VAT Legislations and Tax Filing Requirements

VerifiedAdded on 2020/10/23

|13

|3789

|214

AI Summary

The report discusses VAT legislations and rules in the UK, including the importance of maintaining accurate records for VAT return filing. It highlights the penalties and fines associated with late or no returns and provides a summary of the progressions in VAT since its initiation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

INDIRECT TAX

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Source of information on VAT..............................................................................................1

1.2 Interaction of organisation with government agency.............................................................1

1.3 VAT registration requirements..............................................................................................2

1.4 Information required to considered for business documentation of VAT registered business

......................................................................................................................................................2

1.5 Requirements and the frequency of reporting for VAT schemes..........................................3

1.6 Up to date knowledge of changes to codes of practice, regulation or legislation..................3

TASK 2............................................................................................................................................4

2.1 relevant data for a specific period form the accounting system.............................................4

2.2 Calculation of input and outputs using the VAT classification.............................................5

2.3 Calculation of the VAT due to, or form the relevant tax authority........................................6

2.4 VAT return and associated payment with in the statutory time limits..................................6

TASK 3............................................................................................................................................7

3.1 The implications and penalties for an organisation resulting from failure to abide by VAT

regulations....................................................................................................................................7

3.2 Adjustments and declarations for any errors or omission identified in previous VAT

periods..........................................................................................................................................8

TASK 4............................................................................................................................................9

4.1 Inform the managers of the impact that the VAT payment may have organisations cash

flow..............................................................................................................................................9

4.2 VAT legislation which would have an effect on an organization's recording systems.......10

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Source of information on VAT..............................................................................................1

1.2 Interaction of organisation with government agency.............................................................1

1.3 VAT registration requirements..............................................................................................2

1.4 Information required to considered for business documentation of VAT registered business

......................................................................................................................................................2

1.5 Requirements and the frequency of reporting for VAT schemes..........................................3

1.6 Up to date knowledge of changes to codes of practice, regulation or legislation..................3

TASK 2............................................................................................................................................4

2.1 relevant data for a specific period form the accounting system.............................................4

2.2 Calculation of input and outputs using the VAT classification.............................................5

2.3 Calculation of the VAT due to, or form the relevant tax authority........................................6

2.4 VAT return and associated payment with in the statutory time limits..................................6

TASK 3............................................................................................................................................7

3.1 The implications and penalties for an organisation resulting from failure to abide by VAT

regulations....................................................................................................................................7

3.2 Adjustments and declarations for any errors or omission identified in previous VAT

periods..........................................................................................................................................8

TASK 4............................................................................................................................................9

4.1 Inform the managers of the impact that the VAT payment may have organisations cash

flow..............................................................................................................................................9

4.2 VAT legislation which would have an effect on an organization's recording systems.......10

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Indirect tax is being considered as a tax (charge/levied) over services/goods rather than

on any profits or income of an individual (Bahl, 2018). Tax reforms, legislations and standards

are defined in context to VAT. The procedure of business documentation and reporting under

Value Added Tax schemes are defined in this report. Requirements of filing VAT returns in

adequate manner with classification of Value-Added Tax information presented clearly for a

specific period from the accounting system. Penalties and adjustments regarding past returns and

errors justified with in VAT period. Ways to execute Value-added Tax information among

managers communicated with impact of VAT payment. Variations in VAT legislations that have

an impact on an organisation's recording system are also considered in this report.

TASK 1

1.1 Source of information on VAT

Value-added tax (VAT) can be defined as an intake tax that is being applied over a

product at the time when value is basically added at every phase of supply chain, production and

at time of sale. It is being found that VAT, is paid by an individual on cost of a product. There

are type of sources available to get information regarding VAT are as follows;

European commission: It is the governing body that is responsible for introducing

legislations, upholding the the treaties, implementing decisions to day to day business in

European union. This commission provides VAT information. It contains the invoicing details,

charging events, taxable persons, deductions and the VAT return procedures.

The Value - Added Tax and Alternative Sources of Federal Revenue: This is one of

the supporting source of getting the information related to payment of VAT and submission of

return.

HM revenue and customs: This is the non ministerial department of the UK

government. This is one of the the source of getting information regarding collection of VAT,

other nominal charges and taxes.

1.2 Interaction of organisation with government agency

Business organisations have direct relation with government agencies. Organisation have

to take assistance of government agencies to deal with new rules and legislations introduced in

the UK. Retails and manufactures comes in this category to communicate the VAT requirements.

1

Indirect tax is being considered as a tax (charge/levied) over services/goods rather than

on any profits or income of an individual (Bahl, 2018). Tax reforms, legislations and standards

are defined in context to VAT. The procedure of business documentation and reporting under

Value Added Tax schemes are defined in this report. Requirements of filing VAT returns in

adequate manner with classification of Value-Added Tax information presented clearly for a

specific period from the accounting system. Penalties and adjustments regarding past returns and

errors justified with in VAT period. Ways to execute Value-added Tax information among

managers communicated with impact of VAT payment. Variations in VAT legislations that have

an impact on an organisation's recording system are also considered in this report.

