Assignment Front Sheet Learner Name Learner Student I.D. Assessor Name Navroop Sandhu 1017470 Mr. LAM

VerifiedAdded on 2022/02/15

|36

|9707

|279

Assignment

AI Summary

LAM Date issued Submission Deadline Submission Date 11th October 2021 9th December 2021 Resubmission Deadline (If appropriate) Re: Submission Date (If appropriate) Internal Verifier Name Internal Verification Deadline Qualification Unit number and title Pearson BTEC Level 5 Higher National Diploma in Business Unit 10: Financial Accounting Assignment title Assignment: Double entry book-keeping, Preparation of Final Accounts, Bank Reconciliation, Suspense and Control Accounts Criteria reference To achieve the criteria the evidence must show that the student is able to: Evidence

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Assignment front sheet

Learner name Learner Student I.D. Assessor Name

Navroop Sandhu 1017470 Mr. LAM

Date issued Submission Deadline Submission Date

11th October 2021

9th December 2021

Resubmission Deadline (If appropriate) Resubmission Date (If appropriate)

Internal Verifier Name Internal Verification Deadline

Qualification Unit number and title

Pearson BTEC Level 5 Higher National Diploma

in Business Unit 10: Financial Accounting

Assignment

title

Assignment: Double entry book-keeping, Preparation of Final Accounts, Bank

Reconciliation, Suspense and Control Accounts

Criteria

reference To achieve the criteria the evidence must show that the student is able to: Evidence

(Page no.)

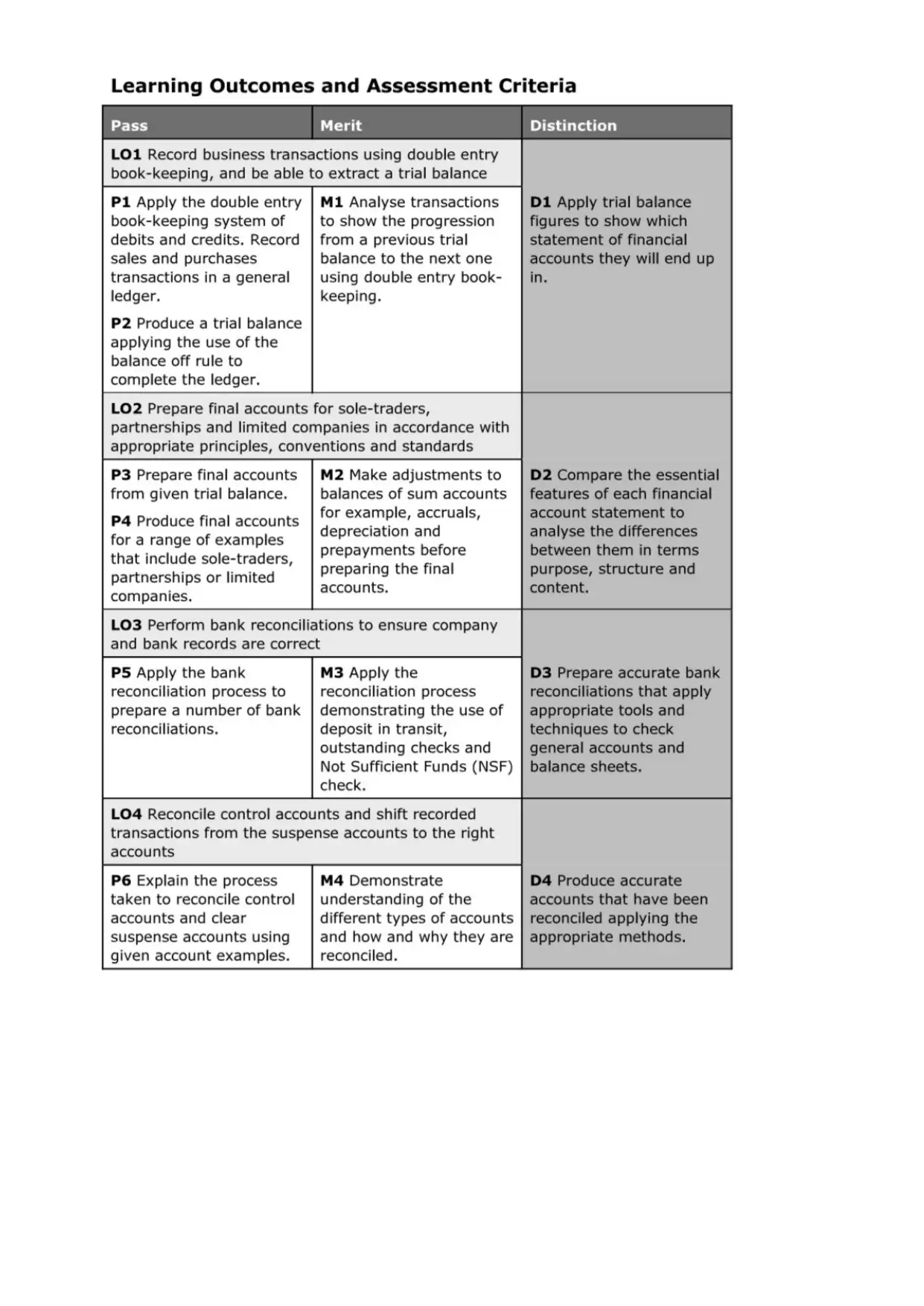

LO1 Record business transactions using double entry book-keeping, and be able to extract a trial balance

P1 Apply the double entry book-keeping system of debits and credits. Record sales and

purchases transactions in a general ledger. 16

P2 Produce a trial balance applying the use of the balance off rule to complete the ledger. 20-22

M1 Analyse transactions to show the progression from a previous trial balance to the next

one using double entry bookkeeping. 22-23

D1 Apply trial balance figures to show which statement of financial accounts they will end

up in. 16-23

LO2 Prepare final accounts for sole-traders, partnerships and limited companies in accordance with

appropriate principles, conventions and standards.

P3 Prepare final accounts from given trial balance. 24

P4 Produce final accounts for a range of examples that include sole-traders,

partnerships or limited companies 26-27

M2 Make adjustments to balances of sum accounts for example, accruals, depreciation

and prepayments before preparing the final accounts. 25

D2 Compare the essential features of each financial account statement to analyse the

differences between them in terms, purpose, structure and content. 28

LO3 Perform bank reconciliations to ensure company and bank records are correct

P5 Apply the bank reconciliation process to prepare a number of bank reconciliations. 32

M3 Apply the reconciliation process, demonstrating the use of deposit in transit, outstanding

checks and Not Sufficient Funds (NSF) check. 33

D3 Prepare accurate bank reconciliations that apply appropriate tools and techniques to

check general accounts and balance sheets.

LO4 Reconcile control accounts and shift recorded transactions from the suspense accounts to the right

accounts

P6 Explain the process taken to reconcile control accounts and clear suspense accounts

using given account examples. 33-34

M4 Demonstrate understanding of the different types of accounts and how and why they

are reconciled.

D4 Produce accurate accounts that have been reconciled applying the appropriate

methods. 34-35

Learner name Learner Student I.D. Assessor Name

Navroop Sandhu 1017470 Mr. LAM

Date issued Submission Deadline Submission Date

11th October 2021

9th December 2021

Resubmission Deadline (If appropriate) Resubmission Date (If appropriate)

Internal Verifier Name Internal Verification Deadline

Qualification Unit number and title

Pearson BTEC Level 5 Higher National Diploma

in Business Unit 10: Financial Accounting

Assignment

title

Assignment: Double entry book-keeping, Preparation of Final Accounts, Bank

Reconciliation, Suspense and Control Accounts

Criteria

reference To achieve the criteria the evidence must show that the student is able to: Evidence

(Page no.)

LO1 Record business transactions using double entry book-keeping, and be able to extract a trial balance

P1 Apply the double entry book-keeping system of debits and credits. Record sales and

purchases transactions in a general ledger. 16

P2 Produce a trial balance applying the use of the balance off rule to complete the ledger. 20-22

M1 Analyse transactions to show the progression from a previous trial balance to the next

one using double entry bookkeeping. 22-23

D1 Apply trial balance figures to show which statement of financial accounts they will end

up in. 16-23

LO2 Prepare final accounts for sole-traders, partnerships and limited companies in accordance with

appropriate principles, conventions and standards.

P3 Prepare final accounts from given trial balance. 24

P4 Produce final accounts for a range of examples that include sole-traders,

partnerships or limited companies 26-27

M2 Make adjustments to balances of sum accounts for example, accruals, depreciation

and prepayments before preparing the final accounts. 25

D2 Compare the essential features of each financial account statement to analyse the

differences between them in terms, purpose, structure and content. 28

LO3 Perform bank reconciliations to ensure company and bank records are correct

P5 Apply the bank reconciliation process to prepare a number of bank reconciliations. 32

M3 Apply the reconciliation process, demonstrating the use of deposit in transit, outstanding

checks and Not Sufficient Funds (NSF) check. 33

D3 Prepare accurate bank reconciliations that apply appropriate tools and techniques to

check general accounts and balance sheets.

LO4 Reconcile control accounts and shift recorded transactions from the suspense accounts to the right

accounts

P6 Explain the process taken to reconcile control accounts and clear suspense accounts

using given account examples. 33-34

M4 Demonstrate understanding of the different types of accounts and how and why they

are reconciled.

D4 Produce accurate accounts that have been reconciled applying the appropriate

methods. 34-35

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Learner declaration

Plagiarism

Plagiarism is a particular form of cheating. Plagiarism must be avoided at all costs and students who break the rules,

however innocently, may be penalised. It is your responsibility to ensure that you understand correct referencing

practices. As a university level student, you are expected to use appropriate references throughout and keep carefully

detailed notes of all your sources of materials for material you have used in your work, including any material

downloaded from the Internet. Please consult the relevant unit lecturer or your course tutor if you need any further advice.

Student Declaration

I certify that the assignment submission is entirely my own work and I fully understand the consequences of

plagiarism. I understand that making a false declaration is a form of malpractice.

Student signature: Navroop Sandhu Date:25-11-2021

Plagiarism

Plagiarism is a particular form of cheating. Plagiarism must be avoided at all costs and students who break the rules,

however innocently, may be penalised. It is your responsibility to ensure that you understand correct referencing

practices. As a university level student, you are expected to use appropriate references throughout and keep carefully

detailed notes of all your sources of materials for material you have used in your work, including any material

downloaded from the Internet. Please consult the relevant unit lecturer or your course tutor if you need any further advice.

Student Declaration

I certify that the assignment submission is entirely my own work and I fully understand the consequences of

plagiarism. I understand that making a false declaration is a form of malpractice.

Student signature: Navroop Sandhu Date:25-11-2021

BTEC Assignment Brief

Qualification Pearson BTEC Level 5 Higher National Diploma in Business

Unit or Component

number and title Unit 10: Financial Accounting

Learning aim(s)

To introduce students to essential financial accounting principles and techniques which will

enable them to record and prepare basic final accounts as well as how to prepare accounts for

sole trader, partnership and limited companies.

Assignment title Assignment: Double entry book-keeping, Preparation of Final Accounts, Bank

Reconciliation, Suspense and Control Accounts

Assessor Mr. Lam

Vocational Scenario

or Context

You have been working in modern CPA firm for 10 years; you are also employed as a senior

accountant. You need to demonstrate different set of accounting skill for small medium

firms, such as sole trader, partnership or limited company. You lead the junior team and

mentoring them to be a professional accountant.

You need to undertake the FOUR activities on applying the double entry book-keeping

system, including the adjusting entries and prepare the final accounts. Besides, you need to

consider which regulations need to apply in preparing financial statements. Also, to identify

the differences between financial report and financial accounting. You are required to

explain certain accounting principles that should be taken into account when preparing

financial statements.

On the other hand, you need to explain what bank reconciliation is and why it is necessary

with detailed explanation of the relevant concepts and process. The preparation of bank

reconciliation statement with simulated data is required. Control and suspense accounts are

another significant areas in accounting, you need to depict the nature of each of them and

analyse who can they support the preparation of financial statements. The preparation of

statement of sales ledger control account and reconciliation with sales ledger balance is

necessary.

Qualification Pearson BTEC Level 5 Higher National Diploma in Business

Unit or Component

number and title Unit 10: Financial Accounting

Learning aim(s)

To introduce students to essential financial accounting principles and techniques which will

enable them to record and prepare basic final accounts as well as how to prepare accounts for

sole trader, partnership and limited companies.

Assignment title Assignment: Double entry book-keeping, Preparation of Final Accounts, Bank

Reconciliation, Suspense and Control Accounts

Assessor Mr. Lam

Vocational Scenario

or Context

You have been working in modern CPA firm for 10 years; you are also employed as a senior

accountant. You need to demonstrate different set of accounting skill for small medium

firms, such as sole trader, partnership or limited company. You lead the junior team and

mentoring them to be a professional accountant.

You need to undertake the FOUR activities on applying the double entry book-keeping

system, including the adjusting entries and prepare the final accounts. Besides, you need to

consider which regulations need to apply in preparing financial statements. Also, to identify

the differences between financial report and financial accounting. You are required to

explain certain accounting principles that should be taken into account when preparing

financial statements.

On the other hand, you need to explain what bank reconciliation is and why it is necessary

with detailed explanation of the relevant concepts and process. The preparation of bank

reconciliation statement with simulated data is required. Control and suspense accounts are

another significant areas in accounting, you need to depict the nature of each of them and

analyse who can they support the preparation of financial statements. The preparation of

statement of sales ledger control account and reconciliation with sales ledger balance is

necessary.

Tasks

Your report should cover the followings:

1. Show journal entries and posting to relevant accounts in general ledger.

2. To show the significances of trial balance and its main components.

3. The attributes of quality accounting information and regulations to apply in preparing

financial statements.

4. Preparation of adjusting entries and compiling the financial statements accordingly.

5. Depict the differences between financial report and financial accounting.

6. Illustration of relevant accounting principles in preparing financial statements.

7. Nature of bank reconciliation statement, its main concepts, process of preparation,

preparation with simulated data.

8. Nature of control and suspense account, how they can support the financial accounting.

9. Preparation of sales ledger control account and how it can reconcile with sales ledger

balance.

Submission Format - In accordance with the questions requirement, the assignment must be presented with

clear explanation of relevant accounting concepts and clear demonstration of calculation

in spreadsheet.

- Assignment must be typed using 12-point font. For qualitative question, please make

sure your work is 1 line spaced. An additional line space between paragraphs, or indent

the first line of each paragraph.

- Either Times New Roman or Arial consistently throughout the report, including in tables

and figures.

- In answering any qualitative questions, all assignments are expected to have correct

grammar, punctuation, spelling, and referencing should be shown at the final page of

assignment.

Sources of

information to

support you with this

Assignment

1. Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial Accounting:

IFRS (3rd ed.). New Jersey: John Wiley & Sons.

2. Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2018). Accounting Principles

(13th ed.). New Jersey: John Wiley & Sons.

3. Wild, J., Shaw, K., & Chiappetta, B. (2018). Fundamental Accounting Principles

(24 th ed.). New York: McGraw-Hill.

