Advanced Investment Management Assignment

VerifiedAdded on 2022/09/14

|12

|2293

|12

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ADVANCED INVESTMENT MANAGEMENT

Advanced Investment Management

Student Name:

Student Number:

Authors Note:

Advanced Investment Management

Student Name:

Student Number:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADVANCED INVESTMENT MANAGEMENT

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Using the covariance matrix providing discussion regarding the rationale for choosing the 5

specific companies:....................................................................................................................2

Creating 5 different portfolios:...................................................................................................3

Recommending one portfolio to the client and explaining rational for the choice:...................4

Conducting an empirical test of the CAPM by describing the setup of CAPM and justify its

merits:.........................................................................................................................................5

Including a brief report summarizing the recent research regarding active or passive

management of investments:......................................................................................................5

Conclusion:................................................................................................................................6

References and Bibliography:....................................................................................................8

Appendix:...................................................................................................................................9

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Using the covariance matrix providing discussion regarding the rationale for choosing the 5

specific companies:....................................................................................................................2

Creating 5 different portfolios:...................................................................................................3

Recommending one portfolio to the client and explaining rational for the choice:...................4

Conducting an empirical test of the CAPM by describing the setup of CAPM and justify its

merits:.........................................................................................................................................5

Including a brief report summarizing the recent research regarding active or passive

management of investments:......................................................................................................5

Conclusion:................................................................................................................................6

References and Bibliography:....................................................................................................8

Appendix:...................................................................................................................................9

ADVANCED INVESTMENT MANAGEMENT

Introduction:

The overall assessment directly aims in evaluating five different portfolios and

detecting the most adequate investment option that can be used by the investors to generate

high level of returns in the process. The adequate analysis of the covariance matrix is

conducted to identify the rationale behind choosing the five specific companies for

investment. This would eventually help in creating five different portfolios that would have

significant alterations towards its risk and return attributes. This could eventually help in

adequately recommending one of the portfolios to the client that would be suitable for

appropriate investments. For the evaluation is conducted on the Capital Asset Pricing Model

relevant calculations are conducted for each of the companies to detect and justify its merits.

Lastly, a summarization of the overall results of the recent research is conducted to identify

whether active and passive management of investment it is better for investors.

Discussion:

Using the covariance matrix providing discussion regarding the rationale for choosing

the 5 specific companies:

In the below appendix information regarding the covariance matrix for the five

selected companies is adequate represented this information is conducted to identify the

rationale behind the selection of such organization. The analysis has been conducted on the

basis of covariance values which tend to reach from 0.005601132 to 0.00509459. The

covariance matrix is mainly used for identifying the overall portfolio variance, which is

considered as an appropriate measure to derive the portfolio values and determine the risk

attributes of the investment. The analysis of the covariance value is relatively conducted for

detecting the overall standard deviation and the various condition of a particular stock, which

Introduction:

The overall assessment directly aims in evaluating five different portfolios and

detecting the most adequate investment option that can be used by the investors to generate

high level of returns in the process. The adequate analysis of the covariance matrix is

conducted to identify the rationale behind choosing the five specific companies for

investment. This would eventually help in creating five different portfolios that would have

significant alterations towards its risk and return attributes. This could eventually help in

adequately recommending one of the portfolios to the client that would be suitable for

appropriate investments. For the evaluation is conducted on the Capital Asset Pricing Model

relevant calculations are conducted for each of the companies to detect and justify its merits.

Lastly, a summarization of the overall results of the recent research is conducted to identify

whether active and passive management of investment it is better for investors.

Discussion:

Using the covariance matrix providing discussion regarding the rationale for choosing

the 5 specific companies:

In the below appendix information regarding the covariance matrix for the five

selected companies is adequate represented this information is conducted to identify the

rationale behind the selection of such organization. The analysis has been conducted on the

basis of covariance values which tend to reach from 0.005601132 to 0.00509459. The

covariance matrix is mainly used for identifying the overall portfolio variance, which is

considered as an appropriate measure to derive the portfolio values and determine the risk

attributes of the investment. The analysis of the covariance value is relatively conducted for

detecting the overall standard deviation and the various condition of a particular stock, which

