Financial Performance Analysis of Trainline: 2013-2016 and Beyond

VerifiedAdded on 2020/01/23

|14

|3975

|204

Report

AI Summary

This report presents a comprehensive financial analysis of Trainline, a small to medium-sized enterprise (SME) operating in the railway ticket distribution and services sector. The analysis begins with a critical evaluation of Trainline's performance from 2013 to 2016, employing ratio analysis to assess profitability, liquidity, efficiency, and solvency. The report then constructs a projected cash budget for the period of 2017 to 2019, providing insights into the company's future financial health. It further examines the sources of finance available to Trainline, specifically focusing on the statement of financial position (SOFP) and techniques for evaluating investment proposals. Additionally, the report discusses the role of the entrepreneurial ecosystem in Trainline's development. Finally, it delves into the ethical considerations crucial for the issuance of an Initial Public Offering (IPO). The report concludes with a synthesis of the findings, emphasizing key financial trends and strategic recommendations for Trainline.

FINANCE IN SME

CONTEXT

CONTEXT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Q1. Critical analysis of Trainline’s performance over 2013-2016 using ratio analysis..............3

QUESTION 2..................................................................................................................................7

Preparing estimated cash budget for TrainLine for the period of 2017 to 2019..........................7

QUESTION 3..................................................................................................................................9

Critically evaluate the sources of finance in SOFP and techniques to evaluate investment

proposal........................................................................................................................................9

QUESTION 4................................................................................................................................11

Discuss the extent to which the entrepreneurial ecosystem has been responsible for the

development of Trainline...........................................................................................................11

QUESTION 5................................................................................................................................11

Critical discussion of ethical consideration that must be taken into account for IPO issuance.11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

Q1. Critical analysis of Trainline’s performance over 2013-2016 using ratio analysis..............3

QUESTION 2..................................................................................................................................7

Preparing estimated cash budget for TrainLine for the period of 2017 to 2019..........................7

QUESTION 3..................................................................................................................................9

Critically evaluate the sources of finance in SOFP and techniques to evaluate investment

proposal........................................................................................................................................9

QUESTION 4................................................................................................................................11

Discuss the extent to which the entrepreneurial ecosystem has been responsible for the

development of Trainline...........................................................................................................11

QUESTION 5................................................................................................................................11

Critical discussion of ethical consideration that must be taken into account for IPO issuance.11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

As per European definition, Small and medium sized enterprise has been defined as a

corporation who employ less than 250 person and whose total turnover did not exceed the

maximum level of 50 million Euro. They play an important role in the growth of the economy as

they contribute towards the GDP, generate employment and satisfy consumer need. In order to

execute their day-to-day functions, SMEs require funds and utilize it in an efficient manner for

effective and proper financial management. Trainline is a small business unit that deliver various

services i.e. railway ticket, distribution and other ancillary facilities to the consumers. The

proposed report here emphasizes upon the performance evaluation and financial status analysis

of Trainline. Moreover, it will also looks upon variety of financial sources and discuss the ethical

consideration that firm needs to taken into consideration at the time of IPO issue.

Q1. Critical analysis of Trainline’s performance over 2013-2016 using ratio analysis

Ratio analysis is a great technique that is often used by number of financial managers to

evaluate and analyse the success of business operations and financial position at the end of the

period. There are number of ratios that are categorized into profitability, efficiency, liquidity &

solvency as well. With the given scenario, Trainline’s performance is analysed underneath:

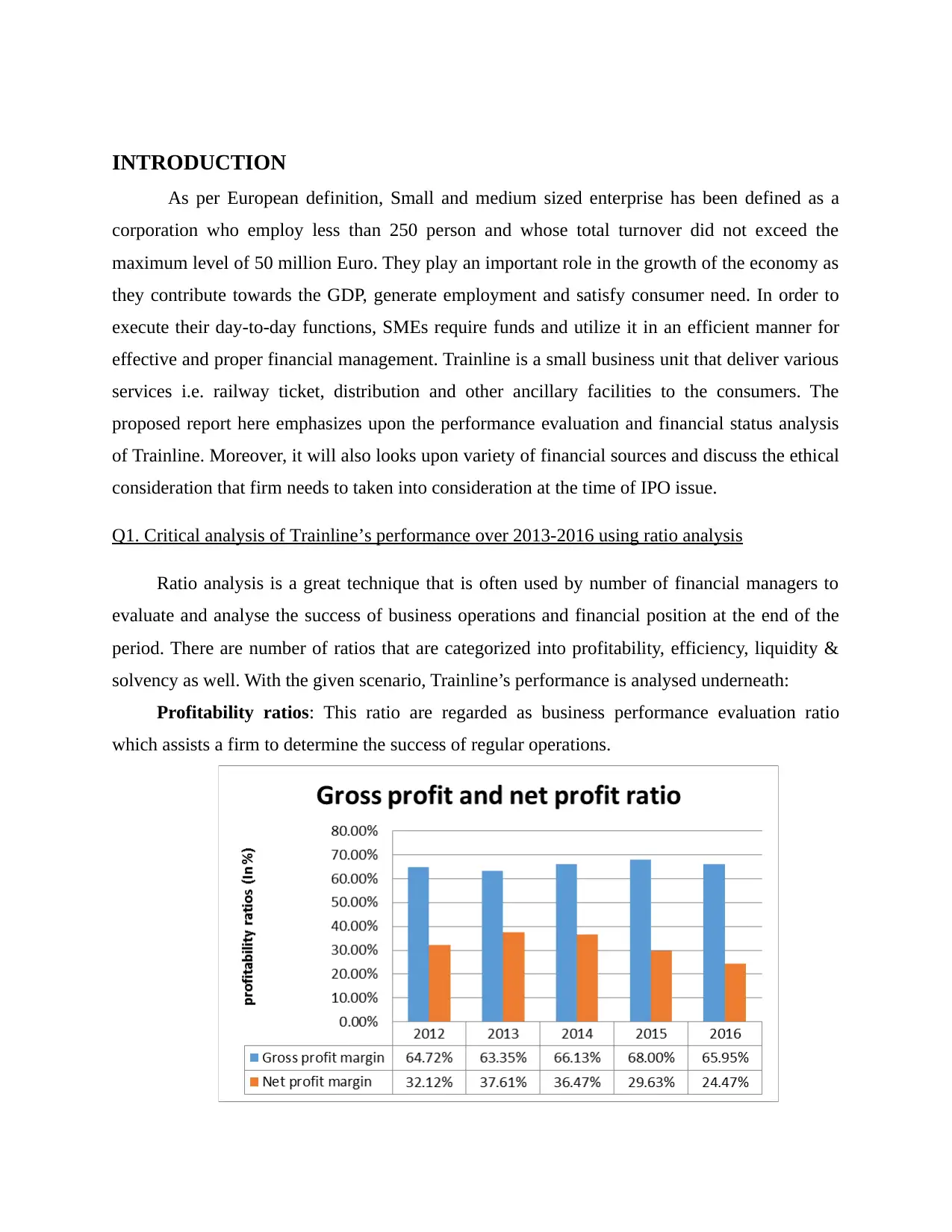

Profitability ratios: This ratio are regarded as business performance evaluation ratio

which assists a firm to determine the success of regular operations.

As per European definition, Small and medium sized enterprise has been defined as a

corporation who employ less than 250 person and whose total turnover did not exceed the

maximum level of 50 million Euro. They play an important role in the growth of the economy as

they contribute towards the GDP, generate employment and satisfy consumer need. In order to

execute their day-to-day functions, SMEs require funds and utilize it in an efficient manner for

effective and proper financial management. Trainline is a small business unit that deliver various

services i.e. railway ticket, distribution and other ancillary facilities to the consumers. The

proposed report here emphasizes upon the performance evaluation and financial status analysis

of Trainline. Moreover, it will also looks upon variety of financial sources and discuss the ethical

consideration that firm needs to taken into consideration at the time of IPO issue.

Q1. Critical analysis of Trainline’s performance over 2013-2016 using ratio analysis

Ratio analysis is a great technique that is often used by number of financial managers to

evaluate and analyse the success of business operations and financial position at the end of the

period. There are number of ratios that are categorized into profitability, efficiency, liquidity &

solvency as well. With the given scenario, Trainline’s performance is analysed underneath:

Profitability ratios: This ratio are regarded as business performance evaluation ratio

which assists a firm to determine the success of regular operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gross profit margin(GPM): It is used to examine that whether Trainline has

generated good return on sales by mark-up or not. In 2015, it goes to the highest level of

68% which was 64.72% in 2012 and after came down to 65.95% in 2015. Decreased GM

is a poor sign because of sudden and drastic increase in cost by 21.72%, whilst, turnover

gone up by 14.39% because Trainline acquired Captain Train which is a leading ticket

retailing firm. Therefore, managers must pay focus in this area and make right pricing

mechanism and rationalized cost measures to maximize GPM (Najjar, 2013).

Net profit margin (NPM): In 2013, it gone up to 37.61%, thereafter, it reflects a

continuous downward trend to 24.47% in 2016. High administrative cost is the most

important reason behind this because in 2016, YOY growth in it was founded to 29.19%.

Further, interest revenues of the firm also declined by 43.45% in 2015 and after, it gone up

by 15.43% in 2016. Less ratio is a sign that Trainline’s profitability performance came

down which arise the need of rationalized cost measures needs to be taken for profit

maximization (Ahmed and Manab, 2016).

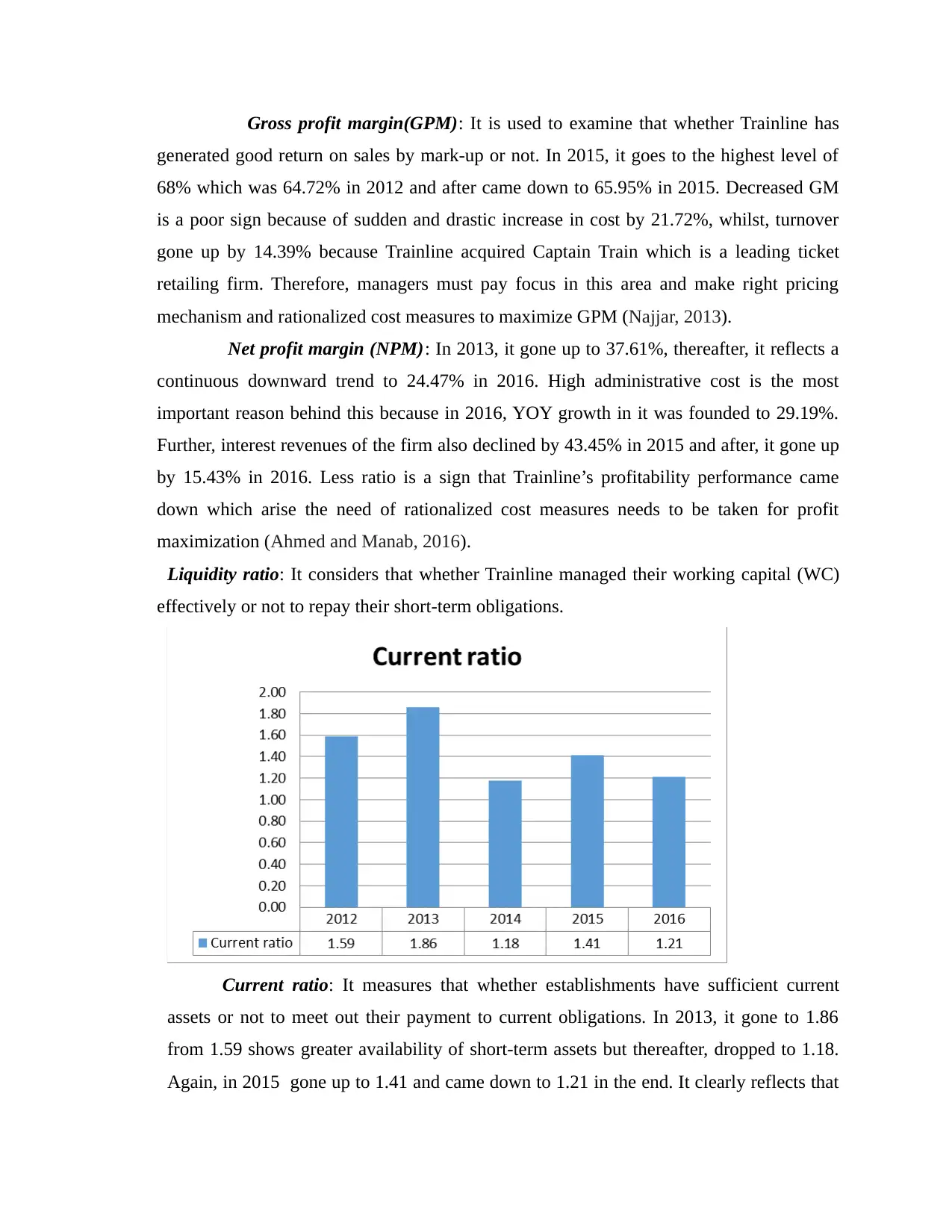

Liquidity ratio: It considers that whether Trainline managed their working capital (WC)

