ACC568 - Audit Report: Financial Analysis of Turnkey Creek Wines

VerifiedAdded on 2023/06/07

|13

|3458

|57

Report

AI Summary

This report presents an audit plan for Turnkey Creek Wines (TCW) for the year ending June 30, 2018, prepared for the audit manager of Miller Yates Howarth (MYH). It examines TCW's financial performance, focusing on ratio analysis across accounts receivable, current investments, property assets, and marketing expenses. The report identifies audit risks, including increasing receivable days, declining returns on investment and assets, and rising marketing expenses, along with corresponding audit steps to mitigate these risks. Furthermore, it evaluates internal controls related to purchasing and accounts payable, highlighting weaknesses. The analysis extends to other key financial ratios, such as current and quick ratios, debt-to-equity ratio, times interest earned, and days in inventory, to assess overall business risks. The report also discusses effective internal controls and tests of control within the company's IT systems and approval mechanisms. The report aims to provide a comprehensive audit perspective, covering financial analysis, risk assessment, and internal control evaluations.

Accounting for

Management

Decisions

Management

Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Executive Summary

In the given assignment, a report is to be prepared on the audit planning to be made for the audit

of one of the clients, named Turnkey Creek Wines. The audit planning procedures, the high-risk

areas and the comments on the internal control being maintained by the company has been

mentioned in the report which is being prepared for the manager of the audit division of the

accounting firm named Miller Yates Howarth (MYH). Besides this entire ratio computation has

been done and the major risk areas in accounts receivables, current investment, property assets

and marketing expenses has been shown in the below report. Lasly, the weaknesses in the

internal control areas pertaining to purchase and accounts payable has also been highlighted.

2 | P a g e

Executive Summary

In the given assignment, a report is to be prepared on the audit planning to be made for the audit

of one of the clients, named Turnkey Creek Wines. The audit planning procedures, the high-risk

areas and the comments on the internal control being maintained by the company has been

mentioned in the report which is being prepared for the manager of the audit division of the

accounting firm named Miller Yates Howarth (MYH). Besides this entire ratio computation has

been done and the major risk areas in accounts receivables, current investment, property assets

and marketing expenses has been shown in the below report. Lasly, the weaknesses in the

internal control areas pertaining to purchase and accounts payable has also been highlighted.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Analysis and discussion...............................................................................................................................5

Question 1A.............................................................................................................................................5

Question 1B.............................................................................................................................................7

Question 2A.............................................................................................................................................8

Question 2B.............................................................................................................................................9

References.................................................................................................................................................11

3 | P a g e

Contents

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Analysis and discussion...............................................................................................................................5

Question 1A.............................................................................................................................................5

Question 1B.............................................................................................................................................7

Question 2A.............................................................................................................................................8

Question 2B.............................................................................................................................................9

References.................................................................................................................................................11

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Introduction

The audit plan for the client Trunkey Creek Wines is to be prepared for the year ended 30th June

2018. TCW is one of the significant clients of MYH for long. The principle activities in which

the client deals in is growing grapes for the wine production, production and distribution of

different types of wines, beef cattle production on the surplus lands and investment of the surplus

funds. The insufficient rainfall has rendered few of the lands to be unsuitable for grape wine

production, which is now being used for beef cattle production. However, due to average

increase of 2% in the temperature, the sparkling wine production is being affected and the

company is looking to purchase some lands in the cooler climates. The Wagyu beef, which is

being produced by the company, is being sold and marketed through Wagyu Selling Group

(WSG) in which TWC has significant shareholding (Alexander, 2016).

Several ratios of the company for the last 3 years have been computed and also the internal

control being maintained in the company in the areas of purchase, procurement, booking of the

orders in the system, invoice verification, payment to creditors, delivery of service, invoicing,

booking the liability and payment to creditors have been discussed in the case study.