4. Wild, J., & Shaw, K. (2018). Financial and Managerial Accounting (8th ed.). New

York: McGraw-Hill.

Other assessment

materials attached to

this Assignment

Brief

Nil

Activities 1

Your report should cover the followings:

1. Show journal entries and posting to relevant accounts in general ledger.

2. To show the significances of trial balance and its main components.

3. The attributes of quality accounting information and regulations to apply in preparing

financial statements.

4. Preparation of adjusting entries and compiling the financial statements accordingly.

5. Depict the differences between financial report and financial accounting.

6. Illustration of relevant accounting principles in preparing financial statements.

7. Nature of bank reconciliation statement, its main concepts, process of preparation,

preparation with simulated data.

8. Nature of control and suspense account, how they can support the financial accounting.

9. Preparation of sales ledger control account and how it can reconcile with sales ledger

balance.

Submission Format - In accordance with the questions requirement, the assignment must be presented with

clear explanation of relevant accounting concepts and clear demonstration of calculation

in spreadsheet.

- Assignment must be typed using 12-point font. For qualitative question, please make

sure your work is 1 line spaced. An additional line space between paragraphs, or indent

the first line of each paragraph.

- Either Times New Roman or Arial consistently throughout the report, including in tables

and figures.

- In answering any qualitative questions, all assignments are expected to have correct

grammar, punctuation, spelling, and referencing should be shown at the final page of

assignment.

Sources of

information to

support you with this

Assignment

1. Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial Accounting:

IFRS (3rd ed.). New Jersey: John Wiley & Sons.

2. Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2018). Accounting Principles

(13th ed.). New Jersey: John Wiley & Sons.

3. Wild, J., Shaw, K., & Chiappetta, B. (2018). Fundamental Accounting Principles

(24 th ed.). New York: McGraw-Hill.

4. Wild, J., & Shaw, K. (2018). Financial and Managerial Accounting (8th ed.). New

York: McGraw-Hill.

Other assessment

materials attached to

this Assignment

Brief

Nil

Activities 1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

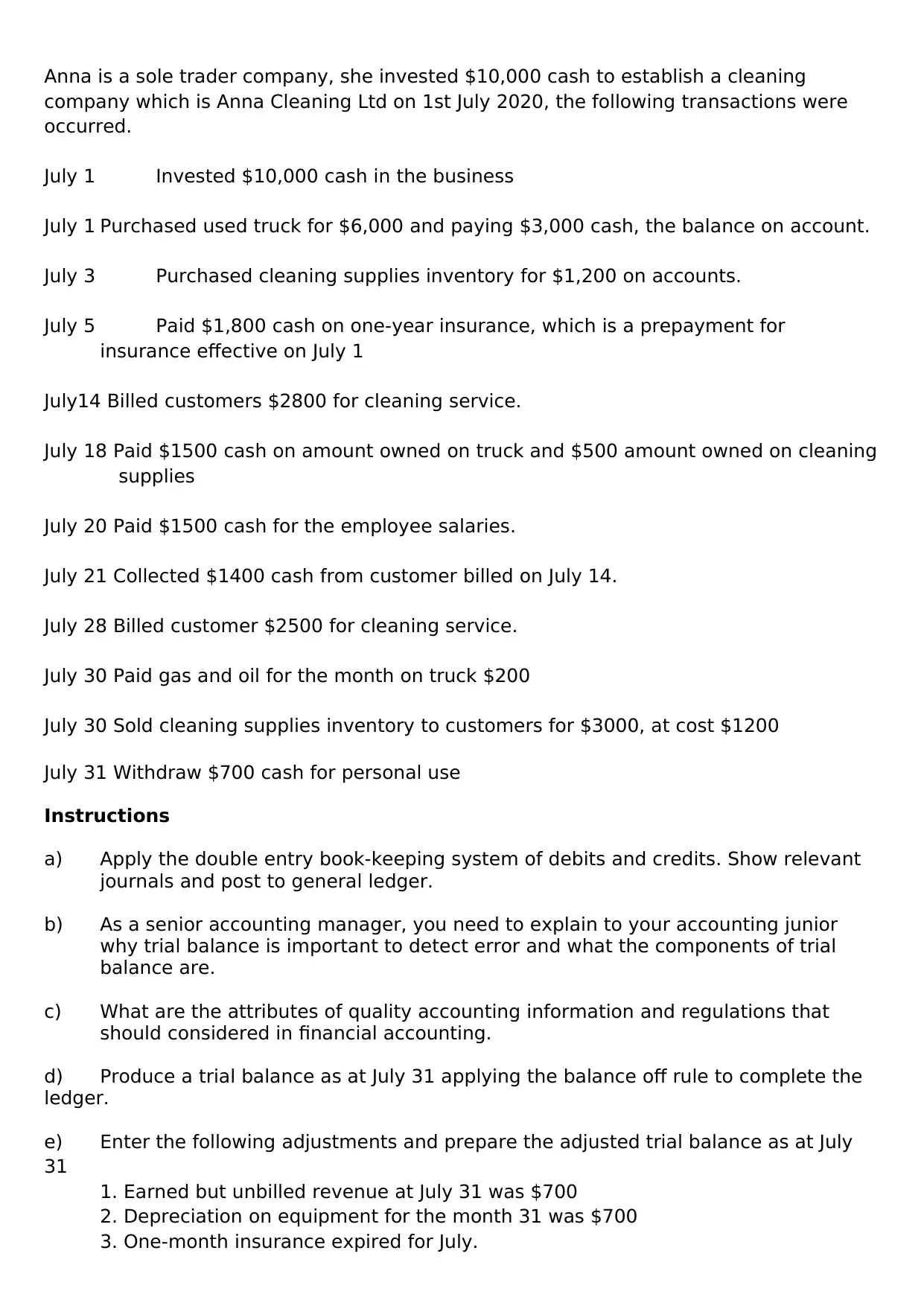

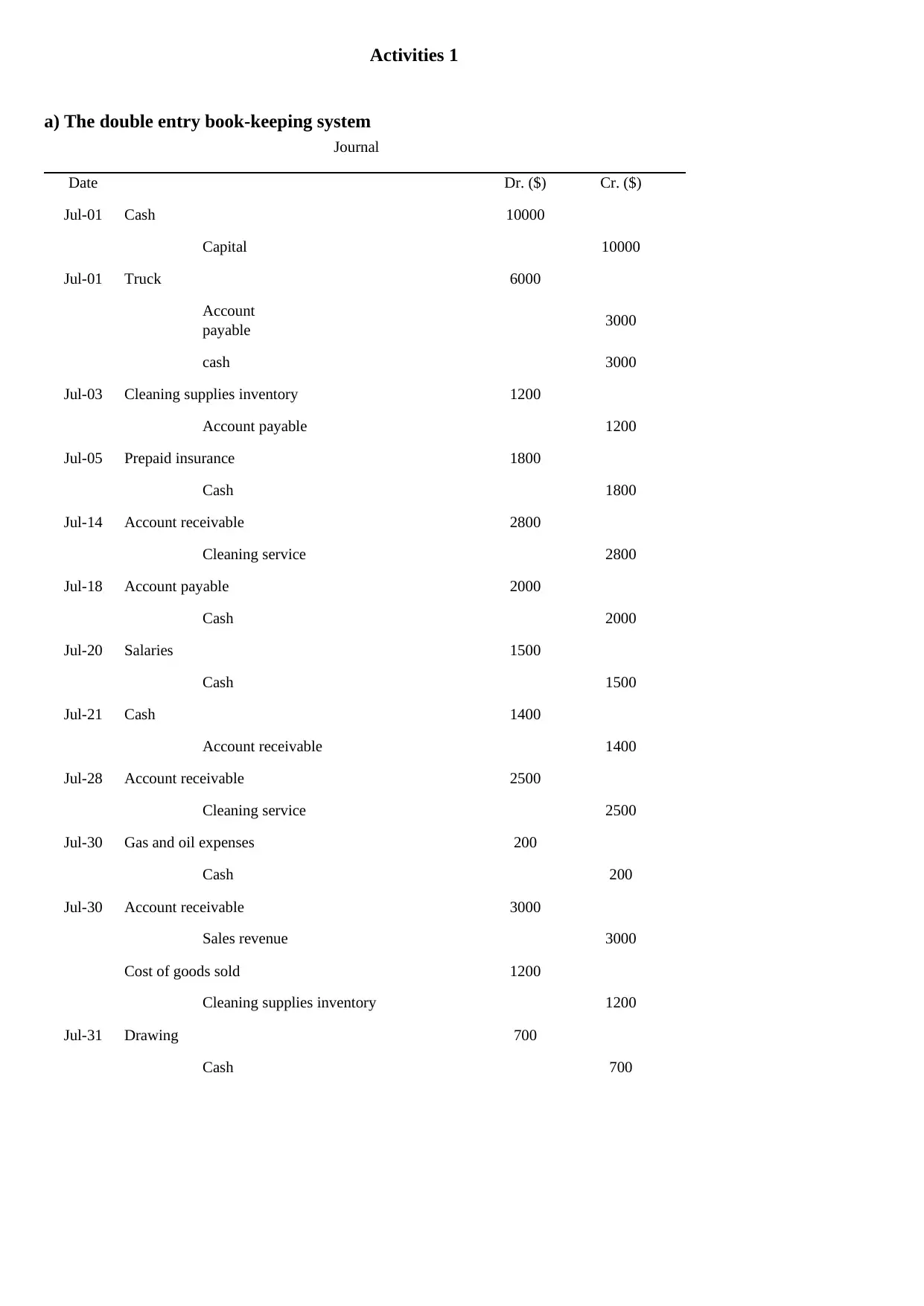

Anna is a sole trader company, she invested $10,000 cash to establish a cleaning

company which is Anna Cleaning Ltd on 1st July 2020, the following transactions were

occurred.

July 1 Invested $10,000 cash in the business

July 1 Purchased used truck for $6,000 and paying $3,000 cash, the balance on account.

July 3 Purchased cleaning supplies inventory for $1,200 on accounts.

July 5 Paid $1,800 cash on one-year insurance, which is a prepayment for

insurance effective on July 1

July14 Billed customers $2800 for cleaning service.

July 18 Paid $1500 cash on amount owned on truck and $500 amount owned on cleaning

supplies

July 20 Paid $1500 cash for the employee salaries.

July 21 Collected $1400 cash from customer billed on July 14.

July 28 Billed customer $2500 for cleaning service.

July 30 Paid gas and oil for the month on truck $200

July 30 Sold cleaning supplies inventory to customers for $3000, at cost $1200

July 31 Withdraw $700 cash for personal use

Instructions

a) Apply the double entry book-keeping system of debits and credits. Show relevant

journals and post to general ledger.

b) As a senior accounting manager, you need to explain to your accounting junior

why trial balance is important to detect error and what the components of trial

balance are.

c) What are the attributes of quality accounting information and regulations that

should considered in financial accounting.

d) Produce a trial balance as at July 31 applying the balance off rule to complete the

ledger.

e) Enter the following adjustments and prepare the adjusted trial balance as at July

31

1. Earned but unbilled revenue at July 31 was $700

2. Depreciation on equipment for the month 31 was $700

3. One-month insurance expired for July.

company which is Anna Cleaning Ltd on 1st July 2020, the following transactions were

occurred.

July 1 Invested $10,000 cash in the business

July 1 Purchased used truck for $6,000 and paying $3,000 cash, the balance on account.

July 3 Purchased cleaning supplies inventory for $1,200 on accounts.

July 5 Paid $1,800 cash on one-year insurance, which is a prepayment for

insurance effective on July 1

July14 Billed customers $2800 for cleaning service.

July 18 Paid $1500 cash on amount owned on truck and $500 amount owned on cleaning

supplies

July 20 Paid $1500 cash for the employee salaries.

July 21 Collected $1400 cash from customer billed on July 14.

July 28 Billed customer $2500 for cleaning service.

July 30 Paid gas and oil for the month on truck $200

July 30 Sold cleaning supplies inventory to customers for $3000, at cost $1200

July 31 Withdraw $700 cash for personal use

Instructions

a) Apply the double entry book-keeping system of debits and credits. Show relevant

journals and post to general ledger.

b) As a senior accounting manager, you need to explain to your accounting junior

why trial balance is important to detect error and what the components of trial

balance are.

c) What are the attributes of quality accounting information and regulations that

should considered in financial accounting.

d) Produce a trial balance as at July 31 applying the balance off rule to complete the

ledger.

e) Enter the following adjustments and prepare the adjusted trial balance as at July

31

1. Earned but unbilled revenue at July 31 was $700

2. Depreciation on equipment for the month 31 was $700

3. One-month insurance expired for July.

4. Accrued but unpaid employee salaries were $500.

f) Prepare final accounts from adjusted trial balance.

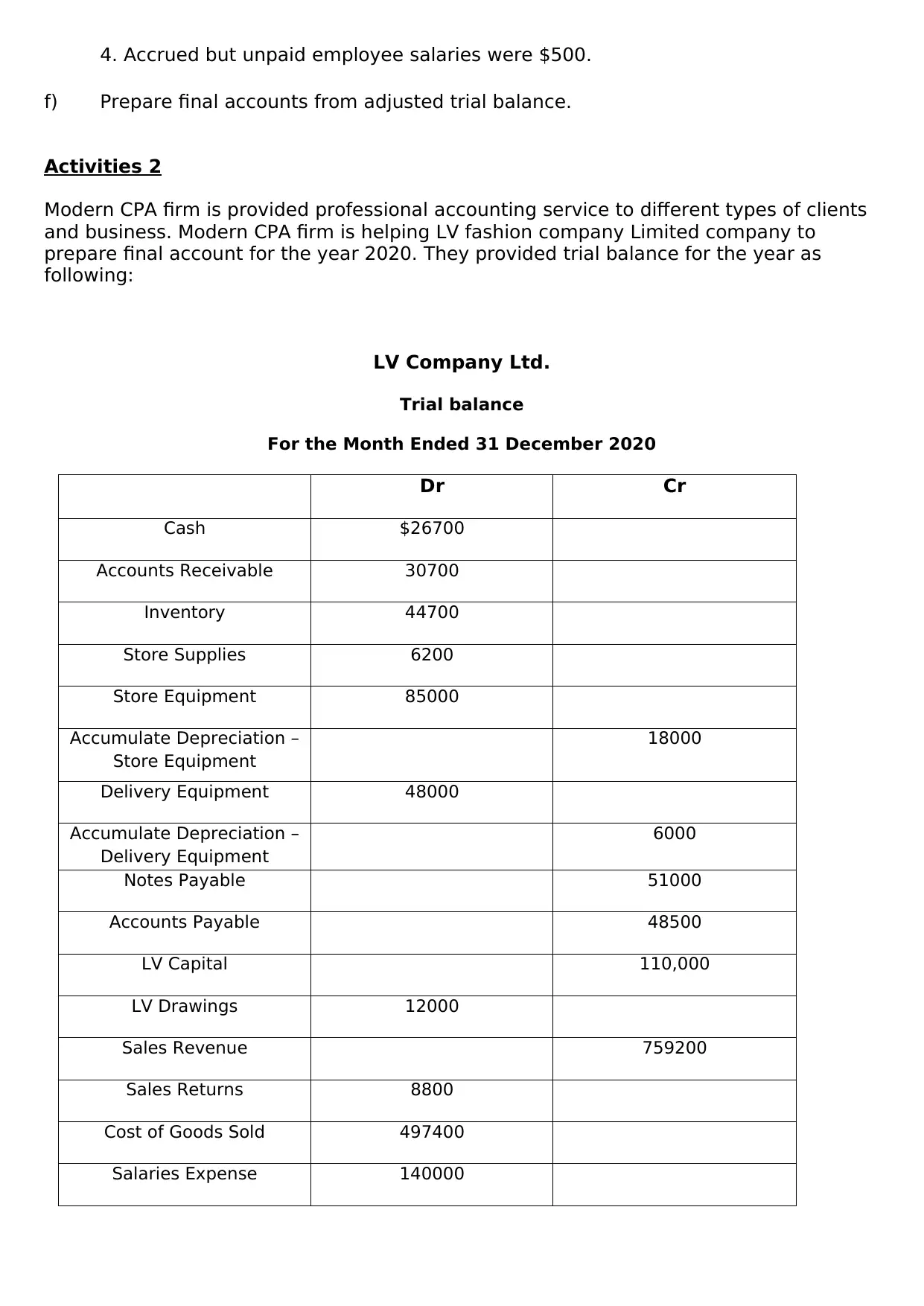

Activities 2

Modern CPA firm is provided professional accounting service to different types of clients

and business. Modern CPA firm is helping LV fashion company Limited company to

prepare final account for the year 2020. They provided trial balance for the year as

following:

LV Company Ltd.

