Auditing and Assurance in Various Contexts

VerifiedAdded on 2020/03/02

|15

|3083

|131

AI Summary

The assignment delves into the concept of auditing and assurance, examining its application in diverse fields. It includes a discussion on the audit process, the role of auditors, and various types of audits conducted. The text analyzes case studies illustrating audits in areas such as clinical research, project management, and financial institutions. Furthermore, it explores the challenges faced by auditors and the importance of maintaining objectivity and integrity.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDIT ASSURANCE AND COMPLIANCE

Audit Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Audit Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

AUDIT ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question No 1................................................................................................................2

(a) Application of analytical procedure to the financial report information of DIPL............2

(b) Impact of analytical review on the audit planning for the year ended 30th June 2015...........5

Answer to Question 2......................................................................................................................7

Answer to Question No 3................................................................................................................9

(a) Key risk factors related to the misstatement in the financial reporting............................9

(b) Effect of risk on the conduct of audit..............................................................................10

Reference List................................................................................................................................11

Bibliography..................................................................................................................................13

AUDIT ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question No 1................................................................................................................2

(a) Application of analytical procedure to the financial report information of DIPL............2

(b) Impact of analytical review on the audit planning for the year ended 30th June 2015...........5

Answer to Question 2......................................................................................................................7

Answer to Question No 3................................................................................................................9

(a) Key risk factors related to the misstatement in the financial reporting............................9

(b) Effect of risk on the conduct of audit..............................................................................10

Reference List................................................................................................................................11

Bibliography..................................................................................................................................13

2

AUDIT ASSURANCE AND COMPLIANCE

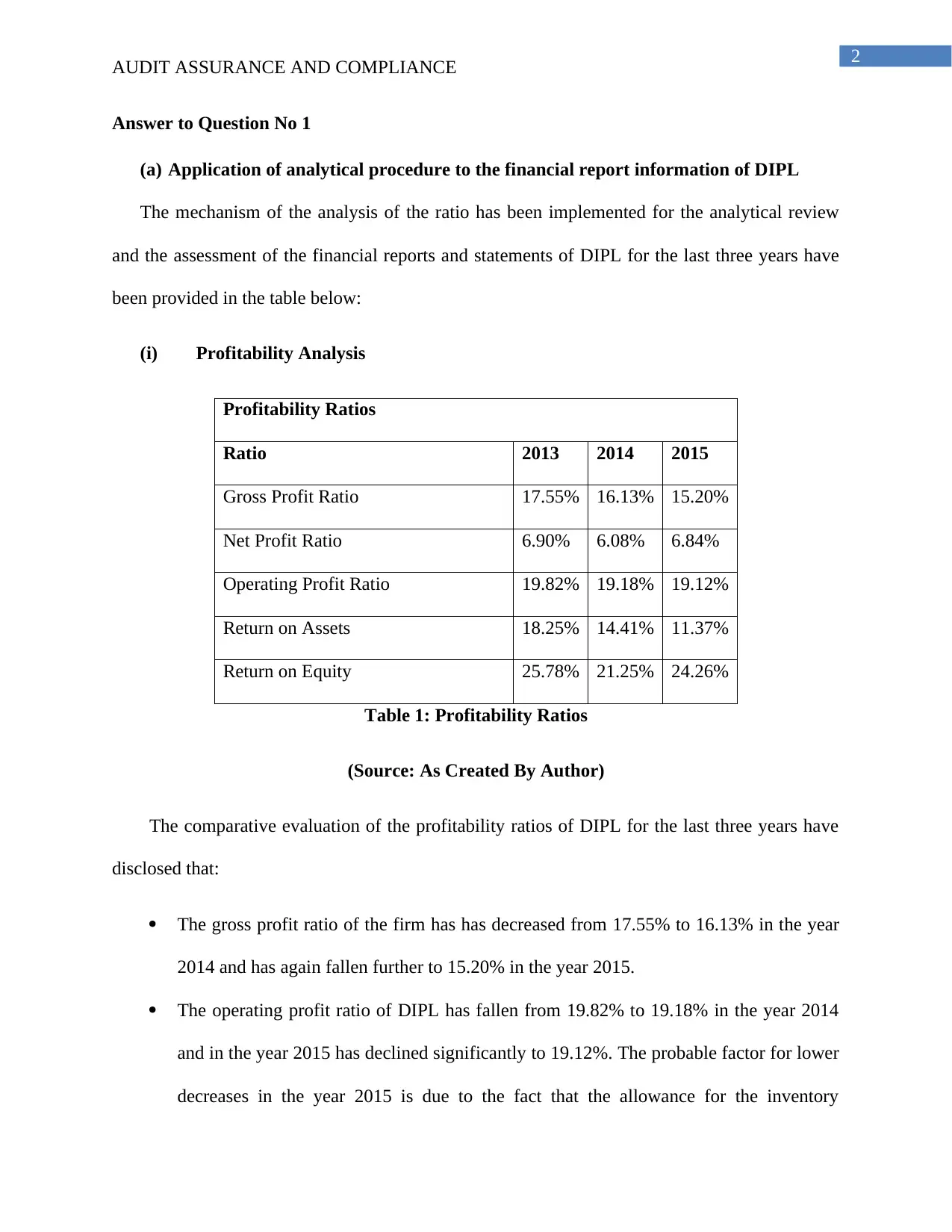

Answer to Question No 1

(a) Application of analytical procedure to the financial report information of DIPL

