Analysis of VAT Regulations, Calculation, and Reporting for Businesses

VerifiedAdded on 2020/10/22

|13

|4114

|233

Report

AI Summary

This report provides a comprehensive overview of Value Added Tax (VAT) regulations, calculations, and reporting. It begins by identifying sources of VAT information and the interaction of organizations with Her Majesty's Revenue and Customs (HMRC). It then details VAT registration requirements, the information included on business documentation, and the requirements and frequency of reporting VAT schemes. The report explores the calculation of VAT, including inputs and outputs, and the preparation of VAT returns within statutory time limits. It addresses the implications and penalties for non-compliance with VAT regulations, adjustments for errors, and the communication of VAT information within an organization. The report uses examples to illustrate VAT calculations and provides insights into the impact of VAT payments on cash flows and financial forecasts, as well as the effect of VAT legislation changes on record-keeping systems. The report covers various VAT schemes like Annual Accounting, Cash Accounting, Flat Rate Scheme and Standard Scheme.

INDIRECT TAX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1. Identification of sources of VAT information.....................................................................1

1.2. Interaction of organisations with relevant government agency...........................................1

1.3. VAT Registration Requirements.........................................................................................2

1.4. Identification of information included on business documentation of VAT registered

businesses....................................................................................................................................3

1.5. Requirements and Frequency of reporting VAT schemes...................................................4

1.6. Maintaining up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................4

TASK 2............................................................................................................................................5

2.1 Extract relevant data for a specific period from the accounting system...............................5

2.2 Calculation of inputs and outputs using VAT classifications...............................................5

2.3 Calculation of VAT due to, or from the relevant tax authority.............................................6

2.4. VAT return and associated payment within the statutory time limits..................................7

TASK 3............................................................................................................................................8

3.1 Implications and Penalties for an organisation Resulting from Failure to Abide by VAT

Regulations..................................................................................................................................8

3.2. Adjustments and Declarations for Errors or Omissions Identified in Previous VAT

Periods.........................................................................................................................................9

TASK 4..........................................................................................................................................10

4.1. Informing Managers about the Impact of VAT Payment on an organisation's Cash Flows

and Financial Forecasts.............................................................................................................10

4.2. Advising People about Changes in VAT Legislation's Effect on Organisation's Record

Keeping System........................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERNCES.................................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1. Identification of sources of VAT information.....................................................................1

1.2. Interaction of organisations with relevant government agency...........................................1

1.3. VAT Registration Requirements.........................................................................................2

1.4. Identification of information included on business documentation of VAT registered

businesses....................................................................................................................................3

1.5. Requirements and Frequency of reporting VAT schemes...................................................4

1.6. Maintaining up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................4

TASK 2............................................................................................................................................5

2.1 Extract relevant data for a specific period from the accounting system...............................5

2.2 Calculation of inputs and outputs using VAT classifications...............................................5

2.3 Calculation of VAT due to, or from the relevant tax authority.............................................6

2.4. VAT return and associated payment within the statutory time limits..................................7

TASK 3............................................................................................................................................8

3.1 Implications and Penalties for an organisation Resulting from Failure to Abide by VAT

Regulations..................................................................................................................................8

3.2. Adjustments and Declarations for Errors or Omissions Identified in Previous VAT

Periods.........................................................................................................................................9

TASK 4..........................................................................................................................................10

4.1. Informing Managers about the Impact of VAT Payment on an organisation's Cash Flows

and Financial Forecasts.............................................................................................................10

4.2. Advising People about Changes in VAT Legislation's Effect on Organisation's Record

Keeping System........................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERNCES.................................................................................................................................12

INTRODUCTION

Indirect Tax refers to the amount collected by an entity present in the supply chain, for

instance, a producer or retailer, which in turns get paid to government (Wang, Caminada and

Goudswaard, 2012). This amount is paid by customers on purchase of the company's offerings.

The most prominent example of indirect tax is the Value Added Tax.. The report covers a

detailed understanding of VAT regulations and calculation of VAT returns in a timely and

accurate way. It also includes a detailed discussion of VAT penalties and various adjustments for

previous errors and communication of VAT information within the organisation.

TASK 1

1.1. Identification of sources of VAT information

Value Added Tax is a form of indirect tax which is placed on a company's offerings

whenever a specific value is added at stages of supply chain, i.e., from production to ultimate

sales of the product. Within the UK government, there are various sources which provide

effective information on VAT.

