Financial Accounting

20 Pages4294 Words65 Views

Added on 2023-01-12

Financial Accounting

Added on 2023-01-12

ShareRelated Documents

FINANCIAL ACCOUNTING

TABLE OF CONTENTS

INTRODUTION .............................................................................................................................3

INFORMATION BOOKLET..........................................................................................................3

LO1..................................................................................................................................................3

Double entry book–keeping and trial balance and regulations....................................................3

Case Study 1................................................................................................................................4

Case Study 2................................................................................................................................4

Case Study 3................................................................................................................................5

Case Study 4................................................................................................................................5

Case Study 5................................................................................................................................8

Difference between the financial reports and financial statements. ...........................................9

LO2................................................................................................................................................10

Explanation of the accounts for sole trader, partnership and limited company and their

differences..................................................................................................................................10

Final accounts of sole trader, partnership and company............................................................11

LO3................................................................................................................................................14

Explanation of the reconciliation process and tools & techniques used for checking general

ledger accounts. Explanation on variances and importance of the correctly entered figures....14

Bank Reconciliation Statement..................................................................................................15

LO4................................................................................................................................................16

Explanation of the control accounts and their use in financial accounting................................16

Description of process for reconciling control accounts and need to reconcile the accounts....17

Explanation on purpose of suspense accounts and their difference from the control accounts.18

Control Account.........................................................................................................................19

CONCLUSION .............................................................................................................................20

REFERENCES..............................................................................................................................21

INTRODUTION .............................................................................................................................3

INFORMATION BOOKLET..........................................................................................................3

LO1..................................................................................................................................................3

Double entry book–keeping and trial balance and regulations....................................................3

Case Study 1................................................................................................................................4

Case Study 2................................................................................................................................4

Case Study 3................................................................................................................................5

Case Study 4................................................................................................................................5

Case Study 5................................................................................................................................8

Difference between the financial reports and financial statements. ...........................................9

LO2................................................................................................................................................10

Explanation of the accounts for sole trader, partnership and limited company and their

differences..................................................................................................................................10

Final accounts of sole trader, partnership and company............................................................11

LO3................................................................................................................................................14

Explanation of the reconciliation process and tools & techniques used for checking general

ledger accounts. Explanation on variances and importance of the correctly entered figures....14

Bank Reconciliation Statement..................................................................................................15

LO4................................................................................................................................................16

Explanation of the control accounts and their use in financial accounting................................16

Description of process for reconciling control accounts and need to reconcile the accounts....17

Explanation on purpose of suspense accounts and their difference from the control accounts.18

Control Account.........................................................................................................................19

CONCLUSION .............................................................................................................................20

REFERENCES..............................................................................................................................21

INTRODUTION

Financial accounting refers to process of preparing the financial statements which represents

the financial position and performance of the company. These financial information is useful for

both the internal management and stakeholders of the company such as creditors, investors,

suppliers and customers. Financial accounting is different from managerial accounting that

prepares financial records for the internal management of the company. Financial statements

prepared by the company are income statement, balance sheet and cash flow statements. They

are prepared by the company as per the applicable accounting standards. Present report will be

revealing about the concepts and methods of financial accounting. It will provide explanation on

double entry book keeping, financial reports and the financial statements. It will also provide

about the sole traders, partnership and limited company form of doing business. Report will

address the reconciliation process and techniques used for checking the balances of general

ledger and the use of control accounts in financial accounting. The concepts will be explained

with the help of examples and case studies. Study will enhance the understanding of financial

accounting concepts and techniques.

INFORMATION BOOKLET

LO1

Double entry book–keeping and trial balance and regulations.

Book keeping or double entry system

means that every transaction of the business

affects minimum two accounts. It is to be

recorded in at least two accounts.. It was

established for giving equal effects to the

debit and credit side of the balances. Double

entry requires the accounting equation to be

in balance i.e. assets = owner’s equity +

liabilities. This requires the balance in assets

side should be equal to the balance in

liabilities and equity side.

Trial balance is statement prepared in

double entry system containing the debits

and credit balances of all the ledger

accounts. Trial balance is prepared after

closing the ledger accounts for balancing the

debits and credit side of all the accounts of

business. Trial balance is prepared by the

business for ensuring that entries recorded

for the financial transactions in the ledger

accounts and are balanced at the end. The

debit and credit side of the trial balance

should be equal. In a double entry system

trial balance is used for the preparation of

financial statements. Balance of the accounts

in trial balance is transferred to the

3

Financial accounting refers to process of preparing the financial statements which represents

the financial position and performance of the company. These financial information is useful for

both the internal management and stakeholders of the company such as creditors, investors,

suppliers and customers. Financial accounting is different from managerial accounting that

prepares financial records for the internal management of the company. Financial statements

prepared by the company are income statement, balance sheet and cash flow statements. They

are prepared by the company as per the applicable accounting standards. Present report will be

revealing about the concepts and methods of financial accounting. It will provide explanation on

double entry book keeping, financial reports and the financial statements. It will also provide

about the sole traders, partnership and limited company form of doing business. Report will

address the reconciliation process and techniques used for checking the balances of general

ledger and the use of control accounts in financial accounting. The concepts will be explained

with the help of examples and case studies. Study will enhance the understanding of financial

accounting concepts and techniques.