The mechanism of the analysis of the ratio has been implemented for the analytical review

and the assessment of the financial reports and statements of DIPL for the last three years have

been provided in the table below:

(i) Profitability Analysis

Profitability Ratios

Ratio 2013 2014 2015

Gross Profit Ratio 17.55% 16.13% 15.20%

Net Profit Ratio 6.90% 6.08% 6.84%

Operating Profit Ratio 19.82% 19.18% 19.12%

Return on Assets 18.25% 14.41% 11.37%

Return on Equity 25.78% 21.25% 24.26%

Table 1: Profitability Ratios

(Source: As Created By Author)

The comparative evaluation of the profitability ratios of DIPL for the last three years have

disclosed that:

The gross profit ratio of the firm has has decreased from 17.55% to 16.13% in the year

2014 and has again fallen further to 15.20% in the year 2015.

The operating profit ratio of DIPL has fallen from 19.82% to 19.18% in the year 2014

and in the year 2015 has declined significantly to 19.12%. The probable factor for lower

decreases in the year 2015 is due to the fact that the allowance for the inventory

AUDIT ASSURANCE AND COMPLIANCE

Answer to Question No 1

(a) Application of analytical procedure to the financial report information of DIPL

The mechanism of the analysis of the ratio has been implemented for the analytical review

and the assessment of the financial reports and statements of DIPL for the last three years have

been provided in the table below:

(i) Profitability Analysis

Profitability Ratios

Ratio 2013 2014 2015

Gross Profit Ratio 17.55% 16.13% 15.20%

Net Profit Ratio 6.90% 6.08% 6.84%

Operating Profit Ratio 19.82% 19.18% 19.12%

Return on Assets 18.25% 14.41% 11.37%

Return on Equity 25.78% 21.25% 24.26%

Table 1: Profitability Ratios

(Source: As Created By Author)

The comparative evaluation of the profitability ratios of DIPL for the last three years have

disclosed that:

The gross profit ratio of the firm has has decreased from 17.55% to 16.13% in the year

2014 and has again fallen further to 15.20% in the year 2015.

The operating profit ratio of DIPL has fallen from 19.82% to 19.18% in the year 2014

and in the year 2015 has declined significantly to 19.12%. The probable factor for lower

decreases in the year 2015 is due to the fact that the allowance for the inventory

3

AUDIT ASSURANCE AND COMPLIANCE

undesirability has been written back in the year 2015 and there is a rise in the storage

fees of the e-book even.

It has been observed that the net profit ratio of the firm has fallen in the year 2014 even

though the ratio has enhanced in the year 2015. The main factor for the rise in the net

profit ratio is due to the savings that has been noticed in tax during the year 2015

because of increased interest expenditure in the year 2015.

The return on equity has decreased from 25.75% to 21.25% in the year 2014 and later

the value has increased to 24.26% in the year 2015.

(ii) Liquidity Analysis

Liquidity ratios

Ratio 2013 2014 2015

Current Ratio 1.42 1.47 1.50

Quick Ratio 0.83 0.94 0.85

Table 2: Liquidity Ratios

(Source: As Created by Author)

The analysis of the liquidity ratio of DIPL has depicted that:

The liquidity condition of the organization has enriched slightly in the year 2015 and

this value has been viewed with the help of the current ratio. The current ratio in the

year 2013 is 1.42 and in the year 2014 has raised to 1.47. The ratio has even increased

significantly in the year 2015 to 1.50.

AUDIT ASSURANCE AND COMPLIANCE

undesirability has been written back in the year 2015 and there is a rise in the storage

fees of the e-book even.

It has been observed that the net profit ratio of the firm has fallen in the year 2014 even

though the ratio has enhanced in the year 2015. The main factor for the rise in the net

profit ratio is due to the savings that has been noticed in tax during the year 2015

because of increased interest expenditure in the year 2015.

The return on equity has decreased from 25.75% to 21.25% in the year 2014 and later

the value has increased to 24.26% in the year 2015.

(ii) Liquidity Analysis

Liquidity ratios

Ratio 2013 2014 2015

Current Ratio 1.42 1.47 1.50

Quick Ratio 0.83 0.94 0.85

Table 2: Liquidity Ratios

(Source: As Created by Author)

The analysis of the liquidity ratio of DIPL has depicted that:

The liquidity condition of the organization has enriched slightly in the year 2015 and

this value has been viewed with the help of the current ratio. The current ratio in the

year 2013 is 1.42 and in the year 2014 has raised to 1.47. The ratio has even increased

significantly in the year 2015 to 1.50.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