One such source of information is Value Added Tax Act, 1994. This act within the

country is related with VAT and provides effective information on this aspect which provides

effective information on the same. In addition to this, there are various provisions that are

covered under this act which are required by companies to comply with to effectively manage

VAT within their organisation.

Another source of information is government websites, which consists of online portals

where individuals as well as organisations could collect information related to VAT. These sites

provide information about the changes that take place each year in the acts associated with VAT,

which are necessary for the organisation be updated with (Sterner, 2012).

Another source by which organisations could get effective VAT information are the

journals that are issued by government and various taxation agencies which could provide the

organisation with the data and information on how the firm could effectively manage, calculate,

collect and pay VAT to the government.

1.2. Interaction of organisations with relevant government agency

It is imperative for any organisation to effectively interact with various government

agencies to gain a better understanding on how to develop a legal framework of managing and

Indirect Tax refers to the amount collected by an entity present in the supply chain, for

instance, a producer or retailer, which in turns get paid to government (Wang, Caminada and

Goudswaard, 2012). This amount is paid by customers on purchase of the company's offerings.

The most prominent example of indirect tax is the Value Added Tax.. The report covers a

detailed understanding of VAT regulations and calculation of VAT returns in a timely and

accurate way. It also includes a detailed discussion of VAT penalties and various adjustments for

previous errors and communication of VAT information within the organisation.

TASK 1

1.1. Identification of sources of VAT information

Value Added Tax is a form of indirect tax which is placed on a company's offerings

whenever a specific value is added at stages of supply chain, i.e., from production to ultimate

sales of the product. Within the UK government, there are various sources which provide

effective information on VAT.

One such source of information is Value Added Tax Act, 1994. This act within the

country is related with VAT and provides effective information on this aspect which provides

effective information on the same. In addition to this, there are various provisions that are

covered under this act which are required by companies to comply with to effectively manage

VAT within their organisation.

Another source of information is government websites, which consists of online portals

where individuals as well as organisations could collect information related to VAT. These sites

provide information about the changes that take place each year in the acts associated with VAT,

which are necessary for the organisation be updated with (Sterner, 2012).

Another source by which organisations could get effective VAT information are the

journals that are issued by government and various taxation agencies which could provide the

organisation with the data and information on how the firm could effectively manage, calculate,

collect and pay VAT to the government.

1.2. Interaction of organisations with relevant government agency

It is imperative for any organisation to effectively interact with various government

agencies to gain a better understanding on how to develop a legal framework of managing and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

filing indirect taxes. One such government organisation is Her Majesty's Revenue and Customs

which is a department within the UK which undertakes collection of taxes as well as

administration of various other regulatory regimes which also includes National Minimum

Wage.

There are various ways in which companies could interact with this organisation

regarding indirect taxes. This entity has its own website which enlists information about various

taxes and systems that are required by companies to perform ethical work frame regarding the

taxation system. The company could use this website to interact with this organisation regarding

various queries associated with filing of taxes. In addition to this, the company has postal service

too which allows the firms to interact the officials of this agency via formal letters where the

company could receive formal notices from the agencies regarding information associated with

their taxation (Pradhan and Ghosh, 2012).

Within the website there are details of the operative timings of the company throughout

the week where the agency is functional and open for interaction. Such information could be

quite useful for organisation so that they could approach the agency within in an appropriate and

timely manner.

1.3. VAT Registration Requirements

For any functional organisation, it is imperative that it be acquainted with various

requirements that are necessary for VAT registration. These requirements are necessary to be

complied by the organisation for appropriate filing of VAT returns. Within UK, it is crucial for

companies to register its business with HMRC for VAT in case the VAT taxable turnover of the

company gets more than £85,000. It is required by the firm to charge right amount of VAT and

effectively submit their VAT returns. In addition to this it is needed by the company to keep their

VAT records as well as VAT account (Penu, 2016).

There are two types of methods which are required to be considered by companies for

their VAT registration. These methods are as follows: Compulsory Registration: It is essential and compulsory for firms to register for VAT if

the firm expects its VAT taxable turnover to be higher than £85,000 in a period of next

30 days or if the VAT taxable turnover be more than the this amount over the past 12

months. It is also required for the firm to register even if it sells goods that are exempted

which is a department within the UK which undertakes collection of taxes as well as

administration of various other regulatory regimes which also includes National Minimum

Wage.

There are various ways in which companies could interact with this organisation

regarding indirect taxes. This entity has its own website which enlists information about various

taxes and systems that are required by companies to perform ethical work frame regarding the

taxation system. The company could use this website to interact with this organisation regarding

various queries associated with filing of taxes. In addition to this, the company has postal service

too which allows the firms to interact the officials of this agency via formal letters where the

company could receive formal notices from the agencies regarding information associated with

their taxation (Pradhan and Ghosh, 2012).

