Comprehensive Taxation Law Report: Fringe Benefits and Income Tax

VerifiedAdded on 2020/05/28

|12

|2448

|99

Report

AI Summary

This report delves into various aspects of taxation law, focusing on fringe benefit tax (FBT) and income tax implications. The report begins with a case study on an employee, Charlie, and the FBT implications of a company car, analyzing both the statutory and operating cost methods for calculating FBT. It also examines the inclusion of additional benefits like wedding expenses and accommodation in the FBT calculation. The report then explores income tax consequences for Alan, a locum doctor, who receives payments in the form of wine and fees. It differentiates between business and hobby activities, using the case of Betty and Alan's marmalade production to illustrate the characteristics of a business. Finally, the report addresses the income tax implications of barter transactions, considering the principles of the ITAA 1997 and relevant rulings.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to requirement 1:...........................................................................................................2

Answer to question 1..................................................................................................................2

Ascertainment of the Car FBT:..................................................................................................2

Answer to requirement 2:...........................................................................................................5

Answer to A:..............................................................................................................................5

Answer to B:..............................................................................................................................6

Answer to C:..............................................................................................................................7

Answer to D:..............................................................................................................................8

Reference List:...........................................................................................................................9

Table of Contents

Answer to requirement 1:...........................................................................................................2

Answer to question 1..................................................................................................................2

Ascertainment of the Car FBT:..................................................................................................2

Answer to requirement 2:...........................................................................................................5

Answer to A:..............................................................................................................................5

Answer to B:..............................................................................................................................6

Answer to C:..............................................................................................................................7

Answer to D:..............................................................................................................................8

Reference List:...........................................................................................................................9

2TAXATION LAW

Answer to requirement 1:

Answer to question 1

As discussed in the “Subsection 136 (1) under Fringe Benefit Tax Assessment Act

1986” the use of the vehicle for an individual person will be considered as the personal use of

that particular if the person is not relating the use of vehicle to his employment income (Jones

2017). This case study is highlighting this fact that Charlie is an employee of Shiny Homes

and also does his duties as an agent of real estate.

Shiny Homes is known for the execution of work culture related to landscaping along

with the employment within it. This organization has provided one car to Charlie. This is

identified in the “section 7 of the FBTAA 1986” that one employee who is provided with a

car from his company should be falling under the fringe benefit tax.

Ascertainment of the Car FBT:

The car that Charlie got from Shiny Homes has travelled 80,000 km. Now, in this

total distance Charlie has used the car for his personal usages in 30,000 km and rest 50,000

km has been used for the business purposes. So under “sub-section 136 (1)”, the utility of the

car that is not used for the assessable income will be considered as the employees own

personal expenses (Richards 2014). Consequently, “para 3 of the FBTAA 1986” states that

the expense that is occurred due to the business usages must be logged into the log book to

find out the actual cost incurred for the business usages which will be helpful to calculate the

fringe benefit of the car using operating method.

Now there is consequently a statutory method for determining the fringe benefit tax of

the car. So in consideration with the “section 10A and Section 10 B of the FBTAA 1986”

states that the assessable amount for fringe benefit calculated by the operating cost method

Answer to requirement 1:

Answer to question 1

As discussed in the “Subsection 136 (1) under Fringe Benefit Tax Assessment Act

1986” the use of the vehicle for an individual person will be considered as the personal use of

that particular if the person is not relating the use of vehicle to his employment income (Jones

2017). This case study is highlighting this fact that Charlie is an employee of Shiny Homes

and also does his duties as an agent of real estate.

Shiny Homes is known for the execution of work culture related to landscaping along

with the employment within it. This organization has provided one car to Charlie. This is

identified in the “section 7 of the FBTAA 1986” that one employee who is provided with a

car from his company should be falling under the fringe benefit tax.

Ascertainment of the Car FBT:

The car that Charlie got from Shiny Homes has travelled 80,000 km. Now, in this

total distance Charlie has used the car for his personal usages in 30,000 km and rest 50,000

km has been used for the business purposes. So under “sub-section 136 (1)”, the utility of the

car that is not used for the assessable income will be considered as the employees own

personal expenses (Richards 2014). Consequently, “para 3 of the FBTAA 1986” states that

the expense that is occurred due to the business usages must be logged into the log book to

find out the actual cost incurred for the business usages which will be helpful to calculate the

fringe benefit of the car using operating method.

