Advanced Financial Accounting

VerifiedAdded on 2023/01/17

|8

|1542

|92

AI Summary

This document provides answers to questions on various topics in advanced financial accounting, including IFRS 16, Disclosure Initiative of IFRS, Changes in Financing Liabilities, IASB Updates, Importance of Special Purpose Financial Statements, New Accounting Standards, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Name of the Student

Name of the University

Author’s Note

Advanced Financial Accounting

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Answer to Question 1.................................................................................................................2

Answer to Question 2.................................................................................................................4

References..................................................................................................................................7

Table of Contents

Answer to Question 1.................................................................................................................2

Answer to Question 2.................................................................................................................4

References..................................................................................................................................7

2ADVANCED FINANCIAL ACCOUNTING

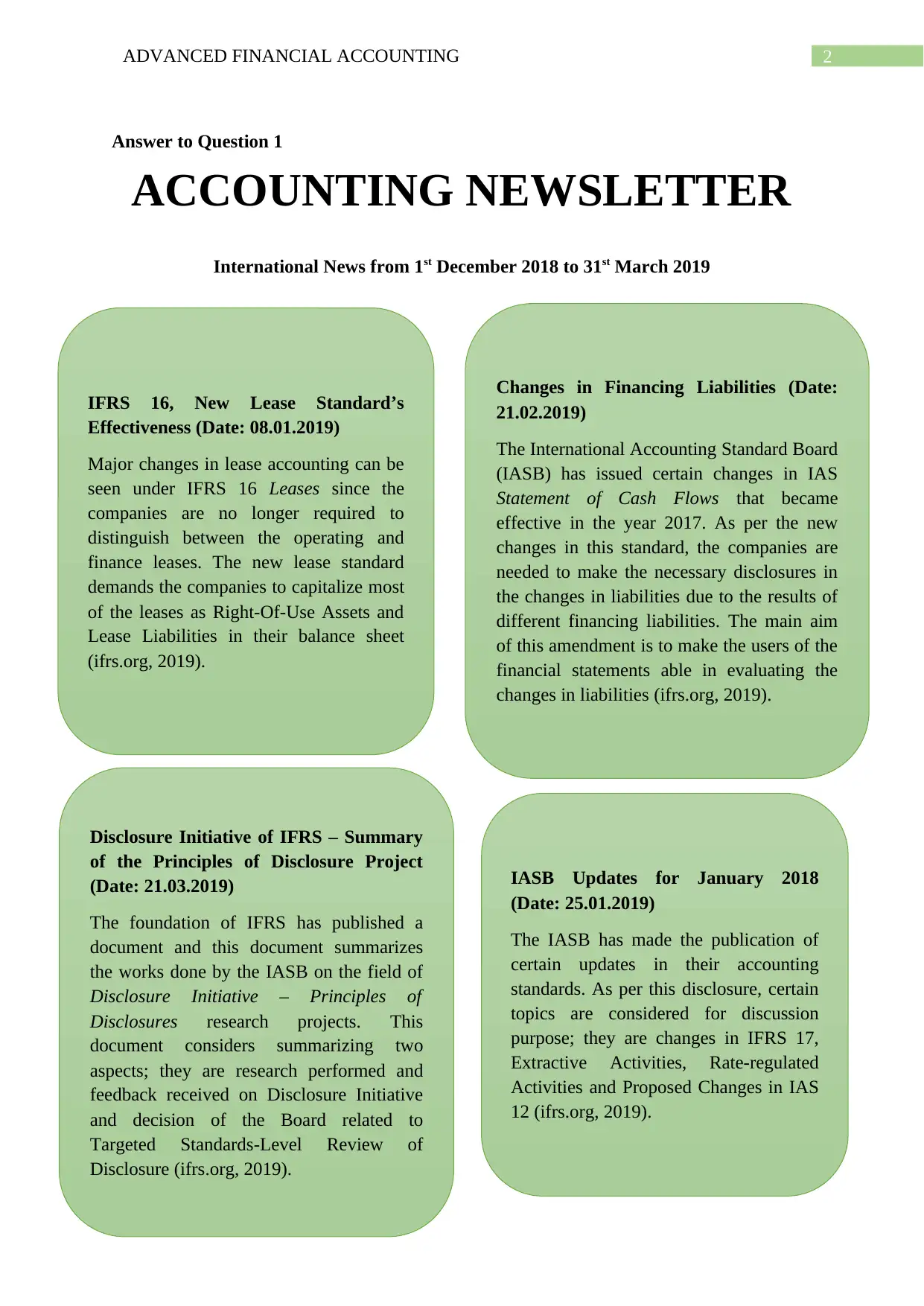

Answer to Question 1

ACCOUNTING NEWSLETTER

International News from 1st December 2018 to 31st March 2019

IFRS 16, New Lease Standard’s

Effectiveness (Date: 08.01.2019)

Major changes in lease accounting can be

seen under IFRS 16 Leases since the

companies are no longer required to

distinguish between the operating and

finance leases. The new lease standard

demands the companies to capitalize most

of the leases as Right-Of-Use Assets and

Lease Liabilities in their balance sheet

(ifrs.org, 2019).