TASK 1

1.1 Source of information on VAT

Value-added tax (VAT) can be defined as an intake tax that is being applied over a

product at the time when value is basically added at every phase of supply chain, production and

at time of sale. It is being found that VAT, is paid by an individual on cost of a product. There

are type of sources available to get information regarding VAT are as follows;

European commission: It is the governing body that is responsible for introducing

legislations, upholding the the treaties, implementing decisions to day to day business in

European union. This commission provides VAT information. It contains the invoicing details,

charging events, taxable persons, deductions and the VAT return procedures.

The Value - Added Tax and Alternative Sources of Federal Revenue: This is one of

the supporting source of getting the information related to payment of VAT and submission of

return.

HM revenue and customs: This is the non ministerial department of the UK

government. This is one of the the source of getting information regarding collection of VAT,

other nominal charges and taxes.

1.2 Interaction of organisation with government agency

Business organisations have direct relation with government agencies. Organisation have

to take assistance of government agencies to deal with new rules and legislations introduced in

the UK. Retails and manufactures comes in this category to communicate the VAT requirements.

1

Organisations interact with government agencies through formal communication medium. For

example, A manufacturer can communicate have to apply for VAT registration for come in

existence in the eyes of government (Cnossen, 2013).

1.3 VAT registration requirements

VAT registration is required if the turnover of the organisation exceeds form £85000.

VAT registration is Mandatory if taxable turnover is found more than £85000 in the next 30 day

period or if organisation had a VAT taxable turnover more than £85000 over the last 12 months.

For instance of future traders occurs taxable turnover during 1st April 2017 and 31th March 2018

than Future Traders have to register for VAT till 30th April 2018. and effective date will be 1st

May 2018.

Registration of VAT is done by filling form online as well as offline too, mostly business

entities such as partnership firms or companies opt for online registrations for themselves.

Organisation can register through agents just to provide necessary information like VAT returns

(Capéau, Decoster and Phillips, 2014). After registration company get their value added tax

number from HM Revenue and Customs (HMRC). such as VAT1A form provided for those who

are distance sellers, VAT1B I for importers and VAT1C if company wants to dispose their

assets. After completion of VAT registration organisations receive their VAT certificates within

30 working days. It is directly sent to their online VAT accounts or by post if registered offline

through an agent.

1.4 Information required to considered for business documentation of VAT registered business

There is type of information is required to considers while filing registration for business.

HMRC provides information related to registration of VAT.

Form VAT1 for all class of members that contains applicants details provided by HMRC

of (full name, home address, date of birth and National Insurance number (or Tax ID if

the applicant is a foreign national). If assesses provide tax ID that it requires to submit

another three documents as 1 copy of government identification like driving licence and

national identity and 2 copies of correspondence that contains the mane and address, bank

statement is an alternative document in option.

Form VAT2 it is required maintain if business is a partnership form

Form VAT50 and VAT51 if b

Form VAT5L Applies if the business activities involve land and property

2

example, A manufacturer can communicate have to apply for VAT registration for come in

existence in the eyes of government (Cnossen, 2013).

1.3 VAT registration requirements

VAT registration is required if the turnover of the organisation exceeds form £85000.

VAT registration is Mandatory if taxable turnover is found more than £85000 in the next 30 day

period or if organisation had a VAT taxable turnover more than £85000 over the last 12 months.

For instance of future traders occurs taxable turnover during 1st April 2017 and 31th March 2018

than Future Traders have to register for VAT till 30th April 2018. and effective date will be 1st

May 2018.

Registration of VAT is done by filling form online as well as offline too, mostly business

entities such as partnership firms or companies opt for online registrations for themselves.

Organisation can register through agents just to provide necessary information like VAT returns

(Capéau, Decoster and Phillips, 2014). After registration company get their value added tax

number from HM Revenue and Customs (HMRC). such as VAT1A form provided for those who

are distance sellers, VAT1B I for importers and VAT1C if company wants to dispose their

assets. After completion of VAT registration organisations receive their VAT certificates within

30 working days. It is directly sent to their online VAT accounts or by post if registered offline

through an agent.

1.4 Information required to considered for business documentation of VAT registered business

There is type of information is required to considers while filing registration for business.

HMRC provides information related to registration of VAT.

Form VAT1 for all class of members that contains applicants details provided by HMRC

of (full name, home address, date of birth and National Insurance number (or Tax ID if

the applicant is a foreign national). If assesses provide tax ID that it requires to submit

another three documents as 1 copy of government identification like driving licence and

national identity and 2 copies of correspondence that contains the mane and address, bank

statement is an alternative document in option.