ADVANCED INVESTMENT MANAGEMENT

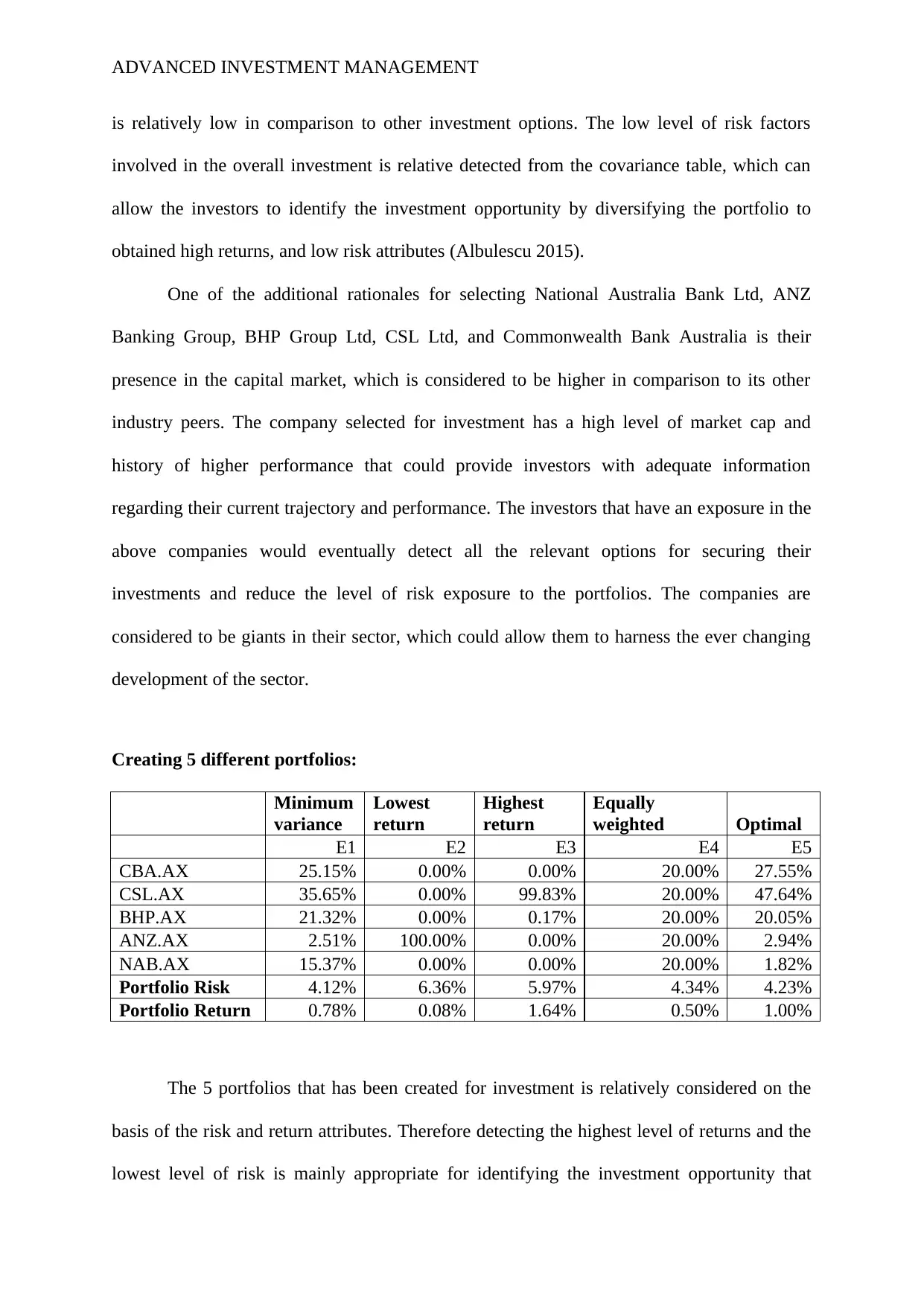

is relatively low in comparison to other investment options. The low level of risk factors

involved in the overall investment is relative detected from the covariance table, which can

allow the investors to identify the investment opportunity by diversifying the portfolio to

obtained high returns, and low risk attributes (Albulescu 2015).

One of the additional rationales for selecting National Australia Bank Ltd, ANZ

Banking Group, BHP Group Ltd, CSL Ltd, and Commonwealth Bank Australia is their

presence in the capital market, which is considered to be higher in comparison to its other

industry peers. The company selected for investment has a high level of market cap and

history of higher performance that could provide investors with adequate information

regarding their current trajectory and performance. The investors that have an exposure in the

above companies would eventually detect all the relevant options for securing their

investments and reduce the level of risk exposure to the portfolios. The companies are

considered to be giants in their sector, which could allow them to harness the ever changing

development of the sector.

Creating 5 different portfolios:

Minimum

variance

Lowest

return

Highest

return

Equally

weighted Optimal

E1 E2 E3 E4 E5

CBA.AX 25.15% 0.00% 0.00% 20.00% 27.55%

CSL.AX 35.65% 0.00% 99.83% 20.00% 47.64%

BHP.AX 21.32% 0.00% 0.17% 20.00% 20.05%

ANZ.AX 2.51% 100.00% 0.00% 20.00% 2.94%

NAB.AX 15.37% 0.00% 0.00% 20.00% 1.82%

Portfolio Risk 4.12% 6.36% 5.97% 4.34% 4.23%

Portfolio Return 0.78% 0.08% 1.64% 0.50% 1.00%

The 5 portfolios that has been created for investment is relatively considered on the

basis of the risk and return attributes. Therefore detecting the highest level of returns and the

lowest level of risk is mainly appropriate for identifying the investment opportunity that

is relatively low in comparison to other investment options. The low level of risk factors

involved in the overall investment is relative detected from the covariance table, which can

allow the investors to identify the investment opportunity by diversifying the portfolio to

obtained high returns, and low risk attributes (Albulescu 2015).

One of the additional rationales for selecting National Australia Bank Ltd, ANZ

Banking Group, BHP Group Ltd, CSL Ltd, and Commonwealth Bank Australia is their

presence in the capital market, which is considered to be higher in comparison to its other

industry peers. The company selected for investment has a high level of market cap and

history of higher performance that could provide investors with adequate information

regarding their current trajectory and performance. The investors that have an exposure in the

above companies would eventually detect all the relevant options for securing their

investments and reduce the level of risk exposure to the portfolios. The companies are

considered to be giants in their sector, which could allow them to harness the ever changing

development of the sector.