4 | P a g e

Introduction

The audit plan for the client Trunkey Creek Wines is to be prepared for the year ended 30th June

2018. TCW is one of the significant clients of MYH for long. The principle activities in which

the client deals in is growing grapes for the wine production, production and distribution of

different types of wines, beef cattle production on the surplus lands and investment of the surplus

funds. The insufficient rainfall has rendered few of the lands to be unsuitable for grape wine

production, which is now being used for beef cattle production. However, due to average

increase of 2% in the temperature, the sparkling wine production is being affected and the

company is looking to purchase some lands in the cooler climates. The Wagyu beef, which is

being produced by the company, is being sold and marketed through Wagyu Selling Group

(WSG) in which TWC has significant shareholding (Alexander, 2016).

Several ratios of the company for the last 3 years have been computed and also the internal

control being maintained in the company in the areas of purchase, procurement, booking of the

orders in the system, invoice verification, payment to creditors, delivery of service, invoicing,

booking the liability and payment to creditors have been discussed in the case study.

4 | P a g e

5

Analysis and discussion

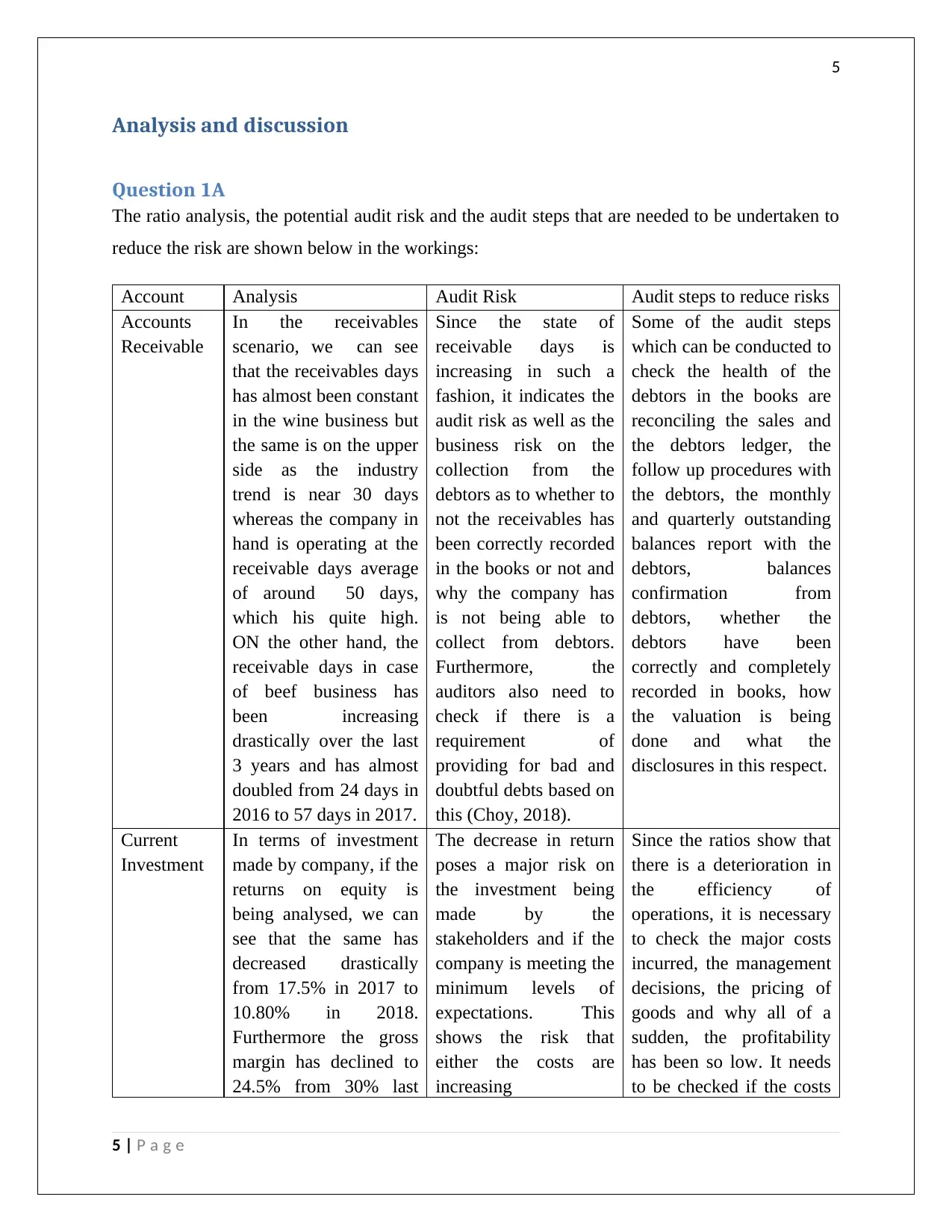

Question 1A

The ratio analysis, the potential audit risk and the audit steps that are needed to be undertaken to

reduce the risk are shown below in the workings:

Account Analysis Audit Risk Audit steps to reduce risks

Accounts

Receivable

In the receivables

scenario, we can see

that the receivables days

has almost been constant

in the wine business but

the same is on the upper

side as the industry

trend is near 30 days

whereas the company in

hand is operating at the

receivable days average

of around 50 days,

which his quite high.

ON the other hand, the

receivable days in case

of beef business has

been increasing

drastically over the last

3 years and has almost

doubled from 24 days in

2016 to 57 days in 2017.

Since the state of

receivable days is

increasing in such a

fashion, it indicates the

audit risk as well as the

business risk on the

collection from the

debtors as to whether to

not the receivables has

been correctly recorded

in the books or not and

why the company has

is not being able to

collect from debtors.

Furthermore, the

auditors also need to

check if there is a

requirement of

providing for bad and

doubtful debts based on

this (Choy, 2018).

Some of the audit steps

which can be conducted to

check the health of the

debtors in the books are

reconciling the sales and

the debtors ledger, the

follow up procedures with

