Indirect Tax: VAT Regulations, Calculations, and Penalties Report

VerifiedAdded on 2020/12/09

|16

|3925

|483

Report

AI Summary

This report offers a comprehensive examination of Value Added Tax (VAT) regulations, encompassing various aspects such as VAT schemes, calculations of input and output VAT for different classifications (standard, zero-rated, and exempt supplies), and the process of calculating VAT due to or from tax authorities. It explores the implications and penalties for organizations failing to comply with VAT regulations, including adjustments for errors and omissions. The report also delves into the impact of VAT payments on cash flow and financial forecasts, as well as changes in VAT legislation and their effects on organizational recording systems. The analysis includes a review of data extraction from accounting systems, the importance of business documentation, and the various VAT schemes required for reporting purposes. The report aims to provide a clear understanding of VAT's role in indirect taxation and its impact on businesses.

Indirect Tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. 1 Source of information on VAT.............................................................................................1

1.2 an organisation should interact with the relevant government agency..................................1

1 . 4 Information that must be included on business documentation of VAT registered

businesses.....................................................................................................................................2

1 .5 VAT schemes required for reporting purposes.....................................................................2

1 . 6 Be aware about relevant changes of legislation and codes of practices..............................3

TASK 2 ...........................................................................................................................................4

2 . 1 Extraction of Data from the accounting system...................................................................4

2 . 2 Calculation of input and output for various VAT classifications........................................5

2 . 3 Calculating VAT due to/from the relevant tax authority.....................................................8

2 . 4 Submission of VAT return & associated payment under statutory time limits ..................8

TASK 3............................................................................................................................................8

3.1 Implications and Penalties for an organisation resulting from failure to abide by VAT

regulations....................................................................................................................................8

3.2 Adjustments and Declarations for any errors or omissions identified in previous VAT

periods..........................................................................................................................................9

TASK 4 .........................................................................................................................................10

4 . 1 Impact that the VAT payment may have on an organisation’s cash flow and financial

forecasts.....................................................................................................................................10

4 . 2 Changes in VAT legislation which would have an effect on an organisation’s recording

systems ......................................................................................................................................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. 1 Source of information on VAT.............................................................................................1

1.2 an organisation should interact with the relevant government agency..................................1

1 . 4 Information that must be included on business documentation of VAT registered

businesses.....................................................................................................................................2

1 .5 VAT schemes required for reporting purposes.....................................................................2

1 . 6 Be aware about relevant changes of legislation and codes of practices..............................3

TASK 2 ...........................................................................................................................................4

2 . 1 Extraction of Data from the accounting system...................................................................4

2 . 2 Calculation of input and output for various VAT classifications........................................5

2 . 3 Calculating VAT due to/from the relevant tax authority.....................................................8

2 . 4 Submission of VAT return & associated payment under statutory time limits ..................8

TASK 3............................................................................................................................................8

3.1 Implications and Penalties for an organisation resulting from failure to abide by VAT

regulations....................................................................................................................................8

3.2 Adjustments and Declarations for any errors or omissions identified in previous VAT

periods..........................................................................................................................................9

TASK 4 .........................................................................................................................................10

4 . 1 Impact that the VAT payment may have on an organisation’s cash flow and financial

forecasts.....................................................................................................................................10

4 . 2 Changes in VAT legislation which would have an effect on an organisation’s recording

systems ......................................................................................................................................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Similar to direct taxation, indirect taxation is a charge on goods and services produced

and sold within a country for a given accounting period. There are many types of indirect taxes

present globally. One such type of tax is Value Added Tax (VAT). This project report aims to

provide an understanding of VAT regulations, calculations of returns, penalties and their

implications as well as treatment of errors and adjustment made thereof. It also analyses the key

changes in VAT legislation in recent years and their impact on organizations and there cash

flows, financial forecasts as well as recording systems. Input and output for VAT classifications

are also mentioned and the impact of the VAT payment on corporation's cash flow has also

discussed in the report.

TASK 1

1. 1 Source of information on VAT

VAT is known to be the Value Added Tax that is applied on services and goods with

their value added on each production steps initiating from manufacturing to sales. It is a

consumption tax and VAT amount is paid by taxable people which is computed by subtracting

those inputs that are utilise for goods and services production from products cost. Even so, VAT

is not relevant for every cities and few places are exempt from this kind of tax.

Some important data can be available in the sites of federal government. Other

information sources can be acquirable from the portal of HMRC which is accountable for

collecting tax in all over United Kingdom. Whole applicable information about tax or another

problems for tax payable is related by HM revenue and cost also facilitates solution for tax

payer.

1.2 an organisation should interact with the relevant government agency

While registering the value added tax, company has to obey some essential process.

These methods considered forms of registration that is to be fill up by firm with appropriate

information. At the time of registration methods, applicants have to tackle some problems that

are resolved through the agencies of government. There are various kinds of registration form

which are available as per the business types. For clarifying those problems agencies of

government facilitates some assistance to organisation.