Trial balance

For the Month Ended 31 December 2020

Dr Cr

Cash $26700

Accounts Receivable 30700

Inventory 44700

Store Supplies 6200

Store Equipment 85000

Accumulate Depreciation –

Store Equipment

18000

Delivery Equipment 48000

Accumulate Depreciation –

Delivery Equipment

6000

Notes Payable 51000

Accounts Payable 48500

LV Capital 110,000

LV Drawings 12000

Sales Revenue 759200

Sales Returns 8800

Cost of Goods Sold 497400

Salaries Expense 140000

f) Prepare final accounts from adjusted trial balance.

Activities 2

Modern CPA firm is provided professional accounting service to different types of clients

and business. Modern CPA firm is helping LV fashion company Limited company to

prepare final account for the year 2020. They provided trial balance for the year as

following:

LV Company Ltd.

Trial balance

For the Month Ended 31 December 2020

Dr Cr

Cash $26700

Accounts Receivable 30700

Inventory 44700

Store Supplies 6200

Store Equipment 85000

Accumulate Depreciation –

Store Equipment

18000

Delivery Equipment 48000

Accumulate Depreciation –

Delivery Equipment

6000

Notes Payable 51000

Accounts Payable 48500

LV Capital 110,000

LV Drawings 12000

Sales Revenue 759200

Sales Returns 8800

Cost of Goods Sold 497400

Salaries Expense 140000

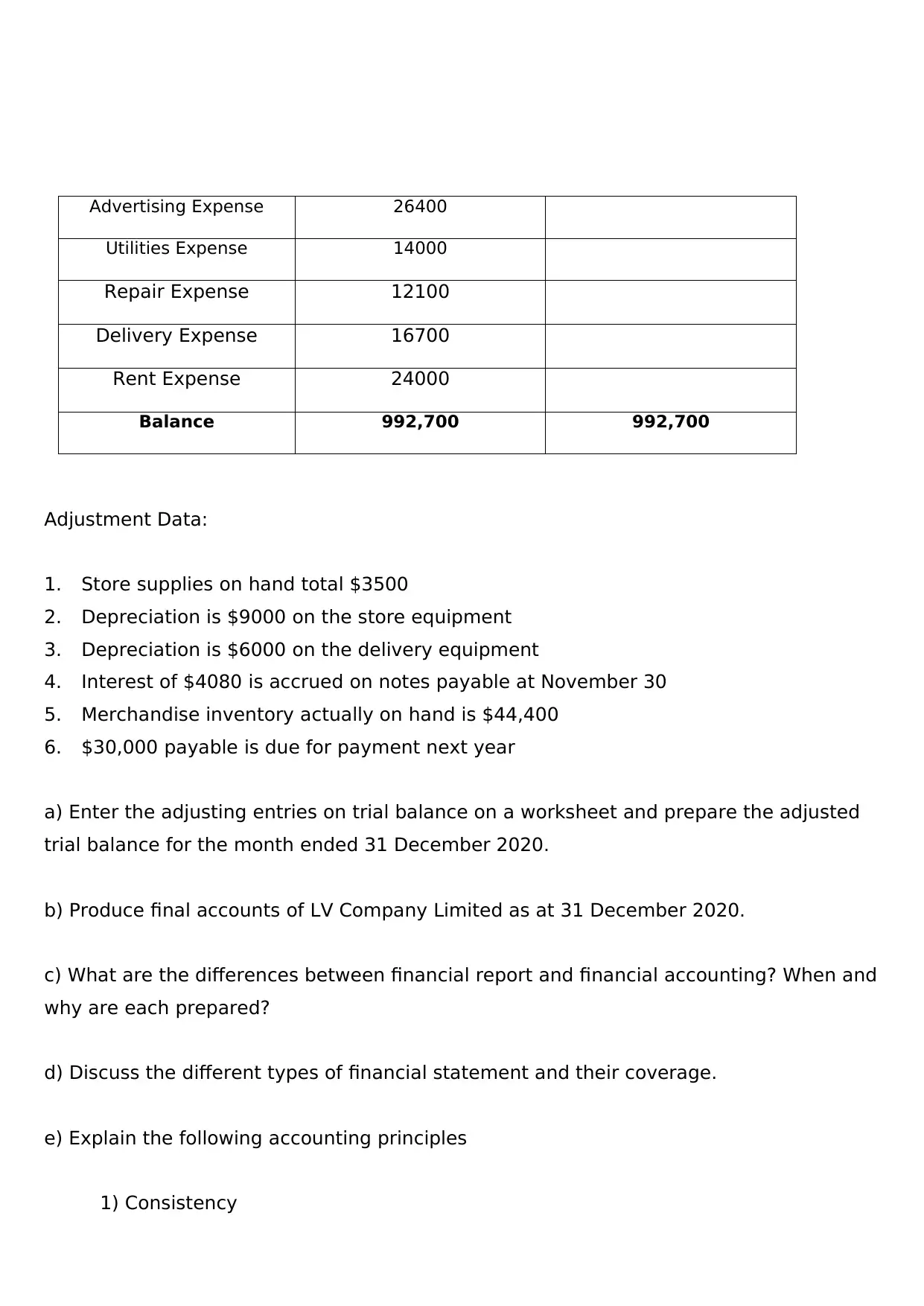

Advertising Expense 26400

Utilities Expense 14000

Repair Expense 12100

Delivery Expense 16700

Rent Expense 24000

Balance 992,700 992,700

Adjustment Data:

1. Store supplies on hand total $3500

2. Depreciation is $9000 on the store equipment

3. Depreciation is $6000 on the delivery equipment

4. Interest of $4080 is accrued on notes payable at November 30

5. Merchandise inventory actually on hand is $44,400

6. $30,000 payable is due for payment next year

a) Enter the adjusting entries on trial balance on a worksheet and prepare the adjusted

trial balance for the month ended 31 December 2020.

b) Produce final accounts of LV Company Limited as at 31 December 2020.

c) What are the differences between financial report and financial accounting? When and

why are each prepared?

d) Discuss the different types of financial statement and their coverage.

e) Explain the following accounting principles

1) Consistency

Utilities Expense 14000

Repair Expense 12100

Delivery Expense 16700

Rent Expense 24000

Balance 992,700 992,700

Adjustment Data:

1. Store supplies on hand total $3500

2. Depreciation is $9000 on the store equipment

3. Depreciation is $6000 on the delivery equipment

4. Interest of $4080 is accrued on notes payable at November 30

5. Merchandise inventory actually on hand is $44,400

6. $30,000 payable is due for payment next year

a) Enter the adjusting entries on trial balance on a worksheet and prepare the adjusted

trial balance for the month ended 31 December 2020.

b) Produce final accounts of LV Company Limited as at 31 December 2020.

c) What are the differences between financial report and financial accounting? When and

why are each prepared?

d) Discuss the different types of financial statement and their coverage.

e) Explain the following accounting principles

1) Consistency

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2) Materiality

3) Fully disclosure

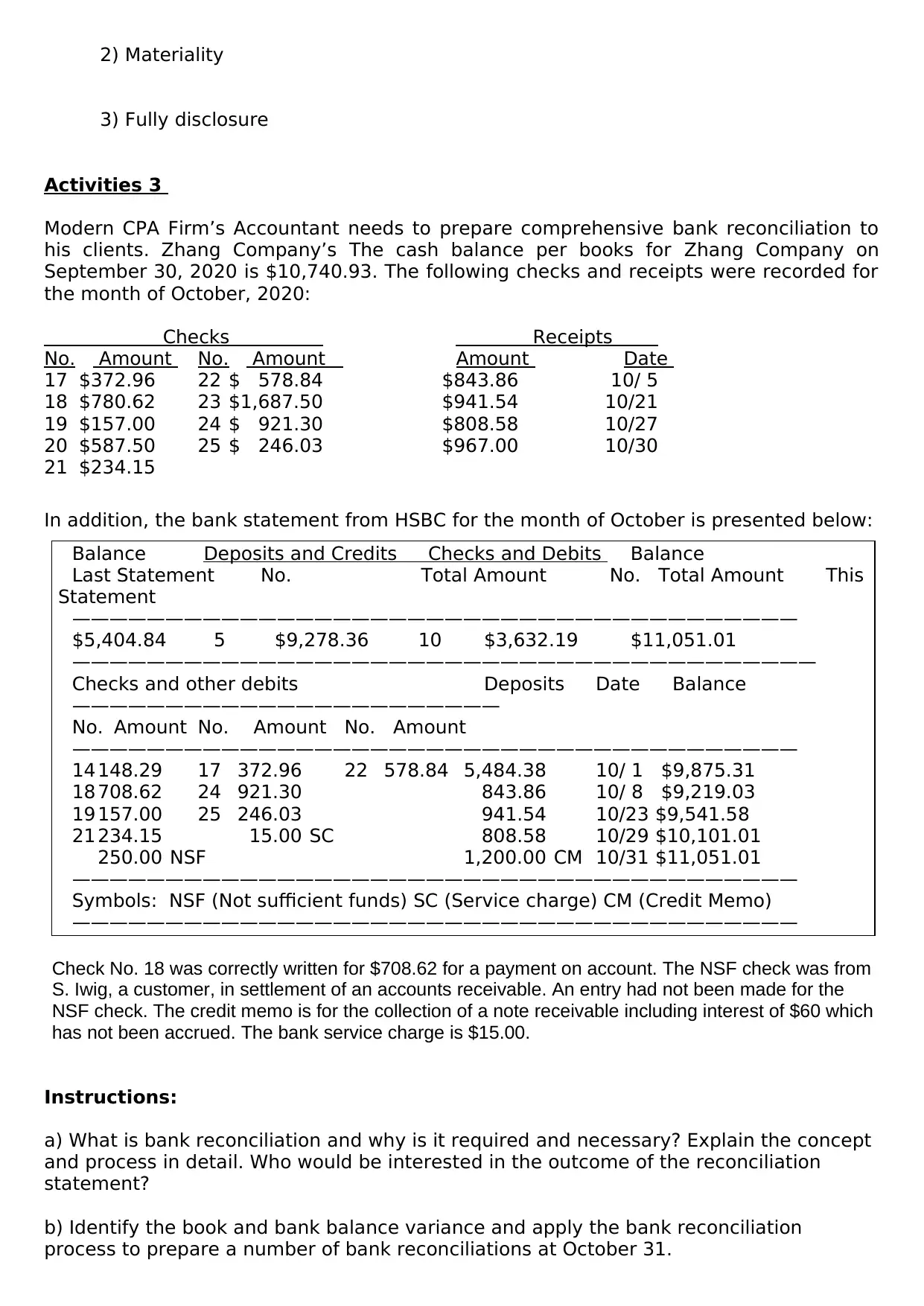

Activities 3

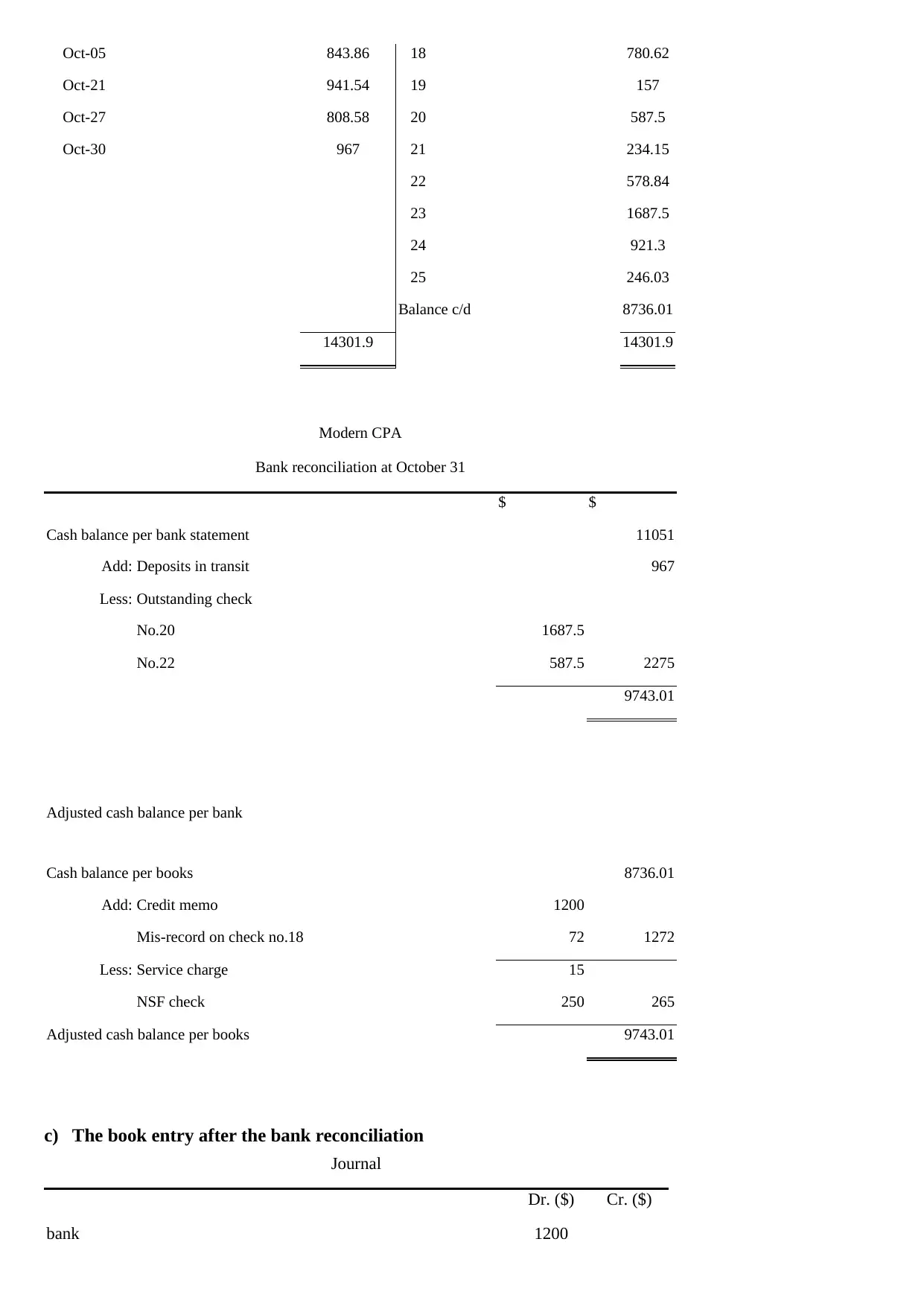

Modern CPA Firm’s Accountant needs to prepare comprehensive bank reconciliation to

his clients. Zhang Company’s The cash balance per books for Zhang Company on

September 30, 2020 is $10,740.93. The following checks and receipts were recorded for

the month of October, 2020:

Checks Receipts

No. Amount No. Amount Amount Date

17 $372.96 22 $ 578.84 $843.86 10/ 5

18 $780.62 23 $1,687.50 $941.54 10/21

19 $157.00 24 $ 921.30 $808.58 10/27

20 $587.50 25 $ 246.03 $967.00 10/30

21 $234.15

In addition, the bank statement from HSBC for the month of October is presented below:

Balance Deposits and Credits Checks and Debits Balance

Last Statement No. Total Amount No. Total Amount This

Statement

———————————————————————————————————————

$5,404.84 5 $9,278.36 10 $3,632.19 $11,051.01

————————————————————————————————————————

Checks and other debits Deposits Date Balance

———————————————————————

No. Amount No. Amount No. Amount

———————————————————————————————————————

14 148.29 17 372.96 22 578.84 5,484.38 10/ 1 $9,875.31

18 708.62 24 921.30 843.86 10/ 8 $9,219.03

19 157.00 25 246.03 941.54 10/23 $9,541.58

21 234.15 15.00 SC 808.58 10/29 $10,101.01

250.00 NSF 1,200.00 CM 10/31 $11,051.01

———————————————————————————————————————

Symbols: NSF (Not sufficient funds) SC (Service charge) CM (Credit Memo)

———————————————————————————————————————

Check No. 18 was correctly written for $708.62 for a payment on account. The NSF check was from

S. Iwig, a customer, in settlement of an accounts receivable. An entry had not been made for the

NSF check. The credit memo is for the collection of a note receivable including interest of $60 which

has not been accrued. The bank service charge is $15.00.

Instructions:

a) What is bank reconciliation and why is it required and necessary? Explain the concept

and process in detail. Who would be interested in the outcome of the reconciliation

statement?

b) Identify the book and bank balance variance and apply the bank reconciliation

process to prepare a number of bank reconciliations at October 31.

3) Fully disclosure

Activities 3

Modern CPA Firm’s Accountant needs to prepare comprehensive bank reconciliation to

his clients. Zhang Company’s The cash balance per books for Zhang Company on

September 30, 2020 is $10,740.93. The following checks and receipts were recorded for

the month of October, 2020:

Checks Receipts

No. Amount No. Amount Amount Date

17 $372.96 22 $ 578.84 $843.86 10/ 5

18 $780.62 23 $1,687.50 $941.54 10/21

19 $157.00 24 $ 921.30 $808.58 10/27

20 $587.50 25 $ 246.03 $967.00 10/30

21 $234.15

In addition, the bank statement from HSBC for the month of October is presented below:

Balance Deposits and Credits Checks and Debits Balance

Last Statement No. Total Amount No. Total Amount This

Statement

———————————————————————————————————————

$5,404.84 5 $9,278.36 10 $3,632.19 $11,051.01

————————————————————————————————————————

Checks and other debits Deposits Date Balance

———————————————————————

No. Amount No. Amount No. Amount

———————————————————————————————————————

14 148.29 17 372.96 22 578.84 5,484.38 10/ 1 $9,875.31

18 708.62 24 921.30 843.86 10/ 8 $9,219.03

19 157.00 25 246.03 941.54 10/23 $9,541.58

21 234.15 15.00 SC 808.58 10/29 $10,101.01

250.00 NSF 1,200.00 CM 10/31 $11,051.01

———————————————————————————————————————

Symbols: NSF (Not sufficient funds) SC (Service charge) CM (Credit Memo)

———————————————————————————————————————

Check No. 18 was correctly written for $708.62 for a payment on account. The NSF check was from

S. Iwig, a customer, in settlement of an accounts receivable. An entry had not been made for the

NSF check. The credit memo is for the collection of a note receivable including interest of $60 which

has not been accrued. The bank service charge is $15.00.

Instructions:

a) What is bank reconciliation and why is it required and necessary? Explain the concept

and process in detail. Who would be interested in the outcome of the reconciliation

statement?

b) Identify the book and bank balance variance and apply the bank reconciliation

process to prepare a number of bank reconciliations at October 31.

c) Prepare the book entry after the bank reconciliation statement.

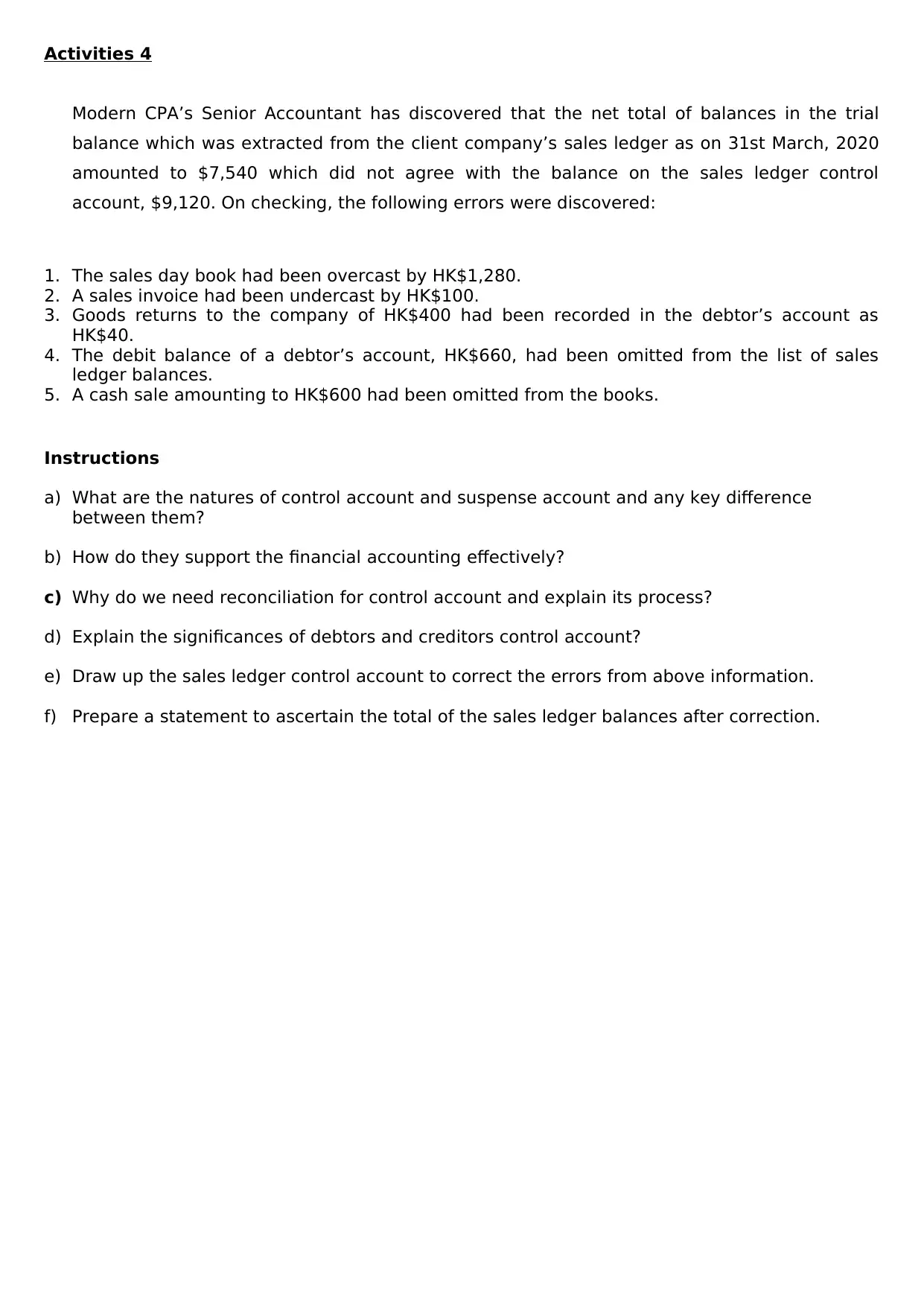

Activities 4

Modern CPA’s Senior Accountant has discovered that the net total of balances in the trial

balance which was extracted from the client company’s sales ledger as on 31st March, 2020

amounted to $7,540 which did not agree with the balance on the sales ledger control

account, $9,120. On checking, the following errors were discovered:

1. The sales day book had been overcast by HK$1,280.

2. A sales invoice had been undercast by HK$100.

3. Goods returns to the company of HK$400 had been recorded in the debtor’s account as

HK$40.

4. The debit balance of a debtor’s account, HK$660, had been omitted from the list of sales

ledger balances.

5. A cash sale amounting to HK$600 had been omitted from the books.

Instructions

a) What are the natures of control account and suspense account and any key difference

between them?

b) How do they support the financial accounting effectively?

c) Why do we need reconciliation for control account and explain its process?

d) Explain the significances of debtors and creditors control account?

e) Draw up the sales ledger control account to correct the errors from above information.

f) Prepare a statement to ascertain the total of the sales ledger balances after correction.

Modern CPA’s Senior Accountant has discovered that the net total of balances in the trial

balance which was extracted from the client company’s sales ledger as on 31st March, 2020

amounted to $7,540 which did not agree with the balance on the sales ledger control

account, $9,120. On checking, the following errors were discovered:

1. The sales day book had been overcast by HK$1,280.

2. A sales invoice had been undercast by HK$100.

3. Goods returns to the company of HK$400 had been recorded in the debtor’s account as

HK$40.

4. The debit balance of a debtor’s account, HK$660, had been omitted from the list of sales

ledger balances.

5. A cash sale amounting to HK$600 had been omitted from the books.

Instructions

a) What are the natures of control account and suspense account and any key difference

between them?

b) How do they support the financial accounting effectively?

c) Why do we need reconciliation for control account and explain its process?

d) Explain the significances of debtors and creditors control account?

e) Draw up the sales ledger control account to correct the errors from above information.

f) Prepare a statement to ascertain the total of the sales ledger balances after correction.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ASSESSMENT RECORD SHEET

Qualification Pearson BTEC Level 5 Higher

National Diploma in Business Learner name

Unit Number and title Unit 10: Financial Accounting Assessor name Mr. Lam

Assignment title Assignment: Double entry book-keeping, Preparation of Final Accounts, Bank

Reconciliation, Suspense and Control Accounts

First Submission

Deadline 25th November 2021 Date submitted

Has an extension to the deadline been approved by the Assessor due to extenuating

circumstances? (If appropriate)

Targeted

criteria To achieve the criteria, the evidence must show that the student is able to: Achieved?

P1 Apply the double entry book-keeping system of debits and credits. Record sales and

purchases transactions in a general ledger.

P2 Produce a trial balance applying the use of the balance off rule to complete the ledger.

P3 Prepare final accounts from given trial balance.

P4 Produce final accounts for a range of examples that include sole-traders, partnerships

or limited companies

P5 Apply the bank reconciliation process to prepare a number of bank reconciliations.

P6 Explain the process taken to reconcile control accounts and clear suspense accounts

using given account examples.

Higher Grade achievements (where applicable)

Grade descriptor

M1 Analyse transactions to show the progression from a previous trial balance to the next

one using double entry bookkeeping.

M2 Make adjustments to balances of sum accounts for example, accruals, depreciation and

prepayments before preparing the final accounts.

M3 Apply the reconciliation process, demonstrating the use of deposit in transit,

outstanding checks and Not Sufficient Funds (NSF) check.

M4 Demonstrate understanding of the different types of accounts and how and why

they are reconciled.

D1 Apply trial balance figures to show which statement of financial accounts they will

end up in

D2 Compare the essential features of each financial account statement to analyse the

differences between them in terms, purpose, structure and content.

D3 Prepare accurate bank reconciliations that apply appropriate tools and techniques to

check general accounts and balance sheets.

D4 Produce accurate accounts that have been reconciled applying the appropriate

methods.

Assessor declaration

I certify that the evidence submitted for this assignment is the learner’s own. The

learner has clearly referenced any sources used in the work. I understand that false

declaration is a form of malpractice.

Assessor signature Date

Date of feedback to learner

Learner signature Date

**Any resubmission evidence must be submitted within 15 working days of learners receiving assessment feedback

Qualification Pearson BTEC Level 5 Higher

National Diploma in Business Learner name

Unit Number and title Unit 10: Financial Accounting Assessor name Mr. Lam

Assignment title Assignment: Double entry book-keeping, Preparation of Final Accounts, Bank

Reconciliation, Suspense and Control Accounts

First Submission

Deadline 25th November 2021 Date submitted

Has an extension to the deadline been approved by the Assessor due to extenuating

circumstances? (If appropriate)

Targeted

criteria To achieve the criteria, the evidence must show that the student is able to: Achieved?

P1 Apply the double entry book-keeping system of debits and credits. Record sales and

purchases transactions in a general ledger.

P2 Produce a trial balance applying the use of the balance off rule to complete the ledger.

P3 Prepare final accounts from given trial balance.

P4 Produce final accounts for a range of examples that include sole-traders, partnerships

or limited companies

P5 Apply the bank reconciliation process to prepare a number of bank reconciliations.

P6 Explain the process taken to reconcile control accounts and clear suspense accounts

using given account examples.

Higher Grade achievements (where applicable)

Grade descriptor

M1 Analyse transactions to show the progression from a previous trial balance to the next

one using double entry bookkeeping.

M2 Make adjustments to balances of sum accounts for example, accruals, depreciation and

prepayments before preparing the final accounts.

M3 Apply the reconciliation process, demonstrating the use of deposit in transit,

outstanding checks and Not Sufficient Funds (NSF) check.

M4 Demonstrate understanding of the different types of accounts and how and why

they are reconciled.

D1 Apply trial balance figures to show which statement of financial accounts they will

end up in

D2 Compare the essential features of each financial account statement to analyse the

differences between them in terms, purpose, structure and content.