Form VAT2 it is required maintain if business is a partnership form

Form VAT50 and VAT51 if b

Form VAT5L Applies if the business activities involve land and property

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Form VAT1614A Applies if assesses seeking to opt to tax land or property and can do so

without permission

Form VAT1614H Only applies if assesses chose to tax land or property but require

HMRC permission

Form VAT68 Applies if client's answered ‘Yes'

1.5 Requirements and the frequency of reporting for VAT schemes

Annual accounting: In this scheme advance VAT payments are required for bill

payments and according to last returns. Submission of 1 VAT return a year (Delgado, Lago‐

Peñas and Mayor, 2015). Though the Standard VAT Accounting Scheme expects organizations

to submit VAT returns on a quarterly premise, the Annual Scheme gives organizations a chance

to make propelled instalments towards their VAT bill and submit one VAT Return every year.

Cash accounting: This is commonly utilized by littler organizations which don't make

buys using a loan and regularly get late instalments. This scheme pursues the standards of money

accounting and in this manner considers the date instalments are made, instead of the date a

receipt is issued.

Flat-rate scheme: A flat rate is used to cover the expenses of business in effective

manner. For business with a turnover under £150,000 (excluding VAT), it is conceivable to pay a

settled rate of VAT to HMRC, at that point keep any VAT charged to clients.

Standard scheme: Under the VAT Standard Accounting Scheme, organizations present

a VAT Return four times each year. Any VAT you owe must be paid quarterly. The amount

VAT assesses should pay or be discounted is determined by looking at the measure of VAT due

on your expenses and the measure of VAT owed on client's sales. Correspondingly, any VAT

discounts that are expected will also be reimbursed quarterly. On the off chance that the sum for

deals is higher than the sum for costs, you should pay HMRC the distinction. In the event that

your expenses are higher than your business, HMRC will discount you the distinction.

1.6 Up to date knowledge of changes to codes of practice, regulation or legislation

Changes and variations in government policies and tax rates are the part of economy.

These changes affect the formation of managing the accounting records effectively and

efficiently. There are following data required to maintain up to date such as;

Statistical records

Software programs

3

without permission

Form VAT1614H Only applies if assesses chose to tax land or property but require

HMRC permission

Form VAT68 Applies if client's answered ‘Yes'

1.5 Requirements and the frequency of reporting for VAT schemes

Annual accounting: In this scheme advance VAT payments are required for bill

payments and according to last returns. Submission of 1 VAT return a year (Delgado, Lago‐

Peñas and Mayor, 2015). Though the Standard VAT Accounting Scheme expects organizations

to submit VAT returns on a quarterly premise, the Annual Scheme gives organizations a chance

to make propelled instalments towards their VAT bill and submit one VAT Return every year.

Cash accounting: This is commonly utilized by littler organizations which don't make

buys using a loan and regularly get late instalments. This scheme pursues the standards of money

accounting and in this manner considers the date instalments are made, instead of the date a

receipt is issued.

Flat-rate scheme: A flat rate is used to cover the expenses of business in effective

manner. For business with a turnover under £150,000 (excluding VAT), it is conceivable to pay a

settled rate of VAT to HMRC, at that point keep any VAT charged to clients.

Standard scheme: Under the VAT Standard Accounting Scheme, organizations present

a VAT Return four times each year. Any VAT you owe must be paid quarterly. The amount

VAT assesses should pay or be discounted is determined by looking at the measure of VAT due

on your expenses and the measure of VAT owed on client's sales. Correspondingly, any VAT

discounts that are expected will also be reimbursed quarterly. On the off chance that the sum for

deals is higher than the sum for costs, you should pay HMRC the distinction. In the event that

your expenses are higher than your business, HMRC will discount you the distinction.

1.6 Up to date knowledge of changes to codes of practice, regulation or legislation

Changes and variations in government policies and tax rates are the part of economy.

These changes affect the formation of managing the accounting records effectively and

efficiently. There are following data required to maintain up to date such as;

Statistical records

Software programs

3

Books of accounts (Invoice, sales, purchase, credit notes)

Records of past returns and rebates, concession certificates

For instance, Government of UK published guidelines on forthcoming changes to digital

record keeping and VAT return requirement (Keen, 2013). As per the guidelines the

organisations have turnover less than £85000. HMRC authorises the VAT returns from agent that

allows a period of time. Organisation is required to retain some records as C79 and VAT

certificates.

TASK 2

2.1 relevant data for a specific period form the accounting system

2.2 Calculation of input and outputs using the VAT classification

Standard rated supplies

4

Records of past returns and rebates, concession certificates

For instance, Government of UK published guidelines on forthcoming changes to digital

record keeping and VAT return requirement (Keen, 2013). As per the guidelines the

organisations have turnover less than £85000. HMRC authorises the VAT returns from agent that

allows a period of time. Organisation is required to retain some records as C79 and VAT

certificates.