Within the website there are details of the operative timings of the company throughout

the week where the agency is functional and open for interaction. Such information could be

quite useful for organisation so that they could approach the agency within in an appropriate and

timely manner.

1.3. VAT Registration Requirements

For any functional organisation, it is imperative that it be acquainted with various

requirements that are necessary for VAT registration. These requirements are necessary to be

complied by the organisation for appropriate filing of VAT returns. Within UK, it is crucial for

companies to register its business with HMRC for VAT in case the VAT taxable turnover of the

company gets more than £85,000. It is required by the firm to charge right amount of VAT and

effectively submit their VAT returns. In addition to this it is needed by the company to keep their

VAT records as well as VAT account (Penu, 2016).

There are two types of methods which are required to be considered by companies for

their VAT registration. These methods are as follows: Compulsory Registration: It is essential and compulsory for firms to register for VAT if

the firm expects its VAT taxable turnover to be higher than £85,000 in a period of next

30 days or if the VAT taxable turnover be more than the this amount over the past 12

months. It is also required for the firm to register even if it sells goods that are exempted

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

from VAT but buy commodities more than £85,000 from registered suppliers for

business use.

Voluntary Registration: An organisations could register for VAT if its business turnover

is less than £85,000. However, it is required for the company to pay HMRC any VAT

amount which is owed to it from the date the firm is registered (Nie and Yue, 2012).

Companies, after receiving its VAT number from HMRC, could sign up for the online

account on its website for submitting VAT returns. In case any company fails to register online,

the firm is required to register online by using various forms which are listed below:

Form VAT1A in case the firm is an EU business and indulged in distance selling to the

UK.

Form VAT1B in case it import goods that more than £85,000 form any other EU country.

Form VAT1C in case the company disposes assets whose 8th and 13th Directive refunds

are claimed.

1.4. Identification of information included on business documentation of VAT registered

businesses

It is quite imperative that firms include effective information on its business

documentation for an appropriate management of VAT within the company. It is imperative for

firms that effective invoices are produced which are considered as the most prominent business

documentation for VAT registration (Karagöz, 2013). There are various information that could

be included in these invoices which are mentioned below:

One imperative information is the date on which the invoice was issued.

It also must include unique sequential number which is quite effective for conducting and

managing the sales.

It must also full name and address of the supplier as well as the customers. In addition, it

must also include the registration number of supplier as well.

The invoice must involve the nature and quantity of the supplied goods.

It also must include unit price exclusive of VAT and breakdown of VAT rate.

It also involves the total amount of VAT payable.

1.5. Requirements and Frequency of reporting VAT schemes

VAT scheme refers to the VAT amount that is paid by business or is claimed back from

HMRC which is the difference between the VAT charged from customers and VAT paid by the

business use.

Voluntary Registration: An organisations could register for VAT if its business turnover

is less than £85,000. However, it is required for the company to pay HMRC any VAT

amount which is owed to it from the date the firm is registered (Nie and Yue, 2012).

Companies, after receiving its VAT number from HMRC, could sign up for the online

account on its website for submitting VAT returns. In case any company fails to register online,

the firm is required to register online by using various forms which are listed below:

Form VAT1A in case the firm is an EU business and indulged in distance selling to the

UK.

Form VAT1B in case it import goods that more than £85,000 form any other EU country.

Form VAT1C in case the company disposes assets whose 8th and 13th Directive refunds

are claimed.

1.4. Identification of information included on business documentation of VAT registered

businesses

It is quite imperative that firms include effective information on its business

documentation for an appropriate management of VAT within the company. It is imperative for

firms that effective invoices are produced which are considered as the most prominent business

documentation for VAT registration (Karagöz, 2013). There are various information that could

be included in these invoices which are mentioned below:

One imperative information is the date on which the invoice was issued.

It also must include unique sequential number which is quite effective for conducting and

managing the sales.

It must also full name and address of the supplier as well as the customers. In addition, it

must also include the registration number of supplier as well.

The invoice must involve the nature and quantity of the supplied goods.

It also must include unit price exclusive of VAT and breakdown of VAT rate.

It also involves the total amount of VAT payable.

