Financial Analysis: Working Capital Management of Kathmandu Holdings

VerifiedAdded on 2020/01/06

|9

|2114

|307

Report

AI Summary

This report examines working capital management practices at Kathmandu Holdings Ltd. (KMD), comparing its performance to Oroton Group Ltd (ORL). It analyzes the cash conversion cycle (CCC), including Days Inventory Outstanding (DIO), Days Sales Outstanding (DSO), and Days Payable Outstanding (DPO), to assess KMD's efficiency in converting resources into cash. The report also evaluates risk and return, calculating monthly returns, capital gains, average monthly returns, standard deviation, and beta value for KMD and the S&P/ASX index. It identifies systematic and unsystematic risks, including interest rate risk, market risk, and liquidity risk, and assesses the impact of market return fluctuations on expected returns. The conclusion emphasizes the importance of optimizing the CCC and managing various financial risks to maximize cash position and investor returns.

Working capital management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

Working capital management..........................................................................................................3

TASK 2.................................................................................................................................................5

Risk and return.................................................................................................................................5

CONCLUSION....................................................................................................................................7

REFERENCES.....................................................................................................................................8

2

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

Working capital management..........................................................................................................3

TASK 2.................................................................................................................................................5

Risk and return.................................................................................................................................5

CONCLUSION....................................................................................................................................7

REFERENCES.....................................................................................................................................8

2

INTRODUCTION

Every commercial establishment whether small or large size needs to assure sufficient amount

of funds to meet their daily operational need, called as working capital. It is important because

without having proper money, they cannot run their routine functioning such as buying material and

payment of salary, bills, accounts payable, rent, rates and taxes etc. The present report lay

emphasize on the different ways of managing working capital in Kathmandu Holding Ltd. (KMD).

Moreover, it will be analysed with its competitor, Oroton Group Ltd (ORL). Effective and efficient

management of WC is a sign of strengthen short-term ability of the company to pay timely to their

current liabilities.

