Applied Econometrics

VerifiedAdded on 2023/02/01

|34

|7312

|97

AI Summary

The paper aims to analyze the money demand function both in the short run and in the long run. The static money demand function has been estimated taking inflation rate, real GDP and interest rate. In order to analyze robustness of the model autocorrelation test has been performed for examining presence of serial correlation in the model. Condition in the short run however is different from that in the long run. In the long run, it is assumed that money demand function is not directly observable and difference between observed money supply tends to adjust towards the expected difference in money supply having certain speed of adjustment. In the long run inclusion of lagged dependent variables may result in the problem of endogeneity where independent variables are found to be related with the error term. In order to eliminate the problem of endogeneity the technique of instrumental variables is used through the estimation method of two stage least square. Each of the series has been tested for unit root by employing the Augmenyed Dicky Fuller test. Finally, Engel Granger test has been performed to examine cointegration among the variables. The money demand function and its associate determinants provide useful implication for policy formulation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: APPLIED ECONOMETRICS

Applied Econometrics

Name of the Student

Name of the University

Course ID

Applied Econometrics

Name of the Student

Name of the University

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1APPLIED ECONOMETRICS

Executive Summary

The paper aims to analyze the money demand function both in the short run and in the long run.

The static money demand function has been estimated taking inflation rate, real GDP and interest

rate. In order to analyze robustness of the model autocorrelation test has been performed for

examining presence of serial correlation in the model. Condition in the short run however is

different from that in the long run. In the long run, it is assumed that money demand function is

not directly observable and difference between observed money supply tends to adjust towards

the expected difference in money supply having certain speed of adjustment. In the long run

inclusion of lagged dependent variables may result in the problem of endogeneity where

independent variables are found to be related with the error term. In order to eliminate the

problem of endogeneity the technique of instrumental variables is used through the estimation

method of two stage least square. Each of the series has been tested for unit root by employing

the Augmenyed Dicky Fuller test. Finally, Engel Granger test has been performed to examine co-

integration among the variables. The money demand function and its associate determinants

provide useful implication for policy formulation.

Executive Summary

The paper aims to analyze the money demand function both in the short run and in the long run.

The static money demand function has been estimated taking inflation rate, real GDP and interest

rate. In order to analyze robustness of the model autocorrelation test has been performed for

examining presence of serial correlation in the model. Condition in the short run however is

different from that in the long run. In the long run, it is assumed that money demand function is

not directly observable and difference between observed money supply tends to adjust towards

the expected difference in money supply having certain speed of adjustment. In the long run

inclusion of lagged dependent variables may result in the problem of endogeneity where

independent variables are found to be related with the error term. In order to eliminate the

problem of endogeneity the technique of instrumental variables is used through the estimation

method of two stage least square. Each of the series has been tested for unit root by employing

the Augmenyed Dicky Fuller test. Finally, Engel Granger test has been performed to examine co-

integration among the variables. The money demand function and its associate determinants

provide useful implication for policy formulation.

2APPLIED ECONOMETRICS

Table of Contents

Question 1........................................................................................................................................4

Question 2........................................................................................................................................6

Question a....................................................................................................................................6

Question b....................................................................................................................................7

Question c....................................................................................................................................8

Question 3........................................................................................................................................8

Question a....................................................................................................................................8

Question b....................................................................................................................................9

Question 4......................................................................................................................................10

Question a..................................................................................................................................10

Question b..................................................................................................................................12

Question c..................................................................................................................................12

Question 5......................................................................................................................................13

Question a..................................................................................................................................13

Question b..................................................................................................................................13

Question c..................................................................................................................................13

Question d..................................................................................................................................13

Question 6......................................................................................................................................14

Question 7......................................................................................................................................15

Table of Contents

Question 1........................................................................................................................................4

Question 2........................................................................................................................................6

Question a....................................................................................................................................6

Question b....................................................................................................................................7

Question c....................................................................................................................................8

Question 3........................................................................................................................................8

Question a....................................................................................................................................8

Question b....................................................................................................................................9

Question 4......................................................................................................................................10

Question a..................................................................................................................................10

Question b..................................................................................................................................12

Question c..................................................................................................................................12

Question 5......................................................................................................................................13

Question a..................................................................................................................................13

Question b..................................................................................................................................13

Question c..................................................................................................................................13

Question d..................................................................................................................................13

Question 6......................................................................................................................................14

Question 7......................................................................................................................................15

3APPLIED ECONOMETRICS

Question a..................................................................................................................................15

Question b..................................................................................................................................15

Question c..................................................................................................................................15

Question 8......................................................................................................................................15

Question a..................................................................................................................................15

Question b..................................................................................................................................16

Question c..................................................................................................................................16

Question 9......................................................................................................................................16

Question a..................................................................................................................................16

Question b..................................................................................................................................18

Question c..................................................................................................................................18

Question 10....................................................................................................................................18

References and Bibliography.........................................................................................................20

Appendix........................................................................................................................................22

Question a..................................................................................................................................15

Question b..................................................................................................................................15

Question c..................................................................................................................................15

Question 8......................................................................................................................................15

Question a..................................................................................................................................15

Question b..................................................................................................................................16

Question c..................................................................................................................................16

Question 9......................................................................................................................................16

Question a..................................................................................................................................16

Question b..................................................................................................................................18

Question c..................................................................................................................................18

Question 10....................................................................................................................................18

References and Bibliography.........................................................................................................20

Appendix........................................................................................................................................22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4APPLIED ECONOMETRICS

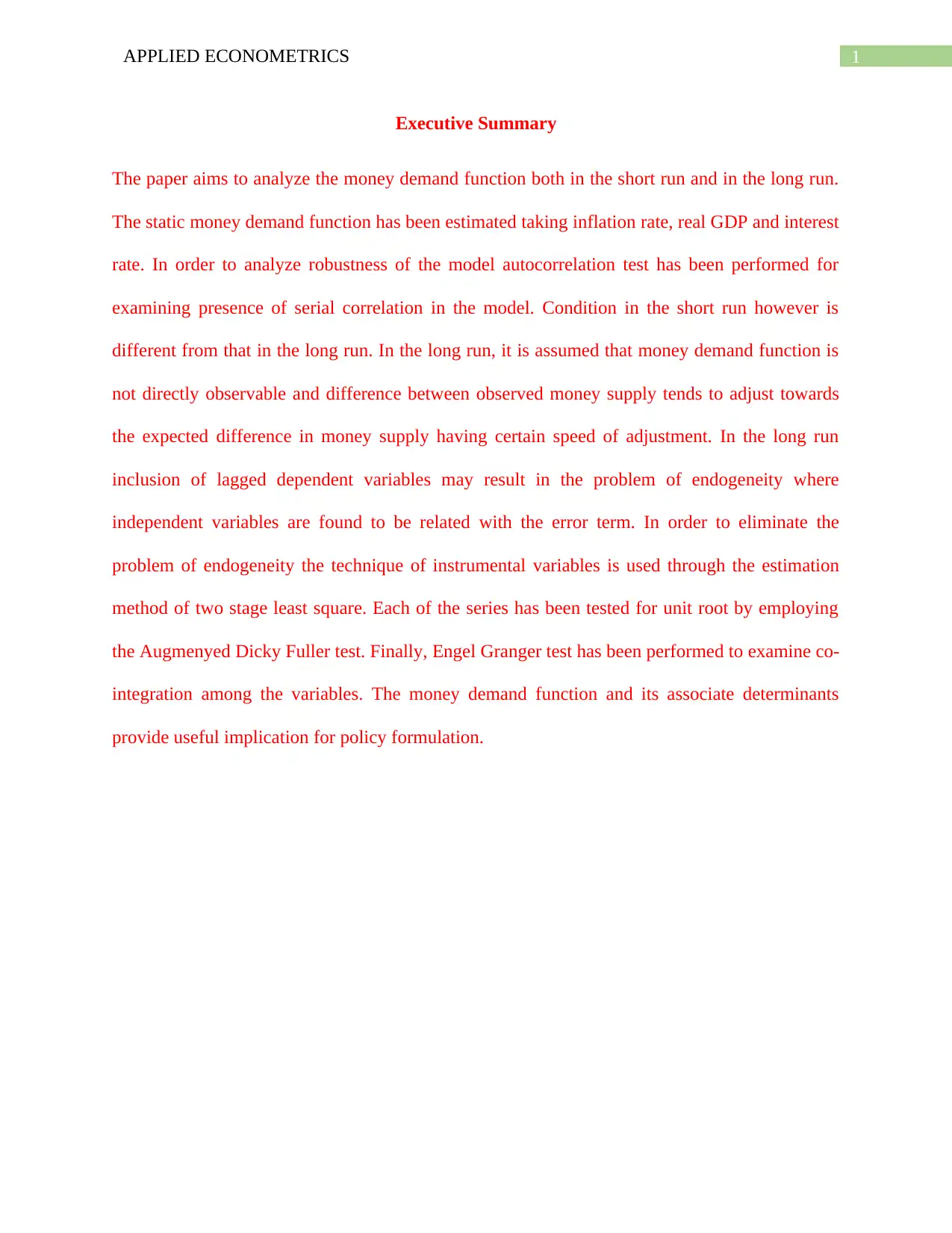

Question 1

Figure 1: Dynamic trend of inflation rate

The inflation series is highly volatile. The series initially increases, reaches peak and then

again declines. Most of the times, inflation rate varies between 0.01 to 0.02 percent.

Question 1

Figure 1: Dynamic trend of inflation rate

The inflation series is highly volatile. The series initially increases, reaches peak and then

again declines. Most of the times, inflation rate varies between 0.01 to 0.02 percent.

5APPLIED ECONOMETRICS

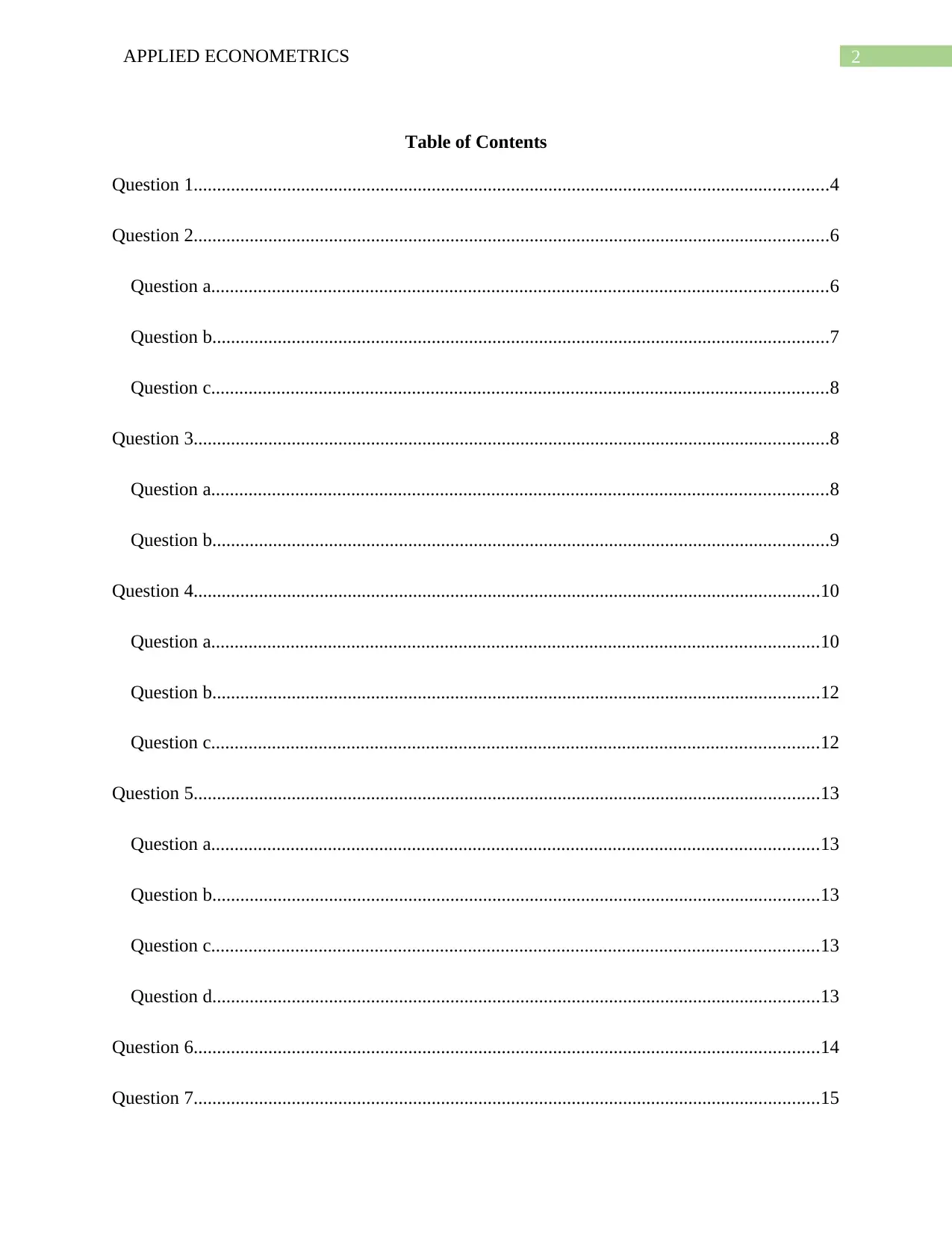

Figure 2: Dynamic trend in interest rate

Like inflation series, the series of interest rate also shows dynamic fluctuating trend.

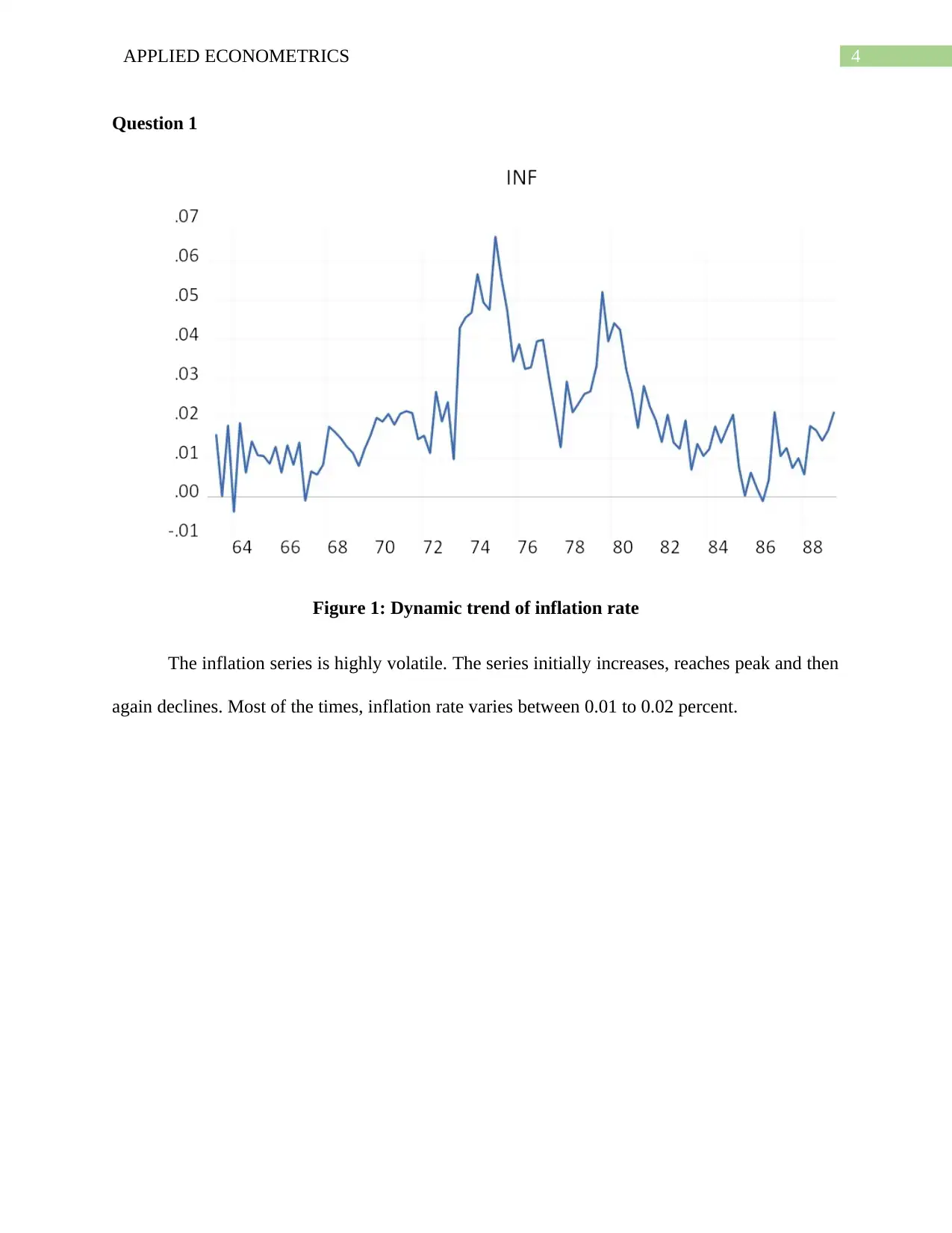

Figure 3: Dynamic trend in real GDP

Figure 2: Dynamic trend in interest rate

Like inflation series, the series of interest rate also shows dynamic fluctuating trend.