1. 3 VAT registration requirements

1

Similar to direct taxation, indirect taxation is a charge on goods and services produced

and sold within a country for a given accounting period. There are many types of indirect taxes

present globally. One such type of tax is Value Added Tax (VAT). This project report aims to

provide an understanding of VAT regulations, calculations of returns, penalties and their

implications as well as treatment of errors and adjustment made thereof. It also analyses the key

changes in VAT legislation in recent years and their impact on organizations and there cash

flows, financial forecasts as well as recording systems. Input and output for VAT classifications

are also mentioned and the impact of the VAT payment on corporation's cash flow has also

discussed in the report.

TASK 1

1. 1 Source of information on VAT

VAT is known to be the Value Added Tax that is applied on services and goods with

their value added on each production steps initiating from manufacturing to sales. It is a

consumption tax and VAT amount is paid by taxable people which is computed by subtracting

those inputs that are utilise for goods and services production from products cost. Even so, VAT

is not relevant for every cities and few places are exempt from this kind of tax.

Some important data can be available in the sites of federal government. Other

information sources can be acquirable from the portal of HMRC which is accountable for

collecting tax in all over United Kingdom. Whole applicable information about tax or another

problems for tax payable is related by HM revenue and cost also facilitates solution for tax

payer.

1.2 an organisation should interact with the relevant government agency

While registering the value added tax, company has to obey some essential process.

These methods considered forms of registration that is to be fill up by firm with appropriate

information. At the time of registration methods, applicants have to tackle some problems that

are resolved through the agencies of government. There are various kinds of registration form

which are available as per the business types. For clarifying those problems agencies of

government facilitates some assistance to organisation.

1. 3 VAT registration requirements

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is necessary for those company to apply for the VAT registration which are having tax

turnover approx £85,000 or more than that. It consider every items which are sold by

organisation and there is not any exemption of Value added tax excluding other than given. VAT

registration is done by filling up online and offline form. Mainly business entities like those

firms who prefer online registrations or partnership company. After completing the registration

process, an online account of VAT is opened by authorities of tax in name of taxable individual.

Firm also can register by the agents for facilitating required information such as returns of VAT.

After this company obtain its VAT number from HMRC.

Also organisation can register themselves by filling the offline registration form like form

VAT1A which is facilitated for distance sellers, for importers form VAT1B I as well as VAT1C

when firm want to sell its assets. After completing the registration of VAT company get their

certificates of VAT under 30 working days. This is sent on its online accounts of VAT or

through post in case of offline registration.

1 . 4 Information that must be included on business documentation of VAT registered businesses

This is important rule within all company is to manage records of business in excel or

word format. So, firms complete this responsibility properly as recorded data of transactions can

available to follow with registration as well as documentation of VAT system requirement. The

business that is registered through VAT are required to consider following accounts and data for

due compliance:

Company required to keep the records because of HMRC Requirements like annual

accounts, invoices, credit or debit notes, VAT accounts, bank statements and so on.

Special VAT records: Usually there are two kinds of records that are to be maintained by

company. First one is about accounts of VAT and invoices of VAT is second. The

account of VAT consider regular records of business and invoices of VAT is for

suppliers. In this invoice is consider as a terminology. This only includes information that

is appropriate for the rules of VAT.

1 .5 VAT schemes required for reporting purposes

Cash accounting scheme: generally the amount of differences among purchase invoices

and sales invoices is a net value that is paid to HM revenue and cost as the returns of

VAT. So, within this scheme VAT should be payable at selling time and reclaimed when

2

turnover approx £85,000 or more than that. It consider every items which are sold by

organisation and there is not any exemption of Value added tax excluding other than given. VAT

registration is done by filling up online and offline form. Mainly business entities like those

firms who prefer online registrations or partnership company. After completing the registration

process, an online account of VAT is opened by authorities of tax in name of taxable individual.

Firm also can register by the agents for facilitating required information such as returns of VAT.

After this company obtain its VAT number from HMRC.

Also organisation can register themselves by filling the offline registration form like form

VAT1A which is facilitated for distance sellers, for importers form VAT1B I as well as VAT1C

when firm want to sell its assets. After completing the registration of VAT company get their

certificates of VAT under 30 working days. This is sent on its online accounts of VAT or

through post in case of offline registration.

1 . 4 Information that must be included on business documentation of VAT registered businesses

This is important rule within all company is to manage records of business in excel or

word format. So, firms complete this responsibility properly as recorded data of transactions can

available to follow with registration as well as documentation of VAT system requirement. The

business that is registered through VAT are required to consider following accounts and data for

due compliance:

Company required to keep the records because of HMRC Requirements like annual

accounts, invoices, credit or debit notes, VAT accounts, bank statements and so on.