TASK 1

Working capital management

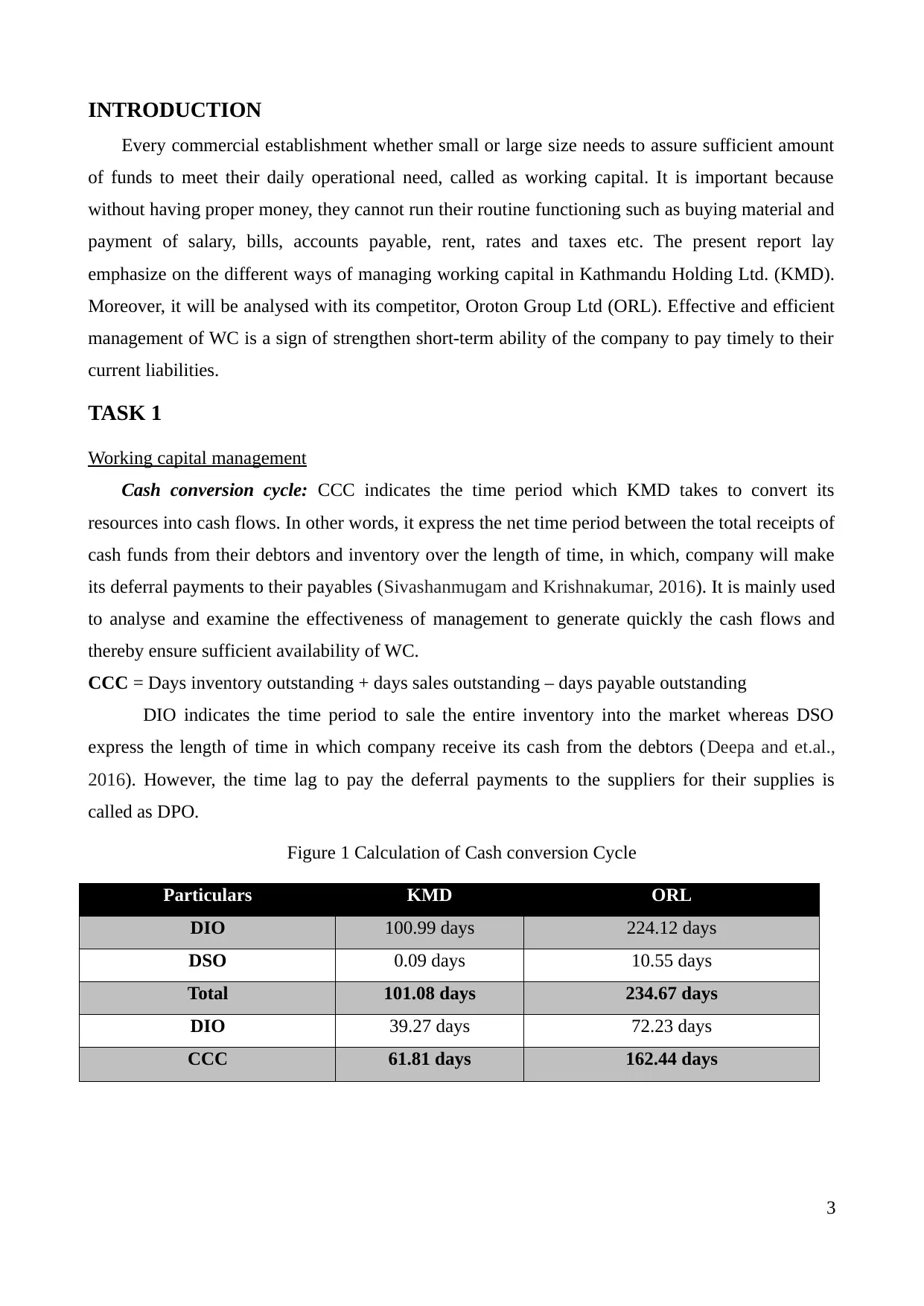

Cash conversion cycle: CCC indicates the time period which KMD takes to convert its

resources into cash flows. In other words, it express the net time period between the total receipts of

cash funds from their debtors and inventory over the length of time, in which, company will make

its deferral payments to their payables (Sivashanmugam and Krishnakumar, 2016). It is mainly used

to analyse and examine the effectiveness of management to generate quickly the cash flows and

thereby ensure sufficient availability of WC.

CCC = Days inventory outstanding + days sales outstanding – days payable outstanding

DIO indicates the time period to sale the entire inventory into the market whereas DSO

express the length of time in which company receive its cash from the debtors (Deepa and et.al.,

2016). However, the time lag to pay the deferral payments to the suppliers for their supplies is

called as DPO.

Figure 1 Calculation of Cash conversion Cycle

Particulars KMD ORL

DIO 100.99 days 224.12 days

DSO 0.09 days 10.55 days

Total 101.08 days 234.67 days

DIO 39.27 days 72.23 days

CCC 61.81 days 162.44 days

3

Every commercial establishment whether small or large size needs to assure sufficient amount

of funds to meet their daily operational need, called as working capital. It is important because

without having proper money, they cannot run their routine functioning such as buying material and

payment of salary, bills, accounts payable, rent, rates and taxes etc. The present report lay

emphasize on the different ways of managing working capital in Kathmandu Holding Ltd. (KMD).

Moreover, it will be analysed with its competitor, Oroton Group Ltd (ORL). Effective and efficient

management of WC is a sign of strengthen short-term ability of the company to pay timely to their

current liabilities.

TASK 1

Working capital management

Cash conversion cycle: CCC indicates the time period which KMD takes to convert its

resources into cash flows. In other words, it express the net time period between the total receipts of

cash funds from their debtors and inventory over the length of time, in which, company will make

its deferral payments to their payables (Sivashanmugam and Krishnakumar, 2016). It is mainly used

to analyse and examine the effectiveness of management to generate quickly the cash flows and

thereby ensure sufficient availability of WC.

CCC = Days inventory outstanding + days sales outstanding – days payable outstanding

DIO indicates the time period to sale the entire inventory into the market whereas DSO

express the length of time in which company receive its cash from the debtors (Deepa and et.al.,

2016). However, the time lag to pay the deferral payments to the suppliers for their supplies is

called as DPO.

