Shavneel Kumar: Implementing Program Governance and Managing Finances

VerifiedAdded on 2021/05/30

|30

|10361

|56

Homework Assignment

AI Summary

This assignment, completed by student Shavneel Kumar, addresses the core concepts of program governance and financial management within the BSB61215 Advanced Diploma of Program Management. The assessment focuses on implementing program governance, managing finances, and ensuring compliance. The assignment involves answering discussion questions that explore the key roles and responsibilities in program governance, the factors for establishing appropriate finance and resource authorities, and the methods for making reliable program governance decisions. The student's responses cover topics like internal controls, stakeholder engagement, financial planning, budget establishment, and variance analysis. The assessment also covers the use of documented methods such as RACI matrices to ensure repeatable and documented methods for decision-making. The assignment highlights the importance of financial management in the context of program success.

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID and full name 41823 – Shavneel shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

ASSESSMENT INSTRUCTIONS

Overview

Prior to commencing the assessments your assessor will explain each task and the terms and

submission of your task. Please consult your assessor if you are unsure of any questions. It is

important that you understand adhere to the terms and conditions and address each task. If any

task I not fully address than your assessment task will not be marked. The assessor will support

you throughout this process.

Written work

The assessment tasks are used to measure your understanding and underpinning skills and

knowledge of this unit of competency. When answering please ensure you address each criteria

and sub point, demonstrate your research of each of the questions and cover the topic in a

logical and structured manner.

Active participation

It is a condition of enrolment that you actively participate in your studies. Active participation is

completing all tasks on time. If you do not participate you will be required to report to Student

Services Coordinator.

Plagiarism

Plagiarism is taking and using someone else's thoughts, writings or inventions and representing

them as your own. Plagiarism is a serious act and may result in a student’s exclusion from a

course. When you have any doubts about including the work of other authors in your

assessment, please consult your trainer/assessor. The following list outlines some of the

activities for which a student can be accused of plagiarism:

Presenting any work by another individual as one's own unintentionally

Handing in assessments markedly similar to or copied from another student

Presenting the work of another individual or group as their own work

Handing in assessments without the adequate acknowledgement of sources used, including

assessments taken totally or in part from the Internet

If it is identified that you have plagiarised within your assessment task, then we will organise a

meeting to discuss this with you.

Copyright

BSBPMG409 Assessment Tool Version 1 Issued 18/03/2017

Page 1 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID and full name 41823 – Shavneel shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

ASSESSMENT INSTRUCTIONS

Overview

Prior to commencing the assessments your assessor will explain each task and the terms and

submission of your task. Please consult your assessor if you are unsure of any questions. It is

important that you understand adhere to the terms and conditions and address each task. If any

task I not fully address than your assessment task will not be marked. The assessor will support

you throughout this process.

Written work

The assessment tasks are used to measure your understanding and underpinning skills and

knowledge of this unit of competency. When answering please ensure you address each criteria

and sub point, demonstrate your research of each of the questions and cover the topic in a

logical and structured manner.

Active participation

It is a condition of enrolment that you actively participate in your studies. Active participation is

completing all tasks on time. If you do not participate you will be required to report to Student

Services Coordinator.

Plagiarism

Plagiarism is taking and using someone else's thoughts, writings or inventions and representing

them as your own. Plagiarism is a serious act and may result in a student’s exclusion from a

course. When you have any doubts about including the work of other authors in your

assessment, please consult your trainer/assessor. The following list outlines some of the

activities for which a student can be accused of plagiarism:

Presenting any work by another individual as one's own unintentionally

Handing in assessments markedly similar to or copied from another student

Presenting the work of another individual or group as their own work

Handing in assessments without the adequate acknowledgement of sources used, including

assessments taken totally or in part from the Internet

If it is identified that you have plagiarised within your assessment task, then we will organise a

meeting to discuss this with you.

Copyright

BSBPMG409 Assessment Tool Version 1 Issued 18/03/2017

Page 1 of 31

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

You must be careful when copying the work of others. The owner of the material may take legal

action against you if the owner's copyright has been infringed. You are allowed to do a certain

amount of copying for research or study purposes. Generally, 10% or one chapter of a book is

acceptable, where the participant is studying with, or employed by, an educational institution.

Competency Outcomes

Each activity in this assessment tasks will be marked as either Satisfactory or Not

Satisfactory.

If your work is marked as Not Satisfactory you will be provided with feedback from your

assessor and then given time to complete the task. Your assessor will provide you with a timeline

in which you will be required to submit your task. Resubmission timeline will be determined by

the assessor and based on the extent of the re-submission.

When you have completed all tasks in this document you will be granted an overall competency

outcome, which will be either Competent or Not Yet Competent.

If your work is marked as Not Yet Competent you will be asked to resubmit the assessment

tasks as indicated by your assessor. You will not be able to gain competency if any of your tasks

are not fully completed.

Assessment Appeals Process

If you are dissatisfied with the outcome of one of the assessment tasks or the final outcome of

the assessment task because you feel that the result is unfair or incorrect, you may request to

have the task/s or overall assessment task reviewed. If you are still dissatisfied with the

outcome, you may lodge a formal assessment appeal. Refer to SBTA’s Complaints/Appeals Policy

and Procedure.