Special VAT records: Usually there are two kinds of records that are to be maintained by

company. First one is about accounts of VAT and invoices of VAT is second. The

account of VAT consider regular records of business and invoices of VAT is for

suppliers. In this invoice is consider as a terminology. This only includes information that

is appropriate for the rules of VAT.

1 .5 VAT schemes required for reporting purposes

Cash accounting scheme: generally the amount of differences among purchase invoices

and sales invoices is a net value that is paid to HM revenue and cost as the returns of

VAT. So, within this scheme VAT should be payable at selling time and reclaimed when

2

payment is done to suppliers by sellers. In order to be an suitable tax payer under the

scheme of VAT, turnover of VAT taxable should not more than £1.35 million.

Annual accounting scheme: this is the scheme that facilitates facilities to company in

order to pay their tax annually. According to this schemes, taxable individuals can file

their returns of VAT only one time within whole year rather than quarterly.

Flat rate scheme: it is mainly formed for records explanation like transactions of purchase

as well as sales. This permit company to utilise flat rates or fixed percentage rate on the

turnover of firm in order to compute VAT due. The fixed rate percentage scheme based

on business types and size. Difference among paid amount and charged amount is kept

with company as its income. VAT reclaimed is not for purchases and exclude definite

capital assets that is more than £2,000 so that it can be consider as eligible tax payable

under this scheme. Also VAT taxable turnover should not be more than £150,000.

Standard scheme:

under this method company pays the returns of VAT quarterly during accounting period. In case

if any amount is remaining then that is also paid quarterly. When any firm have sales amount

which exceeds cost of product then differentiation of that amount is to be payable to HMRC.

1 . 6 Be aware about relevant changes of legislation and codes of practices

All company required to know about the best practices codes as well as legislation for

effectual work. Some are explained below:

Firm should has appropriate knowledge regarding how statistics can be made.

Reducing their information or records.

Data protection through computer software.

Awareness about information of governing body.

There are few essential legislation that is utilise by these information. At the time when

organisation is not sure regarding how legal things affects the company than it has to consult to

some legal people.

Copyright and intellectual property

Personal information

Responsibility

Re-utilisation and sharing of information.

3

scheme of VAT, turnover of VAT taxable should not more than £1.35 million.

Annual accounting scheme: this is the scheme that facilitates facilities to company in

order to pay their tax annually. According to this schemes, taxable individuals can file

their returns of VAT only one time within whole year rather than quarterly.

Flat rate scheme: it is mainly formed for records explanation like transactions of purchase

as well as sales. This permit company to utilise flat rates or fixed percentage rate on the

turnover of firm in order to compute VAT due. The fixed rate percentage scheme based

on business types and size. Difference among paid amount and charged amount is kept

with company as its income. VAT reclaimed is not for purchases and exclude definite

capital assets that is more than £2,000 so that it can be consider as eligible tax payable

under this scheme. Also VAT taxable turnover should not be more than £150,000.

Standard scheme:

under this method company pays the returns of VAT quarterly during accounting period. In case

if any amount is remaining then that is also paid quarterly. When any firm have sales amount

which exceeds cost of product then differentiation of that amount is to be payable to HMRC.

1 . 6 Be aware about relevant changes of legislation and codes of practices

All company required to know about the best practices codes as well as legislation for

effectual work. Some are explained below:

Firm should has appropriate knowledge regarding how statistics can be made.

Reducing their information or records.

Data protection through computer software.

Awareness about information of governing body.

There are few essential legislation that is utilise by these information. At the time when

organisation is not sure regarding how legal things affects the company than it has to consult to

some legal people.

Copyright and intellectual property

Personal information

Responsibility

Re-utilisation and sharing of information.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