Creating 5 different portfolios:

Minimum

variance

Lowest

return

Highest

return

Equally

weighted Optimal

E1 E2 E3 E4 E5

CBA.AX 25.15% 0.00% 0.00% 20.00% 27.55%

CSL.AX 35.65% 0.00% 99.83% 20.00% 47.64%

BHP.AX 21.32% 0.00% 0.17% 20.00% 20.05%

ANZ.AX 2.51% 100.00% 0.00% 20.00% 2.94%

NAB.AX 15.37% 0.00% 0.00% 20.00% 1.82%

Portfolio Risk 4.12% 6.36% 5.97% 4.34% 4.23%

Portfolio Return 0.78% 0.08% 1.64% 0.50% 1.00%

The 5 portfolios that has been created for investment is relatively considered on the

basis of the risk and return attributes. Therefore detecting the highest level of returns and the

lowest level of risk is mainly appropriate for identifying the investment opportunity that

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADVANCED INVESTMENT MANAGEMENT

would be generated from the particular investment. The portfolio that has been created also

consists of minimum variance portfolio, optimal portfolio, lowest return portfolio, highest

return portfolio and equally weighted portfolio. Brandstetter and Lehner (2015) stated that

with the help of different types of portfolios, investors are able to select the best suitable

options that would support their investment criteria and make relevant investment decisions.

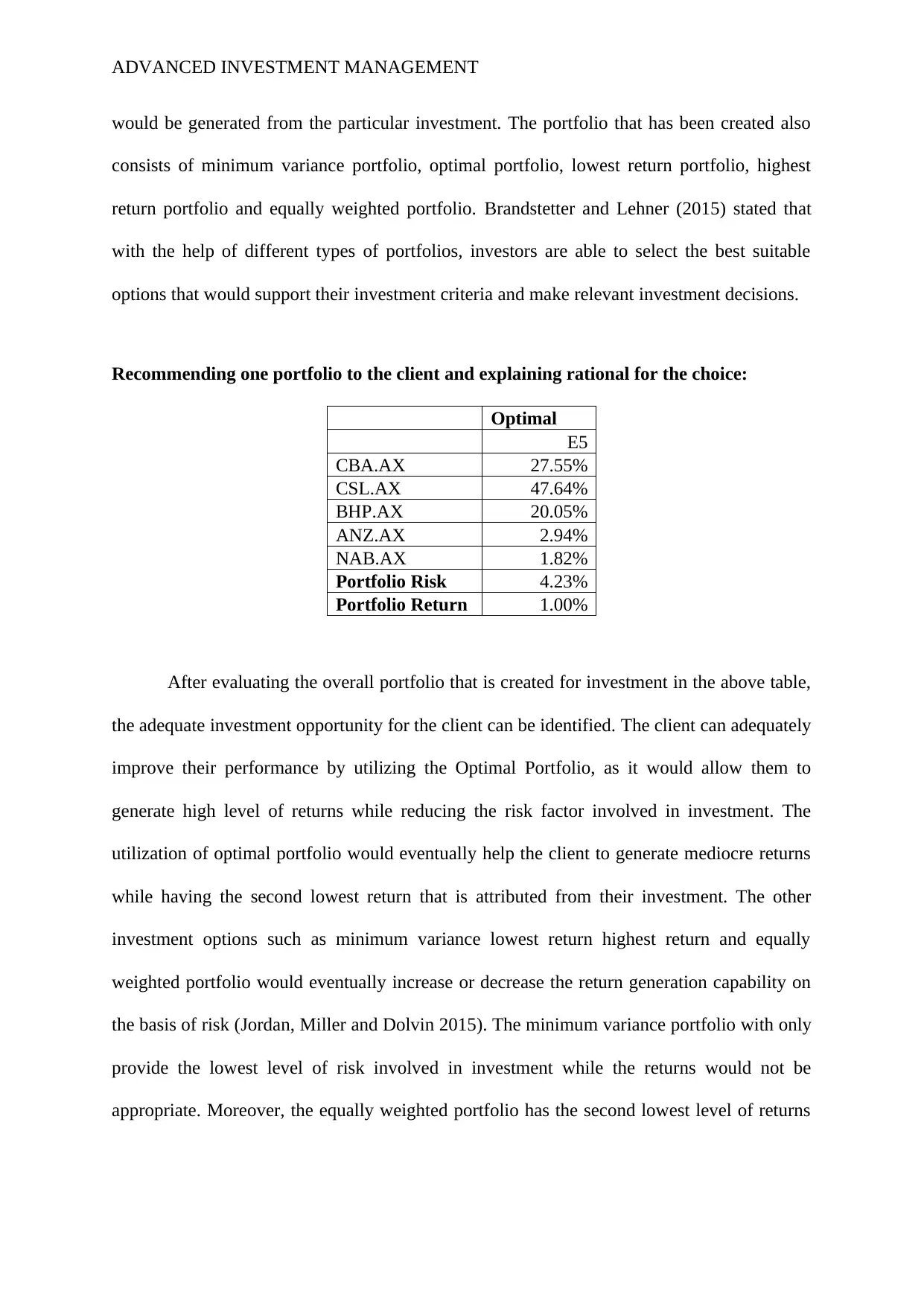

Recommending one portfolio to the client and explaining rational for the choice:

Optimal

E5

CBA.AX 27.55%

CSL.AX 47.64%

BHP.AX 20.05%

ANZ.AX 2.94%

NAB.AX 1.82%

Portfolio Risk 4.23%

Portfolio Return 1.00%

After evaluating the overall portfolio that is created for investment in the above table,

the adequate investment opportunity for the client can be identified. The client can adequately

improve their performance by utilizing the Optimal Portfolio, as it would allow them to

generate high level of returns while reducing the risk factor involved in investment. The

utilization of optimal portfolio would eventually help the client to generate mediocre returns

while having the second lowest return that is attributed from their investment. The other

investment options such as minimum variance lowest return highest return and equally

weighted portfolio would eventually increase or decrease the return generation capability on

the basis of risk (Jordan, Miller and Dolvin 2015). The minimum variance portfolio with only

provide the lowest level of risk involved in investment while the returns would not be

appropriate. Moreover, the equally weighted portfolio has the second lowest level of returns

would be generated from the particular investment. The portfolio that has been created also

consists of minimum variance portfolio, optimal portfolio, lowest return portfolio, highest

return portfolio and equally weighted portfolio. Brandstetter and Lehner (2015) stated that

with the help of different types of portfolios, investors are able to select the best suitable

options that would support their investment criteria and make relevant investment decisions.