Application of the unit – BSBFIM601

This unit describes the skills and knowledge required to undertake budgeting, financial

forecasting and reporting and to allocate and manage resources to achieve the required outputs

for the business unit. It includes contributing to financial bids and estimates, allocating funds,

managing budgets and reporting on financial activity.

It applies to individuals who have managerial responsibilities which include overseeing the

management of financial and other resources across a business unit, a series of business units or

teams, or an organisation. It covers all areas of broad financial management. In a larger

organisation, this work would be supported by specialists in financial management.

Application of the unit – BSBPMG612

This unit describes the skills and knowledge required to implement governance requirements to

ensure effective program management. It includes the performance criteria required to

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 2 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

You must be careful when copying the work of others. The owner of the material may take legal

action against you if the owner's copyright has been infringed. You are allowed to do a certain

amount of copying for research or study purposes. Generally, 10% or one chapter of a book is

acceptable, where the participant is studying with, or employed by, an educational institution.

Competency Outcomes

Each activity in this assessment tasks will be marked as either Satisfactory or Not

Satisfactory.

If your work is marked as Not Satisfactory you will be provided with feedback from your

assessor and then given time to complete the task. Your assessor will provide you with a timeline

in which you will be required to submit your task. Resubmission timeline will be determined by

the assessor and based on the extent of the re-submission.

When you have completed all tasks in this document you will be granted an overall competency

outcome, which will be either Competent or Not Yet Competent.

If your work is marked as Not Yet Competent you will be asked to resubmit the assessment

tasks as indicated by your assessor. You will not be able to gain competency if any of your tasks

are not fully completed.

Assessment Appeals Process

If you are dissatisfied with the outcome of one of the assessment tasks or the final outcome of

the assessment task because you feel that the result is unfair or incorrect, you may request to

have the task/s or overall assessment task reviewed. If you are still dissatisfied with the

outcome, you may lodge a formal assessment appeal. Refer to SBTA’s Complaints/Appeals Policy

and Procedure.

Application of the unit – BSBFIM601

This unit describes the skills and knowledge required to undertake budgeting, financial

forecasting and reporting and to allocate and manage resources to achieve the required outputs

for the business unit. It includes contributing to financial bids and estimates, allocating funds,

managing budgets and reporting on financial activity.

It applies to individuals who have managerial responsibilities which include overseeing the

management of financial and other resources across a business unit, a series of business units or

teams, or an organisation. It covers all areas of broad financial management. In a larger

organisation, this work would be supported by specialists in financial management.

Application of the unit – BSBPMG612

This unit describes the skills and knowledge required to implement governance requirements to

ensure effective program management. It includes the performance criteria required to

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 2 of 31

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

demonstrate competency in implementing systems and processes for decision-making,

management systems, compliance and support.

A program is defined as a set of interrelated projects, each of which has a project manager.

'Multiple projects', or 'a program of projects', refers to a number of related projects managed by

the same person as a program to achieve organisational objective/s.

It applies to individuals who are program managers and those managing a suite of projects (a

program). They operate within assigned authority levels, are responsible for their own

performance and sometimes the performance of others.

Individuals in this role may be operating within an organisation, a business or working as a

consultant.

Assessment matrix

ELEMENTS BSBPMG612 PERFORMANCE CRITERIA ASSESSMENT TASKS

1. Facilitate effective decisions making 1.1, 1.2, 1.3, 1.4 Task 1, 2

2. Implement systems and methods 2.1, 2.2, 2.3, 2.4 Task 1, 2

3. Ensure program compliance 3.1, 3.2, 3.3, 3.4 Task 1, 2

4. Enable program support services 4.1, 4.2, 4.3 Task 1, 2

Performance Evidence Document program role and responsibilities, determine finance and

resource authorities, support program implementation

Task 1, 2

Knowledge Evidence Documentation of program role and responsibilities, design

program, records and configuration system

Task 1, 2

Foundation Skills Reading, Writing, Oral Communication, Navigate the world of work,

interact with others and Get the work done

Task 1, 2

Dimensions of Competency Task skills, task management skills, communication management

skills, analysis & problem solving skills

Task 1, 2

ELEMENTS BSBFIM606 PERFORMANCE CRITERIA ASSESSMENT TASKS

1.1. Plan for financial management 1.1, 1.2, 1.3, 1.6 Task 1, 3

1.2. Establish budgets and allocate funds 2.1, 2.2, 2.3 Task 1, 3

1.3. Implement budgets 3.1, 3.2, 3.3, 3.4, 3.5, 3.6 Task 1, 3

1.4. Report on finances 4.1, 4.2, 4.3, 4.4 Task 1, 3

Performance Evidence Plan for financial management, prepare, implement and revise a Task 1, 3

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 3 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

demonstrate competency in implementing systems and processes for decision-making,

management systems, compliance and support.

A program is defined as a set of interrelated projects, each of which has a project manager.

'Multiple projects', or 'a program of projects', refers to a number of related projects managed by

the same person as a program to achieve organisational objective/s.

It applies to individuals who are program managers and those managing a suite of projects (a

program). They operate within assigned authority levels, are responsible for their own

performance and sometimes the performance of others.

Individuals in this role may be operating within an organisation, a business or working as a

consultant.

