APC308 Financial Management Report: Equity Finance and Appraisal

VerifiedAdded on 2022/12/29

|14

|3702

|38

Report

AI Summary

This report provides a comprehensive analysis of financial management techniques, focusing on equity finance and investment appraisal. The report begins with calculations related to equity finance for Lexbel Plc, determining the number of shares to be issued, theoretical ex-rights price, and earnings...

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Calculation of equity finance for Lexbel Plc: .........................................................................1

b) Critical discussion on benefits of scrip dividends from company's view point and

shareholder's point of view:.........................................................................................................3

TASK 2............................................................................................................................................4

a) Calculation of investment appraisal techniques and providing brief recommendations for

economic feasibility for acquiring machine:................................................................................4

b) Critical evaluation of benefits as well as limitations of each technique of investment

appraisal:......................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Calculation of equity finance for Lexbel Plc: .........................................................................1

b) Critical discussion on benefits of scrip dividends from company's view point and

shareholder's point of view:.........................................................................................................3

TASK 2............................................................................................................................................4

a) Calculation of investment appraisal techniques and providing brief recommendations for

economic feasibility for acquiring machine:................................................................................4

b) Critical evaluation of benefits as well as limitations of each technique of investment

appraisal:......................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

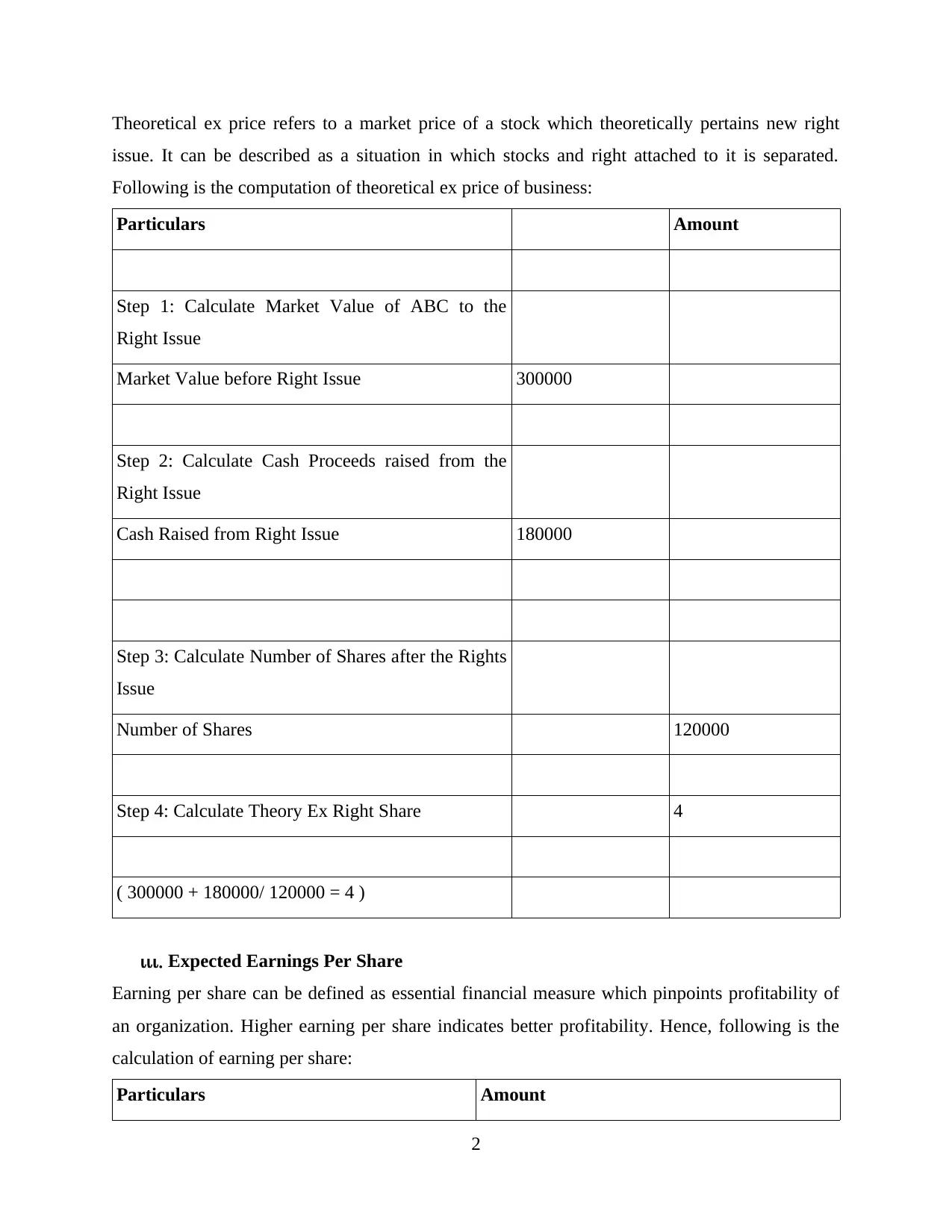

INTRODUCTION

Financial management can be explained as an function that is incorporated in an

organization that is concerned with analysis of financial data for the purpose of evaluating

profitability, expenditures, cash flow as well as credit. It is generally related to working capital

management as it focuses on current assets and liabilities. Motive of incorporating working

capital management is maximization of profit, proper maintenance of cash flow, estimation of

fund requirement and determination of capital structure. This report is based of evaluation of

financial management techniques (Ross and Mughan, 2018). It covers equity analysis of equity

finance of an organization by determining its number of shares, theoretical ex-rights price,

earning per share, and issue price. Further, advantages of crip dividend is critically discussed.

Apart from this, investment appraisal techniques are utilised by application of techniques such as

payback period, accounting rate of return, net present value, and internal rate of return.

TASK 1

a) Calculation of equity finance for Lexbel Plc:

Equity finance: It indicates method of raising capital by the method of selling shares of

an organization to institutional investors, financial institutions as well as public (Susan and

Djajadikerta, 2017). Individuals that purchase share of a company is termed as shareholders of

business as they receive ownership in an organization. Equity financing is opted by an enterprise

for the purpose of meeting its liquidity requirements and hence, it incorporates selling of

company's stock in exchange of cash.

i. Number of shares that is to be issued

Number of shares refers is a financial metric that indicates how many stocks or shares of an

organization is currently owned or acquired by investors. Following is the calculation of number

of shares for company:

Particular Formula Result

Number of shares = 180000 / 0.25 720000

ii. Theoretical ex-rights price

1

Financial management can be explained as an function that is incorporated in an

organization that is concerned with analysis of financial data for the purpose of evaluating

profitability, expenditures, cash flow as well as credit. It is generally related to working capital

management as it focuses on current assets and liabilities. Motive of incorporating working

capital management is maximization of profit, proper maintenance of cash flow, estimation of

fund requirement and determination of capital structure. This report is based of evaluation of

financial management techniques (Ross and Mughan, 2018). It covers equity analysis of equity

finance of an organization by determining its number of shares, theoretical ex-rights price,

earning per share, and issue price. Further, advantages of crip dividend is critically discussed.

Apart from this, investment appraisal techniques are utilised by application of techniques such as

payback period, accounting rate of return, net present value, and internal rate of return.