AUDIT ASSURANCE AND COMPLIANCE

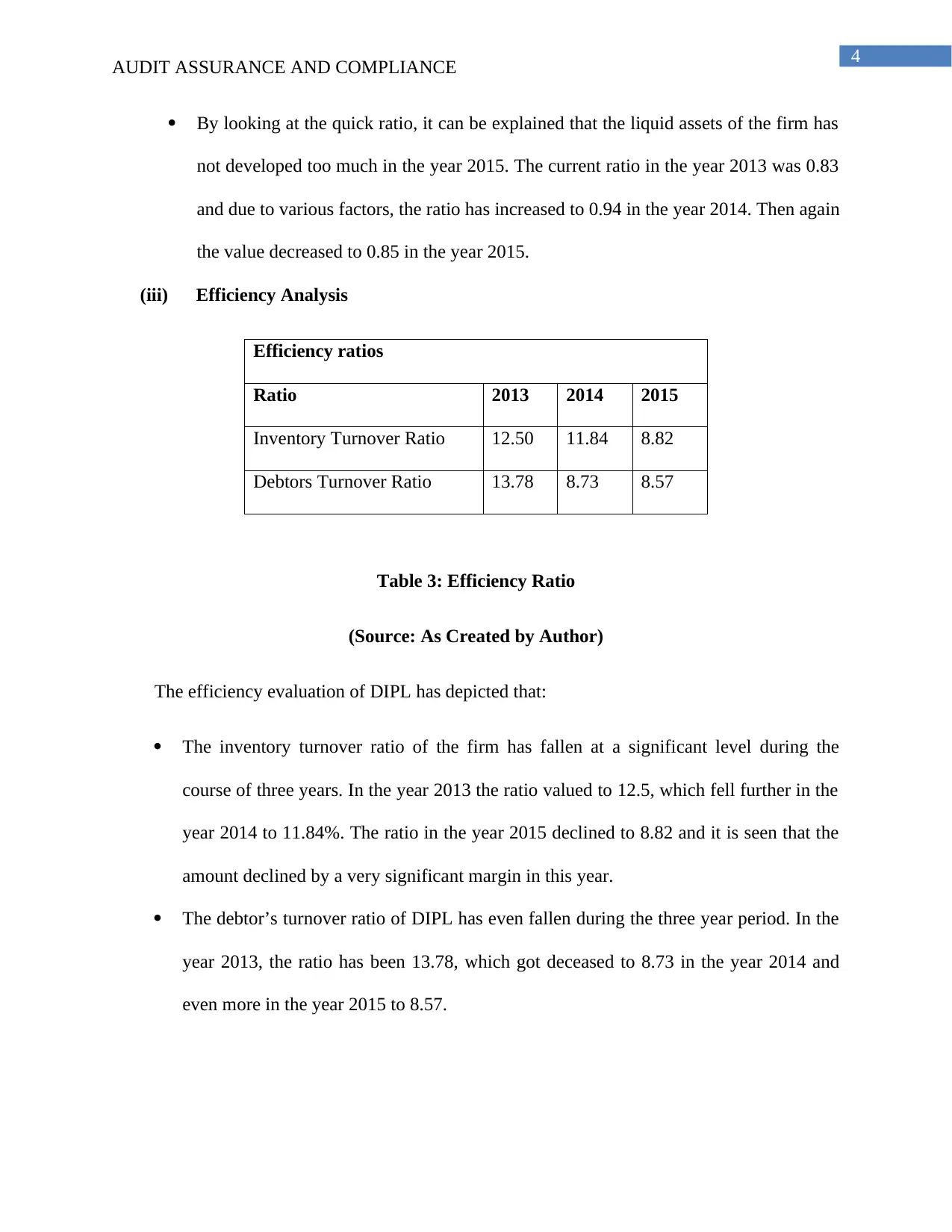

By looking at the quick ratio, it can be explained that the liquid assets of the firm has

not developed too much in the year 2015. The current ratio in the year 2013 was 0.83

and due to various factors, the ratio has increased to 0.94 in the year 2014. Then again

the value decreased to 0.85 in the year 2015.

(iii) Efficiency Analysis

Efficiency ratios

Ratio 2013 2014 2015

Inventory Turnover Ratio 12.50 11.84 8.82

Debtors Turnover Ratio 13.78 8.73 8.57

Table 3: Efficiency Ratio

(Source: As Created by Author)

The efficiency evaluation of DIPL has depicted that:

The inventory turnover ratio of the firm has fallen at a significant level during the

course of three years. In the year 2013 the ratio valued to 12.5, which fell further in the

year 2014 to 11.84%. The ratio in the year 2015 declined to 8.82 and it is seen that the

amount declined by a very significant margin in this year.

The debtor’s turnover ratio of DIPL has even fallen during the three year period. In the

year 2013, the ratio has been 13.78, which got deceased to 8.73 in the year 2014 and

even more in the year 2015 to 8.57.

AUDIT ASSURANCE AND COMPLIANCE

By looking at the quick ratio, it can be explained that the liquid assets of the firm has

not developed too much in the year 2015. The current ratio in the year 2013 was 0.83

and due to various factors, the ratio has increased to 0.94 in the year 2014. Then again

the value decreased to 0.85 in the year 2015.

(iii) Efficiency Analysis

Efficiency ratios

Ratio 2013 2014 2015

Inventory Turnover Ratio 12.50 11.84 8.82

Debtors Turnover Ratio 13.78 8.73 8.57

Table 3: Efficiency Ratio

(Source: As Created by Author)

The efficiency evaluation of DIPL has depicted that:

The inventory turnover ratio of the firm has fallen at a significant level during the

course of three years. In the year 2013 the ratio valued to 12.5, which fell further in the

year 2014 to 11.84%. The ratio in the year 2015 declined to 8.82 and it is seen that the

amount declined by a very significant margin in this year.