Assessment matrix

ELEMENTS BSBPMG612 PERFORMANCE CRITERIA ASSESSMENT TASKS

1. Facilitate effective decisions making 1.1, 1.2, 1.3, 1.4 Task 1, 2

2. Implement systems and methods 2.1, 2.2, 2.3, 2.4 Task 1, 2

3. Ensure program compliance 3.1, 3.2, 3.3, 3.4 Task 1, 2

4. Enable program support services 4.1, 4.2, 4.3 Task 1, 2

Performance Evidence Document program role and responsibilities, determine finance and

resource authorities, support program implementation

Task 1, 2

Knowledge Evidence Documentation of program role and responsibilities, design

program, records and configuration system

Task 1, 2

Foundation Skills Reading, Writing, Oral Communication, Navigate the world of work,

interact with others and Get the work done

Task 1, 2

Dimensions of Competency Task skills, task management skills, communication management

skills, analysis & problem solving skills

Task 1, 2

ELEMENTS BSBFIM606 PERFORMANCE CRITERIA ASSESSMENT TASKS

1.1. Plan for financial management 1.1, 1.2, 1.3, 1.6 Task 1, 3

1.2. Establish budgets and allocate funds 2.1, 2.2, 2.3 Task 1, 3

1.3. Implement budgets 3.1, 3.2, 3.3, 3.4, 3.5, 3.6 Task 1, 3

1.4. Report on finances 4.1, 4.2, 4.3, 4.4 Task 1, 3

Performance Evidence Plan for financial management, prepare, implement and revise a Task 1, 3

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 3 of 31

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

budget, allocate funds and analyse effectiveness of approach

Knowledge Evidence Financial probity, principles of accounting and financial systems,

legislation

Task 1, 3

Foundation Skills Reading, Writing, Oral Communication, Numeracy, Navigate the

world of work, interact with others and Get the work done

Task 1, 3

Dimensions of Competency Task skills, task management skills, communication management

skills, analysis & problem solving skills

Task 1, 3

Assessment task 1: Knowledge and Discussion Questions

Information to students:

This assessment task will enable you to demonstrate your knowledge of:

Implementing program governance

Managing financial

To complete this assessment task, you can research your answers using books provided or

the Internet but your answers must be in your own words.

At the end of this task your assessor will give you feedback. Your assessor will also check all

your answers; if your answers have been copied from other students from your current or

other classes you will be required to resubmit this task again.

Please clarify any questions which you do not understand fully with your trainer and

assessor prior to you completing each question to ensure you are answering your questions

correctly.

Please note that this task is to be typed up when you are submitting the task for marking

unless specified otherwise.

Questions:

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 4 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

budget, allocate funds and analyse effectiveness of approach

Knowledge Evidence Financial probity, principles of accounting and financial systems,

legislation

Task 1, 3

Foundation Skills Reading, Writing, Oral Communication, Numeracy, Navigate the

world of work, interact with others and Get the work done

Task 1, 3

Dimensions of Competency Task skills, task management skills, communication management

skills, analysis & problem solving skills

Task 1, 3

Assessment task 1: Knowledge and Discussion Questions

Information to students:

This assessment task will enable you to demonstrate your knowledge of:

Implementing program governance

Managing financial

To complete this assessment task, you can research your answers using books provided or

the Internet but your answers must be in your own words.

At the end of this task your assessor will give you feedback. Your assessor will also check all

your answers; if your answers have been copied from other students from your current or

other classes you will be required to resubmit this task again.

Please clarify any questions which you do not understand fully with your trainer and

assessor prior to you completing each question to ensure you are answering your questions

correctly.

Please note that this task is to be typed up when you are submitting the task for marking

unless specified otherwise.

Questions:

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 4 of 31

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

Read all discussion points below in class with your colleagues and your trainer and assessor,

and provide answers to each question below.

Answer guide: This assessment task is to be typed with 2 – 5 paragraphs per question

1.1. What roles are required for effective program governance and how you would agree

the key roles, accountabilities and responsibilities with senior stakeholders?

The issue that has been presented in the question refers to the fact that the roles that are required

for the purpose of maintaining effective governance in an organization is that of an executive or a

manager who is required to look after the internal controls that has been implemented within an

organization. This means that the internal controls play a significant role in the controlling of the

aspect of corporate governance in an organization. This means that the different roles also include

the role of an auditor who is willing to audit the quality of the corporate governance statement

(Martinelli and Milosevic 2016).

Moreover, the key roles responsibilities and accountabilities that have been carried out by

the senior stakeholders are also important in developing effective program governance. This

means that the stakeholders on the basis of the agency and the stakeholder theory will result in

the proper establishment of the fact that the stakeholders will certainly have an opinion in regards

to the development of a corporate governance statement. For instance, a veto that is given by a

senior stakeholder will result in the stoppage of a project.

1.2. What factors would need to be considered to ensure that the appropriate finance and

resource authorities were in place with senior stakeholders, throughout the program?

The factors that are needed to be considered for the purpose of ensuring that the appropriate

finance and resource authorities are in place with the senior stakeholders throughout the program

are as follows:

The appropriate finance and the resource authorities will be in place with the senior

stakeholders when the development of a corporate governance statement will result in the

generation of optimum amount profitability of the corporate entity.

the appropriate type of finance that is required will have to be decided by the executives

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 5 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

Read all discussion points below in class with your colleagues and your trainer and assessor,

and provide answers to each question below.

Answer guide: This assessment task is to be typed with 2 – 5 paragraphs per question

1.1. What roles are required for effective program governance and how you would agree

the key roles, accountabilities and responsibilities with senior stakeholders?

