TAXATION LAW 9: Fringe Benefits, Barter System and Taxation

VerifiedAdded on 2020/05/28

|12

|2183

|399

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Taxation Law assignment. Part A addresses fringe benefits, specifically car fringe benefits, detailing the application of the Fringe Benefit Tax Assessment Act 1986, the statutory method, and the operating cost method for determining assessable value. It analyzes a case study involving an employee receiving a company car and considers the implications of personal and private usage. Part B examines income tax implications for individuals, including Alan and Betty, focusing on assessable income from professional fees, the taxability of gifts, and the distinction between business and hobby activities, referencing relevant case law and tax rulings. The assignment further explores the taxation of income derived from barter systems, aligning with ITAA 1936 and GST regulations, and provides detailed calculations and explanations throughout.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Part A:........................................................................................................................................2

Answer to question 1:.................................................................................................................2

Case facts:..................................................................................................................................3

Part B:.........................................................................................................................................6

Answer to question 2:.................................................................................................................6

Answer to question (A):.............................................................................................................6

Answer to question (B):.............................................................................................................7

Answer to question (C):.............................................................................................................8

Answer to question (D):.............................................................................................................8

Reference List:.........................................................................................................................10

Table of Contents

Part A:........................................................................................................................................2

Answer to question 1:.................................................................................................................2

Case facts:..................................................................................................................................3

Part B:.........................................................................................................................................6

Answer to question 2:.................................................................................................................6

Answer to question (A):.............................................................................................................6

Answer to question (B):.............................................................................................................7

Answer to question (C):.............................................................................................................8

Answer to question (D):.............................................................................................................8

Reference List:.........................................................................................................................10

2TAXATION LAW

Part A:

Answer to question 1:

The employers generally provide the fringe benefits to their employees apart from the

salaries and wages. In accordance with the “FBTAA 1986”, this is can be notified that the

relation between the employee and employer is necessary for receiving the benefits (Sikka,

2017). This relation between among two individual enables the utilization of provision under

FBTAA 1986 for determining the tax obligations for both the individuals (employee and

employers).

As discussed in section 7 of the Fringe Benefit Tax Assessment Act 1986 if the

benefit provided by a company is a car then this will be constituted as the car fringe benefit

(Mellon, 2016). This act highlights this fact that providing a car to an employee or providing

the car with lease agreement, this case will be resulting into the car fringe benefit tax for the

employee. According to the elaboration of the fringe benefits, this is clear that if the

employee uses the car for his personal usages instead of the private purposes then also this

will be considered as the fringe benefit for the purpose of taxation.

There are specifically two significant methods for determining the assessable value

for car fringe benefits. These two methods include the statutory formulation methodology and

operating cost methodology. In case of this statutory methodology the considered assessable

amount within the fringe benefit is calculated by the value of the whole car. In addition to

this, section 10A and 10 B of the FBTAA 1986 is considered as associated with the

assessable value of the car fringe benefit in case of the operating cost method (Sharkey &

Murray, 2016). According to the operating cost method, this involves the administration of

the car and also determines the assessable income of involved within the fringe benefits. One

of the important fact involved within these methods are the method, which is identified for

Part A:

Answer to question 1:

The employers generally provide the fringe benefits to their employees apart from the

salaries and wages. In accordance with the “FBTAA 1986”, this is can be notified that the

relation between the employee and employer is necessary for receiving the benefits (Sikka,

2017). This relation between among two individual enables the utilization of provision under

FBTAA 1986 for determining the tax obligations for both the individuals (employee and

employers).

As discussed in section 7 of the Fringe Benefit Tax Assessment Act 1986 if the

benefit provided by a company is a car then this will be constituted as the car fringe benefit

(Mellon, 2016). This act highlights this fact that providing a car to an employee or providing

the car with lease agreement, this case will be resulting into the car fringe benefit tax for the

employee. According to the elaboration of the fringe benefits, this is clear that if the

employee uses the car for his personal usages instead of the private purposes then also this

will be considered as the fringe benefit for the purpose of taxation.