Now there is consequently a statutory method for determining the fringe benefit tax of

the car. So in consideration with the “section 10A and Section 10 B of the FBTAA 1986”

states that the assessable amount for fringe benefit calculated by the operating cost method

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

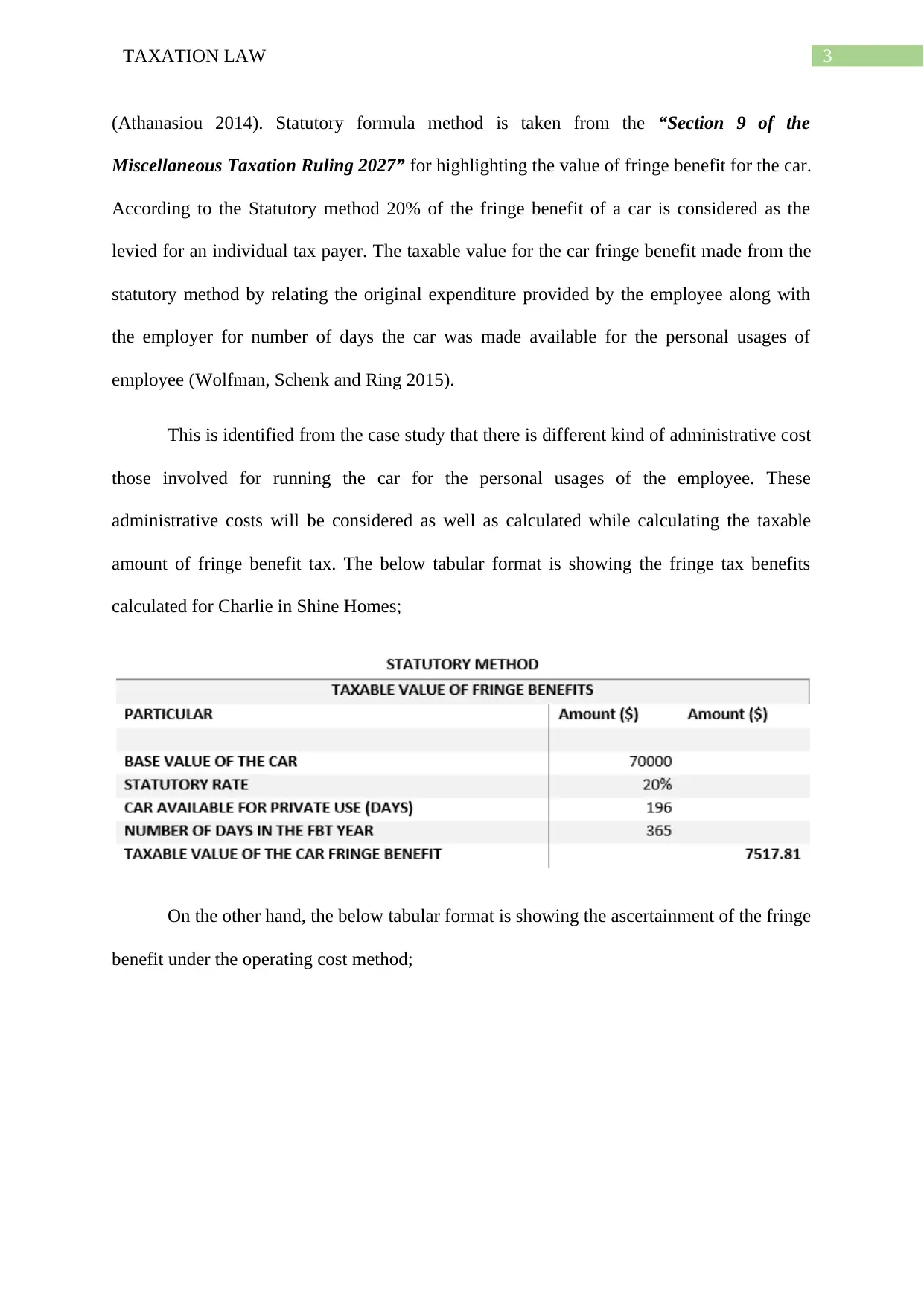

(Athanasiou 2014). Statutory formula method is taken from the “Section 9 of the

Miscellaneous Taxation Ruling 2027” for highlighting the value of fringe benefit for the car.

According to the Statutory method 20% of the fringe benefit of a car is considered as the

levied for an individual tax payer. The taxable value for the car fringe benefit made from the

statutory method by relating the original expenditure provided by the employee along with

the employer for number of days the car was made available for the personal usages of

employee (Wolfman, Schenk and Ring 2015).