Figure 3: Dynamic trend in real GDP

6APPLIED ECONOMETRICS

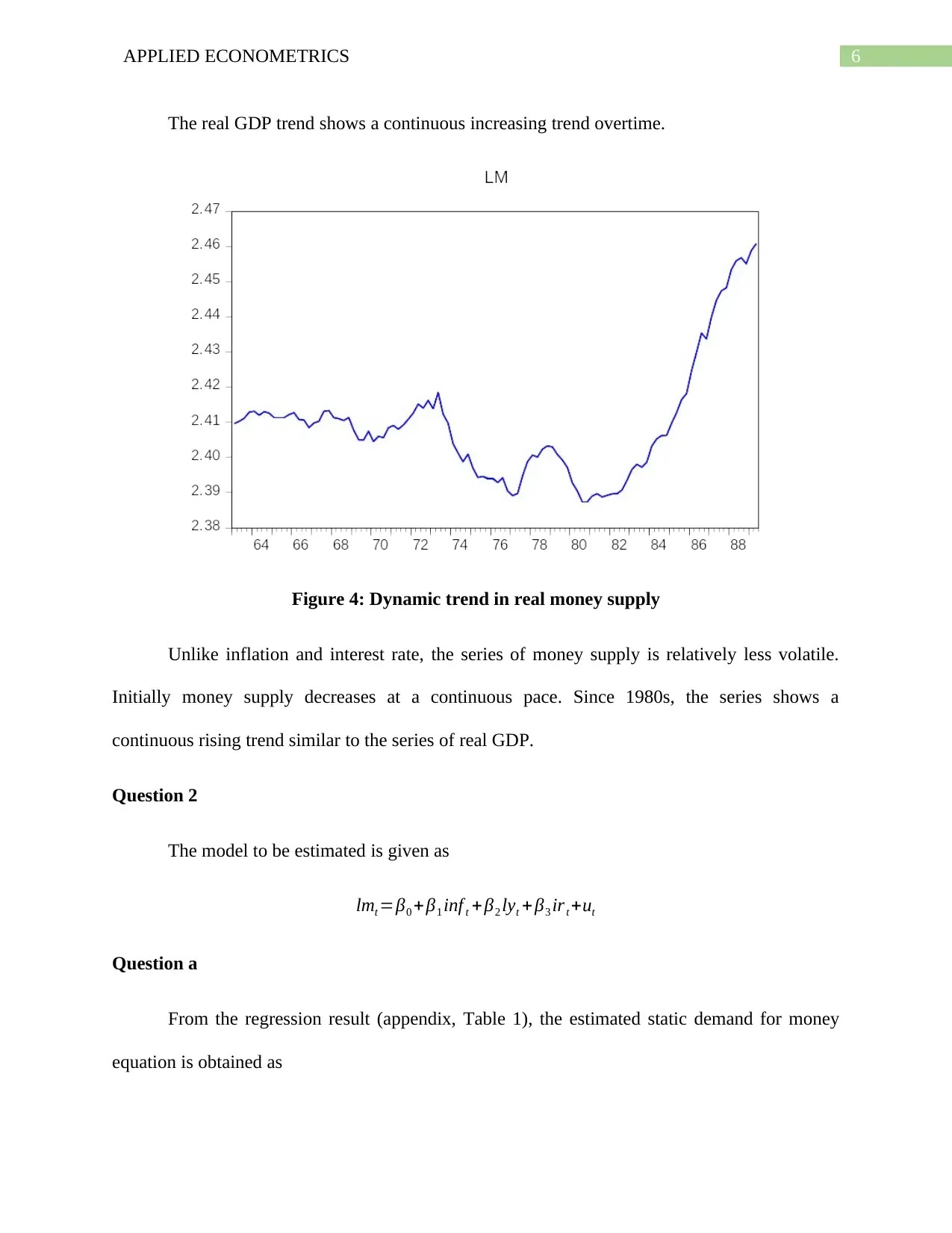

The real GDP trend shows a continuous increasing trend overtime.

Figure 4: Dynamic trend in real money supply

Unlike inflation and interest rate, the series of money supply is relatively less volatile.

Initially money supply decreases at a continuous pace. Since 1980s, the series shows a

continuous rising trend similar to the series of real GDP.

Question 2

The model to be estimated is given as

lmt =β0 +β1 inf t +β2 lyt +β3 irt +ut

Question a

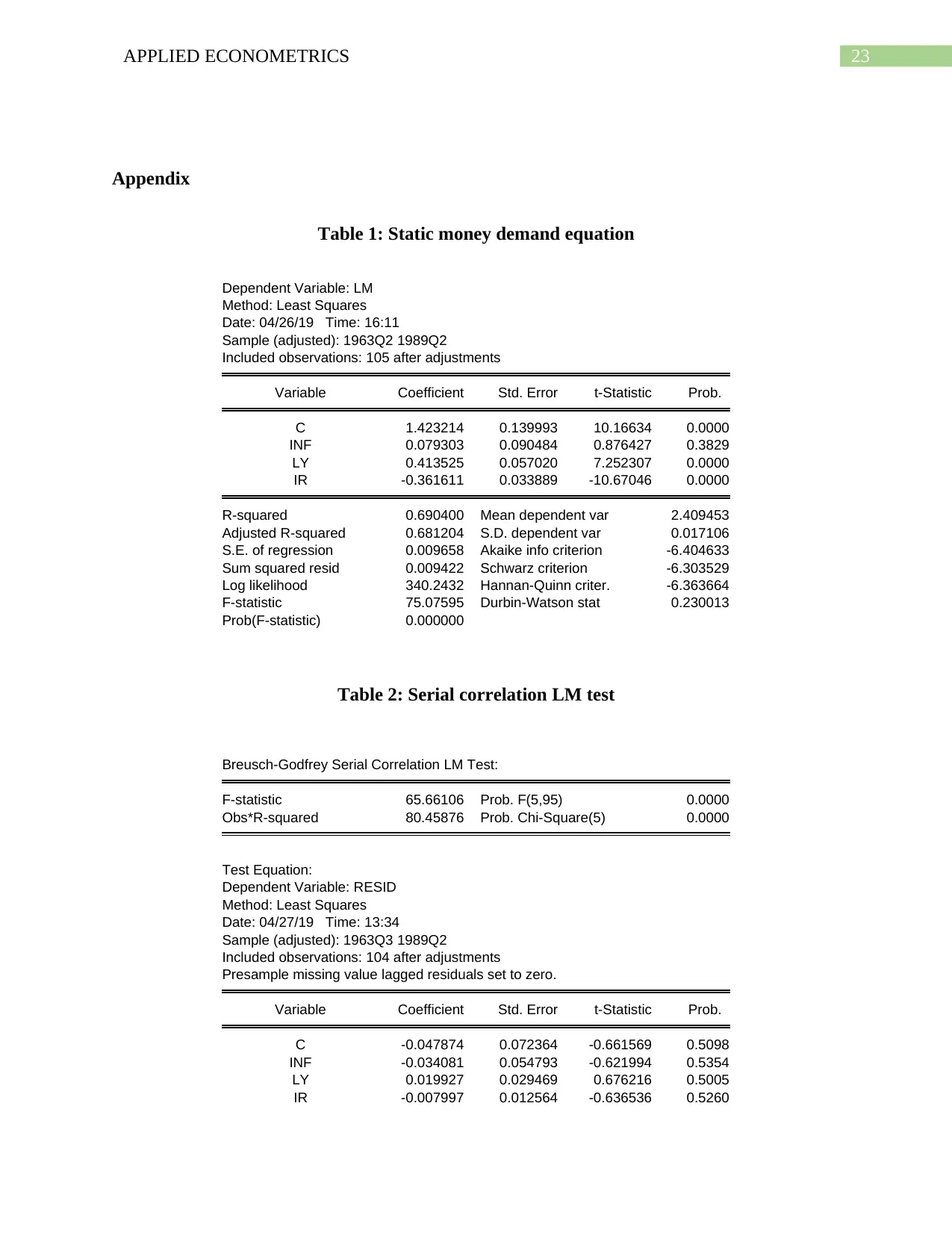

From the regression result (appendix, Table 1), the estimated static demand for money

equation is obtained as

The real GDP trend shows a continuous increasing trend overtime.

Figure 4: Dynamic trend in real money supply

Unlike inflation and interest rate, the series of money supply is relatively less volatile.

Initially money supply decreases at a continuous pace. Since 1980s, the series shows a

continuous rising trend similar to the series of real GDP.

Question 2

The model to be estimated is given as

lmt =β0 +β1 inf t +β2 lyt +β3 irt +ut

Question a

From the regression result (appendix, Table 1), the estimated static demand for money

equation is obtained as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7APPLIED ECONOMETRICS

lmt =1.423214+0.079303inf t +0.0413525 lyt −0.361611 irt

Question b

From the estimated static demand equation, the constant is obtained as 1.423214. The

constant implies slope of the money demand curve. That is all other variables influencing money

demand and such as inflation, real GDP and interest rate are zero, then money demand in the

economy is 1.423214. The coefficient associated with inflation rate is 0.0799303. The positive

value of inflation coefficient means that inflation has a positive relation with money demand

(Johnson 2017, pp. 121-128). That is higher the inflation, higher is the money demand and vice-

versa. More precisely, for 10 percent increase in inflation rate, log of real money balance

increases by 0.7 percent. This is consistent with expectation because during high inflation people

require more money to purchase goods and services increasing demand for money. For real

GDP, the estimated coefficient is 0.0413525. This implies real GDP is again positively

associated with money supply. From the coefficient estimate, it can be said that 10 percent

increase in log real GDP increases money demand by 0.04 percent. Increase in GDP thus

increase money supply and vice versa. A higher GDP implies a higher average income for

people. With increases in income people demand more money. The finding thus is consistent

with expectation. In case of interest rate, the associated coefficient is - -0.361611. The negative

coefficient suggests an inverse association with money demand and interest rate. That is money

demand increase with a decrease in interest rate. This is expected as interest rate is the cost of

holding money and hence is inversely associated with demand for money (Gan 2019).

lmt =1.423214+0.079303inf t +0.0413525 lyt −0.361611 irt

Question b

From the estimated static demand equation, the constant is obtained as 1.423214. The

constant implies slope of the money demand curve. That is all other variables influencing money

demand and such as inflation, real GDP and interest rate are zero, then money demand in the

economy is 1.423214. The coefficient associated with inflation rate is 0.0799303. The positive

value of inflation coefficient means that inflation has a positive relation with money demand

(Johnson 2017, pp. 121-128). That is higher the inflation, higher is the money demand and vice-

versa. More precisely, for 10 percent increase in inflation rate, log of real money balance

increases by 0.7 percent. This is consistent with expectation because during high inflation people

require more money to purchase goods and services increasing demand for money. For real

GDP, the estimated coefficient is 0.0413525. This implies real GDP is again positively

associated with money supply. From the coefficient estimate, it can be said that 10 percent

increase in log real GDP increases money demand by 0.04 percent. Increase in GDP thus

increase money supply and vice versa. A higher GDP implies a higher average income for

people. With increases in income people demand more money. The finding thus is consistent

with expectation. In case of interest rate, the associated coefficient is - -0.361611. The negative

coefficient suggests an inverse association with money demand and interest rate. That is money

demand increase with a decrease in interest rate. This is expected as interest rate is the cost of

holding money and hence is inversely associated with demand for money (Gan 2019).

8APPLIED ECONOMETRICS

Question c

Computed ‘t’ value for inflation rate 0.8764. The critical t value at 5% level of

significance and 101 degrees of freedom is 1.9837. As the absolute value of computed t is less

than the critical t, null hypothesis for no significant relation between inflation and money

demand is accepted. The independent variable, inflation thus is not statistically significant.

Associated p value for the coefficient is 0.3829. The p value exceeds the value of 5%

significance level again implying acceptance of null hypothesis of no significant relation

between dependent and independent variable. The proposed association between inflation and

money demand thus is not statistically significant. The proposed association between real GDP

and money demand thus is statistically significant as the computed t exceeds the critical t and p

value is smaller than the significance level. In case of interest rate a statistically significant but

negative association is obtained between money demand and interest rate.

Question 3

Question a

The joint significance test for the regression model can be performed using the F test. The

null and alternative hypotheses for the test are given as follows.

Null hypothesis: β1 = β2= β3 = 0

Alternative hypothesis: At least any of the β’s is not equal to zero.

The computed F value of the model is 75.07595. The critical F value at 5 percent level of

significance and (3, 101) degrees of freedom is 2.6946. The computed F value exceeds the

critical F value at 5 percent level of significance implying rejection of null hypothesis stating all

Question c

Computed ‘t’ value for inflation rate 0.8764. The critical t value at 5% level of

significance and 101 degrees of freedom is 1.9837. As the absolute value of computed t is less

than the critical t, null hypothesis for no significant relation between inflation and money

demand is accepted. The independent variable, inflation thus is not statistically significant.

Associated p value for the coefficient is 0.3829. The p value exceeds the value of 5%

significance level again implying acceptance of null hypothesis of no significant relation

between dependent and independent variable. The proposed association between inflation and

money demand thus is not statistically significant. The proposed association between real GDP

and money demand thus is statistically significant as the computed t exceeds the critical t and p

value is smaller than the significance level. In case of interest rate a statistically significant but

negative association is obtained between money demand and interest rate.

Question 3

Question a

The joint significance test for the regression model can be performed using the F test. The

null and alternative hypotheses for the test are given as follows.

Null hypothesis: β1 = β2= β3 = 0

Alternative hypothesis: At least any of the β’s is not equal to zero.

The computed F value of the model is 75.07595. The critical F value at 5 percent level of

significance and (3, 101) degrees of freedom is 2.6946. The computed F value exceeds the

critical F value at 5 percent level of significance implying rejection of null hypothesis stating all

9APPLIED ECONOMETRICS

coefficients are zero. This can therefore be said that at least one of the coefficient is significantly

different from zero and hence, the model is jointly significant. The result is again supported by

the p value test. Associated p value for the F statistics is 0.0000. As the p value is less than

significance value of 0.05, the null hypothesis stating that the overall model is insignificant is

rejected. The independent variables in the model thus are jointly significant.

Question b

In multiple regression model adjusted R square is used as a measure of goodness of fit.

