Financial Audit Analysis: Medibank Private Ltd's Annual Report Review

VerifiedAdded on 2023/02/01

|12

|2529

|22

Report

AI Summary

This report provides a comprehensive audit analysis of Medibank Private Ltd, focusing on its financial statements. It begins by explaining the concept of materiality and its application in auditing, particularly in the context of Medibank's financial reporting. The report then examines the notes and disclosures within Medibank's annual reports, highlighting key areas like deferred acquisition costs and contingent liabilities. Analytical procedures, including ratio analysis (current, quick, net profit margin, etc.), are applied to assess the company's liquidity and profitability. A detailed analysis of the cash flow statement, outlining cash inflows and outflows from operations, investment, and financing activities, is also included. The report concludes with an analysis of the auditor's report, assessing the audit opinion and the company's adherence to accounting standards, ultimately providing an overview of Medibank's financial performance and position, based on the audit perspective. The report is a student submission to Desklib.

Running head: AUDIT

Audit

Name of the Student:

Name of the University:

Author’s Note

Audit

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT

Table of Contents

Introduction...............................................................................................................................2

Discussion..................................................................................................................................2

Materiality Concept...............................................................................................................2

Draft Notes and Disclosures..................................................................................................3

Application of Analytical Procedures...................................................................................4

Analysis of the Cash Flow Statement....................................................................................6

Analysis of the Auditor’s Report...........................................................................................8

Conclusion.................................................................................................................................9

Reference.................................................................................................................................10

AUDIT

Table of Contents

Introduction...............................................................................................................................2

Discussion..................................................................................................................................2

Materiality Concept...............................................................................................................2

Draft Notes and Disclosures..................................................................................................3

Application of Analytical Procedures...................................................................................4

Analysis of the Cash Flow Statement....................................................................................6

Analysis of the Auditor’s Report...........................................................................................8

Conclusion.................................................................................................................................9

Reference.................................................................................................................................10

2

AUDIT

Introduction

The main purpose of the assessment is to analyze the business of Medibank Private Ltd

which is engaged in the business of providing insurance products to the customers of Australia.

The assessment would be considering the financial statements of the business from the

perspective of audit and assess what level of materiality is considered by the management of the

company (Asx.com.au., 2019). The assessment would also be assessing the notes and disclosures

which are presented in the annual reports of the business. The analysis would also be showing

key financial ratios of the business for the period of three years. The analysis of ratios would be

identifying certain areas of performance of the business. The analysis would also be assessing

the audit opinion which provided by the auditor of the business.

Discussion

Materiality Concept

The concept of materiality states that the auditor of a business must considers items

which are of significance to the users of the financial statements. The materiality of an item is on

the judgement of the auditor of the business and it is on the basis of this judgment that the

auditor decides how much audit procedures is to be applied to an item for collecting sufficient

and appropriate audit evidences (Kumar & Sharma, 2015). The items which are significant for a

business is considered to be material in nature. Similarly, items which are complex in nature are

also considered to be material in some respect and also items which are shown to be of high

value as demonstrated in the financial statements of the company.

In order to assess the items which are presented in the annual reports of the business, the

concept of planning materiality is considered. In order to arrive at the estimate of planning

AUDIT

Introduction

The main purpose of the assessment is to analyze the business of Medibank Private Ltd

which is engaged in the business of providing insurance products to the customers of Australia.

The assessment would be considering the financial statements of the business from the

perspective of audit and assess what level of materiality is considered by the management of the

company (Asx.com.au., 2019). The assessment would also be assessing the notes and disclosures

which are presented in the annual reports of the business. The analysis would also be showing

key financial ratios of the business for the period of three years. The analysis of ratios would be

identifying certain areas of performance of the business. The analysis would also be assessing

the audit opinion which provided by the auditor of the business.

Discussion

Materiality Concept

The concept of materiality states that the auditor of a business must considers items

which are of significance to the users of the financial statements. The materiality of an item is on

the judgement of the auditor of the business and it is on the basis of this judgment that the

auditor decides how much audit procedures is to be applied to an item for collecting sufficient

and appropriate audit evidences (Kumar & Sharma, 2015). The items which are significant for a

business is considered to be material in nature. Similarly, items which are complex in nature are

also considered to be material in some respect and also items which are shown to be of high

value as demonstrated in the financial statements of the company.

