HI6026: Audit, Assurance and Compliance | Assignment

11 Pages2377 Words41 Views

Holmes Institute Sydney

Audit, Assurance and Compliance (HI6026)

Added on 2020-03-02

About This Document

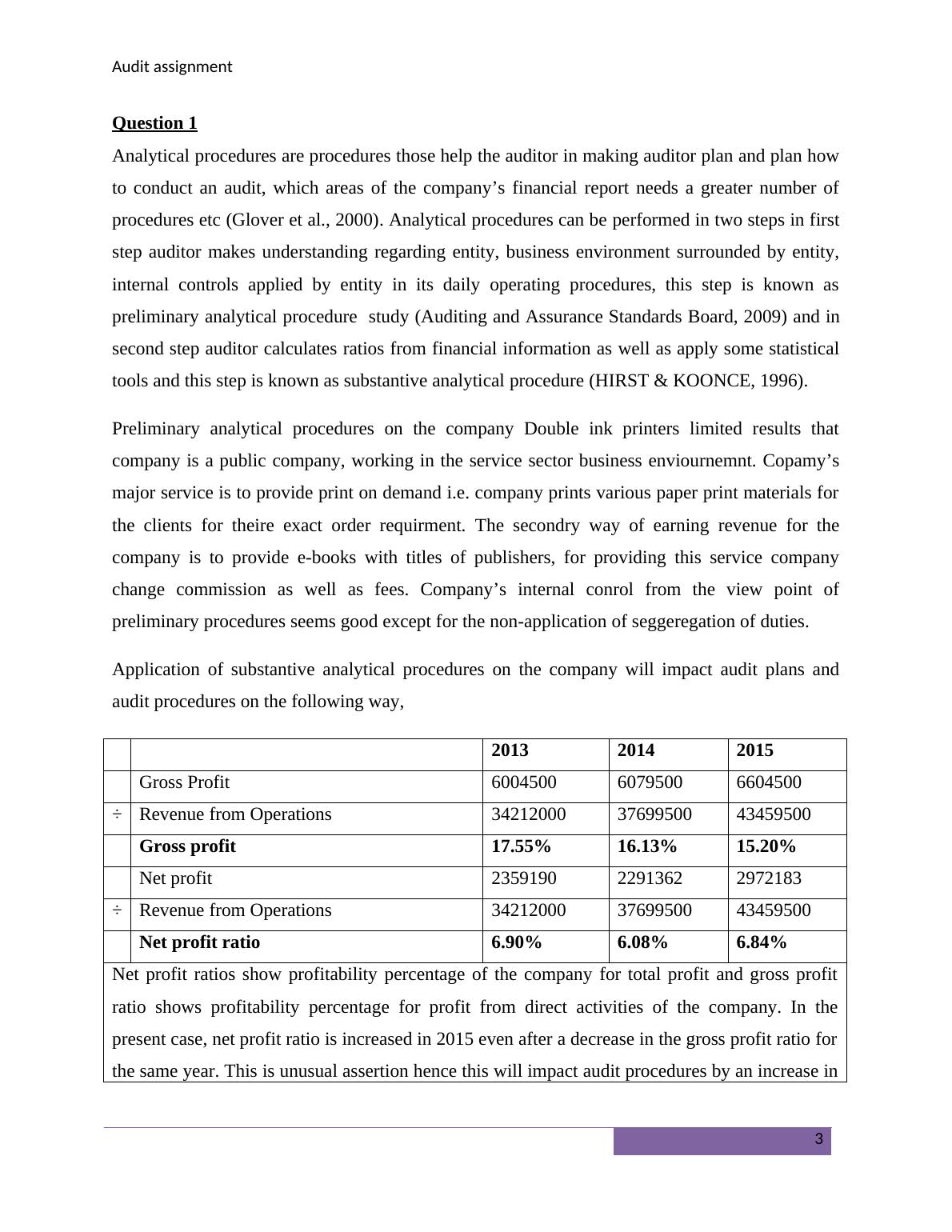

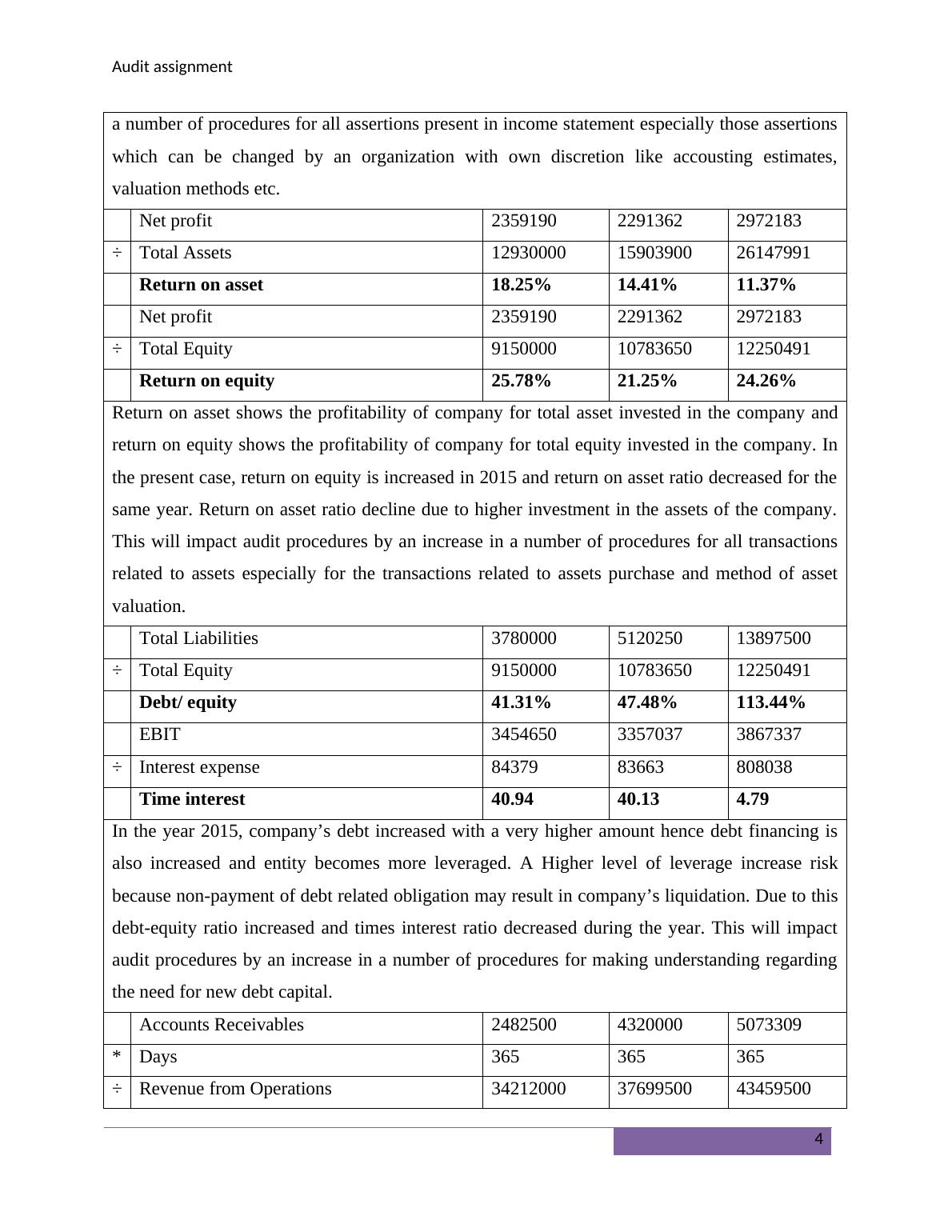

HI6026 - The following document is based on your reading and understanding the document. The paper has some questions answer based on your learnings. The paper has following questions 1. Explain how results influence planning decisions for the audit if analytical procedures to the financial report information of DIPL for the last three year is applied. 2. Conduct risk assessment and find inherent risk factors that arise from the nature of DIPL’s business operations.

HI6026: Audit, Assurance and Compliance | Assignment

Holmes Institute Sydney

Audit, Assurance and Compliance (HI6026)

Added on 2020-03-02

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Analytical Review on Audit Planning for Double Ink Printers Limited

|14

|2717

|309

Report on Auditing and Assurance - HI6026

|13

|2135

|142

Audit - Double Ink Printers Limited | Financial Reports

|8

|1477

|54

HI6026 - Audit, Assurance and Compliance - Case Study

|10

|2515

|43

HI6026 - Audit, Assurance and Compliance, Preliminary Analytical

|8

|2059

|214

HI6026 Audit, Assurance and Compliance | Study

|12

|2632

|58