TASK 1

a) Calculation of equity finance for Lexbel Plc:

Equity finance: It indicates method of raising capital by the method of selling shares of

an organization to institutional investors, financial institutions as well as public (Susan and

Djajadikerta, 2017). Individuals that purchase share of a company is termed as shareholders of

business as they receive ownership in an organization. Equity financing is opted by an enterprise

for the purpose of meeting its liquidity requirements and hence, it incorporates selling of

company's stock in exchange of cash.

i. Number of shares that is to be issued

Number of shares refers is a financial metric that indicates how many stocks or shares of an

organization is currently owned or acquired by investors. Following is the calculation of number

of shares for company:

Particular Formula Result

Number of shares = 180000 / 0.25 720000

ii. Theoretical ex-rights price

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Theoretical ex price refers to a market price of a stock which theoretically pertains new right

issue. It can be described as a situation in which stocks and right attached to it is separated.

Following is the computation of theoretical ex price of business:

Particulars Amount

Step 1: Calculate Market Value of ABC to the

Right Issue

Market Value before Right Issue 300000

Step 2: Calculate Cash Proceeds raised from the

Right Issue

Cash Raised from Right Issue 180000

Step 3: Calculate Number of Shares after the Rights

Issue

Number of Shares 120000

Step 4: Calculate Theory Ex Right Share 4

( 300000 + 180000/ 120000 = 4 )

iii. Expected Earnings Per Share

Earning per share can be defined as essential financial measure which pinpoints profitability of

an organization. Higher earning per share indicates better profitability. Hence, following is the

calculation of earning per share:

Particulars Amount

2

issue. It can be described as a situation in which stocks and right attached to it is separated.

Following is the computation of theoretical ex price of business:

Particulars Amount

Step 1: Calculate Market Value of ABC to the

Right Issue

Market Value before Right Issue 300000

Step 2: Calculate Cash Proceeds raised from the

Right Issue

Cash Raised from Right Issue 180000

Step 3: Calculate Number of Shares after the Rights

Issue

Number of Shares 120000

Step 4: Calculate Theory Ex Right Share 4

( 300000 + 180000/ 120000 = 4 )

iii. Expected Earnings Per Share

Earning per share can be defined as essential financial measure which pinpoints profitability of

an organization. Higher earning per share indicates better profitability. Hence, following is the

calculation of earning per share:

Particulars Amount

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

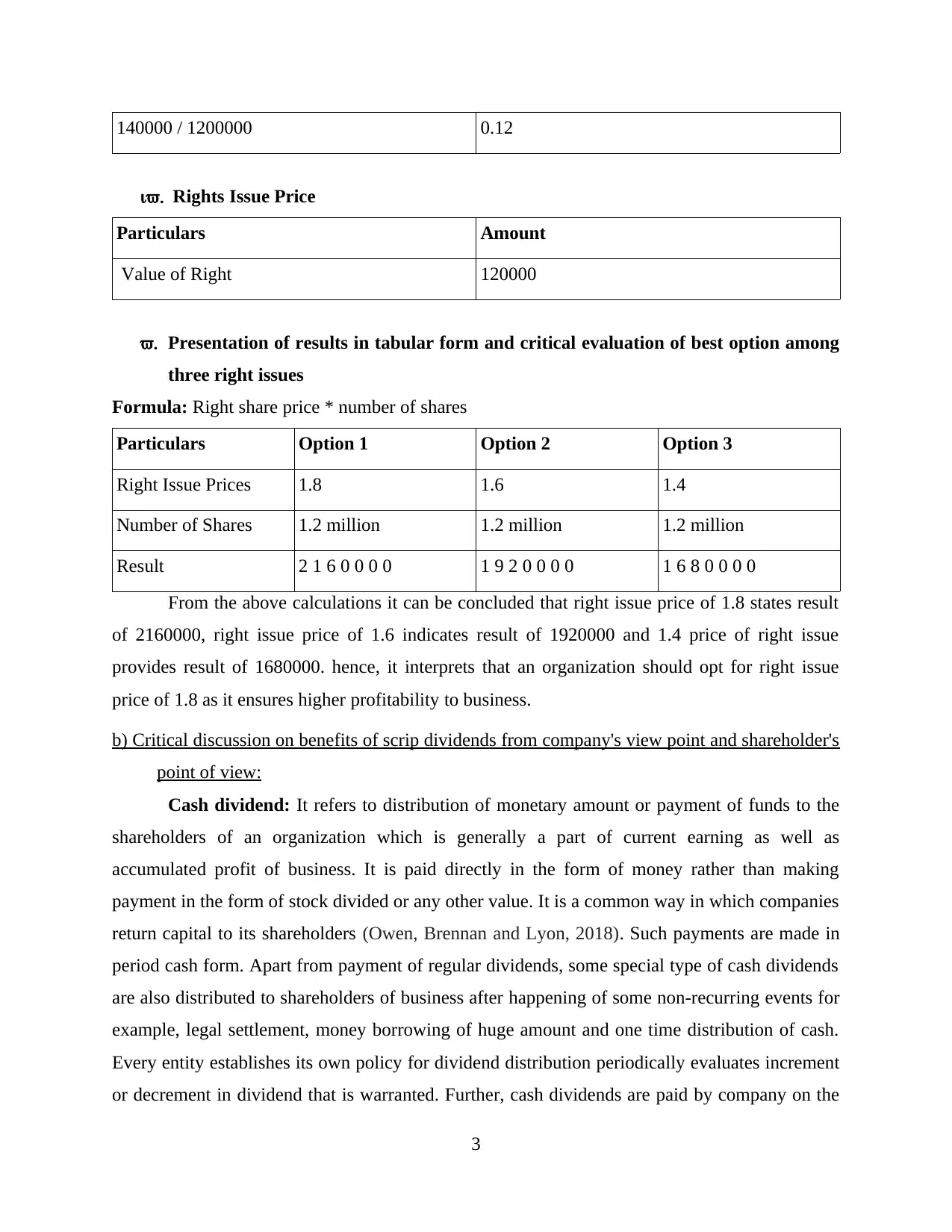

140000 / 1200000 0.12

iv. Rights Issue Price

Particulars Amount

Value of Right 120000

v. Presentation of results in tabular form and critical evaluation of best option among

three right issues

Formula: Right share price * number of shares

Particulars Option 1 Option 2 Option 3

Right Issue Prices 1.8 1.6 1.4

Number of Shares 1.2 million 1.2 million 1.2 million

Result 2 1 6 0 0 0 0 1 9 2 0 0 0 0 1 6 8 0 0 0 0

From the above calculations it can be concluded that right issue price of 1.8 states result

of 2160000, right issue price of 1.6 indicates result of 1920000 and 1.4 price of right issue

provides result of 1680000. hence, it interprets that an organization should opt for right issue

price of 1.8 as it ensures higher profitability to business.

b) Critical discussion on benefits of scrip dividends from company's view point and shareholder's

point of view:

Cash dividend: It refers to distribution of monetary amount or payment of funds to the

shareholders of an organization which is generally a part of current earning as well as

accumulated profit of business. It is paid directly in the form of money rather than making

payment in the form of stock divided or any other value. It is a common way in which companies

return capital to its shareholders (Owen, Brennan and Lyon, 2018). Such payments are made in

period cash form. Apart from payment of regular dividends, some special type of cash dividends

are also distributed to shareholders of business after happening of some non-recurring events for

example, legal settlement, money borrowing of huge amount and one time distribution of cash.