There are specifically two significant methods for determining the assessable value

for car fringe benefits. These two methods include the statutory formulation methodology and

operating cost methodology. In case of this statutory methodology the considered assessable

amount within the fringe benefit is calculated by the value of the whole car. In addition to

this, section 10A and 10 B of the FBTAA 1986 is considered as associated with the

assessable value of the car fringe benefit in case of the operating cost method (Sharkey &

Murray, 2016). According to the operating cost method, this involves the administration of

the car and also determines the assessable income of involved within the fringe benefits. One

of the important fact involved within these methods are the method, which is identified for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

lowest assessable value for the fringe benefit, is considered for calculation of fringe benefit

tax. For using the operating cost method, the employee will require the maintenance of the

expenditure involved in case of the logbook or any related document.

Case facts:

The case study incurs this fact that he is the employee of Shiny Homes Pty Ltd.,

which provides him with a car. This car is allowed for personal as well private usages of

Charlie. In observance with section, 7 of the Fringe Benefit Tax Assessment Act 1986 all the

benefits provided to Charlie in the form of car will be included in car fringe benefit and will

also be calculated for taxation (Robin, 2017). For determining the assessable value of the car

fringe benefit of Charlie both the methods are applied namely the Statutory Method and

Operating Cost Method. In case of the statutory method, the statutory rate of 20% is applied

for determining the fringe benefits involved within Charlie’s case here.

The statutory rate for of 20% is generally multiplied with the base value for the car in

order to ascertain the assessable value of the fringe benefit. The degree of private utilization

made by the employer is not taken in case of determining the assessable value related to the

fringe benefit involved within the statutory Method. On the other hand, in case of the

operating cost method, the total amount for the operating cost involved in administration of

the car is segregated within separation for the personal along with the private usages of the

car. This helps in determining the assessable value for the fringe benefit while calculating the

taxation for the particular car. Therefore, the calculation showed below highlights the

Statutory Method as well as Operating Cost Method;

lowest assessable value for the fringe benefit, is considered for calculation of fringe benefit

tax. For using the operating cost method, the employee will require the maintenance of the

expenditure involved in case of the logbook or any related document.

Case facts:

The case study incurs this fact that he is the employee of Shiny Homes Pty Ltd.,

which provides him with a car. This car is allowed for personal as well private usages of

Charlie. In observance with section, 7 of the Fringe Benefit Tax Assessment Act 1986 all the

benefits provided to Charlie in the form of car will be included in car fringe benefit and will

also be calculated for taxation (Robin, 2017). For determining the assessable value of the car

fringe benefit of Charlie both the methods are applied namely the Statutory Method and

Operating Cost Method. In case of the statutory method, the statutory rate of 20% is applied

for determining the fringe benefits involved within Charlie’s case here.

The statutory rate for of 20% is generally multiplied with the base value for the car in

order to ascertain the assessable value of the fringe benefit. The degree of private utilization

made by the employer is not taken in case of determining the assessable value related to the

fringe benefit involved within the statutory Method. On the other hand, in case of the

operating cost method, the total amount for the operating cost involved in administration of

the car is segregated within separation for the personal along with the private usages of the

car. This helps in determining the assessable value for the fringe benefit while calculating the

taxation for the particular car. Therefore, the calculation showed below highlights the

Statutory Method as well as Operating Cost Method;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