TASK 2

2.1 relevant data for a specific period form the accounting system

2.2 Calculation of input and outputs using the VAT classification

Standard rated supplies

4

Since Cathy plans to start a profitable venture for training inclusive of standard rated

sales for VAT , she will be required to register for VAT as she is making taxable supplies.

Standard rated supplies, as the name suggests, are those items prescribed under the law that have

a general applicable rate of 20% applicable on them. Output and Input VAT have been calculated

below:

Output VAT = 80,000 x 20%= £16,000

£16,000 per month will be due as Output VAT

Input VAT = 15,000 x 20/120= £2,500

£2,500 per month will be recoverable.

Zero-rated supplies

If Cathy plans to start a profitable venture for transport inclusive of zero-rated sales for

VAT , she will be able to apply for exemption from registration for VAT since such supplies

have a nil percent rate applicable on them. However, she should still register as these are taxable

supplies. Output and Input VAT have been calculated below:

Output VAT will not be due in this case.

Input VAT of £2,500 per month will be recoverable.

Exempt supplies

Cathy will not be required or permitted to register for VAT as she will not be making

taxable supplies.

No Output VAT will be due.

No Input VAT will be recoverable.

Calculation of of input and output VAT on exports and imports:

Rule: When a VAT registered business imports goods into the UK from outside the European

Union, then VAT has to be paid at the time of importation. However, this VAT can be reclaimed

as input VAT on the VAT return for the period during which the goods were imported.

If Yung Ltd. Chooses to purchase goods worth £1,000 from a UK supplier, standard rate of 20%

shall be applicable. On the other hand, if Yung Ld. chooses to purchase the goods from a

supplier outside the European Union, it can postpone the payment of VAT on importation by

setting up an account with HM Revenue & Customs. It is necessary to provide a bank guarantee,

but VAT is then accounted for on a monthly basis. When a UK VAT registered business exports

goods outside of the European Union then the supply is zero-rated.

5

sales for VAT , she will be required to register for VAT as she is making taxable supplies.

Standard rated supplies, as the name suggests, are those items prescribed under the law that have

a general applicable rate of 20% applicable on them. Output and Input VAT have been calculated

below:

Output VAT = 80,000 x 20%= £16,000

£16,000 per month will be due as Output VAT

Input VAT = 15,000 x 20/120= £2,500

£2,500 per month will be recoverable.

Zero-rated supplies

If Cathy plans to start a profitable venture for transport inclusive of zero-rated sales for

VAT , she will be able to apply for exemption from registration for VAT since such supplies

have a nil percent rate applicable on them. However, she should still register as these are taxable

supplies. Output and Input VAT have been calculated below:

Output VAT will not be due in this case.

Input VAT of £2,500 per month will be recoverable.

Exempt supplies

Cathy will not be required or permitted to register for VAT as she will not be making

taxable supplies.

No Output VAT will be due.

No Input VAT will be recoverable.

Calculation of of input and output VAT on exports and imports:

Rule: When a VAT registered business imports goods into the UK from outside the European

Union, then VAT has to be paid at the time of importation. However, this VAT can be reclaimed

as input VAT on the VAT return for the period during which the goods were imported.

If Yung Ltd. Chooses to purchase goods worth £1,000 from a UK supplier, standard rate of 20%

shall be applicable. On the other hand, if Yung Ld. chooses to purchase the goods from a

supplier outside the European Union, it can postpone the payment of VAT on importation by

setting up an account with HM Revenue & Customs. It is necessary to provide a bank guarantee,

but VAT is then accounted for on a monthly basis. When a UK VAT registered business exports

goods outside of the European Union then the supply is zero-rated.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3 Calculation of the VAT due to, or form the relevant tax authority

Standard Supplies:

VAT shall be calculated at the general applicable rate of 20%. Cathy will be liable to pay

£16,000 as her Output VAT return for quarterly basis to HMRC and entitled to receive reclaim

on Input VAT return of £2,500.

Zero-Rated Supplies:

As Zero-Rated supplies have zero percent of VAT rate applicable on them, Cathy will not

be liable to pay any tax to HMRC as his VAT return for the year (Kenyon, Langley and

Paquin2012). However, she will entitled to receive reclaim on Input VAT return of £2,500.

Exempt Supplies:

Exempt supplies are tax-exempted from VAT. These may include supplies such as

ambulance, in such case, Cathy will not be liable to pay nor permitted to pay any tax to HMRC

as his VAT return for the year.