The debtor’s turnover ratio of DIPL has even fallen during the three year period. In the

year 2013, the ratio has been 13.78, which got deceased to 8.73 in the year 2014 and

even more in the year 2015 to 8.57.

5

AUDIT ASSURANCE AND COMPLIANCE

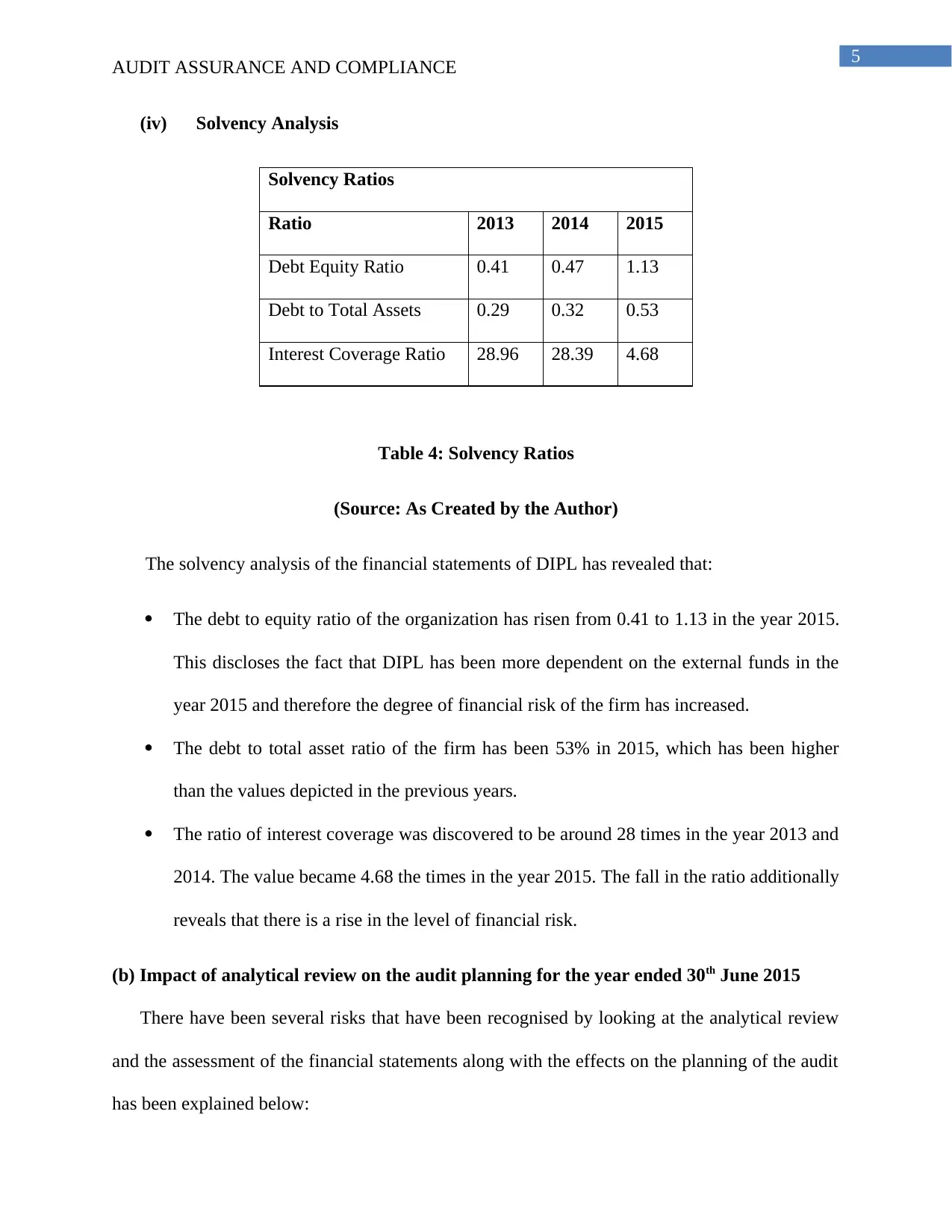

(iv) Solvency Analysis

Solvency Ratios

Ratio 2013 2014 2015

Debt Equity Ratio 0.41 0.47 1.13

Debt to Total Assets 0.29 0.32 0.53

Interest Coverage Ratio 28.96 28.39 4.68

Table 4: Solvency Ratios

(Source: As Created by the Author)

The solvency analysis of the financial statements of DIPL has revealed that:

The debt to equity ratio of the organization has risen from 0.41 to 1.13 in the year 2015.

This discloses the fact that DIPL has been more dependent on the external funds in the

year 2015 and therefore the degree of financial risk of the firm has increased.

The debt to total asset ratio of the firm has been 53% in 2015, which has been higher

than the values depicted in the previous years.

The ratio of interest coverage was discovered to be around 28 times in the year 2013 and

2014. The value became 4.68 the times in the year 2015. The fall in the ratio additionally

reveals that there is a rise in the level of financial risk.