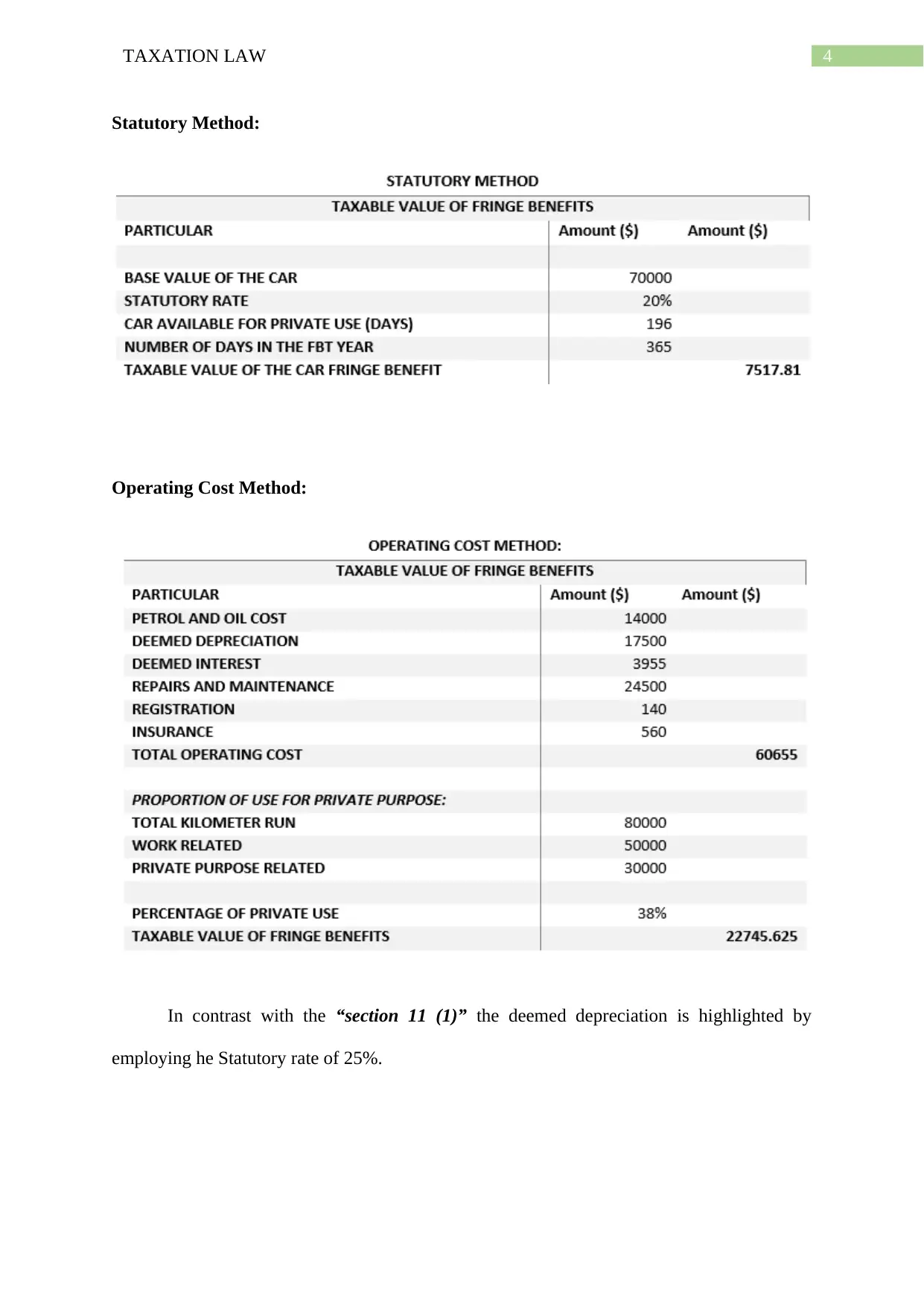

Statutory Method:

Operating Cost Method:

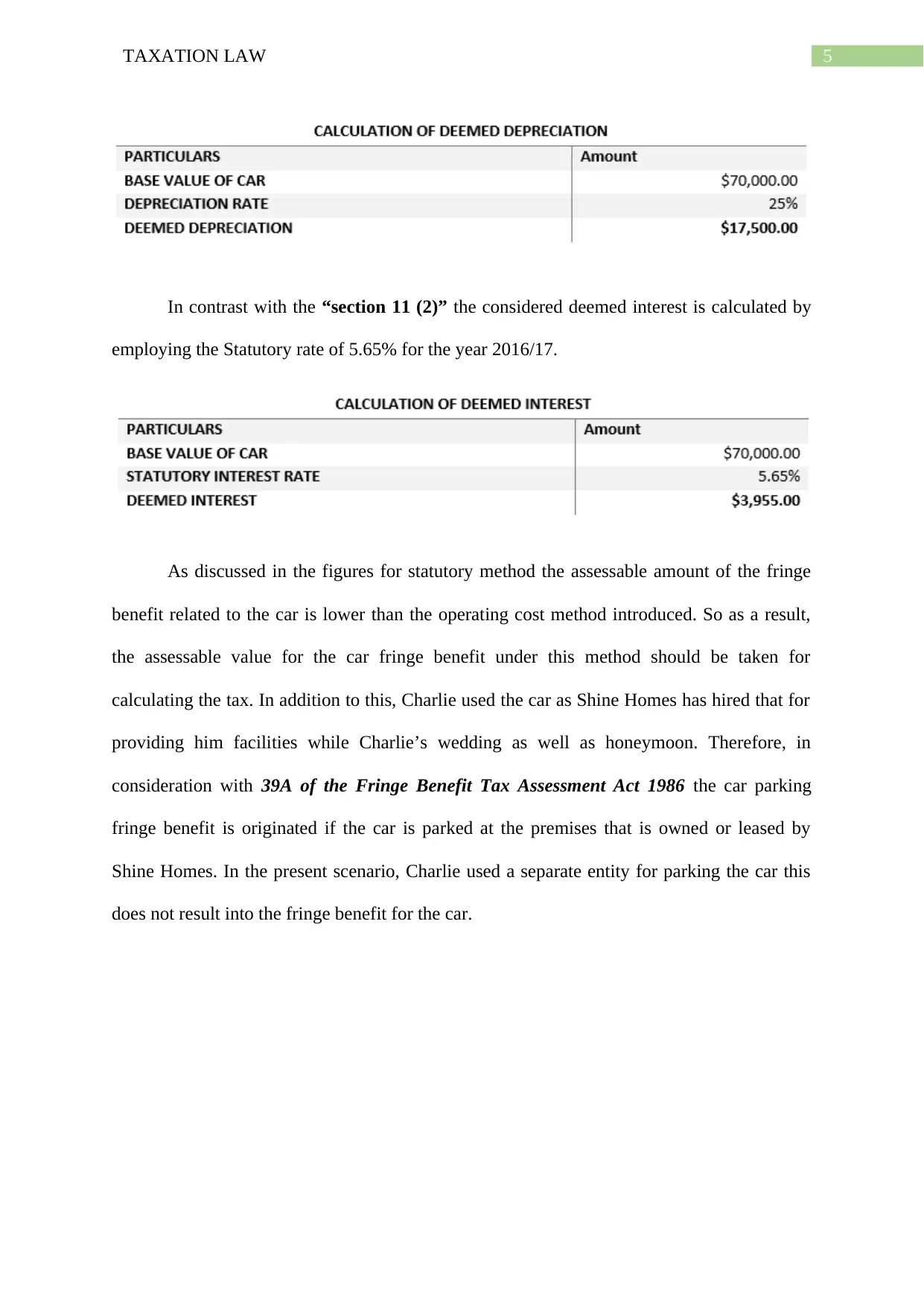

In contrast with the “section 11 (1)” the deemed depreciation is highlighted by

employing he Statutory rate of 25%.

Statutory Method:

Operating Cost Method:

In contrast with the “section 11 (1)” the deemed depreciation is highlighted by

employing he Statutory rate of 25%.

5TAXATION LAW

In contrast with the “section 11 (2)” the considered deemed interest is calculated by

employing the Statutory rate of 5.65% for the year 2016/17.

