Advanced Management Accounting: NPV and IRR Analysis for Investment Appraisal

VerifiedAdded on 2023/06/18

|7

|2033

|176

AI Summary

This report analyzes the financial viability of investing in a new machine for Alzahraa Ltd. using Net Present Value (NPV) and Internal Rate of Return (IRR) approaches. It also provides a critical analysis of sophisticated capital budgeting practices and the effect of uncertainty and irreversibility on capital budgeting decisions. The report concludes with a recommendation not to invest in the project due to negative NPV and IRR less than the cost of capital.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Advance Management

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION......................................................................................................................4

MAIN BODY.............................................................................................................................4

(a) Calculate NPV and IRR and give recommendations based on the results.......................4

(b) Give a critical analysis of the applications and development of the sophisticated capital

budgeting practices.................................................................................................................5

(c) The critical analysis of the effect of uncertainty and irreversibility on capital budgeting

decisions in practice...............................................................................................................6

CONCLUSION..........................................................................................................................7

REFERENCES...........................................................................................................................8

INTRODUCTION......................................................................................................................4

MAIN BODY.............................................................................................................................4

(a) Calculate NPV and IRR and give recommendations based on the results.......................4

(b) Give a critical analysis of the applications and development of the sophisticated capital

budgeting practices.................................................................................................................5

(c) The critical analysis of the effect of uncertainty and irreversibility on capital budgeting

decisions in practice...............................................................................................................6

CONCLUSION..........................................................................................................................7

REFERENCES...........................................................................................................................8

INTRODUCTION

Management accounting can be characterized as a course of giving monetary data and

assets to the executive for decision – making. It can only be utilized by the internal sources of

the association (Gottlieb, Hansson and Johed, 2021). Alzahraa Ltd. is a new organisation

which manufactures a part of car called “Moto”. Several investment appraisal approaches are

used in this report to assess the machine's financial viability. The study gives a

recommendation for purchasing the machine by weighing the advantages, disadvantages, and

outcomes of two investment appraisal methodologies. The Net Present Value (NPV) and

Internal Rate of Return (IRR) are the approaches employed in this report (IRR). The NPV

emphasises the present value of cash flow, whereas the IRR determines the amount of interest

earned on the investment. Because of the variances in their techniques and computations, the

outcomes of these methods may not be comparable. As a result, it's a good idea to try out a

few different investment appraisal methods and grasp their merits and drawbacks before

making a final decision.

MAIN BODY

(a) Calculate NPV and IRR and give recommendations based on the results.

The NPV takes into account the time value of money and demonstrates that cash

received now is preferable than cash received later, indicating the difference between the

present value of cash inflows and outflows over time. The NPV evaluates an investment's

profitability, but the IRR approximates the return earned when the NPV of all cash flows

equals zero. Using the IRR implies that there is some risk involved in calculating the IRR

value. Due to the volatility of cash value, the discount factor (DF) is liable to vary, posing a

risk and uncertainty to the investment's future (Amoako and et. al., 2021). Furthermore, when

making investment selections, both investment assessment approaches have their own set of

advantages and disadvantages.

Management accounting can be characterized as a course of giving monetary data and

assets to the executive for decision – making. It can only be utilized by the internal sources of

the association (Gottlieb, Hansson and Johed, 2021). Alzahraa Ltd. is a new organisation

which manufactures a part of car called “Moto”. Several investment appraisal approaches are

used in this report to assess the machine's financial viability. The study gives a

recommendation for purchasing the machine by weighing the advantages, disadvantages, and

outcomes of two investment appraisal methodologies. The Net Present Value (NPV) and

Internal Rate of Return (IRR) are the approaches employed in this report (IRR). The NPV

emphasises the present value of cash flow, whereas the IRR determines the amount of interest

earned on the investment. Because of the variances in their techniques and computations, the

outcomes of these methods may not be comparable. As a result, it's a good idea to try out a

few different investment appraisal methods and grasp their merits and drawbacks before

making a final decision.