Every entity establishes its own policy for dividend distribution periodically evaluates increment

or decrement in dividend that is warranted. Further, cash dividends are paid by company on the

3

iv. Rights Issue Price

Particulars Amount

Value of Right 120000

v. Presentation of results in tabular form and critical evaluation of best option among

three right issues

Formula: Right share price * number of shares

Particulars Option 1 Option 2 Option 3

Right Issue Prices 1.8 1.6 1.4

Number of Shares 1.2 million 1.2 million 1.2 million

Result 2 1 6 0 0 0 0 1 9 2 0 0 0 0 1 6 8 0 0 0 0

From the above calculations it can be concluded that right issue price of 1.8 states result

of 2160000, right issue price of 1.6 indicates result of 1920000 and 1.4 price of right issue

provides result of 1680000. hence, it interprets that an organization should opt for right issue

price of 1.8 as it ensures higher profitability to business.

b) Critical discussion on benefits of scrip dividends from company's view point and shareholder's

point of view:

Cash dividend: It refers to distribution of monetary amount or payment of funds to the

shareholders of an organization which is generally a part of current earning as well as

accumulated profit of business. It is paid directly in the form of money rather than making

payment in the form of stock divided or any other value. It is a common way in which companies

return capital to its shareholders (Owen, Brennan and Lyon, 2018). Such payments are made in

period cash form. Apart from payment of regular dividends, some special type of cash dividends

are also distributed to shareholders of business after happening of some non-recurring events for

example, legal settlement, money borrowing of huge amount and one time distribution of cash.

Every entity establishes its own policy for dividend distribution periodically evaluates increment

or decrement in dividend that is warranted. Further, cash dividends are paid by company on the

3

basis of per share. Cash dividend is announced by board of directors of an entity on declaration

date which pinpoints payment of certain money per common share. Income statement of an

organization is not affected by payment of cash dividend. However, shareholder's equity as well

as cash balance of business shrinks by same amount.

Equivalent scrip dividend: It can be defined as a activity of issuing new share to the

shareholders instead of paying cash dividend. Scrip dividend is utilised at the time when issues

have less cash available for issuing cash dividend but pertains an intention of paying to

shareholders. It is an alternative for cash dividend and it leads to rolling of dividend payment in

more number of shares (Gertler, Kiyotaki and Prestipino, 2020). It is also referred as a modest

way of issuing stock which pertains no cash payment.

Following are some advantage of equivalent scrip dividend in context to shareholders as

well as companies:

For companies: It enables company for saving cash amount along as no cash payment is

to be made by an organization to its shareholders. It also exempts business from dealing

charges as well as stamp duty which indicates saving of cash in business. Retained cash

can be further utilised for expansion and growth of an entity. It helps company in

enhancing decisions of future capital allocation. Increased number of shares leads to

reduction in bearing of an enterprise as a result of which borrowing capacity of business

increases (Tripathi, Kashiramka and Jain, 2018). Apart from this, share price of company

is also not diluted with payment of equivalent scrip dividend.

For shareholders: Investors or shareholders are provided with options of gaining

additional shares of company rather than paying cash dividend. Shareholders can opt for

suitable option as per their needs. If share are undervalued as per shareholder they can

prefer scrip dividend and get additional shares instead of settling with low cash dividend.

They do not have to pay for transaction cost in this type of dividend which would have

been incurred if same stocks were purchased from brokerage account. Shareholders also

enjoy tax advantage as dividend is received in shares form rather than in the form of cash.

4

date which pinpoints payment of certain money per common share. Income statement of an

organization is not affected by payment of cash dividend. However, shareholder's equity as well

as cash balance of business shrinks by same amount.

Equivalent scrip dividend: It can be defined as a activity of issuing new share to the

shareholders instead of paying cash dividend. Scrip dividend is utilised at the time when issues

have less cash available for issuing cash dividend but pertains an intention of paying to

shareholders. It is an alternative for cash dividend and it leads to rolling of dividend payment in

more number of shares (Gertler, Kiyotaki and Prestipino, 2020). It is also referred as a modest

way of issuing stock which pertains no cash payment.

Following are some advantage of equivalent scrip dividend in context to shareholders as

well as companies:

For companies: It enables company for saving cash amount along as no cash payment is

to be made by an organization to its shareholders. It also exempts business from dealing

charges as well as stamp duty which indicates saving of cash in business. Retained cash

can be further utilised for expansion and growth of an entity. It helps company in

enhancing decisions of future capital allocation. Increased number of shares leads to

reduction in bearing of an enterprise as a result of which borrowing capacity of business

increases (Tripathi, Kashiramka and Jain, 2018). Apart from this, share price of company

is also not diluted with payment of equivalent scrip dividend.

For shareholders: Investors or shareholders are provided with options of gaining

additional shares of company rather than paying cash dividend. Shareholders can opt for

suitable option as per their needs. If share are undervalued as per shareholder they can

prefer scrip dividend and get additional shares instead of settling with low cash dividend.

They do not have to pay for transaction cost in this type of dividend which would have

been incurred if same stocks were purchased from brokerage account. Shareholders also

enjoy tax advantage as dividend is received in shares form rather than in the form of cash.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

