

diversification.

It is more suitable for

large firms with high

levels of diversification.

5 Legal

validity

It ensures compliance with

GAAP

It does not ensure

compliance with GAAP

6 Data

Requireme

nt

The data requirements for its

implementation are

significantly low.

The data requirements

for its implementation

are significantly high.

7 Decision

Making

Due to the inaccuracy of

costing figures, it is not

suitable for decision making.

It is suitable for decision

making as it provides a

true picture of the costs

incurred individual

products.

(The WritePass Journal., 2012)

References

MyAccountingCourse.com, 2019. What is Activity Based Costing (ABC)?. [Online]

Available at: https://www.myaccountingcourse.com/accounting-dictionary/activity-based-costing

[Accessed 19 May 2019].

Accounting For Management, 2019. Advantages and disadvantages of absorption costing. [Online]

Available at: https://www.accountingformanagement.org/advantages-and-disadvantages-of-absorption-

costing/

[Accessed 19 May 2019].

Association of International Certified Professional Accountants, 2019. Activity Based Costing. [Online]

Available at: https://www.cgma.org/resources/tools/essential-tools/activity-based-costing.html

[Accessed 19 May 2019].

essays.pw, 2015. THE HISTORY OF ABSORPTION COSTING ACCOUNTING ESSAY. [Online]

Available at: https://essays.pw/essay/the-history-of-absorption-costing-accounting-essay-8684

[Accessed 19 May 2019].

Gosselin, M., 2013. A Review of Activity-Based Costing: Technique,. [Online]

Available at: https://edisciplinas.usp.br/pluginfile.php/4097711/mod_resource/content/1/Gosselim

%282007%29_A%20Review%20of%20Activity-Based%20Costing.pdf

[Accessed 19 May 2019].

Singh, S., 2018. http://www.accountingnotes.net/cost-accounting/absorption-costing/absorption-costing-

meaning-advantages-and. [Online]

Available at: http://www.accountingnotes.net/cost-accounting/absorption-costing/absorption-costing-

meaning-advantages-and

[Accessed 19 May 2019].

The WritePass Journal., 2012. What are the differences between Absorption costing and ABC. [Online]

Available at: https://writepass.com/journal/2012/12/why-does-the-company-need-either-absorption-costing-

or-abc/

[Accessed 19 May 2019].

MyAccountingCourse.com, 2019. What is Activity Based Costing (ABC)?. [Online]

Available at: https://www.myaccountingcourse.com/accounting-dictionary/activity-based-costing

[Accessed 19 May 2019].

Accounting For Management, 2019. Advantages and disadvantages of absorption costing. [Online]

Available at: https://www.accountingformanagement.org/advantages-and-disadvantages-of-absorption-

costing/

[Accessed 19 May 2019].

Association of International Certified Professional Accountants, 2019. Activity Based Costing. [Online]

Available at: https://www.cgma.org/resources/tools/essential-tools/activity-based-costing.html

[Accessed 19 May 2019].

essays.pw, 2015. THE HISTORY OF ABSORPTION COSTING ACCOUNTING ESSAY. [Online]

Available at: https://essays.pw/essay/the-history-of-absorption-costing-accounting-essay-8684

[Accessed 19 May 2019].

Gosselin, M., 2013. A Review of Activity-Based Costing: Technique,. [Online]

Available at: https://edisciplinas.usp.br/pluginfile.php/4097711/mod_resource/content/1/Gosselim

%282007%29_A%20Review%20of%20Activity-Based%20Costing.pdf

[Accessed 19 May 2019].

Singh, S., 2018. http://www.accountingnotes.net/cost-accounting/absorption-costing/absorption-costing-

meaning-advantages-and. [Online]

Available at: http://www.accountingnotes.net/cost-accounting/absorption-costing/absorption-costing-

meaning-advantages-and

[Accessed 19 May 2019].

The WritePass Journal., 2012. What are the differences between Absorption costing and ABC. [Online]

Available at: https://writepass.com/journal/2012/12/why-does-the-company-need-either-absorption-costing-

or-abc/

[Accessed 19 May 2019].

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.