(b) Impact of analytical review on the audit planning for the year ended 30th June 2015

There have been several risks that have been recognised by looking at the analytical review

and the assessment of the financial statements along with the effects on the planning of the audit

has been explained below:

AUDIT ASSURANCE AND COMPLIANCE

(iv) Solvency Analysis

Solvency Ratios

Ratio 2013 2014 2015

Debt Equity Ratio 0.41 0.47 1.13

Debt to Total Assets 0.29 0.32 0.53

Interest Coverage Ratio 28.96 28.39 4.68

Table 4: Solvency Ratios

(Source: As Created by the Author)

The solvency analysis of the financial statements of DIPL has revealed that:

The debt to equity ratio of the organization has risen from 0.41 to 1.13 in the year 2015.

This discloses the fact that DIPL has been more dependent on the external funds in the

year 2015 and therefore the degree of financial risk of the firm has increased.

The debt to total asset ratio of the firm has been 53% in 2015, which has been higher

than the values depicted in the previous years.

The ratio of interest coverage was discovered to be around 28 times in the year 2013 and

2014. The value became 4.68 the times in the year 2015. The fall in the ratio additionally

reveals that there is a rise in the level of financial risk.

(b) Impact of analytical review on the audit planning for the year ended 30th June 2015

There have been several risks that have been recognised by looking at the analytical review

and the assessment of the financial statements along with the effects on the planning of the audit

has been explained below:

6

AUDIT ASSURANCE AND COMPLIANCE

(i) The condition of profitability of the company has not developed in the year 2025. It is

seen that more fall in the profits in the coming future can increase the subject of going

concern capability of the firm. The detailed evaluation of the organization requires to

be planned in order to discover the future scenarios (ACCA. 2012).

(ii) The current ratio of DIPL has increased in the year 2015. The development has been

mainly due to the writing back the allowance for the inventory loss (Duncan and

Whittington 2014). The explained evaluation of the inventory allowance requires to

be undertaken in order to examine the validity in a precise manner.

(iii) The fall in the efficiency level of the management in order to handle and manage their

current assets requires to be assessed and the probable reasons for the same requires

to be recognised (PCAOB 2015).

(iv) It is seen that there is a rise in the financial risk of the firm. The revelations that are

related to these risks requires to be evaluated in order to examine whether the

evidence for the same has been given out in the financial statements or not.

AUDIT ASSURANCE AND COMPLIANCE

(i) The condition of profitability of the company has not developed in the year 2025. It is

seen that more fall in the profits in the coming future can increase the subject of going

concern capability of the firm. The detailed evaluation of the organization requires to

be planned in order to discover the future scenarios (ACCA. 2012).

(ii) The current ratio of DIPL has increased in the year 2015. The development has been

mainly due to the writing back the allowance for the inventory loss (Duncan and

Whittington 2014). The explained evaluation of the inventory allowance requires to

be undertaken in order to examine the validity in a precise manner.

(iii) The fall in the efficiency level of the management in order to handle and manage their

current assets requires to be assessed and the probable reasons for the same requires

to be recognised (PCAOB 2015).

(iv) It is seen that there is a rise in the financial risk of the firm. The revelations that are

related to these risks requires to be evaluated in order to examine whether the

evidence for the same has been given out in the financial statements or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT ASSURANCE AND COMPLIANCE

Answer to Question 2

The risks related to the business can be described as the probability of incapability of a firm

in order to accomplish their aims and objectives. This incapability can be due to several factors

that are prevalent in the environment of the business, which can be external or internal to the

company (Baylis et al. 2017). The two risk factors which arises from the nature of the operations

of the business of DIPL can be well described as follows:

(i) Financial Risk: The financial risk may be described as the incapability of the

organization to reimburse their long term liabilities within the stipulated time. The

risk rises with the increase in the external liabilities. The debt proportion of the

organization in comparison to the equity has risen in the year 2015 during the time

period of the last three years. This reveals that the degree of financial risk in the year

2015 has increased significantly. It is even seen that there is a rise in the liability of

payment of the fixed interest and the loan repayment burdens within the time

scheduled (Thaweejinda and Senivongse 2014). Therefore, there is an intimidation to

the long term affluence condition of the organization if the company does not have

the capability to make payments for the fixed interest and the principle amount in the

scheduled time.

Material misstatement in the financial reports

There is a probability that the firm may look to influence their financial records so that

they are able to control their debt to equity ratio and the current ratio according to the agreements

and contracts with the lending organization. In order to maintain their current ratio, the

organization can pump up their current assets with the help of increasing receivable values, the

investor or can be both (Shafii, Abidin. and Salleh 2015). In the same way in order to sustain

AUDIT ASSURANCE AND COMPLIANCE

Answer to Question 2

The risks related to the business can be described as the probability of incapability of a firm

in order to accomplish their aims and objectives. This incapability can be due to several factors

that are prevalent in the environment of the business, which can be external or internal to the

company (Baylis et al. 2017). The two risk factors which arises from the nature of the operations

of the business of DIPL can be well described as follows:

(i) Financial Risk: The financial risk may be described as the incapability of the

organization to reimburse their long term liabilities within the stipulated time. The

risk rises with the increase in the external liabilities. The debt proportion of the

organization in comparison to the equity has risen in the year 2015 during the time

period of the last three years. This reveals that the degree of financial risk in the year

2015 has increased significantly. It is even seen that there is a rise in the liability of

payment of the fixed interest and the loan repayment burdens within the time

scheduled (Thaweejinda and Senivongse 2014). Therefore, there is an intimidation to

the long term affluence condition of the organization if the company does not have

the capability to make payments for the fixed interest and the principle amount in the

scheduled time.