In order to assess the items which are presented in the annual reports of the business, the

concept of planning materiality is considered. In order to arrive at the estimate of planning

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT

materiality, the auditor takes the highest value which is presented in the annual reports of the

business and which according to the auditor will make an efficient base for computing planning

materiality of the business (Krishnan & Wang, 2014). The figure of sales is considered for the

business of Medibank Private Ltd. The percentage which is considered by the auditor of the

business is 2% for estimating the planning materiality of the business. The computation of

planning materiality of the business is shown in the equation below:

Planning Materiality=Total Assets of the Company × Percentage estimated

¿ $ 6319.5 million ×2 %

¿ $ 126.39 millions

The planning materiality of the business which is computed is shown to be $ 126.39% on the

basis of which performance materiality of the business would be computed. The performance

materiality of different items is estimated considering planning materiality of the business.

Draft Notes and Disclosures

The notes to accounts of a business also forms a part of the financial statements of the

business and contains explanation and disclosures regarding treatments and transactions of the

business. The management of Medibank ltd has paid special attention while preparing the notes

to accounts of the business and the significant disclosures which are provided in the annual

reports of the business are discussed below in details:

Deferred Acquisition Costs: These are the costs which are incurred in obtaining health

insurance contracts which are deferred and recognize assets which can be effectively

measured by the management. These types of costs are systematically amortized over the

AUDIT

materiality, the auditor takes the highest value which is presented in the annual reports of the

business and which according to the auditor will make an efficient base for computing planning

materiality of the business (Krishnan & Wang, 2014). The figure of sales is considered for the

business of Medibank Private Ltd. The percentage which is considered by the auditor of the

business is 2% for estimating the planning materiality of the business. The computation of

planning materiality of the business is shown in the equation below:

Planning Materiality=Total Assets of the Company × Percentage estimated

¿ $ 6319.5 million ×2 %

¿ $ 126.39 millions

The planning materiality of the business which is computed is shown to be $ 126.39% on the

basis of which performance materiality of the business would be computed. The performance

materiality of different items is estimated considering planning materiality of the business.

Draft Notes and Disclosures

The notes to accounts of a business also forms a part of the financial statements of the

business and contains explanation and disclosures regarding treatments and transactions of the

business. The management of Medibank ltd has paid special attention while preparing the notes

to accounts of the business and the significant disclosures which are provided in the annual

reports of the business are discussed below in details:

Deferred Acquisition Costs: These are the costs which are incurred in obtaining health

insurance contracts which are deferred and recognize assets which can be effectively

measured by the management. These types of costs are systematically amortized over the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT

average expected retention period of the asset. The auditor of the business needs to assess

whether the amounts for the same are appropriate or not and whether appropriate

amortization charges are allowed on the costs.

Working Capital: The management of the company is required to maintain an

appropriate level of cash in the business in order to support the operations of the business.

The cash flow statement shows the cash from operations is shown to be positive (Byrnes

et al., 2018). The auditor of the business needs to check whether the cash transactions are

proper and ensure that there is material misstatement in the financial reports which is

prepared by the business.

Contingent Liability: The notes to account section shows that there is a contingent

liability which I appropriately disclosed in the annual reports of the business which also

means that the business has recognized a chance of loss from the same and therefore

appropriate scrutiny of the situation is to be done by the auditor of the business. The first

step which the auditor needs to assess is that whether the occurrence of the contingent

liability affect the revenue generation of the business.

Application of Analytical Procedures

Analytical procedures is a technique which is used in auditing is for identifying whether

the financial statements are showing true information and whether the same are mathematically

correct. Analytical procedures apply some of quantitative tools such as ratio analysis, trend

analysis. In the case of Medibank Private ltd, the financial statement of 2018 is considered for

analysis and key financial ratios are computed in order to ascertain the profitability and liquidity

of the business are appropriate or not.

AUDIT

average expected retention period of the asset. The auditor of the business needs to assess

whether the amounts for the same are appropriate or not and whether appropriate

amortization charges are allowed on the costs.