MAIN BODY

(a) Calculate NPV and IRR and give recommendations based on the results.

The NPV takes into account the time value of money and demonstrates that cash

received now is preferable than cash received later, indicating the difference between the

present value of cash inflows and outflows over time. The NPV evaluates an investment's

profitability, but the IRR approximates the return earned when the NPV of all cash flows

equals zero. Using the IRR implies that there is some risk involved in calculating the IRR

value. Due to the volatility of cash value, the discount factor (DF) is liable to vary, posing a

risk and uncertainty to the investment's future (Amoako and et. al., 2021). Furthermore, when

making investment selections, both investment assessment approaches have their own set of

advantages and disadvantages.

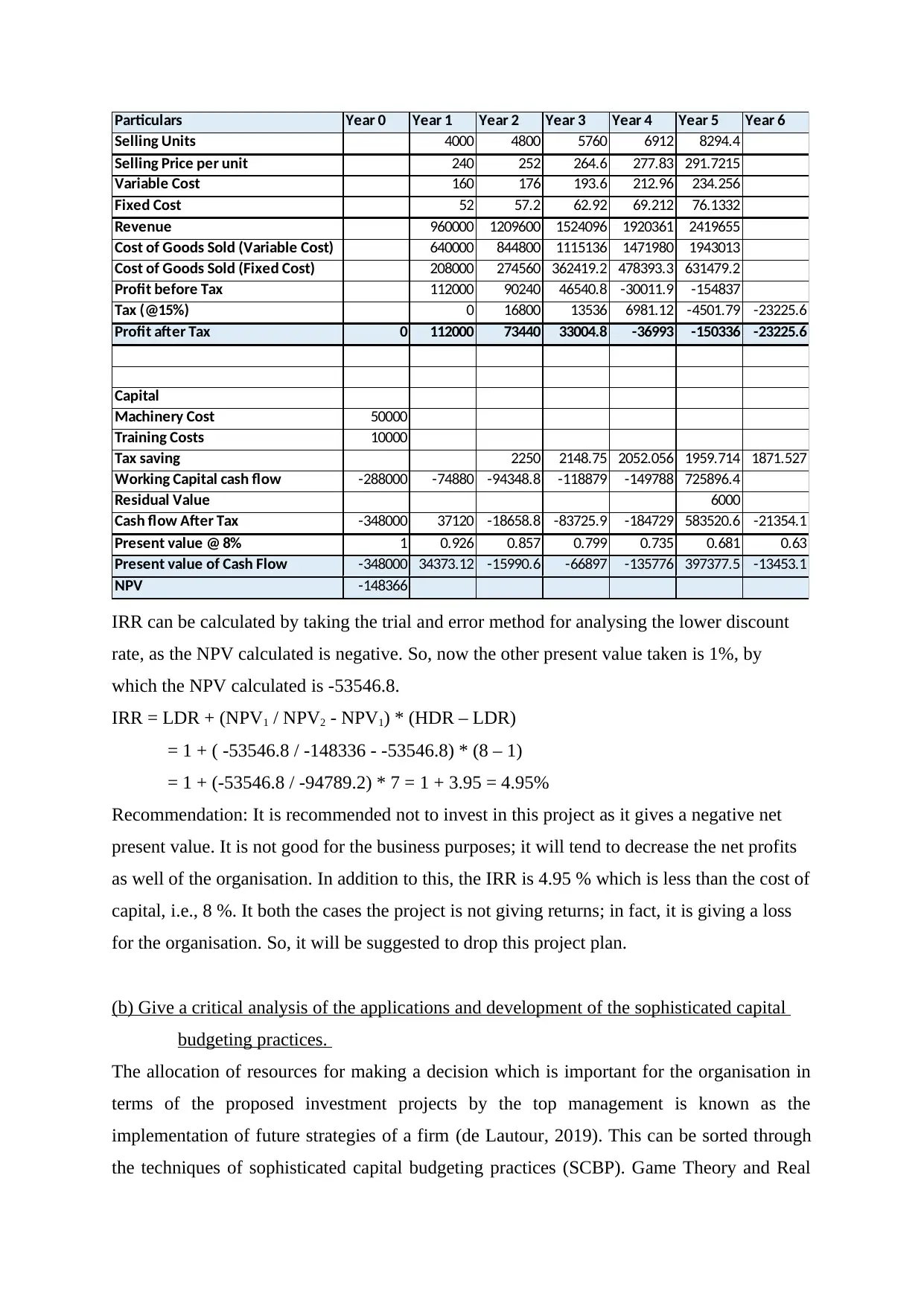

Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Selling Units 4000 4800 5760 6912 8294.4

Selling Price per unit 240 252 264.6 277.83 291.7215

Variable Cost 160 176 193.6 212.96 234.256

Fixed Cost 52 57.2 62.92 69.212 76.1332

Revenue 960000 1209600 1524096 1920361 2419655

Cost of Goods Sold (Variable Cost) 640000 844800 1115136 1471980 1943013

Cost of Goods Sold (Fixed Cost) 208000 274560 362419.2 478393.3 631479.2

Profit before Tax 112000 90240 46540.8 -30011.9 -154837

Tax (@15%) 0 16800 13536 6981.12 -4501.79 -23225.6

Profit after Tax 0 112000 73440 33004.8 -36993 -150336 -23225.6

Capital

Machinery Cost 50000

Training Costs 10000

Tax saving 2250 2148.75 2052.056 1959.714 1871.527

Working Capital cash flow -288000 -74880 -94348.8 -118879 -149788 725896.4

Residual Value 6000

Cash flow After Tax -348000 37120 -18658.8 -83725.9 -184729 583520.6 -21354.1

Present value @ 8% 1 0.926 0.857 0.799 0.735 0.681 0.63

Present value of Cash Flow -348000 34373.12 -15990.6 -66897 -135776 397377.5 -13453.1

NPV -148366

IRR can be calculated by taking the trial and error method for analysing the lower discount

rate, as the NPV calculated is negative. So, now the other present value taken is 1%, by