Figure 1 Calculation of Cash conversion Cycle

Particulars KMD ORL

DIO 100.99 days 224.12 days

DSO 0.09 days 10.55 days

Total 101.08 days 234.67 days

DIO 39.27 days 72.23 days

CCC 61.81 days 162.44 days

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

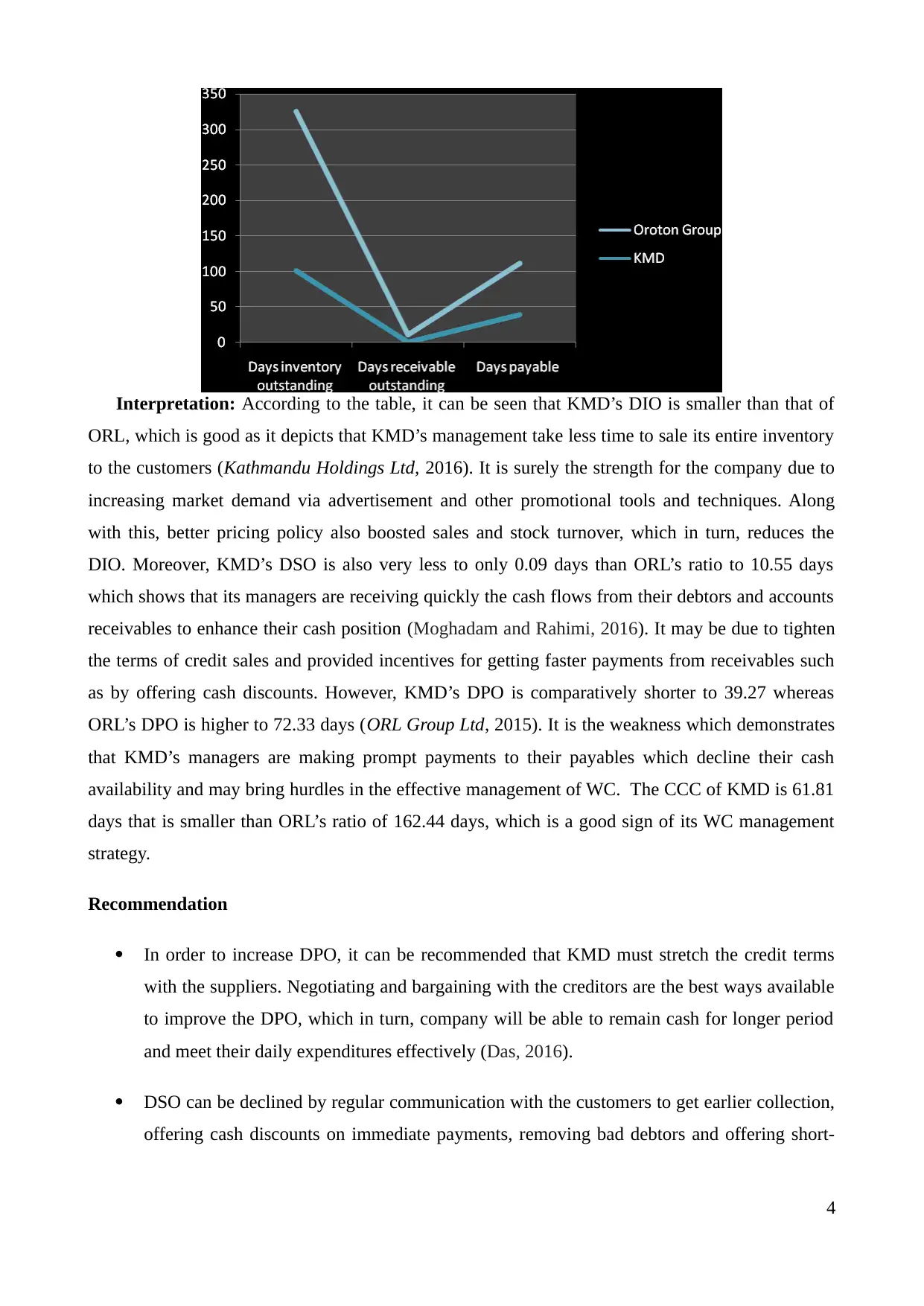

Interpretation: According to the table, it can be seen that KMD’s DIO is smaller than that of

ORL, which is good as it depicts that KMD’s management take less time to sale its entire inventory

to the customers (Kathmandu Holdings Ltd, 2016). It is surely the strength for the company due to

increasing market demand via advertisement and other promotional tools and techniques. Along

with this, better pricing policy also boosted sales and stock turnover, which in turn, reduces the

DIO. Moreover, KMD’s DSO is also very less to only 0.09 days than ORL’s ratio to 10.55 days

which shows that its managers are receiving quickly the cash flows from their debtors and accounts

receivables to enhance their cash position (Moghadam and Rahimi, 2016). It may be due to tighten

the terms of credit sales and provided incentives for getting faster payments from receivables such

as by offering cash discounts. However, KMD’s DPO is comparatively shorter to 39.27 whereas

ORL’s DPO is higher to 72.33 days (ORL Group Ltd, 2015). It is the weakness which demonstrates

that KMD’s managers are making prompt payments to their payables which decline their cash

availability and may bring hurdles in the effective management of WC. The CCC of KMD is 61.81

days that is smaller than ORL’s ratio of 162.44 days, which is a good sign of its WC management

strategy.

Recommendation

In order to increase DPO, it can be recommended that KMD must stretch the credit terms

with the suppliers. Negotiating and bargaining with the creditors are the best ways available

to improve the DPO, which in turn, company will be able to remain cash for longer period

and meet their daily expenditures effectively (Das, 2016).

