ACCT20075 - Audit and Ethics Report: CQUniversity, Term 3, 2019

VerifiedAdded on 2022/09/11

|13

|2957

|15

Report

AI Summary

This report provides a detailed analysis of audit and ethics principles, focusing on the QBE Insurance Group's financial statements for the year 2018. The report begins by calculating materiality, considering both quantitative and qualitative aspects, and analyzing the disclosures and notes to the accounts, including reinsurance, deferred tax, and derivatives. Section 2 delves into analytical procedures, computing and analyzing profitability, liquidity, asset management, and leverage ratios to assess the company's financial performance. The report also discusses the risks associated with these ratios and suggests audit procedures to mitigate them. Finally, the report reviews the cash flow statement, highlighting the cash inflows and outflows, and evaluates the auditor's report, providing a comprehensive overview of the audit process and financial analysis.

Running head: AUDIT AND ETHICS

Audit and Ethics

Name of the Student:

Name of the University:

Author’s Note

Audit and Ethics

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT AND ETHICS

Table of Contents

Section 1..........................................................................................................................................2

Computation of Materiality.........................................................................................................2

Analysis of the Disclosures and Note to Accounts......................................................................3

Section 2..........................................................................................................................................4

Analytical Procedures on the Financial statements.....................................................................4

Section 3..........................................................................................................................................8

Review of Cash Flow Statement..................................................................................................8

Review of the Auditor Report......................................................................................................9

Reference.......................................................................................................................................11

AUDIT AND ETHICS

Table of Contents

Section 1..........................................................................................................................................2

Computation of Materiality.........................................................................................................2

Analysis of the Disclosures and Note to Accounts......................................................................3

Section 2..........................................................................................................................................4

Analytical Procedures on the Financial statements.....................................................................4

Section 3..........................................................................................................................................8

Review of Cash Flow Statement..................................................................................................8

Review of the Auditor Report......................................................................................................9

Reference.......................................................................................................................................11

2

AUDIT AND ETHICS

Section 1

Computation of Materiality

The assessment would be going through the different steps which are associated with

audit for a company. The steps which are required to be carried out by the auditor needs to be

planned ahead so that the auditor is well aware of the areas where focus should be so that quality

audit evidences can be collected. One of the important consideration which the auditor needs to

consider is the materiality of the items which are being considered for the purpose of analysis.

The concept of materiality is derived from importance of the item considering the items which

are of relevance which is presented in the annual report. The materiality concept is considered to

be important as the same has an impact on the decision of the senior officials. The entity which

would be the focus for this assessment is QBE insurance Group. In order to review the audit

evidences, the final report of the entity would be considered for the year 2018 (QBE Insurance

Group Ltd.., 2019). The analysis would also be including key financial ratios which might reveal

data regarding the performance.

The materiality concept is known to cover both the qualitative and quantitative aspects

which is related to reporting framework of a business. Qualitative aspects of reporting

incorporate key items which can have a significant impact on the reporting process of the entity.

The quantitative aspects of a business include items which are of material amount and

misstatement of the same would affect the reporting framework of the business (Legoria,

Melendrez & Reynolds, 2013). The emphasis which the auditor would be placing on materiality

would be decided at the time when the auditor formulates an audit plan for the business.

AUDIT AND ETHICS

Section 1

Computation of Materiality

The assessment would be going through the different steps which are associated with

audit for a company. The steps which are required to be carried out by the auditor needs to be

planned ahead so that the auditor is well aware of the areas where focus should be so that quality

audit evidences can be collected. One of the important consideration which the auditor needs to

consider is the materiality of the items which are being considered for the purpose of analysis.

The concept of materiality is derived from importance of the item considering the items which

are of relevance which is presented in the annual report. The materiality concept is considered to

be important as the same has an impact on the decision of the senior officials. The entity which

would be the focus for this assessment is QBE insurance Group. In order to review the audit

evidences, the final report of the entity would be considered for the year 2018 (QBE Insurance

Group Ltd.., 2019). The analysis would also be including key financial ratios which might reveal

data regarding the performance.