The issue that has been presented in the question refers to the fact that the roles that are required

for the purpose of maintaining effective governance in an organization is that of an executive or a

manager who is required to look after the internal controls that has been implemented within an

organization. This means that the internal controls play a significant role in the controlling of the

aspect of corporate governance in an organization. This means that the different roles also include

the role of an auditor who is willing to audit the quality of the corporate governance statement

(Martinelli and Milosevic 2016).

Moreover, the key roles responsibilities and accountabilities that have been carried out by

the senior stakeholders are also important in developing effective program governance. This

means that the stakeholders on the basis of the agency and the stakeholder theory will result in

the proper establishment of the fact that the stakeholders will certainly have an opinion in regards

to the development of a corporate governance statement. For instance, a veto that is given by a

senior stakeholder will result in the stoppage of a project.

1.2. What factors would need to be considered to ensure that the appropriate finance and

resource authorities were in place with senior stakeholders, throughout the program?

The factors that are needed to be considered for the purpose of ensuring that the appropriate

finance and resource authorities are in place with the senior stakeholders throughout the program

are as follows:

The appropriate finance and the resource authorities will be in place with the senior

stakeholders when the development of a corporate governance statement will result in the

generation of optimum amount profitability of the corporate entity.

the appropriate type of finance that is required will have to be decided by the executives

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 5 of 31

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

or the other official bodies for the purpose of determining the fact as to what kind of debt

should be considered for the purpose of developing the statement.

Moreover, it is very important to analyse the sources of funding that is required for the

purpose of implementing the project. The sources of funding might be the long term or

short term sources of finance. This can be carried out by comparing the paybacks or the

internal rates of returns between the projects in which an estimate of the costs of the

projects are made.

A budget should also be established and the calculation of the overall projects costs have

to be estimated by the totalling of the individual activity costs

The management should also take an initiative to develop a variance analysis for the

purpose of understanding the value of the projects.

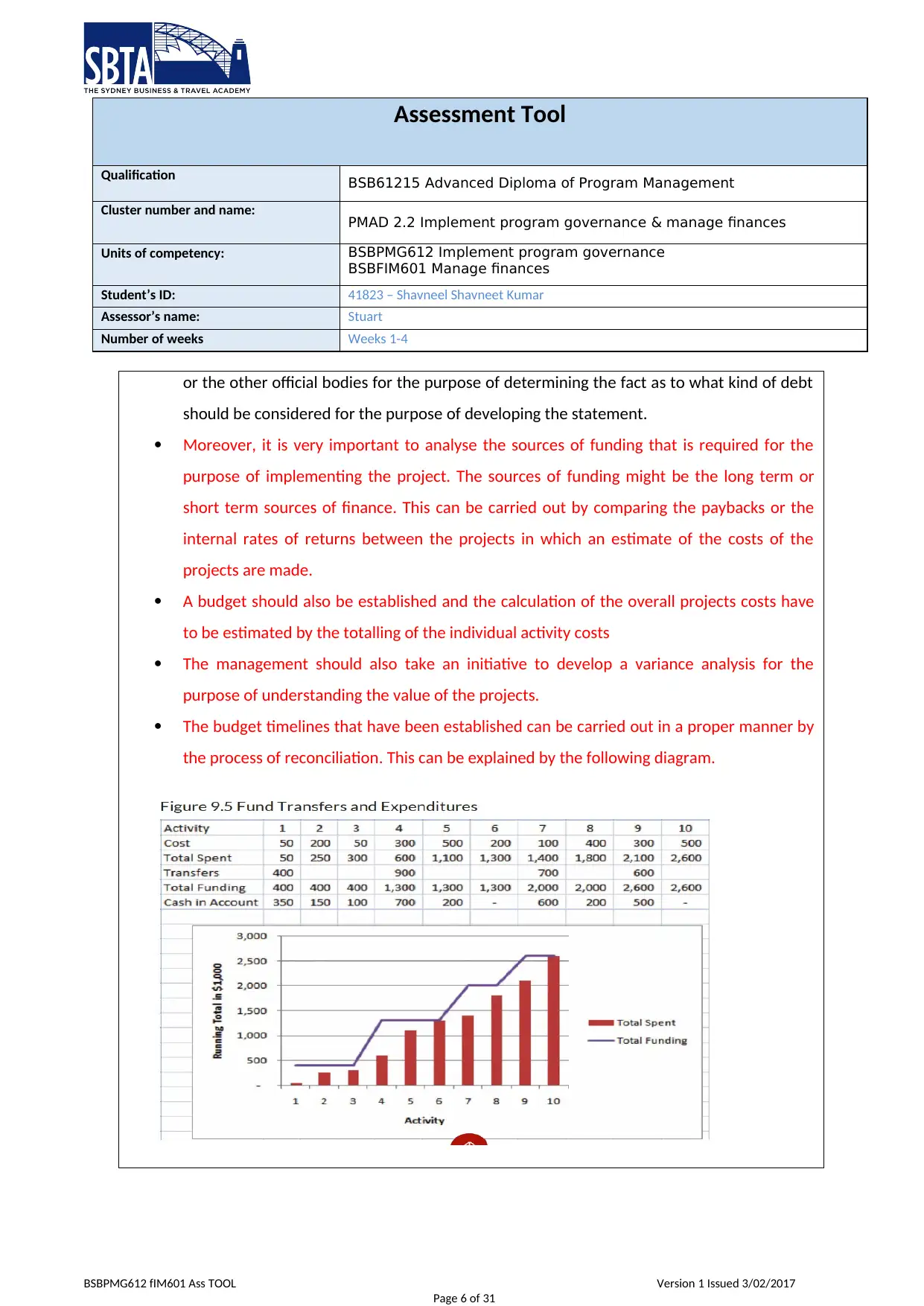

The budget timelines that have been established can be carried out in a proper manner by

the process of reconciliation. This can be explained by the following diagram.