This is identified from the case study that there is different kind of administrative cost

those involved for running the car for the personal usages of the employee. These

administrative costs will be considered as well as calculated while calculating the taxable

amount of fringe benefit tax. The below tabular format is showing the fringe tax benefits

calculated for Charlie in Shine Homes;

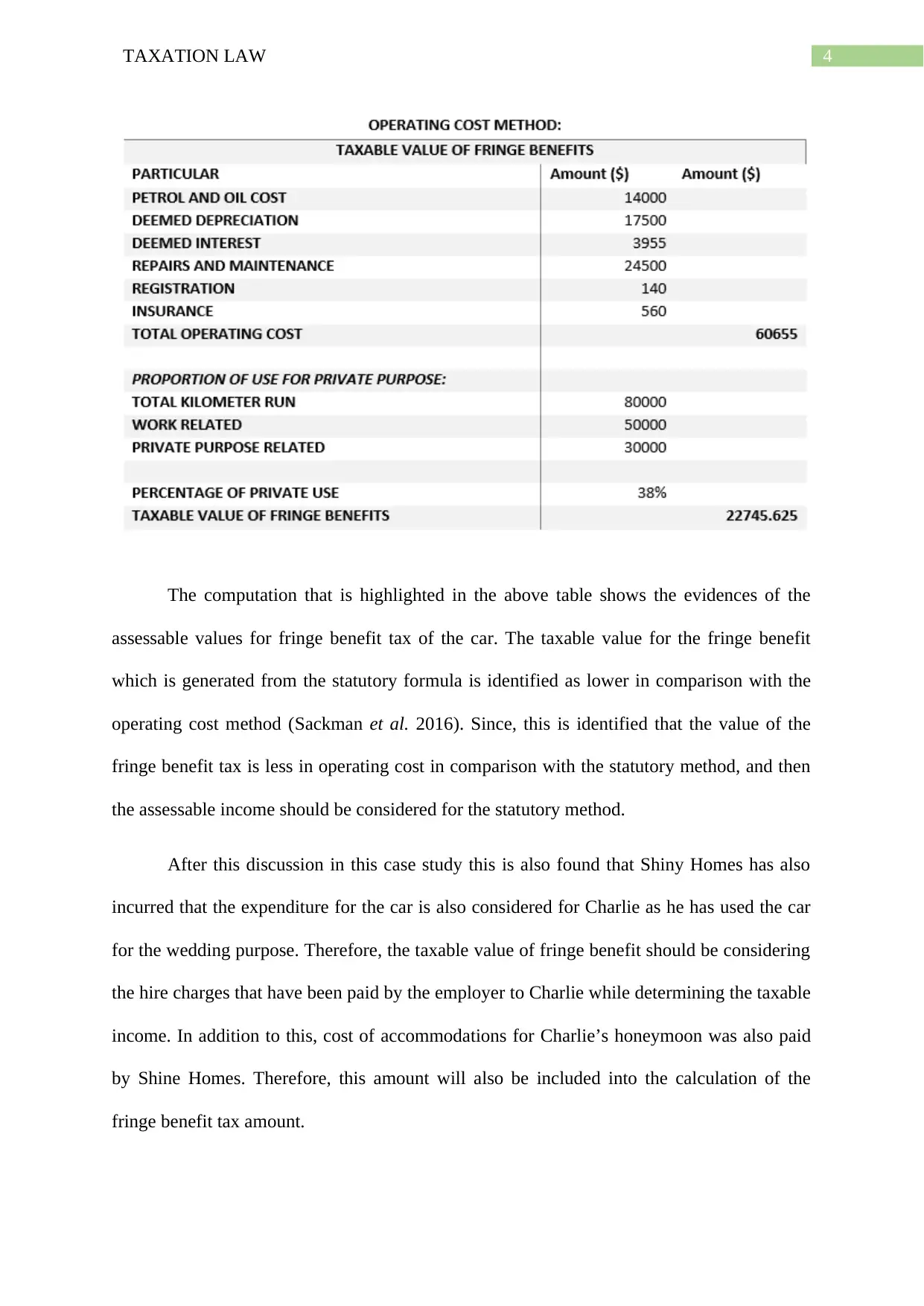

On the other hand, the below tabular format is showing the ascertainment of the fringe

benefit under the operating cost method;

(Athanasiou 2014). Statutory formula method is taken from the “Section 9 of the

Miscellaneous Taxation Ruling 2027” for highlighting the value of fringe benefit for the car.

According to the Statutory method 20% of the fringe benefit of a car is considered as the

levied for an individual tax payer. The taxable value for the car fringe benefit made from the

statutory method by relating the original expenditure provided by the employee along with

the employer for number of days the car was made available for the personal usages of

employee (Wolfman, Schenk and Ring 2015).

