Audit, Assurance and Compliance: Analysis of DIPL's Financials

VerifiedAdded on 2020/03/02

|13

|2797

|63

Report

AI Summary

This report provides a comprehensive analysis of audit, assurance, and compliance practices, focusing on the financial performance of DIPL. It begins with an application of analytical procedures, particularly ratio analysis, to assess profitability, liquidity, efficiency, and solvency over a three-year period. The analysis reveals trends and potential issues, such as declining profitability ratios, fluctuating liquidity, and concerning efficiency and solvency metrics. The report then examines the impact of these analytical methods on audit planning, highlighting the need for detailed evaluations of inventory allowances, management efficiency, and financial risk factors. Furthermore, the report identifies and discusses various business risks, including financial risks related to debt and potential material misstatements in financial reports, as well as risks associated with information technology implementation. It also explores specific financial practices that create risks for the company, such as debt agreements and the nature of the control environment, and it concludes with a discussion of how these risks influence audit planning. This report is a student contribution for Desklib.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Audit, Assurance and Compliance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question 1......................................................................................................................2

Application of Analytical Process of Financial Information.......................................................2

Impact of Analytical Methods on Audit Planning.......................................................................6

Answer to Question 2......................................................................................................................6

Answer to Question 3......................................................................................................................8

Answer to (a)...............................................................................................................................8

Answer to (b)...............................................................................................................................9

References......................................................................................................................................11

Table of Contents

Answer to Question 1......................................................................................................................2

Application of Analytical Process of Financial Information.......................................................2

Impact of Analytical Methods on Audit Planning.......................................................................6

Answer to Question 2......................................................................................................................6

Answer to Question 3......................................................................................................................8

Answer to (a)...............................................................................................................................8

Answer to (b)...............................................................................................................................9

References......................................................................................................................................11

2AUDIT, ASSURANCE AND COMPLIANCE

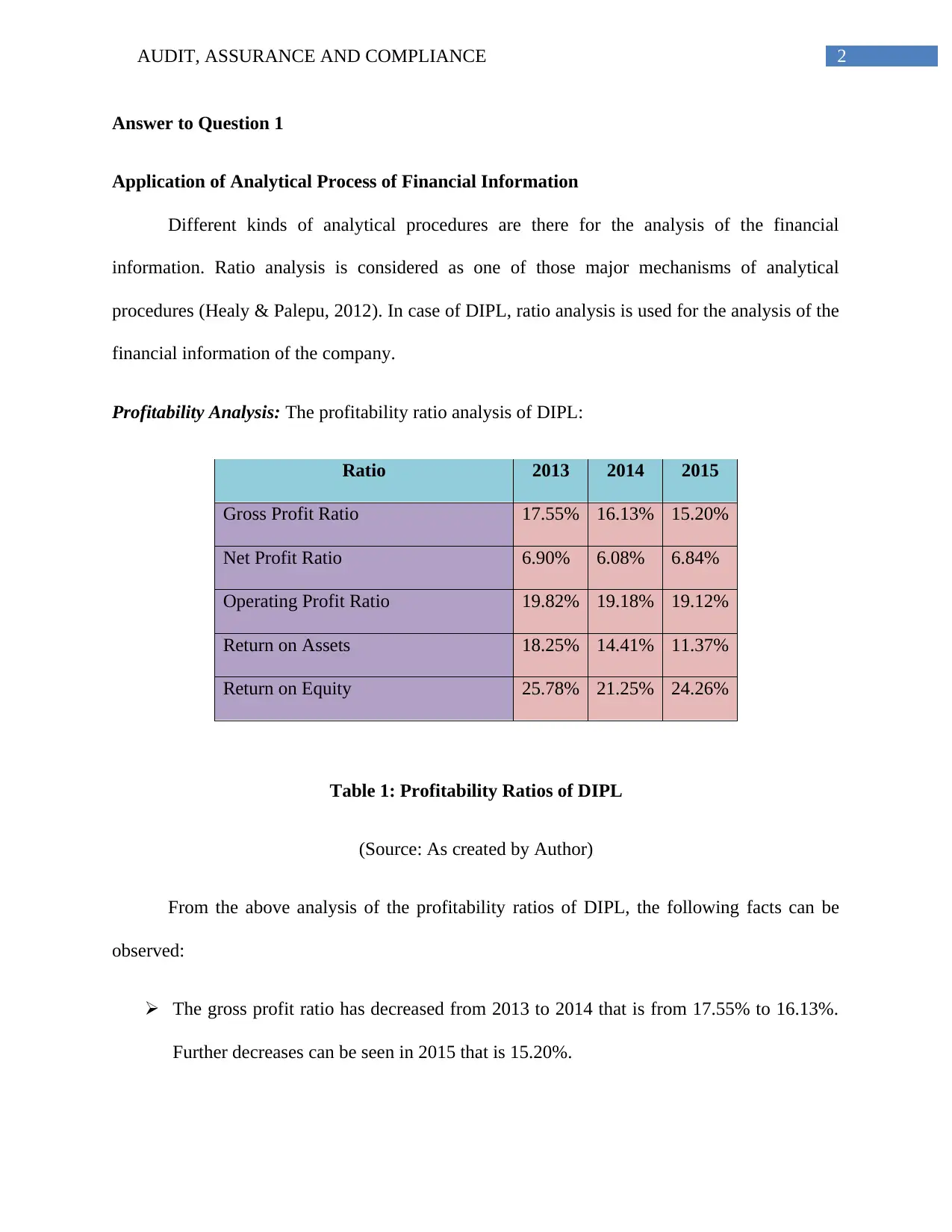

Answer to Question 1

Application of Analytical Process of Financial Information

Different kinds of analytical procedures are there for the analysis of the financial