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 6 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

or the other official bodies for the purpose of determining the fact as to what kind of debt

should be considered for the purpose of developing the statement.

Moreover, it is very important to analyse the sources of funding that is required for the

purpose of implementing the project. The sources of funding might be the long term or

short term sources of finance. This can be carried out by comparing the paybacks or the

internal rates of returns between the projects in which an estimate of the costs of the

projects are made.

A budget should also be established and the calculation of the overall projects costs have

to be estimated by the totalling of the individual activity costs

The management should also take an initiative to develop a variance analysis for the

purpose of understanding the value of the projects.

The budget timelines that have been established can be carried out in a proper manner by

the process of reconciliation. This can be explained by the following diagram.

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 6 of 31

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

1.3. How do you ensure that reliable program governance decisions regarding complex

priorities and competing demands on the program were made using repeatable and

documented methods?

The issue that has been presented in the question refers to the fact as to how it has been

determined that the reliable program governance decisions in regards to the priorities that have

been complicated in nature and the competitive demands on the program were made using

documented and repeatable methods. This can be ensured with the help of the fact that results

that have been drawn are in accordance to the results that have been drawn from the industrial

benchmark of the company. Moreover, the issue of documented methods can also be found in the

papers that have states the details. A RACI matrix can be used for this purpose. The acronym RACI

stands for responsible, accountable, consulted and informed. Therefore, a RACI matrix consists of

the decisions and the activities that should be taken by an authority for the people belonging to an

organization.

1.4. Why is it important to compare decision making processes and outcomes against

program objectives?

It is important to carry out the comparison between the decision making processes and

outcomes that have been derived from the objectives of the program in order to analyze the

importance of the different components of the corporate governance statement. This means that

if the objectives of the corporate governance statement match with the outcomes of the same

then the corporate governance that will be established in the company will result in the achieving

of the desired results. Moreover, the comparison will also help in the identification of the

loopholes of the management of the company. Furthermore, the use of the correct procedures will

help in the attainment of the program objectives.

1.5. How do program controls help ensure program governance makes timely and

effective decisions?

The program controls that help in the ensuring the program governance will make timely and

effective decisions are generally the internal controls that have been established within a

corporate entity. This means that the internal controls that are incorporated within the structure

of a company results in the identification of the fact accounting statements to where are the

loopholes of the organization and where is the scope to implement improved controls with the

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 7 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

1.3. How do you ensure that reliable program governance decisions regarding complex

priorities and competing demands on the program were made using repeatable and

documented methods?

The issue that has been presented in the question refers to the fact as to how it has been

determined that the reliable program governance decisions in regards to the priorities that have

been complicated in nature and the competitive demands on the program were made using

documented and repeatable methods. This can be ensured with the help of the fact that results

that have been drawn are in accordance to the results that have been drawn from the industrial

benchmark of the company. Moreover, the issue of documented methods can also be found in the

papers that have states the details. A RACI matrix can be used for this purpose. The acronym RACI

stands for responsible, accountable, consulted and informed. Therefore, a RACI matrix consists of

the decisions and the activities that should be taken by an authority for the people belonging to an

organization.

1.4. Why is it important to compare decision making processes and outcomes against

program objectives?

It is important to carry out the comparison between the decision making processes and

outcomes that have been derived from the objectives of the program in order to analyze the

importance of the different components of the corporate governance statement. This means that

if the objectives of the corporate governance statement match with the outcomes of the same

then the corporate governance that will be established in the company will result in the achieving

of the desired results. Moreover, the comparison will also help in the identification of the

loopholes of the management of the company. Furthermore, the use of the correct procedures will

help in the attainment of the program objectives.

1.5. How do program controls help ensure program governance makes timely and

effective decisions?

The program controls that help in the ensuring the program governance will make timely and

effective decisions are generally the internal controls that have been established within a

corporate entity. This means that the internal controls that are incorporated within the structure

of a company results in the identification of the fact accounting statements to where are the

loopholes of the organization and where is the scope to implement improved controls with the

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 7 of 31

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

corporate entity. Moreover, the program controls that ensures the governance of the program.

This means that the program governance will result in effective and timely decisions. The

effectiveness of the controls which are being established within an organization should be timely in

nature.

1.6. What program management systems might be used to ensure effective program

governance takes place?

The program management systems that can be used for the purpose of ensuring effective program

governance is that the management of the program can be carried out with the help of the

different tools and techniques that can be utilized for the purpose of developing the governance

programs are the development of a systematic approach towards the program management

systems. The other types of software that can be utilized for the purpose of the project refer to the

fact that the management might develop a particular kind of governance program. There should be

specific project management systems for the planning of the project in regards to the estimation of

the costs, valuation of the projects and the selection of the right kind of staff for the project.