The materiality concept is known to cover both the qualitative and quantitative aspects

which is related to reporting framework of a business. Qualitative aspects of reporting

incorporate key items which can have a significant impact on the reporting process of the entity.

The quantitative aspects of a business include items which are of material amount and

misstatement of the same would affect the reporting framework of the business (Legoria,

Melendrez & Reynolds, 2013). The emphasis which the auditor would be placing on materiality

would be decided at the time when the auditor formulates an audit plan for the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT AND ETHICS

In order to achieve the estimates of materiality for each of the items, planning materiality

needs to be computed by the auditor. This estimate is used as a basis to judge tolerable errors and

omission which is present in the financial report of the corporate. The analysis of planning

materiality is generally done considering largest and most material figure in the annual report

and the same is multiplied by an assumed percentage considering the auditing guidelines. In the

case of QBE Insurance Group, the figure of total asset is considered to be the base and the figure

for the same is shown to be US$ 39,582 as per the annual report of 2018. The assumed

percentage which is considered for the purpose of analysis is 2% in this case. The formula and

computation process are shown below:

Planning Materiality=Total Assets × Predetermined Percentage

¿ US $ 39,582 million ×2 %

¿ US$ 791.64 million

The planning materiality for the business of QBE Insurance Group is shown to be US$

761.64 million which would be assisting the auditor to compute performance materiality for the

business (Edgley, Jones & Atkins, 2015). The material misstatements can be identified

considering the materiality estimates which is considered by the auditor.

Analysis of the Disclosures and Note to Accounts

The notes to account for an annual report contains vital information which provides

support to the investors to understand the financial position of the business and also complex

treatments which is undertaken by the management. It is therefore imperative that the

information which is disclosed in the draft notes is accurate. The matters which are covered in

the financial reports for the company is shown below:

AUDIT AND ETHICS

In order to achieve the estimates of materiality for each of the items, planning materiality

needs to be computed by the auditor. This estimate is used as a basis to judge tolerable errors and

omission which is present in the financial report of the corporate. The analysis of planning

materiality is generally done considering largest and most material figure in the annual report

and the same is multiplied by an assumed percentage considering the auditing guidelines. In the

case of QBE Insurance Group, the figure of total asset is considered to be the base and the figure

for the same is shown to be US$ 39,582 as per the annual report of 2018. The assumed

percentage which is considered for the purpose of analysis is 2% in this case. The formula and

computation process are shown below:

Planning Materiality=Total Assets × Predetermined Percentage

¿ US $ 39,582 million ×2 %

¿ US$ 791.64 million

The planning materiality for the business of QBE Insurance Group is shown to be US$

761.64 million which would be assisting the auditor to compute performance materiality for the

business (Edgley, Jones & Atkins, 2015). The material misstatements can be identified

considering the materiality estimates which is considered by the auditor.

Analysis of the Disclosures and Note to Accounts

The notes to account for an annual report contains vital information which provides

support to the investors to understand the financial position of the business and also complex

treatments which is undertaken by the management. It is therefore imperative that the

information which is disclosed in the draft notes is accurate. The matters which are covered in

the financial reports for the company is shown below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT AND ETHICS

Reinsurance and other recoveries on outstanding claims: The amount of reinsurance

amount and other recoveries on outstanding claims. The amount is shown to be $ 5,551

million. The auditor needs to consider the amount and apply appropriate audit procedures

so that the auditor can confirm if the amount is fairly represented in the annual report.

Deferred Tax Assets and Liabilities: The final reports of the entity reveal that there are

certain items of tax which are presented in the draft notes of the annual report. The reason

for occurrence of tax items which is primarily due to carried forward losses of the entity

(Baldauf, Steckel & Steller, 2015). The deferred tax assets and liabilities of the entity

contains complex treatments and therefore the auditor needs to review the same.