information. Ratio analysis is considered as one of those major mechanisms of analytical

procedures (Healy & Palepu, 2012). In case of DIPL, ratio analysis is used for the analysis of the

financial information of the company.

Profitability Analysis: The profitability ratio analysis of DIPL:

Ratio 2013 2014 2015

Gross Profit Ratio 17.55% 16.13% 15.20%

Net Profit Ratio 6.90% 6.08% 6.84%

Operating Profit Ratio 19.82% 19.18% 19.12%

Return on Assets 18.25% 14.41% 11.37%

Return on Equity 25.78% 21.25% 24.26%

Table 1: Profitability Ratios of DIPL

(Source: As created by Author)

From the above analysis of the profitability ratios of DIPL, the following facts can be

observed:

The gross profit ratio has decreased from 2013 to 2014 that is from 17.55% to 16.13%.

Further decreases can be seen in 2015 that is 15.20%.

Answer to Question 1

Application of Analytical Process of Financial Information

Different kinds of analytical procedures are there for the analysis of the financial

information. Ratio analysis is considered as one of those major mechanisms of analytical

procedures (Healy & Palepu, 2012). In case of DIPL, ratio analysis is used for the analysis of the

financial information of the company.

Profitability Analysis: The profitability ratio analysis of DIPL:

Ratio 2013 2014 2015

Gross Profit Ratio 17.55% 16.13% 15.20%

Net Profit Ratio 6.90% 6.08% 6.84%

Operating Profit Ratio 19.82% 19.18% 19.12%

Return on Assets 18.25% 14.41% 11.37%

Return on Equity 25.78% 21.25% 24.26%

Table 1: Profitability Ratios of DIPL

(Source: As created by Author)

From the above analysis of the profitability ratios of DIPL, the following facts can be

observed:

The gross profit ratio has decreased from 2013 to 2014 that is from 17.55% to 16.13%.

Further decreases can be seen in 2015 that is 15.20%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT, ASSURANCE AND COMPLIANCE