The obtained value of adjusted R square is 0.6812. The value indicates that inflation, real GDP

and interest rate can together explain 68 percent variation of the dependent variables. As the

independent variables account a considerably higher variability of the dependent variable, the

model is a good fit model.

coefficients are zero. This can therefore be said that at least one of the coefficient is significantly

different from zero and hence, the model is jointly significant. The result is again supported by

the p value test. Associated p value for the F statistics is 0.0000. As the p value is less than

significance value of 0.05, the null hypothesis stating that the overall model is insignificant is

rejected. The independent variables in the model thus are jointly significant.

Question b

In multiple regression model adjusted R square is used as a measure of goodness of fit.

The obtained value of adjusted R square is 0.6812. The value indicates that inflation, real GDP

and interest rate can together explain 68 percent variation of the dependent variables. As the

independent variables account a considerably higher variability of the dependent variable, the

model is a good fit model.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10APPLIED ECONOMETRICS

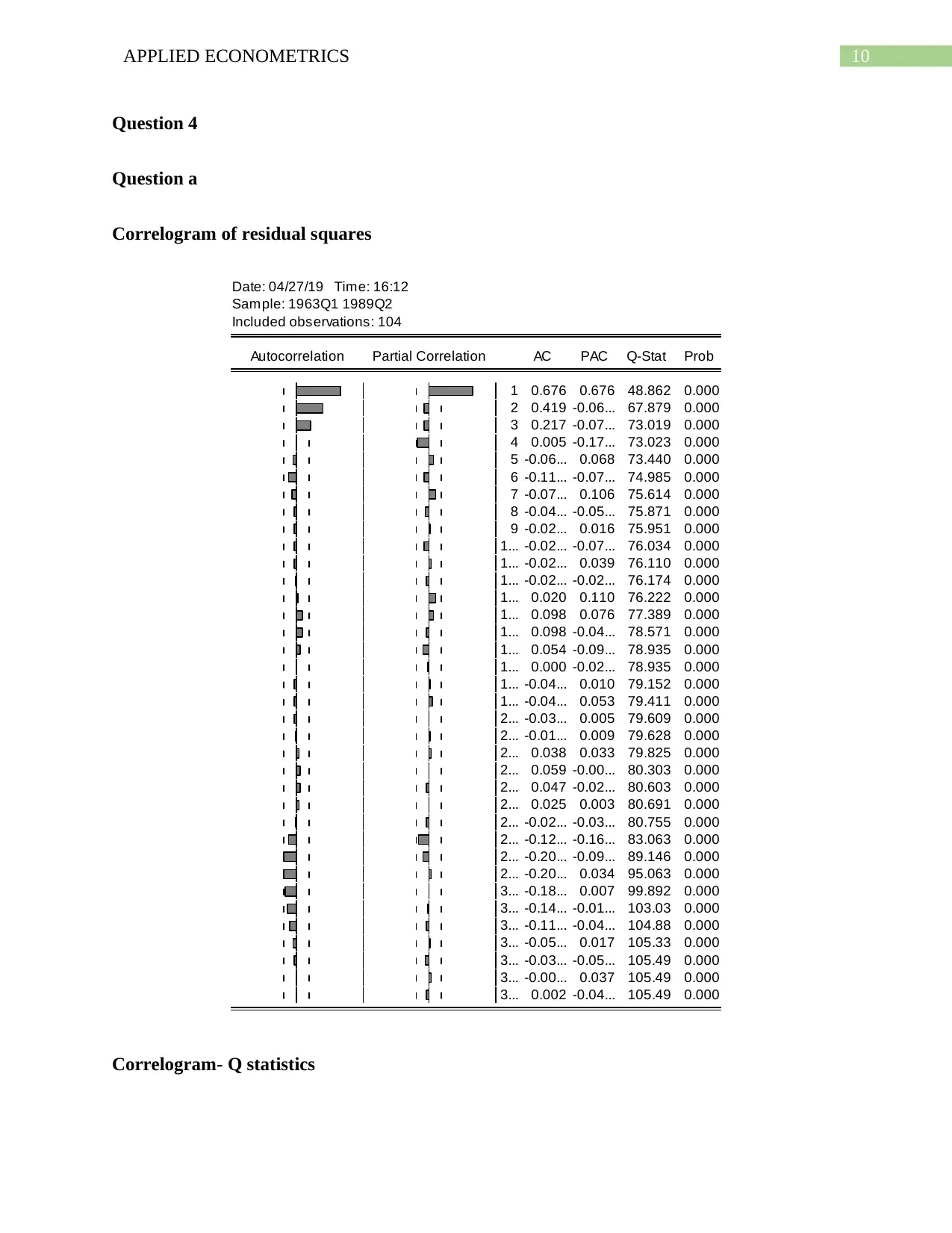

Question 4

Question a

Correlogram of residual squares

Date: 04/27/19 Time: 16:12

Sample: 1963Q1 1989Q2

Included observations: 104

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

1 0.676 0.676 48.862 0.000

2 0.419 -0.06... 67.879 0.000

3 0.217 -0.07... 73.019 0.000

4 0.005 -0.17... 73.023 0.000

5 -0.06... 0.068 73.440 0.000

6 -0.11... -0.07... 74.985 0.000

7 -0.07... 0.106 75.614 0.000

8 -0.04... -0.05... 75.871 0.000

9 -0.02... 0.016 75.951 0.000

1... -0.02... -0.07... 76.034 0.000

1... -0.02... 0.039 76.110 0.000

1... -0.02... -0.02... 76.174 0.000

1... 0.020 0.110 76.222 0.000

1... 0.098 0.076 77.389 0.000

1... 0.098 -0.04... 78.571 0.000

1... 0.054 -0.09... 78.935 0.000

1... 0.000 -0.02... 78.935 0.000

1... -0.04... 0.010 79.152 0.000

1... -0.04... 0.053 79.411 0.000

2... -0.03... 0.005 79.609 0.000

2... -0.01... 0.009 79.628 0.000

2... 0.038 0.033 79.825 0.000

2... 0.059 -0.00... 80.303 0.000

2... 0.047 -0.02... 80.603 0.000

2... 0.025 0.003 80.691 0.000

2... -0.02... -0.03... 80.755 0.000

2... -0.12... -0.16... 83.063 0.000

2... -0.20... -0.09... 89.146 0.000

2... -0.20... 0.034 95.063 0.000

3... -0.18... 0.007 99.892 0.000

3... -0.14... -0.01... 103.03 0.000

3... -0.11... -0.04... 104.88 0.000

3... -0.05... 0.017 105.33 0.000

3... -0.03... -0.05... 105.49 0.000

3... -0.00... 0.037 105.49 0.000

3... 0.002 -0.04... 105.49 0.000

Correlogram- Q statistics

Question 4

Question a

Correlogram of residual squares

Date: 04/27/19 Time: 16:12

Sample: 1963Q1 1989Q2

Included observations: 104

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

1 0.676 0.676 48.862 0.000

2 0.419 -0.06... 67.879 0.000

3 0.217 -0.07... 73.019 0.000

4 0.005 -0.17... 73.023 0.000

5 -0.06... 0.068 73.440 0.000

6 -0.11... -0.07... 74.985 0.000

7 -0.07... 0.106 75.614 0.000

8 -0.04... -0.05... 75.871 0.000

9 -0.02... 0.016 75.951 0.000

1... -0.02... -0.07... 76.034 0.000

1... -0.02... 0.039 76.110 0.000

1... -0.02... -0.02... 76.174 0.000

1... 0.020 0.110 76.222 0.000

1... 0.098 0.076 77.389 0.000

1... 0.098 -0.04... 78.571 0.000

1... 0.054 -0.09... 78.935 0.000

1... 0.000 -0.02... 78.935 0.000

1... -0.04... 0.010 79.152 0.000

1... -0.04... 0.053 79.411 0.000

2... -0.03... 0.005 79.609 0.000

2... -0.01... 0.009 79.628 0.000

2... 0.038 0.033 79.825 0.000

2... 0.059 -0.00... 80.303 0.000

2... 0.047 -0.02... 80.603 0.000

2... 0.025 0.003 80.691 0.000

2... -0.02... -0.03... 80.755 0.000

2... -0.12... -0.16... 83.063 0.000

2... -0.20... -0.09... 89.146 0.000

2... -0.20... 0.034 95.063 0.000

3... -0.18... 0.007 99.892 0.000

3... -0.14... -0.01... 103.03 0.000

3... -0.11... -0.04... 104.88 0.000

3... -0.05... 0.017 105.33 0.000

3... -0.03... -0.05... 105.49 0.000

3... -0.00... 0.037 105.49 0.000

3... 0.002 -0.04... 105.49 0.000

Correlogram- Q statistics

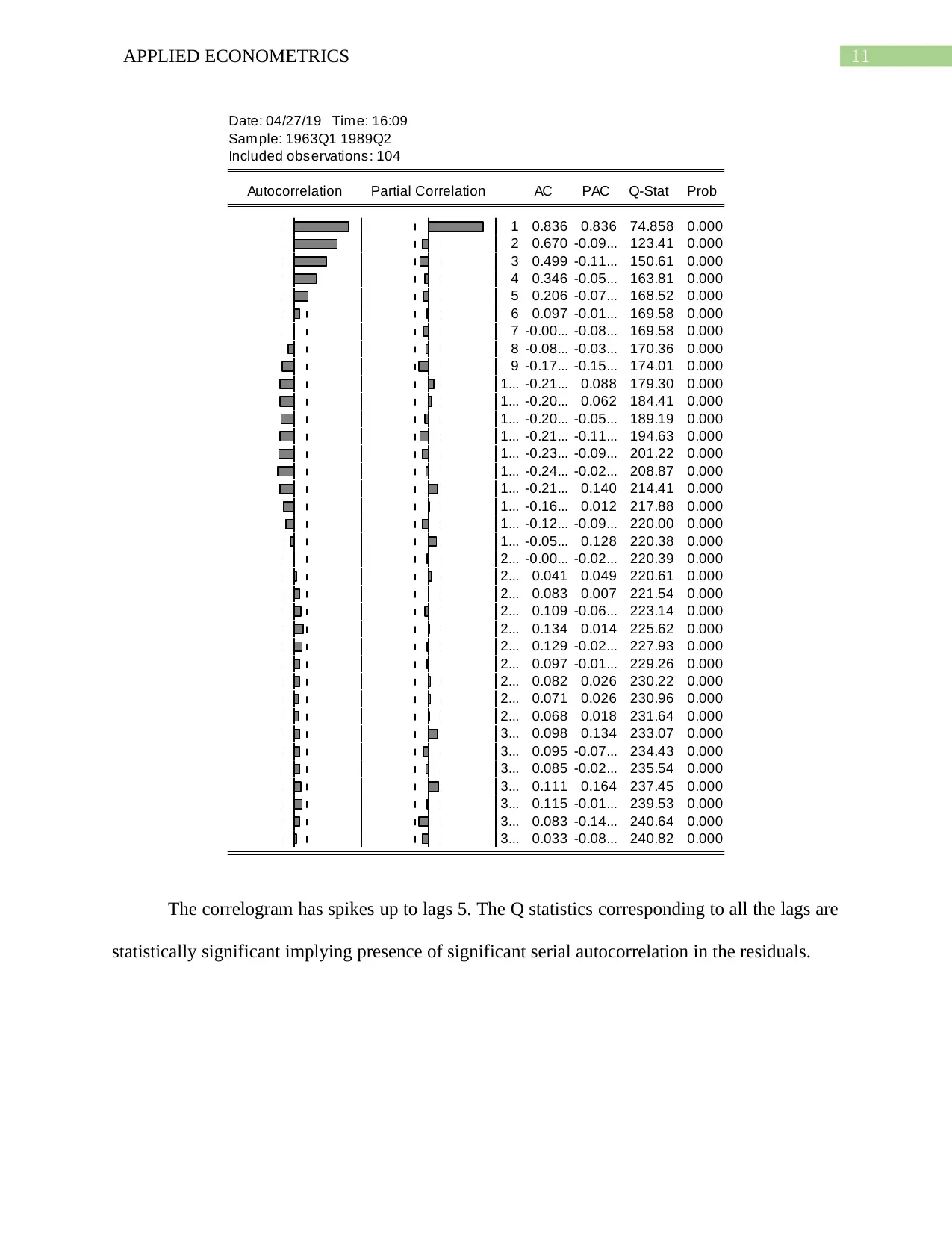

11APPLIED ECONOMETRICS

Date: 04/27/19 Time: 16:09

Sample: 1963Q1 1989Q2

Included observations: 104

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

1 0.836 0.836 74.858 0.000

2 0.670 -0.09... 123.41 0.000

3 0.499 -0.11... 150.61 0.000

4 0.346 -0.05... 163.81 0.000

5 0.206 -0.07... 168.52 0.000

6 0.097 -0.01... 169.58 0.000

7 -0.00... -0.08... 169.58 0.000

8 -0.08... -0.03... 170.36 0.000

9 -0.17... -0.15... 174.01 0.000

1... -0.21... 0.088 179.30 0.000

1... -0.20... 0.062 184.41 0.000

1... -0.20... -0.05... 189.19 0.000

1... -0.21... -0.11... 194.63 0.000

1... -0.23... -0.09... 201.22 0.000

1... -0.24... -0.02... 208.87 0.000

1... -0.21... 0.140 214.41 0.000

1... -0.16... 0.012 217.88 0.000

1... -0.12... -0.09... 220.00 0.000

1... -0.05... 0.128 220.38 0.000

2... -0.00... -0.02... 220.39 0.000

2... 0.041 0.049 220.61 0.000

2... 0.083 0.007 221.54 0.000

2... 0.109 -0.06... 223.14 0.000

2... 0.134 0.014 225.62 0.000

2... 0.129 -0.02... 227.93 0.000

2... 0.097 -0.01... 229.26 0.000

2... 0.082 0.026 230.22 0.000

2... 0.071 0.026 230.96 0.000

2... 0.068 0.018 231.64 0.000

3... 0.098 0.134 233.07 0.000

3... 0.095 -0.07... 234.43 0.000

3... 0.085 -0.02... 235.54 0.000

3... 0.111 0.164 237.45 0.000

3... 0.115 -0.01... 239.53 0.000

3... 0.083 -0.14... 240.64 0.000

3... 0.033 -0.08... 240.82 0.000

The correlogram has spikes up to lags 5. The Q statistics corresponding to all the lags are

statistically significant implying presence of significant serial autocorrelation in the residuals.

Date: 04/27/19 Time: 16:09

Sample: 1963Q1 1989Q2

Included observations: 104

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

1 0.836 0.836 74.858 0.000

2 0.670 -0.09... 123.41 0.000

3 0.499 -0.11... 150.61 0.000

4 0.346 -0.05... 163.81 0.000

5 0.206 -0.07... 168.52 0.000

6 0.097 -0.01... 169.58 0.000

7 -0.00... -0.08... 169.58 0.000

8 -0.08... -0.03... 170.36 0.000

9 -0.17... -0.15... 174.01 0.000

1... -0.21... 0.088 179.30 0.000

1... -0.20... 0.062 184.41 0.000

1... -0.20... -0.05... 189.19 0.000

1... -0.21... -0.11... 194.63 0.000

1... -0.23... -0.09... 201.22 0.000

1... -0.24... -0.02... 208.87 0.000

1... -0.21... 0.140 214.41 0.000

1... -0.16... 0.012 217.88 0.000

1... -0.12... -0.09... 220.00 0.000

1... -0.05... 0.128 220.38 0.000

2... -0.00... -0.02... 220.39 0.000

2... 0.041 0.049 220.61 0.000

2... 0.083 0.007 221.54 0.000

2... 0.109 -0.06... 223.14 0.000

2... 0.134 0.014 225.62 0.000

2... 0.129 -0.02... 227.93 0.000

2... 0.097 -0.01... 229.26 0.000

2... 0.082 0.026 230.22 0.000

2... 0.071 0.026 230.96 0.000

2... 0.068 0.018 231.64 0.000

3... 0.098 0.134 233.07 0.000

3... 0.095 -0.07... 234.43 0.000

3... 0.085 -0.02... 235.54 0.000

3... 0.111 0.164 237.45 0.000

3... 0.115 -0.01... 239.53 0.000

3... 0.083 -0.14... 240.64 0.000

3... 0.033 -0.08... 240.82 0.000

The correlogram has spikes up to lags 5. The Q statistics corresponding to all the lags are

statistically significant implying presence of significant serial autocorrelation in the residuals.