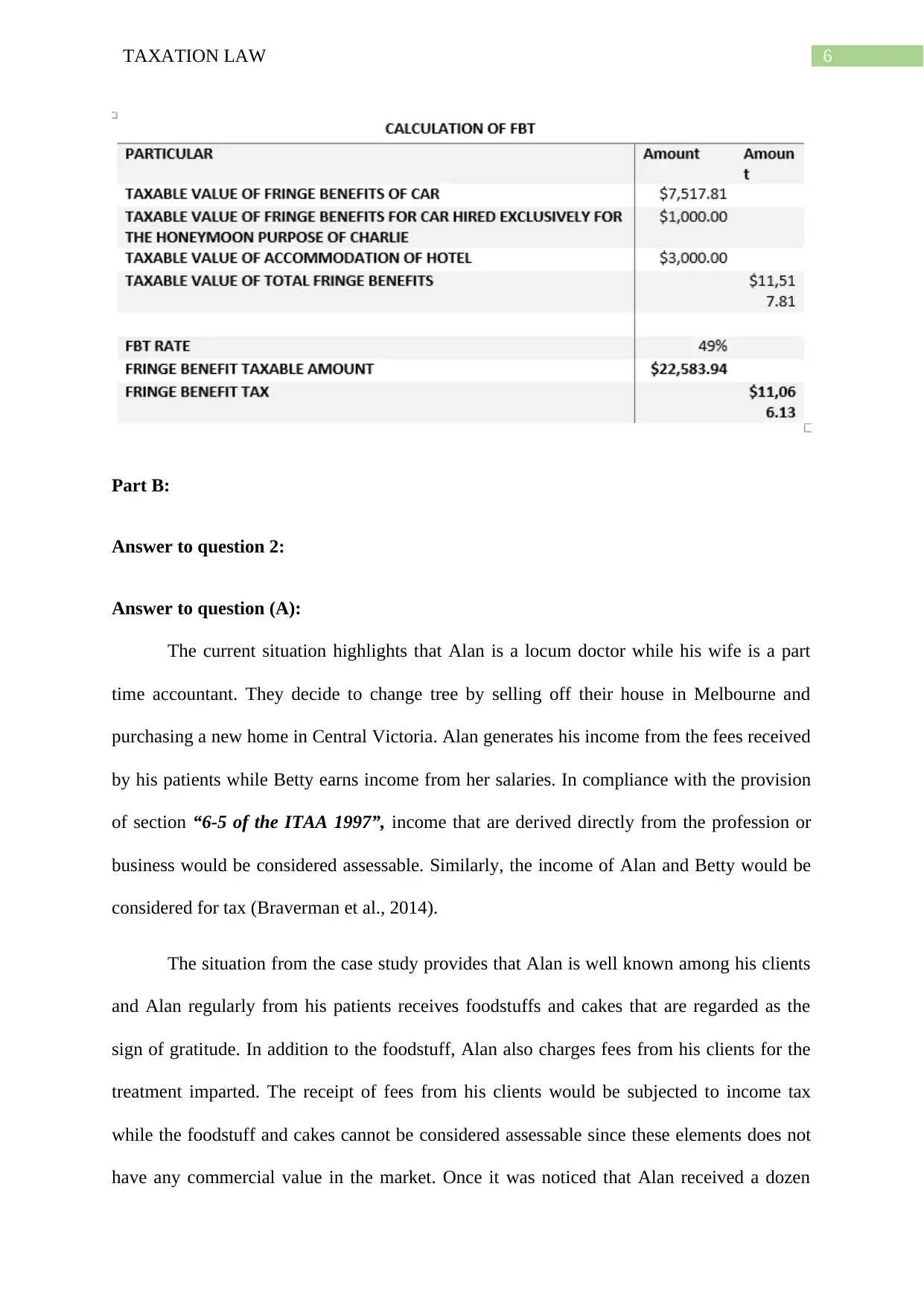

As discussed in the figures for statutory method the assessable amount of the fringe

benefit related to the car is lower than the operating cost method introduced. So as a result,

the assessable value for the car fringe benefit under this method should be taken for

calculating the tax. In addition to this, Charlie used the car as Shine Homes has hired that for

providing him facilities while Charlie’s wedding as well as honeymoon. Therefore, in

consideration with 39A of the Fringe Benefit Tax Assessment Act 1986 the car parking

fringe benefit is originated if the car is parked at the premises that is owned or leased by