1.5. Requirements and Frequency of reporting VAT schemes

VAT scheme refers to the VAT amount that is paid by business or is claimed back from

HMRC which is the difference between the VAT charged from customers and VAT paid by the

business for its purchases. These schemes effectively aid the business to enhance their cash flow

system within the company. There are various schemes that could be used by companies which

are as follows: Annual Accounting: This scheme would allow firms to submit a single VAT return

annually. Throughout the year, companies are required to pay instalments which is based

on its estimated liability with balancing payment due along with the return. Firms could

apply for this scheme in case it expects its taxable supplies to stay below £1.35M in

following 12 months (VAT Annual Accounting Scheme, 2019). Cash Accounting: This scheme is one of the methods of VAT reporting where the VAT

is recorded as per the payments received or paid. It requires organisations to pay for its

sales and reclaim VAT on the purchases after payments made to the suppliers. The VAT

taxable turnover of the firm must be £1.35M or less. Flat Rate Scheme: Under this scheme, the tax paid by the firm would be calculated by

multiplication of VAT flat rate by VAT inclusive turnover. All the businesses regarding

of its nature get a discount of 1% in their first year. The firm is required to have VAT

turnover of £150,000 or less to apply for this scheme.

Standard Scheme: In this VAT reporting method, the VAT is recorded as well as paid as

per the issue of invoices. The company is required to submit the returns quarterly, i.e.,

four times a year. It is required by the firm to pay the difference to HMRC in case the

amount of sales is higher than that of the cost.

1.6. Maintaining up-to-date knowledge of changes to codes of practice, regulation or legislation

Each organisation follows legislations, regulations and codes of practice to effective

operative functions. For an organisation to smoothly conduct its business, it is imperative that the

firm gather up-to-date knowledge in regards with various legislations and regulations that are

provided by government (Joumard, Pisu and Bloch, 2012). It would help organisations in

managing their tax related information in a systematic manner. The changes witnessed in the

regulations aim at reducing the limitations and loopholes of the previous laws. More accurate

practices could be adopted by the firm if it has effective knowledge about these regulations. It

limits the chances of errors and enhance the possibilities of effective business practices such as

appropriate calculation of taxes in accordance with the legal standards.

system within the company. There are various schemes that could be used by companies which

are as follows: Annual Accounting: This scheme would allow firms to submit a single VAT return

annually. Throughout the year, companies are required to pay instalments which is based

on its estimated liability with balancing payment due along with the return. Firms could

apply for this scheme in case it expects its taxable supplies to stay below £1.35M in

following 12 months (VAT Annual Accounting Scheme, 2019). Cash Accounting: This scheme is one of the methods of VAT reporting where the VAT

is recorded as per the payments received or paid. It requires organisations to pay for its

sales and reclaim VAT on the purchases after payments made to the suppliers. The VAT

taxable turnover of the firm must be £1.35M or less. Flat Rate Scheme: Under this scheme, the tax paid by the firm would be calculated by

multiplication of VAT flat rate by VAT inclusive turnover. All the businesses regarding

of its nature get a discount of 1% in their first year. The firm is required to have VAT

turnover of £150,000 or less to apply for this scheme.

Standard Scheme: In this VAT reporting method, the VAT is recorded as well as paid as

per the issue of invoices. The company is required to submit the returns quarterly, i.e.,

four times a year. It is required by the firm to pay the difference to HMRC in case the

amount of sales is higher than that of the cost.

1.6. Maintaining up-to-date knowledge of changes to codes of practice, regulation or legislation

Each organisation follows legislations, regulations and codes of practice to effective

operative functions. For an organisation to smoothly conduct its business, it is imperative that the

firm gather up-to-date knowledge in regards with various legislations and regulations that are

provided by government (Joumard, Pisu and Bloch, 2012). It would help organisations in

managing their tax related information in a systematic manner. The changes witnessed in the

regulations aim at reducing the limitations and loopholes of the previous laws. More accurate

practices could be adopted by the firm if it has effective knowledge about these regulations. It

limits the chances of errors and enhance the possibilities of effective business practices such as

appropriate calculation of taxes in accordance with the legal standards.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

2.1 Extract relevant data for a specific period from the accounting system

Example 1- VAT's standard rate is currently is 20% within the country.

Mark is undergoing the process of completion of his VAT return for quarter ended 31

March, 2018. the following information is available:

Sales invoices totalling is £100000 were issued in respect of standard rated sales.

Standard rated expenses were amounted to £20700.

On 17th February 2018, Mark purchased machinery worth £23100 inclusive of VAT.

Example 2- Thomas is planning to commence trading in future. He operates an aircraft

and is taking three alternative business types in consideration. These are

Training, where sales will be standard rated for VAT

Transport, where sales are planned at Zero rated for VAT

An air ambulance service, where sales will be exempted for VAT.