Material misstatement in the financial reports

There is a probability that the firm may look to influence their financial records so that

they are able to control their debt to equity ratio and the current ratio according to the agreements

and contracts with the lending organization. In order to maintain their current ratio, the

organization can pump up their current assets with the help of increasing receivable values, the

investor or can be both (Shafii, Abidin. and Salleh 2015). In the same way in order to sustain

8

AUDIT ASSURANCE AND COMPLIANCE

their debt to equity ratio, the firm can inflate the equity value with the help of rising values of the

retained earnings.

(ii) Information technological risk

The implementation of the information technology creates several risks to the firm. Any

deficits within the control of information technology can have confrontational effect on the

company.

In the year 2015, the organisation implemented new and innovative IT processes in order to

computerise their accounting roles and then assimilate it on the general ledger system. It is

observed that there has been an increasing pressure on the IT department given by the

management in order to conclude the process in the year 2015 only. There exists a threat to the

accounting information system security because of the probability of the unnatural and natural

calamities and disasters (James 2015).

Material misstatement in the financial reports

The organization could not preserve the equivalency among the new accounting process

and the current software process. There was an issue with respect to the inappropriate allocation

of the transactions to the period. The concept of accounting with respect to the periodicity was

not followed properly (Homb et al. 2014). It could therefore lead to inappropriate profitability

condition presentation and the financial condition of the organization.

AUDIT ASSURANCE AND COMPLIANCE

their debt to equity ratio, the firm can inflate the equity value with the help of rising values of the

retained earnings.

(ii) Information technological risk

The implementation of the information technology creates several risks to the firm. Any

deficits within the control of information technology can have confrontational effect on the

company.

In the year 2015, the organisation implemented new and innovative IT processes in order to

computerise their accounting roles and then assimilate it on the general ledger system. It is

observed that there has been an increasing pressure on the IT department given by the

management in order to conclude the process in the year 2015 only. There exists a threat to the

accounting information system security because of the probability of the unnatural and natural

calamities and disasters (James 2015).

Material misstatement in the financial reports

The organization could not preserve the equivalency among the new accounting process

and the current software process. There was an issue with respect to the inappropriate allocation

of the transactions to the period. The concept of accounting with respect to the periodicity was

not followed properly (Homb et al. 2014). It could therefore lead to inappropriate profitability

condition presentation and the financial condition of the organization.

9

AUDIT ASSURANCE AND COMPLIANCE

Answer to Question No 3

(a) Key risk factors related to the misstatement in the financial reporting

The background data of DIPL as provided in the case study reveals the probability of the

implementation of the deceitful practices of financial reporting by DIPL. The significant risk

factors that are associated with such practices can be recognised as follows:

(i) Debt covenant

There is a lot of burden on the department of finance in order to meet the several debt

covenants. It has been observed that a loan of 7.5 million was undertaken from BDO Finance

Ltd in the year 2015 that was based on the two covenants that have been discussed below:

A minimum current ratio of 1:5:1 is to be sustained.

The debt to equity ratio requires to less than 1.

On the advent of the company failing to stay in line with the above discussed two

requirements will lead to the withdrawing of the loan, which can have an adverse impact on the

activities of the firm. There exists a probability that the current assets may have been pumped up

so that the current ratio can be sustained to 1:5:1. In the same manner, there can be alterations in

the retained earnings so that the debt to equity ratio can be maintained to a value below 1 (Alam

2014).

(ii) Nature of control environment

AUDIT ASSURANCE AND COMPLIANCE

Answer to Question No 3

(a) Key risk factors related to the misstatement in the financial reporting

The background data of DIPL as provided in the case study reveals the probability of the

implementation of the deceitful practices of financial reporting by DIPL. The significant risk

factors that are associated with such practices can be recognised as follows:

(i) Debt covenant

There is a lot of burden on the department of finance in order to meet the several debt

covenants. It has been observed that a loan of 7.5 million was undertaken from BDO Finance

Ltd in the year 2015 that was based on the two covenants that have been discussed below:

A minimum current ratio of 1:5:1 is to be sustained.

The debt to equity ratio requires to less than 1.

On the advent of the company failing to stay in line with the above discussed two

requirements will lead to the withdrawing of the loan, which can have an adverse impact on the

activities of the firm. There exists a probability that the current assets may have been pumped up

so that the current ratio can be sustained to 1:5:1. In the same manner, there can be alterations in

the retained earnings so that the debt to equity ratio can be maintained to a value below 1 (Alam

2014).

(ii) Nature of control environment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

AUDIT ASSURANCE AND COMPLIANCE

The availability of unrefined explanation of the job description and the poor segmentation of

work is another factor of risk, which may lead to the presence of practices that are fraudulent in

nature in the process of financial reporting. The entrance of the purchased inventory and its

quantity and value is recorded by the same individual who is even the accounts payable clerk.

There exists a probability that the inventory may be altered by revealing additional inventory

during the time of arrival (Nalewaik and Mills 2016). There is an absenteeism of an effective

system of the documentation, which aids to limit the fraud.