Derivatives: The senior officials utilize derivatives for the reason of ensuring that the

risks which is related to currency exchange fluctuations is minimized. The auditing

professional needs to ensure that value of derivatives is appropriately portrayed in the

annual reports and also in the drafts notes for the purpose of ensuring clarity in the

financial reporting framework of the business.

Section 2

Analytical Procedures on the Financial statements

There are variety of tools which is available to an auditor for the reason of collecting

audit signs and ensuring that the performance of the business can be measured simultaneously.

Analytical Review is one such tool which allows an auditor to consider performance metrics for

estimating if every aspect is appropriately reported and whether additional evidences are required

for any particular area (Kristensen, 2015). In the case of QBE insurance group, key financial

AUDIT AND ETHICS

Reinsurance and other recoveries on outstanding claims: The amount of reinsurance

amount and other recoveries on outstanding claims. The amount is shown to be $ 5,551

million. The auditor needs to consider the amount and apply appropriate audit procedures

so that the auditor can confirm if the amount is fairly represented in the annual report.

Deferred Tax Assets and Liabilities: The final reports of the entity reveal that there are

certain items of tax which are presented in the draft notes of the annual report. The reason

for occurrence of tax items which is primarily due to carried forward losses of the entity

(Baldauf, Steckel & Steller, 2015). The deferred tax assets and liabilities of the entity

contains complex treatments and therefore the auditor needs to review the same.

Derivatives: The senior officials utilize derivatives for the reason of ensuring that the

risks which is related to currency exchange fluctuations is minimized. The auditing

professional needs to ensure that value of derivatives is appropriately portrayed in the

annual reports and also in the drafts notes for the purpose of ensuring clarity in the

financial reporting framework of the business.

Section 2

Analytical Procedures on the Financial statements

There are variety of tools which is available to an auditor for the reason of collecting

audit signs and ensuring that the performance of the business can be measured simultaneously.

Analytical Review is one such tool which allows an auditor to consider performance metrics for

estimating if every aspect is appropriately reported and whether additional evidences are required

for any particular area (Kristensen, 2015). In the case of QBE insurance group, key financial