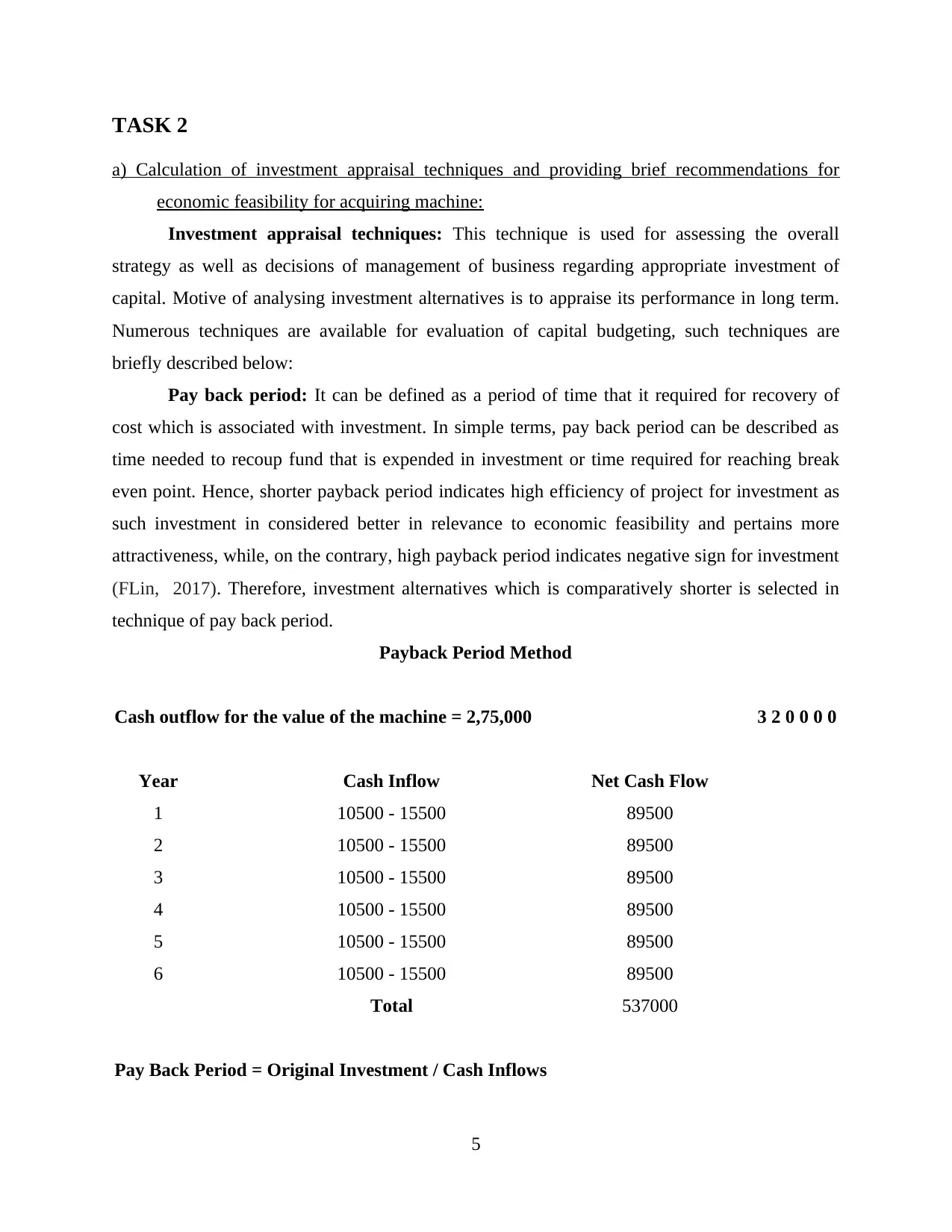

TASK 2

a) Calculation of investment appraisal techniques and providing brief recommendations for

economic feasibility for acquiring machine:

Investment appraisal techniques: This technique is used for assessing the overall

strategy as well as decisions of management of business regarding appropriate investment of

capital. Motive of analysing investment alternatives is to appraise its performance in long term.

Numerous techniques are available for evaluation of capital budgeting, such techniques are

briefly described below:

Pay back period: It can be defined as a period of time that it required for recovery of

cost which is associated with investment. In simple terms, pay back period can be described as

time needed to recoup fund that is expended in investment or time required for reaching break

even point. Hence, shorter payback period indicates high efficiency of project for investment as

such investment in considered better in relevance to economic feasibility and pertains more

attractiveness, while, on the contrary, high payback period indicates negative sign for investment

(FLin, 2017). Therefore, investment alternatives which is comparatively shorter is selected in

technique of pay back period.

Payback Period Method

Cash outflow for the value of the machine = 2,75,000 3 2 0 0 0 0

Year Cash Inflow Net Cash Flow

1 10500 - 15500 89500

2 10500 - 15500 89500

3 10500 - 15500 89500

4 10500 - 15500 89500

5 10500 - 15500 89500

6 10500 - 15500 89500

Total 537000

Pay Back Period = Original Investment / Cash Inflows

5

a) Calculation of investment appraisal techniques and providing brief recommendations for

economic feasibility for acquiring machine:

Investment appraisal techniques: This technique is used for assessing the overall

strategy as well as decisions of management of business regarding appropriate investment of

capital. Motive of analysing investment alternatives is to appraise its performance in long term.

Numerous techniques are available for evaluation of capital budgeting, such techniques are

briefly described below:

Pay back period: It can be defined as a period of time that it required for recovery of

cost which is associated with investment. In simple terms, pay back period can be described as

time needed to recoup fund that is expended in investment or time required for reaching break

even point. Hence, shorter payback period indicates high efficiency of project for investment as

such investment in considered better in relevance to economic feasibility and pertains more

attractiveness, while, on the contrary, high payback period indicates negative sign for investment

(FLin, 2017). Therefore, investment alternatives which is comparatively shorter is selected in

technique of pay back period.