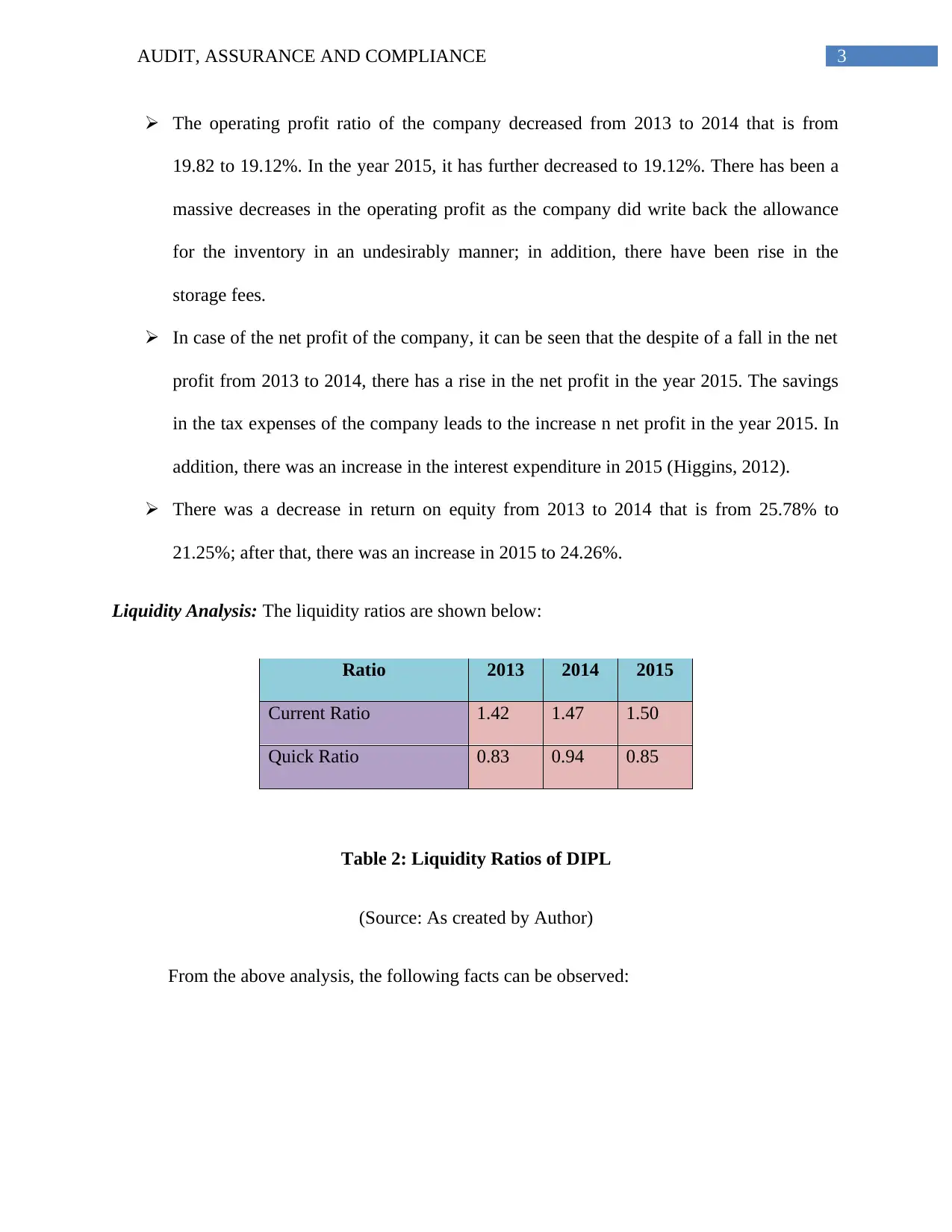

The operating profit ratio of the company decreased from 2013 to 2014 that is from

19.82 to 19.12%. In the year 2015, it has further decreased to 19.12%. There has been a

massive decreases in the operating profit as the company did write back the allowance

for the inventory in an undesirably manner; in addition, there have been rise in the

storage fees.

In case of the net profit of the company, it can be seen that the despite of a fall in the net

profit from 2013 to 2014, there has a rise in the net profit in the year 2015. The savings

in the tax expenses of the company leads to the increase n net profit in the year 2015. In

addition, there was an increase in the interest expenditure in 2015 (Higgins, 2012).

There was a decrease in return on equity from 2013 to 2014 that is from 25.78% to

21.25%; after that, there was an increase in 2015 to 24.26%.

Liquidity Analysis: The liquidity ratios are shown below:

Ratio 2013 2014 2015

Current Ratio 1.42 1.47 1.50

Quick Ratio 0.83 0.94 0.85

Table 2: Liquidity Ratios of DIPL

(Source: As created by Author)

From the above analysis, the following facts can be observed:

The operating profit ratio of the company decreased from 2013 to 2014 that is from

19.82 to 19.12%. In the year 2015, it has further decreased to 19.12%. There has been a

massive decreases in the operating profit as the company did write back the allowance

for the inventory in an undesirably manner; in addition, there have been rise in the

storage fees.

In case of the net profit of the company, it can be seen that the despite of a fall in the net

profit from 2013 to 2014, there has a rise in the net profit in the year 2015. The savings

in the tax expenses of the company leads to the increase n net profit in the year 2015. In

addition, there was an increase in the interest expenditure in 2015 (Higgins, 2012).

There was a decrease in return on equity from 2013 to 2014 that is from 25.78% to

21.25%; after that, there was an increase in 2015 to 24.26%.

Liquidity Analysis: The liquidity ratios are shown below:

Ratio 2013 2014 2015

Current Ratio 1.42 1.47 1.50

Quick Ratio 0.83 0.94 0.85

Table 2: Liquidity Ratios of DIPL

(Source: As created by Author)

From the above analysis, the following facts can be observed:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT, ASSURANCE AND COMPLIANCE