This is identified from the case study that there is different kind of administrative cost

those involved for running the car for the personal usages of the employee. These

administrative costs will be considered as well as calculated while calculating the taxable

amount of fringe benefit tax. The below tabular format is showing the fringe tax benefits

calculated for Charlie in Shine Homes;

On the other hand, the below tabular format is showing the ascertainment of the fringe

benefit under the operating cost method;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The computation that is highlighted in the above table shows the evidences of the

assessable values for fringe benefit tax of the car. The taxable value for the fringe benefit

which is generated from the statutory formula is identified as lower in comparison with the

operating cost method (Sackman et al. 2016). Since, this is identified that the value of the

fringe benefit tax is less in operating cost in comparison with the statutory method, and then

the assessable income should be considered for the statutory method.

After this discussion in this case study this is also found that Shiny Homes has also

incurred that the expenditure for the car is also considered for Charlie as he has used the car

for the wedding purpose. Therefore, the taxable value of fringe benefit should be considering

the hire charges that have been paid by the employer to Charlie while determining the taxable

income. In addition to this, cost of accommodations for Charlie’s honeymoon was also paid

by Shine Homes. Therefore, this amount will also be included into the calculation of the

fringe benefit tax amount.

The computation that is highlighted in the above table shows the evidences of the

assessable values for fringe benefit tax of the car. The taxable value for the fringe benefit

which is generated from the statutory formula is identified as lower in comparison with the

operating cost method (Sackman et al. 2016). Since, this is identified that the value of the

fringe benefit tax is less in operating cost in comparison with the statutory method, and then

the assessable income should be considered for the statutory method.

After this discussion in this case study this is also found that Shiny Homes has also

incurred that the expenditure for the car is also considered for Charlie as he has used the car

for the wedding purpose. Therefore, the taxable value of fringe benefit should be considering

the hire charges that have been paid by the employer to Charlie while determining the taxable

income. In addition to this, cost of accommodations for Charlie’s honeymoon was also paid

by Shine Homes. Therefore, this amount will also be included into the calculation of the

fringe benefit tax amount.