effectively or not to repay their short-term obligations.

Current ratio: It measures that whether establishments have sufficient current

assets or not to meet out their payment to current obligations. In 2013, it gone to 1.86

from 1.59 shows greater availability of short-term assets but thereafter, dropped to 1.18.

Again, in 2015 gone up to 1.41 and came down to 1.21 in the end. It clearly reflects that

generated good return on sales by mark-up or not. In 2015, it goes to the highest level of

68% which was 64.72% in 2012 and after came down to 65.95% in 2015. Decreased GM

is a poor sign because of sudden and drastic increase in cost by 21.72%, whilst, turnover

gone up by 14.39% because Trainline acquired Captain Train which is a leading ticket

retailing firm. Therefore, managers must pay focus in this area and make right pricing

mechanism and rationalized cost measures to maximize GPM (Najjar, 2013).

Net profit margin (NPM): In 2013, it gone up to 37.61%, thereafter, it reflects a

continuous downward trend to 24.47% in 2016. High administrative cost is the most

important reason behind this because in 2016, YOY growth in it was founded to 29.19%.

Further, interest revenues of the firm also declined by 43.45% in 2015 and after, it gone up

by 15.43% in 2016. Less ratio is a sign that Trainline’s profitability performance came

down which arise the need of rationalized cost measures needs to be taken for profit

maximization (Ahmed and Manab, 2016).

Liquidity ratio: It considers that whether Trainline managed their working capital (WC)

effectively or not to repay their short-term obligations.

Current ratio: It measures that whether establishments have sufficient current

assets or not to meet out their payment to current obligations. In 2013, it gone to 1.86

from 1.59 shows greater availability of short-term assets but thereafter, dropped to 1.18.

Again, in 2015 gone up to 1.41 and came down to 1.21 in the end. It clearly reflects that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trainline do not have enough assets i.e. inventory, cash & its equivalent & receivables to

make their deferral payments on time (Lartey, Antwi and Boadi, 2013). Henceforth, WC

strategies and cash management plans needs to be devised by the firm.

Efficiency ratios: This ratios are helpful to examine that firm has significantly

utilized their resources or not to generate high revenues.

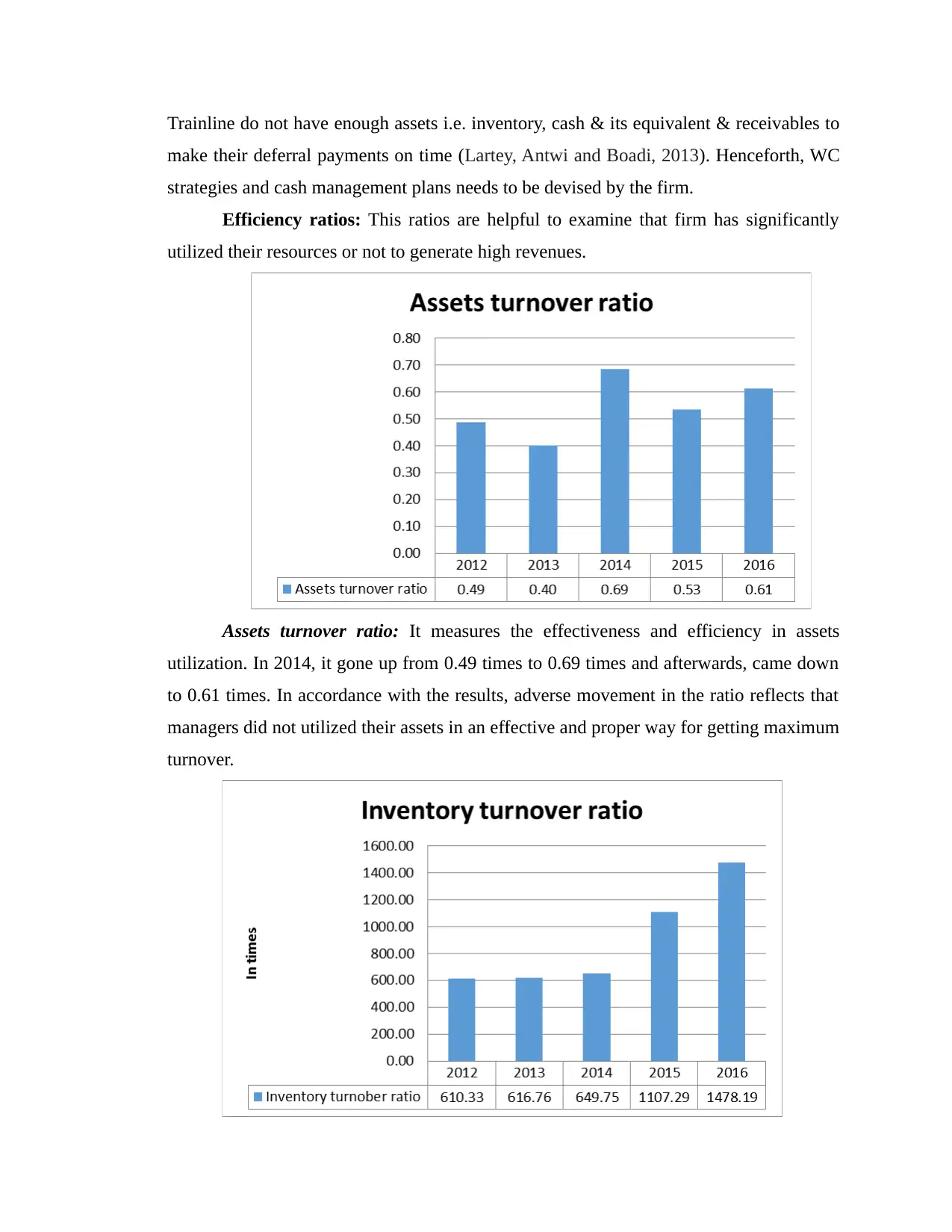

Assets turnover ratio: It measures the effectiveness and efficiency in assets

utilization. In 2014, it gone up from 0.49 times to 0.69 times and afterwards, came down

to 0.61 times. In accordance with the results, adverse movement in the ratio reflects that

managers did not utilized their assets in an effective and proper way for getting maximum

turnover.