INFORMATION BOOKLET

LO1

Double entry book–keeping and trial balance and regulations.

Book keeping or double entry system

means that every transaction of the business

affects minimum two accounts. It is to be

recorded in at least two accounts.. It was

established for giving equal effects to the

debit and credit side of the balances. Double

entry requires the accounting equation to be

in balance i.e. assets = owner’s equity +

liabilities. This requires the balance in assets

side should be equal to the balance in

liabilities and equity side.

Trial balance is statement prepared in

double entry system containing the debits

and credit balances of all the ledger

accounts. Trial balance is prepared after

closing the ledger accounts for balancing the

debits and credit side of all the accounts of

business. Trial balance is prepared by the

business for ensuring that entries recorded

for the financial transactions in the ledger

accounts and are balanced at the end. The

debit and credit side of the trial balance

should be equal. In a double entry system

trial balance is used for the preparation of

financial statements. Balance of the accounts

in trial balance is transferred to the

3

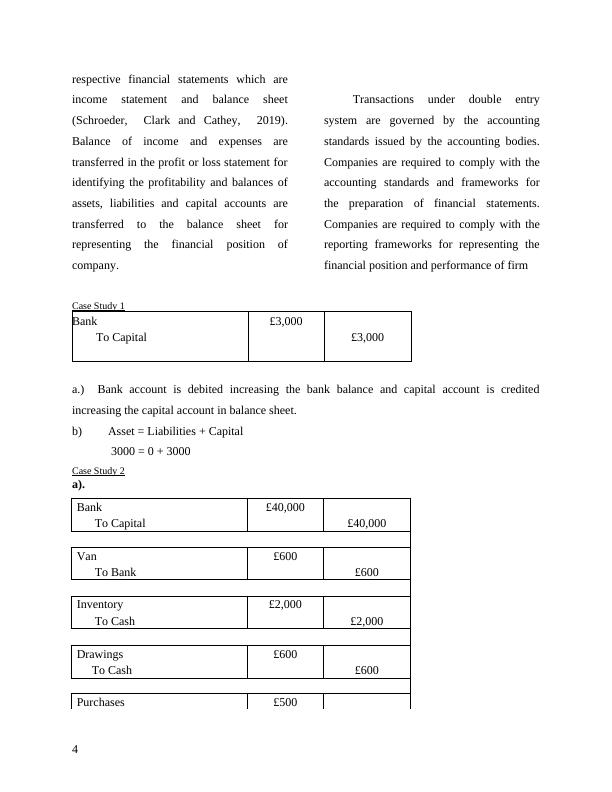

respective financial statements which are

income statement and balance sheet

(Schroeder, Clark and Cathey, 2019).

Balance of income and expenses are

transferred in the profit or loss statement for

identifying the profitability and balances of

assets, liabilities and capital accounts are

transferred to the balance sheet for

representing the financial position of

company.

Transactions under double entry

system are governed by the accounting

standards issued by the accounting bodies.

Companies are required to comply with the

accounting standards and frameworks for

the preparation of financial statements.

Companies are required to comply with the

reporting frameworks for representing the

financial position and performance of firm

Case Study 1

Bank £3,000

To Capital £3,000

a.) Bank account is debited increasing the bank balance and capital account is credited

increasing the capital account in balance sheet.

b) Asset = Liabilities + Capital

3000 = 0 + 3000

Case Study 2

a).

Bank £40,000

To Capital £40,000

Van £600

To Bank £600

Inventory £2,000

To Cash £2,000

Drawings £600

To Cash £600

Purchases £500

4

income statement and balance sheet

(Schroeder, Clark and Cathey, 2019).

Balance of income and expenses are

transferred in the profit or loss statement for

identifying the profitability and balances of

assets, liabilities and capital accounts are

transferred to the balance sheet for

representing the financial position of

company.

Transactions under double entry

system are governed by the accounting

standards issued by the accounting bodies.

Companies are required to comply with the

accounting standards and frameworks for

the preparation of financial statements.

Companies are required to comply with the

reporting frameworks for representing the

financial position and performance of firm

Case Study 1

Bank £3,000

To Capital £3,000

a.) Bank account is debited increasing the bank balance and capital account is credited

increasing the capital account in balance sheet.

b) Asset = Liabilities + Capital

3000 = 0 + 3000

Case Study 2

a).

Bank £40,000

To Capital £40,000

Van £600

To Bank £600

Inventory £2,000

To Cash £2,000

Drawings £600

To Cash £600

Purchases £500

4

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Accounting: Concepts and Techniqueslg...

|21

|4301

|64

Financial Accounting INTRODUCTION 1 TASK 11 Question 1 2 7 TASK 29 Question 1 2 7 CONCLUSION 11 REFERENCES 12 INTRODUCTIONlg...

|14

|1243

|343

Level 5 Higher National diploma: Unit 10 - Financial Accountinglg...

|37

|8455

|8

FINANCIAL ACCOUNTING PRINCIPLE INTROUCTION 1 PART A1 Business Reportlg...

|36

|9395

|326

Financial Accounting: Record Transactions and Prepare Final Accountslg...

|33

|7917

|68

Assignment Front Sheet Learner Name Learner Student I.D. Assessor Name Navroop Sandhu 1017470 Mr. LAMlg...

|36

|9707

|279