1.7. How can a program management office help with program governance and delivery?

The program management office can help with the process of program governance and delivery by

effectively leading to the development of a structure that is not effective in regards to the

particular project. This means that an effective program management will result in the

development of an effective corporate governance program that will effectively delivering of the

desired products. This means that the management of the program aims to determine the quality

of the product that it delivers. In case of the process of project management, the support of the

admin who is at the top of a project is very important. The delivery of the scheduling mechanisms

is another important part of the program, which has to be considered and carried out properly.

Moreover, the issues that are related to business management has to be carefully dealt with by

the member of the project management group.

1.8. What audit and/or compliance requirements would you need to factor in when

designing program governance?

At the time of designing the program governance, the compliance requirements that should be

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 8 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

corporate entity. Moreover, the program controls that ensures the governance of the program.

This means that the program governance will result in effective and timely decisions. The

effectiveness of the controls which are being established within an organization should be timely in

nature.

1.6. What program management systems might be used to ensure effective program

governance takes place?

The program management systems that can be used for the purpose of ensuring effective program

governance is that the management of the program can be carried out with the help of the

different tools and techniques that can be utilized for the purpose of developing the governance

programs are the development of a systematic approach towards the program management

systems. The other types of software that can be utilized for the purpose of the project refer to the

fact that the management might develop a particular kind of governance program. There should be

specific project management systems for the planning of the project in regards to the estimation of

the costs, valuation of the projects and the selection of the right kind of staff for the project.

1.7. How can a program management office help with program governance and delivery?

The program management office can help with the process of program governance and delivery by

effectively leading to the development of a structure that is not effective in regards to the

particular project. This means that an effective program management will result in the

development of an effective corporate governance program that will effectively delivering of the

desired products. This means that the management of the program aims to determine the quality

of the product that it delivers. In case of the process of project management, the support of the

admin who is at the top of a project is very important. The delivery of the scheduling mechanisms

is another important part of the program, which has to be considered and carried out properly.

Moreover, the issues that are related to business management has to be carefully dealt with by

the member of the project management group.

1.8. What audit and/or compliance requirements would you need to factor in when

designing program governance?

At the time of designing the program governance, the compliance requirements that should be

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 8 of 31

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

utilized are that the nature of the program should be defined. The other factors include the

determination of the aspect or the objective of the program. Moreover, at the time of designing

the program governance the factors that should be incorporated are that the corporate

governance statement should be free of any kind of error or misstatement (Hutchings and Shipway

2017). The financial/ IT/ legal compliance that is mandatory for all corporate entities to maintain

should be strictly adhered to.

1.9. How would records be securely maintained to ensure appropriate access and

currency of information?

The records that are required for the for the purpose of maintaining the corporate governance

statement refers to the essential documents of the corporate entity whose corporate governance

program is being designed. This means that the documents are vital in the preparation of the

program and should be maintained securely for the purpose of ensuring appropriate access and

currency of information. This can be achieved by the proper installation of security system within

the corporate organization along with the proper accessory passwords and other data back -up

techniques and tools.

1.10. What steps would you take to rectify a program compliance issue?

The steps that should be incorporated for the purpose of rectifying a compliance issue in regards

to a program refers to the fact that the corporate governance statement or the governance

program should be prepared in such a way that the rectification of the compliance issue has been

carried out in the desired way. Moreover, the other factors that have been included are that the

governance statement that affects the delivery of the program should be effectively amended. The

actions that should be taken for a compliance issue depends on the level of non-compliance that

has been carried out by the staff or other members of the organization.

1.11. What consequences can occur if program governance does not act in an appropriate

and ethical manner when handling compliance issues?

The issue that has been presented in the question is that the consequences that can occur if the

aspect of program governance fails to act in the most appropriate way. The particular happening

that takes place, might result in the development of the corporate standards that are not right or

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 9 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

utilized are that the nature of the program should be defined. The other factors include the

determination of the aspect or the objective of the program. Moreover, at the time of designing

the program governance the factors that should be incorporated are that the corporate

governance statement should be free of any kind of error or misstatement (Hutchings and Shipway

2017). The financial/ IT/ legal compliance that is mandatory for all corporate entities to maintain

should be strictly adhered to.

1.9. How would records be securely maintained to ensure appropriate access and

currency of information?

The records that are required for the for the purpose of maintaining the corporate governance

statement refers to the essential documents of the corporate entity whose corporate governance

program is being designed. This means that the documents are vital in the preparation of the

program and should be maintained securely for the purpose of ensuring appropriate access and

currency of information. This can be achieved by the proper installation of security system within

the corporate organization along with the proper accessory passwords and other data back -up

techniques and tools.

1.10. What steps would you take to rectify a program compliance issue?

The steps that should be incorporated for the purpose of rectifying a compliance issue in regards

to a program refers to the fact that the corporate governance statement or the governance

program should be prepared in such a way that the rectification of the compliance issue has been

carried out in the desired way. Moreover, the other factors that have been included are that the

governance statement that affects the delivery of the program should be effectively amended. The

actions that should be taken for a compliance issue depends on the level of non-compliance that

has been carried out by the staff or other members of the organization.

1.11. What consequences can occur if program governance does not act in an appropriate

and ethical manner when handling compliance issues?