the debtors, the monthly

and quarterly outstanding

balances report with the

debtors, balances

confirmation from

debtors, whether the

debtors have been

correctly and completely

recorded in books, how

the valuation is being

done and what the

disclosures in this respect.

Current

Investment

In terms of investment

made by company, if the

returns on equity is

being analysed, we can

see that the same has

decreased drastically

from 17.5% in 2017 to

10.80% in 2018.

Furthermore the gross

margin has declined to

24.5% from 30% last

The decrease in return

poses a major risk on

the investment being

made by the

stakeholders and if the

company is meeting the

minimum levels of

expectations. This

shows the risk that

either the costs are

increasing

Since the ratios show that

there is a deterioration in

the efficiency of

operations, it is necessary

to check the major costs

incurred, the management

decisions, the pricing of

goods and why all of a

sudden, the profitability

has been so low. It needs

to be checked if the costs

5 | P a g e

Analysis and discussion

Question 1A

The ratio analysis, the potential audit risk and the audit steps that are needed to be undertaken to

reduce the risk are shown below in the workings:

Account Analysis Audit Risk Audit steps to reduce risks

Accounts

Receivable

In the receivables

scenario, we can see

that the receivables days

has almost been constant

in the wine business but

the same is on the upper

side as the industry

trend is near 30 days

whereas the company in

hand is operating at the

receivable days average

of around 50 days,

which his quite high.

ON the other hand, the

receivable days in case

of beef business has

been increasing

drastically over the last

3 years and has almost

doubled from 24 days in

2016 to 57 days in 2017.

Since the state of

receivable days is

increasing in such a

fashion, it indicates the

audit risk as well as the

business risk on the

collection from the

debtors as to whether to

not the receivables has

been correctly recorded

in the books or not and

why the company has

is not being able to

collect from debtors.

Furthermore, the

auditors also need to

check if there is a

requirement of

providing for bad and

doubtful debts based on

this (Choy, 2018).

Some of the audit steps

which can be conducted to

check the health of the

debtors in the books are

reconciling the sales and

the debtors ledger, the

follow up procedures with

the debtors, the monthly

and quarterly outstanding

balances report with the

debtors, balances

confirmation from

debtors, whether the

debtors have been

correctly and completely

recorded in books, how

the valuation is being

done and what the

disclosures in this respect.