Payback Period Method

Cash outflow for the value of the machine = 2,75,000 3 2 0 0 0 0

Year Cash Inflow Net Cash Flow

1 10500 - 15500 89500

2 10500 - 15500 89500

3 10500 - 15500 89500

4 10500 - 15500 89500

5 10500 - 15500 89500

6 10500 - 15500 89500

Total 537000

Pay Back Period = Original Investment / Cash Inflows

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

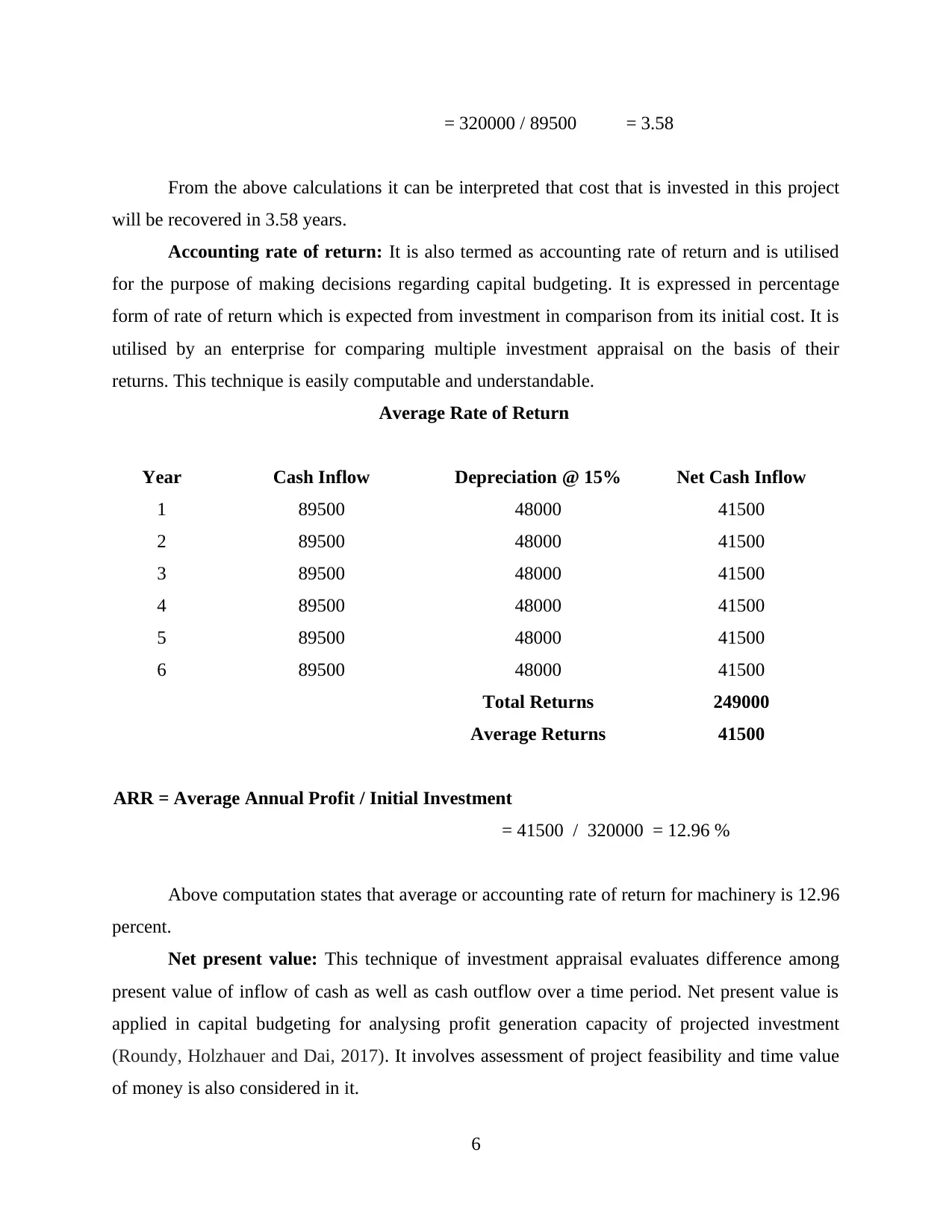

= 320000 / 89500 = 3.58

From the above calculations it can be interpreted that cost that is invested in this project

will be recovered in 3.58 years.

Accounting rate of return: It is also termed as accounting rate of return and is utilised

for the purpose of making decisions regarding capital budgeting. It is expressed in percentage

form of rate of return which is expected from investment in comparison from its initial cost. It is

utilised by an enterprise for comparing multiple investment appraisal on the basis of their

returns. This technique is easily computable and understandable.

Average Rate of Return

Year Cash Inflow Depreciation @ 15% Net Cash Inflow

1 89500 48000 41500

2 89500 48000 41500

3 89500 48000 41500

4 89500 48000 41500

5 89500 48000 41500

6 89500 48000 41500

Total Returns 249000

Average Returns 41500

ARR = Average Annual Profit / Initial Investment

= 41500 / 320000 = 12.96 %

Above computation states that average or accounting rate of return for machinery is 12.96

percent.

Net present value: This technique of investment appraisal evaluates difference among

present value of inflow of cash as well as cash outflow over a time period. Net present value is

applied in capital budgeting for analysing profit generation capacity of projected investment

(Roundy, Holzhauer and Dai, 2017). It involves assessment of project feasibility and time value

of money is also considered in it.

6

From the above calculations it can be interpreted that cost that is invested in this project

will be recovered in 3.58 years.

Accounting rate of return: It is also termed as accounting rate of return and is utilised

for the purpose of making decisions regarding capital budgeting. It is expressed in percentage

form of rate of return which is expected from investment in comparison from its initial cost. It is

utilised by an enterprise for comparing multiple investment appraisal on the basis of their

returns. This technique is easily computable and understandable.

Average Rate of Return

Year Cash Inflow Depreciation @ 15% Net Cash Inflow

1 89500 48000 41500

2 89500 48000 41500

3 89500 48000 41500

4 89500 48000 41500

5 89500 48000 41500

6 89500 48000 41500

Total Returns 249000

Average Returns 41500

ARR = Average Annual Profit / Initial Investment

= 41500 / 320000 = 12.96 %

Above computation states that average or accounting rate of return for machinery is 12.96

percent.

Net present value: This technique of investment appraisal evaluates difference among

present value of inflow of cash as well as cash outflow over a time period. Net present value is

applied in capital budgeting for analysing profit generation capacity of projected investment

(Roundy, Holzhauer and Dai, 2017). It involves assessment of project feasibility and time value

of money is also considered in it.

6

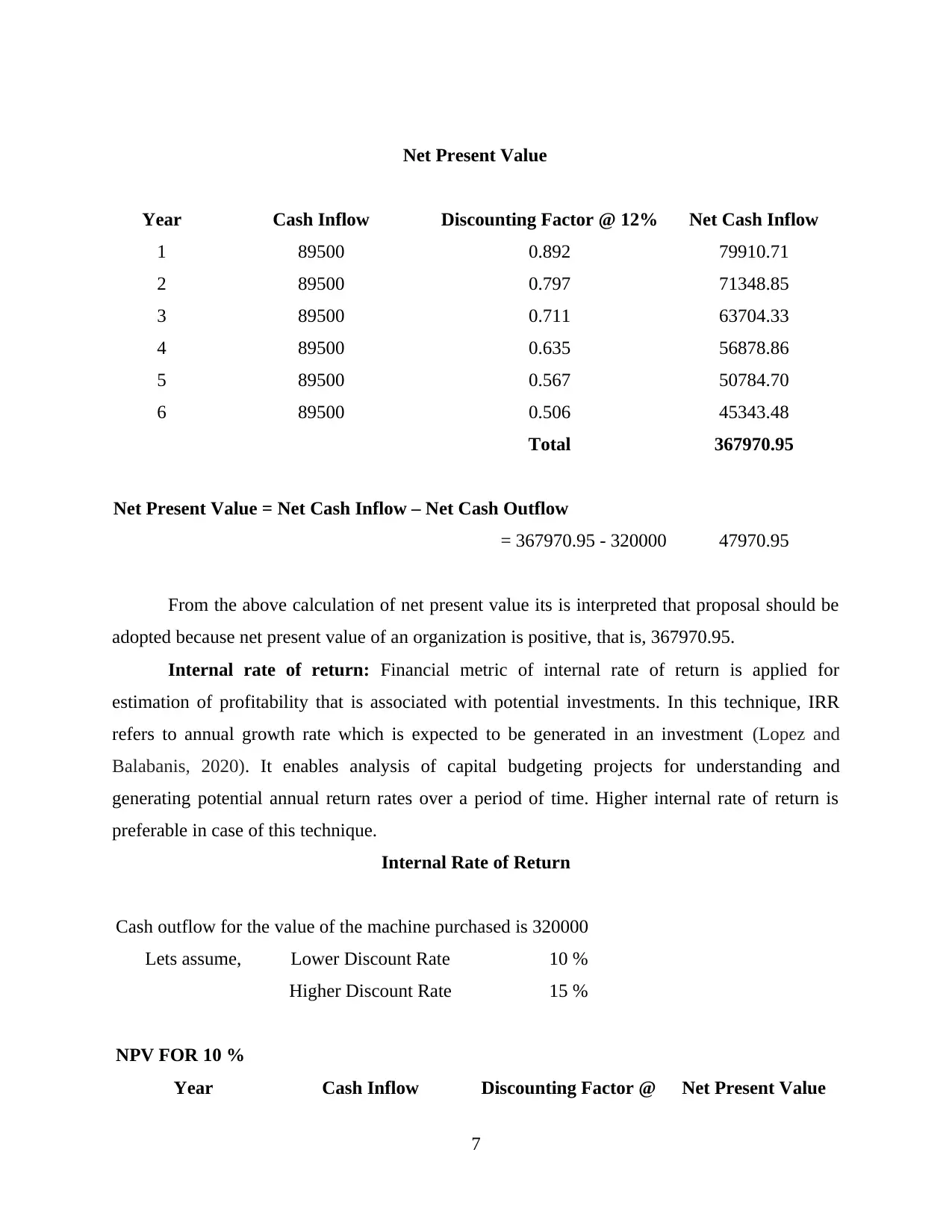

Net Present Value

Year Cash Inflow Discounting Factor @ 12% Net Cash Inflow

1 89500 0.892 79910.71

2 89500 0.797 71348.85

3 89500 0.711 63704.33

4 89500 0.635 56878.86

5 89500 0.567 50784.70

6 89500 0.506 45343.48

Total 367970.95

Net Present Value = Net Cash Inflow – Net Cash Outflow

= 367970.95 - 320000 47970.95

From the above calculation of net present value its is interpreted that proposal should be

adopted because net present value of an organization is positive, that is, 367970.95.