12APPLIED ECONOMETRICS

Question b

Consequences of autocorrelation on OLS estimator

Presence of autocorrelation affects the OLS estimator in the following ways.

When the error terms suffer from autocorrelation, then OLS estimators though give an

unbiased result but fail to satisfy the minimum variance property.

In the presence of autocorrelation among the disturbance term, variance computed by

OLS method is larger than variance computed by other method. As a result, the

significance of t and f under OLS no longer give a valid result (Giles and Beattie 2018,

pp. 99-116).

The autocorrelation among the error terms seriously underestimate the variance of

disturbances.

OLS estimators are no longer asymptotic if the random error terms suffer from

autocorrelation.

Question c

In order to test presence of serial autocorrelation in the error terms, LM test is used. The

null and alternative hypotheses of the test are as follows

Null hypothesis: There is no serial autocorrelation in the residuals

Alternative hypothesis: Serial autocorrelation presents in the residuals

The result of LM test is given in appendix (Table 2). The p value associated with LM

statistics is 0.0000. As the p value is less than significance level of 0.05, the null hypothesis of no

serial autocorrelation in the residual terms is rejected. The LM test thus indicates presence of

Question b

Consequences of autocorrelation on OLS estimator

Presence of autocorrelation affects the OLS estimator in the following ways.

When the error terms suffer from autocorrelation, then OLS estimators though give an

unbiased result but fail to satisfy the minimum variance property.

In the presence of autocorrelation among the disturbance term, variance computed by

OLS method is larger than variance computed by other method. As a result, the

significance of t and f under OLS no longer give a valid result (Giles and Beattie 2018,

pp. 99-116).

The autocorrelation among the error terms seriously underestimate the variance of

disturbances.

OLS estimators are no longer asymptotic if the random error terms suffer from

autocorrelation.

Question c

In order to test presence of serial autocorrelation in the error terms, LM test is used. The

null and alternative hypotheses of the test are as follows

Null hypothesis: There is no serial autocorrelation in the residuals

Alternative hypothesis: Serial autocorrelation presents in the residuals

The result of LM test is given in appendix (Table 2). The p value associated with LM

statistics is 0.0000. As the p value is less than significance level of 0.05, the null hypothesis of no

serial autocorrelation in the residual terms is rejected. The LM test thus indicates presence of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13APPLIED ECONOMETRICS

serial autocorrelation in the residuals supporting the result obtained from correlogram and Q

statistics.

Question 5

Question a

The model in equation (1) uses independent variables such as rate of inflation, real GDP

and interest rate to predict the desired level of money supply in the economy. Under the new

specification, money supply depends on expected level of money supply and the money supply

in the previous period.

Question b

The model for long run money demand is given as

lnMt −lnMt −1=δ (lnMt

¿−lnMt −1)

The regression result with new specification is given in appendix (Table 3). The

estimated long run money demand equation as obtained from the regression is

lnMt −lnMt −1=0.9999(lnM t

¿−lnM t−1)

The output shows that the difference between expected money supply and that of

previous period money supply has a positive influence on the different between actual money

supply and money supply in the previous period. The associated p value of the coefficient is

0.0000. This shows the independent variable in the model is statistically insignificant.

Question c

The speed of adjustment to the long run level is 0.99.

serial autocorrelation in the residuals supporting the result obtained from correlogram and Q

statistics.

Question 5

Question a

The model in equation (1) uses independent variables such as rate of inflation, real GDP

and interest rate to predict the desired level of money supply in the economy. Under the new

specification, money supply depends on expected level of money supply and the money supply

in the previous period.

Question b

The model for long run money demand is given as

lnMt −lnMt −1=δ (lnMt

¿−lnMt −1)

The regression result with new specification is given in appendix (Table 3). The

estimated long run money demand equation as obtained from the regression is

lnMt −lnMt −1=0.9999(lnM t

¿−lnM t−1)

The output shows that the difference between expected money supply and that of

previous period money supply has a positive influence on the different between actual money

supply and money supply in the previous period. The associated p value of the coefficient is

0.0000. This shows the independent variable in the model is statistically insignificant.

Question c

The speed of adjustment to the long run level is 0.99.

14APPLIED ECONOMETRICS

Question d

The static money demand model in the long run can be specified as

lnMt −lnMt −1=β0 + β1 (inf t−inf t−1 ) + β2 (ly¿¿ t−lyt−1 )+ β3 (irt −irt −1)+ut ¿

The estimated static money demand equation in the long run is obtained as (Table 4)

lnMt −lnMt −1=−0.999679−0.065064 ( inf t−inf t−1 ) +0.286499(ly ¿¿ t−lyt −1)−0.047124 (irt−irt−1 )¿

The new model of long run money demand equation includes lagged values for all of the

independent variables. For inflation the sign of coefficient now become negative. That means in

the long run association the difference between current and previous period inflation is inversely

associated with the difference between current period money supply and that of the previous

period money supply That is higher the difference between inflation in the two period lower is

the difference between money supply. Like equation (1), real GDP is positively associated with

money supply in long run while interest rate has a negative association with money supply. All

the independent variables in the long have become statistically significant unlike in model (1)

where inflation turned out to be statistically insignificant.

Question 6

In order to perform autocorrelation test for the new model LM test is used. The obtained

result from the LM test is produced in appendix (Table 5). P value of the LM statistics is 0.0003.

The significant p value is less than the statistical significance level of 0.05. This implies rejection

of null hypothesis of no serial autocorrelation in the residuals. The error terms in the long run

money demand model thus also suffers from the problem of serial autocorrelation.

Question d

The static money demand model in the long run can be specified as

lnMt −lnMt −1=β0 + β1 (inf t−inf t−1 ) + β2 (ly¿¿ t−lyt−1 )+ β3 (irt −irt −1)+ut ¿

The estimated static money demand equation in the long run is obtained as (Table 4)

lnMt −lnMt −1=−0.999679−0.065064 ( inf t−inf t−1 ) +0.286499(ly ¿¿ t−lyt −1)−0.047124 (irt−irt−1 )¿

The new model of long run money demand equation includes lagged values for all of the

independent variables. For inflation the sign of coefficient now become negative. That means in

the long run association the difference between current and previous period inflation is inversely

associated with the difference between current period money supply and that of the previous

period money supply That is higher the difference between inflation in the two period lower is

the difference between money supply. Like equation (1), real GDP is positively associated with

money supply in long run while interest rate has a negative association with money supply. All

the independent variables in the long have become statistically significant unlike in model (1)

where inflation turned out to be statistically insignificant.

Question 6

In order to perform autocorrelation test for the new model LM test is used. The obtained

result from the LM test is produced in appendix (Table 5). P value of the LM statistics is 0.0003.

The significant p value is less than the statistical significance level of 0.05. This implies rejection

of null hypothesis of no serial autocorrelation in the residuals. The error terms in the long run

money demand model thus also suffers from the problem of serial autocorrelation.

15APPLIED ECONOMETRICS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16APPLIED ECONOMETRICS

Question 7

Question a

In a statistical model endogeneity problem refers to the correlation between the

independent variable and that of the error term. Error term in the model accounts for all the

variation that are not explained by the independent variables of the model (Sande and Ghosh

2018, pp.185-204). The inclusion of lagged dependent variables and GDP, inflation and interest

rate may lead to endogeneity problem because of interconnectedness among the variables.

Question b

Presence of endogeneity distorts OLS estimation of a model. Endogeneity has serious

implications for OLS estimates. In a model that suffers from endogeneity problem, the OLS

estimation gives biased and inconsistent estimates for the parameters (Gordon 2015, pp. 99-116).

With a biased estimation, the hypotheses tests are unable to provide a statistically valid result.

Question c

In order to deal with endogeneity problem either Ad Hoc solution or instrumental

variable methods are used.

Question 8

Question a

The selected instrument include one period lagged values of money supply, inflation, real

GDP and interest rate. The lagged values are chosen as instruments as these are independent of

error terms (Amsler, Prokhorov and Schmidt 2016, pp.280-288).

Question 7

Question a

In a statistical model endogeneity problem refers to the correlation between the

independent variable and that of the error term. Error term in the model accounts for all the

variation that are not explained by the independent variables of the model (Sande and Ghosh

2018, pp.185-204). The inclusion of lagged dependent variables and GDP, inflation and interest

rate may lead to endogeneity problem because of interconnectedness among the variables.

Question b

Presence of endogeneity distorts OLS estimation of a model. Endogeneity has serious

implications for OLS estimates. In a model that suffers from endogeneity problem, the OLS

estimation gives biased and inconsistent estimates for the parameters (Gordon 2015, pp. 99-116).

With a biased estimation, the hypotheses tests are unable to provide a statistically valid result.

Question c

In order to deal with endogeneity problem either Ad Hoc solution or instrumental

variable methods are used.

Question 8

Question a

The selected instrument include one period lagged values of money supply, inflation, real

GDP and interest rate. The lagged values are chosen as instruments as these are independent of

error terms (Amsler, Prokhorov and Schmidt 2016, pp.280-288).

17APPLIED ECONOMETRICS

Question b

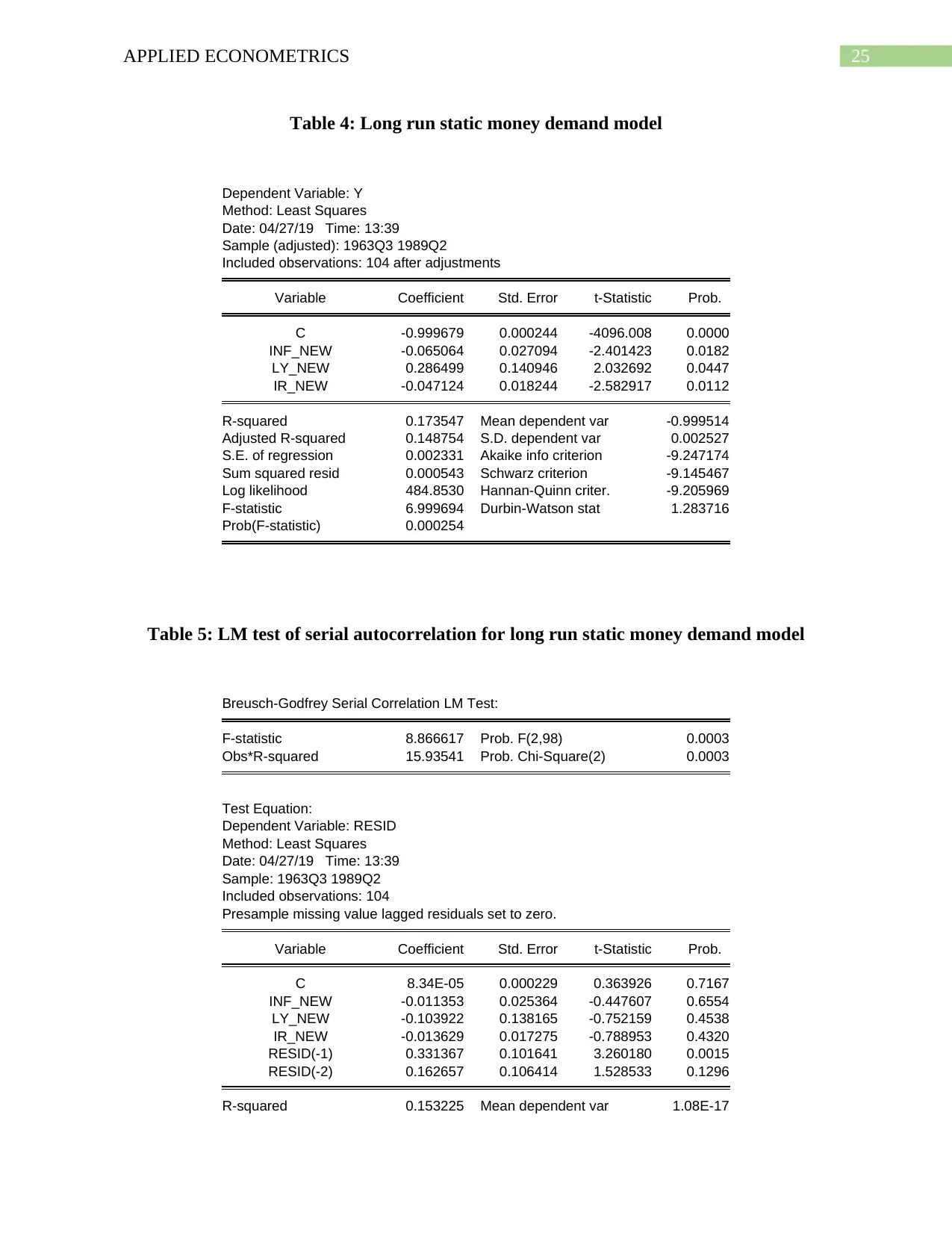

The estimated result with two stage least square is given in appendix (Table 6). The value

of coefficient though is almost same as that obtained by using OLS in Q5, running two stage

least square correct for bias present due to endogenety problem and therefore gives a preferable

result.

Question c

When the TSLS estimation of long run static money demand function (Table 7) is

compared to the static model of equation 1, a contractionary result is obtained. All the variables

in TSLS are statistically insignificant. The result of equation 1, however showed a statically

significant relation between money supply and that of real GDP and interest.

The comparison of TSLS with the obtained result for static long run money demand

equation again reveals a contradictory result. Unlike the OLS estimation, all the independent

variables are statistically insignificant. The coefficient values are smaller under TSLS than that

under OLS in equation 1.

Question 9

Question a

The Augmented Dicky-Fuller test or ADF test is used test stationarity of a particular time

series model (Paparoditis and Politis 2018, pp.955-973). In order to test the stationary of lm, inf,

ly and ir, ADF test is performed for the individual series. The null and alternative hypotheses for

ADF tests are given as follows

Null hypothesis: The series has a unit root

Question b

The estimated result with two stage least square is given in appendix (Table 6). The value

of coefficient though is almost same as that obtained by using OLS in Q5, running two stage

least square correct for bias present due to endogenety problem and therefore gives a preferable

result.

Question c

When the TSLS estimation of long run static money demand function (Table 7) is

compared to the static model of equation 1, a contractionary result is obtained. All the variables

in TSLS are statistically insignificant. The result of equation 1, however showed a statically

significant relation between money supply and that of real GDP and interest.

The comparison of TSLS with the obtained result for static long run money demand

equation again reveals a contradictory result. Unlike the OLS estimation, all the independent

variables are statistically insignificant. The coefficient values are smaller under TSLS than that

under OLS in equation 1.