Shine Homes. In the present scenario, Charlie used a separate entity for parking the car this

does not result into the fringe benefit for the car.

In contrast with the “section 11 (2)” the considered deemed interest is calculated by

employing the Statutory rate of 5.65% for the year 2016/17.

As discussed in the figures for statutory method the assessable amount of the fringe

benefit related to the car is lower than the operating cost method introduced. So as a result,

the assessable value for the car fringe benefit under this method should be taken for

calculating the tax. In addition to this, Charlie used the car as Shine Homes has hired that for

providing him facilities while Charlie’s wedding as well as honeymoon. Therefore, in

consideration with 39A of the Fringe Benefit Tax Assessment Act 1986 the car parking

fringe benefit is originated if the car is parked at the premises that is owned or leased by

Shine Homes. In the present scenario, Charlie used a separate entity for parking the car this

does not result into the fringe benefit for the car.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Part B:

Answer to question 2:

Answer to question (A):

The current situation highlights that Alan is a locum doctor while his wife is a part

time accountant. They decide to change tree by selling off their house in Melbourne and

purchasing a new home in Central Victoria. Alan generates his income from the fees received

by his patients while Betty earns income from her salaries. In compliance with the provision

of section “6-5 of the ITAA 1997”, income that are derived directly from the profession or

business would be considered assessable. Similarly, the income of Alan and Betty would be

considered for tax (Braverman et al., 2014).

The situation from the case study provides that Alan is well known among his clients

and Alan regularly from his patients receives foodstuffs and cakes that are regarded as the

sign of gratitude. In addition to the foodstuff, Alan also charges fees from his clients for the

treatment imparted. The receipt of fees from his clients would be subjected to income tax

while the foodstuff and cakes cannot be considered assessable since these elements does not

have any commercial value in the market. Once it was noticed that Alan received a dozen

Part B:

Answer to question 2:

Answer to question (A):

The current situation highlights that Alan is a locum doctor while his wife is a part

time accountant. They decide to change tree by selling off their house in Melbourne and

purchasing a new home in Central Victoria. Alan generates his income from the fees received

by his patients while Betty earns income from her salaries. In compliance with the provision

of section “6-5 of the ITAA 1997”, income that are derived directly from the profession or

business would be considered assessable. Similarly, the income of Alan and Betty would be

considered for tax (Braverman et al., 2014).

The situation from the case study provides that Alan is well known among his clients

and Alan regularly from his patients receives foodstuffs and cakes that are regarded as the

sign of gratitude. In addition to the foodstuff, Alan also charges fees from his clients for the

treatment imparted. The receipt of fees from his clients would be subjected to income tax

while the foodstuff and cakes cannot be considered assessable since these elements does not

have any commercial value in the market. Once it was noticed that Alan received a dozen

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

bottles of wine from one of his client as he saved his client dog from a snakebite. The wine

bottles received by Alan carried market value of $360. Therefore, the receipt of wine by Alan

from his client would be included into his taxable income because it contained commercial

value and will be liable for income under the provision of “section 6-5 of the ITAA 1997”

(Hodgson & Pearce, 2015).

Answer to question (B):

In accordance with the “taxation ruling of TR 97/11”, a determination is made whether

the person is engaged in the activities of primary production or hobby. The ruling is helpful

in providing an understanding of an individual indulgence in business or hobby (Black,

2017). To differentiate between hobby and business, the below listed differences provides a

better understanding;

a. Activities that comprises of the sale of goods commercial will be held as business.