Internal rate of return: Financial metric of internal rate of return is applied for

estimation of profitability that is associated with potential investments. In this technique, IRR

refers to annual growth rate which is expected to be generated in an investment (Lopez and

Balabanis, 2020). It enables analysis of capital budgeting projects for understanding and

generating potential annual return rates over a period of time. Higher internal rate of return is

preferable in case of this technique.

Internal Rate of Return

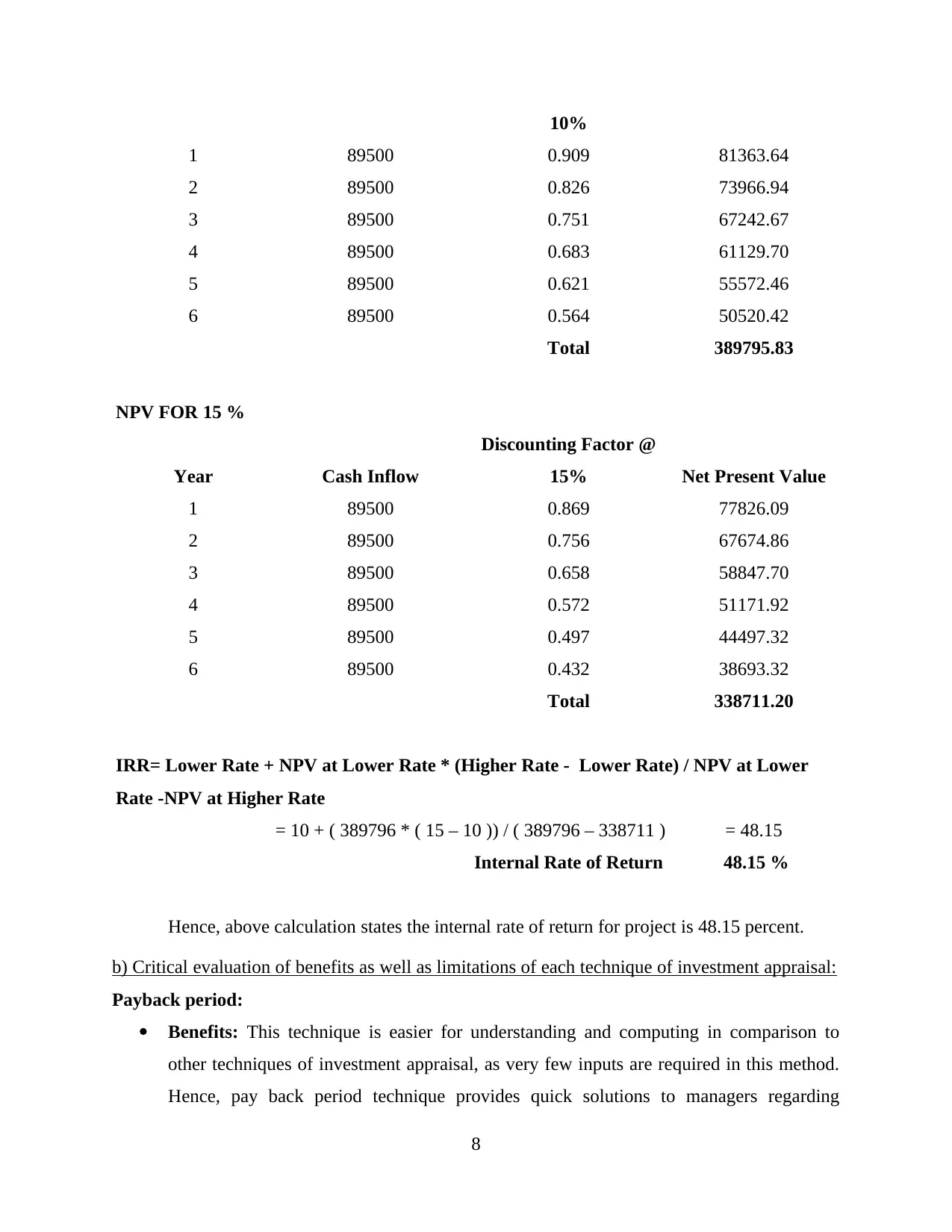

Cash outflow for the value of the machine purchased is 320000

Lets assume, Lower Discount Rate 10 %

Higher Discount Rate 15 %

NPV FOR 10 %

Year Cash Inflow Discounting Factor @ Net Present Value

7

Year Cash Inflow Discounting Factor @ 12% Net Cash Inflow

1 89500 0.892 79910.71

2 89500 0.797 71348.85

3 89500 0.711 63704.33

4 89500 0.635 56878.86

5 89500 0.567 50784.70

6 89500 0.506 45343.48

Total 367970.95

Net Present Value = Net Cash Inflow – Net Cash Outflow

= 367970.95 - 320000 47970.95

From the above calculation of net present value its is interpreted that proposal should be

adopted because net present value of an organization is positive, that is, 367970.95.

Internal rate of return: Financial metric of internal rate of return is applied for

estimation of profitability that is associated with potential investments. In this technique, IRR

refers to annual growth rate which is expected to be generated in an investment (Lopez and

Balabanis, 2020). It enables analysis of capital budgeting projects for understanding and

generating potential annual return rates over a period of time. Higher internal rate of return is

preferable in case of this technique.

Internal Rate of Return

Cash outflow for the value of the machine purchased is 320000

Lets assume, Lower Discount Rate 10 %

Higher Discount Rate 15 %

NPV FOR 10 %

Year Cash Inflow Discounting Factor @ Net Present Value

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10%

1 89500 0.909 81363.64

2 89500 0.826 73966.94

3 89500 0.751 67242.67

4 89500 0.683 61129.70

5 89500 0.621 55572.46

6 89500 0.564 50520.42

Total 389795.83

NPV FOR 15 %

Year Cash Inflow

Discounting Factor @

15% Net Present Value

1 89500 0.869 77826.09

2 89500 0.756 67674.86

3 89500 0.658 58847.70

4 89500 0.572 51171.92

5 89500 0.497 44497.32

6 89500 0.432 38693.32

Total 338711.20

IRR= Lower Rate + NPV at Lower Rate * (Higher Rate - Lower Rate) / NPV at Lower

Rate -NPV at Higher Rate

= 10 + ( 389796 * ( 15 – 10 )) / ( 389796 – 338711 ) = 48.15

Internal Rate of Return 48.15 %

Hence, above calculation states the internal rate of return for project is 48.15 percent.

b) Critical evaluation of benefits as well as limitations of each technique of investment appraisal:

Payback period:

Benefits: This technique is easier for understanding and computing in comparison to

other techniques of investment appraisal, as very few inputs are required in this method.