5

AUDIT AND ETHICS

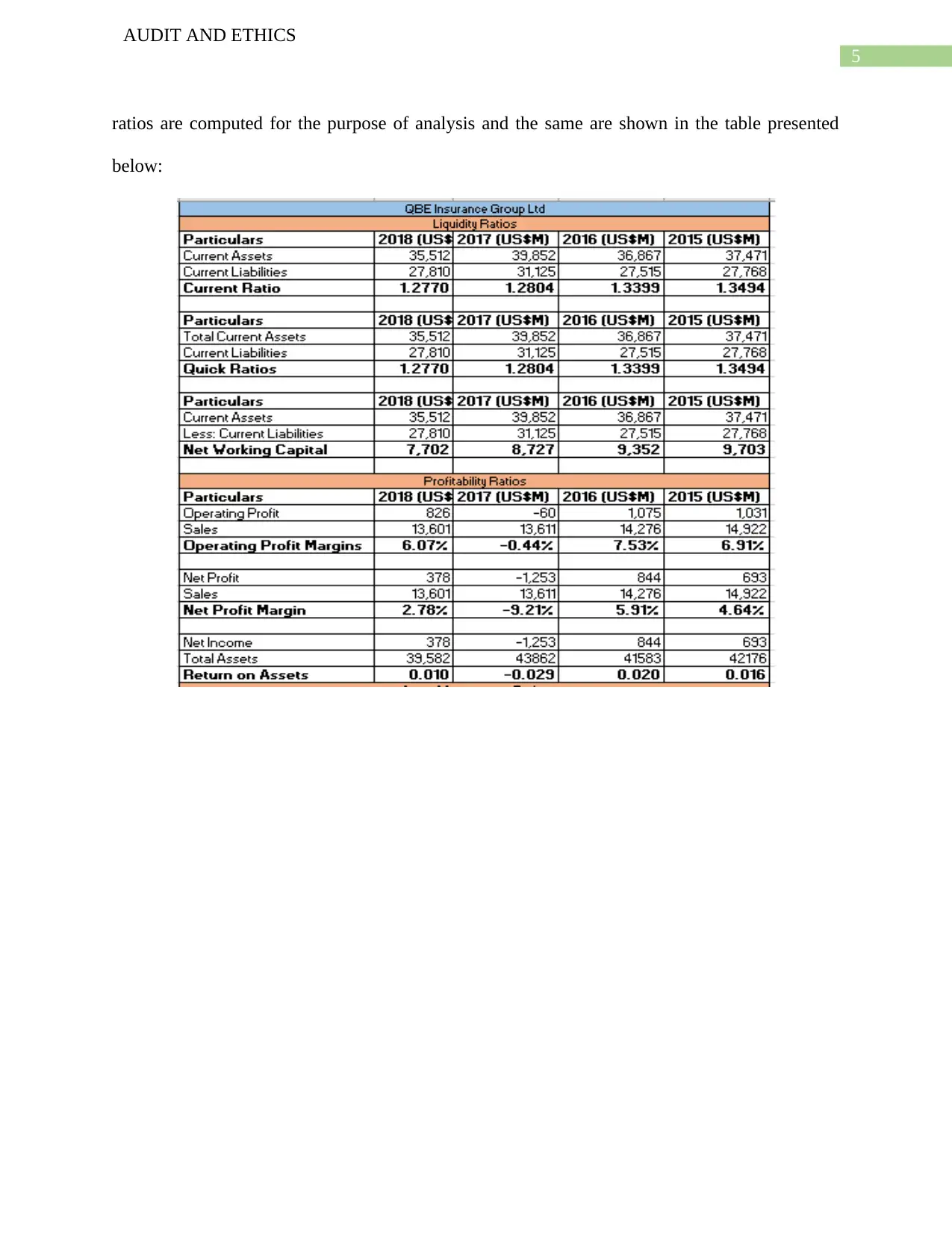

ratios are computed for the purpose of analysis and the same are shown in the table presented

below:

AUDIT AND ETHICS

ratios are computed for the purpose of analysis and the same are shown in the table presented

below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT AND ETHICS

Profitability Ratios

The profitability ratios show the capability of the entity to make profits from the

operations of the business. The corporation of QBE Insurance group principle activity is to

provide insurance coverage and therefore such are considered for the purpose of computing the

operating profit margin for the entity (Omar et al., 2014). The operating profit ratio for the entity

shows tremendous improvements considering the net loss which was suffered by the company in

previous year. The estimate is shown to be 6.07% which is significantly high. In the case of Net

profit margin as well. some improvements are noticed which is computed to be 2.78% during

2018 which suggest that the senior officials are attempting to make up for the losses which is

incurred by the business earlier. The return on assets also shows improvement from previous

year which is a positive factor for the entity. The risks which are associated with the profitability

aspect for a business is that the sales revenue and expenses might be misstated affecting the risks

AUDIT AND ETHICS

Profitability Ratios

The profitability ratios show the capability of the entity to make profits from the

operations of the business. The corporation of QBE Insurance group principle activity is to

provide insurance coverage and therefore such are considered for the purpose of computing the

operating profit margin for the entity (Omar et al., 2014). The operating profit ratio for the entity

shows tremendous improvements considering the net loss which was suffered by the company in

previous year. The estimate is shown to be 6.07% which is significantly high. In the case of Net

profit margin as well. some improvements are noticed which is computed to be 2.78% during

2018 which suggest that the senior officials are attempting to make up for the losses which is

incurred by the business earlier. The return on assets also shows improvement from previous

year which is a positive factor for the entity. The risks which are associated with the profitability

aspect for a business is that the sales revenue and expenses might be misstated affecting the risks

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT AND ETHICS

of the business. The risks can have a direct impact on the profits of the business and affect the

growth of the business.