2 . 1 Extraction of Data from the accounting system

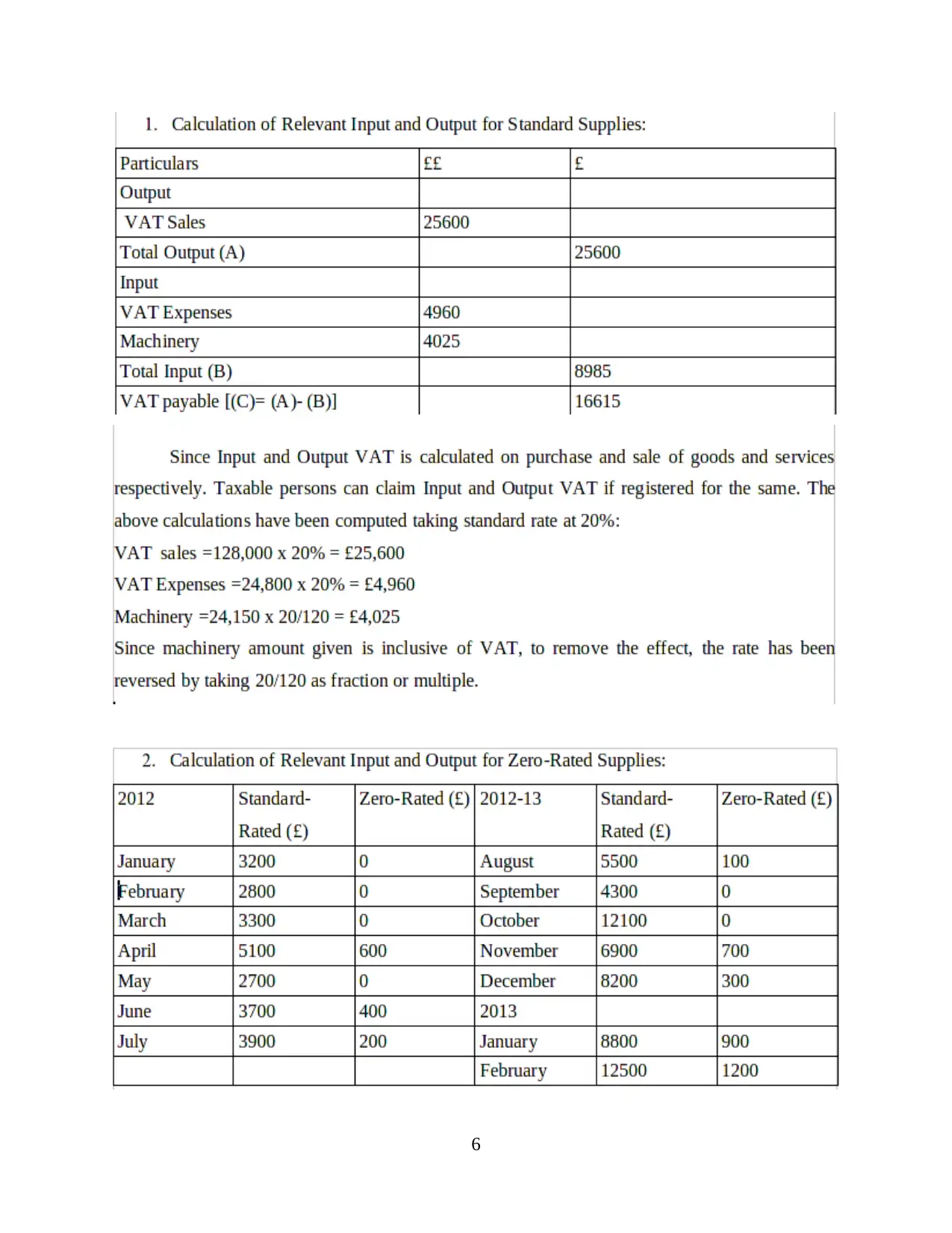

1. Data for calculation of relevant Input and Output for Standard Supplies (year 2012-13):

Zoe is in the process of completing the VAT return for the quarter which is ended 31 March

2013. There are information available which is :

Totalling of sales invoices £128,000 were issued in respect of standard rated sales.

Standard rated expenditures are the amount of £24,800.

On 20 February 2013 Gwen purchased a machinery which is the cost of £24,150. This

figure is inclusive of VAT. Until unless there is any information is given all above figures are

exclusive of VAT.

2.Data for calculation of Relevant Input and Output for Exempt Supplies:

Cathy will commence trading in the near future. She operates a small aeroplane, and is

considering three alternative types of business. These are (1) training, in which case all sales will

be standard rated for VAT, (2) transport, in which case all sales will be zero-rated for VAT, and

(3) an air ambulance service, in which case all sales will be exempt from VAT (Dustmann and

Frattini, 2014).