Hence, pay back period technique provides quick solutions to managers regarding

8

1 89500 0.909 81363.64

2 89500 0.826 73966.94

3 89500 0.751 67242.67

4 89500 0.683 61129.70

5 89500 0.621 55572.46

6 89500 0.564 50520.42

Total 389795.83

NPV FOR 15 %

Year Cash Inflow

Discounting Factor @

15% Net Present Value

1 89500 0.869 77826.09

2 89500 0.756 67674.86

3 89500 0.658 58847.70

4 89500 0.572 51171.92

5 89500 0.497 44497.32

6 89500 0.432 38693.32

Total 338711.20

IRR= Lower Rate + NPV at Lower Rate * (Higher Rate - Lower Rate) / NPV at Lower

Rate -NPV at Higher Rate

= 10 + ( 389796 * ( 15 – 10 )) / ( 389796 – 338711 ) = 48.15

Internal Rate of Return 48.15 %

Hence, above calculation states the internal rate of return for project is 48.15 percent.

b) Critical evaluation of benefits as well as limitations of each technique of investment appraisal:

Payback period:

Benefits: This technique is easier for understanding and computing in comparison to

other techniques of investment appraisal, as very few inputs are required in this method.

Hence, pay back period technique provides quick solutions to managers regarding

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decision making of best suited project for investment. It provides crucial information to

decision makers in context to time period of return that is provided by project. It enables

businesses which prefer liquidity to evaluate cost of investment and time period of its

recovery. This information is crucial for organizations that are small and pertains limited

resources (Turnock, 2017). It is most suitable for industries that incorporate with rapid

changes in technology or operates in uncertain environment, as it is difficult to project

future inflows of cash in such uncertain business environment.

Limitations: One of the major disadvantage associated with technique of pay back period

is that time value of money is ignored during its computation. Apart from this, flow of

cash is considered till the time period of recovery of initial investment, hence, cash flow

that is generated after initial investment recovery is ignored. It pertains no guarantee on

profitability of project and return on investment is also ignored. This technique

sometimes provide unrealistic results as normal business scenarios are not considered.

Accounting rate of return:

Benefits: While considering benefits of accounting rate of return technique of investment

appraisal it can be stated that, it is simple tool which is widely used and understood. It

enables evaluation of actual profitability in context to investment in project because it

considers revenues as well as costs that is associated with investment. Basis of this

technique is accounting information of business hence, there is no requirement of another

special reports (Beare, Caldwell and Millikan, 2018). It measures profitability factor of

an investment as its basis is accounting profit. It facilitates quick decision making as

project that pertains comparatively higher accounting rate of return is selected.

Limitations: Time value of money is not taken into account in this method. Apart from

this, cash flow is also ignored while computing accounting rate of return. It is not

necessary that ARR remains constant over entire life of project, hence, fair return cannot

be evaluated. External factors which affect profitability of project is not considering in

this technique and along with it, life time period of various projects is not taken into

consideration.

Net present value:

Benefits: Primary advantage of net present value is that it evaluates time factor during

computation. It considers discounted cash flow of an investment which facilitates

9

decision makers in context to time period of return that is provided by project. It enables

businesses which prefer liquidity to evaluate cost of investment and time period of its

recovery. This information is crucial for organizations that are small and pertains limited

resources (Turnock, 2017). It is most suitable for industries that incorporate with rapid

changes in technology or operates in uncertain environment, as it is difficult to project

future inflows of cash in such uncertain business environment.

Limitations: One of the major disadvantage associated with technique of pay back period

is that time value of money is ignored during its computation. Apart from this, flow of

cash is considered till the time period of recovery of initial investment, hence, cash flow

that is generated after initial investment recovery is ignored. It pertains no guarantee on

profitability of project and return on investment is also ignored. This technique

sometimes provide unrealistic results as normal business scenarios are not considered.

Accounting rate of return:

Benefits: While considering benefits of accounting rate of return technique of investment

appraisal it can be stated that, it is simple tool which is widely used and understood. It

enables evaluation of actual profitability in context to investment in project because it

considers revenues as well as costs that is associated with investment. Basis of this

technique is accounting information of business hence, there is no requirement of another

special reports (Beare, Caldwell and Millikan, 2018). It measures profitability factor of

an investment as its basis is accounting profit. It facilitates quick decision making as

project that pertains comparatively higher accounting rate of return is selected.

Limitations: Time value of money is not taken into account in this method. Apart from

this, cash flow is also ignored while computing accounting rate of return. It is not

necessary that ARR remains constant over entire life of project, hence, fair return cannot

be evaluated. External factors which affect profitability of project is not considering in

this technique and along with it, life time period of various projects is not taken into

consideration.

Net present value:

Benefits: Primary advantage of net present value is that it evaluates time factor during

computation. It considers discounted cash flow of an investment which facilitates

9

determination of viability of a project. Apart from this, technique of net present value

ensures formulation of better strategies regarding investments by evaluating size and risk

associated with projects. It ensures enhancement of profitability of business (Oyigbo and

Ugwu, 2017).

Limitations: Determination of opportunity cost becomes a critical task in this technique

as initial outlay is underestimated in it. Along with it, sunk cost is also ignored in the

technique of accounting rate of return. It can lead to misleading of information as cost

can be selected as per convenience. This technique is helpful in comparison of projects

that are of small size but it is not suitable for comparison of large size projects. Further,

identification of appropriate discounting rate for representation of actual risk premium for

investment comes up as a challenge.

Internal rate of return:

Benefits: Foremost benefit associated with computation of internal rate of return is that

time value of money is taken into consideration in this method. Required return rate or

hurdle rate is not needed while calculating IRR, hence, it is simple for interpretation and

even it neglects risk of misleading results. No particular basis or criteria is there for

selection of internal rate of return, hence, uniform ranking system is there (Knoblauch

and Trutnevyte, 2018). Importance is provided to cash flows in this technique whether

that cash is earned currently or later (Chen, Li and Sun, 2020).

Limitations: Computation of internal rate of return ignores economies of scale. Size as

well as scope of investment projects are ignored in this method. It also incorporates some

unrealistic assumptions , such as, reinvestment future cash flow at similar rate of internal

rate of return. For computation of more than two projects, this technique of capital

budgeting is not appropriate. It only compares the cash amount which is generated and

focuses on projected cash flows only, as potential costs associated with projects and its

impact on profitability of an enterprise is totally ignored.

CONCLUSION

From the above report it can be concluded that financial management is an essential

activity of an enterprise that incorporates procedure of planning, organizing and controlling of

financial resources of business with the motive of achieving its goals or objectives. Aim of

financial management is to effective utilise available capital funds in business which is its

10

ensures formulation of better strategies regarding investments by evaluating size and risk

associated with projects. It ensures enhancement of profitability of business (Oyigbo and

Ugwu, 2017).

Limitations: Determination of opportunity cost becomes a critical task in this technique

as initial outlay is underestimated in it. Along with it, sunk cost is also ignored in the

technique of accounting rate of return. It can lead to misleading of information as cost

can be selected as per convenience. This technique is helpful in comparison of projects

that are of small size but it is not suitable for comparison of large size projects. Further,

identification of appropriate discounting rate for representation of actual risk premium for

investment comes up as a challenge.