The auditor in such a case needs to confirm if the results are actual and based on current

performance. The auditor needs to apply vouching practices on the sales revenue and also the

insurance income so as to confirm if the figures actually match up or not. In addition to this, the

auditor also needs to place a close review on the expenses so that it can be confirmed that the

same are genuine. The auditor of the business can advise the management on the areas where

risks have arisen and suggest appropriate internal control procedures so that the risks related to

audit for a business can be managed properly.

Liquidity Ratios

The liquidity ratios for an entity shows the cash situation for the entity and how liquid is

the business for making investments in new projects. The liquidity ratios show current ratio

which has slightly deteriorated which needs to be improved by the senior officials so that the

business has ample cash or liquid cash. In a similar manner, the quick ratio also reveals a decline

which is due to a slight fall in the quick assets of the business. This in terms has also impacted

the working capital of the business. Any deficiency in the liquidity situation of a business can

impact the operations of the business and thereby also affect the revenue generation capacity for

the business. It is to be further noted that the business would not be able to meet the current

obligations of the business if proper control is not maintained

The auditor of the business needs to review the assets and liabilities of current nature of

QBE Insurance group for accuracy and ensuring that no asset or liability is misrepresented in the

financial statement (Delen, Kuzey & Uyar, 2013). The auditor would be applying sampling

technique along with verification procedure so that the accurate picture is available for the

AUDIT AND ETHICS

of the business. The risks can have a direct impact on the profits of the business and affect the

growth of the business.

The auditor in such a case needs to confirm if the results are actual and based on current

performance. The auditor needs to apply vouching practices on the sales revenue and also the

insurance income so as to confirm if the figures actually match up or not. In addition to this, the

auditor also needs to place a close review on the expenses so that it can be confirmed that the

same are genuine. The auditor of the business can advise the management on the areas where

risks have arisen and suggest appropriate internal control procedures so that the risks related to

audit for a business can be managed properly.

Liquidity Ratios

The liquidity ratios for an entity shows the cash situation for the entity and how liquid is

the business for making investments in new projects. The liquidity ratios show current ratio

which has slightly deteriorated which needs to be improved by the senior officials so that the

business has ample cash or liquid cash. In a similar manner, the quick ratio also reveals a decline

which is due to a slight fall in the quick assets of the business. This in terms has also impacted

the working capital of the business. Any deficiency in the liquidity situation of a business can

impact the operations of the business and thereby also affect the revenue generation capacity for

the business. It is to be further noted that the business would not be able to meet the current

obligations of the business if proper control is not maintained

The auditor of the business needs to review the assets and liabilities of current nature of

QBE Insurance group for accuracy and ensuring that no asset or liability is misrepresented in the

financial statement (Delen, Kuzey & Uyar, 2013). The auditor would be applying sampling

technique along with verification procedure so that the accurate picture is available for the

8

AUDIT AND ETHICS

purpose of making judgements. The auditor of the business can advise the management to

supervise the cash inflows and outflows of the business so that cash position of the business can

be controlled.