DSO can be declined by regular communication with the customers to get earlier collection,

offering cash discounts on immediate payments, removing bad debtors and offering short-

4

ORL, which is good as it depicts that KMD’s management take less time to sale its entire inventory

to the customers (Kathmandu Holdings Ltd, 2016). It is surely the strength for the company due to

increasing market demand via advertisement and other promotional tools and techniques. Along

with this, better pricing policy also boosted sales and stock turnover, which in turn, reduces the

DIO. Moreover, KMD’s DSO is also very less to only 0.09 days than ORL’s ratio to 10.55 days

which shows that its managers are receiving quickly the cash flows from their debtors and accounts

receivables to enhance their cash position (Moghadam and Rahimi, 2016). It may be due to tighten

the terms of credit sales and provided incentives for getting faster payments from receivables such

as by offering cash discounts. However, KMD’s DPO is comparatively shorter to 39.27 whereas

ORL’s DPO is higher to 72.33 days (ORL Group Ltd, 2015). It is the weakness which demonstrates

that KMD’s managers are making prompt payments to their payables which decline their cash

availability and may bring hurdles in the effective management of WC. The CCC of KMD is 61.81

days that is smaller than ORL’s ratio of 162.44 days, which is a good sign of its WC management

strategy.

Recommendation

In order to increase DPO, it can be recommended that KMD must stretch the credit terms

with the suppliers. Negotiating and bargaining with the creditors are the best ways available

to improve the DPO, which in turn, company will be able to remain cash for longer period

and meet their daily expenditures effectively (Das, 2016).

DSO can be declined by regular communication with the customers to get earlier collection,

offering cash discounts on immediate payments, removing bad debtors and offering short-

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

term credit facilities as well.

Supply chain Finance is also considered as suitable way to improve WC efficiency (Working

capital management strategy, 2012). Further, effective management of market demand and

inventory optimization also helps to set maximum stock level and manage cash flow.