Current

Investment

In terms of investment

made by company, if the

returns on equity is

being analysed, we can

see that the same has

decreased drastically

from 17.5% in 2017 to

10.80% in 2018.

Furthermore the gross

margin has declined to

24.5% from 30% last

The decrease in return

poses a major risk on

the investment being

made by the

stakeholders and if the

company is meeting the

minimum levels of

expectations. This

shows the risk that

either the costs are

increasing

Since the ratios show that

there is a deterioration in

the efficiency of

operations, it is necessary

to check the major costs

incurred, the management

decisions, the pricing of

goods and why all of a

sudden, the profitability

has been so low. It needs

to be checked if the costs

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

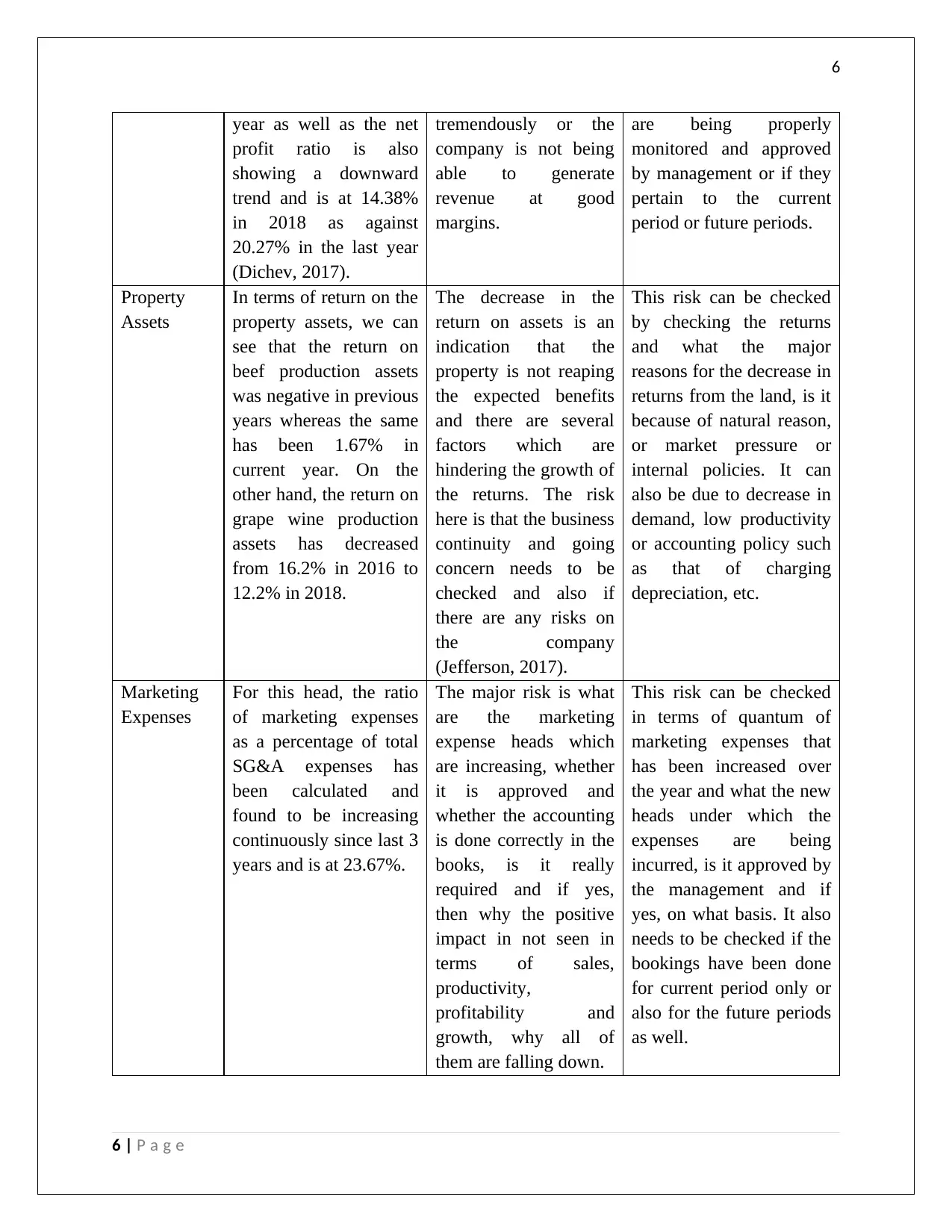

6

year as well as the net

profit ratio is also

showing a downward

trend and is at 14.38%

in 2018 as against

20.27% in the last year

(Dichev, 2017).

tremendously or the

company is not being

able to generate

revenue at good

margins.

are being properly

monitored and approved

by management or if they

pertain to the current

period or future periods.

Property

Assets

In terms of return on the

property assets, we can

see that the return on

beef production assets

was negative in previous

years whereas the same

has been 1.67% in

current year. On the

other hand, the return on

grape wine production

assets has decreased

from 16.2% in 2016 to

12.2% in 2018.

The decrease in the

return on assets is an

indication that the

property is not reaping

the expected benefits

and there are several

factors which are

hindering the growth of

the returns. The risk

here is that the business

continuity and going

concern needs to be

checked and also if

there are any risks on

the company

(Jefferson, 2017).

This risk can be checked

by checking the returns

and what the major

reasons for the decrease in

returns from the land, is it

because of natural reason,

or market pressure or

internal policies. It can

also be due to decrease in

demand, low productivity

or accounting policy such

as that of charging

depreciation, etc.

Marketing

Expenses

For this head, the ratio

of marketing expenses

as a percentage of total

SG&A expenses has

been calculated and

found to be increasing

continuously since last 3

years and is at 23.67%.

The major risk is what

are the marketing

expense heads which

are increasing, whether