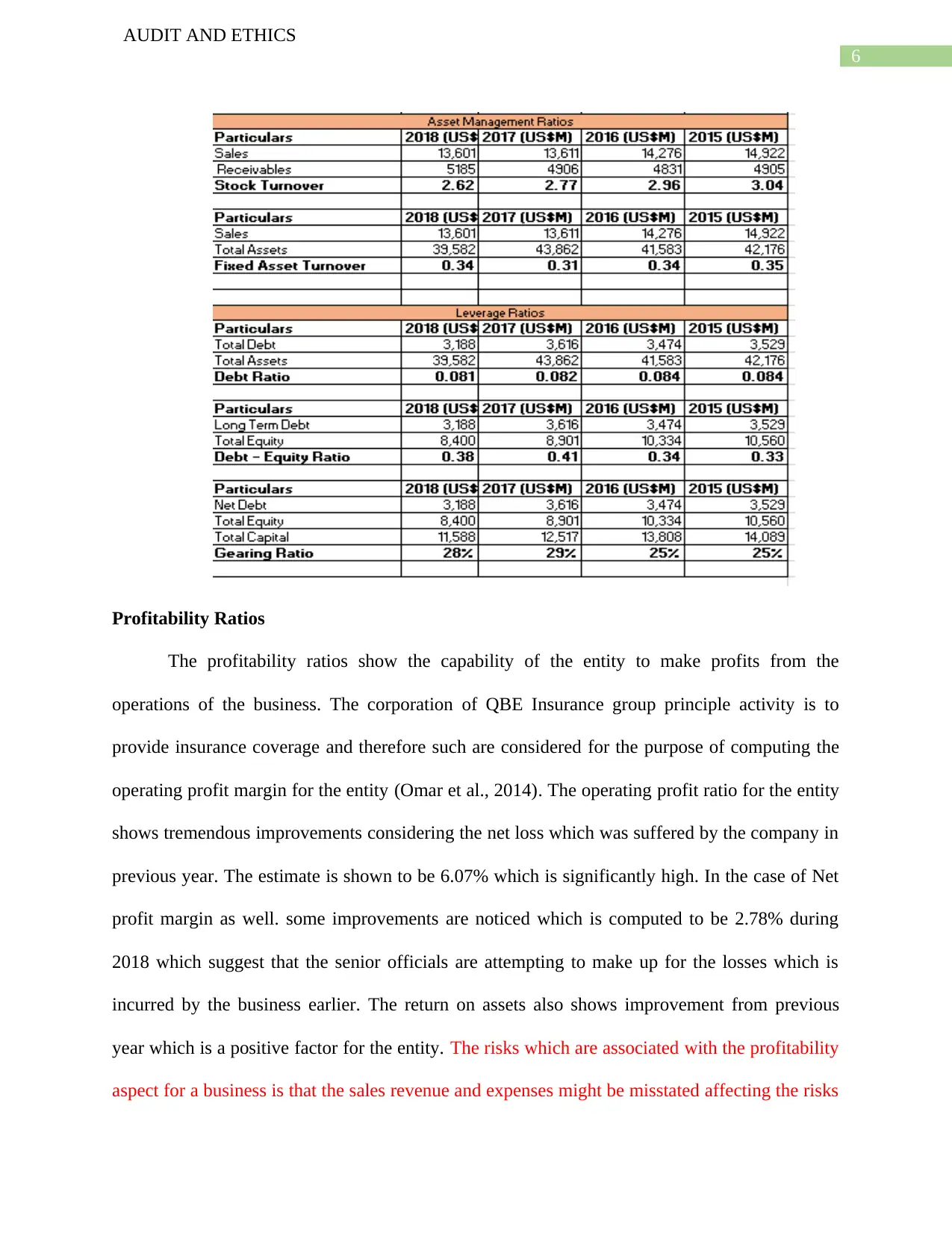

Asset Management Ratios

These ratios forms part of efficiency ratios shows how well a business can manage the

assets so that it can operate for a long time while at the same time generate profits from the

operations. The receivable turnover ratio for QBE Insurance group is shown to be 2.62 in 2018

which shows a decline which is not a good sign for the business and improvements needs to be

made in terms of efficiency. The total asset turnover ratio shows improvements which is a sign

that the senior officials is managing the assets in an appropriate manner for generating desired

amount of revenue from operations of the business. The efficiency position is important as if the

same is impacted in any manner than the same would also be affecting the profitability and

accuracy of the reporting framework of the business.

The auditor in such a case needs to perform verification of the assets so that it can be

established that the assets are proper and the same are represented effectively with accurate

disclosures (Rakićević et al., 2016). The auditor can also take help from an expert for valuing the

insurance assets for estimating the accuracy of the financial reports.

Leverage Ratios

The leverage ratios show the capital composition which is used by the managers for

financing the operations of the entity. In the case of the business of QBE Insurance group, the

debt ratio shows a decline which is a sign that the managers are trying to reduce the debt mix

from the capital structure so that the same can be made more balanced (Faello, 2015). The debt

equity ratio and gearing ratio which is computed for the business also reveal similar information.