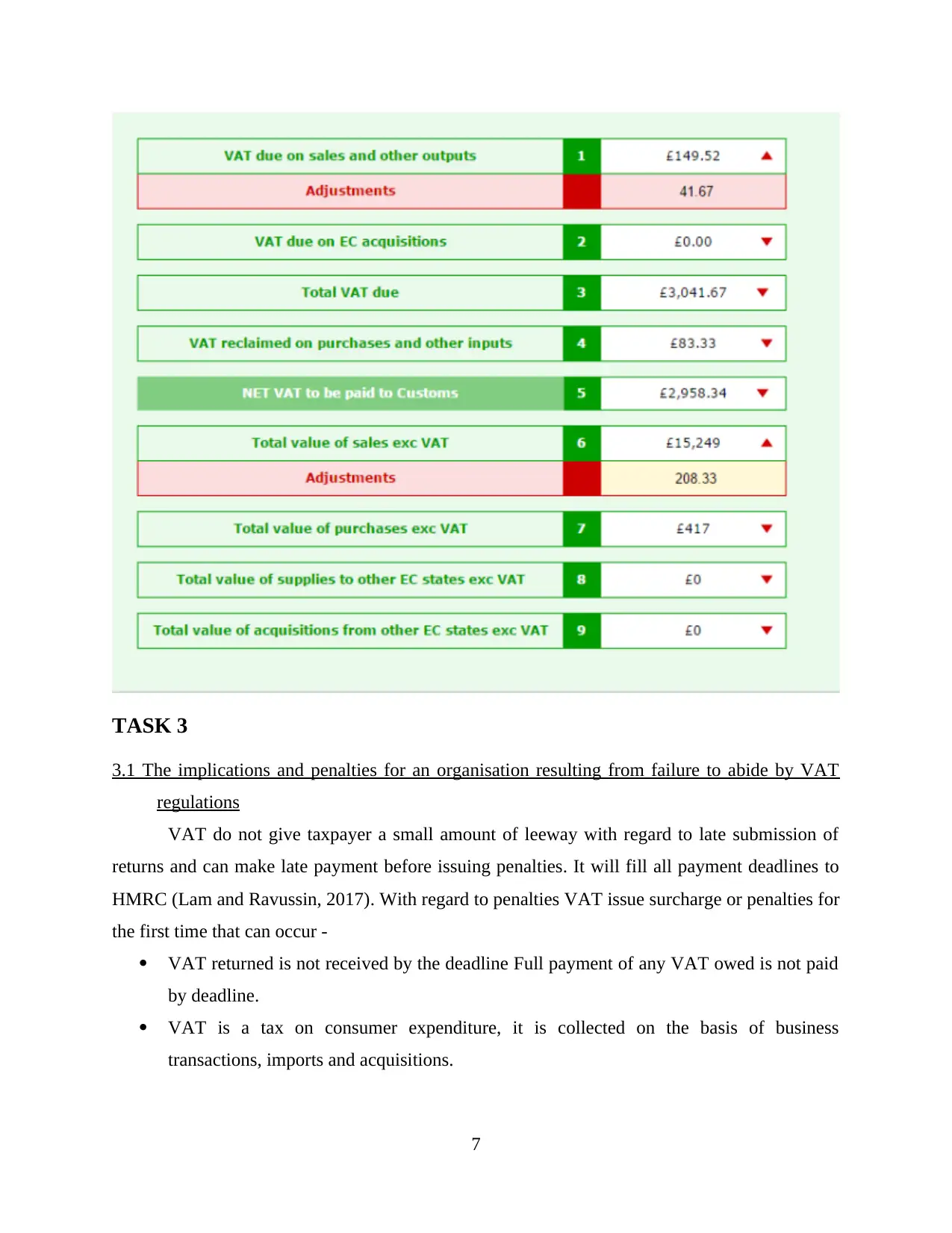

2.4 VAT return and associated payment with in the statutory time limits

A VAT return of Rollin traders Ltd is submitted below form the assessment year ended

31st December 2018.

6

Standard Supplies:

VAT shall be calculated at the general applicable rate of 20%. Cathy will be liable to pay

£16,000 as her Output VAT return for quarterly basis to HMRC and entitled to receive reclaim

on Input VAT return of £2,500.

Zero-Rated Supplies:

As Zero-Rated supplies have zero percent of VAT rate applicable on them, Cathy will not

be liable to pay any tax to HMRC as his VAT return for the year (Kenyon, Langley and

Paquin2012). However, she will entitled to receive reclaim on Input VAT return of £2,500.

Exempt Supplies:

Exempt supplies are tax-exempted from VAT. These may include supplies such as

ambulance, in such case, Cathy will not be liable to pay nor permitted to pay any tax to HMRC

as his VAT return for the year.

2.4 VAT return and associated payment with in the statutory time limits

A VAT return of Rollin traders Ltd is submitted below form the assessment year ended

31st December 2018.

6

TASK 3

3.1 The implications and penalties for an organisation resulting from failure to abide by VAT

regulations

VAT do not give taxpayer a small amount of leeway with regard to late submission of

returns and can make late payment before issuing penalties. It will fill all payment deadlines to

HMRC (Lam and Ravussin, 2017). With regard to penalties VAT issue surcharge or penalties for

the first time that can occur -

VAT returned is not received by the deadline Full payment of any VAT owed is not paid

by deadline.

VAT is a tax on consumer expenditure, it is collected on the basis of business

transactions, imports and acquisitions.