Question 9

Question a

The Augmented Dicky-Fuller test or ADF test is used test stationarity of a particular time

series model (Paparoditis and Politis 2018, pp.955-973). In order to test the stationary of lm, inf,

ly and ir, ADF test is performed for the individual series. The null and alternative hypotheses for

ADF tests are given as follows

Null hypothesis: The series has a unit root

18APPLIED ECONOMETRICS

Alternative hypothesis: The series does not have a unit root

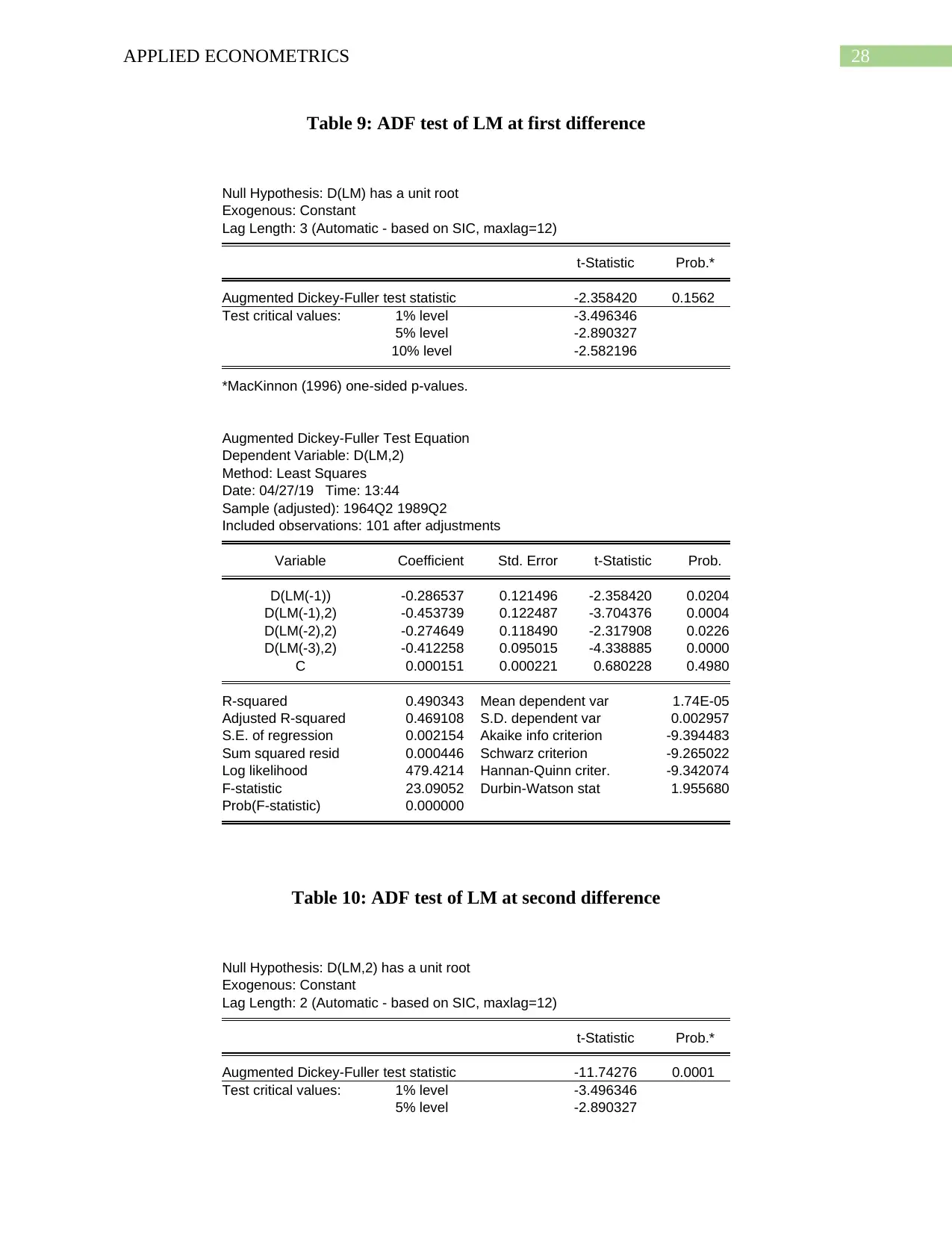

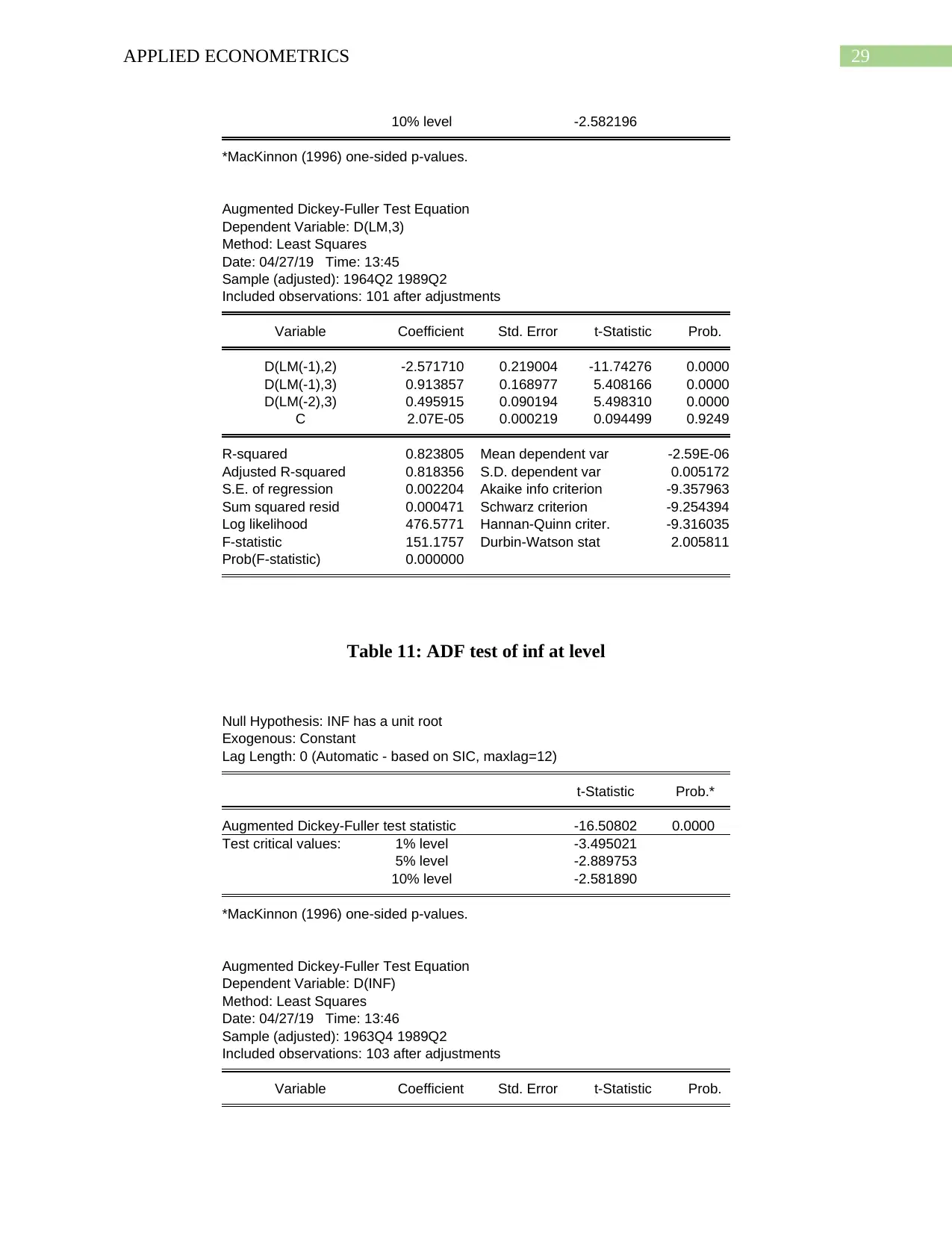

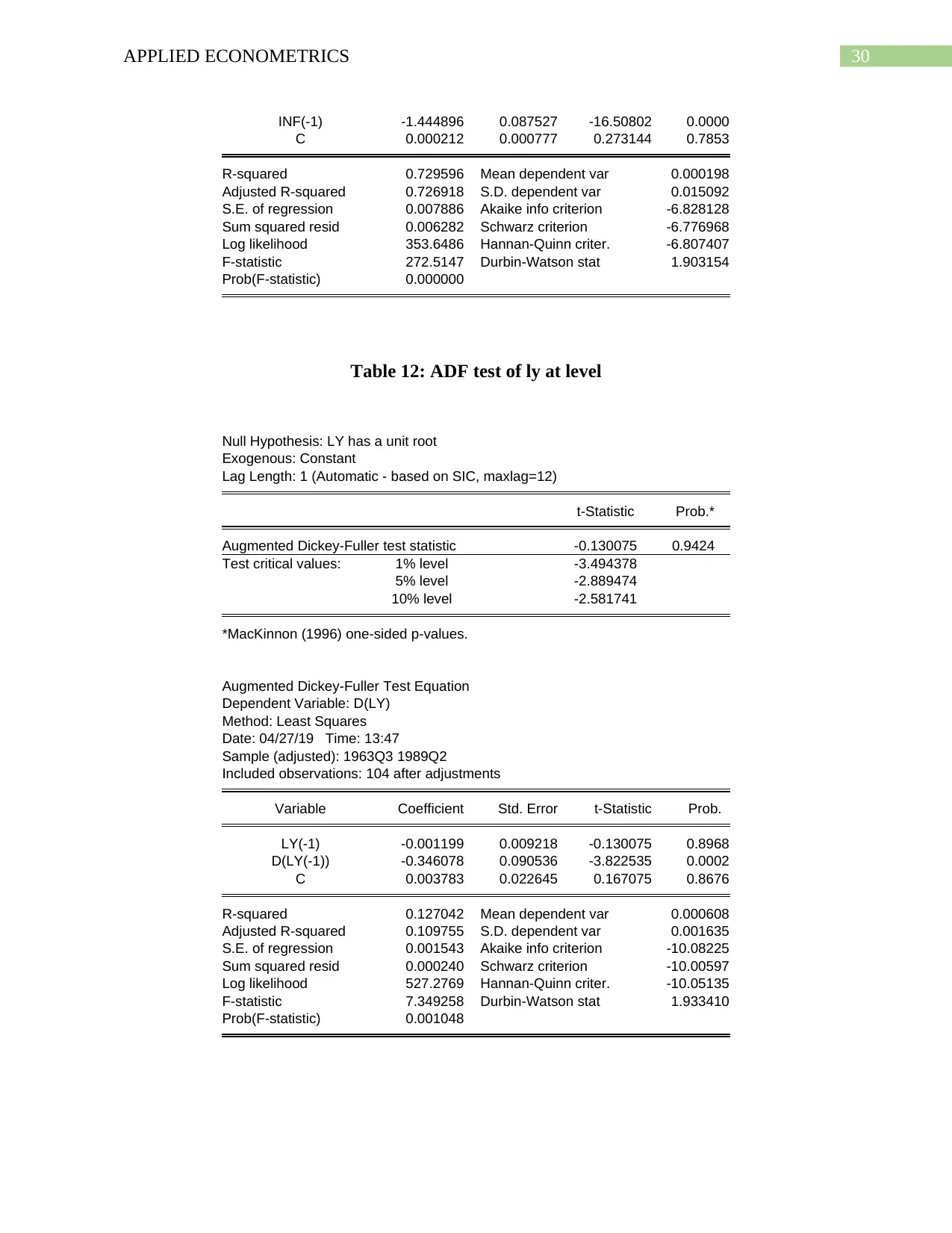

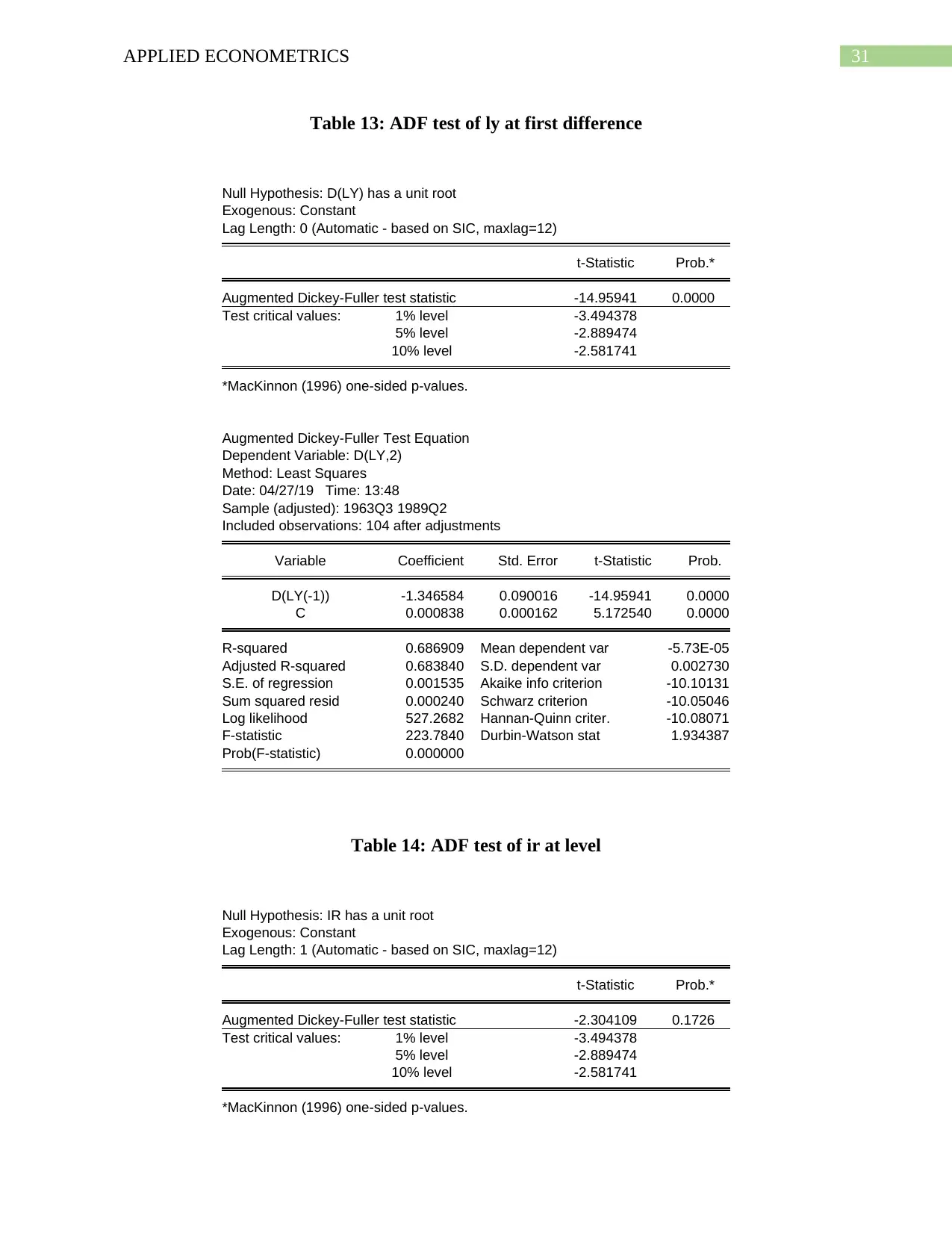

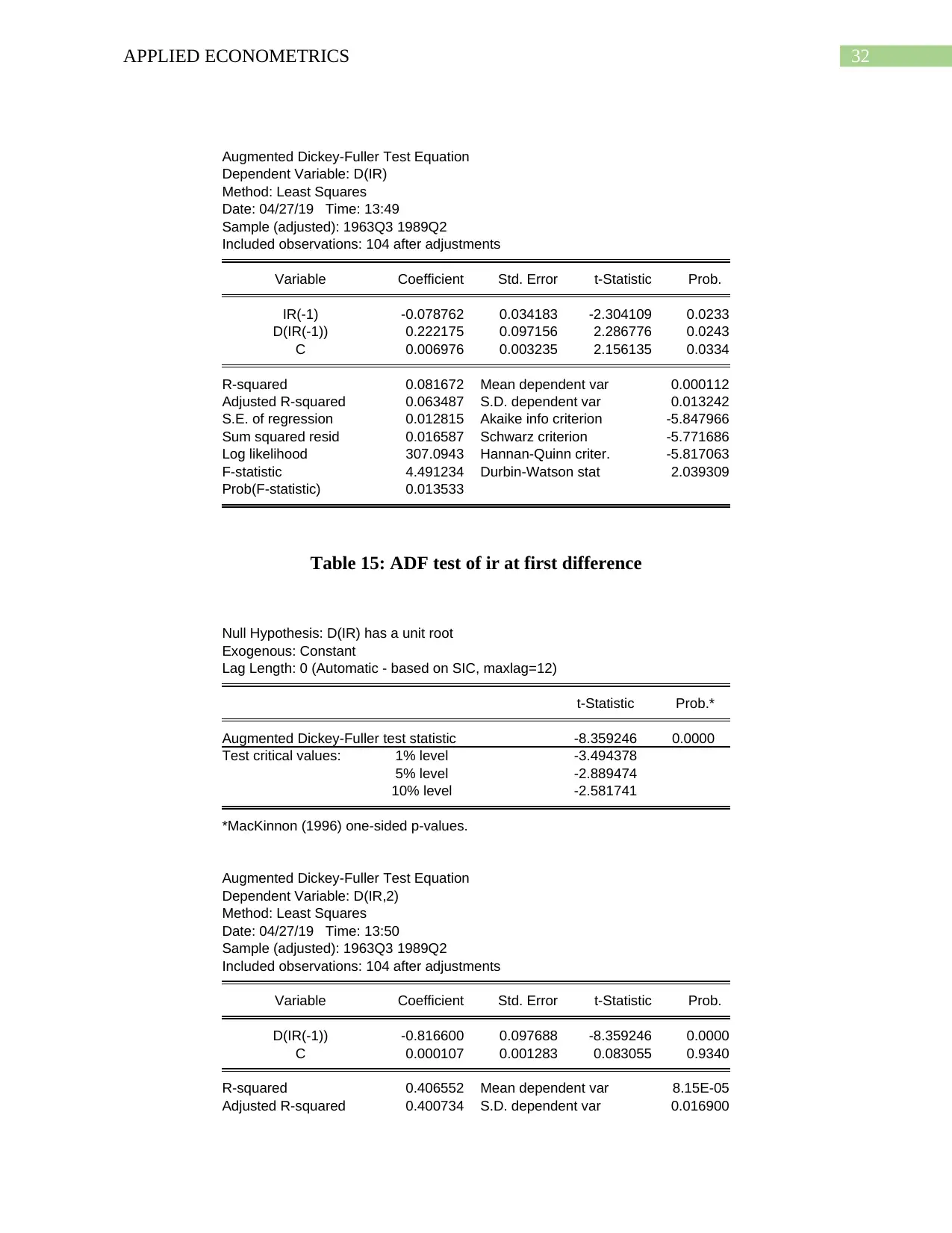

The ADF tests for each of series are given in Appendix (Table 8 – Table 15). The test include

maximum lag of 12 based of Schwarz Info Criterion (SIC).

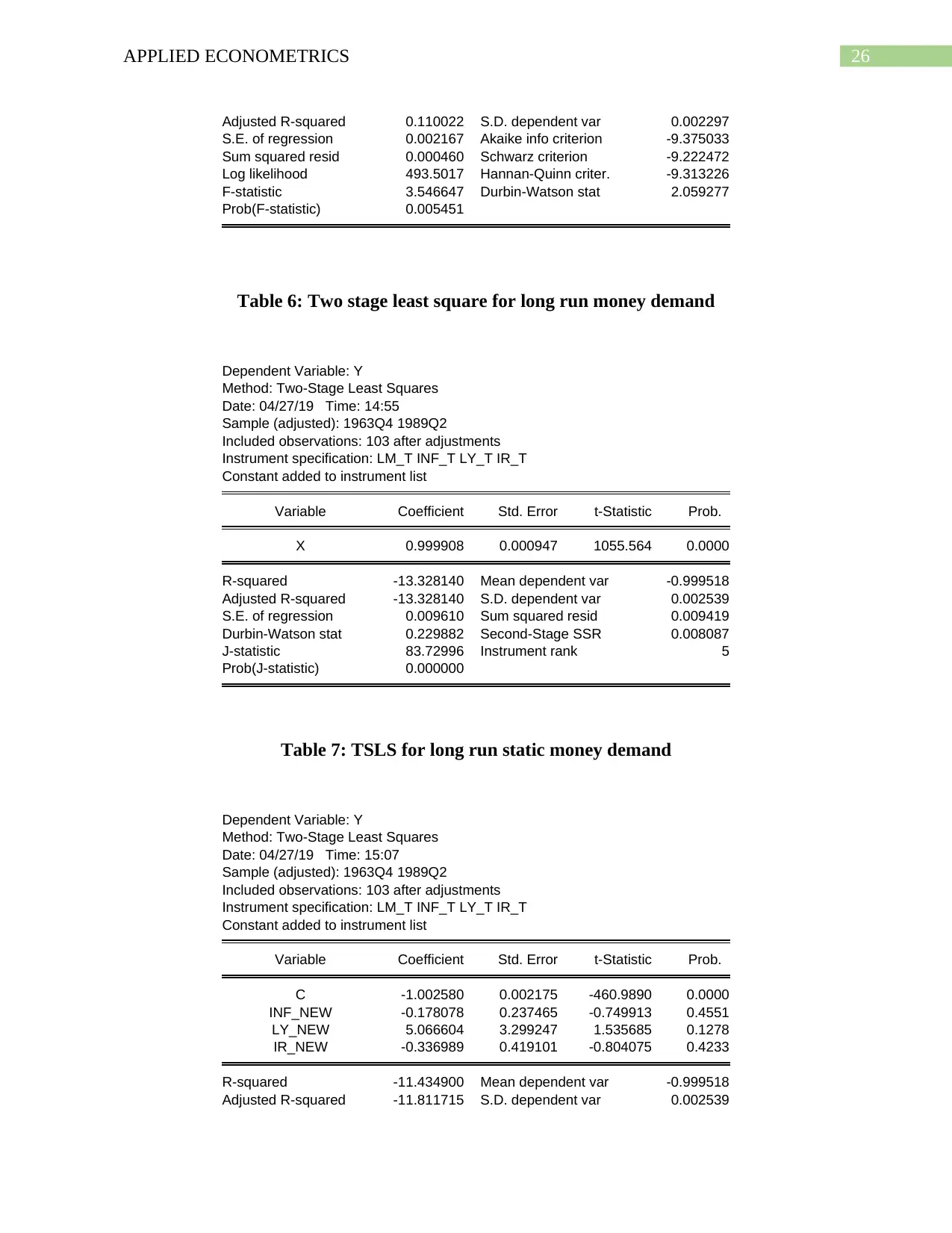

For the money supply series, the ADF test performed at levels show that the absolute

value of computed t (1.0075) is less than critical t value (3.4963, 2.8903 and 2.5821) at 1%, 5%

and 10% level of significance. The null hypothesis that the series has a unit root is thus accepted.

The result is further supported by the obtained p value. The associated p value is 0.7484. As the

p value is larger than the significance value, this again implies acceptance of null hypothesis

indicating the series has unit root.

In case of inflation series, the ADF test performed at levels show that the absolute value

of computed t (16.5080) is greater than critical t value (3.4963, 2.8903 and 2.5821) at 1%, 5%

and 10% level of significance. The null hypothesis that the series has a unit root is thus rejected.

The result is further supported by the obtained p value. The associated p value is 0.0000. As the

p value is less than the significance value, this again implies rejection of null hypothesis

indicating the series is stationary at level.

For real GDP series, the ADF test performed at levels show that the absolute value of

computed t (0.130075) is less than critical t value (3.4963, 2.8903 and 2.5821) at 1%, 5% and

10% level of significance. The null hypothesis that the series has a unit root is thus accepted. The

result is further supported by the obtained p value. The associated p value is 0.9424. As the p

value is larger than the significance value, this again implies acceptance of null hypothesis

indicating the series has unit root.

Alternative hypothesis: The series does not have a unit root

The ADF tests for each of series are given in Appendix (Table 8 – Table 15). The test include

maximum lag of 12 based of Schwarz Info Criterion (SIC).

For the money supply series, the ADF test performed at levels show that the absolute

value of computed t (1.0075) is less than critical t value (3.4963, 2.8903 and 2.5821) at 1%, 5%

and 10% level of significance. The null hypothesis that the series has a unit root is thus accepted.

The result is further supported by the obtained p value. The associated p value is 0.7484. As the

p value is larger than the significance value, this again implies acceptance of null hypothesis

indicating the series has unit root.

In case of inflation series, the ADF test performed at levels show that the absolute value

of computed t (16.5080) is greater than critical t value (3.4963, 2.8903 and 2.5821) at 1%, 5%

and 10% level of significance. The null hypothesis that the series has a unit root is thus rejected.

The result is further supported by the obtained p value. The associated p value is 0.0000. As the

p value is less than the significance value, this again implies rejection of null hypothesis

indicating the series is stationary at level.

For real GDP series, the ADF test performed at levels show that the absolute value of

computed t (0.130075) is less than critical t value (3.4963, 2.8903 and 2.5821) at 1%, 5% and