Changes in Financing Liabilities (Date:

21.02.2019)

The International Accounting Standard Board

(IASB) has issued certain changes in IAS

Statement of Cash Flows that became

effective in the year 2017. As per the new

changes in this standard, the companies are

needed to make the necessary disclosures in

the changes in liabilities due to the results of

different financing liabilities. The main aim

of this amendment is to make the users of the

financial statements able in evaluating the

changes in liabilities (ifrs.org, 2019).

Disclosure Initiative of IFRS – Summary

of the Principles of Disclosure Project

(Date: 21.03.2019)

The foundation of IFRS has published a

document and this document summarizes

the works done by the IASB on the field of

Disclosure Initiative – Principles of

Disclosures research projects. This

document considers summarizing two

aspects; they are research performed and

feedback received on Disclosure Initiative

and decision of the Board related to

Targeted Standards-Level Review of

Disclosure (ifrs.org, 2019).

IASB Updates for January 2018

(Date: 25.01.2019)

The IASB has made the publication of

certain updates in their accounting

standards. As per this disclosure, certain

topics are considered for discussion

purpose; they are changes in IFRS 17,

Extractive Activities, Rate-regulated

Activities and Proposed Changes in IAS

12 (ifrs.org, 2019).

Answer to Question 1

ACCOUNTING NEWSLETTER

International News from 1st December 2018 to 31st March 2019

IFRS 16, New Lease Standard’s

Effectiveness (Date: 08.01.2019)

Major changes in lease accounting can be

seen under IFRS 16 Leases since the

companies are no longer required to

distinguish between the operating and

finance leases. The new lease standard

demands the companies to capitalize most

of the leases as Right-Of-Use Assets and

Lease Liabilities in their balance sheet

(ifrs.org, 2019).

Changes in Financing Liabilities (Date:

21.02.2019)

The International Accounting Standard Board

(IASB) has issued certain changes in IAS

Statement of Cash Flows that became

effective in the year 2017. As per the new

changes in this standard, the companies are

needed to make the necessary disclosures in

the changes in liabilities due to the results of

different financing liabilities. The main aim

of this amendment is to make the users of the

financial statements able in evaluating the

changes in liabilities (ifrs.org, 2019).

Disclosure Initiative of IFRS – Summary

of the Principles of Disclosure Project

(Date: 21.03.2019)

The foundation of IFRS has published a

document and this document summarizes

the works done by the IASB on the field of

Disclosure Initiative – Principles of

Disclosures research projects. This

document considers summarizing two

aspects; they are research performed and

feedback received on Disclosure Initiative

and decision of the Board related to

Targeted Standards-Level Review of

Disclosure (ifrs.org, 2019).

IASB Updates for January 2018

(Date: 25.01.2019)

The IASB has made the publication of

certain updates in their accounting

standards. As per this disclosure, certain

topics are considered for discussion

purpose; they are changes in IFRS 17,

Extractive Activities, Rate-regulated

Activities and Proposed Changes in IAS

12 (ifrs.org, 2019).