7

3.1 The implications and penalties for an organisation resulting from failure to abide by VAT

regulations

VAT do not give taxpayer a small amount of leeway with regard to late submission of

returns and can make late payment before issuing penalties. It will fill all payment deadlines to

HMRC (Lam and Ravussin, 2017). With regard to penalties VAT issue surcharge or penalties for

the first time that can occur -

VAT returned is not received by the deadline Full payment of any VAT owed is not paid

by deadline.

VAT is a tax on consumer expenditure, it is collected on the basis of business

transactions, imports and acquisitions.

7

The implication to regulate any organization by failing to meet all state and federal

guidelines for compliance that can results in serious consequence for businesses. Penalties for

late payments are as follows;

Penalty of £100 naturally collected by the tax department.

If tax arises for association firms, £100 penalty is collected on each member as opposed

to organization firm in respect of all members. Just the delegate partner can request under

some random condition instead of individual partner.

Per day fine of £10 for 90 days will be required if the association can't record data and

file returns with tax authorities with in 3 months. In case of a half year slip by from date

of documenting return, an extra 5% of expense due or £300, whichever higher will be

charged which will add up to another 5% collect or £300, whichever is higher.

3.2 Adjustments and declarations for any errors or omission identified in previous VAT periods

VAT notice 700/45 provides guidelines regarding amendments and changes regarding

errors and adjustments. How to correct VAT errors and make adjustment or claims.

VAT errors on a return already submitted

Inadequate or errors subject to return periods beginning on or after 1st April 2008 where

the due date of the return is on or after 1st April 2009 will be responsible to a penalty if

careless or deliberate (Schenk, Thuronyi and Cui, 2015).

If assesses analyse a error than HMRC take steps to amend that properly. If it is found

that the errors are done intentionally than penalty will be levied to assesses.

Adjustments of errors

According to section 4 guidelines regarding Errors Regime, 2009 of The VAT Act, 1994,

for penalties, modifications must be made subsequent to registering the net estimation of

mistakes. The balanced sum can be incorporated into the present VAT giving in following cases:

In the event that the net value does not surpass £10,000 or

If the net value falls between the range of £10,000 and £50,000 yet does not surpass 1%

of net yields referenced in VAT return presentation for the period in which the mistake is found,

If net estimation of errors does not meet the above criteria or is ordered as a conscious

mistake, a different shape VAT652 must be filled and submitted to HMRC with subtleties

including:

Reasons adding up to reason for such errors

8

guidelines for compliance that can results in serious consequence for businesses. Penalties for

late payments are as follows;

Penalty of £100 naturally collected by the tax department.

If tax arises for association firms, £100 penalty is collected on each member as opposed

to organization firm in respect of all members. Just the delegate partner can request under

some random condition instead of individual partner.

Per day fine of £10 for 90 days will be required if the association can't record data and

file returns with tax authorities with in 3 months. In case of a half year slip by from date

of documenting return, an extra 5% of expense due or £300, whichever higher will be

charged which will add up to another 5% collect or £300, whichever is higher.

3.2 Adjustments and declarations for any errors or omission identified in previous VAT periods

VAT notice 700/45 provides guidelines regarding amendments and changes regarding

errors and adjustments. How to correct VAT errors and make adjustment or claims.

VAT errors on a return already submitted

Inadequate or errors subject to return periods beginning on or after 1st April 2008 where

the due date of the return is on or after 1st April 2009 will be responsible to a penalty if

careless or deliberate (Schenk, Thuronyi and Cui, 2015).

If assesses analyse a error than HMRC take steps to amend that properly. If it is found

that the errors are done intentionally than penalty will be levied to assesses.

Adjustments of errors

According to section 4 guidelines regarding Errors Regime, 2009 of The VAT Act, 1994,

for penalties, modifications must be made subsequent to registering the net estimation of

mistakes. The balanced sum can be incorporated into the present VAT giving in following cases:

In the event that the net value does not surpass £10,000 or

If the net value falls between the range of £10,000 and £50,000 yet does not surpass 1%

of net yields referenced in VAT return presentation for the period in which the mistake is found,

If net estimation of errors does not meet the above criteria or is ordered as a conscious

mistake, a different shape VAT652 must be filled and submitted to HMRC with subtleties

including:

Reasons adding up to reason for such errors

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting time of disclosure of mistake

Kind of mistake - information or yield

Net Value of Errors-both under-pronounced and over-announced sums

Calculation summary for figuring Net Value

In the event that the errors have brought about extra instalments to charge experts

Aggregate sum to be balanced

Subject to case the net value of errors have nil or negligible impact on the net VAT due

on returns both of the above strategies can be utilized to redress the mistakes. The association

must tell HMRC about any sort of intentional blunder made on the association's part.