TASK 2

Risk and return

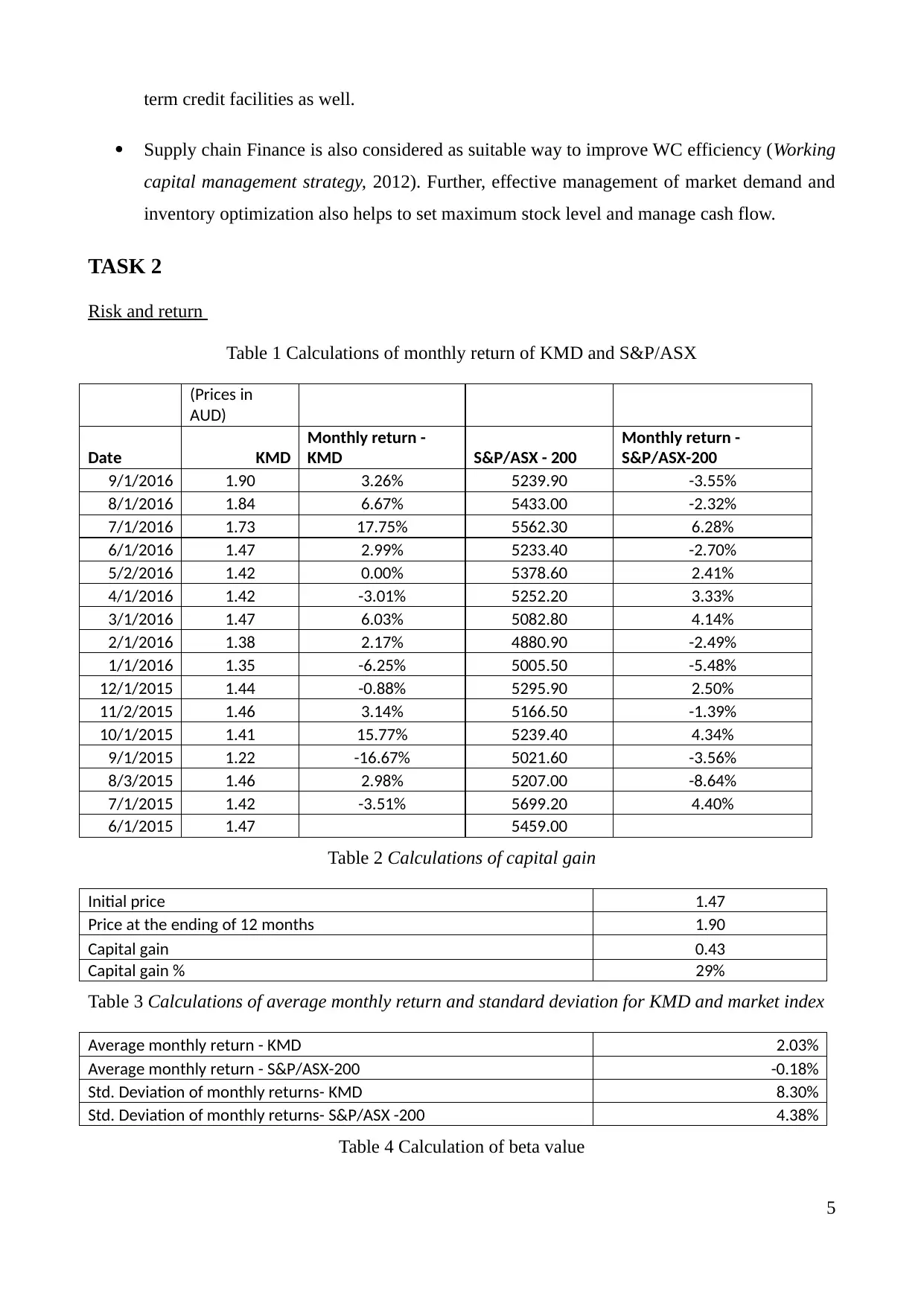

Table 1 Calculations of monthly return of KMD and S&P/ASX

(Prices in

AUD)

Date KMD

Monthly return -

KMD S&P/ASX - 200

Monthly return -

S&P/ASX-200

9/1/2016 1.90 3.26% 5239.90 -3.55%

8/1/2016 1.84 6.67% 5433.00 -2.32%

7/1/2016 1.73 17.75% 5562.30 6.28%

6/1/2016 1.47 2.99% 5233.40 -2.70%

5/2/2016 1.42 0.00% 5378.60 2.41%

4/1/2016 1.42 -3.01% 5252.20 3.33%

3/1/2016 1.47 6.03% 5082.80 4.14%

2/1/2016 1.38 2.17% 4880.90 -2.49%

1/1/2016 1.35 -6.25% 5005.50 -5.48%

12/1/2015 1.44 -0.88% 5295.90 2.50%

11/2/2015 1.46 3.14% 5166.50 -1.39%

10/1/2015 1.41 15.77% 5239.40 4.34%

9/1/2015 1.22 -16.67% 5021.60 -3.56%

8/3/2015 1.46 2.98% 5207.00 -8.64%

7/1/2015 1.42 -3.51% 5699.20 4.40%

6/1/2015 1.47 5459.00

Table 2 Calculations of capital gain

Initial price 1.47

Price at the ending of 12 months 1.90

Capital gain 0.43

Capital gain % 29%

Table 3 Calculations of average monthly return and standard deviation for KMD and market index

Average monthly return - KMD 2.03%

Average monthly return - S&P/ASX-200 -0.18%

Std. Deviation of monthly returns- KMD 8.30%

Std. Deviation of monthly returns- S&P/ASX -200 4.38%

Table 4 Calculation of beta value

5

Supply chain Finance is also considered as suitable way to improve WC efficiency (Working

capital management strategy, 2012). Further, effective management of market demand and

inventory optimization also helps to set maximum stock level and manage cash flow.

TASK 2

Risk and return

Table 1 Calculations of monthly return of KMD and S&P/ASX

(Prices in

AUD)

Date KMD

Monthly return -

KMD S&P/ASX - 200

Monthly return -

S&P/ASX-200

9/1/2016 1.90 3.26% 5239.90 -3.55%

8/1/2016 1.84 6.67% 5433.00 -2.32%

7/1/2016 1.73 17.75% 5562.30 6.28%

6/1/2016 1.47 2.99% 5233.40 -2.70%

5/2/2016 1.42 0.00% 5378.60 2.41%

4/1/2016 1.42 -3.01% 5252.20 3.33%

3/1/2016 1.47 6.03% 5082.80 4.14%

2/1/2016 1.38 2.17% 4880.90 -2.49%

1/1/2016 1.35 -6.25% 5005.50 -5.48%

12/1/2015 1.44 -0.88% 5295.90 2.50%

11/2/2015 1.46 3.14% 5166.50 -1.39%

10/1/2015 1.41 15.77% 5239.40 4.34%

9/1/2015 1.22 -16.67% 5021.60 -3.56%

8/3/2015 1.46 2.98% 5207.00 -8.64%

7/1/2015 1.42 -3.51% 5699.20 4.40%

6/1/2015 1.47 5459.00

Table 2 Calculations of capital gain

Initial price 1.47

Price at the ending of 12 months 1.90

Capital gain 0.43

Capital gain % 29%

Table 3 Calculations of average monthly return and standard deviation for KMD and market index

Average monthly return - KMD 2.03%

Average monthly return - S&P/ASX-200 -0.18%

Std. Deviation of monthly returns- KMD 8.30%

Std. Deviation of monthly returns- S&P/ASX -200 4.38%

Table 4 Calculation of beta value

5

Beta value - KMD 0.77

In the portfolio strategy, diversification concept is of great significance which indicates that

an investor must invest their own money in two or more securities so that loss on one can be

adjusted against other. It is a risk management strategy that helps to minimize the investment risk

on entire portfolio (Berry, 2015). In the given scenario, monthly return for KMD and S&P/ASX are

2.03% and -0.18% whilst the standard deviation is 8.30% and 4.38% respectively. It demonstrates

that there is high investment risk in KMD, therefore, Aunty can use diversification technique,

through which, it can put its money into different securities by examining the potential risk and

return. With the assistance of this, it can minimizes risks and create an efficient portfolio to have

maximum return.