Hobby involves sale among friends and relatives.

b. Business generally consists of repetition of activities. Hobby does not any such

regularity or repetition of activities.

c. Business activities generally comprises of purpose or intention while hobby does not

have any such purpose or intention of executing business activities.

d. The activities of business are generally big in magnitude. Hobby is generally small in

extent and scale.

The characteristics of an activity or the intent of an individual helps in ascertaining

whether the person is carrying on a business or hobby. As held in the case of “Ferguson v F

C of Taxation (1979) amount derived from hobby is an income whereas yielding profit from

those hobby is regarded as carrying on of a business (Kaplan & Nadler, 2015).

bottles of wine from one of his client as he saved his client dog from a snakebite. The wine

bottles received by Alan carried market value of $360. Therefore, the receipt of wine by Alan

from his client would be included into his taxable income because it contained commercial

value and will be liable for income under the provision of “section 6-5 of the ITAA 1997”

(Hodgson & Pearce, 2015).

Answer to question (B):

In accordance with the “taxation ruling of TR 97/11”, a determination is made whether

the person is engaged in the activities of primary production or hobby. The ruling is helpful

in providing an understanding of an individual indulgence in business or hobby (Black,

2017). To differentiate between hobby and business, the below listed differences provides a

better understanding;

a. Activities that comprises of the sale of goods commercial will be held as business.

Hobby involves sale among friends and relatives.

b. Business generally consists of repetition of activities. Hobby does not any such

regularity or repetition of activities.

c. Business activities generally comprises of purpose or intention while hobby does not

have any such purpose or intention of executing business activities.

d. The activities of business are generally big in magnitude. Hobby is generally small in

extent and scale.

The characteristics of an activity or the intent of an individual helps in ascertaining

whether the person is carrying on a business or hobby. As held in the case of “Ferguson v F

C of Taxation (1979) amount derived from hobby is an income whereas yielding profit from

those hobby is regarded as carrying on of a business (Kaplan & Nadler, 2015).

8TAXATION LAW

Answer to question (C):

The case study introduces that Betty started making marmalade that became well

known among her neighbours. This made her open a stall and put up her marmalade on sale

during second Sunday of each month. Alan sold the additional or the leftover amount to the

local supplier frequently.

According to the decision of commissioner in “Martin v. FC of T (1953), no form of

sole actions would be capable of interpreting an exclusive indication and contained

overlapping indicators (Miller & Oats, 2016). In the current situation of Alan and Betty, the

activities contained the purpose of profit and had regularity. As a result, the selling of

marmalade is regarded as business activities and profit generated from such business would

be considered for assessment of tax.

Answer to question (D):

As it has been defined by the ATO, any form of transactions that arises from the

barter system shall be accompanying income tax consequences and GST. The transactions

from the barter system will be treated equivalent to the transactions of cash and credit. It is

noteworthy to denote that “Subsection 25 (1) of the ITAA 1936” defines that earnings

generated from the barter system would be accompanying tax consequences (Stiglitz, &

Rosengard, 2015).

The federal court in the case of “Federal Commissioner. Of T. v. Cooke & Sherden

1980” stated that income that is earned from the barter system would be considered for

assessment since they are considered equivalent to cash and credit dealings (Barkoczy, 2016).

With reference to the above judgement, both Alan and Betty would be held liable for tax and

GST under the “GSTR 1999” for the earnings derived from barter system. The income from

barter system is treated equivalent to the business dealings made in cash and credit.

Answer to question (C):

The case study introduces that Betty started making marmalade that became well

known among her neighbours. This made her open a stall and put up her marmalade on sale

during second Sunday of each month. Alan sold the additional or the leftover amount to the

local supplier frequently.