TASK 4

4.1 Inform the managers of the impact that the VAT payment may have organisations cash flow

VAT has tremendous impact on association's cash streams similarly with respect to future

foreseeing. These movements have influence on each and every cash related record over an

affiliation which over the long haul impact the VAT control account kept up by selected

associations (Schneider, 2012). However,VAT rates change as time passes by to hold its effect

and capability. It completely depends on the appraisal aggregate, if payable cost is high than net

cash streams available for the association is low and the a different way.

Every association requires to take care of records, import or admission report,

arrangements and purchase sales. For instance, due to advance in VAT rate from 20% to 25%, if

an association needs to settle administrative cost £30,000 as opposed to £15,000 it will direct

effect the net advantage of the association which is adequate to chop any relationship down.

Impact of VAT has serious impact on cash flows. High obligation regard isn't beneficial for the

business, so it is basic perspective in the relationship for thought.

In view of changes in VAT portion, forecast of budget will also change. For example,

Raintree limited is making strategies for the future and the standard evaluation rate changes to

27%, the company should take off proper enhancements in systems as shown by new obligation

rates. So it is totally depend on the evaluation rates which can be change at whatever point.

9

Kind of mistake - information or yield

Net Value of Errors-both under-pronounced and over-announced sums

Calculation summary for figuring Net Value

In the event that the errors have brought about extra instalments to charge experts

Aggregate sum to be balanced

Subject to case the net value of errors have nil or negligible impact on the net VAT due

on returns both of the above strategies can be utilized to redress the mistakes. The association

must tell HMRC about any sort of intentional blunder made on the association's part.

TASK 4

4.1 Inform the managers of the impact that the VAT payment may have organisations cash flow

VAT has tremendous impact on association's cash streams similarly with respect to future

foreseeing. These movements have influence on each and every cash related record over an

affiliation which over the long haul impact the VAT control account kept up by selected

associations (Schneider, 2012). However,VAT rates change as time passes by to hold its effect

and capability. It completely depends on the appraisal aggregate, if payable cost is high than net

cash streams available for the association is low and the a different way.

Every association requires to take care of records, import or admission report,

arrangements and purchase sales. For instance, due to advance in VAT rate from 20% to 25%, if

an association needs to settle administrative cost £30,000 as opposed to £15,000 it will direct

effect the net advantage of the association which is adequate to chop any relationship down.

Impact of VAT has serious impact on cash flows. High obligation regard isn't beneficial for the

business, so it is basic perspective in the relationship for thought.

In view of changes in VAT portion, forecast of budget will also change. For example,

Raintree limited is making strategies for the future and the standard evaluation rate changes to

27%, the company should take off proper enhancements in systems as shown by new obligation

rates. So it is totally depend on the evaluation rates which can be change at whatever point.

9

In this manner, it is a direction for the overseers to guarantee managers kept careful about

these changes. This would ensure versatility for relationship to get these movements so business

can persevere in longer run.

4.2 VAT legislation which would have an effect on an organization's recording systems

Changes in the VAT enactment will impact the hierarchical account framework, for

example, making charge advanced or expelling disconnected structures for VAT enlistment.

Thus, an organization needs to keep up their records in the advanced frame and refreshed. There

are a few difficulties looked by the association and different guides (Weber, 2013). These are

enrolled beneath:

Changes in record keeping framework: - For agreeing to digitalisation, organization

needs to set up their record on spreadsheet or programming which is specifically connected with

the HMRC with the assistance of Application Programming Interface (API).

Timing: - Making charge computerized in regard of VAT will be trailed by most of

organizations from first April 2019. since programming preliminary is as of late open for

citizens.

Changes in VAT return accommodation: - VAT return is submitted to HMRC through

API and information is recorded by the product in the advanced shape (Li and Whalley, 2012).

Manual information recording in HMRC has halted in the wake of propelling of making charge

advanced (MTD).

CONCLUSION

The report summarises the requirements and tax legislations formed in UK. VAT

legislations rules and formations are indicating towards lawful consideration to government. The

ways of maintaining the documents and records helps to file VAT return. With implementation

of legislations and rules VAT returns are filed accurately with in organisation. Consequence of

filing late return or no return lead organisation towards payment of penalties and fines discussed

in the above report. In the end, it is summarised that VAT has experienced numerous

progressions since its initiation and suitable consideration. It should be taken while computing

and consenting to certain standards of VAT.

10

these changes. This would ensure versatility for relationship to get these movements so business

can persevere in longer run.

4.2 VAT legislation which would have an effect on an organization's recording systems

Changes in the VAT enactment will impact the hierarchical account framework, for

example, making charge advanced or expelling disconnected structures for VAT enlistment.

Thus, an organization needs to keep up their records in the advanced frame and refreshed. There

are a few difficulties looked by the association and different guides (Weber, 2013). These are

enrolled beneath:

Changes in record keeping framework: - For agreeing to digitalisation, organization

needs to set up their record on spreadsheet or programming which is specifically connected with

the HMRC with the assistance of Application Programming Interface (API).