5TAXATION LAW

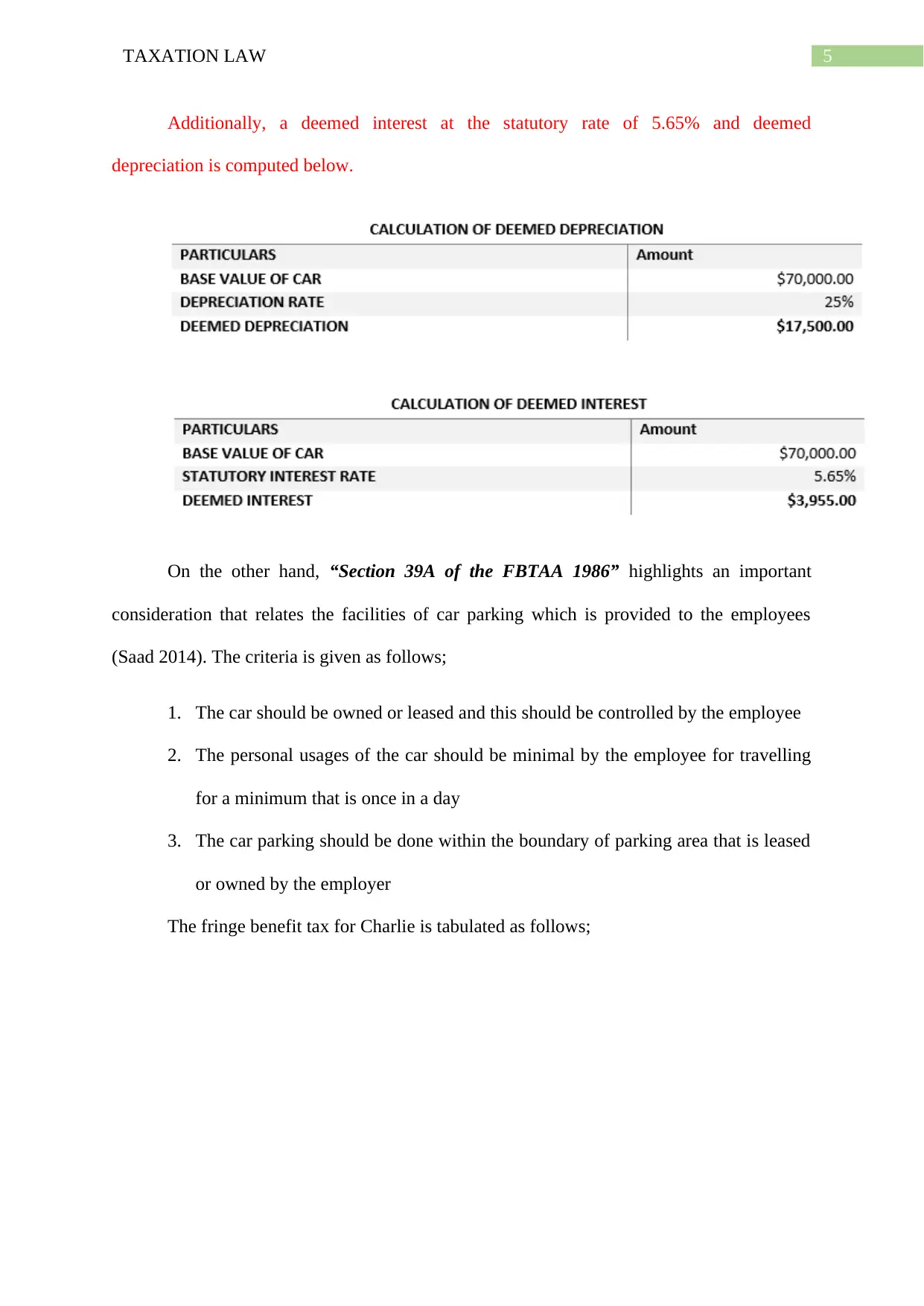

Additionally, a deemed interest at the statutory rate of 5.65% and deemed

depreciation is computed below.

On the other hand, “Section 39A of the FBTAA 1986” highlights an important

consideration that relates the facilities of car parking which is provided to the employees

(Saad 2014). The criteria is given as follows;