AUDIT AND ETHICS

purpose of making judgements. The auditor of the business can advise the management to

supervise the cash inflows and outflows of the business so that cash position of the business can

be controlled.

Asset Management Ratios

These ratios forms part of efficiency ratios shows how well a business can manage the

assets so that it can operate for a long time while at the same time generate profits from the

operations. The receivable turnover ratio for QBE Insurance group is shown to be 2.62 in 2018

which shows a decline which is not a good sign for the business and improvements needs to be

made in terms of efficiency. The total asset turnover ratio shows improvements which is a sign

that the senior officials is managing the assets in an appropriate manner for generating desired

amount of revenue from operations of the business. The efficiency position is important as if the

same is impacted in any manner than the same would also be affecting the profitability and

accuracy of the reporting framework of the business.

The auditor in such a case needs to perform verification of the assets so that it can be

established that the assets are proper and the same are represented effectively with accurate

disclosures (Rakićević et al., 2016). The auditor can also take help from an expert for valuing the

insurance assets for estimating the accuracy of the financial reports.

Leverage Ratios

The leverage ratios show the capital composition which is used by the managers for

financing the operations of the entity. In the case of the business of QBE Insurance group, the

debt ratio shows a decline which is a sign that the managers are trying to reduce the debt mix

from the capital structure so that the same can be made more balanced (Faello, 2015). The debt

equity ratio and gearing ratio which is computed for the business also reveal similar information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT AND ETHICS

This can be regarded as an appropriate step taken by the management for ensuring that the level

of risks of the business is appropriately minimized.

The auditor needs to check the debt capital which is used by the business and if the same

is accurate or not. The auditor also needs to check the figures of equity for confirming that the

value which is portrayed is accurate and there is no misstatement present in the final reports of

the business (Arkan, 2016).

Section 3

Review of Cash Flow Statement

The cash flow statement forms a part of the financial statement and the same portrays the

cash flow for the business which can be inflows as well as outflows. Thee main cash inflows

which is made by the business is from the premiums which is received from the clients and the

main outflows is the claims which the company is required to pay at the time of maturity of the

insurance. The cash flow from operating activities for the year 2018 is shown not to be positive

which may be due to more cash outflows for the period. The cash flow operations show that

company has earned a premium of $ 14,302 million in 2018 which has slightly fallen from

previous year analysis which is shown to be $ 14,565 million. The net cash from operations has

deteriorated significantly as last year the figure was $ 172 million while in 2018 the same is

shown to be in negative and the figure is $ 443 million. The cash which is generated from

investing activities shows that the entity has sold some of the assets for which proceeds has been

generated. The company also has purchased some growth assets and the figure for the same is

shown to be $ 2564 million during the period. This is the main reason that the balance for cash

from investing activities is shown to be appropriate. The cash from financing activities for the

AUDIT AND ETHICS

This can be regarded as an appropriate step taken by the management for ensuring that the level

of risks of the business is appropriately minimized.

The auditor needs to check the debt capital which is used by the business and if the same

is accurate or not. The auditor also needs to check the figures of equity for confirming that the

value which is portrayed is accurate and there is no misstatement present in the final reports of

the business (Arkan, 2016).

Section 3

Review of Cash Flow Statement

The cash flow statement forms a part of the financial statement and the same portrays the

cash flow for the business which can be inflows as well as outflows. Thee main cash inflows

which is made by the business is from the premiums which is received from the clients and the

main outflows is the claims which the company is required to pay at the time of maturity of the

insurance. The cash flow from operating activities for the year 2018 is shown not to be positive

which may be due to more cash outflows for the period. The cash flow operations show that

company has earned a premium of $ 14,302 million in 2018 which has slightly fallen from

previous year analysis which is shown to be $ 14,565 million. The net cash from operations has

deteriorated significantly as last year the figure was $ 172 million while in 2018 the same is

shown to be in negative and the figure is $ 443 million. The cash which is generated from

investing activities shows that the entity has sold some of the assets for which proceeds has been

generated. The company also has purchased some growth assets and the figure for the same is

shown to be $ 2564 million during the period. This is the main reason that the balance for cash

from investing activities is shown to be appropriate. The cash from financing activities for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT AND ETHICS

business also shows a negative balance which is due to the huge repayment of borrowings done

by the management (Gul, Wu & Yang, 2013). In an overall basis, the cash position for the

business has deteriorated for which the senior management needs to take proper steps for

ensuring that the liquidity position for the business is not affected in any manner.