3ADVANCED FINANCIAL ACCOUNTING

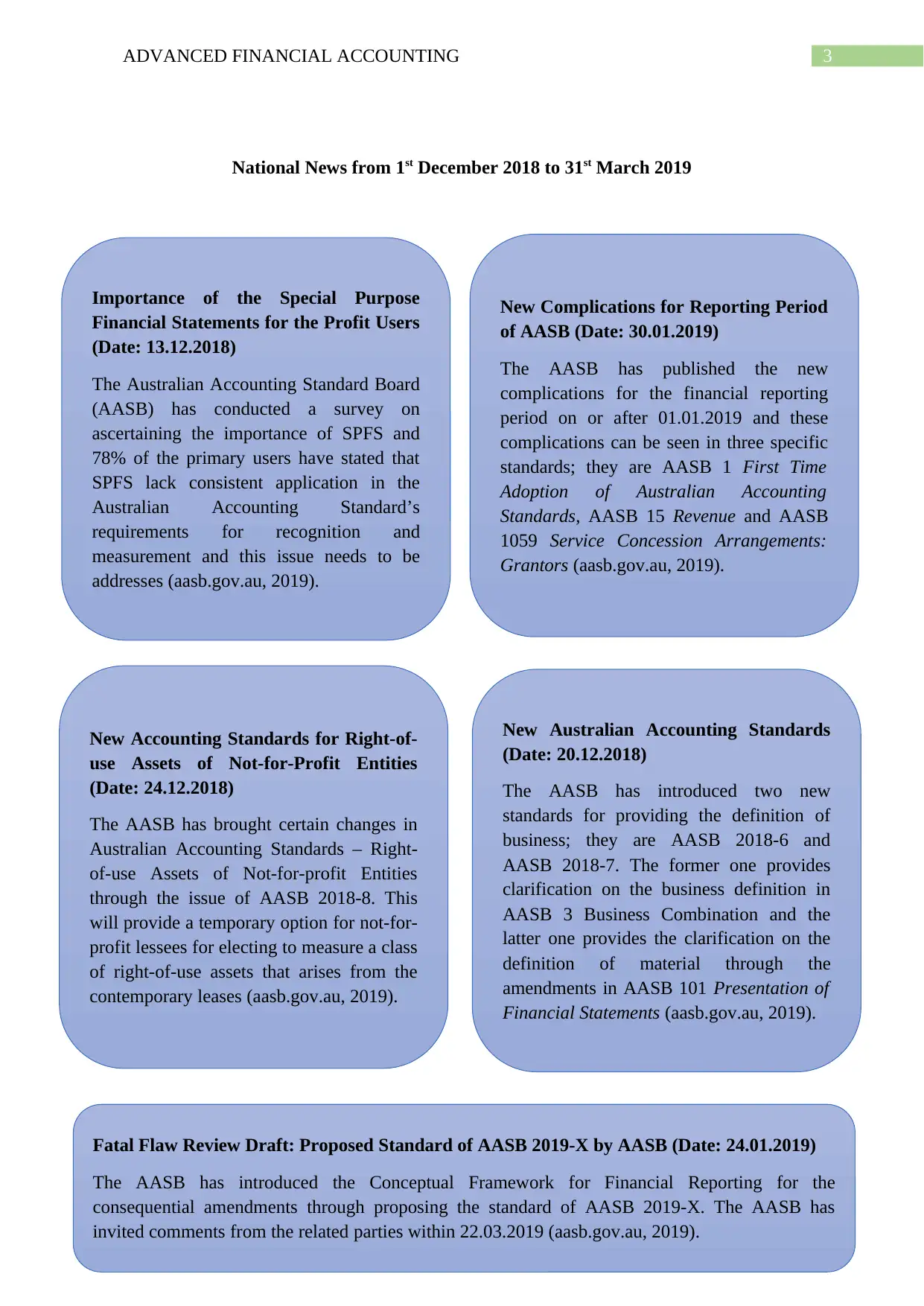

National News from 1st December 2018 to 31st March 2019

Importance of the Special Purpose

Financial Statements for the Profit Users

(Date: 13.12.2018)

The Australian Accounting Standard Board

(AASB) has conducted a survey on

ascertaining the importance of SPFS and

78% of the primary users have stated that

SPFS lack consistent application in the

Australian Accounting Standard’s

requirements for recognition and

measurement and this issue needs to be

addresses (aasb.gov.au, 2019).

New Complications for Reporting Period

of AASB (Date: 30.01.2019)

The AASB has published the new

complications for the financial reporting

period on or after 01.01.2019 and these

complications can be seen in three specific

standards; they are AASB 1 First Time

Adoption of Australian Accounting

Standards, AASB 15 Revenue and AASB

1059 Service Concession Arrangements:

Grantors (aasb.gov.au, 2019).

New Accounting Standards for Right-of-

use Assets of Not-for-Profit Entities

(Date: 24.12.2018)

The AASB has brought certain changes in

Australian Accounting Standards – Right-

of-use Assets of Not-for-profit Entities

through the issue of AASB 2018-8. This

will provide a temporary option for not-for-

profit lessees for electing to measure a class

of right-of-use assets that arises from the

contemporary leases (aasb.gov.au, 2019).

New Australian Accounting Standards

(Date: 20.12.2018)

The AASB has introduced two new

standards for providing the definition of

business; they are AASB 2018-6 and

AASB 2018-7. The former one provides

clarification on the business definition in

AASB 3 Business Combination and the

latter one provides the clarification on the

definition of material through the

amendments in AASB 101 Presentation of

Financial Statements (aasb.gov.au, 2019).

Fatal Flaw Review Draft: Proposed Standard of AASB 2019-X by AASB (Date: 24.01.2019)

The AASB has introduced the Conceptual Framework for Financial Reporting for the

consequential amendments through proposing the standard of AASB 2019-X. The AASB has

invited comments from the related parties within 22.03.2019 (aasb.gov.au, 2019).

National News from 1st December 2018 to 31st March 2019

Importance of the Special Purpose

Financial Statements for the Profit Users

(Date: 13.12.2018)

The Australian Accounting Standard Board

(AASB) has conducted a survey on

ascertaining the importance of SPFS and

78% of the primary users have stated that

SPFS lack consistent application in the

Australian Accounting Standard’s

requirements for recognition and

measurement and this issue needs to be

addresses (aasb.gov.au, 2019).