1. The car should be owned or leased and this should be controlled by the employee

2. The personal usages of the car should be minimal by the employee for travelling

for a minimum that is once in a day

3. The car parking should be done within the boundary of parking area that is leased

or owned by the employer

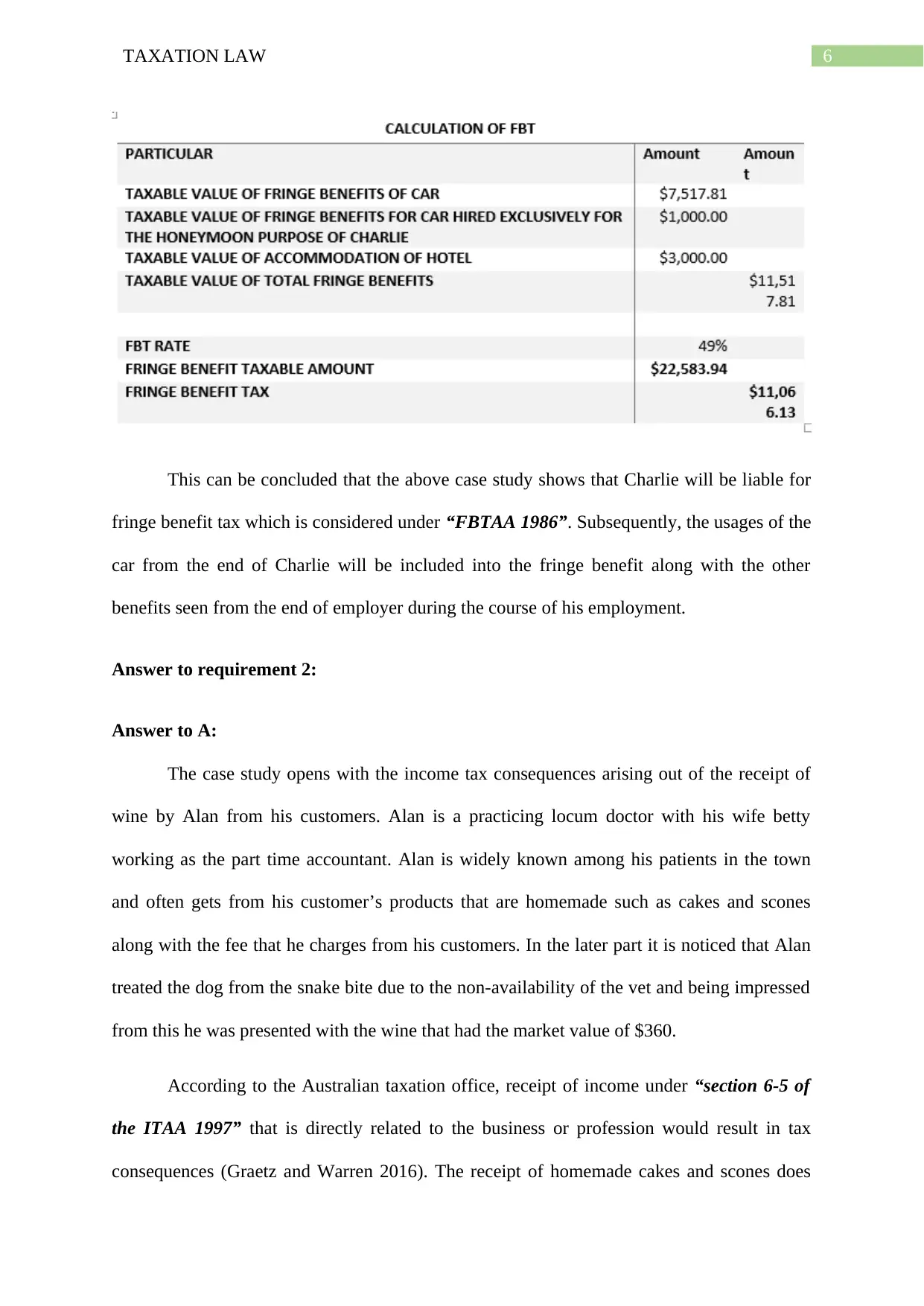

The fringe benefit tax for Charlie is tabulated as follows;

Additionally, a deemed interest at the statutory rate of 5.65% and deemed

depreciation is computed below.

On the other hand, “Section 39A of the FBTAA 1986” highlights an important

consideration that relates the facilities of car parking which is provided to the employees

(Saad 2014). The criteria is given as follows;

1. The car should be owned or leased and this should be controlled by the employee

2. The personal usages of the car should be minimal by the employee for travelling

for a minimum that is once in a day

3. The car parking should be done within the boundary of parking area that is leased

or owned by the employer

The fringe benefit tax for Charlie is tabulated as follows;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

This can be concluded that the above case study shows that Charlie will be liable for

fringe benefit tax which is considered under “FBTAA 1986”. Subsequently, the usages of the

car from the end of Charlie will be included into the fringe benefit along with the other

benefits seen from the end of employer during the course of his employment.

Answer to requirement 2:

Answer to A:

The case study opens with the income tax consequences arising out of the receipt of

wine by Alan from his customers. Alan is a practicing locum doctor with his wife betty

working as the part time accountant. Alan is widely known among his patients in the town

and often gets from his customer’s products that are homemade such as cakes and scones

along with the fee that he charges from his customers. In the later part it is noticed that Alan

treated the dog from the snake bite due to the non-availability of the vet and being impressed

from this he was presented with the wine that had the market value of $360.

According to the Australian taxation office, receipt of income under “section 6-5 of

the ITAA 1997” that is directly related to the business or profession would result in tax

consequences (Graetz and Warren 2016). The receipt of homemade cakes and scones does

This can be concluded that the above case study shows that Charlie will be liable for

fringe benefit tax which is considered under “FBTAA 1986”. Subsequently, the usages of the

car from the end of Charlie will be included into the fringe benefit along with the other

benefits seen from the end of employer during the course of his employment.

Answer to requirement 2:

Answer to A:

The case study opens with the income tax consequences arising out of the receipt of

wine by Alan from his customers. Alan is a practicing locum doctor with his wife betty

working as the part time accountant. Alan is widely known among his patients in the town

and often gets from his customer’s products that are homemade such as cakes and scones

along with the fee that he charges from his customers. In the later part it is noticed that Alan

treated the dog from the snake bite due to the non-availability of the vet and being impressed

from this he was presented with the wine that had the market value of $360.

According to the Australian taxation office, receipt of income under “section 6-5 of

the ITAA 1997” that is directly related to the business or profession would result in tax

consequences (Graetz and Warren 2016). The receipt of homemade cakes and scones does

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

not has any commercial value and the same would not be regarded for income tax

assessment. However, the receipt of wine with the market value of $360 would be liable for

taxation since it has the market value. Similarly, the receipt of fees by Alan from his patients

would be considered for assessment under “section 6-5 of the ITAA 1997”.

Answer to B:

According to the “Taxation ruling of TR 97/11” Hobby is regarded as different from

business since hobby is generally undertaken for recreational purpose while business possess

the intention of making profit (Davis et al. 2015). In compliance with the “taxation ruling of

TR 97/11” it act as the guide in deciding whether the taxpayer is performing the activity of

primary production with the intention of making profit or for only recreational purpose

(Woellner et al. 2017). The below listed factors are vital in determining whether the taxpayer

is carrying on the business or hobby or business;

i. Business usually has the purpose of significant commercial intention while hobby

on the other hand does not have intention of undertaking the commercial activity

ii. Business activities are generally performed with the intention of making profit

while hobby hardly has any motivation of making profit

iii. An individual taxpayer usually holds the objective of indulging in the business

activities while hobby does not have the intention of indulging in the commercial

activities

iv. Whether the person does not have objective of carrying on the business in the

similar process whereas hobby is performed in an ad hoc means (Bevacqua 2015).

v. The business activities are usually planned and it is executed in a commercial

manner whereas hobby is not planned and it is not carried on as a business.

not has any commercial value and the same would not be regarded for income tax

assessment. However, the receipt of wine with the market value of $360 would be liable for

taxation since it has the market value. Similarly, the receipt of fees by Alan from his patients

would be considered for assessment under “section 6-5 of the ITAA 1997”.