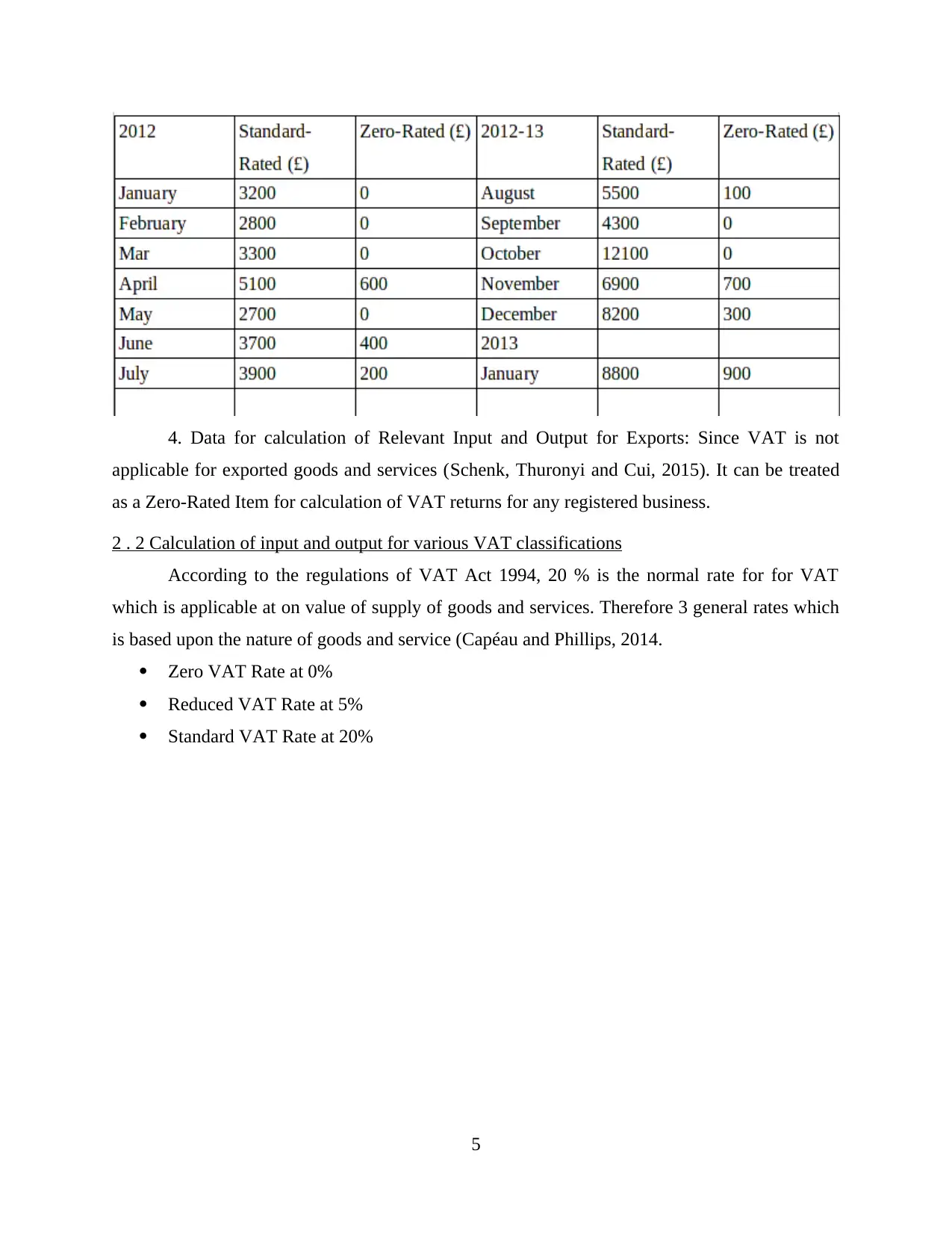

1. Data for calculation of Relevant Input and Output for Zero-Rated Supplies:

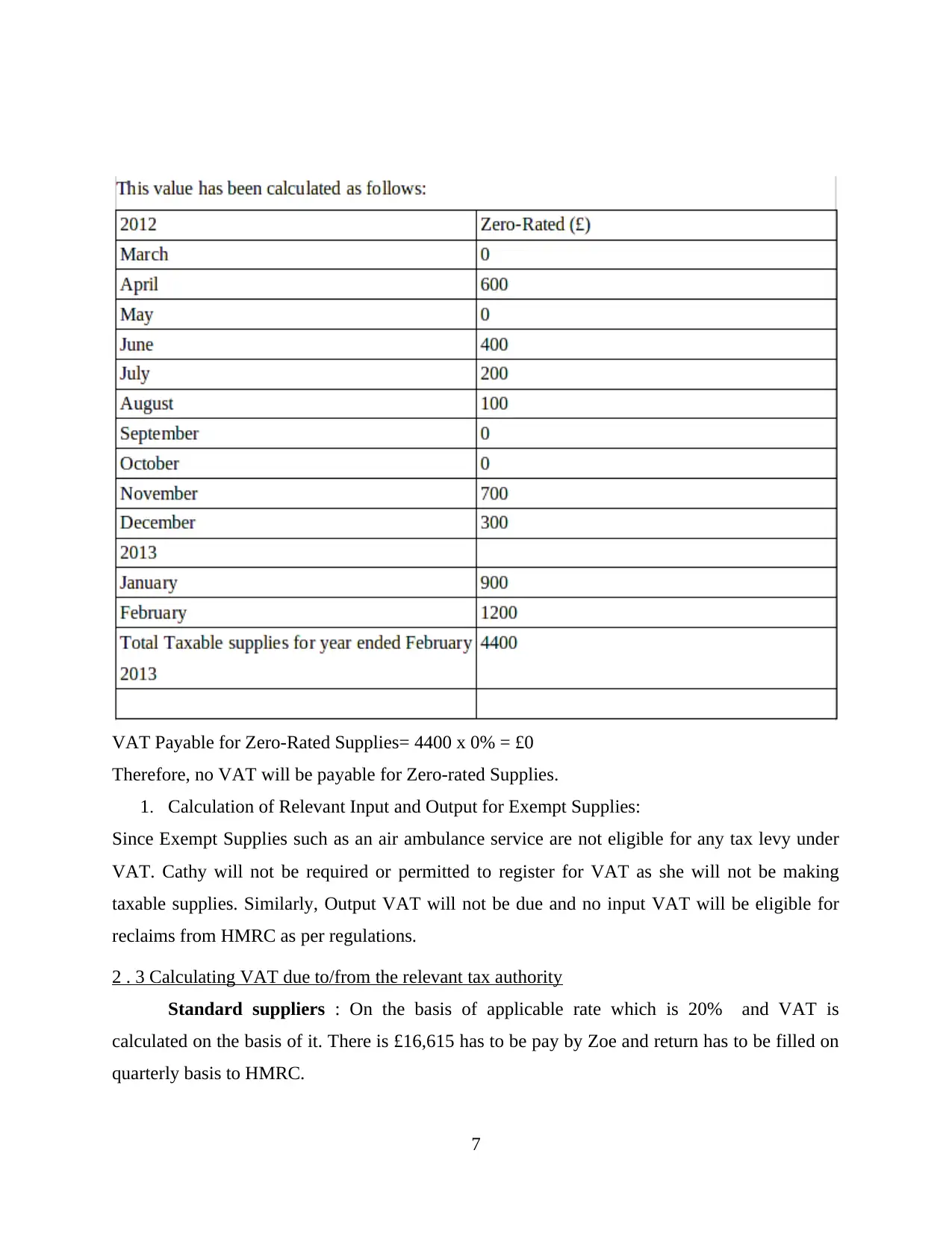

Albert commenced trading on 1 January 2012. His sales have been as follows:

4

2 . 1 Extraction of Data from the accounting system

1. Data for calculation of relevant Input and Output for Standard Supplies (year 2012-13):

Zoe is in the process of completing the VAT return for the quarter which is ended 31 March

2013. There are information available which is :

Totalling of sales invoices £128,000 were issued in respect of standard rated sales.

Standard rated expenditures are the amount of £24,800.

On 20 February 2013 Gwen purchased a machinery which is the cost of £24,150. This

figure is inclusive of VAT. Until unless there is any information is given all above figures are

exclusive of VAT.

2.Data for calculation of Relevant Input and Output for Exempt Supplies:

Cathy will commence trading in the near future. She operates a small aeroplane, and is

considering three alternative types of business. These are (1) training, in which case all sales will

be standard rated for VAT, (2) transport, in which case all sales will be zero-rated for VAT, and

(3) an air ambulance service, in which case all sales will be exempt from VAT (Dustmann and

Frattini, 2014).

1. Data for calculation of Relevant Input and Output for Zero-Rated Supplies:

Albert commenced trading on 1 January 2012. His sales have been as follows:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Data for calculation of Relevant Input and Output for Exports: Since VAT is not

applicable for exported goods and services (Schenk, Thuronyi and Cui, 2015). It can be treated

as a Zero-Rated Item for calculation of VAT returns for any registered business.

2 . 2 Calculation of input and output for various VAT classifications

According to the regulations of VAT Act 1994, 20 % is the normal rate for for VAT

which is applicable at on value of supply of goods and services. Therefore 3 general rates which