Timing: - Making charge computerized in regard of VAT will be trailed by most of

organizations from first April 2019. since programming preliminary is as of late open for

citizens.

Changes in VAT return accommodation: - VAT return is submitted to HMRC through

API and information is recorded by the product in the advanced shape (Li and Whalley, 2012).

Manual information recording in HMRC has halted in the wake of propelling of making charge

advanced (MTD).

CONCLUSION

The report summarises the requirements and tax legislations formed in UK. VAT

legislations rules and formations are indicating towards lawful consideration to government. The

ways of maintaining the documents and records helps to file VAT return. With implementation

of legislations and rules VAT returns are filed accurately with in organisation. Consequence of

filing late return or no return lead organisation towards payment of penalties and fines discussed

in the above report. In the end, it is summarised that VAT has experienced numerous

progressions since its initiation and suitable consideration. It should be taken while computing

and consenting to certain standards of VAT.

10

REFERENCES

Books and Journals:

Albayrak, Ö., 2017. Redistributive Effects of Indirect Taxes in Turkey 2003. Ankara Üniversitesi

Sosyal Bilimler Dergisi. 2(1).

Bahl, R., 2018. The Guatemalan tax reform. Routledge.

Delgado, F. J., Lago‐Peñas, S. and Mayor, M., 2015. On the determinants of local tax rates: new

evidence from Spain. Contemporary Economic Policy. 33(2). pp.351-368.

Keen, M. M., 2013. Targeting, cascading, and indirect tax desig (No. 13-57). International

Monetary Fund.

Kenyon, D. A., Langley, A. H. and Paquin, B. P., 2012. Rethinking property tax incentives for

business. Cambridge, MA: Lincoln Institute of Land Policy.

Lam, Y. Y. and Ravussin, E., 2017. Indirect calorimetry: an indispensable tool to understand and

predict obesity. European journal of clinical nutrition. 71(3). p.318.

Li, C. and Whalley, J., 2012. Indirect tax initiatives and global rebalancing (No. w17919).

National Bureau of Economic Research.

Littlewood, J., Murphy, R. J. and Wang, L., 2013. Importance of policy support and feedstock

prices on economic feasibility of bioethanol production from wheat straw in the

UK. Renewable and Sustainable Energy Reviews. 17. pp.291-300.

Schenk, A., Thuronyi, V. and Cui, W., 2015. Value added tax. Cambridge University Press.

Schneider, A., 2012. State-building and tax regimes in Central America. Cambridge University

Press.

Weber, D., 2013. Abuse of Law in European Tax Law: An Overview and Some Recent Trends

in the Direct and Indirect Tax Case Law of the ECJ-part 1. European Taxation. 53(6).

pp.251-264.

Williams, C. and Martinez, A., 2014. Do small business start-ups test-trade in the informal

economy? Evidence from a UK survey. International Journal of Entrepreneurship and

Small Business. 22(1).

11

Books and Journals:

Albayrak, Ö., 2017. Redistributive Effects of Indirect Taxes in Turkey 2003. Ankara Üniversitesi

Sosyal Bilimler Dergisi. 2(1).

Bahl, R., 2018. The Guatemalan tax reform. Routledge.

Delgado, F. J., Lago‐Peñas, S. and Mayor, M., 2015. On the determinants of local tax rates: new

evidence from Spain. Contemporary Economic Policy. 33(2). pp.351-368.

Keen, M. M., 2013. Targeting, cascading, and indirect tax desig (No. 13-57). International

Monetary Fund.

Kenyon, D. A., Langley, A. H. and Paquin, B. P., 2012. Rethinking property tax incentives for

business. Cambridge, MA: Lincoln Institute of Land Policy.

Lam, Y. Y. and Ravussin, E., 2017. Indirect calorimetry: an indispensable tool to understand and

predict obesity. European journal of clinical nutrition. 71(3). p.318.

Li, C. and Whalley, J., 2012. Indirect tax initiatives and global rebalancing (No. w17919).

National Bureau of Economic Research.

Littlewood, J., Murphy, R. J. and Wang, L., 2013. Importance of policy support and feedstock

prices on economic feasibility of bioethanol production from wheat straw in the

UK. Renewable and Sustainable Energy Reviews. 17. pp.291-300.

Schenk, A., Thuronyi, V. and Cui, W., 2015. Value added tax. Cambridge University Press.

Schneider, A., 2012. State-building and tax regimes in Central America. Cambridge University

Press.

Weber, D., 2013. Abuse of Law in European Tax Law: An Overview and Some Recent Trends

in the Direct and Indirect Tax Case Law of the ECJ-part 1. European Taxation. 53(6).

pp.251-264.

Williams, C. and Martinez, A., 2014. Do small business start-ups test-trade in the informal

economy? Evidence from a UK survey. International Journal of Entrepreneurship and

Small Business. 22(1).

11

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.