it is approved and

whether the accounting

is done correctly in the

books, is it really

required and if yes,

then why the positive

impact in not seen in

terms of sales,

productivity,

profitability and

growth, why all of

them are falling down.

This risk can be checked

in terms of quantum of

marketing expenses that

has been increased over

the year and what the new

heads under which the

expenses are being

incurred, is it approved by

the management and if

yes, on what basis. It also

needs to be checked if the

bookings have been done

for current period only or

also for the future periods

as well.

6 | P a g e

year as well as the net

profit ratio is also

showing a downward

trend and is at 14.38%

in 2018 as against

20.27% in the last year

(Dichev, 2017).

tremendously or the

company is not being

able to generate

revenue at good

margins.

are being properly

monitored and approved

by management or if they

pertain to the current

period or future periods.

Property

Assets

In terms of return on the

property assets, we can

see that the return on

beef production assets

was negative in previous

years whereas the same

has been 1.67% in

current year. On the

other hand, the return on

grape wine production

assets has decreased

from 16.2% in 2016 to

12.2% in 2018.

The decrease in the

return on assets is an

indication that the

property is not reaping

the expected benefits

and there are several

factors which are

hindering the growth of

the returns. The risk

here is that the business

continuity and going

concern needs to be

checked and also if

there are any risks on

the company

(Jefferson, 2017).

This risk can be checked

by checking the returns

and what the major

reasons for the decrease in

returns from the land, is it

because of natural reason,

or market pressure or

internal policies. It can

also be due to decrease in

demand, low productivity

or accounting policy such

as that of charging

depreciation, etc.

Marketing

Expenses

For this head, the ratio

of marketing expenses

as a percentage of total

SG&A expenses has

been calculated and

found to be increasing

continuously since last 3

years and is at 23.67%.

The major risk is what

are the marketing

expense heads which

are increasing, whether

it is approved and

whether the accounting

is done correctly in the

books, is it really

required and if yes,

then why the positive

impact in not seen in

terms of sales,

productivity,

profitability and

growth, why all of

them are falling down.