Systematic risk

This risk refers to the possibility of market volatility which can arise severe difficulties and

also can collapse the entire business of the KMD. The main reason for this risk is only the

fluctuations in external market which is outside the control of business, therefore, also called market

risk and un-diversifiable risk.

(Bromiley, P. and et.al., 2015)

Interest rate risk: If bank increase their lending rates than it will incline the cost of

borrowing for the KMD (Valipour, M. and et.al., 2015). Thus, the heavier the cost of debt results in

net profitability and decreases their operational performance.

Market risk: Risk of falling in stock price due to market risk like tough competition,

changing customer behaviour and many others are called market risk.

Unsystematic risk

This is also known as residual and specific risk, in which, KMD’s internal factors are

responsible for the risk occurred. It can be arise due to inefficient management of inventory, cash

position and sudden strike by the labour force etc.

6

In the portfolio strategy, diversification concept is of great significance which indicates that

an investor must invest their own money in two or more securities so that loss on one can be

adjusted against other. It is a risk management strategy that helps to minimize the investment risk

on entire portfolio (Berry, 2015). In the given scenario, monthly return for KMD and S&P/ASX are

2.03% and -0.18% whilst the standard deviation is 8.30% and 4.38% respectively. It demonstrates

that there is high investment risk in KMD, therefore, Aunty can use diversification technique,

through which, it can put its money into different securities by examining the potential risk and

return. With the assistance of this, it can minimizes risks and create an efficient portfolio to have

maximum return.

Systematic risk

This risk refers to the possibility of market volatility which can arise severe difficulties and

also can collapse the entire business of the KMD. The main reason for this risk is only the

fluctuations in external market which is outside the control of business, therefore, also called market

risk and un-diversifiable risk.

(Bromiley, P. and et.al., 2015)

Interest rate risk: If bank increase their lending rates than it will incline the cost of

borrowing for the KMD (Valipour, M. and et.al., 2015). Thus, the heavier the cost of debt results in

net profitability and decreases their operational performance.

Market risk: Risk of falling in stock price due to market risk like tough competition,

changing customer behaviour and many others are called market risk.

Unsystematic risk

This is also known as residual and specific risk, in which, KMD’s internal factors are

responsible for the risk occurred. It can be arise due to inefficient management of inventory, cash

position and sudden strike by the labour force etc.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