10% level of significance. The null hypothesis that the series has a unit root is thus accepted. The

result is further supported by the obtained p value. The associated p value is 0.9424. As the p

value is larger than the significance value, this again implies acceptance of null hypothesis

indicating the series has unit root.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19APPLIED ECONOMETRICS

For the interest rate series, the ADF test performed at levels show that the absolute value

of computed t (2.304109) is less than critical t value (3.4963, 2.8903 and 2.5821) at 1%, 5% and

10% level of significance. The null hypothesis that the series has a unit root is thus accepted. The

result is further supported by the obtained p value. The associated p value is 0.1726. As the p

value is larger than the significance value, this again implies acceptance of null hypothesis

indicating the series has unit root.

Question b

The order of integration depends on the level at which the concerned series becomes

stationary. For Money supply (lm), the series is stationary at second difference. It can therefore

be said that the series is integrated with order 2, I(2). In case of inflation series, it is stationary at

level and thus is integrated of order 0 or I (0). Both real GDP (ly) and interest rate (ir) are

stationary at first difference and therefore are integrated of order 1 or I(1).

Question c

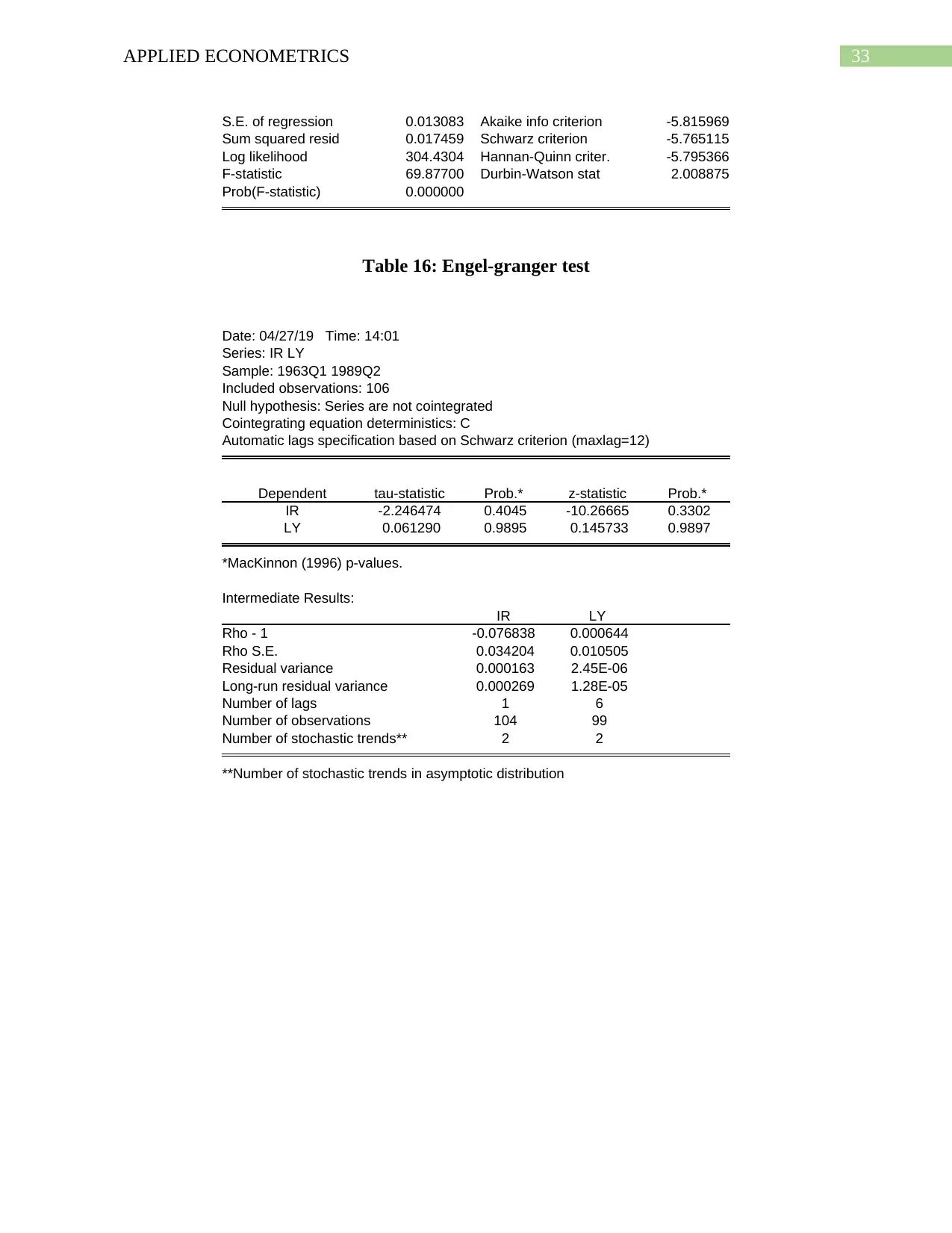

In order to be co-integrated the two variables need to be stationary at same level. Not all

the four variables are stationary at same level and therefore, all of them are not co-integrated

(Lee and Lee 2015, pp.3154-3171). The seroes ly and ir both are integrated of order 1 and

therefore, might be co-integrated. Co-integration test performed for the two variables and the

result is given in appendix (Table 16). The co-integration equation includes maximum lag of 12

as selected by SIC. The associated p values for IR and LY are respectively 0.3302 and 0.9897.

As both the values are greater than significance level of 0.05, the null hypothesis that the series

are not co-integrated are accepted. The variables thus are not co-integrated.

Question 10

For the interest rate series, the ADF test performed at levels show that the absolute value

of computed t (2.304109) is less than critical t value (3.4963, 2.8903 and 2.5821) at 1%, 5% and

10% level of significance. The null hypothesis that the series has a unit root is thus accepted. The

result is further supported by the obtained p value. The associated p value is 0.1726. As the p

value is larger than the significance value, this again implies acceptance of null hypothesis

indicating the series has unit root.

Question b

The order of integration depends on the level at which the concerned series becomes

stationary. For Money supply (lm), the series is stationary at second difference. It can therefore

be said that the series is integrated with order 2, I(2). In case of inflation series, it is stationary at

level and thus is integrated of order 0 or I (0). Both real GDP (ly) and interest rate (ir) are

stationary at first difference and therefore are integrated of order 1 or I(1).

Question c

In order to be co-integrated the two variables need to be stationary at same level. Not all

the four variables are stationary at same level and therefore, all of them are not co-integrated

(Lee and Lee 2015, pp.3154-3171). The seroes ly and ir both are integrated of order 1 and

therefore, might be co-integrated. Co-integration test performed for the two variables and the

result is given in appendix (Table 16). The co-integration equation includes maximum lag of 12

as selected by SIC. The associated p values for IR and LY are respectively 0.3302 and 0.9897.