This risk can be checked

in terms of quantum of

marketing expenses that

has been increased over

the year and what the new

heads under which the

expenses are being

incurred, is it approved by

the management and if

yes, on what basis. It also

needs to be checked if the

bookings have been done

for current period only or

also for the future periods

as well.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

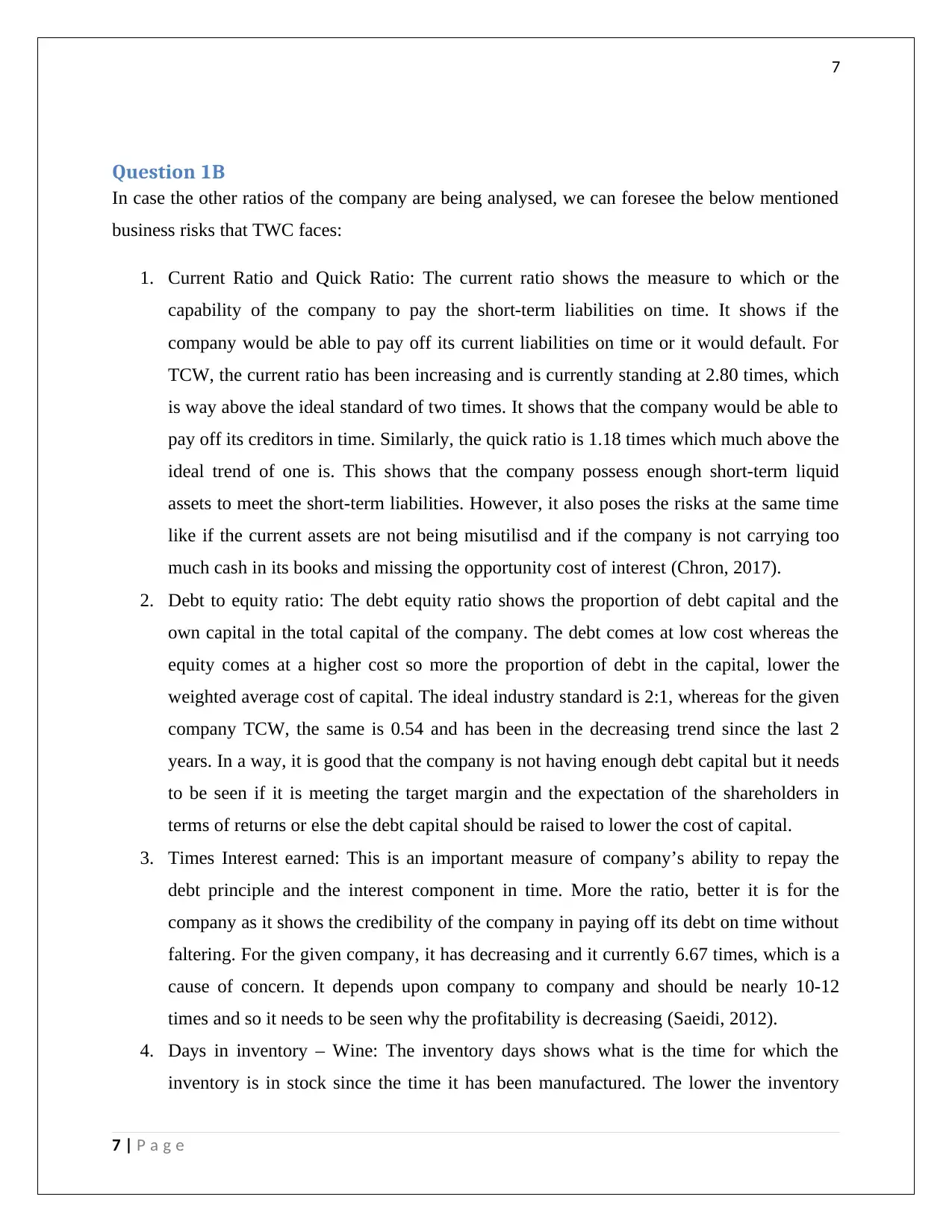

7

Question 1B

In case the other ratios of the company are being analysed, we can foresee the below mentioned

business risks that TWC faces:

1. Current Ratio and Quick Ratio: The current ratio shows the measure to which or the

capability of the company to pay the short-term liabilities on time. It shows if the

company would be able to pay off its current liabilities on time or it would default. For

TCW, the current ratio has been increasing and is currently standing at 2.80 times, which

is way above the ideal standard of two times. It shows that the company would be able to

pay off its creditors in time. Similarly, the quick ratio is 1.18 times which much above the

ideal trend of one is. This shows that the company possess enough short-term liquid

assets to meet the short-term liabilities. However, it also poses the risks at the same time

like if the current assets are not being misutilisd and if the company is not carrying too

much cash in its books and missing the opportunity cost of interest (Chron, 2017).

2. Debt to equity ratio: The debt equity ratio shows the proportion of debt capital and the

own capital in the total capital of the company. The debt comes at low cost whereas the

equity comes at a higher cost so more the proportion of debt in the capital, lower the

weighted average cost of capital. The ideal industry standard is 2:1, whereas for the given

company TCW, the same is 0.54 and has been in the decreasing trend since the last 2

years. In a way, it is good that the company is not having enough debt capital but it needs

to be seen if it is meeting the target margin and the expectation of the shareholders in

terms of returns or else the debt capital should be raised to lower the cost of capital.

3. Times Interest earned: This is an important measure of company’s ability to repay the

debt principle and the interest component in time. More the ratio, better it is for the

company as it shows the credibility of the company in paying off its debt on time without

faltering. For the given company, it has decreasing and it currently 6.67 times, which is a

cause of concern. It depends upon company to company and should be nearly 10-12

times and so it needs to be seen why the profitability is decreasing (Saeidi, 2012).

4. Days in inventory – Wine: The inventory days shows what is the time for which the

inventory is in stock since the time it has been manufactured. The lower the inventory

7 | P a g e

Question 1B

In case the other ratios of the company are being analysed, we can foresee the below mentioned

business risks that TWC faces:

1. Current Ratio and Quick Ratio: The current ratio shows the measure to which or the

capability of the company to pay the short-term liabilities on time. It shows if the

company would be able to pay off its current liabilities on time or it would default. For

TCW, the current ratio has been increasing and is currently standing at 2.80 times, which

is way above the ideal standard of two times. It shows that the company would be able to

pay off its creditors in time. Similarly, the quick ratio is 1.18 times which much above the

ideal trend of one is. This shows that the company possess enough short-term liquid

assets to meet the short-term liabilities. However, it also poses the risks at the same time

like if the current assets are not being misutilisd and if the company is not carrying too

much cash in its books and missing the opportunity cost of interest (Chron, 2017).

2. Debt to equity ratio: The debt equity ratio shows the proportion of debt capital and the

own capital in the total capital of the company. The debt comes at low cost whereas the

equity comes at a higher cost so more the proportion of debt in the capital, lower the

weighted average cost of capital. The ideal industry standard is 2:1, whereas for the given

company TCW, the same is 0.54 and has been in the decreasing trend since the last 2

years. In a way, it is good that the company is not having enough debt capital but it needs

to be seen if it is meeting the target margin and the expectation of the shareholders in

terms of returns or else the debt capital should be raised to lower the cost of capital.

3. Times Interest earned: This is an important measure of company’s ability to repay the

debt principle and the interest component in time. More the ratio, better it is for the

company as it shows the credibility of the company in paying off its debt on time without

faltering. For the given company, it has decreasing and it currently 6.67 times, which is a

cause of concern. It depends upon company to company and should be nearly 10-12

times and so it needs to be seen why the profitability is decreasing (Saeidi, 2012).

4. Days in inventory – Wine: The inventory days shows what is the time for which the

inventory is in stock since the time it has been manufactured. The lower the inventory

7 | P a g e

8

days, the better it is for the company. Though it has been decreasing from 460 days in

2016 to 367 days in 2018, but still the number of days for which the inventory is in hand

is way too high considering the industry trend and steps needs to be taken to reduce the

same so that the inventory does not become obsolete (Raiborn, Butler, & Martin, 2016).