Answer to B:

According to the “Taxation ruling of TR 97/11” Hobby is regarded as different from

business since hobby is generally undertaken for recreational purpose while business possess

the intention of making profit (Davis et al. 2015). In compliance with the “taxation ruling of

TR 97/11” it act as the guide in deciding whether the taxpayer is performing the activity of

primary production with the intention of making profit or for only recreational purpose

(Woellner et al. 2017). The below listed factors are vital in determining whether the taxpayer

is carrying on the business or hobby or business;

i. Business usually has the purpose of significant commercial intention while hobby

on the other hand does not have intention of undertaking the commercial activity

ii. Business activities are generally performed with the intention of making profit

while hobby hardly has any motivation of making profit

iii. An individual taxpayer usually holds the objective of indulging in the business

activities while hobby does not have the intention of indulging in the commercial

activities

iv. Whether the person does not have objective of carrying on the business in the

similar process whereas hobby is performed in an ad hoc means (Bevacqua 2015).

v. The business activities are usually planned and it is executed in a commercial

manner whereas hobby is not planned and it is not carried on as a business.

8TAXATION LAW

According to the verdict that has been passed in the case of “Evans v Federal

Commissioner of Taxation (1989) 20 ATR” the federal court of law has stated whether or

not the hobby constitutes a recreational activity (Lang 2014). The amount of revenue or

income that is derived from the activities of hobby will not be considered income whereas the

activities that are repetitive or having the intention of profit would be considered as business

activities.

Answer to C:

As defined under the “taxation ruling of TR 97/11” it is transacting with the taxpayer

that are conducting the activities of primary productions. Similarly, under the “section 6 (1)

of the ITAA 1997” an individual carrying on the business of cultivation on land would be

regarded as carrying on the activities of primary production (Miller and Oats 2016). On

conducting the primary activities of production the court of law has asserted its by stating

whether or not the individual taxpayer is carrying on the business for profit or have indulged

for recreational purpose.

The evidence presented from situation of Betty and Alan it is found that Betty makes

marmalade which soon became very known among her neighbours. In the later stages she

considered opening a stall in the Newtown Market. On every second Sunday she set up her

stall and the excess amount is sold by Alan to the supplier on constant basis. An assertion can

be bought forward in respect of the present situation of Alan and Betty that the activities

possessed the business characteristics with repetitive nature. Citing the reference of “Martin

v. Federal Commissioner of Taxation (1953)” the judgement of the court asserted that there

is not a singular factor which would offer a conclusive evidence (Davison, Monotti and

Wiseman 2015). The activities of Alan and Betty had coinciding indicators of commercial

nature that carried the objective of making profit with business intentions.

According to the verdict that has been passed in the case of “Evans v Federal

Commissioner of Taxation (1989) 20 ATR” the federal court of law has stated whether or

not the hobby constitutes a recreational activity (Lang 2014). The amount of revenue or

income that is derived from the activities of hobby will not be considered income whereas the

activities that are repetitive or having the intention of profit would be considered as business

activities.

Answer to C:

As defined under the “taxation ruling of TR 97/11” it is transacting with the taxpayer

that are conducting the activities of primary productions. Similarly, under the “section 6 (1)

of the ITAA 1997” an individual carrying on the business of cultivation on land would be

regarded as carrying on the activities of primary production (Miller and Oats 2016). On

conducting the primary activities of production the court of law has asserted its by stating

whether or not the individual taxpayer is carrying on the business for profit or have indulged

for recreational purpose.

The evidence presented from situation of Betty and Alan it is found that Betty makes

marmalade which soon became very known among her neighbours. In the later stages she

considered opening a stall in the Newtown Market. On every second Sunday she set up her

stall and the excess amount is sold by Alan to the supplier on constant basis. An assertion can

be bought forward in respect of the present situation of Alan and Betty that the activities

possessed the business characteristics with repetitive nature. Citing the reference of “Martin

v. Federal Commissioner of Taxation (1953)” the judgement of the court asserted that there

is not a singular factor which would offer a conclusive evidence (Davison, Monotti and

Wiseman 2015). The activities of Alan and Betty had coinciding indicators of commercial

nature that carried the objective of making profit with business intentions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Answer to D:

As it has been stated under the “Subsection 25 (1) of the ITAA 1936” a taxpayer

deriving income from the barter system is liable for income tax consequences. The instances

provided under the “taxation ruling of IT 2668” states that transactions of barter system and

business exchange will be having both the income tax liabilities and GST. This is because the

transactions of barter system are treated in a similar manner to that of the transactions in cash

or credit. Similarly, the situations of Alan and Betty, the extent of value received under the

barter system is reliant on the nature of amount received by the recipients.