Recommending one portfolio to the client and explaining rational for the choice:

Optimal

E5

CBA.AX 27.55%

CSL.AX 47.64%

BHP.AX 20.05%

ANZ.AX 2.94%

NAB.AX 1.82%

Portfolio Risk 4.23%

Portfolio Return 1.00%

After evaluating the overall portfolio that is created for investment in the above table,

the adequate investment opportunity for the client can be identified. The client can adequately

improve their performance by utilizing the Optimal Portfolio, as it would allow them to

generate high level of returns while reducing the risk factor involved in investment. The

utilization of optimal portfolio would eventually help the client to generate mediocre returns

while having the second lowest return that is attributed from their investment. The other

investment options such as minimum variance lowest return highest return and equally

weighted portfolio would eventually increase or decrease the return generation capability on

the basis of risk (Jordan, Miller and Dolvin 2015). The minimum variance portfolio with only

provide the lowest level of risk involved in investment while the returns would not be

appropriate. Moreover, the equally weighted portfolio has the second lowest level of returns

ADVANCED INVESTMENT MANAGEMENT

from an investment. The utilization of the optimal portfolio would relatively increase the

exposure of CSL limited, while using the overall exposure to ANZ and NAB.

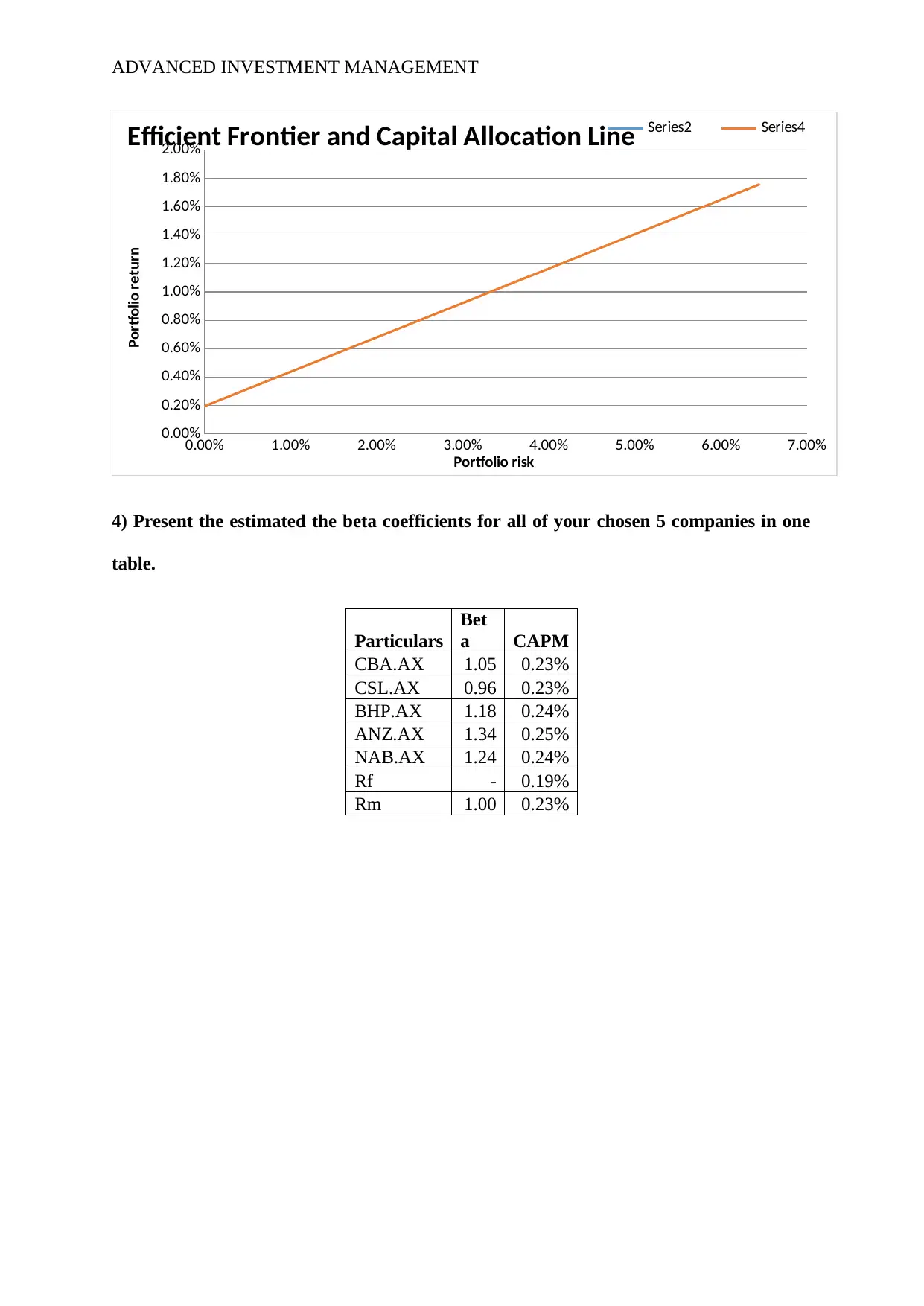

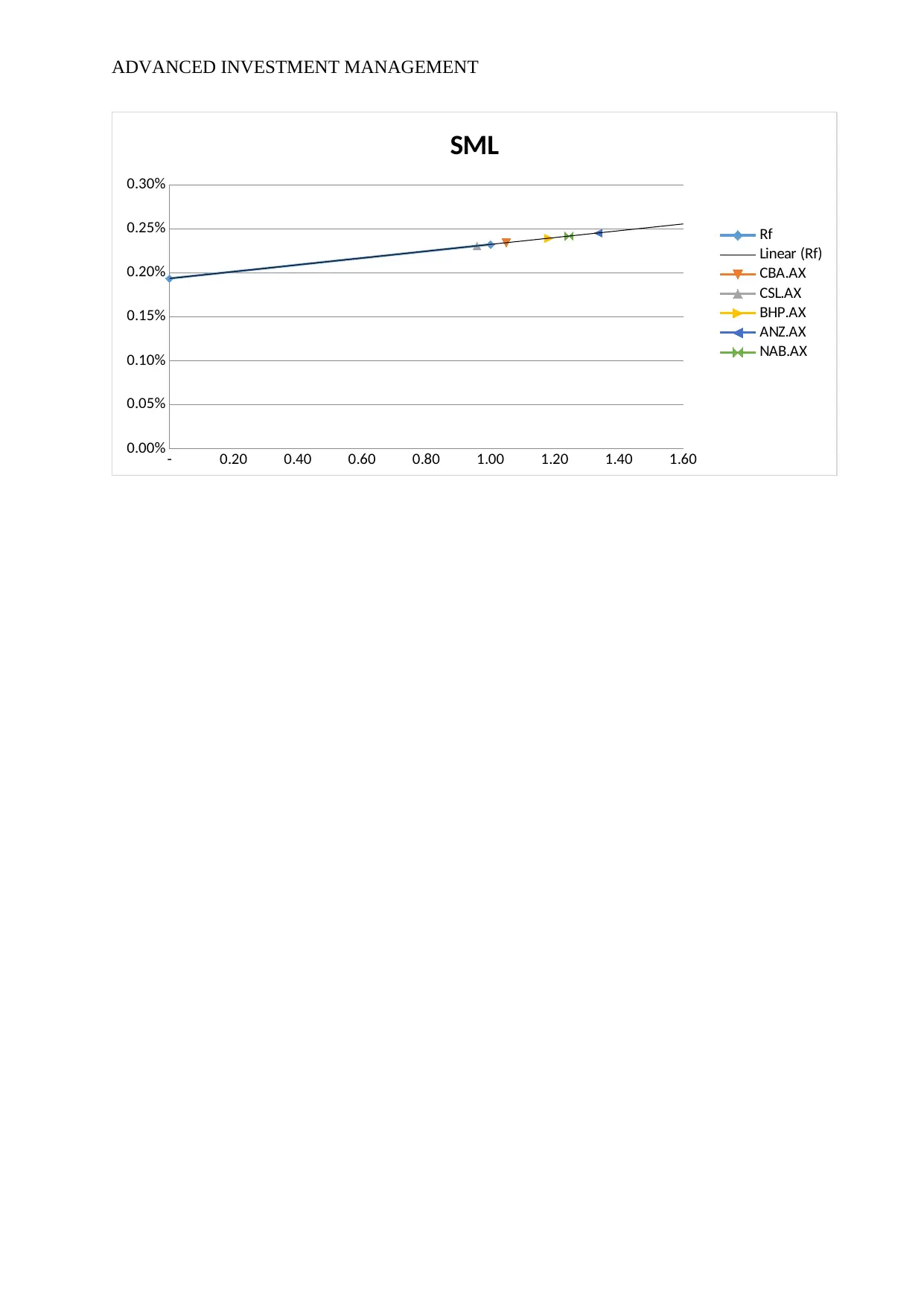

Conducting an empirical test of the CAPM by describing the setup of CAPM and justify

its merits:

The analysis of the appendix has a relatively provided adequate information regarding

the capital asset pricing model that has been used for calculating the returns of each stock.

The graph also presents the overall security market line on which all the returns of the