Working Capital: The management of the company is required to maintain an

appropriate level of cash in the business in order to support the operations of the business.

The cash flow statement shows the cash from operations is shown to be positive (Byrnes

et al., 2018). The auditor of the business needs to check whether the cash transactions are

proper and ensure that there is material misstatement in the financial reports which is

prepared by the business.

Contingent Liability: The notes to account section shows that there is a contingent

liability which I appropriately disclosed in the annual reports of the business which also

means that the business has recognized a chance of loss from the same and therefore

appropriate scrutiny of the situation is to be done by the auditor of the business. The first

step which the auditor needs to assess is that whether the occurrence of the contingent

liability affect the revenue generation of the business.

Application of Analytical Procedures

Analytical procedures is a technique which is used in auditing is for identifying whether

the financial statements are showing true information and whether the same are mathematically

correct. Analytical procedures apply some of quantitative tools such as ratio analysis, trend

analysis. In the case of Medibank Private ltd, the financial statement of 2018 is considered for

analysis and key financial ratios are computed in order to ascertain the profitability and liquidity

of the business are appropriate or not.

5

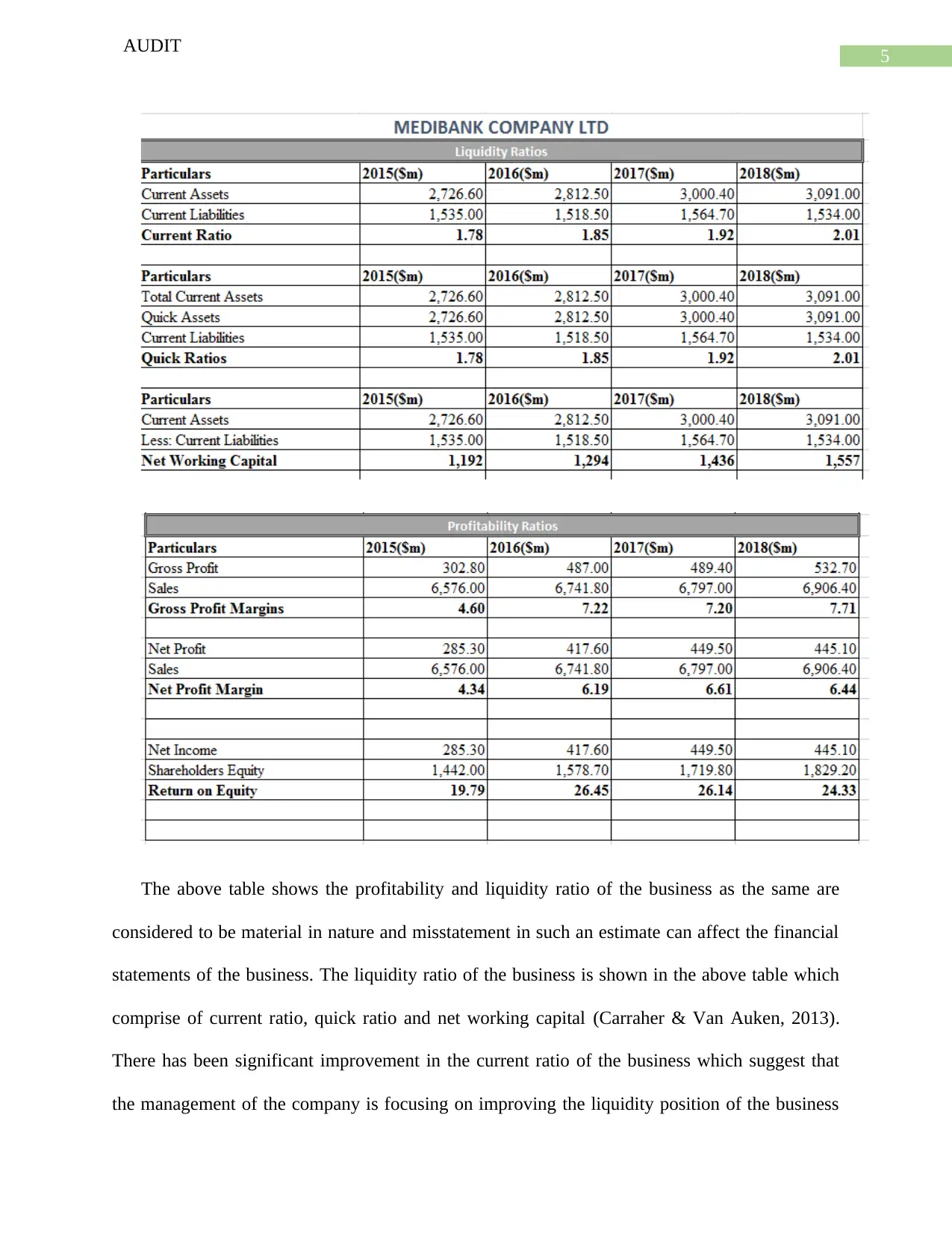

AUDIT

The above table shows the profitability and liquidity ratio of the business as the same are

considered to be material in nature and misstatement in such an estimate can affect the financial

statements of the business. The liquidity ratio of the business is shown in the above table which

comprise of current ratio, quick ratio and net working capital (Carraher & Van Auken, 2013).

There has been significant improvement in the current ratio of the business which suggest that

the management of the company is focusing on improving the liquidity position of the business

AUDIT

The above table shows the profitability and liquidity ratio of the business as the same are

considered to be material in nature and misstatement in such an estimate can affect the financial

statements of the business. The liquidity ratio of the business is shown in the above table which

comprise of current ratio, quick ratio and net working capital (Carraher & Van Auken, 2013).

There has been significant improvement in the current ratio of the business which suggest that

the management of the company is focusing on improving the liquidity position of the business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT

which is quite natural as the business is a bank. The net working capital of the bank is shown to

