Financial Analysis Report: Audit and Assurance of DIPL Ltd.

VerifiedAdded on 2020/03/04

|8

|2103

|37

Report

AI Summary

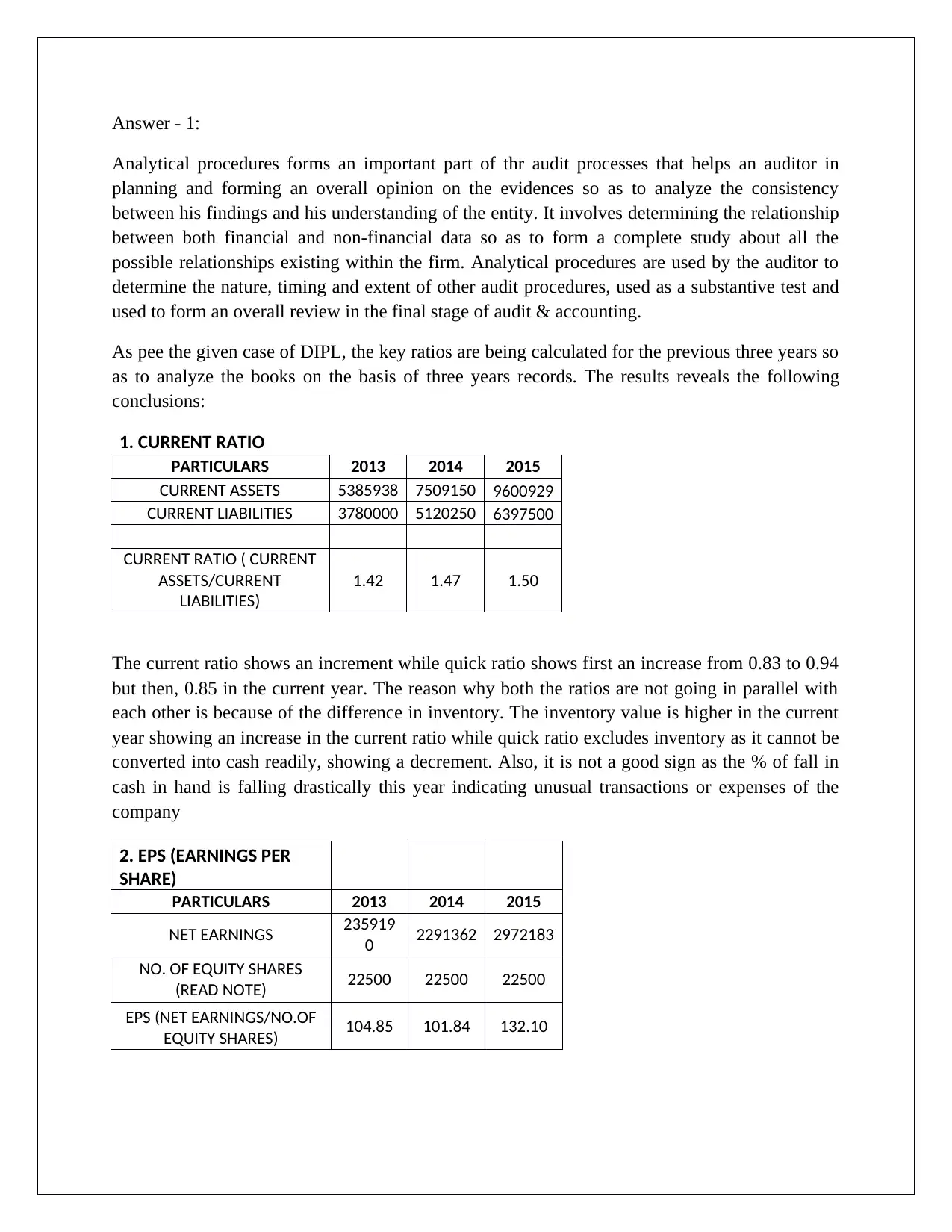

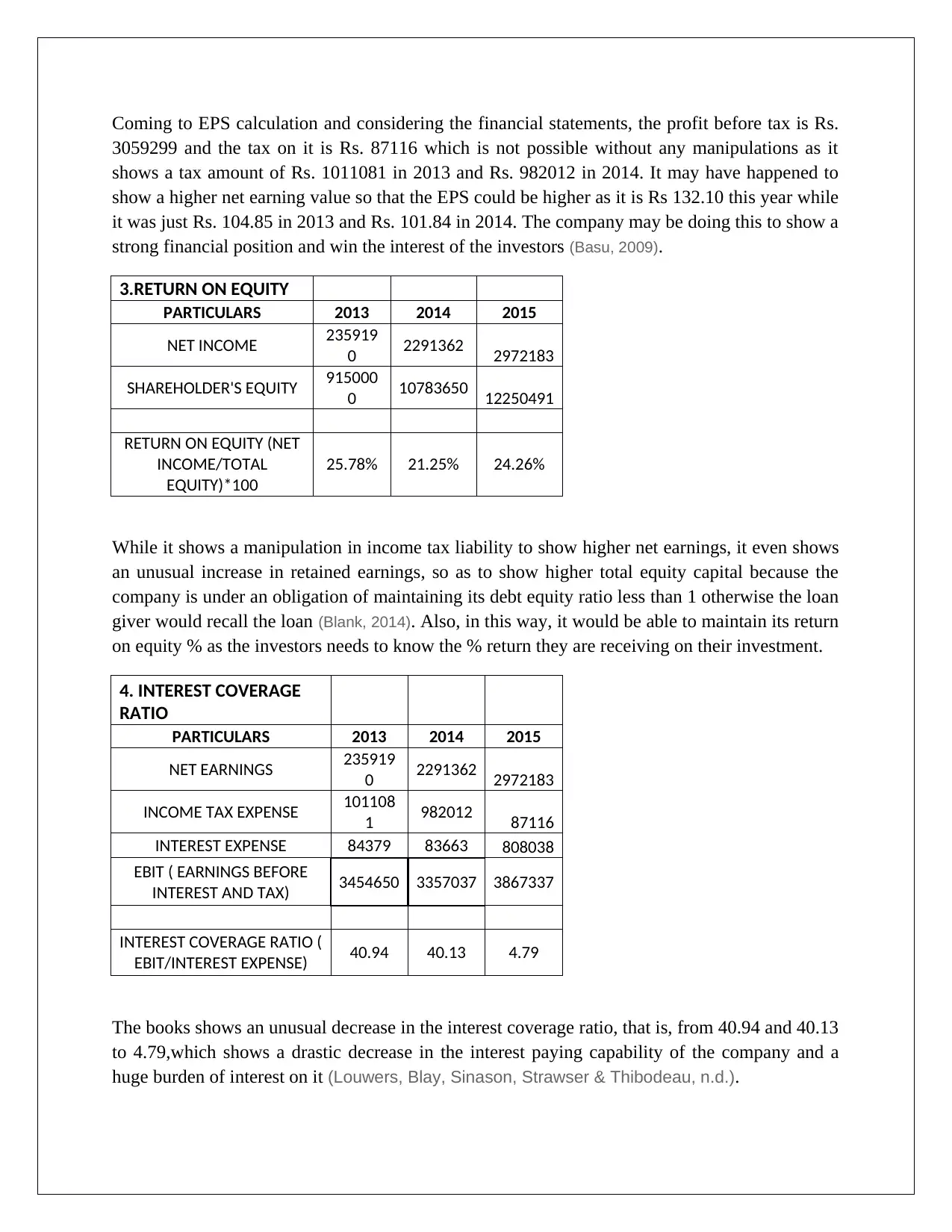

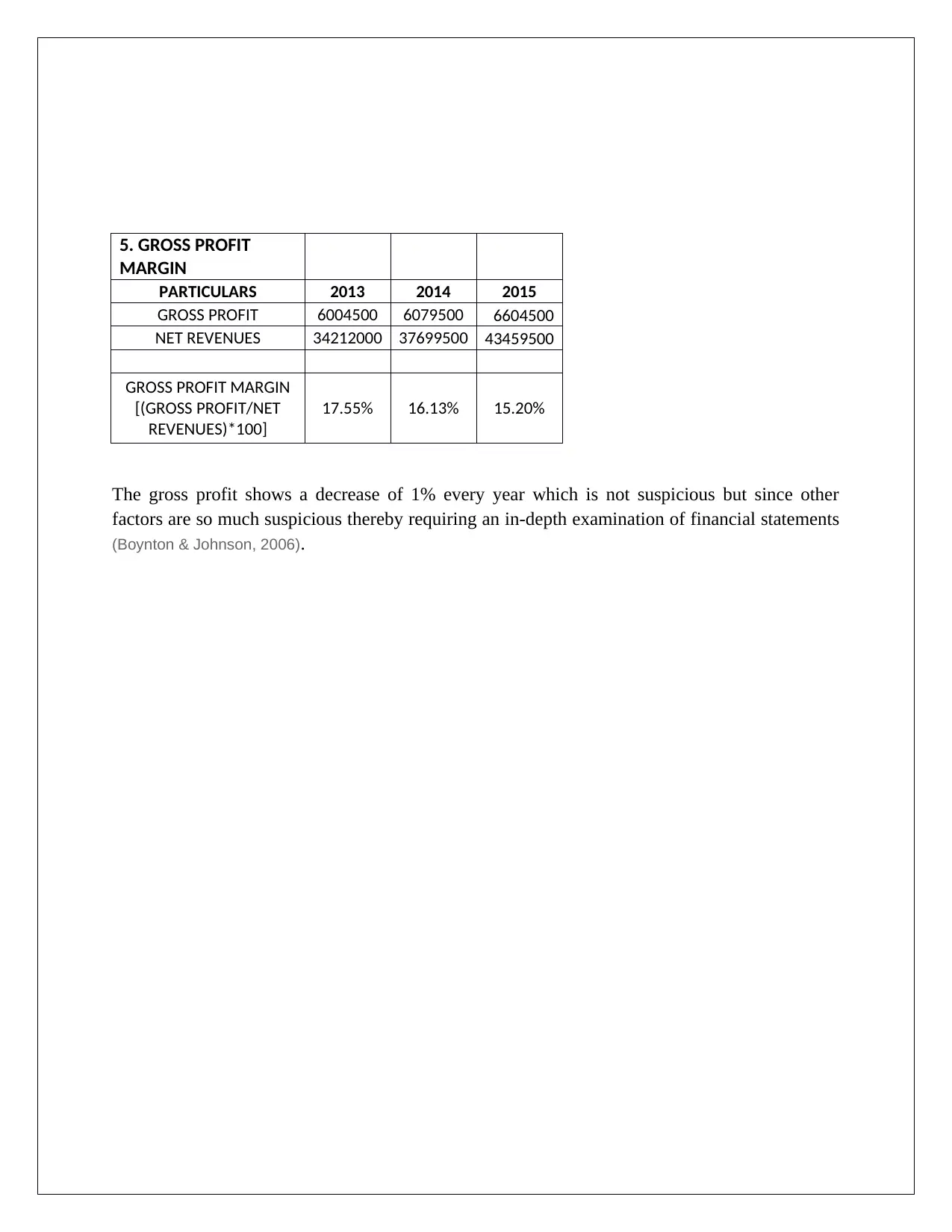

This report presents an audit and assurance analysis of DIPL Ltd.'s financial statements. It begins by examining analytical procedures, including the calculation and interpretation of key financial ratios such as current ratio, EPS, return on equity, interest coverage ratio, and gross profit margin over a three-year period. The analysis reveals potential red flags, including manipulations in tax expenses and earnings per share, unusual changes in the interest coverage ratio, and a declining gross profit margin. The report then delves into risk assessment procedures, identifying inherent risks related to inventory control and cash payment recording. Finally, it explores fraud risk factors within DIPL Ltd., highlighting unusual expenditures, changes in asset depreciation, the acquisition of another firm, and the adoption of a new IT system. The report concludes with a discussion of the potential implications of these findings and relevant references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.