which the NPV calculated is -53546.8.

IRR = LDR + (NPV1 / NPV2 - NPV1) * (HDR – LDR)

= 1 + ( -53546.8 / -148336 - -53546.8) * (8 – 1)

= 1 + (-53546.8 / -94789.2) * 7 = 1 + 3.95 = 4.95%

Recommendation: It is recommended not to invest in this project as it gives a negative net

present value. It is not good for the business purposes; it will tend to decrease the net profits

as well of the organisation. In addition to this, the IRR is 4.95 % which is less than the cost of

capital, i.e., 8 %. It both the cases the project is not giving returns; in fact, it is giving a loss

for the organisation. So, it will be suggested to drop this project plan.

(b) Give a critical analysis of the applications and development of the sophisticated capital

budgeting practices.

The allocation of resources for making a decision which is important for the organisation in

terms of the proposed investment projects by the top management is known as the

implementation of future strategies of a firm (de Lautour, 2019). This can be sorted through

the techniques of sophisticated capital budgeting practices (SCBP). Game Theory and Real

Selling Units 4000 4800 5760 6912 8294.4

Selling Price per unit 240 252 264.6 277.83 291.7215

Variable Cost 160 176 193.6 212.96 234.256

Fixed Cost 52 57.2 62.92 69.212 76.1332

Revenue 960000 1209600 1524096 1920361 2419655

Cost of Goods Sold (Variable Cost) 640000 844800 1115136 1471980 1943013

Cost of Goods Sold (Fixed Cost) 208000 274560 362419.2 478393.3 631479.2

Profit before Tax 112000 90240 46540.8 -30011.9 -154837

Tax (@15%) 0 16800 13536 6981.12 -4501.79 -23225.6

Profit after Tax 0 112000 73440 33004.8 -36993 -150336 -23225.6

Capital

Machinery Cost 50000

Training Costs 10000

Tax saving 2250 2148.75 2052.056 1959.714 1871.527

Working Capital cash flow -288000 -74880 -94348.8 -118879 -149788 725896.4

Residual Value 6000

Cash flow After Tax -348000 37120 -18658.8 -83725.9 -184729 583520.6 -21354.1

Present value @ 8% 1 0.926 0.857 0.799 0.735 0.681 0.63

Present value of Cash Flow -348000 34373.12 -15990.6 -66897 -135776 397377.5 -13453.1