make their deferral payments on time (Lartey, Antwi and Boadi, 2013). Henceforth, WC

strategies and cash management plans needs to be devised by the firm.

Efficiency ratios: This ratios are helpful to examine that firm has significantly

utilized their resources or not to generate high revenues.

Assets turnover ratio: It measures the effectiveness and efficiency in assets

utilization. In 2014, it gone up from 0.49 times to 0.69 times and afterwards, came down

to 0.61 times. In accordance with the results, adverse movement in the ratio reflects that

managers did not utilized their assets in an effective and proper way for getting maximum

turnover.

Inventory turnover ratio: Unlike above, this ratio only measures the efficiency of

the business to perfectly utilize their stock or inventory balance. Above graph clearly

reflects the consistent upward trend as it got improved from 610.33 to 1478.19 which

depicts that inventory utilization efficiency of the Trainline has been maximized. It

clearly shows quick conversion or transformation of goods into sales to get higher

turnover (Islam, Alam and Hossain, 2014).

Solvency position: It is directly related to the long-term financial position which

examine the capital structure decisions to repay long-term obligations of the business on correct

time.

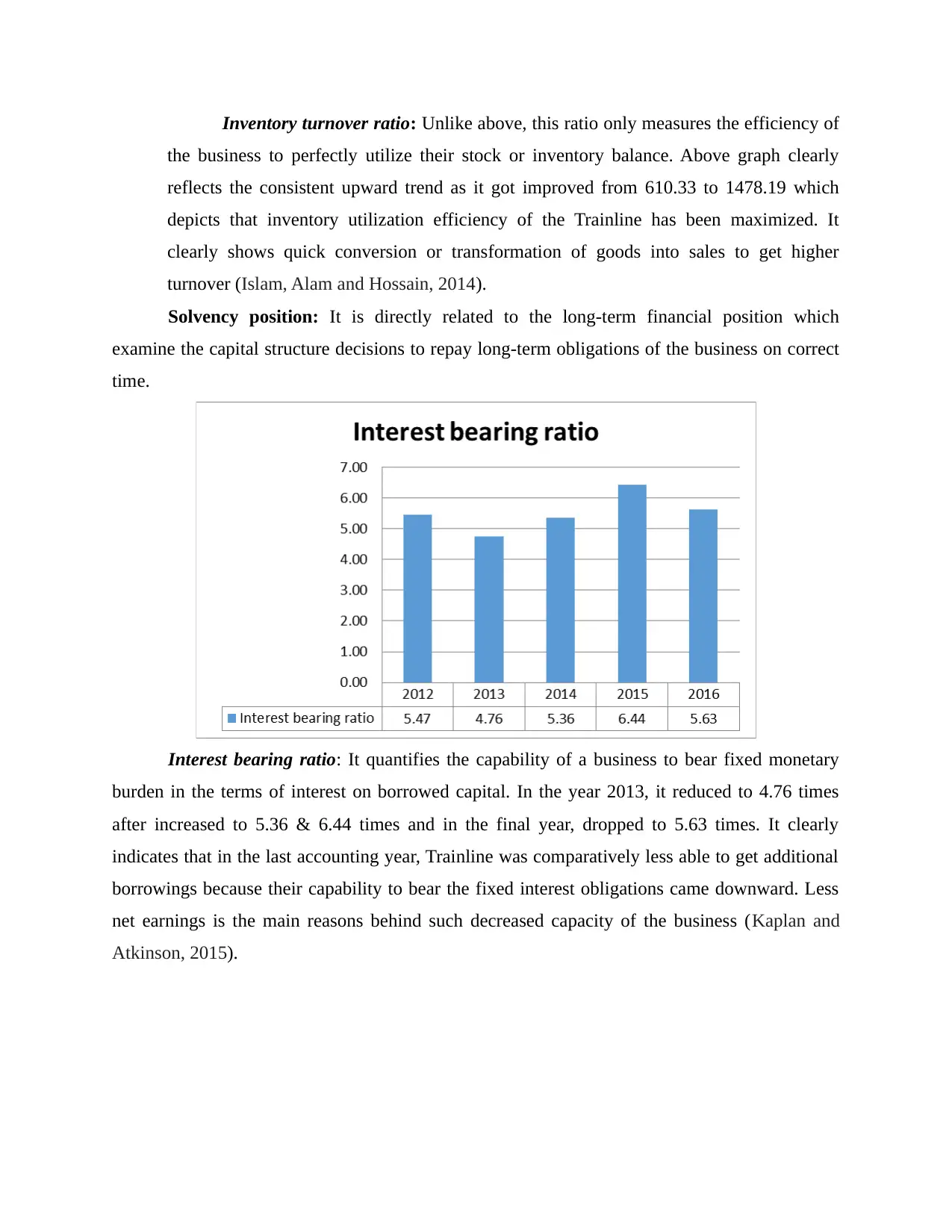

Interest bearing ratio: It quantifies the capability of a business to bear fixed monetary

burden in the terms of interest on borrowed capital. In the year 2013, it reduced to 4.76 times

after increased to 5.36 & 6.44 times and in the final year, dropped to 5.63 times. It clearly

indicates that in the last accounting year, Trainline was comparatively less able to get additional

borrowings because their capability to bear the fixed interest obligations came downward. Less

net earnings is the main reasons behind such decreased capacity of the business (Kaplan and

Atkinson, 2015).

the business to perfectly utilize their stock or inventory balance. Above graph clearly

reflects the consistent upward trend as it got improved from 610.33 to 1478.19 which

depicts that inventory utilization efficiency of the Trainline has been maximized. It

clearly shows quick conversion or transformation of goods into sales to get higher

turnover (Islam, Alam and Hossain, 2014).