The issue that has been presented in the question is that the consequences that can occur if the

aspect of program governance fails to act in the most appropriate way. The particular happening

that takes place, might result in the development of the corporate standards that are not right or

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 9 of 31

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

has been falling upon the employees of the organization. This means that the different standards

that have been utilized might result in the ruining of the compliance issue in case the program

governance does not act in an ethical or appropriate manner. In case of a breach in the ethical

standards of the program, the consequences can be as severe as the cancelling of the license of a

project.

1.12. What kinds of management and governance support needs do programs have?

The management and the governance support that the programs need to have refer to the fact

that the governance needs in goods should be properly defined and clarified for the purpose of

defining the program. Moreover, the management and the governance support that should be

included for developing a corporate governance statement refer to the fact that the management

of the organization should be aware about the needs and particulars of the corporate entity. This

means that the governance support that the program should receive is that the program should be

defined in the nature of the objectives that it aims to fulfil. The senior stakeholders or the

management of a corporate entity is also skilled at the process of strategic reporting that is

effective in the selection of the projects. Moreover, the section of the projects can be carried out

with the help of the different techniques like NPV and other payback methods. (Regezi et al. 2016).

1.13. What steps would you need to take to establish skill development support systems

for program personnel to meet program needs?

The steps that are needed to be incorporated for the purpose of establishment of the skill

development support system refer to the fact that the program personnel should meet up to the

needs of the program. This means that the program personnel should be skilled enough in order to

understand and carry out the requirements of the program. Moreover, the other requirements

include that the program personnel should be a good communicator. This is due to the fact that

the skill development system has been designed in such a way that it should be explained to the

different members of the organization. This means that the skill development support system

should be established in such a way that the program personnel get to understand and know about

the developments that have been incorporated. It should be noted here that it is also very

important to train the staff in order to enhance their degree of performance.

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 10 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

has been falling upon the employees of the organization. This means that the different standards

that have been utilized might result in the ruining of the compliance issue in case the program

governance does not act in an ethical or appropriate manner. In case of a breach in the ethical

standards of the program, the consequences can be as severe as the cancelling of the license of a

project.

1.12. What kinds of management and governance support needs do programs have?

The management and the governance support that the programs need to have refer to the fact

that the governance needs in goods should be properly defined and clarified for the purpose of

defining the program. Moreover, the management and the governance support that should be

included for developing a corporate governance statement refer to the fact that the management

of the organization should be aware about the needs and particulars of the corporate entity. This

means that the governance support that the program should receive is that the program should be

defined in the nature of the objectives that it aims to fulfil. The senior stakeholders or the

management of a corporate entity is also skilled at the process of strategic reporting that is

effective in the selection of the projects. Moreover, the section of the projects can be carried out

with the help of the different techniques like NPV and other payback methods. (Regezi et al. 2016).

1.13. What steps would you need to take to establish skill development support systems

for program personnel to meet program needs?

The steps that are needed to be incorporated for the purpose of establishment of the skill

development support system refer to the fact that the program personnel should meet up to the

needs of the program. This means that the program personnel should be skilled enough in order to

understand and carry out the requirements of the program. Moreover, the other requirements

include that the program personnel should be a good communicator. This is due to the fact that

the skill development system has been designed in such a way that it should be explained to the

different members of the organization. This means that the skill development support system

should be established in such a way that the program personnel get to understand and know about

the developments that have been incorporated. It should be noted here that it is also very

important to train the staff in order to enhance their degree of performance.

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 10 of 31

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

1.14.What factors would you need to consider designing and effective program knowledge

management system that can support current and future organisation requirements, for

program development?

The factors that are needed to be considered for the designing of the program knowledge

management system that will help in the supporting of the current and the future organizational

needs is that the development of the program, should be carried out in a particular way. This

means that the information that has been delivered by it is easy to understand and undertake.

Moreover, the other considerations include the conveying of the information should be simple and

in accordance to the needs of the organization.

1.15. What is meant by financial probity?

Financial probity refers to the standard of ethics that have been maintained for the purpose of

ensuring the fact that whether the financial statements of the corporate entity have been

prepared in accordance to the delegated standards of ethics. Moreover, the other considerations

that have been included refer to the fact that the aspect financial probity is a primary requirement

in the different corporate organizations and is an important topic for the purpose of ensuring the

fact that the audit of the financial statements have been carried out with the required number of

ethical standards.

1.16. Describe the principles of accounting and financial systems

The principles of accounting and financial systems refer to the fact that the principles that have

been adhered to while preparing the financial statements of the corporate organization. The

management of the corporate entities takes an optimum amount of initiative for the purpose of

developing the accounting standards that should be adhered to while preparing the financial

statements. The accounting regulatory bodies of the different countries have developed these

accounting standards (Rashid 2017). This means that the principles of accounting and financial

systems are developed by the accounting regulatory bodies on the basis of the regulatory settings

and other social, political or economic settings of the country to which the accounting body

belongs to. These principles like the double entry principle states that each entry should be made

twice in order to cancel out their effects. These accounting principles act as the base of the subject.

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 11 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

1.14.What factors would you need to consider designing and effective program knowledge

management system that can support current and future organisation requirements, for

program development?

The factors that are needed to be considered for the designing of the program knowledge

management system that will help in the supporting of the current and the future organizational

needs is that the development of the program, should be carried out in a particular way. This

means that the information that has been delivered by it is easy to understand and undertake.

Moreover, the other considerations include the conveying of the information should be simple and

in accordance to the needs of the organization.