As both the values are greater than significance level of 0.05, the null hypothesis that the series

are not co-integrated are accepted. The variables thus are not co-integrated.

Question 10

20APPLIED ECONOMETRICS

Demand for money refers to the amount of money that people I the economy willing to

hold at a certain point of time. The theory of liquidity preference suggests that money demand

depends on income and interest rate. Income is positively associated with money demand while

interest rate is inversely associated with money demand (Mele and Stefanski 2019, pp.393-410).

The analysis of the paper include an additional variable inflation for estimating money demand

function. The discussion provides useful insights related to money demand in the short run and

that in the long run. Monetary policy deals with money supply in the economy. Depending on

state of the economy, central bank takes the decision regarding expansionary or tight monetary

policy. In the short run, money demand has a positive significance association with real GDP.

That means policies to stimulate GDP and economic growth increase money demand as well. In

order to reduce money demand and controls inflationary pressure government should take a tight

monetary policy by increasing interest rate . Interest rate, which is the reward of saving, is

negatively associated with money demand (Palley 2015, pp.1-23). Therefore, government

policies of lowering interest rate (part of expansionary monetary policy) to encourage investment

has a positive impact on money demand. Higher money demand in turn brings a higher inflation

through demand-pull inflation. Policymakers therefore should take a policy that can balance

between macroeconomic variables such as inflation, real GDP and interest and that of real

money balances. In the long run however money supply quickly adjusts to the expected money

supply.

Demand for money refers to the amount of money that people I the economy willing to

hold at a certain point of time. The theory of liquidity preference suggests that money demand

depends on income and interest rate. Income is positively associated with money demand while

interest rate is inversely associated with money demand (Mele and Stefanski 2019, pp.393-410).

The analysis of the paper include an additional variable inflation for estimating money demand

function. The discussion provides useful insights related to money demand in the short run and

that in the long run. Monetary policy deals with money supply in the economy. Depending on

state of the economy, central bank takes the decision regarding expansionary or tight monetary

policy. In the short run, money demand has a positive significance association with real GDP.

That means policies to stimulate GDP and economic growth increase money demand as well. In

order to reduce money demand and controls inflationary pressure government should take a tight

monetary policy by increasing interest rate . Interest rate, which is the reward of saving, is

negatively associated with money demand (Palley 2015, pp.1-23). Therefore, government

policies of lowering interest rate (part of expansionary monetary policy) to encourage investment

has a positive impact on money demand. Higher money demand in turn brings a higher inflation

through demand-pull inflation. Policymakers therefore should take a policy that can balance

between macroeconomic variables such as inflation, real GDP and interest and that of real

money balances. In the long run however money supply quickly adjusts to the expected money

supply.

21APPLIED ECONOMETRICS

References and Bibliography

Amsler, C., Prokhorov, A. and Schmidt, P., 2016. Endogeneity in stochastic frontier

models. Journal of Econometrics, 190(2), pp.280-288.

Becu, J.M., Grandvalet, Y., Ambroise, C. and Dalmasso, C., 2017. Beyond support in two-stage

variable selection. Statistics and Computing, 27(1), pp.169-179.

Carrera, C. and Flores, J., 2017. Modelling and forecasting money demand: divide and

conquer (No. 2017-91).

Chatterjee, S. and Hadi, A.S., 2015. Regression analysis by example. John Wiley & Sons.

Darlington, R.B. and Hayes, A.F., 2016. Regression analysis and linear models: Concepts,

applications, and implementation. Guilford Publications.

Fox, J., 2015. Applied regression analysis and generalized linear models. Sage Publications.

Gan, P.T., 2019. Economic uncertainty, precautionary motive and the augmented form of money

demand function. Evolutionary and Institutional Economics Review, pp.1-27.

Giles, D.E. and Beattie, M., 2018. Autocorrelation pre-test estimation in models with a lagged

dependent variable. In Specification analysis in the linear model (pp. 99-116). Routledge.

Goodwin, N., Harris, J.M., Nelson, J.A., Roach, B. and Torras, M., 2015. Macroeconomics in

context. Routledge.

Gordon, D.V., 2015. The endogeneity problem in applied fisheries econometrics: A critical

review. Environmental and Resource Economics, 61(1), pp.115-125.

References and Bibliography

Amsler, C., Prokhorov, A. and Schmidt, P., 2016. Endogeneity in stochastic frontier

models. Journal of Econometrics, 190(2), pp.280-288.

Becu, J.M., Grandvalet, Y., Ambroise, C. and Dalmasso, C., 2017. Beyond support in two-stage

variable selection. Statistics and Computing, 27(1), pp.169-179.

Carrera, C. and Flores, J., 2017. Modelling and forecasting money demand: divide and

conquer (No. 2017-91).

Chatterjee, S. and Hadi, A.S., 2015. Regression analysis by example. John Wiley & Sons.

Darlington, R.B. and Hayes, A.F., 2016. Regression analysis and linear models: Concepts,

applications, and implementation. Guilford Publications.

Fox, J., 2015. Applied regression analysis and generalized linear models. Sage Publications.

Gan, P.T., 2019. Economic uncertainty, precautionary motive and the augmented form of money

demand function. Evolutionary and Institutional Economics Review, pp.1-27.

Giles, D.E. and Beattie, M., 2018. Autocorrelation pre-test estimation in models with a lagged

dependent variable. In Specification analysis in the linear model (pp. 99-116). Routledge.

Goodwin, N., Harris, J.M., Nelson, J.A., Roach, B. and Torras, M., 2015. Macroeconomics in

context. Routledge.

Gordon, D.V., 2015. The endogeneity problem in applied fisheries econometrics: A critical

review. Environmental and Resource Economics, 61(1), pp.115-125.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22APPLIED ECONOMETRICS

Johnson, H.G., 2017. The Demand for Money: Estimation of Structural Equations.

In Macroeconomics and Monetary Theory (pp. 121-128). Routledge.

Jonung, L., 2017. Demand for money: an analysis of the long-run behavior of the velocity of

circulation. Routledge.

Lee, H. and Lee, J., 2015. More powerful Engle–Granger cointegration tests. Journal of

Statistical Computation and Simulation, 85(15), pp.3154-3171.

Mele, A. and Stefanski, R., 2019. Velocity in the long run: Money and structural

transformation. Review of Economic Dynamics, 31, pp.393-410.

Palley, T.I., 2015. Money, fiscal policy, and interest rates: A critique of Modern Monetary

Theory. Review of Political Economy, 27(1), pp.1-23.

Paparoditis, E. and Politis, D.N., 2018. The asymptotic size and power of the augmented

Dickey–Fuller test for a unit root. Econometric Reviews, 37(9), pp.955-973.

Petit-Bois, M., Baek, E.K., Van den Noortgate, W., Beretvas, S.N. and Ferron, J.M., 2016. The

consequences of modeling autocorrelation when synthesizing single-case studies using a three-

level model. Behavior research methods, 48(2), pp.803-812.

Sande, J.B. and Ghosh, M., 2018. Endogeneity in survey research. International Journal of

Research in Marketing, 35(2), pp.185-204.

Schumacker, R.E., 2017. Interaction and nonlinear effects in structural equation modeling.

Routledge.

Uribe, M. and Schmitt-Grohé, S., 2017. Open economy macroeconomics. Princeton University

Press.

Johnson, H.G., 2017. The Demand for Money: Estimation of Structural Equations.

In Macroeconomics and Monetary Theory (pp. 121-128). Routledge.

Jonung, L., 2017. Demand for money: an analysis of the long-run behavior of the velocity of

circulation. Routledge.

Lee, H. and Lee, J., 2015. More powerful Engle–Granger cointegration tests. Journal of

Statistical Computation and Simulation, 85(15), pp.3154-3171.

Mele, A. and Stefanski, R., 2019. Velocity in the long run: Money and structural

transformation. Review of Economic Dynamics, 31, pp.393-410.

Palley, T.I., 2015. Money, fiscal policy, and interest rates: A critique of Modern Monetary

Theory. Review of Political Economy, 27(1), pp.1-23.

Paparoditis, E. and Politis, D.N., 2018. The asymptotic size and power of the augmented

Dickey–Fuller test for a unit root. Econometric Reviews, 37(9), pp.955-973.

Petit-Bois, M., Baek, E.K., Van den Noortgate, W., Beretvas, S.N. and Ferron, J.M., 2016. The

consequences of modeling autocorrelation when synthesizing single-case studies using a three-

level model. Behavior research methods, 48(2), pp.803-812.

Sande, J.B. and Ghosh, M., 2018. Endogeneity in survey research. International Journal of

Research in Marketing, 35(2), pp.185-204.

Schumacker, R.E., 2017. Interaction and nonlinear effects in structural equation modeling.

Routledge.

Uribe, M. and Schmitt-Grohé, S., 2017. Open economy macroeconomics. Princeton University

Press.

23APPLIED ECONOMETRICS

Appendix

Table 1: Static money demand equation

Dependent Variable: LM

Method: Least Squares

Date: 04/26/19 Time: 16:11

Sample (adjusted): 1963Q2 1989Q2

Included observations: 105 after adjustments

Variable Coefficient Std. Error t-Statistic Prob.

C 1.423214 0.139993 10.16634 0.0000

INF 0.079303 0.090484 0.876427 0.3829

LY 0.413525 0.057020 7.252307 0.0000

IR -0.361611 0.033889 -10.67046 0.0000

R-squared 0.690400 Mean dependent var 2.409453

Adjusted R-squared 0.681204 S.D. dependent var 0.017106

S.E. of regression 0.009658 Akaike info criterion -6.404633

Sum squared resid 0.009422 Schwarz criterion -6.303529

Log likelihood 340.2432 Hannan-Quinn criter. -6.363664

F-statistic 75.07595 Durbin-Watson stat 0.230013

Prob(F-statistic) 0.000000

Table 2: Serial correlation LM test

Breusch-Godfrey Serial Correlation LM Test:

F-statistic 65.66106 Prob. F(5,95) 0.0000

Obs*R-squared 80.45876 Prob. Chi-Square(5) 0.0000

Test Equation:

Dependent Variable: RESID

Method: Least Squares

Date: 04/27/19 Time: 13:34

Sample (adjusted): 1963Q3 1989Q2

Included observations: 104 after adjustments

Presample missing value lagged residuals set to zero.

Variable Coefficient Std. Error t-Statistic Prob.

C -0.047874 0.072364 -0.661569 0.5098

INF -0.034081 0.054793 -0.621994 0.5354

LY 0.019927 0.029469 0.676216 0.5005

IR -0.007997 0.012564 -0.636536 0.5260

Appendix

Table 1: Static money demand equation

Dependent Variable: LM

Method: Least Squares

Date: 04/26/19 Time: 16:11

Sample (adjusted): 1963Q2 1989Q2

Included observations: 105 after adjustments

Variable Coefficient Std. Error t-Statistic Prob.

C 1.423214 0.139993 10.16634 0.0000

INF 0.079303 0.090484 0.876427 0.3829

LY 0.413525 0.057020 7.252307 0.0000

IR -0.361611 0.033889 -10.67046 0.0000

R-squared 0.690400 Mean dependent var 2.409453

Adjusted R-squared 0.681204 S.D. dependent var 0.017106

S.E. of regression 0.009658 Akaike info criterion -6.404633

Sum squared resid 0.009422 Schwarz criterion -6.303529

Log likelihood 340.2432 Hannan-Quinn criter. -6.363664

F-statistic 75.07595 Durbin-Watson stat 0.230013

Prob(F-statistic) 0.000000

Table 2: Serial correlation LM test

Breusch-Godfrey Serial Correlation LM Test:

F-statistic 65.66106 Prob. F(5,95) 0.0000

Obs*R-squared 80.45876 Prob. Chi-Square(5) 0.0000

Test Equation:

Dependent Variable: RESID

Method: Least Squares

Date: 04/27/19 Time: 13:34

Sample (adjusted): 1963Q3 1989Q2

Included observations: 104 after adjustments

Presample missing value lagged residuals set to zero.

Variable Coefficient Std. Error t-Statistic Prob.

C -0.047874 0.072364 -0.661569 0.5098

INF -0.034081 0.054793 -0.621994 0.5354

LY 0.019927 0.029469 0.676216 0.5005

IR -0.007997 0.012564 -0.636536 0.5260

24APPLIED ECONOMETRICS

RESID(-1) 1.038066 0.106109 9.783014 0.0000

RESID(-2) -0.066647 0.146891 -0.453719 0.6511

RESID(-3) -0.141486 0.145558 -0.972022 0.3335

RESID(-4) 0.151278 0.149153 1.014244 0.3130

RESID(-5) -0.126483 0.109919 -1.150697 0.2527

R-squared 0.773642 Mean dependent var 0.001623

Adjusted R-squared 0.754580 S.D. dependent var 0.009523

S.E. of regression 0.004718 Akaike info criterion -7.792394

Sum squared resid 0.002114 Schwarz criterion -7.563552

Log likelihood 414.2045 Hannan-Quinn criter. -7.699683

F-statistic 40.58612 Durbin-Watson stat 1.955545

Prob(F-statistic) 0.000000

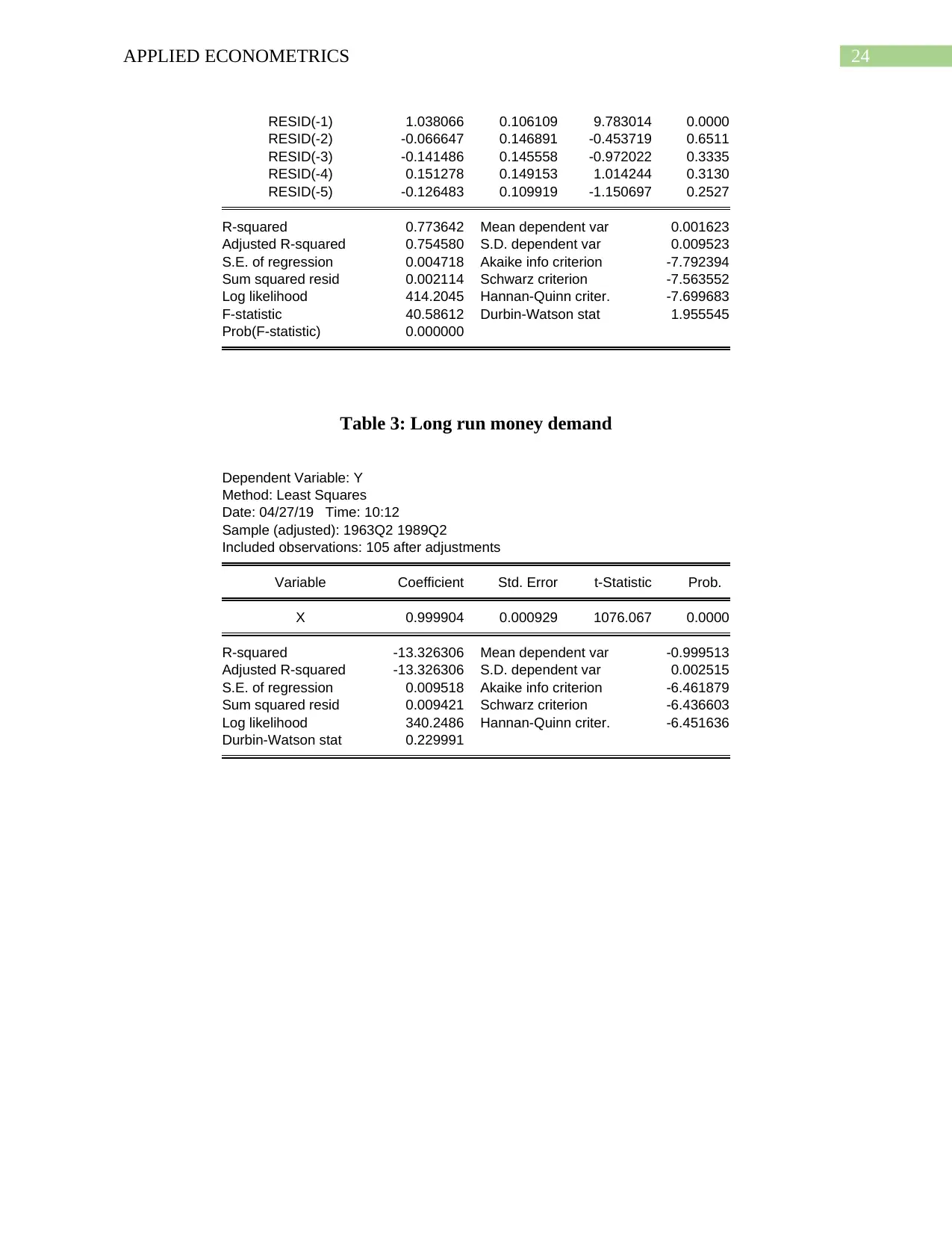

Table 3: Long run money demand

Dependent Variable: Y

Method: Least Squares

Date: 04/27/19 Time: 10:12

Sample (adjusted): 1963Q2 1989Q2

Included observations: 105 after adjustments

Variable Coefficient Std. Error t-Statistic Prob.