Internal rate of return:

Benefits: Foremost benefit associated with computation of internal rate of return is that

time value of money is taken into consideration in this method. Required return rate or

hurdle rate is not needed while calculating IRR, hence, it is simple for interpretation and

even it neglects risk of misleading results. No particular basis or criteria is there for

selection of internal rate of return, hence, uniform ranking system is there (Knoblauch

and Trutnevyte, 2018). Importance is provided to cash flows in this technique whether

that cash is earned currently or later (Chen, Li and Sun, 2020).

Limitations: Computation of internal rate of return ignores economies of scale. Size as

well as scope of investment projects are ignored in this method. It also incorporates some

unrealistic assumptions , such as, reinvestment future cash flow at similar rate of internal

rate of return. For computation of more than two projects, this technique of capital

budgeting is not appropriate. It only compares the cash amount which is generated and

focuses on projected cash flows only, as potential costs associated with projects and its

impact on profitability of an enterprise is totally ignored.

CONCLUSION

From the above report it can be concluded that financial management is an essential

activity of an enterprise that incorporates procedure of planning, organizing and controlling of

financial resources of business with the motive of achieving its goals or objectives. Aim of

financial management is to effective utilise available capital funds in business which is its

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

essential economic resource. It can be examined as an activity that is incorporated by finance

manager of company for reducing cost that is incurred in it ans ensuring high fund availability.

Apart from it, this report interprets that equity financing leads to finance expansion and it plays

a critical role in growth or expansion of an organization. Cash dividend and equivalent scrip

dividend are two types of methods which can be utilised for paying dividend to shareholders.

Further, investment appraisal techniques is applied for deciding on appropriate project for

investment. Net present value, internal rate of return, payback period and average rate of return

are some techniques which is utilised for investment appraisal.

11

manager of company for reducing cost that is incurred in it ans ensuring high fund availability.

Apart from it, this report interprets that equity financing leads to finance expansion and it plays

a critical role in growth or expansion of an organization. Cash dividend and equivalent scrip

dividend are two types of methods which can be utilised for paying dividend to shareholders.

Further, investment appraisal techniques is applied for deciding on appropriate project for

investment. Net present value, internal rate of return, payback period and average rate of return

are some techniques which is utilised for investment appraisal.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals:

Beare, H., Caldwell, B. J. and Millikan, R. H., 2018. Creating an excellent school: Some new

management techniques. Routledge.

Chen, Z., Li, C. and Sun, W., 2020. Bitcoin price prediction using machine learning: An

approach to sample dimension engineering. Journal of Computational and Applied

Mathematics. 365. p.112395.

Gertler, M., Kiyotaki, N. and Prestipino, A., 2020. A macroeconomic model with financial

panics. The Review of Economic Studies. 87(1). pp.240-288.

Knoblauch, T. A. and Trutnevyte, E., 2018. Siting enhanced geothermal systems (EGS): Heat

benefits versus induced seismicity risks from an investor and societal

perspective. Energy. 164. pp.1311-1325.

Lin, L., 2017. Managing the risks of equity crowdfunding: lessons from China. Journal of

Corporate Law Studies. 17(2). pp.327-366.

Lopez, C. and Balabanis, G., 2020. Country image appraisal: More than just ticking

boxes. Journal of Business Research. 117. pp.764-779.

Owen, R., Brennan, G. and Lyon, F., 2018. Enabling investment for the transition to a low

carbon economy: government policy to finance early stage green innovation. Current

Opinion in Environmental Sustainability. 31. pp.137-145.

Oyigbo, T. E. and Ugwu, O. O., 2017. Appraisal of key performance indicators on road

infrastructure financed by public-private partnership in Nigeria. Nigerian Journal of

Technology. 36(4). pp.1049-1058.

Ross, J. M. and Mughan, S., 2018. The effect of fiscal Illusion on public sector financial

management: Evidence from local government property assessment. Public Finance

Review. 46(4). pp.635-664.

Roundy, P., Holzhauer, H. and Dai, Y., 2017. Finance or philanthropy? Exploring the

motivations and criteria of impact investors. Social Responsibility Journal.

Susan, M. and Djajadikerta, H., 2017. Understanding financial knowledge, financial attitude, and

financial behavior of college students in Indonesia. Advanced Science Letters. 23(9).

pp.8762-8765.

Tripathi, M., Kashiramka, S. and Jain, P. K., 2018. Flexibility in measuring corporate financial

performance, EVA versus conventional earnings measures: Evidences from India and

China. Global Journal of Flexible Systems Management. 19(2). pp.123-138.

Turnock, D. ed., 2017. Foreign direct investment and regional development in east central

Europe and the former Soviet Union: A collection of essays in memory of Professor

Francis' Frank'Carter. Routledge.

12

Books and journals:

Beare, H., Caldwell, B. J. and Millikan, R. H., 2018. Creating an excellent school: Some new

management techniques. Routledge.

Chen, Z., Li, C. and Sun, W., 2020. Bitcoin price prediction using machine learning: An

approach to sample dimension engineering. Journal of Computational and Applied

Mathematics. 365. p.112395.

Gertler, M., Kiyotaki, N. and Prestipino, A., 2020. A macroeconomic model with financial

panics. The Review of Economic Studies. 87(1). pp.240-288.

Knoblauch, T. A. and Trutnevyte, E., 2018. Siting enhanced geothermal systems (EGS): Heat

benefits versus induced seismicity risks from an investor and societal

perspective. Energy. 164. pp.1311-1325.

Lin, L., 2017. Managing the risks of equity crowdfunding: lessons from China. Journal of

Corporate Law Studies. 17(2). pp.327-366.

Lopez, C. and Balabanis, G., 2020. Country image appraisal: More than just ticking

boxes. Journal of Business Research. 117. pp.764-779.

Owen, R., Brennan, G. and Lyon, F., 2018. Enabling investment for the transition to a low

carbon economy: government policy to finance early stage green innovation. Current

Opinion in Environmental Sustainability. 31. pp.137-145.

Oyigbo, T. E. and Ugwu, O. O., 2017. Appraisal of key performance indicators on road

infrastructure financed by public-private partnership in Nigeria. Nigerian Journal of

Technology. 36(4). pp.1049-1058.

Ross, J. M. and Mughan, S., 2018. The effect of fiscal Illusion on public sector financial

management: Evidence from local government property assessment. Public Finance

Review. 46(4). pp.635-664.

Roundy, P., Holzhauer, H. and Dai, Y., 2017. Finance or philanthropy? Exploring the

motivations and criteria of impact investors. Social Responsibility Journal.

Susan, M. and Djajadikerta, H., 2017. Understanding financial knowledge, financial attitude, and

financial behavior of college students in Indonesia. Advanced Science Letters. 23(9).

pp.8762-8765.

Tripathi, M., Kashiramka, S. and Jain, P. K., 2018. Flexibility in measuring corporate financial

performance, EVA versus conventional earnings measures: Evidences from India and

China. Global Journal of Flexible Systems Management. 19(2). pp.123-138.

Turnock, D. ed., 2017. Foreign direct investment and regional development in east central

Europe and the former Soviet Union: A collection of essays in memory of Professor

Francis' Frank'Carter. Routledge.

12

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.