investment are aligned. This mainly indicates that the values derived from the capital asset

pricing model are relatively adequate where the returns that is provided and expected from

the stocks are in lieu with the market trend. The beta coefficients for all the five companies

are relatively conducted by utilizing the Excel function. The returns of the market and the

other stocks are utilized for detecting the conditions of the investments. The beta levels are

relatively conducted to identify the risk levels of an organization and determine how much

fluctuations the share price would face when the capital market is volatile (Lahr and Mina

2016). Thus, with the help of beta values investors are able to understand and comprehend

the investment options that would help in reducing the level of risk and increasing return

generation capability of their portfolio.

Including a brief report summarizing the recent research regarding active or passive

management of investments:

The research that has been conducted for the investors relatively indicates that active

management of investments is better for an investor perspective in comparison to passive

management. The investors with the help of active management are able to identify all the

relevant changes to the investment portfolio and stabilize the level of risk that is affecting

their investment. The use of passive management would relatively increase the risk exposure

from an investment. The utilization of the optimal portfolio would relatively increase the

exposure of CSL limited, while using the overall exposure to ANZ and NAB.

Conducting an empirical test of the CAPM by describing the setup of CAPM and justify

its merits:

The analysis of the appendix has a relatively provided adequate information regarding

the capital asset pricing model that has been used for calculating the returns of each stock.