D3 Prepare accurate bank reconciliations that apply appropriate tools and techniques to

check general accounts and balance sheets.

D4 Produce accurate accounts that have been reconciled applying the appropriate

methods.

Assessor declaration

I certify that the evidence submitted for this assignment is the learner’s own. The

learner has clearly referenced any sources used in the work. I understand that false

declaration is a form of malpractice.

Assessor signature Date

Date of feedback to learner

Learner signature Date

**Any resubmission evidence must be submitted within 15 working days of learners receiving assessment feedback

Resubmission

Deadline Date submitted

Targeted

criteria

Criteria

achieved Assessment comments

General comments

Learner Declaration

I certify that the evidence submitted for this assignment is my own. I have clearly

referenced any sources used in the work. I understand that false declaration is a form of

malpractice.

Learner signature Date

Assessor declaration

I certify that the evidence submitted for this assignment is the learner’s own. The

learner has clearly referenced any sources used in the work. I understand that false

declaration is a form of malpractice.

Assessor signature Date

Date of feedback to learner

**Any resubmission evidence must be submitted within 15 working days of learners receiving assessment feedback

Deadline Date submitted

Targeted

criteria

Criteria

achieved Assessment comments

General comments

Learner Declaration

I certify that the evidence submitted for this assignment is my own. I have clearly

referenced any sources used in the work. I understand that false declaration is a form of

malpractice.

Learner signature Date

Assessor declaration

I certify that the evidence submitted for this assignment is the learner’s own. The

learner has clearly referenced any sources used in the work. I understand that false

declaration is a form of malpractice.

Assessor signature Date

Date of feedback to learner

**Any resubmission evidence must be submitted within 15 working days of learners receiving assessment feedback

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Higher Nationals - Summative Assignment Feedback Form

Student Name/ID

Unit Title Unit 10: Financial Accounting

Assignment Number 1 Assessor Mr. Lam

Submission Deadline 9th December 2021 Date submitted

Re-submission Deadline Date re-submitted

Assessor Feedback:

Grade: Assessor Signature: Date:

Learner Signature: Date:

Resubmission Feedback:

Grade: Assessor Signature: Date:

Learner Signature: Date:

Internal Verifier’s Comments:

Signature & Date:

* Please note that grade decisions are provisional. They are only confirmed once internal and external moderation has

taken place and grades decisions have been agreed at the assessment board.

Student Name/ID

Unit Title Unit 10: Financial Accounting

Assignment Number 1 Assessor Mr. Lam

Submission Deadline 9th December 2021 Date submitted

Re-submission Deadline Date re-submitted

Assessor Feedback:

Grade: Assessor Signature: Date:

Learner Signature: Date:

Resubmission Feedback:

Grade: Assessor Signature: Date:

Learner Signature: Date:

Internal Verifier’s Comments:

Signature & Date:

* Please note that grade decisions are provisional. They are only confirmed once internal and external moderation has

taken place and grades decisions have been agreed at the assessment board.

Pearson BTEC Level 5 Higher National Diploma in Business

Unit 10: Financial accounting

Assignment 1

Assignment Title: Fundamental financial accounting

Student Name: Navroop Sandhu

Class: BA

Assessor Name: Mr. Lam

Date issued: 11-10-2021

Completion date:

Submitted on:

Content

Pearson Education 2016

Higher Education Qualifications

Summative Assignment Feedback

Form

Unit 10: Financial accounting

Assignment 1

Assignment Title: Fundamental financial accounting

Student Name: Navroop Sandhu

Class: BA

Assessor Name: Mr. Lam

Date issued: 11-10-2021

Completion date:

Submitted on:

Content

Pearson Education 2016

Higher Education Qualifications

Summative Assignment Feedback

Form

Contents

Assignment front sheet...........................................................................................................................................1

Plagiarism..............................................................................................................................................................3

BTEC Assignment Brief............................................................................................................................................4

Activities 1............................................................................................................................................................17

a) The double entry book-keeping system................................................................................................17

b) Concept of trial balance.........................................................................................................................18

c) financial accounting................................................................................................................................18

d)Trial balance.............................................................................................................................................20

e) Adjustment entry.....................................................................................................................................23

f) Final account............................................................................................................................................24

Activities 2............................................................................................................................................................25

a) Adjusting trial balance...........................................................................................................................25

b) Final account...........................................................................................................................................26

d) The different types of financial statement............................................................................................28

e) accounting principles-............................................................................................................................29

Activities 3............................................................................................................................................................31

a) The concept of bank reconciliation statement...................................................................................31

b) Bank reconciliation statement.............................................................................................................32

c) The book entry after the bank reconciliation....................................................................................33

Activities 4............................................................................................................................................................33

a) Natures of control account and suspense account...............................................................................33

c) Reconciliation for control account......................................................................................................34

d) The role of debtor and creditors accounts..........................................................................................34

e) Sales ledger control account................................................................................................................35

f) A statement to ascertain the total of the sales ledger balance after correction................................35

References List.......................................................................................................................................................36

Assignment front sheet...........................................................................................................................................1

Plagiarism..............................................................................................................................................................3

BTEC Assignment Brief............................................................................................................................................4

Activities 1............................................................................................................................................................17

a) The double entry book-keeping system................................................................................................17

b) Concept of trial balance.........................................................................................................................18

c) financial accounting................................................................................................................................18

d)Trial balance.............................................................................................................................................20

e) Adjustment entry.....................................................................................................................................23

f) Final account............................................................................................................................................24

Activities 2............................................................................................................................................................25

a) Adjusting trial balance...........................................................................................................................25

b) Final account...........................................................................................................................................26

d) The different types of financial statement............................................................................................28

e) accounting principles-............................................................................................................................29

Activities 3............................................................................................................................................................31

a) The concept of bank reconciliation statement...................................................................................31

b) Bank reconciliation statement.............................................................................................................32

c) The book entry after the bank reconciliation....................................................................................33

Activities 4............................................................................................................................................................33

a) Natures of control account and suspense account...............................................................................33

c) Reconciliation for control account......................................................................................................34

d) The role of debtor and creditors accounts..........................................................................................34

e) Sales ledger control account................................................................................................................35

f) A statement to ascertain the total of the sales ledger balance after correction................................35

References List.......................................................................................................................................................36

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Activities 1

a) The double entry book-keeping system

Journal

Date Dr. ($) Cr. ($)

Jul-01 Cash 10000

Capital 10000

Jul-01 Truck 6000

Account

payable 3000

cash 3000

Jul-03 Cleaning supplies inventory 1200

Account payable 1200

Jul-05 Prepaid insurance 1800

Cash 1800

Jul-14 Account receivable 2800

Cleaning service 2800

Jul-18 Account payable 2000

Cash 2000

Jul-20 Salaries 1500

Cash 1500

Jul-21 Cash 1400

Account receivable 1400

Jul-28 Account receivable 2500

Cleaning service 2500

Jul-30 Gas and oil expenses 200

Cash 200

Jul-30 Account receivable 3000

Sales revenue 3000

Cost of goods sold 1200

Cleaning supplies inventory 1200

Jul-31 Drawing 700

Cash 700

a) The double entry book-keeping system

Journal

Date Dr. ($) Cr. ($)

Jul-01 Cash 10000

Capital 10000

Jul-01 Truck 6000

Account

payable 3000

cash 3000

Jul-03 Cleaning supplies inventory 1200

Account payable 1200

Jul-05 Prepaid insurance 1800

Cash 1800

Jul-14 Account receivable 2800

Cleaning service 2800

Jul-18 Account payable 2000

Cash 2000

Jul-20 Salaries 1500

Cash 1500

Jul-21 Cash 1400

Account receivable 1400

Jul-28 Account receivable 2500

Cleaning service 2500

Jul-30 Gas and oil expenses 200

Cash 200

Jul-30 Account receivable 3000

Sales revenue 3000

Cost of goods sold 1200

Cleaning supplies inventory 1200

Jul-31 Drawing 700

Cash 700

b) Concept of trial balance

A trial balance is a report that rundowns the balance of all broad record records of an organization at one point on

schedule. The records pondered a trial balance are identified with all significant bookkeeping things, including resources,

liabilities, value, incomes, costs, gains, and misfortunes. It is basically used to distinguish the equilibrium between

charges and credits sections from the exchanges recorded in the overall record at one point on schedule. Notwithstanding

mistake discovery, the preliminary equilibrium is ready to make the fundamental changing sections to the overall record.

It is arranged again after the changing sections are presented on guarantee that the all-out charges and credits are as yet

adjusted. It's anything but an authority budget summary. It is normally utilized inside and isn't disseminated to individuals

outside the organization. (CFI, 2021)

Why preliminary equilibrium is imperative to identify blunder

When there is an irregularity between all out charge adjusts and complete credit adjusts implies there are at least one

blunder in twofold sections and the record balance in the preliminary equilibrium is/aren't right. The last bookkeeping will

wrong, undercast or cloudy of net benefit/deficit in pay proclamation, lop-sidedness in the assertion of monetary position.

A preliminary equilibrium recognize blunder made in the recording of exchanges by checking whether the sums of charge

and credit adjusts removed from record accounts are equivalent, actually look at the arithmetical precision of accounting

passages. (Kenton, 2020)

In any case, preliminary equilibrium may not distinguish all blunders, there are a few limits, not all types of errors can be

called attention to. This implies that it may not 100% right of the records, despite the fact that we have a decent

preliminary equilibrium (Kristin, 2021) . The trial balance might adjust in any event, when the accompanying mix-up has

been made:

1) Not even journalized was an exchange that is totally absent,

2) When some unacceptable number was written in the records of both

3) If a posting was made in the erroneous record, yet in the right sum

4) A passage that was never totally posted in the record

5) Double posting of a passage by mistake

The parts of trial balance

A preliminary equilibrium ought to incorporate a record number, account outline, and the last charge or credit balance in

each record. Moreover, the last date of the bookkeeping time frame for which the report is created ought to be shown.

1) Asset, costs and drawing are charge balance

2) Liabilities, capital and incomes are credit balance

c) financial accounting

A trial balance is a report that rundowns the balance of all broad record records of an organization at one point on

schedule. The records pondered a trial balance are identified with all significant bookkeeping things, including resources,

liabilities, value, incomes, costs, gains, and misfortunes. It is basically used to distinguish the equilibrium between

charges and credits sections from the exchanges recorded in the overall record at one point on schedule. Notwithstanding

mistake discovery, the preliminary equilibrium is ready to make the fundamental changing sections to the overall record.

It is arranged again after the changing sections are presented on guarantee that the all-out charges and credits are as yet

adjusted. It's anything but an authority budget summary. It is normally utilized inside and isn't disseminated to individuals

outside the organization. (CFI, 2021)

Why preliminary equilibrium is imperative to identify blunder

When there is an irregularity between all out charge adjusts and complete credit adjusts implies there are at least one

blunder in twofold sections and the record balance in the preliminary equilibrium is/aren't right. The last bookkeeping will

wrong, undercast or cloudy of net benefit/deficit in pay proclamation, lop-sidedness in the assertion of monetary position.

A preliminary equilibrium recognize blunder made in the recording of exchanges by checking whether the sums of charge

and credit adjusts removed from record accounts are equivalent, actually look at the arithmetical precision of accounting

passages. (Kenton, 2020)

In any case, preliminary equilibrium may not distinguish all blunders, there are a few limits, not all types of errors can be

called attention to. This implies that it may not 100% right of the records, despite the fact that we have a decent

preliminary equilibrium (Kristin, 2021) . The trial balance might adjust in any event, when the accompanying mix-up has

been made:

1) Not even journalized was an exchange that is totally absent,

2) When some unacceptable number was written in the records of both

3) If a posting was made in the erroneous record, yet in the right sum

4) A passage that was never totally posted in the record

5) Double posting of a passage by mistake

The parts of trial balance

A preliminary equilibrium ought to incorporate a record number, account outline, and the last charge or credit balance in

each record. Moreover, the last date of the bookkeeping time frame for which the report is created ought to be shown.

1) Asset, costs and drawing are charge balance

2) Liabilities, capital and incomes are credit balance

c) financial accounting

The financial account is important for a nation's equilibrium of instalments. The other two sections are the capital record

and the current record. The capital record estimates monetary exchanges that don't influence pay, creation, or investment

funds. Models incorporate worldwide exchanges of penetrating freedoms, brand names, and copyrights. The current

record estimates worldwide exchange of labour and products in addition to net gain and move instalments.

The monetary record is an estimation of increments or diminishes in global responsibility for. The proprietors can be

people, organizations, the public authority, or its national bank. The resources incorporate direct ventures, protections like

stocks and securities, and items like gold and hard money.

The monetary record provides details regarding the adjustment of all out worldwide resources held. You can see whether

the quantity of resources held expanded or diminished. It doesn't let you know how much in all out resources is at present

being held. (AMADEO, 2021)

Considerations of financial accounting

1) The type of possession

Proprietors should figure out which type of association to choose when starting another business. The choice of

it characterizes what bookkeeping procedures to utilize. Distinctive type of proprietorship has diverse

prerequisite on doing monetary bookkeeping. For sole broker and organization, as they are limitless

organization, there are no particular configuration. Notwithstanding, for restricted organizations, the fiscal

summaries ought to be founded on organizations' mandate prerequisite. (Averkamp, 2021)

2) Types of companies

Contrast with unlisted organization, the guideline of recorded organizations on monetary bookkeeping is stricter, they

need to follow a few prerequisites of Securities and Future Commission. Since, recorded organization need to unveil their

monetary data to public, unlisted organization just need to uncover their monetary data to inside partners. In this manner,

while doing a monetary bookkeeping, we are expected to thoughtful with regards to the kind of organizations, recorded

organizations might have more guideline on doing monetary bookkeeping. (Averkamp, 2021)

Regulation of financial accounting

1) Generally acknowledged bookkeeping rule (GAAP) Organizations are liable for introducing data on their incomes,

benefit making exercises, and by and large monetary conditions under sound accounting guidelines (GAAP). The pay

explanation, monetary record and income articulation are required. (Ross, 2021)

2) Accounting principle

Accruals

Gathering bookkeeping is one of two fundamental strategies for keeping your books, and for most organizations, it's the

most reliable way. In this article, Business.org clarifies what gathering bookkeeping means and how it assists you with

keeping your business' financials on target. Most organizations utilize one of two principle bookkeeping strategies to

maintain their books in control the one is gathering bookkeeping and the other is cash bookkeeping. In case you utilize

the accumulation strategy, you record monetary exchanges when they happen, not when cash really leaves or enters your

record. With cash bookkeeping, the inverse is valid: you will not make a diary section for your monetary exchanges until

the money has really been kept in or taken out from a ledger. (McQuarrie, 2020)

and the current record. The capital record estimates monetary exchanges that don't influence pay, creation, or investment

funds. Models incorporate worldwide exchanges of penetrating freedoms, brand names, and copyrights. The current

record estimates worldwide exchange of labour and products in addition to net gain and move instalments.

The monetary record is an estimation of increments or diminishes in global responsibility for. The proprietors can be

people, organizations, the public authority, or its national bank. The resources incorporate direct ventures, protections like

stocks and securities, and items like gold and hard money.