Solvency position: It is directly related to the long-term financial position which

examine the capital structure decisions to repay long-term obligations of the business on correct

time.

Interest bearing ratio: It quantifies the capability of a business to bear fixed monetary

burden in the terms of interest on borrowed capital. In the year 2013, it reduced to 4.76 times

after increased to 5.36 & 6.44 times and in the final year, dropped to 5.63 times. It clearly

indicates that in the last accounting year, Trainline was comparatively less able to get additional

borrowings because their capability to bear the fixed interest obligations came downward. Less

net earnings is the main reasons behind such decreased capacity of the business (Kaplan and

Atkinson, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 2

Preparing estimated cash budget for TrainLine for the period of 2017 to 2019

Cash budget is the statement which helps to the firm in order to determine and assess

future financial data by taking base to the past financial years. When past financial performance

of the business entity has increasing trend then in the future also it will grow. The respective

statement of assessing financial performance includes mainly two headings such as incomes as

well as outcomes. By comparing both the aspects management is able to know that there is a

situation of cash deficit or surplus in the firm (Trejos and Wright, 2016). When net cash balance

at the end of year then it shows that TrainLine is able to manage expenses to increase profit. On

the other side, when cash incomes are lower as compare to disposals then TrainLine is unable to

perform well in the overall industry. Further, in accordance to financial performance of

TrainLine from the fiscal year 2013-2016 cash budget is to be prepared for further accounting

period. Projected or estimated cash budget over the period from 2017 to 2019 for the TrainLine

is stated as below:

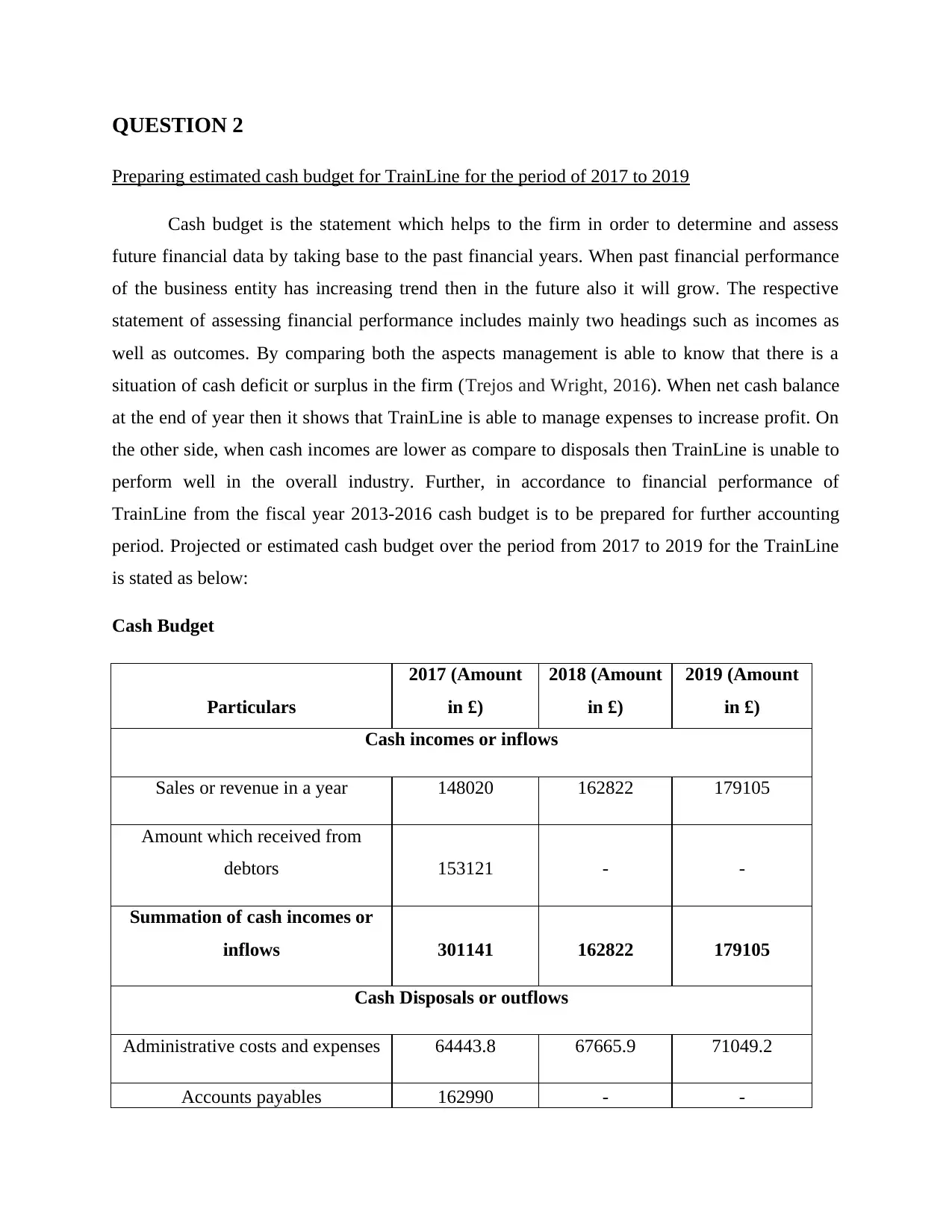

Cash Budget

Particulars

2017 (Amount

in £)

2018 (Amount

in £)

2019 (Amount

in £)

