Australian Taxation Law - PDF

12 Pages2448 Words99 Views

Added on 2020-05-28

Australian Taxation Law - PDF

Added on 2020-05-28

ShareRelated Documents

Running head: TAXATION LAWTaxation LawName of the StudentName of the UniversityAuthors NoteCourse ID

TAXATION LAW1Table of ContentsAnswer to requirement 1:...........................................................................................................2Answer to question 1..................................................................................................................2Ascertainment of the Car FBT:..................................................................................................2Answer to requirement 2:...........................................................................................................5Answer to A:..............................................................................................................................5Answer to B:..............................................................................................................................6Answer to C:..............................................................................................................................7Answer to D:..............................................................................................................................8Reference List:...........................................................................................................................9

TAXATION LAW2Answer to requirement 1:Answer to question 1 As discussed in the “Subsection 136 (1) under Fringe Benefit Tax Assessment Act1986” the use of the vehicle for an individual person will be considered as the personal use ofthat particular if the person is not relating the use of vehicle to his employment income (Jones2017). This case study is highlighting this fact that Charlie is an employee of Shiny Homesand also does his duties as an agent of real estate. Shiny Homes is known for the execution of work culture related to landscaping alongwith the employment within it. This organization has provided one car to Charlie. This isidentified in the “section 7 of the FBTAA 1986” that one employee who is provided with acar from his company should be falling under the fringe benefit tax. Ascertainment of the Car FBT:The car that Charlie got from Shiny Homes has travelled 80,000 km. Now, in thistotal distance Charlie has used the car for his personal usages in 30,000 km and rest 50,000km has been used for the business purposes. So under “sub-section 136 (1)”, the utility of thecar that is not used for the assessable income will be considered as the employees ownpersonal expenses (Richards 2014). Consequently, “para 3 of the FBTAA 1986” states thatthe expense that is occurred due to the business usages must be logged into the log book tofind out the actual cost incurred for the business usages which will be helpful to calculate thefringe benefit of the car using operating method. Now there is consequently a statutory method for determining the fringe benefit tax ofthe car. So in consideration with the “section 10A and Section 10 B of the FBTAA 1986”states that the assessable amount for fringe benefit calculated by the operating cost method

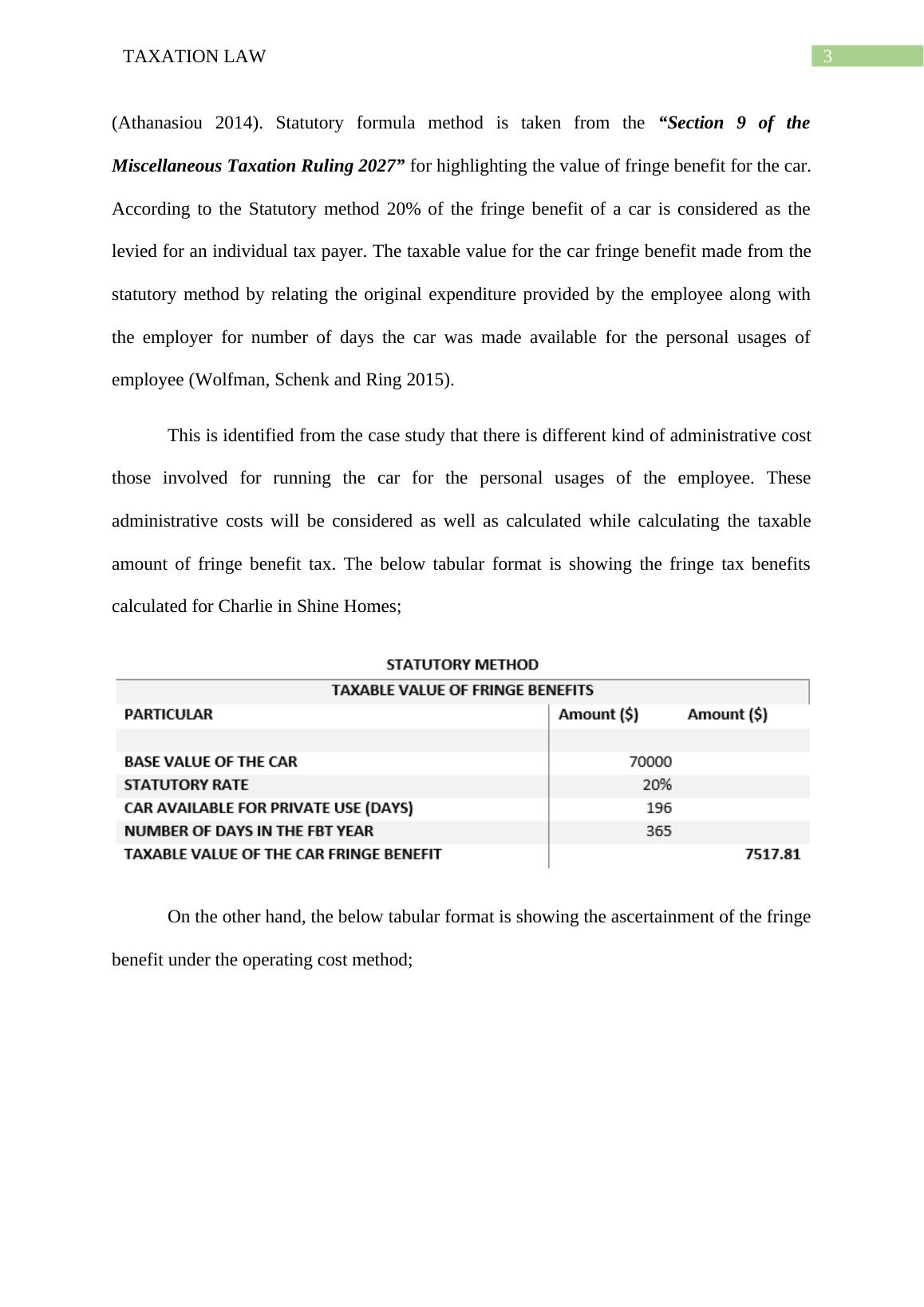

TAXATION LAW3(Athanasiou 2014). Statutory formula method is taken from the “Section 9 of theMiscellaneous Taxation Ruling 2027” for highlighting the value of fringe benefit for the car.According to the Statutory method 20% of the fringe benefit of a car is considered as thelevied for an individual tax payer. The taxable value for the car fringe benefit made from thestatutory method by relating the original expenditure provided by the employee along withthe employer for number of days the car was made available for the personal usages ofemployee (Wolfman, Schenk and Ring 2015). This is identified from the case study that there is different kind of administrative costthose involved for running the car for the personal usages of the employee. Theseadministrative costs will be considered as well as calculated while calculating the taxableamount of fringe benefit tax. The below tabular format is showing the fringe tax benefitscalculated for Charlie in Shine Homes;On the other hand, the below tabular format is showing the ascertainment of the fringebenefit under the operating cost method;

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Fringe Benefit Tax Assessment Act 1986lg...

|11

|2284

|34

Assignment on Taxation Lawlg...

|14

|3084

|39

Case Study - Taxation Lawlg...

|10

|1748

|51

Answer to question 1: Taxation Law Name of the Student Name of the University Authorslg...

|12

|2450

|268

Taxation Law Assignment - Fringe Benefit Taxlg...

|8

|1309

|36

TAXATION LAW TAXATION LAW 9 9 Taxation Law Name of the University Authorlg...

|12

|2183

|399