The graph also presents the overall security market line on which all the returns of the

investment are aligned. This mainly indicates that the values derived from the capital asset

pricing model are relatively adequate where the returns that is provided and expected from

the stocks are in lieu with the market trend. The beta coefficients for all the five companies

are relatively conducted by utilizing the Excel function. The returns of the market and the

other stocks are utilized for detecting the conditions of the investments. The beta levels are

relatively conducted to identify the risk levels of an organization and determine how much

fluctuations the share price would face when the capital market is volatile (Lahr and Mina

2016). Thus, with the help of beta values investors are able to understand and comprehend

the investment options that would help in reducing the level of risk and increasing return

generation capability of their portfolio.

Including a brief report summarizing the recent research regarding active or passive

management of investments:

The research that has been conducted for the investors relatively indicates that active

management of investments is better for an investor perspective in comparison to passive

management. The investors with the help of active management are able to identify all the

relevant changes to the investment portfolio and stabilize the level of risk that is affecting

their investment. The use of passive management would relatively increase the risk exposure

ADVANCED INVESTMENT MANAGEMENT

of the investors and force them to incur losses in the long run due to the inactive management

of the portfolios. Baker and Ricciardi (2014) stated that passive management in portfolios

does not allow the investors to accommodate the changes that has been made due to the

fluctuations in the market.

During the current era the overall fluctuations in the capital market is subject to the

alterations in the perspective of investors and other announcements made by government and

organizations. The continuous delivery of information to the investors regarding different

attributes of the investment is relatively altering the overall perspective of investors regarding

the investment scope. The continuous changes have relatively increased the concern for the

investors to actively manage their investments for reducing the level of risk that is faced

while conducting investments in the capital market. Investors that are following the passive

management system are relatively not able to comprehend the changes and make adequate

returns from their investments due to the change in the pricing conditions of the investments

(Bebchuk, Cohen and Hirst 2017). Investors are currently reliant on the mispricing that is

present within the capital market due to the continuous flow of information from organization

to the investors. Thus, investors utilizing the active management scheme would eventually

benefit from the mispricing and generate adequate returns in the process.

Conclusion:

The assessment has adequately provided the adequate investment opportunity to the

investors in the form of the optimal portfolio that could help in reducing the level of risk and

simultaneously generate adequate returns in the process. Therefore, relevant discussion has

been conducted on the choice of the five stocks that is used for creating the optimal portfolio.

The low level of covariance that is involved in the returns of the five stocks is the main

reason behind the selection of the organizations as investments. The recommendation for the

of the investors and force them to incur losses in the long run due to the inactive management

of the portfolios. Baker and Ricciardi (2014) stated that passive management in portfolios

does not allow the investors to accommodate the changes that has been made due to the

fluctuations in the market.

During the current era the overall fluctuations in the capital market is subject to the

alterations in the perspective of investors and other announcements made by government and

organizations. The continuous delivery of information to the investors regarding different

attributes of the investment is relatively altering the overall perspective of investors regarding

the investment scope. The continuous changes have relatively increased the concern for the

investors to actively manage their investments for reducing the level of risk that is faced

while conducting investments in the capital market. Investors that are following the passive

management system are relatively not able to comprehend the changes and make adequate

returns from their investments due to the change in the pricing conditions of the investments

(Bebchuk, Cohen and Hirst 2017). Investors are currently reliant on the mispricing that is

present within the capital market due to the continuous flow of information from organization

to the investors. Thus, investors utilizing the active management scheme would eventually

benefit from the mispricing and generate adequate returns in the process.

Conclusion:

The assessment has adequately provided the adequate investment opportunity to the

investors in the form of the optimal portfolio that could help in reducing the level of risk and

simultaneously generate adequate returns in the process. Therefore, relevant discussion has

been conducted on the choice of the five stocks that is used for creating the optimal portfolio.

The low level of covariance that is involved in the returns of the five stocks is the main

reason behind the selection of the organizations as investments. The recommendation for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED INVESTMENT MANAGEMENT

client is the optimal portfolio, as it comprises of adequate returns with the second lowest risk

involved in investment. The adequate derivation of the CAPM formula has directly indicated

that ANZ Bank requires the highest return, as the beta levels of the organization is highest

among the five selected stocks. Lastly, it is understood that investors need to engage in active

management of their investments, as the overall investment scope changes with the flow of

information into the capital market.

client is the optimal portfolio, as it comprises of adequate returns with the second lowest risk

involved in investment. The adequate derivation of the CAPM formula has directly indicated

that ANZ Bank requires the highest return, as the beta levels of the organization is highest

among the five selected stocks. Lastly, it is understood that investors need to engage in active

management of their investments, as the overall investment scope changes with the flow of

information into the capital market.

ADVANCED INVESTMENT MANAGEMENT

References and Bibliography:

Albulescu, C.T., 2015. Do Foreign Direct and Portfolio Investments Affect Long-term

Economic Growth in Central and Eastern Europe?. Procedia economics and finance, 23,

pp.507-512.

Au.finance.yahoo.com. 2019. Yahoo is now a part of Oath. [online] Available at:

https://au.finance.yahoo.com/ [Accessed 31 Aug. 2019].

Baker, H.K. and Ricciardi, V., 2014. Investor behavior: The psychology of financial planning

and investing. John Wiley & Sons.

Bebchuk, L.A., Cohen, A. and Hirst, S., 2017. The agency problems of institutional

investors. Journal of Economic Perspectives, 31(3), pp.89-102.

Brandstetter, L. and Lehner, O.M., 2015. Opening the market for impact investments: The

need for adapted portfolio tools. Entrepreneurship Research Journal, 5(2), pp.87-107.