Cash incomes or inflows

Sales or revenue in a year 148020 162822 179105

Amount which received from

debtors 153121 - -

Summation of cash incomes or

inflows 301141 162822 179105

Cash Disposals or outflows

Administrative costs and expenses 64443.8 67665.9 71049.2

Accounts payables 162990 - -

Preparing estimated cash budget for TrainLine for the period of 2017 to 2019

Cash budget is the statement which helps to the firm in order to determine and assess

future financial data by taking base to the past financial years. When past financial performance

of the business entity has increasing trend then in the future also it will grow. The respective

statement of assessing financial performance includes mainly two headings such as incomes as

well as outcomes. By comparing both the aspects management is able to know that there is a

situation of cash deficit or surplus in the firm (Trejos and Wright, 2016). When net cash balance

at the end of year then it shows that TrainLine is able to manage expenses to increase profit. On

the other side, when cash incomes are lower as compare to disposals then TrainLine is unable to

perform well in the overall industry. Further, in accordance to financial performance of

TrainLine from the fiscal year 2013-2016 cash budget is to be prepared for further accounting

period. Projected or estimated cash budget over the period from 2017 to 2019 for the TrainLine

is stated as below:

Cash Budget

Particulars

2017 (Amount

in £)

2018 (Amount

in £)

2019 (Amount

in £)

Cash incomes or inflows

Sales or revenue in a year 148020 162822 179105

Amount which received from

debtors 153121 - -

Summation of cash incomes or

inflows 301141 162822 179105

Cash Disposals or outflows

Administrative costs and expenses 64443.8 67665.9 71049.2

Accounts payables 162990 - -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Summation of cash disposals or

outflows 227434 67665.9 71049.2

Net cash balance (deficit /

surplus) 73707.7 95156.5 108055

Add: Cash balance at the

beginning of the year 44408 118116 213272

Cash balance at the end of year 118116 213272 321328

Interpretation

From the above mentioned table of cash budget it can be interpreted that sales of the

TrainLine increases by 10% at every year which shows that company is able to sale more

number of rail tickets. On the other side expenses of the TrainLine are also raised in same

accounting period but with the 5% rate only. Hence, it clearly indicates that level of expenses

and revenue both will increase in the future years but with the lower and higher growth rate. It is

a clear indication of growing the TrainLine in the industry where it exists and operates currently

(Damodaran, 2016). It can be depicted from the cash budget that revenue of the TrainLine are

increases over the year which are worth of £148020, £162822 and £179105 in the FY 2017, 2018

and 2019 respectively. On the other hand side when talking about expenditures then its level also

enhance which is worth of £227434, £6766.5 and £71049.2 for the same periods. It can be

analysed that total expenses are lower as compare to total incomes which is the most profitable

situation for the company like as TrainLine.

In addition to this, net cash balance at the end of every year is positive and having

increasing trend which shows that performance of TrainLine will be better in the future. On the

basis of above table it can be clearly visualized that TrainLine will generate return or net cash

balance in the year 2017 worth of £73707.7 which is better and shows that management has

effective control on the expenses (Cash Budget, 2013). Further, in the next year i.e. 2018 cash

outflows 227434 67665.9 71049.2

Net cash balance (deficit /

surplus) 73707.7 95156.5 108055

Add: Cash balance at the

beginning of the year 44408 118116 213272

Cash balance at the end of year 118116 213272 321328

Interpretation

From the above mentioned table of cash budget it can be interpreted that sales of the

TrainLine increases by 10% at every year which shows that company is able to sale more

number of rail tickets. On the other side expenses of the TrainLine are also raised in same

accounting period but with the 5% rate only. Hence, it clearly indicates that level of expenses

and revenue both will increase in the future years but with the lower and higher growth rate. It is

a clear indication of growing the TrainLine in the industry where it exists and operates currently

(Damodaran, 2016). It can be depicted from the cash budget that revenue of the TrainLine are

increases over the year which are worth of £148020, £162822 and £179105 in the FY 2017, 2018

and 2019 respectively. On the other hand side when talking about expenditures then its level also

enhance which is worth of £227434, £6766.5 and £71049.2 for the same periods. It can be

analysed that total expenses are lower as compare to total incomes which is the most profitable

situation for the company like as TrainLine.

In addition to this, net cash balance at the end of every year is positive and having

increasing trend which shows that performance of TrainLine will be better in the future. On the

basis of above table it can be clearly visualized that TrainLine will generate return or net cash

balance in the year 2017 worth of £73707.7 which is better and shows that management has

effective control on the expenses (Cash Budget, 2013). Further, in the next year i.e. 2018 cash

balance increases and reaches up to £95156.5 due to having effectual strategies to attract

customers for purchasing rail tickets sell by it. It can be forecasted from the respective cash

budget that TrainLine’s cash balance will be enhance from £95156.5 to £108055 which describes

that selling of train tickets will be increase up to greater level. Overall it can be said that the

company TrainLine’s performance will be profitable and increasing trend in the every FY from

2017 to 2019.

QUESTION 3

Critically evaluate the sources of finance in SOFP and techniques to evaluate investment

proposal

With the stated case scenario, it can be seen that in the year 2012, it can be seen that in

the year 2012, Trainline’s total equity capital & reserve was 95,715, out of which, total share

capital was reported to 35882, share premium reserve was 44,249 and retained profits were

15,584. However, there was no debt taken by Trainline to meet out their financial need. It may be

because of high cost of debt, instability in corporate earnings, volatile market demand etc.

Thereafter, in 2013, it goes upward to 135,585 because of higher retained profits worth 55,454.

Afterwards, it shows a huge decline in the total equity as it came to 41967, 76821 and 56158

respectively because repayment of capital to the investors out of the share premium reserve.

Trainline’s capital structure consists of only the equity capital may be due to high cost of

borrowings on debt capital.

This structure of the firm cannot be considered efficient because firm did not incorporate

debt funds in the business and financed only through equity capital. Undoubtedly, debt brings

fixed financial burden to the entity by charging a fixed rate of interest, but still, it brings wide

range of benefits also. One of the most important benefit that debt capital provides is taxation

benefits. Trainline can utilize debt funds and get taxation advantages on the interest payment

made periodically accordance with the debt covenants (Bhowmik and Saha, 2013). In UK,

taxation regulatory body, HMRC (Her Majesty Revenue & Custom) give taxation relief to the

Trainline on the interest charged which minimizes taxation payment and drive larger return.