With reference to the verdict of the federal commissioner in the case of “FC of T. v.

Cooke & Sherden 1980” value received in the form of cash or kind by Allan and Betty under

the barter system would have both the tax and GST consequences under the “ITAA 1997 and

GSTR 1999” (Mihaylov et al. 2015). The reason for tax consequences is that the transactions

from the barter system is holding the identical value of cash or credit transactions.

Answer to D:

As it has been stated under the “Subsection 25 (1) of the ITAA 1936” a taxpayer

deriving income from the barter system is liable for income tax consequences. The instances

provided under the “taxation ruling of IT 2668” states that transactions of barter system and

business exchange will be having both the income tax liabilities and GST. This is because the

transactions of barter system are treated in a similar manner to that of the transactions in cash

or credit. Similarly, the situations of Alan and Betty, the extent of value received under the

barter system is reliant on the nature of amount received by the recipients.

With reference to the verdict of the federal commissioner in the case of “FC of T. v.

Cooke & Sherden 1980” value received in the form of cash or kind by Allan and Betty under

the barter system would have both the tax and GST consequences under the “ITAA 1997 and

GSTR 1999” (Mihaylov et al. 2015). The reason for tax consequences is that the transactions

from the barter system is holding the identical value of cash or credit transactions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Reference List:

Athanasiou, A., 2014. Get together (right now)-Ordinary income and Div 7A?. Taxation in

Australia, 49(5), p.279.

Bevacqua, J., 2015. ATO accountability and taxpayer fairness: An assessment of the proposal

to split the Australian taxation office. UNSWLJ, 38, p.995.

Davis, A.K., Guenther, D.A., Krull, L.K. and Williams, B.M., 2015. Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), pp.47-68.

Davison, M., Monotti, A. and Wiseman, L., 2015. Australian intellectual property law.

Cambridge University Press.

Graetz, M.J. and Warren, A.C., 2016. Integration of corporate and shareholder taxes.

Jones, D., 2017. Tax and accounting income-Worlds apart?. Taxation in Australia, 52(1),

p.14.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Mihaylov, G., Tretola, J., Yawson, A. and Zurbruegg, R., 2015. Tax compliance behaviour in

Australian self-managed superannuation funds.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Richards, R., 2014. Taxation: Employee share schemes. Law Society Journal: the official

journal of the Law Society of New South Wales, 52(3), p.40.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Sackman, J., Van Brunt, R., Rohan, P.J. and Reskin, M., 2016. Tax Issues in Condemnation

Cases (Vol. 7). Nichols on Eminent Domain.

Reference List:

Athanasiou, A., 2014. Get together (right now)-Ordinary income and Div 7A?. Taxation in

Australia, 49(5), p.279.

Bevacqua, J., 2015. ATO accountability and taxpayer fairness: An assessment of the proposal

to split the Australian taxation office. UNSWLJ, 38, p.995.

Davis, A.K., Guenther, D.A., Krull, L.K. and Williams, B.M., 2015. Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), pp.47-68.

Davison, M., Monotti, A. and Wiseman, L., 2015. Australian intellectual property law.

Cambridge University Press.

Graetz, M.J. and Warren, A.C., 2016. Integration of corporate and shareholder taxes.

Jones, D., 2017. Tax and accounting income-Worlds apart?. Taxation in Australia, 52(1),

p.14.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Mihaylov, G., Tretola, J., Yawson, A. and Zurbruegg, R., 2015. Tax compliance behaviour in

Australian self-managed superannuation funds.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Richards, R., 2014. Taxation: Employee share schemes. Law Society Journal: the official

journal of the Law Society of New South Wales, 52(3), p.40.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Sackman, J., Van Brunt, R., Rohan, P.J. and Reskin, M., 2016. Tax Issues in Condemnation

Cases (Vol. 7). Nichols on Eminent Domain.

11TAXATION LAW

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Wolfman, B., Schenk, D.H. and Ring, D.M., 2015. Ethical Problems in Federal Tax

Practice. Wolters Kluwer Law & Business.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Wolfman, B., Schenk, D.H. and Ring, D.M., 2015. Ethical Problems in Federal Tax

Practice. Wolters Kluwer Law & Business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.