Investing.com. 2019. Australia 10-Year Bond Historical Data - Investing.com. [online]

Available at: https://www.investing.com/rates-bonds/australia-10-year-bond-yield-historical-

data [Accessed 31 Aug. 2019].

Jordan, B.D., Miller, T.W. and Dolvin, S.D., 2015. Fundamentals of investments: valuation

and management. McGraw-Hill Education.

Lahr, H. and Mina, A., 2016. Venture capital investments and the technological performance

of portfolio firms. Research Policy, 45(1), pp.303-318.

Reserve Bank of Australia. 2019. Cash Rate. [online] Available at:

https://www.rba.gov.au/statistics/cash-rate/ [Accessed 31 Aug. 2019].

References and Bibliography:

Albulescu, C.T., 2015. Do Foreign Direct and Portfolio Investments Affect Long-term

Economic Growth in Central and Eastern Europe?. Procedia economics and finance, 23,

pp.507-512.

Au.finance.yahoo.com. 2019. Yahoo is now a part of Oath. [online] Available at:

https://au.finance.yahoo.com/ [Accessed 31 Aug. 2019].

Baker, H.K. and Ricciardi, V., 2014. Investor behavior: The psychology of financial planning

and investing. John Wiley & Sons.

Bebchuk, L.A., Cohen, A. and Hirst, S., 2017. The agency problems of institutional

investors. Journal of Economic Perspectives, 31(3), pp.89-102.

Brandstetter, L. and Lehner, O.M., 2015. Opening the market for impact investments: The

need for adapted portfolio tools. Entrepreneurship Research Journal, 5(2), pp.87-107.

Investing.com. 2019. Australia 10-Year Bond Historical Data - Investing.com. [online]

Available at: https://www.investing.com/rates-bonds/australia-10-year-bond-yield-historical-

data [Accessed 31 Aug. 2019].

Jordan, B.D., Miller, T.W. and Dolvin, S.D., 2015. Fundamentals of investments: valuation

and management. McGraw-Hill Education.

Lahr, H. and Mina, A., 2016. Venture capital investments and the technological performance

of portfolio firms. Research Policy, 45(1), pp.303-318.

Reserve Bank of Australia. 2019. Cash Rate. [online] Available at:

https://www.rba.gov.au/statistics/cash-rate/ [Accessed 31 Aug. 2019].

ADVANCED INVESTMENT MANAGEMENT

Us.spindices.com. 2019. S&P/ASX 300 (AUD) - S&P Dow Jones Indices. [online] Available

at: https://us.spindices.com/indices/equity/sp-asx-300 [Accessed 31 Aug. 2019].

Appendix:

1) Identify your portfolios and shares (with names and ASX identification codes).

Present all the key performance and risk measures in one table.

ASX

Code Name Key performance

CBA.AX Commonwealth Bank Australia One of the leaders in financials sector

CSL.AX CSL Ltd One of the leaders in health care sector

BHP.AX BHP Group Ltd One of the leaders in materials sector

ANZ.AX ANZ Banking Group One of the leaders in financials sector

NAB.AX National Australia Bank Ltd One of the leaders in financials sector

2) Include the covariance matrix. Do not present the raw share prices, index or the

returns data.