The monetary record provides details regarding the adjustment of all out worldwide resources held. You can see whether

the quantity of resources held expanded or diminished. It doesn't let you know how much in all out resources is at present

being held. (AMADEO, 2021)

Considerations of financial accounting

1) The type of possession

Proprietors should figure out which type of association to choose when starting another business. The choice of

it characterizes what bookkeeping procedures to utilize. Distinctive type of proprietorship has diverse

prerequisite on doing monetary bookkeeping. For sole broker and organization, as they are limitless

organization, there are no particular configuration. Notwithstanding, for restricted organizations, the fiscal

summaries ought to be founded on organizations' mandate prerequisite. (Averkamp, 2021)

2) Types of companies

Contrast with unlisted organization, the guideline of recorded organizations on monetary bookkeeping is stricter, they

need to follow a few prerequisites of Securities and Future Commission. Since, recorded organization need to unveil their

monetary data to public, unlisted organization just need to uncover their monetary data to inside partners. In this manner,

while doing a monetary bookkeeping, we are expected to thoughtful with regards to the kind of organizations, recorded

organizations might have more guideline on doing monetary bookkeeping. (Averkamp, 2021)

Regulation of financial accounting

1) Generally acknowledged bookkeeping rule (GAAP) Organizations are liable for introducing data on their incomes,

benefit making exercises, and by and large monetary conditions under sound accounting guidelines (GAAP). The pay

explanation, monetary record and income articulation are required. (Ross, 2021)

2) Accounting principle

Accruals

Gathering bookkeeping is one of two fundamental strategies for keeping your books, and for most organizations, it's the

most reliable way. In this article, Business.org clarifies what gathering bookkeeping means and how it assists you with

keeping your business' financials on target. Most organizations utilize one of two principle bookkeeping strategies to

maintain their books in control the one is gathering bookkeeping and the other is cash bookkeeping. In case you utilize

the accumulation strategy, you record monetary exchanges when they happen, not when cash really leaves or enters your

record. With cash bookkeeping, the inverse is valid: you will not make a diary section for your monetary exchanges until

the money has really been kept in or taken out from a ledger. (McQuarrie, 2020)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In case there are no gathering guideline, the genuine degree of financial activity inside an organization won't really

address the measure of pay, cost, and benefit or misfortune in a year.

Going concern

Going concern is a bookkeeping rule that has the capital needed to keep on working endlessly before evidence

unexpectedly is given. This word frequently applies to the capacity of an organization to create adequate gains to remain

get by on the lookout or departure chapter 11. In monetary reports, a few expenses and resources might be delayed if a

company is viewed as a going concern. At the point when a business is presently not an issue, it should start unveiling

that information on its fiscal reports. If a company is certainly not a proceeding with concern, it implies that it has failed

and exchanged its resources. For instance, since the tech bust in the last part of the 1990s, many spot coms will at this

point don't influence organizations. (KENTON, 2021)

1) Accounting standard

Which is the rule to set up the fiscal reports, as indicated by Hong Kong Accounting Standards (HKAS) given by the

Hong Kong Institute of Certified Public Accountants.

HKFRS characterized norms for distinguishing proof, estimation, show and revelation identifying with exchanges and

occasions that are important in budget reports for general purposes. HKFRS depends on the Financial Statements

Preparation and Presentation System that examines the standards basic the subtleties contained in the Financial

Statements for General Purpose. In for all intents and purposes all conditions, the sensible use of HKFRS, with extra

revelation where appropriate, brings about budget reports which offer an exact and reasonable view. the SME Financial

Reporting Framework (SME-FRF) and Financial Reporting Standard (SME-FRS) gave from them are the monetary report

standard for SME-FRF. (CARLSON, 2019)

d)Trial balance

Cash

Date $ Date $

Jul-21

Account

receivabl

e

1400 Jul-05

Prepaid

insuranc

e

1800

Jul-01 capital 10000 Jul-01 Truck 3000

Jul-18 Account payable 2000

Jul-20 Salaries 1500

Jul-31 Drawing 700

Jul-30

Gas and

oil

expenses

200

Jul-31 Balances c/d 2200

11400 11400

Capital

Date $ Date $

address the measure of pay, cost, and benefit or misfortune in a year.

Going concern

Going concern is a bookkeeping rule that has the capital needed to keep on working endlessly before evidence

unexpectedly is given. This word frequently applies to the capacity of an organization to create adequate gains to remain

get by on the lookout or departure chapter 11. In monetary reports, a few expenses and resources might be delayed if a

company is viewed as a going concern. At the point when a business is presently not an issue, it should start unveiling

that information on its fiscal reports. If a company is certainly not a proceeding with concern, it implies that it has failed

and exchanged its resources. For instance, since the tech bust in the last part of the 1990s, many spot coms will at this

point don't influence organizations. (KENTON, 2021)

1) Accounting standard

Which is the rule to set up the fiscal reports, as indicated by Hong Kong Accounting Standards (HKAS) given by the

Hong Kong Institute of Certified Public Accountants.

HKFRS characterized norms for distinguishing proof, estimation, show and revelation identifying with exchanges and

occasions that are important in budget reports for general purposes. HKFRS depends on the Financial Statements

Preparation and Presentation System that examines the standards basic the subtleties contained in the Financial

Statements for General Purpose. In for all intents and purposes all conditions, the sensible use of HKFRS, with extra

revelation where appropriate, brings about budget reports which offer an exact and reasonable view. the SME Financial

Reporting Framework (SME-FRF) and Financial Reporting Standard (SME-FRS) gave from them are the monetary report

standard for SME-FRF. (CARLSON, 2019)

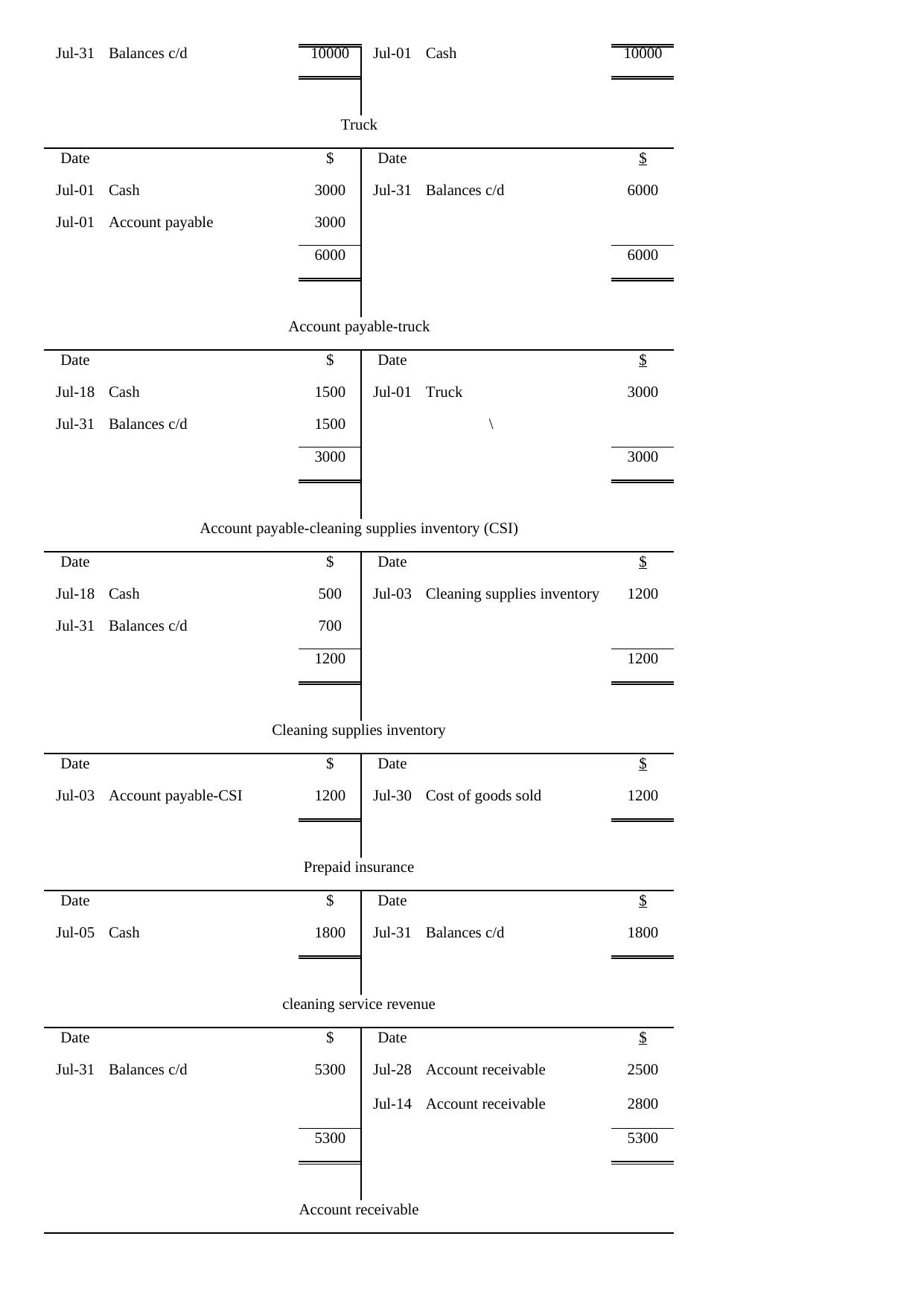

d)Trial balance

Cash

Date $ Date $

Jul-21

Account

receivabl

e

1400 Jul-05

Prepaid

insuranc

e

1800

Jul-01 capital 10000 Jul-01 Truck 3000

Jul-18 Account payable 2000

Jul-20 Salaries 1500

Jul-31 Drawing 700

Jul-30

Gas and

oil

expenses

200

Jul-31 Balances c/d 2200

11400 11400

Capital

Date $ Date $

Jul-31 Balances c/d 10000 Jul-01 Cash 10000

Truck

Date $ Date $

Jul-01 Cash 3000 Jul-31 Balances c/d 6000

Jul-01 Account payable 3000

6000 6000

Account payable-truck

Date $ Date $

Jul-18 Cash 1500 Jul-01 Truck 3000

Jul-31 Balances c/d 1500 \

3000 3000

Account payable-cleaning supplies inventory (CSI)

Date $ Date $

Jul-18 Cash 500 Jul-03 Cleaning supplies inventory 1200

Jul-31 Balances c/d 700

1200 1200

Cleaning supplies inventory

Date $ Date $

Jul-03 Account payable-CSI 1200 Jul-30 Cost of goods sold 1200

Prepaid insurance

Date $ Date $

Jul-05 Cash 1800 Jul-31 Balances c/d 1800

cleaning service revenue

Date $ Date $

Jul-31 Balances c/d 5300 Jul-28 Account receivable 2500

Jul-14 Account receivable 2800

5300 5300

Account receivable

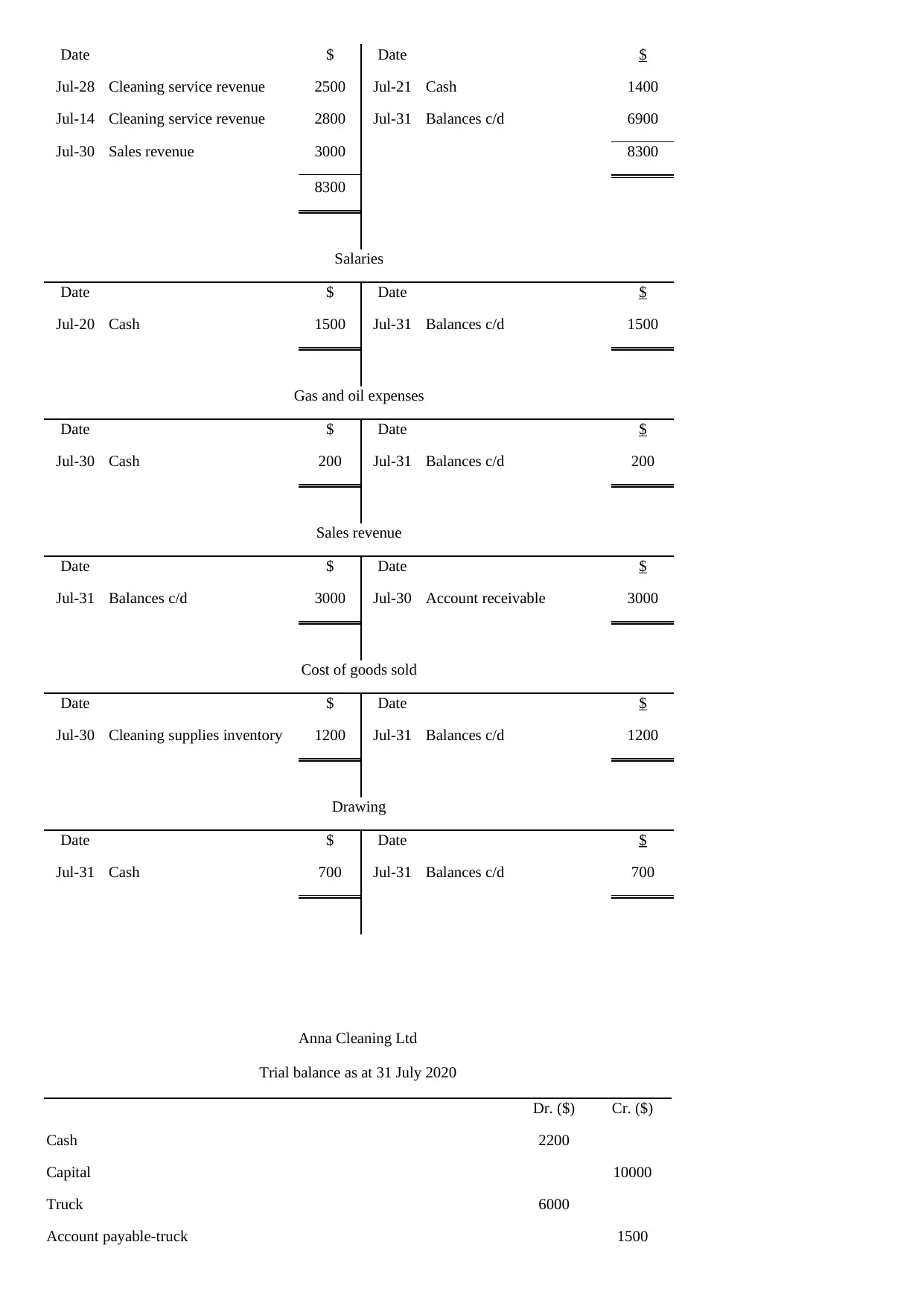

Truck

Date $ Date $

Jul-01 Cash 3000 Jul-31 Balances c/d 6000

Jul-01 Account payable 3000

6000 6000

Account payable-truck

Date $ Date $

Jul-18 Cash 1500 Jul-01 Truck 3000

Jul-31 Balances c/d 1500 \

3000 3000

Account payable-cleaning supplies inventory (CSI)