is based upon the nature of goods and service (Capéau and Phillips, 2014.

Zero VAT Rate at 0%

Reduced VAT Rate at 5%

Standard VAT Rate at 20%

5

applicable for exported goods and services (Schenk, Thuronyi and Cui, 2015). It can be treated

as a Zero-Rated Item for calculation of VAT returns for any registered business.

2 . 2 Calculation of input and output for various VAT classifications

According to the regulations of VAT Act 1994, 20 % is the normal rate for for VAT

which is applicable at on value of supply of goods and services. Therefore 3 general rates which

is based upon the nature of goods and service (Capéau and Phillips, 2014.

Zero VAT Rate at 0%

Reduced VAT Rate at 5%

Standard VAT Rate at 20%

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

VAT Payable for Zero-Rated Supplies= 4400 x 0% = £0

Therefore, no VAT will be payable for Zero-rated Supplies.

1. Calculation of Relevant Input and Output for Exempt Supplies:

Since Exempt Supplies such as an air ambulance service are not eligible for any tax levy under

VAT. Cathy will not be required or permitted to register for VAT as she will not be making

taxable supplies. Similarly, Output VAT will not be due and no input VAT will be eligible for

reclaims from HMRC as per regulations.

2 . 3 Calculating VAT due to/from the relevant tax authority

Standard suppliers : On the basis of applicable rate which is 20% and VAT is

calculated on the basis of it. There is £16,615 has to be pay by Zoe and return has to be filled on

quarterly basis to HMRC.

7

Therefore, no VAT will be payable for Zero-rated Supplies.

1. Calculation of Relevant Input and Output for Exempt Supplies:

Since Exempt Supplies such as an air ambulance service are not eligible for any tax levy under

VAT. Cathy will not be required or permitted to register for VAT as she will not be making

taxable supplies. Similarly, Output VAT will not be due and no input VAT will be eligible for

reclaims from HMRC as per regulations.