NPV -148366

IRR can be calculated by taking the trial and error method for analysing the lower discount

rate, as the NPV calculated is negative. So, now the other present value taken is 1%, by

which the NPV calculated is -53546.8.

IRR = LDR + (NPV1 / NPV2 - NPV1) * (HDR – LDR)

= 1 + ( -53546.8 / -148336 - -53546.8) * (8 – 1)

= 1 + (-53546.8 / -94789.2) * 7 = 1 + 3.95 = 4.95%

Recommendation: It is recommended not to invest in this project as it gives a negative net

present value. It is not good for the business purposes; it will tend to decrease the net profits

as well of the organisation. In addition to this, the IRR is 4.95 % which is less than the cost of

capital, i.e., 8 %. It both the cases the project is not giving returns; in fact, it is giving a loss

for the organisation. So, it will be suggested to drop this project plan.

(b) Give a critical analysis of the applications and development of the sophisticated capital

budgeting practices.

The allocation of resources for making a decision which is important for the organisation in

terms of the proposed investment projects by the top management is known as the

implementation of future strategies of a firm (de Lautour, 2019). This can be sorted through

the techniques of sophisticated capital budgeting practices (SCBP). Game Theory and Real

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Option Reasoning are examples of SCBP. The one focuses on strategizing a company's 'game

plan,' while the other bases its practise on real-life logic. GT is based on the idea of tailoring

a company's business plan to rational players called strategic decision-makers and then

assessing their results. Specific uncertainties, according to GT, can affect the best investment

criterion. ROR, on the other hand, is based on the idea of providing managers with rational

financial options when an investment presents a chance. Expansion, delay, postponements,

and mothballing are some of these alternatives (Nsor-Ambala, 2020).

Traditional approaches such as NPV and IRR are supplemented rather than replaced

by SCBP. These alternatives provide organisational flexibility because future decisions may

result in potential rewards. The readiness to invest is a significant difference between ROR

and GT, since ROR prefers to wait investment in order to acquire more data, but GT

investigates the concept of 'losing out' the investment to another company interested in

investing in advance. Advanced capital budgeting techniques such as NPV and IRR, on the

other hand, consider the time value of money, cash flows, and risk.

In the Alzahraa, the value of money of time is considered to be an important factor, as

it is the new organisations in the market and keeping the business solvent is very crucial and

essential. Although, due to lack of concern in the future investment and cost, it has to

eliminate the project because it will incur the losses to the firm.

When using SCBP, organizations are expected to spend more time, resources, and

money implementing it efficiently. The larger companies are more likely to adopt different

decision-making practices than smaller companies because of the level of facilities,

resources, and assets that need to implement these ideas. They are exposed to greater

expertise in this area, which results in them having greater capacity and willingness to adapt

to different household practices. Companies are more likely to adopt SCBP when there is

financial uncertainty rather than social market and input uncertainty. Consequently, capital

planning helps managers select investments with high returns and an acceptable risk of

return.

(c) The critical analysis of the effect of uncertainty and irreversibility on capital budgeting

decisions in practice.

Companies use SCBP when there is a certain risk and uncertainty associated with it. In

general, the higher the risk, the more valuable is an investment. It shows that uncertainty is

the main difference between existing information and unknown and unavailable information.

Additionally, companies adjust their payback period and discount factor to handle this, which

plan,' while the other bases its practise on real-life logic. GT is based on the idea of tailoring

a company's business plan to rational players called strategic decision-makers and then

assessing their results. Specific uncertainties, according to GT, can affect the best investment

criterion. ROR, on the other hand, is based on the idea of providing managers with rational

financial options when an investment presents a chance. Expansion, delay, postponements,

and mothballing are some of these alternatives (Nsor-Ambala, 2020).