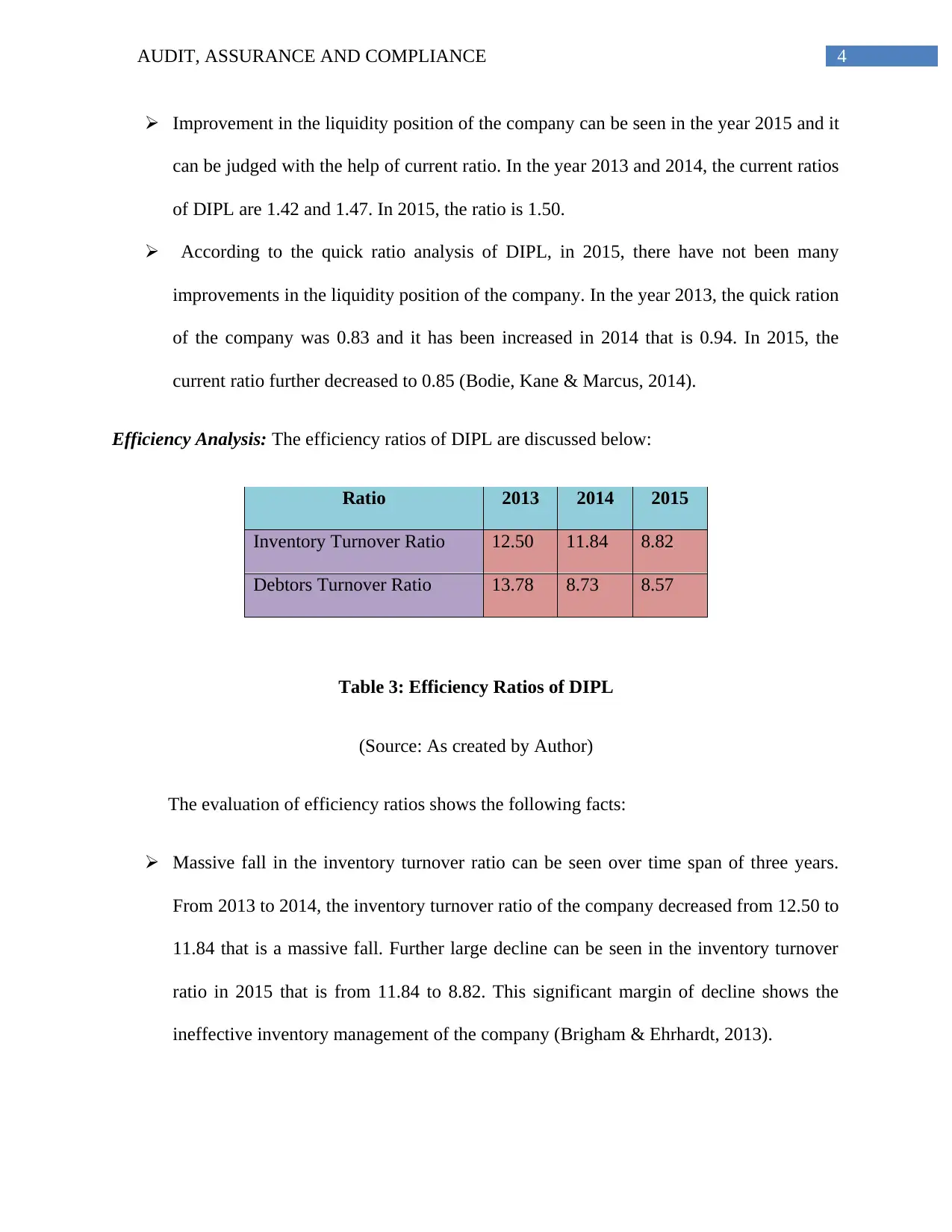

Improvement in the liquidity position of the company can be seen in the year 2015 and it

can be judged with the help of current ratio. In the year 2013 and 2014, the current ratios

of DIPL are 1.42 and 1.47. In 2015, the ratio is 1.50.

According to the quick ratio analysis of DIPL, in 2015, there have not been many

improvements in the liquidity position of the company. In the year 2013, the quick ration

of the company was 0.83 and it has been increased in 2014 that is 0.94. In 2015, the

current ratio further decreased to 0.85 (Bodie, Kane & Marcus, 2014).

Efficiency Analysis: The efficiency ratios of DIPL are discussed below:

Ratio 2013 2014 2015

Inventory Turnover Ratio 12.50 11.84 8.82

Debtors Turnover Ratio 13.78 8.73 8.57

Table 3: Efficiency Ratios of DIPL

(Source: As created by Author)

The evaluation of efficiency ratios shows the following facts:

Massive fall in the inventory turnover ratio can be seen over time span of three years.

From 2013 to 2014, the inventory turnover ratio of the company decreased from 12.50 to

11.84 that is a massive fall. Further large decline can be seen in the inventory turnover

ratio in 2015 that is from 11.84 to 8.82. This significant margin of decline shows the

ineffective inventory management of the company (Brigham & Ehrhardt, 2013).

Improvement in the liquidity position of the company can be seen in the year 2015 and it

can be judged with the help of current ratio. In the year 2013 and 2014, the current ratios

of DIPL are 1.42 and 1.47. In 2015, the ratio is 1.50.

According to the quick ratio analysis of DIPL, in 2015, there have not been many

improvements in the liquidity position of the company. In the year 2013, the quick ration

of the company was 0.83 and it has been increased in 2014 that is 0.94. In 2015, the

current ratio further decreased to 0.85 (Bodie, Kane & Marcus, 2014).

Efficiency Analysis: The efficiency ratios of DIPL are discussed below:

Ratio 2013 2014 2015

Inventory Turnover Ratio 12.50 11.84 8.82

Debtors Turnover Ratio 13.78 8.73 8.57

Table 3: Efficiency Ratios of DIPL

(Source: As created by Author)

The evaluation of efficiency ratios shows the following facts:

Massive fall in the inventory turnover ratio can be seen over time span of three years.

From 2013 to 2014, the inventory turnover ratio of the company decreased from 12.50 to

11.84 that is a massive fall. Further large decline can be seen in the inventory turnover

ratio in 2015 that is from 11.84 to 8.82. This significant margin of decline shows the

ineffective inventory management of the company (Brigham & Ehrhardt, 2013).