New Complications for Reporting Period

of AASB (Date: 30.01.2019)

The AASB has published the new

complications for the financial reporting

period on or after 01.01.2019 and these

complications can be seen in three specific

standards; they are AASB 1 First Time

Adoption of Australian Accounting

Standards, AASB 15 Revenue and AASB

1059 Service Concession Arrangements:

Grantors (aasb.gov.au, 2019).

New Accounting Standards for Right-of-

use Assets of Not-for-Profit Entities

(Date: 24.12.2018)

The AASB has brought certain changes in

Australian Accounting Standards – Right-

of-use Assets of Not-for-profit Entities

through the issue of AASB 2018-8. This

will provide a temporary option for not-for-

profit lessees for electing to measure a class

of right-of-use assets that arises from the

contemporary leases (aasb.gov.au, 2019).

New Australian Accounting Standards

(Date: 20.12.2018)

The AASB has introduced two new

standards for providing the definition of

business; they are AASB 2018-6 and

AASB 2018-7. The former one provides

clarification on the business definition in

AASB 3 Business Combination and the

latter one provides the clarification on the

definition of material through the

amendments in AASB 101 Presentation of

Financial Statements (aasb.gov.au, 2019).

Fatal Flaw Review Draft: Proposed Standard of AASB 2019-X by AASB (Date: 24.01.2019)

The AASB has introduced the Conceptual Framework for Financial Reporting for the

consequential amendments through proposing the standard of AASB 2019-X. The AASB has

invited comments from the related parties within 22.03.2019 (aasb.gov.au, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ADVANCED FINANCIAL ACCOUNTING