be favourable and the same is shown to be on the rise which shows that bank is conducting its

operations well and has enough capital for financing any project which the management of the

business wishes.

The profitability ratio of the business shows net profit margin, gross profit margin and return

on equity which are all considered to be financial indicators of success for a business. The net

profit margin of the business is shown to have slightly fallen which is mainly due to more

expenses which is incurred by the business. The auditor need to assess the balances of revenues

and expenses by applying vouching procedures (Christensen, Glover & Wood, 2013). The

balances for expenses needs to be assessed by the auditor in order to ensure that the same are

accurately presented by the management of the company. The profitability ratio of the business

shows that there has been significant increase in the same which shows that the business is

performing well in the market.

Analysis of the Cash Flow Statement

The cash flow statement forms a part of the financial statements of the business and the

same effectively represents the cash inflows and outflows of a business. In other words, the cash

flow statements effectively portray the liquidity position of a business and also classifies the

activities of the business on the cash from operations, cash from investment and cash from

financing (William Jr, Glover & Prawitt, 2016). The company which is considered Medibank

Private ltd has effectively presented the cash flow statement in the ann8ual report of the business

in a generally accepted format. An extract of the cash flow statement of the business is shown

below:

AUDIT

which is quite natural as the business is a bank. The net working capital of the bank is shown to

be favourable and the same is shown to be on the rise which shows that bank is conducting its

operations well and has enough capital for financing any project which the management of the

business wishes.

The profitability ratio of the business shows net profit margin, gross profit margin and return

on equity which are all considered to be financial indicators of success for a business. The net

profit margin of the business is shown to have slightly fallen which is mainly due to more

expenses which is incurred by the business. The auditor need to assess the balances of revenues

and expenses by applying vouching procedures (Christensen, Glover & Wood, 2013). The

balances for expenses needs to be assessed by the auditor in order to ensure that the same are

accurately presented by the management of the company. The profitability ratio of the business

shows that there has been significant increase in the same which shows that the business is

performing well in the market.