The going concern principle is affected when there are some negative signs for the

business and in the case of QBE Insurance group, no such negative factors can be identified. The

profitability for the business has improved which is an indicator that the business is making

improvements (Lennox, Wu & Zhang, 2014). The liquidity position for the business has declined

slightly but the same can be improved with a little emphasis by the management. It can be said

that the indicators suggest that the going concern principle is not affected and the business would

be continuing its operations for foreseeable future.

Review of the Auditor Report

The annual report for the company for the year 2018 shows that the auditor for the

business is PwC which is regarded as one of the established firms in the field of auditing. The

auditors are of the opinion that the financial reports are showing true and fair view and there is

no material misstatement in the annual reports.

The key audit matters include gross discounted central estimate, valuation of goodwill,

reinsurance and other claims of the business. These items are of complex nature and therefore the

auditor needs to provide special emphasis on such matters.

AUDIT AND ETHICS

business also shows a negative balance which is due to the huge repayment of borrowings done

by the management (Gul, Wu & Yang, 2013). In an overall basis, the cash position for the

business has deteriorated for which the senior management needs to take proper steps for

ensuring that the liquidity position for the business is not affected in any manner.

The going concern principle is affected when there are some negative signs for the

business and in the case of QBE Insurance group, no such negative factors can be identified. The

profitability for the business has improved which is an indicator that the business is making

improvements (Lennox, Wu & Zhang, 2014). The liquidity position for the business has declined

slightly but the same can be improved with a little emphasis by the management. It can be said

that the indicators suggest that the going concern principle is not affected and the business would

be continuing its operations for foreseeable future.

Review of the Auditor Report

The annual report for the company for the year 2018 shows that the auditor for the

business is PwC which is regarded as one of the established firms in the field of auditing. The

auditors are of the opinion that the financial reports are showing true and fair view and there is

no material misstatement in the annual reports.

The key audit matters include gross discounted central estimate, valuation of goodwill,

reinsurance and other claims of the business. These items are of complex nature and therefore the

auditor needs to provide special emphasis on such matters.

11

AUDIT AND ETHICS

Reference

Arkan, T. (2016). The importance of financial ratios in predicting stock price trends: A case

study in emerging markets. Finanse, Rynki Finansowe, Ubezpieczenia, 79(1), 13-26.

Baldauf, J., Steckel, R., & Steller, M. (2015). The Influence of Audit Risk and Materiality

Guidelines on Auditor’s Planning Materiality Assessment. Accounting and Finance

Research, 4(4), 97-114.

Delen, D., Kuzey, C., & Uyar, A. (2013). Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), 3970-3983.

Edgley, C., Jones, M. J., & Atkins, J. (2015). The adoption of the materiality concept in social

and environmental reporting assurance: A field study approach. The British Accounting

Review, 47(1), 1-18.

AUDIT AND ETHICS

Reference

Arkan, T. (2016). The importance of financial ratios in predicting stock price trends: A case

study in emerging markets. Finanse, Rynki Finansowe, Ubezpieczenia, 79(1), 13-26.

Baldauf, J., Steckel, R., & Steller, M. (2015). The Influence of Audit Risk and Materiality

Guidelines on Auditor’s Planning Materiality Assessment. Accounting and Finance

Research, 4(4), 97-114.

Delen, D., Kuzey, C., & Uyar, A. (2013). Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), 3970-3983.

Edgley, C., Jones, M. J., & Atkins, J. (2015). The adoption of the materiality concept in social

and environmental reporting assurance: A field study approach. The British Accounting

Review, 47(1), 1-18.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.