(b) Effect of risk on the conduct of audit

The auditors requires to construct their audit plan in a process that the degree of risk can be

reduced or eliminated to most possible extent. The impact of deceitful factors of risk on the

conduct of the audit can be discussed as below:

(i) Impact of debt covenants on the audit plan: The amount of current assets and

current liabilities requires to be corroborated in a careful manner thereby to examine

whether there are any current asset inflation or current liabilities deflation or not. In

the same way, the equity balance requires to be examined through the cautious

confirmation of the retained earnings (Lad and Dahl 2014).

(ii) Impact of control environment on the audit plan: The balance of inventory

requires to be examined. The amount of the orders that has been placed for the

purchase of the inventory requires to be harmonized with the quantity that is received

thereby recognising whether there are any alterations has been undertaken by the

accounts payable clerk or not (Simons, Bester and Moll 2017).

AUDIT ASSURANCE AND COMPLIANCE

The availability of unrefined explanation of the job description and the poor segmentation of

work is another factor of risk, which may lead to the presence of practices that are fraudulent in

nature in the process of financial reporting. The entrance of the purchased inventory and its

quantity and value is recorded by the same individual who is even the accounts payable clerk.

There exists a probability that the inventory may be altered by revealing additional inventory

during the time of arrival (Nalewaik and Mills 2016). There is an absenteeism of an effective

system of the documentation, which aids to limit the fraud.

(b) Effect of risk on the conduct of audit

The auditors requires to construct their audit plan in a process that the degree of risk can be

reduced or eliminated to most possible extent. The impact of deceitful factors of risk on the

conduct of the audit can be discussed as below:

(i) Impact of debt covenants on the audit plan: The amount of current assets and

current liabilities requires to be corroborated in a careful manner thereby to examine

whether there are any current asset inflation or current liabilities deflation or not. In

the same way, the equity balance requires to be examined through the cautious

confirmation of the retained earnings (Lad and Dahl 2014).

(ii) Impact of control environment on the audit plan: The balance of inventory

requires to be examined. The amount of the orders that has been placed for the

purchase of the inventory requires to be harmonized with the quantity that is received

thereby recognising whether there are any alterations has been undertaken by the

accounts payable clerk or not (Simons, Bester and Moll 2017).

11

AUDIT ASSURANCE AND COMPLIANCE

Reference List

ACCA. (2012). Audit Risk. Retrieved from ACCA Website:

http://www.accaglobal.com/in/en/student/exam-support-resources/fundamentals-exams-study-

resources/f8/technical-articles/audit-risk0.html

Alam, I.U., 2014. Effectual compliance audit of vendors development.

Baylis, R.M., Burnap, P., Clatworthy, M.A., Gad, M.A. and Pong, C.K., 2017. Private lenders’

demand for audit. Journal of Accounting and Economics.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance and

audit: Does this equal security?. In Proceedings of the 7th International Conference on Security

of Information and Networks (p. 77). ACM.

Homb, N.M., Sheybani, S., Derby, D. and Wood, K., 2014. Audit and feedback intervention: An

examination of differences in chiropractic record-keeping compliance. Journal of Chiropractic

Education, 28(2), pp.123-129.

James, K., 2016. POLK STATE OFFICE BUILDING NASHVILLE, TENNESSEE 37243-1402

PHONE (615) 401-7841 Independent Auditor's Report for Federal Awards (Uniform Guidance).

Those standards and the Uniform Guidance require that we plan and perform the audit to obtain

reasonable assurance about whether noncompliance with the types of compliance requirements

AUDIT ASSURANCE AND COMPLIANCE

Reference List

ACCA. (2012). Audit Risk. Retrieved from ACCA Website:

http://www.accaglobal.com/in/en/student/exam-support-resources/fundamentals-exams-study-

resources/f8/technical-articles/audit-risk0.html

Alam, I.U., 2014. Effectual compliance audit of vendors development.

Baylis, R.M., Burnap, P., Clatworthy, M.A., Gad, M.A. and Pong, C.K., 2017. Private lenders’

demand for audit. Journal of Accounting and Economics.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance and

audit: Does this equal security?. In Proceedings of the 7th International Conference on Security

of Information and Networks (p. 77). ACM.

Homb, N.M., Sheybani, S., Derby, D. and Wood, K., 2014. Audit and feedback intervention: An

examination of differences in chiropractic record-keeping compliance. Journal of Chiropractic

Education, 28(2), pp.123-129.

James, K., 2016. POLK STATE OFFICE BUILDING NASHVILLE, TENNESSEE 37243-1402

PHONE (615) 401-7841 Independent Auditor's Report for Federal Awards (Uniform Guidance).

Those standards and the Uniform Guidance require that we plan and perform the audit to obtain

reasonable assurance about whether noncompliance with the types of compliance requirements

12

AUDIT ASSURANCE AND COMPLIANCE

referred to above that could have a direct and material effect on a major federal program

occurred. An audit includes examining, on a test basis, evidence about Cheatham.... Opinion on

Each Major Federal Program.

Lad, P.M. and Dahl, R., 2014. Audit of the informed consent process as a part of a clinical

research quality assurance program. Science and engineering ethics, 20(2), pp.469-479.

Nalewaik, A. and Mills, A., 2016. Project Performance Review: Capturing the Value of Audit,

Oversight, and Compliance for Project Success. CRC Press.