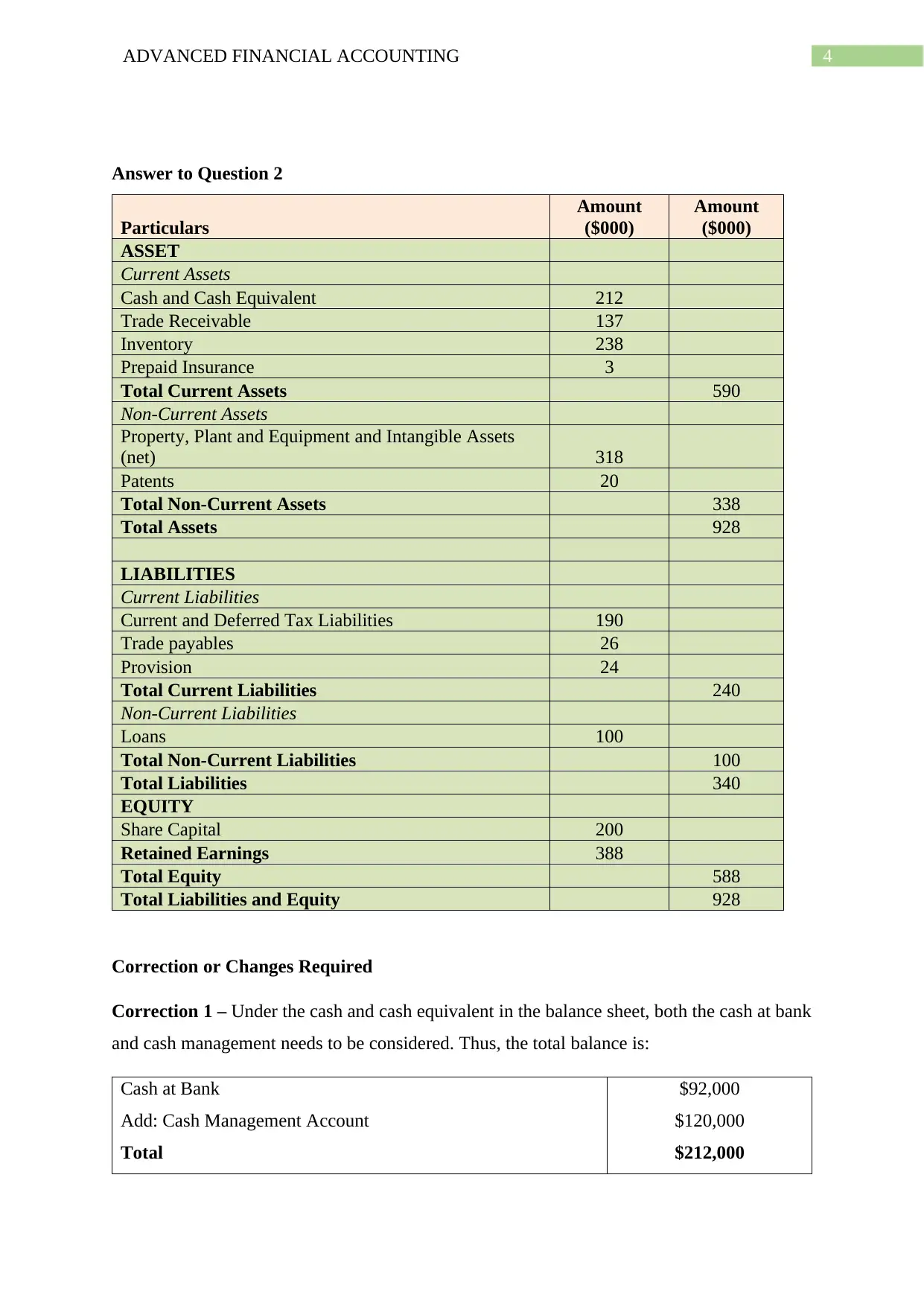

Answer to Question 2

Particulars

Amount

($000)

Amount

($000)

ASSET

Current Assets

Cash and Cash Equivalent 212

Trade Receivable 137

Inventory 238

Prepaid Insurance 3

Total Current Assets 590

Non-Current Assets

Property, Plant and Equipment and Intangible Assets

(net) 318

Patents 20

Total Non-Current Assets 338

Total Assets 928

LIABILITIES

Current Liabilities

Current and Deferred Tax Liabilities 190

Trade payables 26

Provision 24

Total Current Liabilities 240

Non-Current Liabilities

Loans 100

Total Non-Current Liabilities 100

Total Liabilities 340

EQUITY

Share Capital 200

Retained Earnings 388

Total Equity 588

Total Liabilities and Equity 928

Correction or Changes Required

Correction 1 – Under the cash and cash equivalent in the balance sheet, both the cash at bank

and cash management needs to be considered. Thus, the total balance is:

Cash at Bank

Add: Cash Management Account

Total

$92,000

$120,000

$212,000

Answer to Question 2

Particulars

Amount

($000)

Amount

($000)

ASSET

Current Assets

Cash and Cash Equivalent 212

Trade Receivable 137

Inventory 238

Prepaid Insurance 3

Total Current Assets 590

Non-Current Assets

Property, Plant and Equipment and Intangible Assets

(net) 318

Patents 20

Total Non-Current Assets 338

Total Assets 928

LIABILITIES

Current Liabilities

Current and Deferred Tax Liabilities 190

Trade payables 26

Provision 24

Total Current Liabilities 240

Non-Current Liabilities

Loans 100

Total Non-Current Liabilities 100

Total Liabilities 340

EQUITY

Share Capital 200

Retained Earnings 388

Total Equity 588

Total Liabilities and Equity 928

Correction or Changes Required

Correction 1 – Under the cash and cash equivalent in the balance sheet, both the cash at bank

and cash management needs to be considered. Thus, the total balance is:

Cash at Bank

Add: Cash Management Account

Total

$92,000

$120,000

$212,000

5ADVANCED FINANCIAL ACCOUNTING

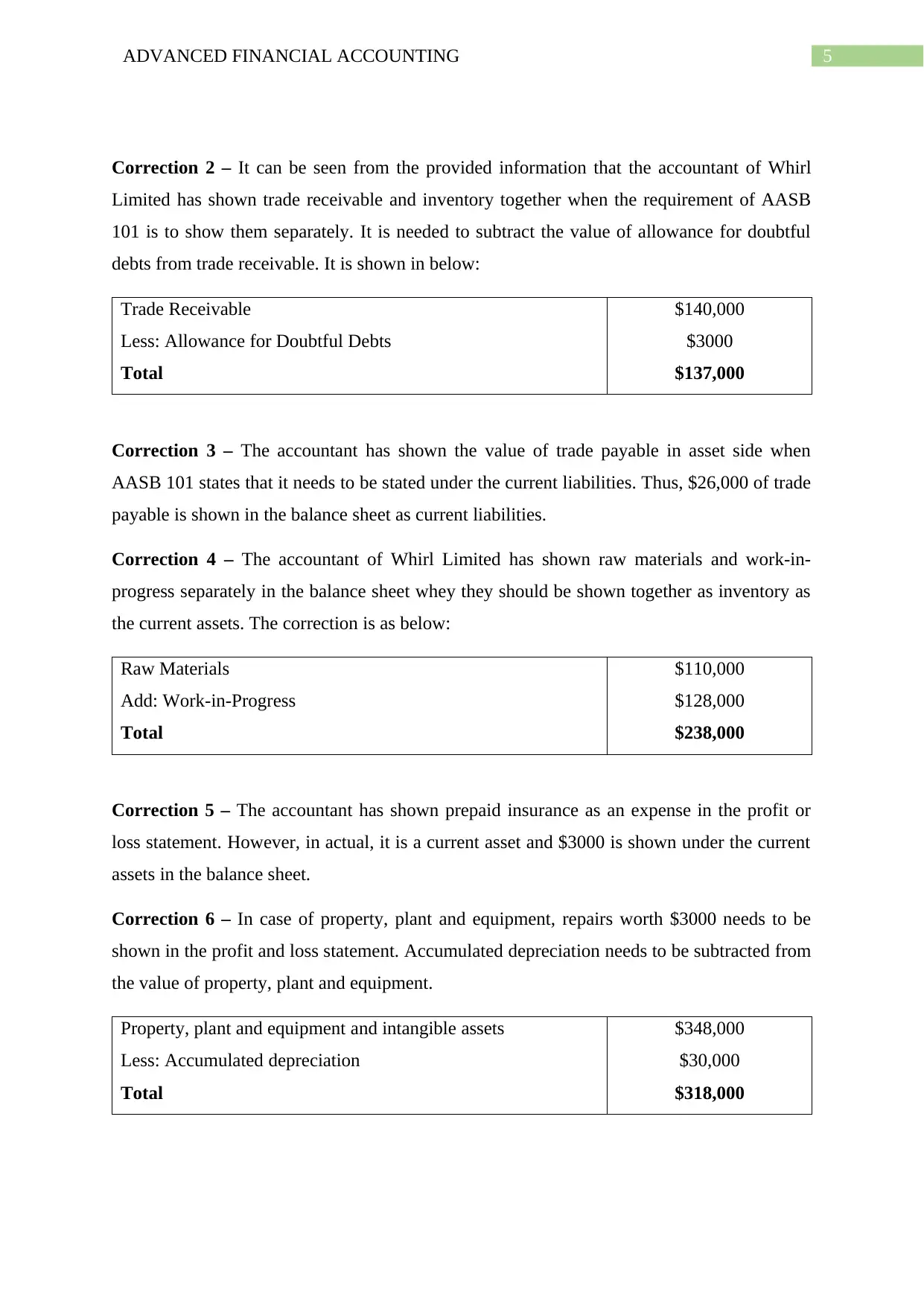

Correction 2 – It can be seen from the provided information that the accountant of Whirl

Limited has shown trade receivable and inventory together when the requirement of AASB

101 is to show them separately. It is needed to subtract the value of allowance for doubtful

debts from trade receivable. It is shown in below:

Trade Receivable

Less: Allowance for Doubtful Debts

Total

$140,000

$3000

$137,000

Correction 3 – The accountant has shown the value of trade payable in asset side when

AASB 101 states that it needs to be stated under the current liabilities. Thus, $26,000 of trade

payable is shown in the balance sheet as current liabilities.

Correction 4 – The accountant of Whirl Limited has shown raw materials and work-in-

progress separately in the balance sheet whey they should be shown together as inventory as

the current assets. The correction is as below:

Raw Materials

Add: Work-in-Progress

Total

$110,000

$128,000

$238,000

Correction 5 – The accountant has shown prepaid insurance as an expense in the profit or

loss statement. However, in actual, it is a current asset and $3000 is shown under the current

assets in the balance sheet.

Correction 6 – In case of property, plant and equipment, repairs worth $3000 needs to be

shown in the profit and loss statement. Accumulated depreciation needs to be subtracted from

the value of property, plant and equipment.

Property, plant and equipment and intangible assets

Less: Accumulated depreciation

Total

$348,000

$30,000

$318,000

Correction 2 – It can be seen from the provided information that the accountant of Whirl

Limited has shown trade receivable and inventory together when the requirement of AASB

101 is to show them separately. It is needed to subtract the value of allowance for doubtful

debts from trade receivable. It is shown in below:

Trade Receivable

Less: Allowance for Doubtful Debts

Total

$140,000

$3000

$137,000

Correction 3 – The accountant has shown the value of trade payable in asset side when

AASB 101 states that it needs to be stated under the current liabilities. Thus, $26,000 of trade

payable is shown in the balance sheet as current liabilities.

Correction 4 – The accountant of Whirl Limited has shown raw materials and work-in-

progress separately in the balance sheet whey they should be shown together as inventory as

the current assets. The correction is as below:

Raw Materials

Add: Work-in-Progress

Total

$110,000

$128,000

$238,000

Correction 5 – The accountant has shown prepaid insurance as an expense in the profit or

loss statement. However, in actual, it is a current asset and $3000 is shown under the current

assets in the balance sheet.

Correction 6 – In case of property, plant and equipment, repairs worth $3000 needs to be

shown in the profit and loss statement. Accumulated depreciation needs to be subtracted from

the value of property, plant and equipment.