1.15. What is meant by financial probity?

Financial probity refers to the standard of ethics that have been maintained for the purpose of

ensuring the fact that whether the financial statements of the corporate entity have been

prepared in accordance to the delegated standards of ethics. Moreover, the other considerations

that have been included refer to the fact that the aspect financial probity is a primary requirement

in the different corporate organizations and is an important topic for the purpose of ensuring the

fact that the audit of the financial statements have been carried out with the required number of

ethical standards.

1.16. Describe the principles of accounting and financial systems

The principles of accounting and financial systems refer to the fact that the principles that have

been adhered to while preparing the financial statements of the corporate organization. The

management of the corporate entities takes an optimum amount of initiative for the purpose of

developing the accounting standards that should be adhered to while preparing the financial

statements. The accounting regulatory bodies of the different countries have developed these

accounting standards (Rashid 2017). This means that the principles of accounting and financial

systems are developed by the accounting regulatory bodies on the basis of the regulatory settings

and other social, political or economic settings of the country to which the accounting body

belongs to. These principles like the double entry principle states that each entry should be made

twice in order to cancel out their effects. These accounting principles act as the base of the subject.

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 11 of 31

Assessment Tool

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

1.17. What are INCOTERMS?

INCOTERM refers to the particular process that should be incorporated by a seller of a particular

good that needs to be transported. This means that the seller has the responsibility to take up the

cost in regards to the transporting of the goods and also is responsible for the insurance in regards

to the shipping of the goods to the particular destination point. This means that the seller falls

under the effect of the term, INCOTERM. Moreover, it has been founded out that the seller has to

bear the risk of carrying the product and also has to take up the responsibility of insurance of the

goods that have to be transferred to the point of destination.

1.18. What is the trades practice Act?

The trade practices act refers to that particular act that has been defined as an Act that will result

in the providence of the operation of the economic system does not result in the concentration of

economic power to the common detriment. This is for the control of monopolies, for the

prohibition of monopolistic and restrictive trade practices and for matters connected therewith or

incidental thereto. Therefore, this is known accounting statements the Trade Practices Act

1.19. What is the World Trade Organisation?

The World Trade Organization refers to the point of purchase that has been constructed in order to

access a common link for the purpose of developing the unison of the different business links and

other related issues. This means that the World Trade Organization acts accounting statements

centre of trade for different organizations and institutions. This means that the different

organizations that have been developed under a particular type of business should be registered

under the official bodies of the World Trade Organization (Larsen and Marx 2017).

1.20. What are Bilateral and Regional Free Trade Agreements?

"Trade" means any trade, business, industry, profession or occupation relating to the production,

supply, distribution or control of goods and includes the provision of any services;

"trade association" means a body of persons (whether incorporated or not) which is formed for the

purpose of furthering the trade interests of its members or of persons represented by its

members; "trade practice" means any practice relating to the carrying on of any trade. Moreover,

it includes-anything done by any person which controls or affects the price charged by, or the

method of trading of, any trader or any class of trader; a single or isolated action of any person in

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 12 of 31

Qualification BSB61215 Advanced Diploma of Program Management

Cluster number and name: PMAD 2.2 Implement program governance & manage finances

Units of competency: BSBPMG612 Implement program governance

BSBFIM601 Manage finances

Student’s ID: 41823 – Shavneel Shavneet Kumar

Assessor’s name: Stuart

Number of weeks Weeks 1-4

1.17. What are INCOTERMS?

INCOTERM refers to the particular process that should be incorporated by a seller of a particular

good that needs to be transported. This means that the seller has the responsibility to take up the

cost in regards to the transporting of the goods and also is responsible for the insurance in regards

to the shipping of the goods to the particular destination point. This means that the seller falls

under the effect of the term, INCOTERM. Moreover, it has been founded out that the seller has to

bear the risk of carrying the product and also has to take up the responsibility of insurance of the

goods that have to be transferred to the point of destination.

1.18. What is the trades practice Act?

The trade practices act refers to that particular act that has been defined as an Act that will result

in the providence of the operation of the economic system does not result in the concentration of

economic power to the common detriment. This is for the control of monopolies, for the

prohibition of monopolistic and restrictive trade practices and for matters connected therewith or

incidental thereto. Therefore, this is known accounting statements the Trade Practices Act

1.19. What is the World Trade Organisation?

The World Trade Organization refers to the point of purchase that has been constructed in order to

access a common link for the purpose of developing the unison of the different business links and

other related issues. This means that the World Trade Organization acts accounting statements

centre of trade for different organizations and institutions. This means that the different

organizations that have been developed under a particular type of business should be registered

under the official bodies of the World Trade Organization (Larsen and Marx 2017).

1.20. What are Bilateral and Regional Free Trade Agreements?

"Trade" means any trade, business, industry, profession or occupation relating to the production,

supply, distribution or control of goods and includes the provision of any services;

"trade association" means a body of persons (whether incorporated or not) which is formed for the

purpose of furthering the trade interests of its members or of persons represented by its

members; "trade practice" means any practice relating to the carrying on of any trade. Moreover,

it includes-anything done by any person which controls or affects the price charged by, or the

method of trading of, any trader or any class of trader; a single or isolated action of any person in

BSBPMG612 fIM601 Ass TOOL Version 1 Issued 3/02/2017

Page 12 of 31

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.