5AUDIT, ASSURANCE AND COMPLIANCE

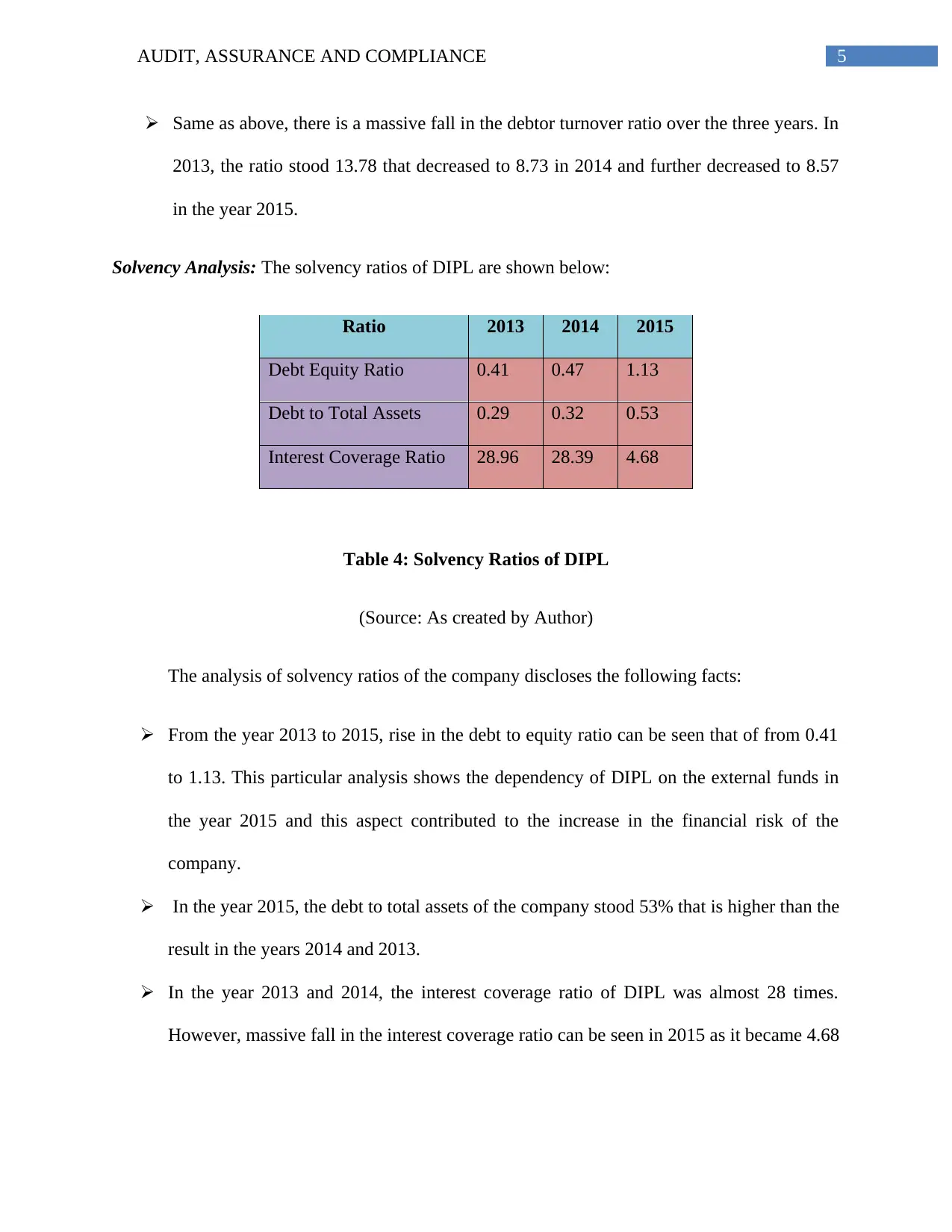

Same as above, there is a massive fall in the debtor turnover ratio over the three years. In

2013, the ratio stood 13.78 that decreased to 8.73 in 2014 and further decreased to 8.57

in the year 2015.

Solvency Analysis: The solvency ratios of DIPL are shown below:

Ratio 2013 2014 2015

Debt Equity Ratio 0.41 0.47 1.13

Debt to Total Assets 0.29 0.32 0.53

Interest Coverage Ratio 28.96 28.39 4.68

Table 4: Solvency Ratios of DIPL

(Source: As created by Author)

The analysis of solvency ratios of the company discloses the following facts:

From the year 2013 to 2015, rise in the debt to equity ratio can be seen that of from 0.41

to 1.13. This particular analysis shows the dependency of DIPL on the external funds in

the year 2015 and this aspect contributed to the increase in the financial risk of the

company.

In the year 2015, the debt to total assets of the company stood 53% that is higher than the

result in the years 2014 and 2013.

In the year 2013 and 2014, the interest coverage ratio of DIPL was almost 28 times.

However, massive fall in the interest coverage ratio can be seen in 2015 as it became 4.68

Same as above, there is a massive fall in the debtor turnover ratio over the three years. In

2013, the ratio stood 13.78 that decreased to 8.73 in 2014 and further decreased to 8.57

in the year 2015.