Another benefit associated with the borrowed capital is it does not transfer any controlling right

to the lenders & financial institutions, as a result, business control can be secured in the owner’s

customers for purchasing rail tickets sell by it. It can be forecasted from the respective cash

budget that TrainLine’s cash balance will be enhance from £95156.5 to £108055 which describes

that selling of train tickets will be increase up to greater level. Overall it can be said that the

company TrainLine’s performance will be profitable and increasing trend in the every FY from

2017 to 2019.

QUESTION 3

Critically evaluate the sources of finance in SOFP and techniques to evaluate investment

proposal

With the stated case scenario, it can be seen that in the year 2012, it can be seen that in

the year 2012, Trainline’s total equity capital & reserve was 95,715, out of which, total share

capital was reported to 35882, share premium reserve was 44,249 and retained profits were

15,584. However, there was no debt taken by Trainline to meet out their financial need. It may be

because of high cost of debt, instability in corporate earnings, volatile market demand etc.

Thereafter, in 2013, it goes upward to 135,585 because of higher retained profits worth 55,454.

Afterwards, it shows a huge decline in the total equity as it came to 41967, 76821 and 56158

respectively because repayment of capital to the investors out of the share premium reserve.

Trainline’s capital structure consists of only the equity capital may be due to high cost of

borrowings on debt capital.

This structure of the firm cannot be considered efficient because firm did not incorporate

debt funds in the business and financed only through equity capital. Undoubtedly, debt brings

fixed financial burden to the entity by charging a fixed rate of interest, but still, it brings wide

range of benefits also. One of the most important benefit that debt capital provides is taxation

benefits. Trainline can utilize debt funds and get taxation advantages on the interest payment

made periodically accordance with the debt covenants (Bhowmik and Saha, 2013). In UK,

taxation regulatory body, HMRC (Her Majesty Revenue & Custom) give taxation relief to the

Trainline on the interest charged which minimizes taxation payment and drive larger return.

Another benefit associated with the borrowed capital is it does not transfer any controlling right

to the lenders & financial institutions, as a result, business control can be secured in the owner’s

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

hand without any dilution. In this way, they can devise plans, formulate corporate strategies and

expansion strategies by their own, In contrast, equity capital did not require fixed payment of

dividend, still, there are no taxation benefits associated and at the same time, investors are

invited in the board meetings, hence, their voting power can alter the decisions.

In business planning, many times, companies have to invest money in long-term financial

projects. In accordance with the given scenario, managers are interested in investing money in a

new project, but they are concerned regarding its viability. It can be easily tested by applying

capital budgeting tools and techniques. In the earlier times, investors were risk-averse, therefore,

they desire to put money in such a project which will get back the initial investment quickly.

Payback period is the best way to identify the time duration in which initial investment can be

get back promptly (Baum and Crosby, 2014). However, as the method did not consider time

value, therefore, discounted payback period has been developed to overcome its drawback.

Again, it has been criticised because it ignores totally the post-pay back cash flows, therefore,

Trainline can use accounting rate of return to find out the actual profitability percentage that will

drive favourable profit to an entity. However, criticism of the method states that it did not

consider actual cash flows and use profit figures to determine the profit percentage.

However, now-a-days, net present value (NPV) gains superior priority among investors

because it discounts the expected cash inflows at a given rate and subtracts the total of it from the

initial outlay. High as well as positive NPV drive good return to the organization whereas

negative NPV shows enviable project (Götze, Northcott and Schuster, 2015). There is only one

criticism of it that is it use fixed cost of capital for whole the project life which is not considered

accurate & realistic in the dynamic corporate world. In addition, IRR (Internal rate of return) is

another method which reflects the cost of capital at where discounted cash inflows & beginning

cost outlay will be equal.

From the comparative evaluation, it becomes clear that Trainline must use NPV technique

to assess and evaluate project viability and adjust risk by considering the time-value.

expansion strategies by their own, In contrast, equity capital did not require fixed payment of

dividend, still, there are no taxation benefits associated and at the same time, investors are

invited in the board meetings, hence, their voting power can alter the decisions.

In business planning, many times, companies have to invest money in long-term financial

projects. In accordance with the given scenario, managers are interested in investing money in a

new project, but they are concerned regarding its viability. It can be easily tested by applying

capital budgeting tools and techniques. In the earlier times, investors were risk-averse, therefore,

they desire to put money in such a project which will get back the initial investment quickly.

Payback period is the best way to identify the time duration in which initial investment can be

get back promptly (Baum and Crosby, 2014). However, as the method did not consider time

value, therefore, discounted payback period has been developed to overcome its drawback.

Again, it has been criticised because it ignores totally the post-pay back cash flows, therefore,

Trainline can use accounting rate of return to find out the actual profitability percentage that will

drive favourable profit to an entity. However, criticism of the method states that it did not

consider actual cash flows and use profit figures to determine the profit percentage.

However, now-a-days, net present value (NPV) gains superior priority among investors

because it discounts the expected cash inflows at a given rate and subtracts the total of it from the

initial outlay. High as well as positive NPV drive good return to the organization whereas

negative NPV shows enviable project (Götze, Northcott and Schuster, 2015). There is only one

criticism of it that is it use fixed cost of capital for whole the project life which is not considered

accurate & realistic in the dynamic corporate world. In addition, IRR (Internal rate of return) is

another method which reflects the cost of capital at where discounted cash inflows & beginning

cost outlay will be equal.

From the comparative evaluation, it becomes clear that Trainline must use NPV technique

to assess and evaluate project viability and adjust risk by considering the time-value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 4

Discuss the extent to which the entrepreneurial ecosystem has been responsible for the

development of Trainline

Ecosystem has an integral and key role in every company which helps in business process

in terms of several financial aspects. In the current scenario the company such as TrainLine

which provides online rail tickets to the customers and going to expand firm. For expansion of

business it requires huge amount of money which is raised from various sources of finance.

Entrepreneurial ecosystem provides various financial supports and managing it in proper and

adequate manner to make it’s financial health very strong (Antras and Foley, 2015). The

respective system provides finance to the TrainLine through venture capitalists, angel investors

and other financing sources. Apart from this, the ecosystem of entrepreneurial has a main

characteristic that it helps to the management of company in order to tolerate failure and risks

occur at the workplace. When the firm is highly able to tolerate and manage risk in better way

then it becomes profitable which is one part of ecosystem.