For each alternative Thomas sales will be £75000 per month (VAT exclusive) and his

standard rated expenses would be £12500 per month(VAT inclusive).

2.2 Calculation of inputs and outputs using VAT classifications

1. Standard supplies: Example1

Output VAT

Sales (100,000*20%)

£20,000

Input VAT

Expenses (20700*20%) (£4140)

Machinery (23100*20/120) (£3850)

VAT payable £12010

Example 2

2.1 Extract relevant data for a specific period from the accounting system

Example 1- VAT's standard rate is currently is 20% within the country.

Mark is undergoing the process of completion of his VAT return for quarter ended 31

March, 2018. the following information is available:

Sales invoices totalling is £100000 were issued in respect of standard rated sales.

Standard rated expenses were amounted to £20700.

On 17th February 2018, Mark purchased machinery worth £23100 inclusive of VAT.

Example 2- Thomas is planning to commence trading in future. He operates an aircraft

and is taking three alternative business types in consideration. These are

Training, where sales will be standard rated for VAT

Transport, where sales are planned at Zero rated for VAT

An air ambulance service, where sales will be exempted for VAT.

For each alternative Thomas sales will be £75000 per month (VAT exclusive) and his

standard rated expenses would be £12500 per month(VAT inclusive).

2.2 Calculation of inputs and outputs using VAT classifications

1. Standard supplies: Example1

Output VAT

Sales (100,000*20%)

£20,000

Input VAT

Expenses (20700*20%) (£4140)

Machinery (23100*20/120) (£3850)

VAT payable £12010

Example 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In this example Cathy will be required to register for VAT as taxable supplies are made

by her. Output VAT of £15000 (75000*20%) per month will be due and input tax of £2083

(12500*20/120) per month will be receivable.

2. Exempted supplies: Thomas will not permitted to register for VAT taxable supplies will

not be made.

3. Zero -rated supplies: Exemption from registration for VAT could be applied by Thomas

since zero-rated supplies are being made, otherwise he should still register as these are

taxable supplies (Hansen, 2014).

Output VAT will not be due but input VAT of £2083 per month will be recoverable.

4. Exports: VAT is charged on the goods that are used in European Union otherwise no

VAT would be charged. Exported goods could be charged with zero-rated which would

allow businesses to enjoy input credit.

2.3 Calculation of VAT due to, or from the relevant tax authority

Amount due to tax department is that amount which is required to be paid to other

business organisations is higher than the received amount.. To effectively calculate amount of

due from or due to the appropriate authority input and output tax calculations will be done.

Standard supplies- General applicable rate is 20% on which VAT amount will be

calculated. Mark will be liable to pay £12010 to VAT department which is authorised by

HMRC. In another case Cathy is required to pay an amount of £13500 to the department

as net VAT payable.

Zero-rated supplies: This means the offerings which are not exempted from tax but rate

with which tax charged remains zero. This aids in taking credit to the business input tax

paid. Thomas is exempted from registration and does not require to pay any output tax to

the government. Input tax receivable is worth £2083.

Exempted supplies: Registration is not required for supply of commodities and services

which are registered as exempted. So, output VAT will not be payable and no input tax

would be recovered (Fukuyama, 2013).

by her. Output VAT of £15000 (75000*20%) per month will be due and input tax of £2083

(12500*20/120) per month will be receivable.

2. Exempted supplies: Thomas will not permitted to register for VAT taxable supplies will

not be made.

3. Zero -rated supplies: Exemption from registration for VAT could be applied by Thomas

since zero-rated supplies are being made, otherwise he should still register as these are

taxable supplies (Hansen, 2014).

Output VAT will not be due but input VAT of £2083 per month will be recoverable.

4. Exports: VAT is charged on the goods that are used in European Union otherwise no

VAT would be charged. Exported goods could be charged with zero-rated which would

allow businesses to enjoy input credit.

2.3 Calculation of VAT due to, or from the relevant tax authority

Amount due to tax department is that amount which is required to be paid to other

business organisations is higher than the received amount.. To effectively calculate amount of

due from or due to the appropriate authority input and output tax calculations will be done.

Standard supplies- General applicable rate is 20% on which VAT amount will be

calculated. Mark will be liable to pay £12010 to VAT department which is authorised by

HMRC. In another case Cathy is required to pay an amount of £13500 to the department

as net VAT payable.