Date $ Date $

Jul-18 Cash 500 Jul-03 Cleaning supplies inventory 1200

Jul-31 Balances c/d 700

1200 1200

Cleaning supplies inventory

Date $ Date $

Jul-03 Account payable-CSI 1200 Jul-30 Cost of goods sold 1200

Prepaid insurance

Date $ Date $

Jul-05 Cash 1800 Jul-31 Balances c/d 1800

cleaning service revenue

Date $ Date $

Jul-31 Balances c/d 5300 Jul-28 Account receivable 2500

Jul-14 Account receivable 2800

5300 5300

Account receivable

Date $ Date $

Jul-28 Cleaning service revenue 2500 Jul-21 Cash 1400

Jul-14 Cleaning service revenue 2800 Jul-31 Balances c/d 6900

Jul-30 Sales revenue 3000 8300

8300

Salaries

Date $ Date $

Jul-20 Cash 1500 Jul-31 Balances c/d 1500

Gas and oil expenses

Date $ Date $

Jul-30 Cash 200 Jul-31 Balances c/d 200

Sales revenue

Date $ Date $

Jul-31 Balances c/d 3000 Jul-30 Account receivable 3000

Cost of goods sold

Date $ Date $

Jul-30 Cleaning supplies inventory 1200 Jul-31 Balances c/d 1200

Drawing

Date $ Date $

Jul-31 Cash 700 Jul-31 Balances c/d 700

Anna Cleaning Ltd

Trial balance as at 31 July 2020

Dr. ($) Cr. ($)

Cash 2200

Capital 10000

Truck 6000

Account payable-truck 1500

Jul-28 Cleaning service revenue 2500 Jul-21 Cash 1400

Jul-14 Cleaning service revenue 2800 Jul-31 Balances c/d 6900

Jul-30 Sales revenue 3000 8300

8300

Salaries

Date $ Date $

Jul-20 Cash 1500 Jul-31 Balances c/d 1500

Gas and oil expenses

Date $ Date $

Jul-30 Cash 200 Jul-31 Balances c/d 200

Sales revenue

Date $ Date $

Jul-31 Balances c/d 3000 Jul-30 Account receivable 3000

Cost of goods sold

Date $ Date $

Jul-30 Cleaning supplies inventory 1200 Jul-31 Balances c/d 1200

Drawing

Date $ Date $

Jul-31 Cash 700 Jul-31 Balances c/d 700

Anna Cleaning Ltd

Trial balance as at 31 July 2020

Dr. ($) Cr. ($)

Cash 2200

Capital 10000

Truck 6000

Account payable-truck 1500

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

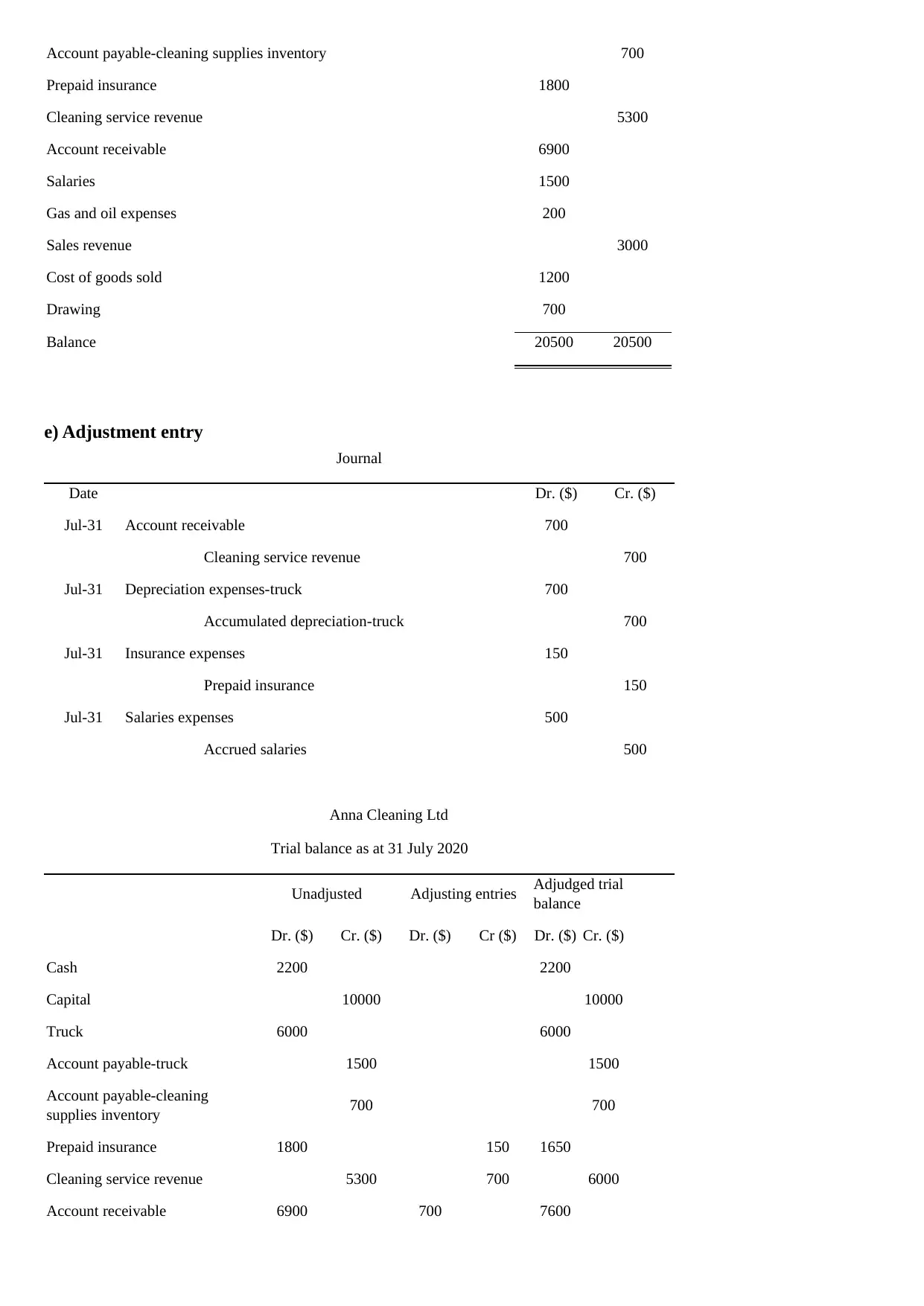

Account payable-cleaning supplies inventory 700

Prepaid insurance 1800

Cleaning service revenue 5300

Account receivable 6900

Salaries 1500

Gas and oil expenses 200

Sales revenue 3000

Cost of goods sold 1200

Drawing 700

Balance 20500 20500

e) Adjustment entry

Journal

Date Dr. ($) Cr. ($)

Jul-31 Account receivable 700

Cleaning service revenue 700

Jul-31 Depreciation expenses-truck 700

Accumulated depreciation-truck 700

Jul-31 Insurance expenses 150

Prepaid insurance 150

Jul-31 Salaries expenses 500

Accrued salaries 500

Anna Cleaning Ltd

Trial balance as at 31 July 2020

Unadjusted Adjusting entries Adjudged trial

balance

Dr. ($) Cr. ($) Dr. ($) Cr ($) Dr. ($) Cr. ($)

Cash 2200 2200

Capital 10000 10000

Truck 6000 6000

Account payable-truck 1500 1500

Account payable-cleaning

supplies inventory 700 700

Prepaid insurance 1800 150 1650

Cleaning service revenue 5300 700 6000

Account receivable 6900 700 7600

Prepaid insurance 1800

Cleaning service revenue 5300

Account receivable 6900

Salaries 1500

Gas and oil expenses 200

Sales revenue 3000

Cost of goods sold 1200

Drawing 700

Balance 20500 20500

e) Adjustment entry

Journal

Date Dr. ($) Cr. ($)

Jul-31 Account receivable 700

Cleaning service revenue 700

Jul-31 Depreciation expenses-truck 700

Accumulated depreciation-truck 700

Jul-31 Insurance expenses 150

Prepaid insurance 150

Jul-31 Salaries expenses 500

Accrued salaries 500

Anna Cleaning Ltd

Trial balance as at 31 July 2020

Unadjusted Adjusting entries Adjudged trial

balance

Dr. ($) Cr. ($) Dr. ($) Cr ($) Dr. ($) Cr. ($)