Solvency Analysis: The solvency ratios of DIPL are shown below:

Ratio 2013 2014 2015

Debt Equity Ratio 0.41 0.47 1.13

Debt to Total Assets 0.29 0.32 0.53

Interest Coverage Ratio 28.96 28.39 4.68

Table 4: Solvency Ratios of DIPL

(Source: As created by Author)

The analysis of solvency ratios of the company discloses the following facts:

From the year 2013 to 2015, rise in the debt to equity ratio can be seen that of from 0.41

to 1.13. This particular analysis shows the dependency of DIPL on the external funds in

the year 2015 and this aspect contributed to the increase in the financial risk of the

company.

In the year 2015, the debt to total assets of the company stood 53% that is higher than the

result in the years 2014 and 2013.

In the year 2013 and 2014, the interest coverage ratio of DIPL was almost 28 times.

However, massive fall in the interest coverage ratio can be seen in 2015 as it became 4.68

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT, ASSURANCE AND COMPLIANCE

times. The rise in the financial risk can is the contributor towards the fall in the ratio

(Brigham & Houston, 2012).

Impact of Analytical Methods on Audit Planning

In the year 2015, there is not any development in profitability situation of the company.

More falls in the profitability ratio in future can endanger the going concern capacity of

the company. Thus, detailed analysis and evaluation of the company is needed.

There is an increase in current ratio in 2015. The writing back inventory loss allowance is

the main contributor of this increase. There is a need for the explained evaluation of the

inventory allowances of the company.

There is a fall in the efficiency level of the company. It indicates the inefficiency level of

the management of the company. Thus, for the efficient handling of the current assets of

the company, the current solvency position of the company needs to be analyzed and

evaluated (Vogel, 2014).

From the ratio analysis, it can be seen that there is an increase in the financial risk of the

company. Thus, all the factors related with this risks need to be analyzed and evaluated in

order to reduce the financial risk of the company (Weil, Schipper & Francis, 2013).

Answer to Question 2

Business risks can be described as the probability regarding the incapability of the

business organizations for the achievements of their business aims and objectives. Various

reasons lead to the incapability of the business organizations; and these in capabilities can be

categorized as external and internal factors of the business environment (Zamboni & Litschig,

times. The rise in the financial risk can is the contributor towards the fall in the ratio

(Brigham & Houston, 2012).

Impact of Analytical Methods on Audit Planning

In the year 2015, there is not any development in profitability situation of the company.

More falls in the profitability ratio in future can endanger the going concern capacity of

the company. Thus, detailed analysis and evaluation of the company is needed.

There is an increase in current ratio in 2015. The writing back inventory loss allowance is

the main contributor of this increase. There is a need for the explained evaluation of the

inventory allowances of the company.

There is a fall in the efficiency level of the company. It indicates the inefficiency level of

the management of the company. Thus, for the efficient handling of the current assets of

the company, the current solvency position of the company needs to be analyzed and

evaluated (Vogel, 2014).

From the ratio analysis, it can be seen that there is an increase in the financial risk of the

company. Thus, all the factors related with this risks need to be analyzed and evaluated in

order to reduce the financial risk of the company (Weil, Schipper & Francis, 2013).

Answer to Question 2

Business risks can be described as the probability regarding the incapability of the

business organizations for the achievements of their business aims and objectives. Various

reasons lead to the incapability of the business organizations; and these in capabilities can be

categorized as external and internal factors of the business environment (Zamboni & Litschig,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT, ASSURANCE AND COMPLIANCE

2013). The following discussion well describes the risk factors that can be raised from the

business operations of DIPL.

I. Financial Risk: Financial risk is one of the major risks in the organizations. Financial risk

refers to the incapability of the business organizations for reimbursing their long-term liabilities

within the mentioned timeframe. The rise in the external liabilities increases the organizational

financial risks (Christoffersen, 2012). In case of DIPL, it can be seen that there is a significant

rise in the debts in comparison of equity in the financial year of 2015. In addition, it can also be

seen that there is a rise in the liabilities regarding payment of the fixed interests and this

increased the burden of loan repayment of the company within the provided time. Thus, it can be

said that the financial risk of the company will be increased in case the company do not have the

financial capability to repay the business liabilities (Kou, Peng & Wang, 2014).

Material Misstatements in the Financial Reports: There is a fare probability that the business

organization will try to influence their financial records in order to control the debt to equity ratio

and current ratio of the business as per the agreement with the money lending institutes. For the

maintenance of the desired current ratio, the management can increase the current assets by

increase the value of the receivables, inventories and others. In addition, in order to maintain the

desired debt to equity ratio, the company can manipulate value of equities by increasing the

amount of retained earnings (Jones, 2012).

II. Risk of Information Technology: Several risks are raised from the implementation of the

information technology in the company. Deficit in the implementation of information technology

may create adverse effect on the business organization. For the computerization of accounting

systems along with the general ledger system, DIPL made implementation of the new as well as

2013). The following discussion well describes the risk factors that can be raised from the

business operations of DIPL.