Zero-rated supplies: This means the offerings which are not exempted from tax but rate

with which tax charged remains zero. This aids in taking credit to the business input tax

paid. Thomas is exempted from registration and does not require to pay any output tax to

the government. Input tax receivable is worth £2083.

Exempted supplies: Registration is not required for supply of commodities and services

which are registered as exempted. So, output VAT will not be payable and no input tax

would be recovered (Fukuyama, 2013).

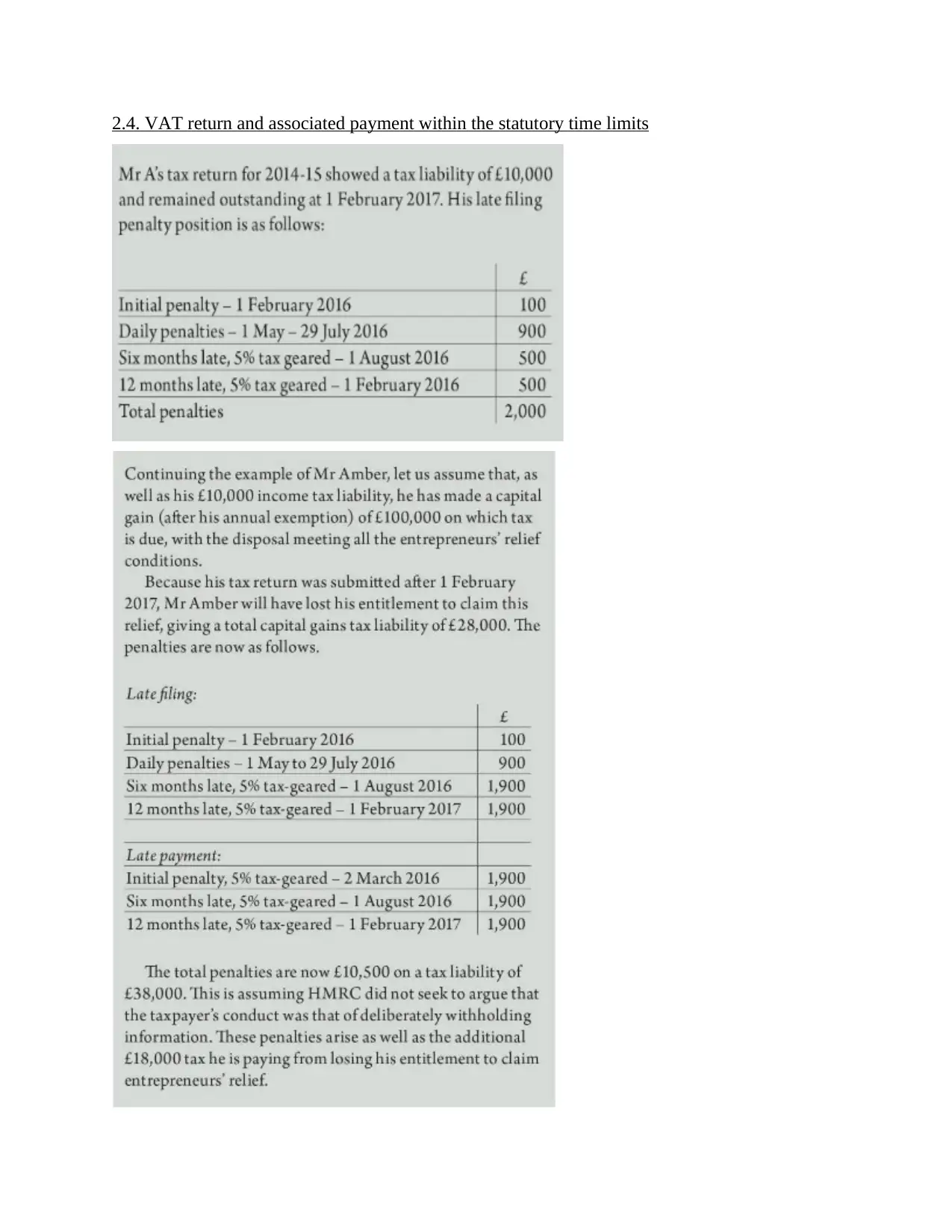

2.4. VAT return and associated payment within the statutory time limits

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

3.1 Implications and Penalties for an organisation Resulting from Failure to Abide by VAT

Regulations

The results and penalties which HMRC Department will charge are different for different

types of mistakes made by a company. These can be related to the maintenance of records. firms

must have to keep records of last six years in order to avoid the penalty from HMRC (Ehrhart,

2013). The amount of penalty is £ 500 for breaching this requirement. The amount of penalties

increases as the frequency of the mistakes done increases. For the very first time, £ 5 per day will

be charged, and if the mistake is also occurred earlier than the charge will increase to £ 10 per

day within the period of previous two years, and it is £ 15 in case an organisation is breaching

the same law for more than one time.