Property, plant and equipment and intangible assets

Less: Accumulated depreciation

Total

$348,000

$30,000

$318,000

6ADVANCED FINANCIAL ACCOUNTING

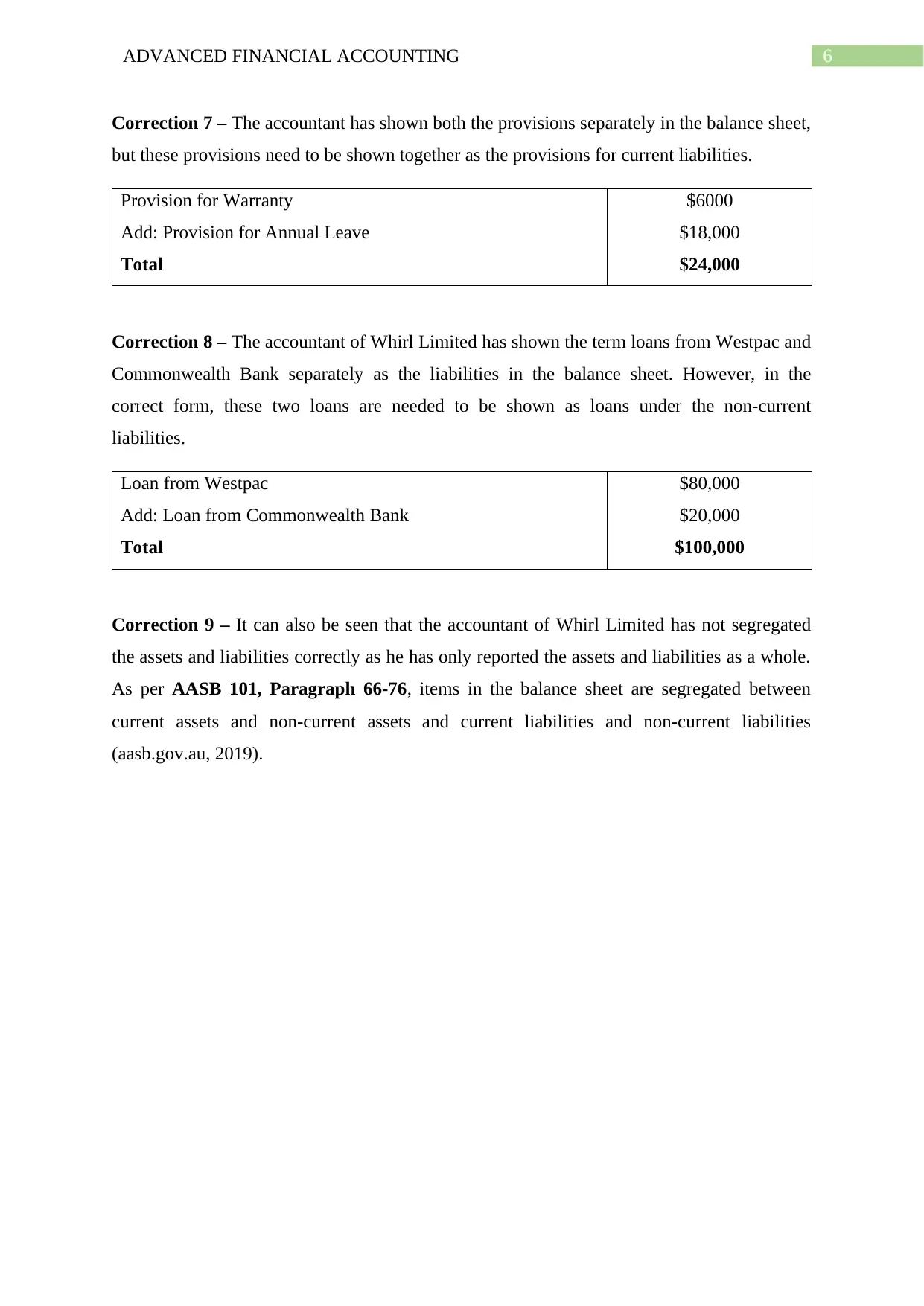

Correction 7 – The accountant has shown both the provisions separately in the balance sheet,

but these provisions need to be shown together as the provisions for current liabilities.

Provision for Warranty

Add: Provision for Annual Leave

Total

$6000

$18,000

$24,000

Correction 8 – The accountant of Whirl Limited has shown the term loans from Westpac and

Commonwealth Bank separately as the liabilities in the balance sheet. However, in the

correct form, these two loans are needed to be shown as loans under the non-current

liabilities.

Loan from Westpac

Add: Loan from Commonwealth Bank

Total

$80,000

$20,000

$100,000

Correction 9 – It can also be seen that the accountant of Whirl Limited has not segregated

the assets and liabilities correctly as he has only reported the assets and liabilities as a whole.

As per AASB 101, Paragraph 66-76, items in the balance sheet are segregated between

current assets and non-current assets and current liabilities and non-current liabilities

(aasb.gov.au, 2019).

Correction 7 – The accountant has shown both the provisions separately in the balance sheet,

but these provisions need to be shown together as the provisions for current liabilities.