I. Financial Risk: Financial risk is one of the major risks in the organizations. Financial risk

refers to the incapability of the business organizations for reimbursing their long-term liabilities

within the mentioned timeframe. The rise in the external liabilities increases the organizational

financial risks (Christoffersen, 2012). In case of DIPL, it can be seen that there is a significant

rise in the debts in comparison of equity in the financial year of 2015. In addition, it can also be

seen that there is a rise in the liabilities regarding payment of the fixed interests and this

increased the burden of loan repayment of the company within the provided time. Thus, it can be

said that the financial risk of the company will be increased in case the company do not have the

financial capability to repay the business liabilities (Kou, Peng & Wang, 2014).

Material Misstatements in the Financial Reports: There is a fare probability that the business

organization will try to influence their financial records in order to control the debt to equity ratio

and current ratio of the business as per the agreement with the money lending institutes. For the

maintenance of the desired current ratio, the management can increase the current assets by

increase the value of the receivables, inventories and others. In addition, in order to maintain the

desired debt to equity ratio, the company can manipulate value of equities by increasing the

amount of retained earnings (Jones, 2012).

II. Risk of Information Technology: Several risks are raised from the implementation of the

information technology in the company. Deficit in the implementation of information technology

may create adverse effect on the business organization. For the computerization of accounting

systems along with the general ledger system, DIPL made implementation of the new as well as

8AUDIT, ASSURANCE AND COMPLIANCE

innovative IT processes in the year 2015. In this process, the management of the company

created immense pressure on the IT department employees in order to conclude the new system.

Thus, it many happen that the employees take the route of fraud in order to cope up with the

immense pressure by the management of the company (Schwalbe, 2015).

Material Misstatements in the Financial Reports: It has been seen that the company failed to

perceive the equivalency in the current IT system. Issues can be seen of the inappropriate

allocation of the financial and accounting transactions of the year by the new IT system. The

accounting concepts along with the standards are not followed effectively. This whole process

leads to the inappropriate preparation of the financial statements of the company and it also leads

to the material misstatement of the financial reports of the company (Willcocks, 2013).

Answer to Question 3

Answer to (a)

As per the information of the provided case study of DIPL, there are fault full financial

practices in the organization that creates some major risk factors for the company. Two of these

risk factors are discussed below:

Risk Type Explanation

Debt Agreement

Risk

Massive amount of burden can be seen on the finance department of DIPL

so that all the dent agreements can be maintained. From the case study, it

can be seen that the company tool a loan of 7.5 million from BDO Finance

Limited in 2015 based on the following loan covenant:

The maintenance of a minimum 1.5:1 current ratio, and

innovative IT processes in the year 2015. In this process, the management of the company

created immense pressure on the IT department employees in order to conclude the new system.

Thus, it many happen that the employees take the route of fraud in order to cope up with the

immense pressure by the management of the company (Schwalbe, 2015).

Material Misstatements in the Financial Reports: It has been seen that the company failed to

perceive the equivalency in the current IT system. Issues can be seen of the inappropriate

allocation of the financial and accounting transactions of the year by the new IT system. The

accounting concepts along with the standards are not followed effectively. This whole process

leads to the inappropriate preparation of the financial statements of the company and it also leads

to the material misstatement of the financial reports of the company (Willcocks, 2013).

Answer to Question 3

Answer to (a)

As per the information of the provided case study of DIPL, there are fault full financial

practices in the organization that creates some major risk factors for the company. Two of these

risk factors are discussed below:

Risk Type Explanation

Debt Agreement

Risk

Massive amount of burden can be seen on the finance department of DIPL

so that all the dent agreements can be maintained. From the case study, it

can be seen that the company tool a loan of 7.5 million from BDO Finance

Limited in 2015 based on the following loan covenant:

The maintenance of a minimum 1.5:1 current ratio, and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT, ASSURANCE AND COMPLIANCE

The maintenance of >1 debt to equity ratio.

In case the company fails to maintain the above discussed rations, the loan

will be withdrawn and this process will have adverse effects on the financial

position of the company. Thus, there is a possibility of manipulation of the

current assets in order to sustain the required current ratio. In the same way,

there can be possibility of influencing the retained earnings so that required

debt to equity ratio can be maintained (Arens, Elder & Mark, 2012).

Nature of Control

Environment

Another major factor of risk in the organization is the undefined explanation

of the job descriptions and ineffective segmentation of job responsibilities.

This process can lead to the financial fraudulent regarding the reporting of

financial reports. It can be seen that the accounts payable clerk is

responsible for maintenance of inventory and value of inventory. Thus,

there is a fare risk of alteration of additional inventory at the time of

inventory arrival. Apart from this, the absence of an effective

documentation system is becoming a price reason for accounting and

financial frauds (Gurran, Norman & Hamin, 2013).

Answer to (b)

The auditors need to develop the audit plan in such a manner so that the amount of risk

can be minimized or diminished in the most effective manner. The following discussion shows

the impact of risks in the audit planning:

1. Debt Agreement Impact on the Audit Plan: The amount of current assets and the amount of

current liabilities needs to be supportive to each other in an appropriate way in order to

The maintenance of >1 debt to equity ratio.