Analysis of the Cash Flow Statement

The cash flow statement forms a part of the financial statements of the business and the

same effectively represents the cash inflows and outflows of a business. In other words, the cash

flow statements effectively portray the liquidity position of a business and also classifies the

activities of the business on the cash from operations, cash from investment and cash from

financing (William Jr, Glover & Prawitt, 2016). The company which is considered Medibank

Private ltd has effectively presented the cash flow statement in the ann8ual report of the business

in a generally accepted format. An extract of the cash flow statement of the business is shown

below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

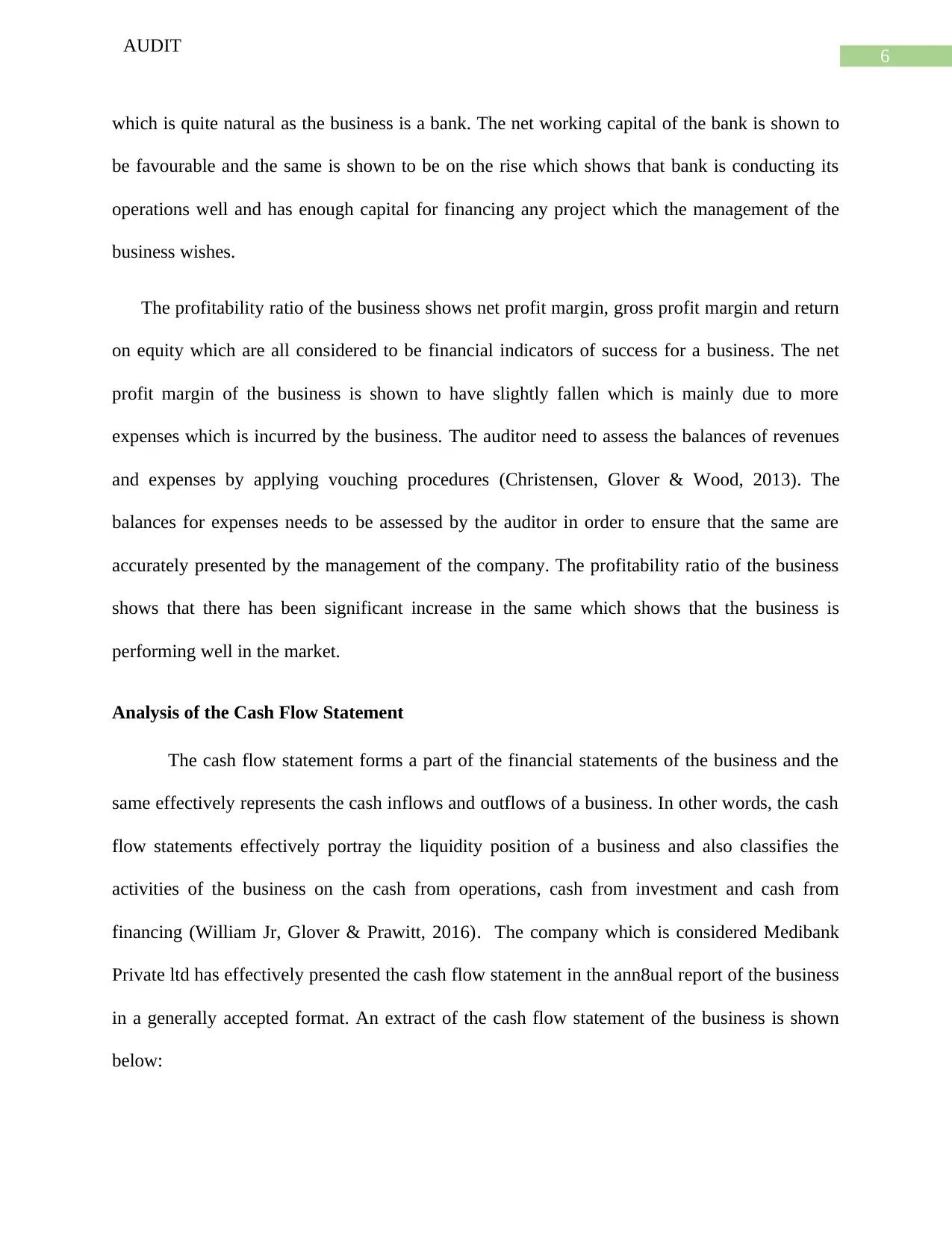

AUDIT

Figure 1: Cash flow Statement of Medibank Private ltd

Source: (Asx.com.au. 2019)