Traditional approaches such as NPV and IRR are supplemented rather than replaced

by SCBP. These alternatives provide organisational flexibility because future decisions may

result in potential rewards. The readiness to invest is a significant difference between ROR

and GT, since ROR prefers to wait investment in order to acquire more data, but GT

investigates the concept of 'losing out' the investment to another company interested in

investing in advance. Advanced capital budgeting techniques such as NPV and IRR, on the

other hand, consider the time value of money, cash flows, and risk.

In the Alzahraa, the value of money of time is considered to be an important factor, as

it is the new organisations in the market and keeping the business solvent is very crucial and

essential. Although, due to lack of concern in the future investment and cost, it has to

eliminate the project because it will incur the losses to the firm.

When using SCBP, organizations are expected to spend more time, resources, and

money implementing it efficiently. The larger companies are more likely to adopt different

decision-making practices than smaller companies because of the level of facilities,

resources, and assets that need to implement these ideas. They are exposed to greater

expertise in this area, which results in them having greater capacity and willingness to adapt

to different household practices. Companies are more likely to adopt SCBP when there is

financial uncertainty rather than social market and input uncertainty. Consequently, capital

planning helps managers select investments with high returns and an acceptable risk of

return.

(c) The critical analysis of the effect of uncertainty and irreversibility on capital budgeting

decisions in practice.

Companies use SCBP when there is a certain risk and uncertainty associated with it. In

general, the higher the risk, the more valuable is an investment. It shows that uncertainty is

the main difference between existing information and unknown and unavailable information.

Additionally, companies adjust their payback period and discount factor to handle this, which

inevitably delays investment decisions in the long run. Small firms are more inclined to

irreversibility and uncertainty, so their decision to refrain from investing is usually based on a

lack of funds. In the case of Alzahraa, a company that has been new in the market and has

started its operation for approximately two years, investing in machines required several

investment appraisal methods to be used to make it a viable option for the company.

However, larger companies often have separate owner and control teams, which can reduce

the uncertainty in investment valuation. Managers have greater control over resources and

assets without suffering the consequences of bad decisions. This effect should be offset if

there is a viable option to await an investment decision (Cowton, 2018).

In relation to this, a SCBP, for example, ROR uses non- systematic and systematic

risk, handling the level of irreversibility. When a real option offers more flexibility, most

corporations employ payback approaches such as the Capital Asset Pricing Model (CAPM),

which solely deals with non-systematic risks via portfolio theory and diversification and does

not provide a procedure for analysing systematic risk. ROR does not challenge the dominance

of NPV, IRR, or PB, but it does provide a better understanding of irreversibility and

uncertainty. Using standard capital budgeting approaches like NPV or IRR has become a

bookmark, leading in the certainty of these on the capital budgeting decisions. Demand

uncertainty, a lack of internal capital, high interest rates, and uncertain interest rates are all

factors that contribute to investment delays. This is because to the fact that smaller businesses

choose high interest rates and UC above uncertainty and finance.

CONCLUSION

For the foreseeable future, capital budgeting approaches will be adopted to varying degrees,

and corporations will choose their favourite way. Most businesses bend the rules to achieve

their own goals; it's a complex topic that's tough to summarise. In the case of Baby Boss Ltd,

using both NPV and IRR to determine whether it was a good investment was ideal. Further

analysis, is done to analyse the finer aspects of the investment using sophisticated capital

budgeting methods. Capital budgeting is a term that encompasses two important decisions: an

investment decision and the financial decision that goes along with it. Acceptance of the

investment means that the company will commit itself financially to the initiative on an

arbitrary basis, including risk and uncertainty. Project delays, cost overruns, and legal

restrictions can result in total costs being suspended or increased. In addition, companies

irreversibility and uncertainty, so their decision to refrain from investing is usually based on a

lack of funds. In the case of Alzahraa, a company that has been new in the market and has

started its operation for approximately two years, investing in machines required several

investment appraisal methods to be used to make it a viable option for the company.