In case the company fails to maintain the above discussed rations, the loan

will be withdrawn and this process will have adverse effects on the financial

position of the company. Thus, there is a possibility of manipulation of the

current assets in order to sustain the required current ratio. In the same way,

there can be possibility of influencing the retained earnings so that required

debt to equity ratio can be maintained (Arens, Elder & Mark, 2012).

Nature of Control

Environment

Another major factor of risk in the organization is the undefined explanation

of the job descriptions and ineffective segmentation of job responsibilities.

This process can lead to the financial fraudulent regarding the reporting of

financial reports. It can be seen that the accounts payable clerk is

responsible for maintenance of inventory and value of inventory. Thus,

there is a fare risk of alteration of additional inventory at the time of

inventory arrival. Apart from this, the absence of an effective

documentation system is becoming a price reason for accounting and

financial frauds (Gurran, Norman & Hamin, 2013).

Answer to (b)

The auditors need to develop the audit plan in such a manner so that the amount of risk

can be minimized or diminished in the most effective manner. The following discussion shows

the impact of risks in the audit planning:

1. Debt Agreement Impact on the Audit Plan: The amount of current assets and the amount of

current liabilities needs to be supportive to each other in an appropriate way in order to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT, ASSURANCE AND COMPLIANCE

determine whether there is any presence of inflation in the current assets of the organization f

there is any deflation in the current liabilities of the organization. In the same manner, there is a

need for the examination of the equity balances in order to confirm the fact whether there is any

inflation in the amounts or not (Chou, 2015).

2. Control Environment Impact on the Audit Plan: There is a strong need to examine the

inventory balance of the company. There needs to be a harmonized process between the purchase

of inventory and the received quantity of inventory in order to verify the fact that whether there

is any alterations made in the accounts payable of the organization or not (Balaniuk et al., 2012).

determine whether there is any presence of inflation in the current assets of the organization f

there is any deflation in the current liabilities of the organization. In the same manner, there is a

need for the examination of the equity balances in order to confirm the fact whether there is any

inflation in the amounts or not (Chou, 2015).

2. Control Environment Impact on the Audit Plan: There is a strong need to examine the

inventory balance of the company. There needs to be a harmonized process between the purchase

of inventory and the received quantity of inventory in order to verify the fact that whether there

is any alterations made in the accounts payable of the organization or not (Balaniuk et al., 2012).

11AUDIT, ASSURANCE AND COMPLIANCE

References

Arens, A. A., Elder, R. J., & Mark, B. (2012). Auditing and assurance services: an integrated

approach. Boston: Prentice Hall.

Balaniuk, R., Bessiere, P., Mazer, E., & Cobbe, P. (2012). Risk based government audit planning

using naïve bayes classifiers. In Advances in Knowledge-Based and Intelligent

Information and Engineering Systems.

Bodie, Z., Kane, A., & Marcus, A. J. (2014). Investments, 10e. McGraw-Hill Education.

Brigham, E. F., & Ehrhardt, M. C. (2013). Financial management: Theory & practice. Cengage

Learning.

Brigham, E. F., & Houston, J. F. (2012). Fundamentals of financial management. Cengage

Learning.

Chou, D. C. (2015). Cloud computing risk and audit issues. Computer Standards &

Interfaces, 42, 137-142.

Christoffersen, P. F. (2012). Elements of financial risk management. Academic Press.

Gurran, N., Norman, B., & Hamin, E. (2013). Climate change adaptation in coastal Australia: an

audit of planning practice. Ocean & coastal management, 86, 100-109.

Healy, P. M., & Palepu, K. G. (2012). Business analysis valuation: Using financial statements.

Cengage Learning.

Higgins, R. C. (2012). Analysis for financial management. McGraw-Hill/Irwin.

References

Arens, A. A., Elder, R. J., & Mark, B. (2012). Auditing and assurance services: an integrated

approach. Boston: Prentice Hall.

Balaniuk, R., Bessiere, P., Mazer, E., & Cobbe, P. (2012). Risk based government audit planning

using naïve bayes classifiers. In Advances in Knowledge-Based and Intelligent

Information and Engineering Systems.

Bodie, Z., Kane, A., & Marcus, A. J. (2014). Investments, 10e. McGraw-Hill Education.

Brigham, E. F., & Ehrhardt, M. C. (2013). Financial management: Theory & practice. Cengage

Learning.

Brigham, E. F., & Houston, J. F. (2012). Fundamentals of financial management. Cengage

Learning.

Chou, D. C. (2015). Cloud computing risk and audit issues. Computer Standards &

Interfaces, 42, 137-142.

Christoffersen, P. F. (2012). Elements of financial risk management. Academic Press.

Gurran, N., Norman, B., & Hamin, E. (2013). Climate change adaptation in coastal Australia: an

audit of planning practice. Ocean & coastal management, 86, 100-109.

Healy, P. M., & Palepu, K. G. (2012). Business analysis valuation: Using financial statements.

Cengage Learning.

Higgins, R. C. (2012). Analysis for financial management. McGraw-Hill/Irwin.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.