The cash flow statement effectively shows all the activities of the business which is

related to the operations of the business and also the cash inflows and outflows of the business

during the period. The major source of cash inflow for the business is shown to be from premium

received from the clients while major outflows is shown to be claim payments which is paid by

the bank (Hay, Knechel & Willekens, 2014). The cash from operating activities of the business is

shown to be higher than previous year which suggest that the business has improved its

AUDIT

Figure 1: Cash flow Statement of Medibank Private ltd

Source: (Asx.com.au. 2019)

The cash flow statement effectively shows all the activities of the business which is

related to the operations of the business and also the cash inflows and outflows of the business

during the period. The major source of cash inflow for the business is shown to be from premium

received from the clients while major outflows is shown to be claim payments which is paid by

the bank (Hay, Knechel & Willekens, 2014). The cash from operating activities of the business is

shown to be higher than previous year which suggest that the business has improved its

8

AUDIT

operational level. The payment receipts of the business is shown to have increased from $

6,278.8 million to around $ 6,355.5 million which shows that there has been significant amount

of increase in the cash inflows which is generated by the business. The cash receipts of the

business are appropriate which is the main reason due to which there is a positive cash inflow for

the business (Knechel & Salterio, 2016). The major investing activities which is portrayed in the

cash flow statement is sale of land and buildings and purchases of assets in order to carry out its

business more efficiently. The major activity which is undertaken by the management of the

company in terms of financing activities reflect the dividends which is paid by the management

of the company during the period.

The going concern principle of a business is important in determining whether the annual

reports are prepared for a continuity basis. The principles that the business which is preparing

financial reports are preparing it with the intention that they want to continue their operations

with the intention of earning more profits for the business (Oprisor, 2015). The principle is of

significant importance to an auditor as well in forming an opinion on the financial statements of

the business. In other words, the principle means that the business which is conducting its

operations has no intention of stooping the process. The annual report of Medibank Private ltd

shows that the performance of the business is favourable in terms of profitability, efficiency and

liquidity position of the business (Sandvig et al., 2014). Therefore, it can be said that there are no

signs that the principle of going concern of the business might be affected in any manner. The

company is also positively responding to the needs of the shareholders and this shows that the

interest of the shareholders is considered which suggest that the business is still developing.

AUDIT

operational level. The payment receipts of the business is shown to have increased from $

6,278.8 million to around $ 6,355.5 million which shows that there has been significant amount

of increase in the cash inflows which is generated by the business. The cash receipts of the

business are appropriate which is the main reason due to which there is a positive cash inflow for

the business (Knechel & Salterio, 2016). The major investing activities which is portrayed in the

cash flow statement is sale of land and buildings and purchases of assets in order to carry out its

business more efficiently. The major activity which is undertaken by the management of the

company in terms of financing activities reflect the dividends which is paid by the management

of the company during the period.

The going concern principle of a business is important in determining whether the annual

reports are prepared for a continuity basis. The principles that the business which is preparing

financial reports are preparing it with the intention that they want to continue their operations

with the intention of earning more profits for the business (Oprisor, 2015). The principle is of

significant importance to an auditor as well in forming an opinion on the financial statements of

the business. In other words, the principle means that the business which is conducting its

operations has no intention of stooping the process. The annual report of Medibank Private ltd

shows that the performance of the business is favourable in terms of profitability, efficiency and

liquidity position of the business (Sandvig et al., 2014). Therefore, it can be said that there are no

signs that the principle of going concern of the business might be affected in any manner. The

company is also positively responding to the needs of the shareholders and this shows that the

interest of the shareholders is considered which suggest that the business is still developing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT

Analysis of the Auditor’s Report

As per the opinion of the auditor of the business the financial statements are effectively

represented which follows all rules and regulations of Australian Accounting standards. The

annual reports also follow all relevant accounting standards and provisions of Corporation Act

2001 of Australia. This signifies that the auditor has issued an unqualified audit report to the

company signifying everything is all right with the annual reports of the business. This also

means that the financial statements of the business are showing a true and fair view of the

financial situation of the business (Nuijten, van Twist & van der Steen, 2015). As per the annual

report of the business, there are no additional paragraphs included in the financial statements of

the business. This is another positive sign for the business.