However, larger companies often have separate owner and control teams, which can reduce

the uncertainty in investment valuation. Managers have greater control over resources and

assets without suffering the consequences of bad decisions. This effect should be offset if

there is a viable option to await an investment decision (Cowton, 2018).

In relation to this, a SCBP, for example, ROR uses non- systematic and systematic

risk, handling the level of irreversibility. When a real option offers more flexibility, most

corporations employ payback approaches such as the Capital Asset Pricing Model (CAPM),

which solely deals with non-systematic risks via portfolio theory and diversification and does

not provide a procedure for analysing systematic risk. ROR does not challenge the dominance

of NPV, IRR, or PB, but it does provide a better understanding of irreversibility and

uncertainty. Using standard capital budgeting approaches like NPV or IRR has become a

bookmark, leading in the certainty of these on the capital budgeting decisions. Demand

uncertainty, a lack of internal capital, high interest rates, and uncertain interest rates are all

factors that contribute to investment delays. This is because to the fact that smaller businesses

choose high interest rates and UC above uncertainty and finance.

CONCLUSION

For the foreseeable future, capital budgeting approaches will be adopted to varying degrees,

and corporations will choose their favourite way. Most businesses bend the rules to achieve

their own goals; it's a complex topic that's tough to summarise. In the case of Baby Boss Ltd,

using both NPV and IRR to determine whether it was a good investment was ideal. Further

analysis, is done to analyse the finer aspects of the investment using sophisticated capital

budgeting methods. Capital budgeting is a term that encompasses two important decisions: an

investment decision and the financial decision that goes along with it. Acceptance of the

investment means that the company will commit itself financially to the initiative on an

arbitrary basis, including risk and uncertainty. Project delays, cost overruns, and legal

restrictions can result in total costs being suspended or increased. In addition, companies

choose to invest in their future (in terms of direction, growth and expansion). This can have

an impact on future projects that companies are investigating and evaluating.

REFERENCES

Books and Journals

Gottlieb, U., Hansson, H. and Johed, G., 2021. Institutionalised management accounting and

control in farm businesses. Scandinavian Journal of Management. 37(2). p.101153.

Amoako, G.K. and et. al., 2021. Institutional isomorphism, environmental management

accounting and environmental accountability: a review. Environment, Development

and Sustainability. pp.1-16.

de Lautour, V.J., 2019. Historical Perspectives on Strategy, Ethics and Management

Accounting. In Strategic Management Accounting, Volume III. (pp. 1-50). Palgrave

Macmillan, Cham.

Nsor-Ambala, R., 2020. Impact of exam type on exam scores, anxiety, and knowledge

retention in a cost and management accounting course. Accounting Education. 29(1).

pp.32-56.

Cowton, C.J., 2018. Management Accounting and New Information Technology.

In Management Information Systems. (pp. 115-126). Routledge.

an impact on future projects that companies are investigating and evaluating.

REFERENCES

Books and Journals

Gottlieb, U., Hansson, H. and Johed, G., 2021. Institutionalised management accounting and

control in farm businesses. Scandinavian Journal of Management. 37(2). p.101153.

Amoako, G.K. and et. al., 2021. Institutional isomorphism, environmental management

accounting and environmental accountability: a review. Environment, Development

and Sustainability. pp.1-16.

de Lautour, V.J., 2019. Historical Perspectives on Strategy, Ethics and Management

Accounting. In Strategic Management Accounting, Volume III. (pp. 1-50). Palgrave

Macmillan, Cham.

Nsor-Ambala, R., 2020. Impact of exam type on exam scores, anxiety, and knowledge

retention in a cost and management accounting course. Accounting Education. 29(1).

pp.32-56.

Cowton, C.J., 2018. Management Accounting and New Information Technology.

In Management Information Systems. (pp. 115-126). Routledge.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.