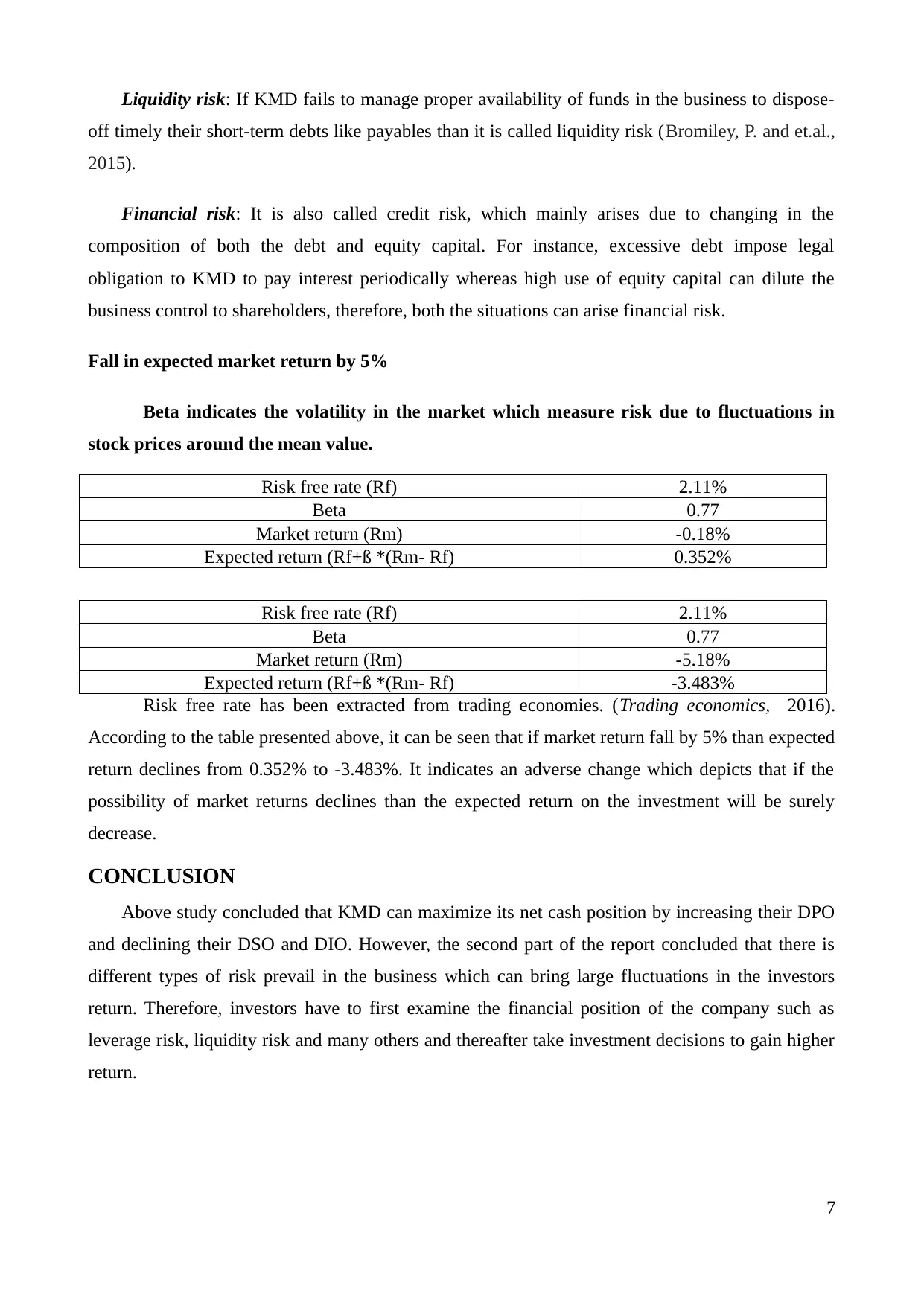

Liquidity risk: If KMD fails to manage proper availability of funds in the business to dispose-

off timely their short-term debts like payables than it is called liquidity risk (Bromiley, P. and et.al.,

2015).

Financial risk: It is also called credit risk, which mainly arises due to changing in the

composition of both the debt and equity capital. For instance, excessive debt impose legal

obligation to KMD to pay interest periodically whereas high use of equity capital can dilute the

business control to shareholders, therefore, both the situations can arise financial risk.

Fall in expected market return by 5%

Beta indicates the volatility in the market which measure risk due to fluctuations in

stock prices around the mean value.

Risk free rate (Rf) 2.11%

Beta 0.77

Market return (Rm) -0.18%

Expected return (Rf+ß *(Rm- Rf) 0.352%

Risk free rate (Rf) 2.11%

Beta 0.77

Market return (Rm) -5.18%

Expected return (Rf+ß *(Rm- Rf) -3.483%

Risk free rate has been extracted from trading economies. (Trading economics, 2016).

According to the table presented above, it can be seen that if market return fall by 5% than expected

return declines from 0.352% to -3.483%. It indicates an adverse change which depicts that if the

possibility of market returns declines than the expected return on the investment will be surely

decrease.

CONCLUSION

Above study concluded that KMD can maximize its net cash position by increasing their DPO

and declining their DSO and DIO. However, the second part of the report concluded that there is

different types of risk prevail in the business which can bring large fluctuations in the investors

return. Therefore, investors have to first examine the financial position of the company such as

leverage risk, liquidity risk and many others and thereafter take investment decisions to gain higher

return.

7

off timely their short-term debts like payables than it is called liquidity risk (Bromiley, P. and et.al.,

2015).

Financial risk: It is also called credit risk, which mainly arises due to changing in the

composition of both the debt and equity capital. For instance, excessive debt impose legal

obligation to KMD to pay interest periodically whereas high use of equity capital can dilute the

business control to shareholders, therefore, both the situations can arise financial risk.

Fall in expected market return by 5%

Beta indicates the volatility in the market which measure risk due to fluctuations in

stock prices around the mean value.

Risk free rate (Rf) 2.11%

Beta 0.77

Market return (Rm) -0.18%

Expected return (Rf+ß *(Rm- Rf) 0.352%

Risk free rate (Rf) 2.11%

Beta 0.77

Market return (Rm) -5.18%

Expected return (Rf+ß *(Rm- Rf) -3.483%

Risk free rate has been extracted from trading economies. (Trading economics, 2016).