Covariance

Matrix CBA.AX CSL.AX BHP.AX ANZ.AX NAB.AX

CBA.AX

0.00325171

1

0.00075858

4

0.00087877

9 0.00249071 0.00232816

CSL.AX

0.00075858

4

0.00357071

5

0.00056011

3

0.00073754

6

0.00061217

4

BHP.AX

0.00087877

9

0.00056011

3 0.00509459

0.00094336

1

0.00107689

7

ANZ.AX 0.00249071

0.00073754

6

0.00094336

1

0.00404186

1

0.00327897

5

NAB.AX 0.00232816

0.00061217

4

0.00107689

7

0.00327897

5

0.00377543

6

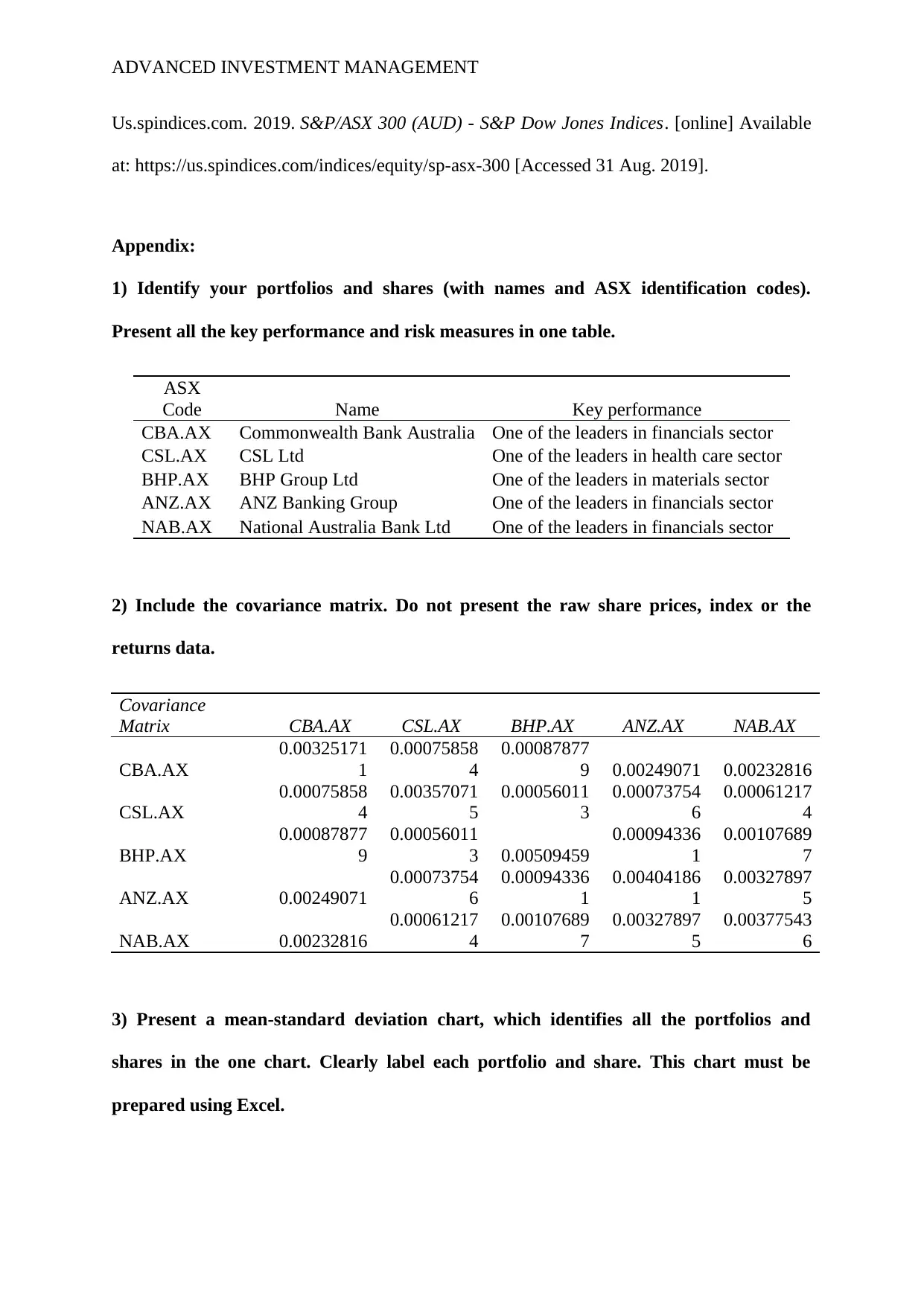

3) Present a mean-standard deviation chart, which identifies all the portfolios and

shares in the one chart. Clearly label each portfolio and share. This chart must be

prepared using Excel.

Us.spindices.com. 2019. S&P/ASX 300 (AUD) - S&P Dow Jones Indices. [online] Available

at: https://us.spindices.com/indices/equity/sp-asx-300 [Accessed 31 Aug. 2019].

Appendix:

1) Identify your portfolios and shares (with names and ASX identification codes).

Present all the key performance and risk measures in one table.

ASX

Code Name Key performance

CBA.AX Commonwealth Bank Australia One of the leaders in financials sector

CSL.AX CSL Ltd One of the leaders in health care sector

BHP.AX BHP Group Ltd One of the leaders in materials sector

ANZ.AX ANZ Banking Group One of the leaders in financials sector

NAB.AX National Australia Bank Ltd One of the leaders in financials sector

2) Include the covariance matrix. Do not present the raw share prices, index or the

returns data.

Covariance

Matrix CBA.AX CSL.AX BHP.AX ANZ.AX NAB.AX

CBA.AX

0.00325171

1

0.00075858

4

0.00087877

9 0.00249071 0.00232816

CSL.AX

0.00075858

4

0.00357071

5

0.00056011

3

0.00073754

6

0.00061217

4

BHP.AX

0.00087877

9

0.00056011

3 0.00509459

0.00094336

1

0.00107689

7

ANZ.AX 0.00249071

0.00073754

6

0.00094336

1

0.00404186

1

0.00327897

5

NAB.AX 0.00232816

0.00061217

4

0.00107689

7

0.00327897

5

0.00377543

6

3) Present a mean-standard deviation chart, which identifies all the portfolios and

shares in the one chart. Clearly label each portfolio and share. This chart must be

prepared using Excel.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADVANCED INVESTMENT MANAGEMENT

0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 7.00%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

2.00%

Efficient Frontier and Capital Allocation Line Series2 Series4

Portfolio risk

Portfolio return

4) Present the estimated the beta coefficients for all of your chosen 5 companies in one

table.

Particulars

Bet

a CAPM

CBA.AX 1.05 0.23%

CSL.AX 0.96 0.23%

BHP.AX 1.18 0.24%

ANZ.AX 1.34 0.25%

NAB.AX 1.24 0.24%

Rf - 0.19%

Rm 1.00 0.23%

0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 7.00%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

2.00%

Efficient Frontier and Capital Allocation Line Series2 Series4

Portfolio risk

Portfolio return

4) Present the estimated the beta coefficients for all of your chosen 5 companies in one

table.

Particulars

Bet

a CAPM

CBA.AX 1.05 0.23%

CSL.AX 0.96 0.23%

BHP.AX 1.18 0.24%

ANZ.AX 1.34 0.25%

NAB.AX 1.24 0.24%

Rf - 0.19%

Rm 1.00 0.23%

ADVANCED INVESTMENT MANAGEMENT

- 0.20 0.40 0.60 0.80 1.00 1.20 1.40 1.60

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

SML

Rf

Linear (Rf)

CBA.AX

CSL.AX

BHP.AX

ANZ.AX

NAB.AX

- 0.20 0.40 0.60 0.80 1.00 1.20 1.40 1.60

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

SML

Rf

Linear (Rf)

CBA.AX

CSL.AX

BHP.AX

ANZ.AX

NAB.AX

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.