Cash 2200 2200

Capital 10000 10000

Truck 6000 6000

Account payable-truck 1500 1500

Account payable-cleaning

supplies inventory 700 700

Prepaid insurance 1800 150 1650

Cleaning service revenue 5300 700 6000

Account receivable 6900 700 7600

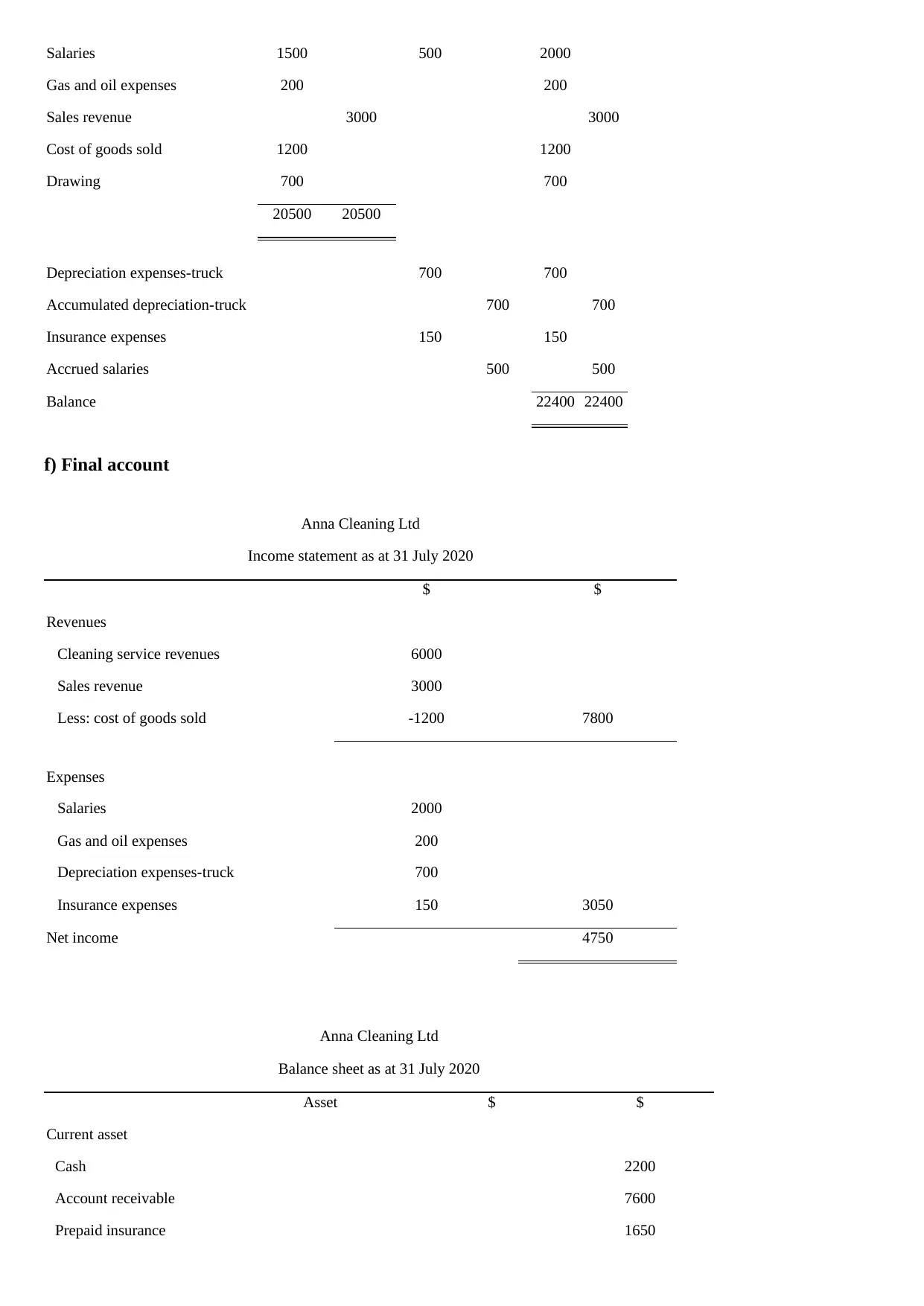

Salaries 1500 500 2000

Gas and oil expenses 200 200

Sales revenue 3000 3000

Cost of goods sold 1200 1200

Drawing 700 700

20500 20500

Depreciation expenses-truck 700 700

Accumulated depreciation-truck 700 700

Insurance expenses 150 150

Accrued salaries 500 500

Balance 22400 22400

f) Final account

Anna Cleaning Ltd

Income statement as at 31 July 2020

$ $

Revenues

Cleaning service revenues 6000

Sales revenue 3000

Less: cost of goods sold -1200 7800

Expenses

Salaries 2000

Gas and oil expenses 200

Depreciation expenses-truck 700

Insurance expenses 150 3050

Net income 4750

Anna Cleaning Ltd

Balance sheet as at 31 July 2020

Asset $ $

Current asset

Cash 2200

Account receivable 7600

Prepaid insurance 1650

Gas and oil expenses 200 200

Sales revenue 3000 3000

Cost of goods sold 1200 1200

Drawing 700 700

20500 20500

Depreciation expenses-truck 700 700

Accumulated depreciation-truck 700 700

Insurance expenses 150 150

Accrued salaries 500 500

Balance 22400 22400

f) Final account

Anna Cleaning Ltd

Income statement as at 31 July 2020

$ $

Revenues

Cleaning service revenues 6000

Sales revenue 3000

Less: cost of goods sold -1200 7800

Expenses

Salaries 2000

Gas and oil expenses 200

Depreciation expenses-truck 700

Insurance expenses 150 3050

Net income 4750

Anna Cleaning Ltd

Balance sheet as at 31 July 2020

Asset $ $

Current asset

Cash 2200

Account receivable 7600

Prepaid insurance 1650

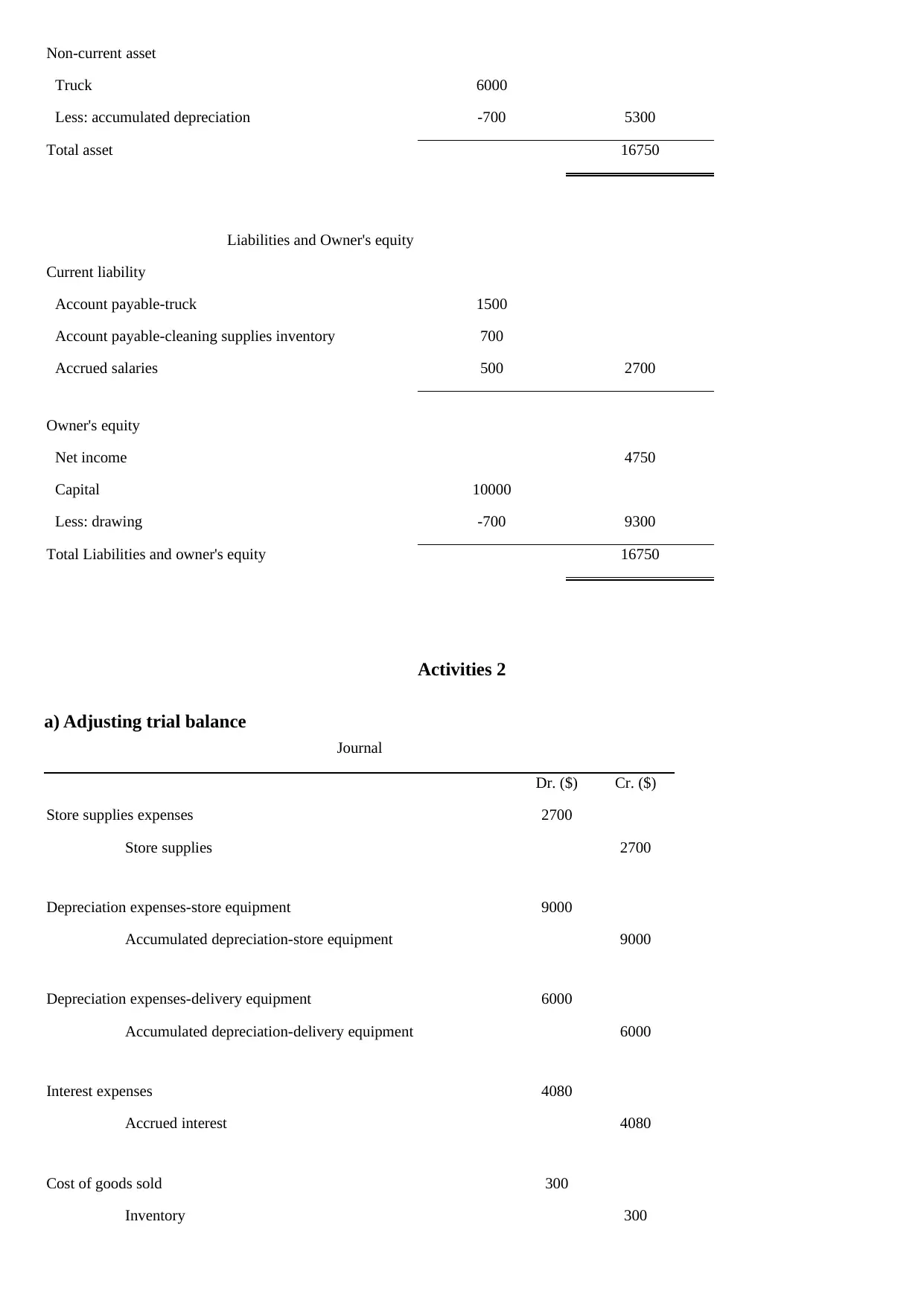

Non-current asset

Truck 6000

Less: accumulated depreciation -700 5300

Total asset 16750

Liabilities and Owner's equity

Current liability

Account payable-truck 1500

Account payable-cleaning supplies inventory 700

Accrued salaries 500 2700

Owner's equity

Net income 4750

Capital 10000

Less: drawing -700 9300

Total Liabilities and owner's equity 16750

Activities 2

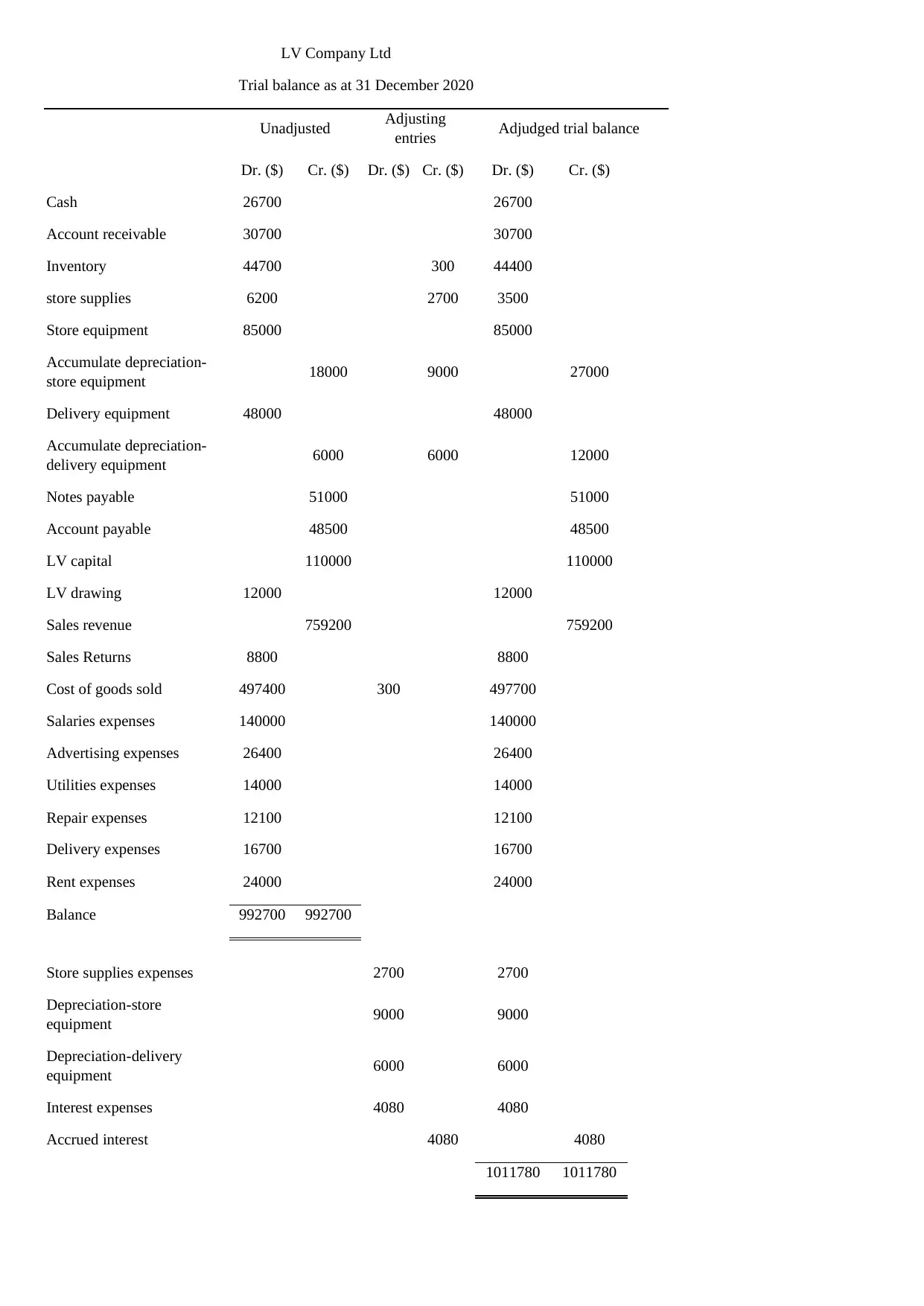

a) Adjusting trial balance

Journal

Dr. ($) Cr. ($)

Store supplies expenses 2700

Store supplies 2700

Depreciation expenses-store equipment 9000

Accumulated depreciation-store equipment 9000

Depreciation expenses-delivery equipment 6000

Accumulated depreciation-delivery equipment 6000

Interest expenses 4080

Accrued interest 4080

Cost of goods sold 300

Inventory 300

Truck 6000

Less: accumulated depreciation -700 5300

Total asset 16750

Liabilities and Owner's equity

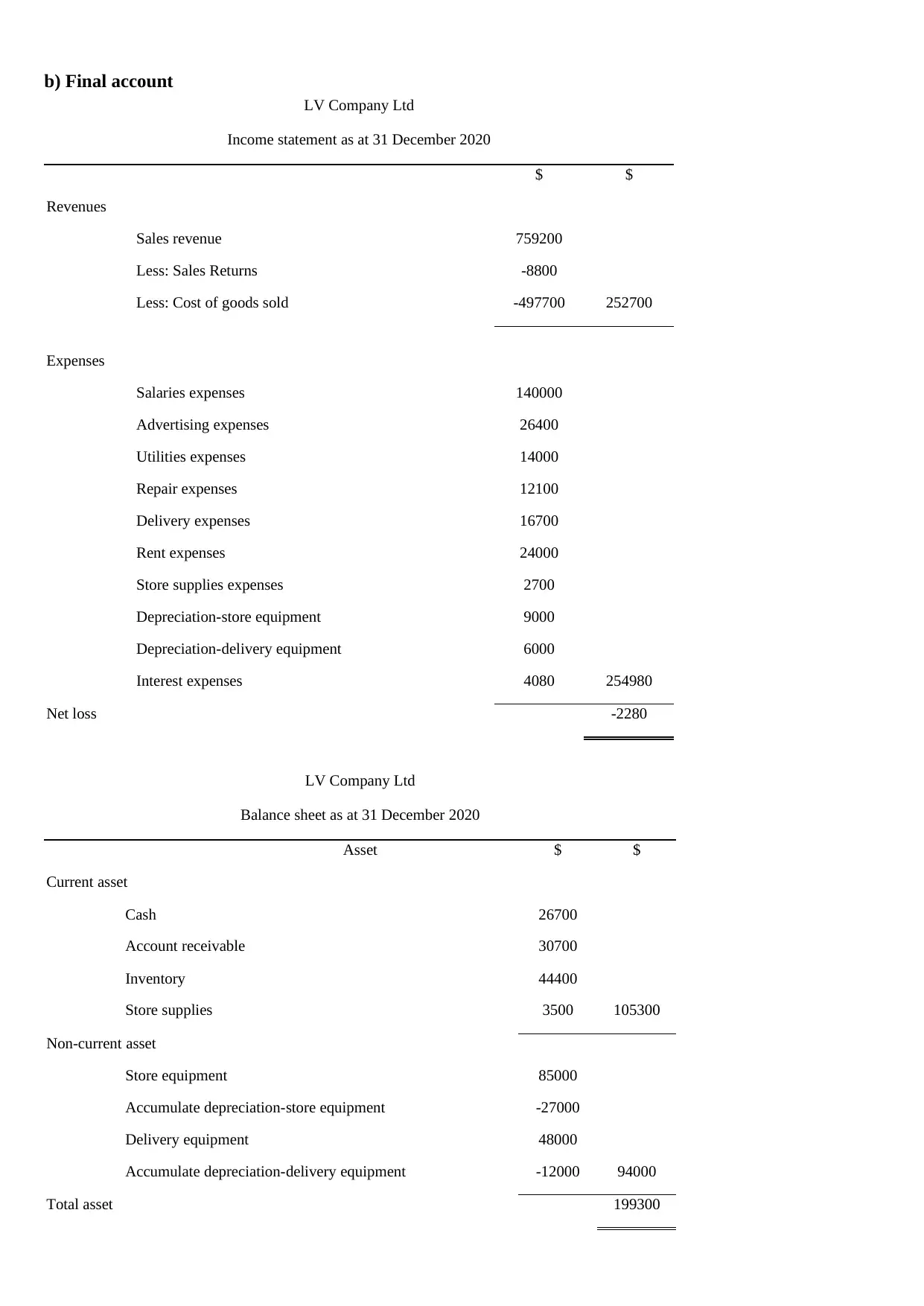

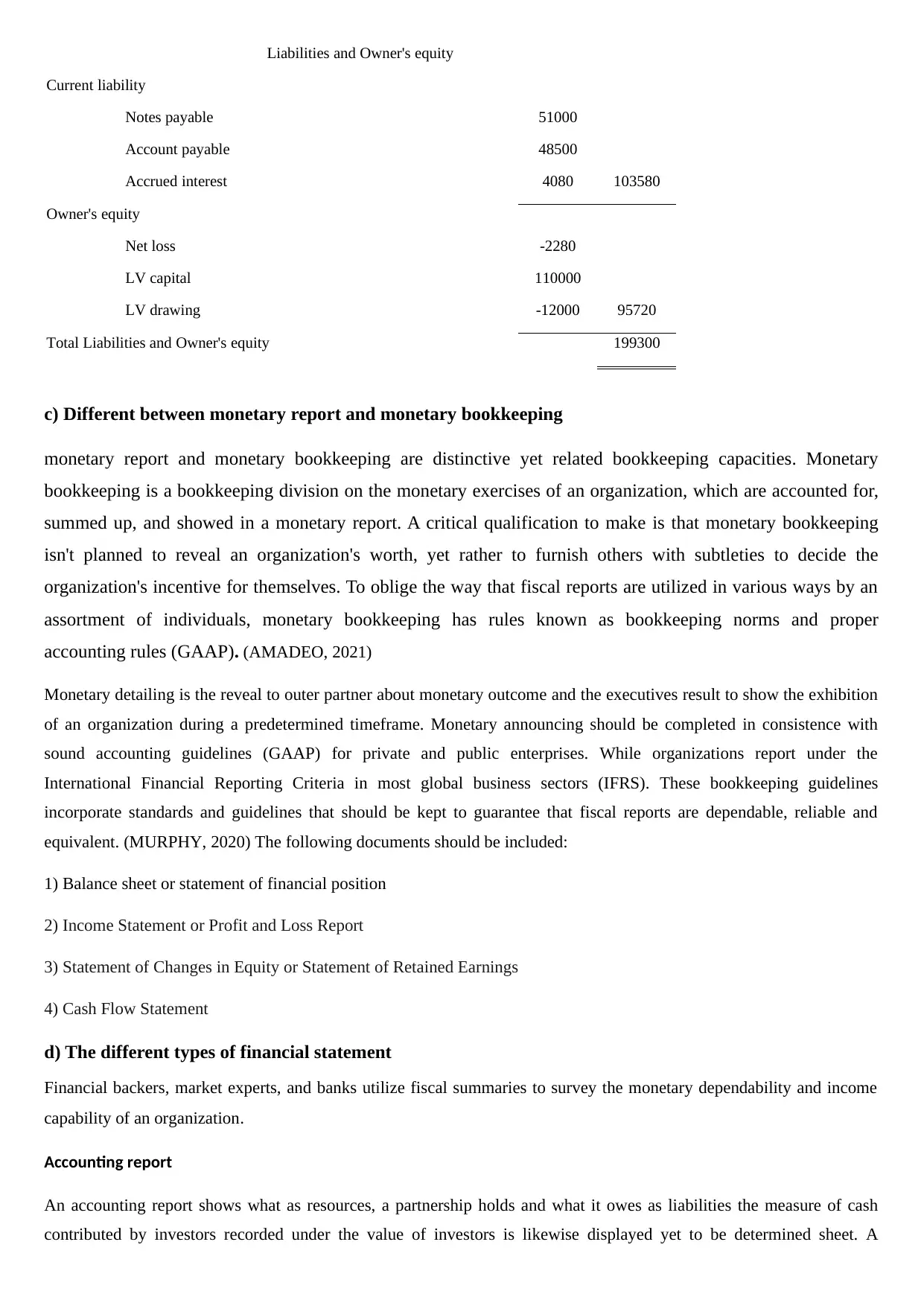

Current liability