According to the table presented above, it can be seen that if market return fall by 5% than expected

return declines from 0.352% to -3.483%. It indicates an adverse change which depicts that if the

possibility of market returns declines than the expected return on the investment will be surely

decrease.

CONCLUSION

Above study concluded that KMD can maximize its net cash position by increasing their DPO

and declining their DSO and DIO. However, the second part of the report concluded that there is

different types of risk prevail in the business which can bring large fluctuations in the investors

return. Therefore, investors have to first examine the financial position of the company such as

leverage risk, liquidity risk and many others and thereafter take investment decisions to gain higher

return.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Berry, C. H., 2015. Corporate growth and diversification. Princeton University Press.

Bromiley, P. and et.al., 2015. Enterprise risk management: Review, critique, and research

directions. Long range planning. 48(4). pp. 265-276.

Das, S., 2016. Impact of cash conversion cycle for measuring the efficiency of cash management: A

study on pharmaceutical sector. Accounting. 2(4). pp. 143-150.

Deepa, N. and et.al., 2016. Influence of Cash Conversion Cycle on Financial Performance of

Coconut Oil Mills in Western Tamil Nadu. Indian Journal of Economics and Development.

12(1). pp. 143-150.

Moghadam, A. and Rahimi, M., 2016. The Relationship between Working Capital Management and

Cash Flows on the Financial Performance of Manufacturing Firms. Asian Journal of

Research in Banking and Finance. 6(6). pp. 34-42.

Sivashanmugam, C. and Krishnakumar, S., 2016. Working Capital Management and Corporate

Profitability: Empirical Evidences from Indian Cement Companies. Asian Journal of

Research in Social Sciences and Humanities. 6(7). pp. 1471-1486.

Valipour, M. and et.al., 2015. Forecasting stock systematic risk using Heuristic Algorithms. Journal

of productivity and development. 1(1). pp. 36-41.

Online

Kathmandu Holdings Ltd. 2016. [PDF]. Available

through<:http://192.168.1.18/projectfiles/internal_cust_document/201609141957240651473

854794_147354901.pdf>. [Accessed on 16th September 2016].

ORL Group Ltd. 2015. [Online]. Available through: <

http://financials.morningstar.com/ratios/r.html?t=ORL>. [Accessed on 16th September

2016].

Trading economics. 2016. [Online]. Available through:

http://www.tradingeconomics.com/australia/government-bond-yieldRegards. [Accessed on

16th September 2016].

Working capital management strategy. 2012. [Online]. Available through: < http://www.strategy-at-

risk.com/2012/11/27/working-capital-strategy-revisited/>. [Accessed on 16th September

2016].

8

Books and Journals

Berry, C. H., 2015. Corporate growth and diversification. Princeton University Press.

Bromiley, P. and et.al., 2015. Enterprise risk management: Review, critique, and research

directions. Long range planning. 48(4). pp. 265-276.

Das, S., 2016. Impact of cash conversion cycle for measuring the efficiency of cash management: A

study on pharmaceutical sector. Accounting. 2(4). pp. 143-150.

Deepa, N. and et.al., 2016. Influence of Cash Conversion Cycle on Financial Performance of

Coconut Oil Mills in Western Tamil Nadu. Indian Journal of Economics and Development.

12(1). pp. 143-150.

Moghadam, A. and Rahimi, M., 2016. The Relationship between Working Capital Management and

Cash Flows on the Financial Performance of Manufacturing Firms. Asian Journal of

Research in Banking and Finance. 6(6). pp. 34-42.

Sivashanmugam, C. and Krishnakumar, S., 2016. Working Capital Management and Corporate

Profitability: Empirical Evidences from Indian Cement Companies. Asian Journal of

Research in Social Sciences and Humanities. 6(7). pp. 1471-1486.

Valipour, M. and et.al., 2015. Forecasting stock systematic risk using Heuristic Algorithms. Journal

of productivity and development. 1(1). pp. 36-41.

Online

Kathmandu Holdings Ltd. 2016. [PDF]. Available

through<:http://192.168.1.18/projectfiles/internal_cust_document/201609141957240651473

854794_147354901.pdf>. [Accessed on 16th September 2016].

ORL Group Ltd. 2015. [Online]. Available through: <

http://financials.morningstar.com/ratios/r.html?t=ORL>. [Accessed on 16th September

2016].

Trading economics. 2016. [Online]. Available through:

http://www.tradingeconomics.com/australia/government-bond-yieldRegards. [Accessed on

16th September 2016].

Working capital management strategy. 2012. [Online]. Available through: < http://www.strategy-at-

risk.com/2012/11/27/working-capital-strategy-revisited/>. [Accessed on 16th September

2016].

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.