PCAOB. (2015). The Auditor's Consideration of an Entity's Ability to Continue as a Going

Concern. Retrieved April 2017, from https://pcaobus.org/Standards/Auditing/Pages/AU341.aspx

Shafii, Z., Abidin, A.Z. and Salleh, S., 2015. Integrated internal-external Shariah audit model:

A proposal towards the enhancement of Shariah assurance practices in Islamic financial

institutions (No. 1436-7).

Simons, R.C., Bester, A. and Moll, M., 2017. Exploring variability among quality management

system auditors when rating the severity of audit findings at a nuclear power plant. South African

Journal of Industrial Engineering, 28(1), pp.145-163.

Thaweejinda, J. and Senivongse, T., 2014, May. Semantic search for cloud providers with

security conformance to Cloud Controls Matrix. In Computer Science and Software Engineering

(JCSSE), 2014 11th International Joint Conference on (pp. 286-291). IEEE.

AUDIT ASSURANCE AND COMPLIANCE

referred to above that could have a direct and material effect on a major federal program

occurred. An audit includes examining, on a test basis, evidence about Cheatham.... Opinion on

Each Major Federal Program.

Lad, P.M. and Dahl, R., 2014. Audit of the informed consent process as a part of a clinical

research quality assurance program. Science and engineering ethics, 20(2), pp.469-479.

Nalewaik, A. and Mills, A., 2016. Project Performance Review: Capturing the Value of Audit,

Oversight, and Compliance for Project Success. CRC Press.

PCAOB. (2015). The Auditor's Consideration of an Entity's Ability to Continue as a Going

Concern. Retrieved April 2017, from https://pcaobus.org/Standards/Auditing/Pages/AU341.aspx

Shafii, Z., Abidin, A.Z. and Salleh, S., 2015. Integrated internal-external Shariah audit model:

A proposal towards the enhancement of Shariah assurance practices in Islamic financial

institutions (No. 1436-7).

Simons, R.C., Bester, A. and Moll, M., 2017. Exploring variability among quality management

system auditors when rating the severity of audit findings at a nuclear power plant. South African

Journal of Industrial Engineering, 28(1), pp.145-163.

Thaweejinda, J. and Senivongse, T., 2014, May. Semantic search for cloud providers with

security conformance to Cloud Controls Matrix. In Computer Science and Software Engineering

(JCSSE), 2014 11th International Joint Conference on (pp. 286-291). IEEE.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

AUDIT ASSURANCE AND COMPLIANCE

Bibliography

Brawley, S., Clark, J., Dixon, C., Ford, L., Nielsen, E., Ross, S. and Upton, S., 2015. History on

trial: Evaluating learning outcomes through audit and accreditation in a national standards

environment. Teaching and Learning Inquiry: The ISSOTL Journal, 3(2), pp.89-105.

Escobar, M.P. and Demeritt, D., 2017. Paperwork and the decoupling of audit and animal

welfare: The challenges of materiality for better regulation. Environment and Planning C:

Politics and Space, 35(1), pp.169-190.

Ismanto, S. and Hassan, C.H., 2017. A Clinical Audit for Compliance on the Innovated

Radiographic Technique at a Radiologic Unit. ASEAN Journal on Science and Technolgy for

Development, 33(1), pp.1-9.

Melidis, C., Bosch, W.R., Izewska, J., Fidarova, E., Zubizarreta, E., Ishikura, S., Followill, D.,

Galvin, J., Xiao, Y., Ebert, M.A. and Kron, T., 2014. Radiation therapy quality assurance in

clinical trials–Global Harmonisation Group. Radiotherapy and oncology: journal of the

European Society for Therapeutic Radiology and Oncology, 111(3), p.327.

Loconto, A.M., 2017. Models of assurance: Diversity and standardization of modes of

intermediation. The ANNALS of the American Academy of Political and Social Science, 670(1),

pp.112-132.

AUDIT ASSURANCE AND COMPLIANCE

Bibliography

Brawley, S., Clark, J., Dixon, C., Ford, L., Nielsen, E., Ross, S. and Upton, S., 2015. History on

trial: Evaluating learning outcomes through audit and accreditation in a national standards

environment. Teaching and Learning Inquiry: The ISSOTL Journal, 3(2), pp.89-105.

Escobar, M.P. and Demeritt, D., 2017. Paperwork and the decoupling of audit and animal

welfare: The challenges of materiality for better regulation. Environment and Planning C:

Politics and Space, 35(1), pp.169-190.

Ismanto, S. and Hassan, C.H., 2017. A Clinical Audit for Compliance on the Innovated

Radiographic Technique at a Radiologic Unit. ASEAN Journal on Science and Technolgy for

Development, 33(1), pp.1-9.

Melidis, C., Bosch, W.R., Izewska, J., Fidarova, E., Zubizarreta, E., Ishikura, S., Followill, D.,

Galvin, J., Xiao, Y., Ebert, M.A. and Kron, T., 2014. Radiation therapy quality assurance in

clinical trials–Global Harmonisation Group. Radiotherapy and oncology: journal of the

European Society for Therapeutic Radiology and Oncology, 111(3), p.327.

Loconto, A.M., 2017. Models of assurance: Diversity and standardization of modes of

intermediation. The ANNALS of the American Academy of Political and Social Science, 670(1),

pp.112-132.

14

AUDIT ASSURANCE AND COMPLIANCE

AUDIT ASSURANCE AND COMPLIANCE

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.