It is also important to know that these penalties will not be deducted in already paid

amount of the VAT Return, instead the company has to pay the VAT amount without involving

the Penalised amount in the Return amount (Deb Pal, Pohit and Roy, 2012).

Mostly the penalties are calculated on the basis “PLR” which stands for Potential Lost

Revenue. It is additional amount that is to be paid by the business in b reach of law. It is used for

the calculation of the amount to be charged from a business for the breach of certain law of

VAT. Certain criteria are set by HMRC for different types of errors such as for the careless

errors- the charge will be 30% of PLR, Deliberate Errors- the charge will be 70% of PLR, and

for Deliberate and Concealed Errors- the charge will be 100% of PLR.

In case a firm does not follow the rules and regulations of VAT, it will have to incur these

penalties.

3.2. Adjustments and Declarations for Errors or Omissions Identified in Previous VAT Periods

As HMRC sets up the penalties and implications for the non follow of rules and

regulations related to tax payment, it also provides measures to companies in making over their

mistakes, errors and omissions in their previous records of VAT Return. The best is to self

declare the mistake in any to HMRC before the department finds out it. It will prevent the

business from being effected by their intervention (Dalton, 2013).

3.1 Implications and Penalties for an organisation Resulting from Failure to Abide by VAT

Regulations

The results and penalties which HMRC Department will charge are different for different

types of mistakes made by a company. These can be related to the maintenance of records. firms

must have to keep records of last six years in order to avoid the penalty from HMRC (Ehrhart,

2013). The amount of penalty is £ 500 for breaching this requirement. The amount of penalties

increases as the frequency of the mistakes done increases. For the very first time, £ 5 per day will

be charged, and if the mistake is also occurred earlier than the charge will increase to £ 10 per

day within the period of previous two years, and it is £ 15 in case an organisation is breaching

the same law for more than one time.

It is also important to know that these penalties will not be deducted in already paid

amount of the VAT Return, instead the company has to pay the VAT amount without involving

the Penalised amount in the Return amount (Deb Pal, Pohit and Roy, 2012).

Mostly the penalties are calculated on the basis “PLR” which stands for Potential Lost

Revenue. It is additional amount that is to be paid by the business in b reach of law. It is used for

the calculation of the amount to be charged from a business for the breach of certain law of

VAT. Certain criteria are set by HMRC for different types of errors such as for the careless

errors- the charge will be 30% of PLR, Deliberate Errors- the charge will be 70% of PLR, and

for Deliberate and Concealed Errors- the charge will be 100% of PLR.

In case a firm does not follow the rules and regulations of VAT, it will have to incur these

penalties.

3.2. Adjustments and Declarations for Errors or Omissions Identified in Previous VAT Periods

As HMRC sets up the penalties and implications for the non follow of rules and

regulations related to tax payment, it also provides measures to companies in making over their

mistakes, errors and omissions in their previous records of VAT Return. The best is to self

declare the mistake in any to HMRC before the department finds out it. It will prevent the

business from being effected by their intervention (Dalton, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If any omissions or errors of equal to or less than £ 10,000 are to be adjusted than they

can be easily rectified by a company by informing to the HMRC Department. But the Deliberate

Errors made by the company must be shown separately. For this, companies have to calculate the

net amount remaining due to HMRC Department and the amount that it has already paid to

HRMC and then payment of remaining amount will settle down the omission.

The adjustment will be done while filing the next Return to HMRC, in case if any amount

is remaining due to HMRC, than it will be recorded in the Box 1 and if any amount has to be

taken back from HMRC than it must be written clearly in Box 4.

TASK 4

4.1. Informing Managers about the Impact of VAT Payment on an organisation's Cash Flows and

Financial Forecasts

The impact depends upon the type and turnover of any business. In order to get tax

advantages the managers of the should hire experts of tax legislations. There are two impacts of

value added tax on the profitability of a firm. The neutrality in the purchase and sales is sue to

the fact that companies register themselves for VAT and get net value of their sales and

purchases made by them (Aasness and Nygård, 2014). Due to this, they get and proper

estimation of their future forecasts regarding the expenses and income which will incur of their

relative sales and purchases. It will help them in knowing the VAT, they have to pay in future. In

case if an organisation is dealing in good which are exempted from the payment of VAT but the

value of those obtained goods are relatively high then VAT will be charged on the cost of

acquisition of those goods or services. The costs also affects the cash flow. As the business is

providing goods to their customers on credit basis, them the difference between the time of

selling and the time of getting the amount of those goods from the customers are different.