2 . 3 Calculating VAT due to/from the relevant tax authority

Standard suppliers : On the basis of applicable rate which is 20% and VAT is

calculated on the basis of it. There is £16,615 has to be pay by Zoe and return has to be filled on

quarterly basis to HMRC.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zero based suppliers : On these types of suppliers there is zero percent rate of VAT is

applicable, VAT does not payable by Albert because it is not liable to pay.

Exempt suppliers : These types of suppliers does not liable to pay VAT because they

are exempted. It involves ambulance, in such case, tax does not paid by Cathy on the basis of its

VAT return of the year (Schenk and Cui, 2015).

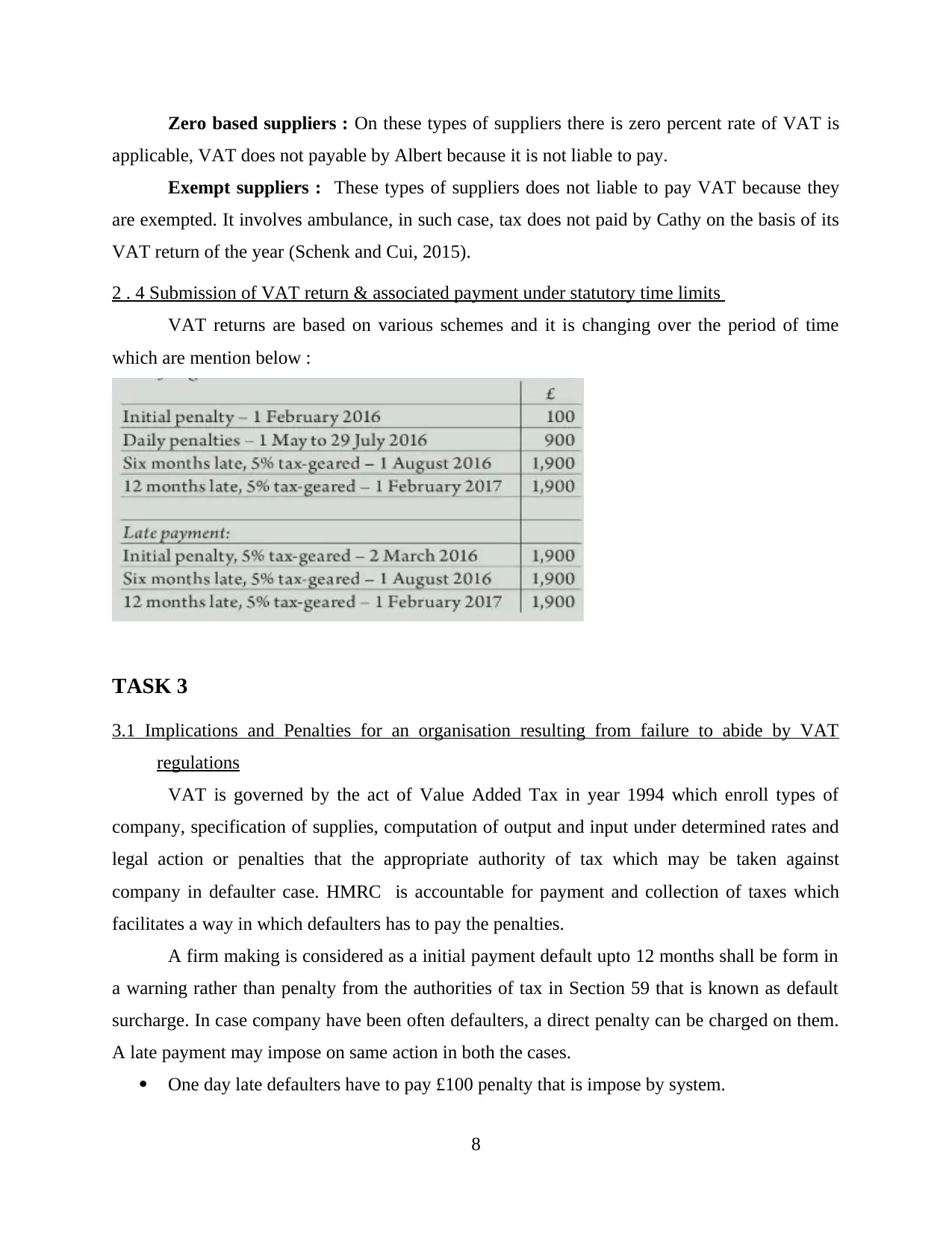

2 . 4 Submission of VAT return & associated payment under statutory time limits

VAT returns are based on various schemes and it is changing over the period of time

which are mention below :

TASK 3

3.1 Implications and Penalties for an organisation resulting from failure to abide by VAT

regulations

VAT is governed by the act of Value Added Tax in year 1994 which enroll types of

company, specification of supplies, computation of output and input under determined rates and

legal action or penalties that the appropriate authority of tax which may be taken against

company in defaulter case. HMRC is accountable for payment and collection of taxes which

facilitates a way in which defaulters has to pay the penalties.