Provision for Warranty

Add: Provision for Annual Leave

Total

$6000

$18,000

$24,000

Correction 8 – The accountant of Whirl Limited has shown the term loans from Westpac and

Commonwealth Bank separately as the liabilities in the balance sheet. However, in the

correct form, these two loans are needed to be shown as loans under the non-current

liabilities.

Loan from Westpac

Add: Loan from Commonwealth Bank

Total

$80,000

$20,000

$100,000

Correction 9 – It can also be seen that the accountant of Whirl Limited has not segregated

the assets and liabilities correctly as he has only reported the assets and liabilities as a whole.

As per AASB 101, Paragraph 66-76, items in the balance sheet are segregated between

current assets and non-current assets and current liabilities and non-current liabilities

(aasb.gov.au, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED FINANCIAL ACCOUNTING

References

Aasb.gov.au. (2019). Presentation of Financial Statements. Retrieved 7 April 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf

IFRS . (2019). Ifrs.org. Retrieved 7 April 2019, from

https://www.ifrs.org/news-and-events/2019/01/ifrs-16-is-now-effective/

IFRS . (2019). Ifrs.org. Retrieved 7 April 2019, from

https://www.ifrs.org/news-and-events/2019/02/feature-changes-in-financing-

liabilities/

IFRS . (2019). Ifrs.org. Retrieved 7 April 2019, from

https://www.ifrs.org/news-and-events/2019/03/disclosure-initiative-principles-of-

disclosure-project-summary-now-available/

IFRS . (2019). Ifrs.org. Retrieved 7 April 2019, from

https://www.ifrs.org/news-and-events/2019/01/january-iasb-update-published/

News . (2019). Aasb.gov.au. Retrieved 7 April 2019, from

https://www.aasb.gov.au/News/How-special-are-special-purpose-financial-

statements---For-profit-User-and-Preparer-Survey-Results?newsID=310714

News . (2019). Aasb.gov.au. Retrieved 7 April 2019, from

https://www.aasb.gov.au/News/New-compilations-for-reporting-periods-beginning-

on-or-after-1-1-19?newsID=310722

News . (2019). Aasb.gov.au. Retrieved 7 April 2019, from

https://www.aasb.gov.au/News/New-Accounting-Standard--Right-of-Use-Assets-of-

Not-for-Profit-Entities?newsID=310718

News . (2019). Aasb.gov.au. Retrieved 7 April 2019, from

https://www.aasb.gov.au/News/New-Australian-Accounting-Standards?

newsID=310717

News . (2019). Aasb.gov.au. Retrieved 7 April 2019, from

https://www.aasb.gov.au/News/Fatal-flaw-review-draft---Proposed-Standard-AASB-

2019-X-Amendments-to-Australian-Accounting-Standards---References-to-the-

Conceptual-Framework?newsID=310721

References

Aasb.gov.au. (2019). Presentation of Financial Statements. Retrieved 7 April 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf

IFRS . (2019). Ifrs.org. Retrieved 7 April 2019, from

https://www.ifrs.org/news-and-events/2019/01/ifrs-16-is-now-effective/

IFRS . (2019). Ifrs.org. Retrieved 7 April 2019, from

https://www.ifrs.org/news-and-events/2019/02/feature-changes-in-financing-

liabilities/

IFRS . (2019). Ifrs.org. Retrieved 7 April 2019, from

https://www.ifrs.org/news-and-events/2019/03/disclosure-initiative-principles-of-

disclosure-project-summary-now-available/

IFRS . (2019). Ifrs.org. Retrieved 7 April 2019, from

https://www.ifrs.org/news-and-events/2019/01/january-iasb-update-published/

News . (2019). Aasb.gov.au. Retrieved 7 April 2019, from

https://www.aasb.gov.au/News/How-special-are-special-purpose-financial-

statements---For-profit-User-and-Preparer-Survey-Results?newsID=310714

News . (2019). Aasb.gov.au. Retrieved 7 April 2019, from

https://www.aasb.gov.au/News/New-compilations-for-reporting-periods-beginning-

on-or-after-1-1-19?newsID=310722

News . (2019). Aasb.gov.au. Retrieved 7 April 2019, from

https://www.aasb.gov.au/News/New-Accounting-Standard--Right-of-Use-Assets-of-

Not-for-Profit-Entities?newsID=310718

News . (2019). Aasb.gov.au. Retrieved 7 April 2019, from

https://www.aasb.gov.au/News/New-Australian-Accounting-Standards?

newsID=310717

News . (2019). Aasb.gov.au. Retrieved 7 April 2019, from

https://www.aasb.gov.au/News/Fatal-flaw-review-draft---Proposed-Standard-AASB-

2019-X-Amendments-to-Australian-Accounting-Standards---References-to-the-

Conceptual-Framework?newsID=310721

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.