The overall entrepreneurial ecosystem is based on the regulatory and authority body

which is government of the country. The government formulates different rules and regulations

as well as laws for operating in the industry. When the TrainLine will employ such laws then it

able to provide better services to the customers. Being a service industry’s business organisation

it needs to provide higher quality of services by which it can attract more consumers (Ehrhardt

and Brigham, 2016) Hence, it can be said that with the help of better laws, rules and regulations

the management of TrainLine is highly able to increase level of sales and profit. Further,

ultimately the business will develop up to higher level in the overall segment.

QUESTION 5

Critical discussion of ethical consideration that must be taken into account for IPO issuance

Ethics are the necessary and key aspect of each and every business organisation which

helps to it in order to create better image in eyes of buyers as well as corporations. All the

entities take care of ethics at the workplace by which it can easily achieve objectives and targets.

When the firm is going to take any kind of decisions or making strategies then always takes into

Discuss the extent to which the entrepreneurial ecosystem has been responsible for the

development of Trainline

Ecosystem has an integral and key role in every company which helps in business process

in terms of several financial aspects. In the current scenario the company such as TrainLine

which provides online rail tickets to the customers and going to expand firm. For expansion of

business it requires huge amount of money which is raised from various sources of finance.

Entrepreneurial ecosystem provides various financial supports and managing it in proper and

adequate manner to make it’s financial health very strong (Antras and Foley, 2015). The

respective system provides finance to the TrainLine through venture capitalists, angel investors

and other financing sources. Apart from this, the ecosystem of entrepreneurial has a main

characteristic that it helps to the management of company in order to tolerate failure and risks

occur at the workplace. When the firm is highly able to tolerate and manage risk in better way

then it becomes profitable which is one part of ecosystem.

The overall entrepreneurial ecosystem is based on the regulatory and authority body

which is government of the country. The government formulates different rules and regulations

as well as laws for operating in the industry. When the TrainLine will employ such laws then it

able to provide better services to the customers. Being a service industry’s business organisation

it needs to provide higher quality of services by which it can attract more consumers (Ehrhardt

and Brigham, 2016) Hence, it can be said that with the help of better laws, rules and regulations

the management of TrainLine is highly able to increase level of sales and profit. Further,

ultimately the business will develop up to higher level in the overall segment.

QUESTION 5

Critical discussion of ethical consideration that must be taken into account for IPO issuance

Ethics are the necessary and key aspect of each and every business organisation which

helps to it in order to create better image in eyes of buyers as well as corporations. All the

entities take care of ethics at the workplace by which it can easily achieve objectives and targets.

When the firm is going to take any kind of decisions or making strategies then always takes into

consideration to the ethics. In context to such aspect, when TrainLine going to issue its shares

using Initial Public Offerings (IPO) then it has to take care various ethical consideration. When

the company go for IPO process then it needs to provide each and every kind of information

which is useful for the investors because it will be a parameter for taking investment decisions

for the shareholders (Fracassi, 2016). In order to this, the management of TrainLine should keep

in mind various ratios like as earning per share, price earning ratio etc. Because when the firm

has higher return, profit and such ratios then it can provide positive and better return to the

shareholders.

Apart from this, the TrainLine company has to show and provide a prospectus which

includes firm’s vision, financial performance, level of profitability etc. which helps to assist the

investors in order to invest money or not. When financial health of the TrainLine is higher and

strong then more number of shareholders attracts towards it. With help of financial performance

it able to know that company is how much able to generate profit at the end of an accounting

period. On the basis of this, potential investors are easily able to assess value of return by

considering level of profit. Base of assessing future return is profit because higher the yield leads

to provide more dividend amount to them. Moreover, while issuing shares through IPO the

management of TrainLine should provide all the terms and conditions regarding trading of shares

and return on the money which is invested in it. Furthermore, the TrainLine requires to appoint a

particular manager who is able to manage and regulate overall stock and shares in appropriate

way (Perkowski and Prömel, 2016). With this to all the investors are given equal and same

opportunities to each and every shareholders and investors. By considering such analysis of

ethical considerations it can be said that TrainLine needs to use such terms and aspects while

issuing share in stock market through IPO.

CONCLUSION

It can be articulated from the current project that, financial performance of the TrainLine

is not better in the industry and performing poor. Profitability as well as liquidity both the

aspects of financial are reduced which shows that it not able to generate better profit. Further, the

company should make strategies to attract customers and control over the expenses which are

incurred to produce services. On the basis of cash budget it can be depicted that in the future

using Initial Public Offerings (IPO) then it has to take care various ethical consideration. When

the company go for IPO process then it needs to provide each and every kind of information

which is useful for the investors because it will be a parameter for taking investment decisions

for the shareholders (Fracassi, 2016). In order to this, the management of TrainLine should keep

in mind various ratios like as earning per share, price earning ratio etc. Because when the firm

has higher return, profit and such ratios then it can provide positive and better return to the

shareholders.

Apart from this, the TrainLine company has to show and provide a prospectus which

includes firm’s vision, financial performance, level of profitability etc. which helps to assist the

investors in order to invest money or not. When financial health of the TrainLine is higher and

strong then more number of shareholders attracts towards it. With help of financial performance

it able to know that company is how much able to generate profit at the end of an accounting

period. On the basis of this, potential investors are easily able to assess value of return by

considering level of profit. Base of assessing future return is profit because higher the yield leads

to provide more dividend amount to them. Moreover, while issuing shares through IPO the

management of TrainLine should provide all the terms and conditions regarding trading of shares

and return on the money which is invested in it. Furthermore, the TrainLine requires to appoint a

particular manager who is able to manage and regulate overall stock and shares in appropriate

way (Perkowski and Prömel, 2016). With this to all the investors are given equal and same

opportunities to each and every shareholders and investors. By considering such analysis of

ethical considerations it can be said that TrainLine needs to use such terms and aspects while

issuing share in stock market through IPO.

CONCLUSION

It can be articulated from the current project that, financial performance of the TrainLine

is not better in the industry and performing poor. Profitability as well as liquidity both the

aspects of financial are reduced which shows that it not able to generate better profit. Further, the

company should make strategies to attract customers and control over the expenses which are

incurred to produce services. On the basis of cash budget it can be depicted that in the future

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.