A firm making is considered as a initial payment default upto 12 months shall be form in

a warning rather than penalty from the authorities of tax in Section 59 that is known as default

surcharge. In case company have been often defaulters, a direct penalty can be charged on them.

A late payment may impose on same action in both the cases.

One day late defaulters have to pay £100 penalty that is impose by system.

8

applicable, VAT does not payable by Albert because it is not liable to pay.

Exempt suppliers : These types of suppliers does not liable to pay VAT because they

are exempted. It involves ambulance, in such case, tax does not paid by Cathy on the basis of its

VAT return of the year (Schenk and Cui, 2015).

2 . 4 Submission of VAT return & associated payment under statutory time limits

VAT returns are based on various schemes and it is changing over the period of time

which are mention below :

TASK 3

3.1 Implications and Penalties for an organisation resulting from failure to abide by VAT

regulations

VAT is governed by the act of Value Added Tax in year 1994 which enroll types of

company, specification of supplies, computation of output and input under determined rates and

legal action or penalties that the appropriate authority of tax which may be taken against

company in defaulter case. HMRC is accountable for payment and collection of taxes which

facilitates a way in which defaulters has to pay the penalties.

A firm making is considered as a initial payment default upto 12 months shall be form in

a warning rather than penalty from the authorities of tax in Section 59 that is known as default

surcharge. In case company have been often defaulters, a direct penalty can be charged on them.

A late payment may impose on same action in both the cases.

One day late defaulters have to pay £100 penalty that is impose by system.

8

In the case of partnership company, penalty of £100 is imposed on all partner instead of

partnership firm as a entire. Only a partner of representative should appeal under some

given condition instead of individual partners.

Day to day penalties of £10 per day for 902 days should be imposed in case firm is not

capable to file returns with authorities of tax in 3 months. If six months lapse for return

filing date than an extra 5% of due taxes or £300, which is more that shall be charged that

will amount to other 5% impose or £300 which one is higher.

3.2 Adjustments and Declarations for any errors or omissions identified in previous VAT periods

Errors or omissions identified in previous

Periods of VAT:

Disclosures of omissions, errors or other types of inaccuracies is important. This kinds of

errors should be reported by filling up VAT652 form and submission to be done to team of VAT

correction. It can be categorised below:

2. An error that is made during accounting period upto four previous years.

3. An error find out which is above reporting beginning.

4. Measured mistake or error that made on intention.

The beginning of error reporting for company is limited to £10,000. Other error that

exceeds this threshold should be reported to HM revenue and costs. To compute the threshold, a

errors of net value is calculated by taking a sum-up of additional due tax to HMRC and

subtracting due tax from this particular amount.

Formula:

[Errors of Net Value = Total Additional tax due to HMRC - Tax Due]

Deliberate errors should be recorded individually to HM revenue and cost in writing

alongwith supportive information which will involve details of discovery error dates, reasons for

amounting to effects of errors and how it happen.

An errors which is identified during accounting period upto four years which has been find out

by HM revenue and costs, a definite interest amount should be imposed on tax due or

misdeclaration penalization in order to claim some amounts.

Adjustments for errors or omissions identified in previous

VAT periods:

9

partnership firm as a entire. Only a partner of representative should appeal under some

given condition instead of individual partners.

Day to day penalties of £10 per day for 902 days should be imposed in case firm is not

capable to file returns with authorities of tax in 3 months. If six months lapse for return

filing date than an extra 5% of due taxes or £300, which is more that shall be charged that

will amount to other 5% impose or £300 which one is higher.

3.2 Adjustments and Declarations for any errors or omissions identified in previous VAT periods

Errors or omissions identified in previous

Periods of VAT:

Disclosures of omissions, errors or other types of inaccuracies is important. This kinds of

errors should be reported by filling up VAT652 form and submission to be done to team of VAT

correction. It can be categorised below:

2. An error that is made during accounting period upto four previous years.

3. An error find out which is above reporting beginning.

4. Measured mistake or error that made on intention.

The beginning of error reporting for company is limited to £10,000. Other error that

exceeds this threshold should be reported to HM revenue and costs. To compute the threshold, a

errors of net value is calculated by taking a sum-up of additional due tax to HMRC and

subtracting due tax from this particular amount.

Formula:

[Errors of Net Value = Total Additional tax due to HMRC - Tax Due]

Deliberate errors should be recorded individually to HM revenue and cost in writing

alongwith supportive information which will involve details of discovery error dates, reasons for

amounting to effects of errors and how it happen.

An errors which is identified during accounting period upto four years which has been find out

by HM revenue and costs, a definite interest amount should be imposed on tax due or

misdeclaration penalization in order to claim some amounts.

Adjustments for errors or omissions identified in previous

VAT periods:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.