In these ways, managers can know the VAT Payment affects on cash flows and future

forecasts of companies.

4.2. Advising People about Changes in VAT Legislation's Effect on Organisation's Record

Keeping System

The affect of changes in the legislations of VAT can vary from companies to companies

and apply in various situations. For getting positive or eradicating the negative affects of change

in the legislations related to VAT, organisations can hire tax advisor to deal with these situations.

can be easily rectified by a company by informing to the HMRC Department. But the Deliberate

Errors made by the company must be shown separately. For this, companies have to calculate the

net amount remaining due to HMRC Department and the amount that it has already paid to

HRMC and then payment of remaining amount will settle down the omission.

The adjustment will be done while filing the next Return to HMRC, in case if any amount

is remaining due to HMRC, than it will be recorded in the Box 1 and if any amount has to be

taken back from HMRC than it must be written clearly in Box 4.

TASK 4

4.1. Informing Managers about the Impact of VAT Payment on an organisation's Cash Flows and

Financial Forecasts

The impact depends upon the type and turnover of any business. In order to get tax

advantages the managers of the should hire experts of tax legislations. There are two impacts of

value added tax on the profitability of a firm. The neutrality in the purchase and sales is sue to

the fact that companies register themselves for VAT and get net value of their sales and

purchases made by them (Aasness and Nygård, 2014). Due to this, they get and proper

estimation of their future forecasts regarding the expenses and income which will incur of their

relative sales and purchases. It will help them in knowing the VAT, they have to pay in future. In

case if an organisation is dealing in good which are exempted from the payment of VAT but the

value of those obtained goods are relatively high then VAT will be charged on the cost of

acquisition of those goods or services. The costs also affects the cash flow. As the business is

providing goods to their customers on credit basis, them the difference between the time of

selling and the time of getting the amount of those goods from the customers are different.

In these ways, managers can know the VAT Payment affects on cash flows and future

forecasts of companies.

4.2. Advising People about Changes in VAT Legislation's Effect on Organisation's Record

Keeping System

The affect of changes in the legislations of VAT can vary from companies to companies

and apply in various situations. For getting positive or eradicating the negative affects of change

in the legislations related to VAT, organisations can hire tax advisor to deal with these situations.

But is not always possible that the change in these legislations will led to negative change only

(Arauco and et. al., 2014). The changes are such as now HMRC Department is not accepting the

manual records instead it suggests companies to keep digital records. It is helpful for a firm as it

reduced the chances of damaging the data or loss of files as they can be now stored without

covering extra space of office. Not only this but it also made easier to store more data than

manual record keeping. The system enhanced the way of working of not only for one firm but

also for other companies. In addition to this, HMRC had made changes such as it will accept the

data only in spreadsheets form by the use of various software and it will be directly connected to

HMRC. It saves time of both HMRC and a company. It also helped in making all the tax related

information into one easy access form (Braunerhjelm and Eklund, 2014).

CONCLUSION

From the above given data, it is summarised that firms should be aware about all the rules

and regulations of VAT so that the company can file VAT Return at right time by doing proper

calculation so that the errors and omissions can be avoided. It will also help in proper working

and avoiding the intervention of HMRC Department in the functioning of companies. Proper

filing of tax will also help in the growth and development of the country.

(Arauco and et. al., 2014). The changes are such as now HMRC Department is not accepting the

manual records instead it suggests companies to keep digital records. It is helpful for a firm as it

reduced the chances of damaging the data or loss of files as they can be now stored without

covering extra space of office. Not only this but it also made easier to store more data than

manual record keeping. The system enhanced the way of working of not only for one firm but

also for other companies. In addition to this, HMRC had made changes such as it will accept the

data only in spreadsheets form by the use of various software and it will be directly connected to

HMRC. It saves time of both HMRC and a company. It also helped in making all the tax related

information into one easy access form (Braunerhjelm and Eklund, 2014).

CONCLUSION

From the above given data, it is summarised that firms should be aware about all the rules

and regulations of VAT so that the company can file VAT Return at right time by doing proper

calculation so that the errors and omissions can be avoided. It will also help in proper working

and avoiding the intervention of HMRC Department in the functioning of companies. Proper

filing of tax will also help in the growth and development of the country.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.