X 0.999904 0.000929 1076.067 0.0000

R-squared -13.326306 Mean dependent var -0.999513

Adjusted R-squared -13.326306 S.D. dependent var 0.002515

S.E. of regression 0.009518 Akaike info criterion -6.461879

Sum squared resid 0.009421 Schwarz criterion -6.436603

Log likelihood 340.2486 Hannan-Quinn criter. -6.451636

Durbin-Watson stat 0.229991

RESID(-1) 1.038066 0.106109 9.783014 0.0000

RESID(-2) -0.066647 0.146891 -0.453719 0.6511

RESID(-3) -0.141486 0.145558 -0.972022 0.3335

RESID(-4) 0.151278 0.149153 1.014244 0.3130

RESID(-5) -0.126483 0.109919 -1.150697 0.2527

R-squared 0.773642 Mean dependent var 0.001623

Adjusted R-squared 0.754580 S.D. dependent var 0.009523

S.E. of regression 0.004718 Akaike info criterion -7.792394

Sum squared resid 0.002114 Schwarz criterion -7.563552

Log likelihood 414.2045 Hannan-Quinn criter. -7.699683

F-statistic 40.58612 Durbin-Watson stat 1.955545

Prob(F-statistic) 0.000000

Table 3: Long run money demand

Dependent Variable: Y

Method: Least Squares

Date: 04/27/19 Time: 10:12

Sample (adjusted): 1963Q2 1989Q2

Included observations: 105 after adjustments

Variable Coefficient Std. Error t-Statistic Prob.

X 0.999904 0.000929 1076.067 0.0000

R-squared -13.326306 Mean dependent var -0.999513

Adjusted R-squared -13.326306 S.D. dependent var 0.002515

S.E. of regression 0.009518 Akaike info criterion -6.461879

Sum squared resid 0.009421 Schwarz criterion -6.436603

Log likelihood 340.2486 Hannan-Quinn criter. -6.451636

Durbin-Watson stat 0.229991

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25APPLIED ECONOMETRICS

Table 4: Long run static money demand model

Dependent Variable: Y

Method: Least Squares

Date: 04/27/19 Time: 13:39

Sample (adjusted): 1963Q3 1989Q2

Included observations: 104 after adjustments

Variable Coefficient Std. Error t-Statistic Prob.

C -0.999679 0.000244 -4096.008 0.0000

INF_NEW -0.065064 0.027094 -2.401423 0.0182

LY_NEW 0.286499 0.140946 2.032692 0.0447

IR_NEW -0.047124 0.018244 -2.582917 0.0112

R-squared 0.173547 Mean dependent var -0.999514

Adjusted R-squared 0.148754 S.D. dependent var 0.002527

S.E. of regression 0.002331 Akaike info criterion -9.247174

Sum squared resid 0.000543 Schwarz criterion -9.145467

Log likelihood 484.8530 Hannan-Quinn criter. -9.205969

F-statistic 6.999694 Durbin-Watson stat 1.283716

Prob(F-statistic) 0.000254

Table 5: LM test of serial autocorrelation for long run static money demand model

Breusch-Godfrey Serial Correlation LM Test:

F-statistic 8.866617 Prob. F(2,98) 0.0003

Obs*R-squared 15.93541 Prob. Chi-Square(2) 0.0003

Test Equation:

Dependent Variable: RESID

Method: Least Squares

Date: 04/27/19 Time: 13:39

Sample: 1963Q3 1989Q2

Included observations: 104

Presample missing value lagged residuals set to zero.

Variable Coefficient Std. Error t-Statistic Prob.

C 8.34E-05 0.000229 0.363926 0.7167

INF_NEW -0.011353 0.025364 -0.447607 0.6554

LY_NEW -0.103922 0.138165 -0.752159 0.4538

IR_NEW -0.013629 0.017275 -0.788953 0.4320

RESID(-1) 0.331367 0.101641 3.260180 0.0015

RESID(-2) 0.162657 0.106414 1.528533 0.1296

R-squared 0.153225 Mean dependent var 1.08E-17

Table 4: Long run static money demand model

Dependent Variable: Y

Method: Least Squares

Date: 04/27/19 Time: 13:39

Sample (adjusted): 1963Q3 1989Q2

Included observations: 104 after adjustments

Variable Coefficient Std. Error t-Statistic Prob.

C -0.999679 0.000244 -4096.008 0.0000

INF_NEW -0.065064 0.027094 -2.401423 0.0182

LY_NEW 0.286499 0.140946 2.032692 0.0447

IR_NEW -0.047124 0.018244 -2.582917 0.0112

R-squared 0.173547 Mean dependent var -0.999514

Adjusted R-squared 0.148754 S.D. dependent var 0.002527

S.E. of regression 0.002331 Akaike info criterion -9.247174

Sum squared resid 0.000543 Schwarz criterion -9.145467

Log likelihood 484.8530 Hannan-Quinn criter. -9.205969

F-statistic 6.999694 Durbin-Watson stat 1.283716

Prob(F-statistic) 0.000254

Table 5: LM test of serial autocorrelation for long run static money demand model

Breusch-Godfrey Serial Correlation LM Test:

F-statistic 8.866617 Prob. F(2,98) 0.0003

Obs*R-squared 15.93541 Prob. Chi-Square(2) 0.0003

Test Equation:

Dependent Variable: RESID

Method: Least Squares

Date: 04/27/19 Time: 13:39

Sample: 1963Q3 1989Q2

Included observations: 104

Presample missing value lagged residuals set to zero.

Variable Coefficient Std. Error t-Statistic Prob.

C 8.34E-05 0.000229 0.363926 0.7167

INF_NEW -0.011353 0.025364 -0.447607 0.6554

LY_NEW -0.103922 0.138165 -0.752159 0.4538

IR_NEW -0.013629 0.017275 -0.788953 0.4320

RESID(-1) 0.331367 0.101641 3.260180 0.0015

RESID(-2) 0.162657 0.106414 1.528533 0.1296

R-squared 0.153225 Mean dependent var 1.08E-17

26APPLIED ECONOMETRICS

Adjusted R-squared 0.110022 S.D. dependent var 0.002297

S.E. of regression 0.002167 Akaike info criterion -9.375033

Sum squared resid 0.000460 Schwarz criterion -9.222472

Log likelihood 493.5017 Hannan-Quinn criter. -9.313226

F-statistic 3.546647 Durbin-Watson stat 2.059277

Prob(F-statistic) 0.005451

Table 6: Two stage least square for long run money demand

Dependent Variable: Y

Method: Two-Stage Least Squares

Date: 04/27/19 Time: 14:55

Sample (adjusted): 1963Q4 1989Q2

Included observations: 103 after adjustments

Instrument specification: LM_T INF_T LY_T IR_T

Constant added to instrument list

Variable Coefficient Std. Error t-Statistic Prob.

X 0.999908 0.000947 1055.564 0.0000

R-squared -13.328140 Mean dependent var -0.999518

Adjusted R-squared -13.328140 S.D. dependent var 0.002539

S.E. of regression 0.009610 Sum squared resid 0.009419

Durbin-Watson stat 0.229882 Second-Stage SSR 0.008087

J-statistic 83.72996 Instrument rank 5

Prob(J-statistic) 0.000000

Table 7: TSLS for long run static money demand

Dependent Variable: Y

Method: Two-Stage Least Squares

Date: 04/27/19 Time: 15:07

Sample (adjusted): 1963Q4 1989Q2

Included observations: 103 after adjustments

Instrument specification: LM_T INF_T LY_T IR_T

Constant added to instrument list

Variable Coefficient Std. Error t-Statistic Prob.

C -1.002580 0.002175 -460.9890 0.0000

INF_NEW -0.178078 0.237465 -0.749913 0.4551

LY_NEW 5.066604 3.299247 1.535685 0.1278

IR_NEW -0.336989 0.419101 -0.804075 0.4233

R-squared -11.434900 Mean dependent var -0.999518

Adjusted R-squared -11.811715 S.D. dependent var 0.002539

Adjusted R-squared 0.110022 S.D. dependent var 0.002297

S.E. of regression 0.002167 Akaike info criterion -9.375033

Sum squared resid 0.000460 Schwarz criterion -9.222472

Log likelihood 493.5017 Hannan-Quinn criter. -9.313226

F-statistic 3.546647 Durbin-Watson stat 2.059277

Prob(F-statistic) 0.005451

Table 6: Two stage least square for long run money demand

Dependent Variable: Y

Method: Two-Stage Least Squares

Date: 04/27/19 Time: 14:55

Sample (adjusted): 1963Q4 1989Q2

Included observations: 103 after adjustments

Instrument specification: LM_T INF_T LY_T IR_T

Constant added to instrument list

Variable Coefficient Std. Error t-Statistic Prob.

X 0.999908 0.000947 1055.564 0.0000

R-squared -13.328140 Mean dependent var -0.999518

Adjusted R-squared -13.328140 S.D. dependent var 0.002539

S.E. of regression 0.009610 Sum squared resid 0.009419

Durbin-Watson stat 0.229882 Second-Stage SSR 0.008087

J-statistic 83.72996 Instrument rank 5

Prob(J-statistic) 0.000000

Table 7: TSLS for long run static money demand

Dependent Variable: Y

Method: Two-Stage Least Squares

Date: 04/27/19 Time: 15:07

Sample (adjusted): 1963Q4 1989Q2

Included observations: 103 after adjustments

Instrument specification: LM_T INF_T LY_T IR_T

Constant added to instrument list

Variable Coefficient Std. Error t-Statistic Prob.

C -1.002580 0.002175 -460.9890 0.0000

INF_NEW -0.178078 0.237465 -0.749913 0.4551

LY_NEW 5.066604 3.299247 1.535685 0.1278

IR_NEW -0.336989 0.419101 -0.804075 0.4233

R-squared -11.434900 Mean dependent var -0.999518

Adjusted R-squared -11.811715 S.D. dependent var 0.002539

27APPLIED ECONOMETRICS

S.E. of regression 0.009087 Sum squared resid 0.008175

F-statistic 0.867052 Durbin-Watson stat 2.653666

Prob(F-statistic) 0.460926 Second-Stage SSR 0.000443

J-statistic 1.061957 Instrument rank 5

Prob(J-statistic) 0.302769

Table 8: ADF test of LM at level

Null Hypothesis: LM has a unit root

Exogenous: Constant

Lag Length: 4 (Automatic - based on SIC, maxlag=12)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -1.007529 0.7484

Test critical values: 1% level -3.496346

5% level -2.890327

10% level -2.582196

*MacKinnon (1996) one-sided p-values.

Augmented Dickey-Fuller Test Equation

Dependent Variable: D(LM)

Method: Least Squares

Date: 04/27/19 Time: 13:43

Sample (adjusted): 1964Q2 1989Q2

Included observations: 101 after adjustments

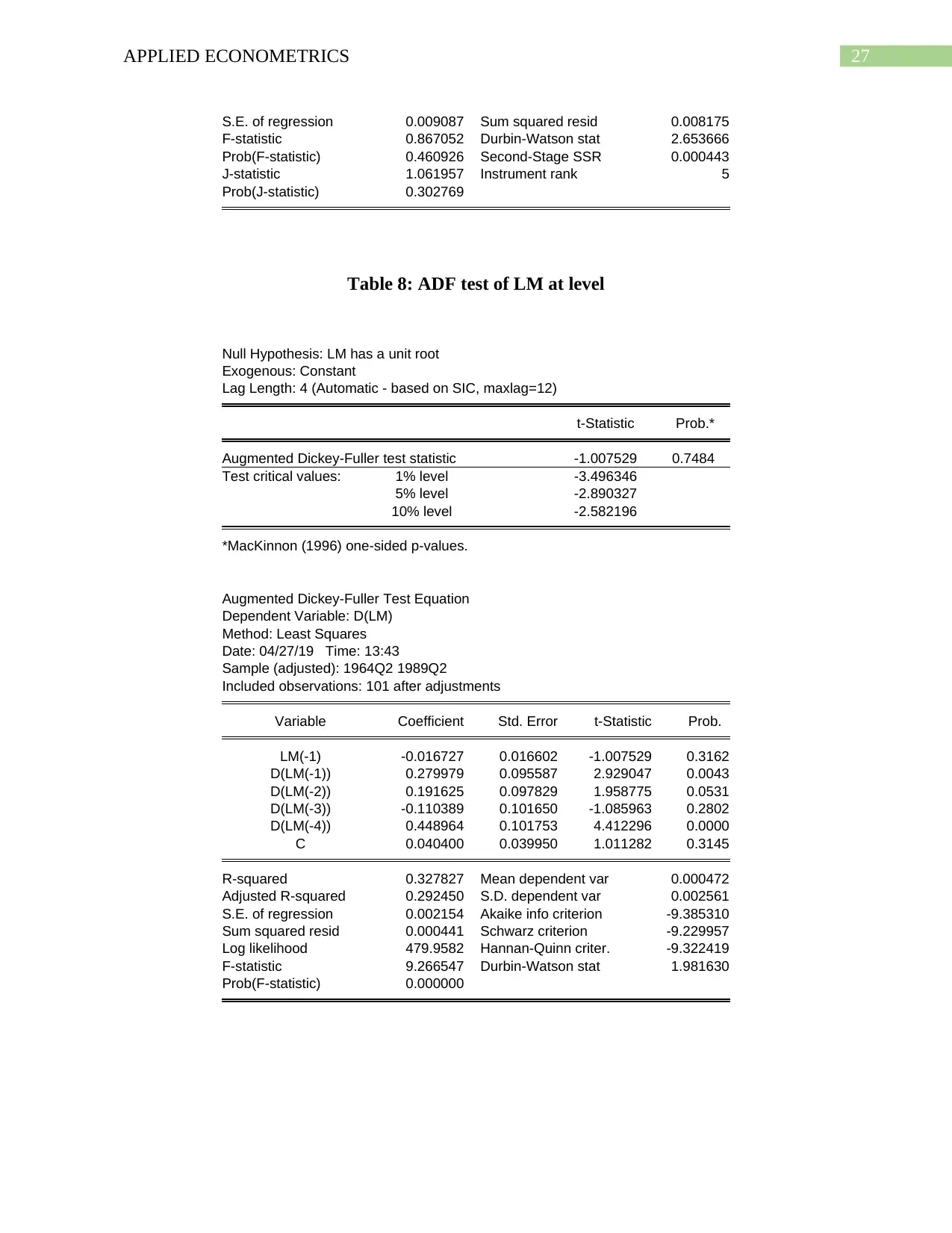

Variable Coefficient Std. Error t-Statistic Prob.

LM(-1) -0.016727 0.016602 -1.007529 0.3162