According to the decision of commissioner in “Martin v. FC of T (1953), no form of

sole actions would be capable of interpreting an exclusive indication and contained

overlapping indicators (Miller & Oats, 2016). In the current situation of Alan and Betty, the

activities contained the purpose of profit and had regularity. As a result, the selling of

marmalade is regarded as business activities and profit generated from such business would

be considered for assessment of tax.

Answer to question (D):

As it has been defined by the ATO, any form of transactions that arises from the

barter system shall be accompanying income tax consequences and GST. The transactions

from the barter system will be treated equivalent to the transactions of cash and credit. It is

noteworthy to denote that “Subsection 25 (1) of the ITAA 1936” defines that earnings

generated from the barter system would be accompanying tax consequences (Stiglitz, &

Rosengard, 2015).

The federal court in the case of “Federal Commissioner. Of T. v. Cooke & Sherden

1980” stated that income that is earned from the barter system would be considered for

assessment since they are considered equivalent to cash and credit dealings (Barkoczy, 2016).

With reference to the above judgement, both Alan and Betty would be held liable for tax and

GST under the “GSTR 1999” for the earnings derived from barter system. The income from

barter system is treated equivalent to the business dealings made in cash and credit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Reference List:

Black, C. (2017). The Attribution of Profits to Permanent Establishments: Testing the

Interaction of Domestic Taxation Laws and Tax Treaties in Practice.

Braverman, D., Marsden, S., & Sadiq, K. (2015). Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl.

Tax'n, 17, 1.

Du Preez, H. (2016). A construction of the fundamental principles of taxation (Doctoral

dissertation, University of Pretoria).

Hodgson, H., & Pearce, P. (2015). TravelSmart or travel tax breaks: is the fringe benefits tax

a barrier to active commuting in Australia? 1. eJournal of Tax Research, 13(3), 819.

Kabinga, M. (2015). Established principles of taxation. Tax justice & poverty.

Kaplan, R. A., & Nadler, M. L. (2015). Airbnb: A case study in occupancy regulation and

taxation. U. Chi. L. Rev. Dialogue, 82, 103.

Mellon, A. W. (2016). Taxation: the people’s business. Pickle Partners Publishing.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

ROBIN, H. (2017). AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Sharkey, N., & Murray, I. (2016). Reinventing administrative leadership in Australian

taxation: beware the fine balance of social psychological and rule of law

principles. Austl. Tax F., 31, 63.

Sikka, P. (2017, January). Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting Forum. Elsevier.

Reference List:

Black, C. (2017). The Attribution of Profits to Permanent Establishments: Testing the

Interaction of Domestic Taxation Laws and Tax Treaties in Practice.

Braverman, D., Marsden, S., & Sadiq, K. (2015). Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl.

Tax'n, 17, 1.

Du Preez, H. (2016). A construction of the fundamental principles of taxation (Doctoral

dissertation, University of Pretoria).

Hodgson, H., & Pearce, P. (2015). TravelSmart or travel tax breaks: is the fringe benefits tax

a barrier to active commuting in Australia? 1. eJournal of Tax Research, 13(3), 819.

Kabinga, M. (2015). Established principles of taxation. Tax justice & poverty.

Kaplan, R. A., & Nadler, M. L. (2015). Airbnb: A case study in occupancy regulation and

taxation. U. Chi. L. Rev. Dialogue, 82, 103.

Mellon, A. W. (2016). Taxation: the people’s business. Pickle Partners Publishing.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

ROBIN, H. (2017). AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Sharkey, N., & Murray, I. (2016). Reinventing administrative leadership in Australian

taxation: beware the fine balance of social psychological and rule of law

principles. Austl. Tax F., 31, 63.

Sikka, P. (2017, January). Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting Forum. Elsevier.

11TAXATION LAW

Stiglitz, J. E., & Rosengard, J. K. (2015). Economics of the Public Sector: Fourth

International Student Edition. WW Norton & Company.

Stiglitz, J. E., & Rosengard, J. K. (2015). Economics of the Public Sector: Fourth

International Student Edition. WW Norton & Company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.