Conclusion

The analysis of the financial position of the business of Medibank Private ltd reveals that the

business is doing well in current market and there is still scope for more development for the

business. The above analysis shows concept and application of materiality for determining the

significance of the items which are material in nature. The above discussion also includes ratio

analysis and identification of key area of performance for the business. The assessment also

shows that cash flow statement of Medibank Private ltd and the nature of the audit opinion which

is provided in the annual reports of the business.

AUDIT

Analysis of the Auditor’s Report

As per the opinion of the auditor of the business the financial statements are effectively

represented which follows all rules and regulations of Australian Accounting standards. The

annual reports also follow all relevant accounting standards and provisions of Corporation Act

2001 of Australia. This signifies that the auditor has issued an unqualified audit report to the

company signifying everything is all right with the annual reports of the business. This also

means that the financial statements of the business are showing a true and fair view of the

financial situation of the business (Nuijten, van Twist & van der Steen, 2015). As per the annual

report of the business, there are no additional paragraphs included in the financial statements of

the business. This is another positive sign for the business.

Conclusion

The analysis of the financial position of the business of Medibank Private ltd reveals that the

business is doing well in current market and there is still scope for more development for the

business. The above analysis shows concept and application of materiality for determining the

significance of the items which are material in nature. The above discussion also includes ratio

analysis and identification of key area of performance for the business. The assessment also

shows that cash flow statement of Medibank Private ltd and the nature of the audit opinion which

is provided in the annual reports of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT

Reference

Asx.com.au. (2019). Retrieved 5 May 2019, from https://www.asx.com.au/asx/share-price-

research/company/MPL

Byrnes, P. E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J. D., &

Vasarhelyi, M. (2018). Evolution of Auditing: From the Traditional Approach to the

Future Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297). Emerald

Publishing Limited.

Carraher, S. & Van Auken, H., (2013). The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Christensen, B.E., Glover, S.M. & Wood, D.A., (2013). Extreme estimation uncertainty and

audit assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Hay, D., Knechel, W. R., & Willekens, M. (Eds.). (2014). The Routledge companion to auditing.

Routledge.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Krishnan, G.V. & Wang, C., (2014). The relation between managerial ability and audit fees and

going concern opinions. Auditing: A Journal of Practice & Theory, 34(3), pp.139-160.

Kumar, R., & Sharma, V. (2015). Auditing: Principles and practice. PHI Learning Pvt. Ltd..

AUDIT

Reference

Asx.com.au. (2019). Retrieved 5 May 2019, from https://www.asx.com.au/asx/share-price-

research/company/MPL

Byrnes, P. E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J. D., &

Vasarhelyi, M. (2018). Evolution of Auditing: From the Traditional Approach to the

Future Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297). Emerald

Publishing Limited.

Carraher, S. & Van Auken, H., (2013). The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Christensen, B.E., Glover, S.M. & Wood, D.A., (2013). Extreme estimation uncertainty and

audit assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Hay, D., Knechel, W. R., & Willekens, M. (Eds.). (2014). The Routledge companion to auditing.

Routledge.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Krishnan, G.V. & Wang, C., (2014). The relation between managerial ability and audit fees and

going concern opinions. Auditing: A Journal of Practice & Theory, 34(3), pp.139-160.

Kumar, R., & Sharma, V. (2015). Auditing: Principles and practice. PHI Learning Pvt. Ltd..

11

AUDIT

Nuijten, A., van Twist, M., & van der Steen, M. (2015). Auditing interactive complexity:

Challenges for the internal audit profession. International Journal of Auditing, 19(3),

195-205.

Oprisor, T. (2015). Auditing integrated reports: Are there solutions to this puzzle?. Procedia

Economics and Finance, 25, 87-95.

Sandvig, C., Hamilton, K., Karahalios, K., & Langbort, C. (2014). Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

AUDIT

Nuijten, A., van Twist, M., & van der Steen, M. (2015). Auditing interactive complexity:

Challenges for the internal audit profession. International Journal of Auditing, 19(3),

195-205.

Oprisor, T. (2015). Auditing integrated reports: Are there solutions to this puzzle?. Procedia

Economics and Finance, 25, 87-95.

Sandvig, C., Hamilton, K., Karahalios, K., & Langbort, C. (2014). Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.