Question 2A

There are many internal controls in the system, which are effective and help the company in

alleviating many types of risks to the company’s operation. The test of control for each of these

identified potentially effective controls have also been mentioned below. The test of control is

the audit procedure to check the effectiveness of the client’s control measures to detect and

prevent the material misstatements in the financials. Depending on their effectiveness, eth

auditor may choose to rely on the same.

Effective control Risk alleviated Test of control

Effective management of the

passwords of the IT system in

the company. Post the

implementation of the new IT

system and resolution of all

the teething issues, this is

being managed and

monitored by management

accountant (Bizfluent, 2017).

The IT system holds a

number of finance

configurations and also a lot

of data. If the configurations

are being altered unauthorised

then it may bring upon the

change in functionality and

can adversely affect the

financial accounting and

results altogether. So this risk

is alleviated. Furthermore,

strict password control exists

over access to programs, only

the access to database is

being enabled, so this also

alleviates the risk that

anybody and everybody

cannot pass financial entries

in the books.

Here the test of control ca be

in the form of checking the

authorization of the people

working in finance team and

other people as well. Also, it

can be checked if the entries

have come from other IDs as

well. Certain, big ticket line

items can be checked if the

same has been approved and

whether there are relevant

supporting for the same.

The 2nd internal control is

approval mechanism for the

orders value limit. If the

ordering amount is between $

10000-30000, it needs to be

This ensures that none of the

section managers, be it grape,

wine or beef production

managers do not order

supplied greater than $10000

The order booking can be

checked in the computer

ordering system as it is

directly linked to the

approved suppliers. A test of

8 | P a g e

days, the better it is for the company. Though it has been decreasing from 460 days in

2016 to 367 days in 2018, but still the number of days for which the inventory is in hand

is way too high considering the industry trend and steps needs to be taken to reduce the

same so that the inventory does not become obsolete (Raiborn, Butler, & Martin, 2016).

Question 2A

There are many internal controls in the system, which are effective and help the company in

alleviating many types of risks to the company’s operation. The test of control for each of these

identified potentially effective controls have also been mentioned below. The test of control is

the audit procedure to check the effectiveness of the client’s control measures to detect and

prevent the material misstatements in the financials. Depending on their effectiveness, eth

auditor may choose to rely on the same.

Effective control Risk alleviated Test of control

Effective management of the

passwords of the IT system in

the company. Post the

implementation of the new IT

system and resolution of all

the teething issues, this is

being managed and

monitored by management

accountant (Bizfluent, 2017).

The IT system holds a

number of finance

configurations and also a lot

of data. If the configurations

are being altered unauthorised

then it may bring upon the

change in functionality and

can adversely affect the

financial accounting and

results altogether. So this risk

is alleviated. Furthermore,

strict password control exists

over access to programs, only

the access to database is

being enabled, so this also

alleviates the risk that

anybody and everybody

cannot pass financial entries

in the books.

Here the test of control ca be

in the form of checking the

authorization of the people

working in finance team and

other people as well. Also, it

can be checked if the entries

have come from other IDs as

well. Certain, big ticket line

items can be checked if the

same has been approved and

whether there are relevant

supporting for the same.

The 2nd internal control is

approval mechanism for the

orders value limit. If the

ordering amount is between $

10000-30000, it needs to be

This ensures that none of the

section managers, be it grape,

wine or beef production

managers do not order

supplied greater than $10000

The order booking can be

checked in the computer

ordering system as it is

directly linked to the

approved suppliers. A test of

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

approved by management

accountant and if the value is

beyond $30000, it is to be

approved by company’s

CEO.

And if it is beyond $50000, it

is to be approved by the

Board.

in one go. The value limits

ensured that no wrong use of

authority is being taken and 4

eye principle is being

followed. Furthermore, it also

avoids the unnecessary

blockage of the funds

(Belton, 2017).

control can be conducted as

to if there are necessary

approvals in hand.

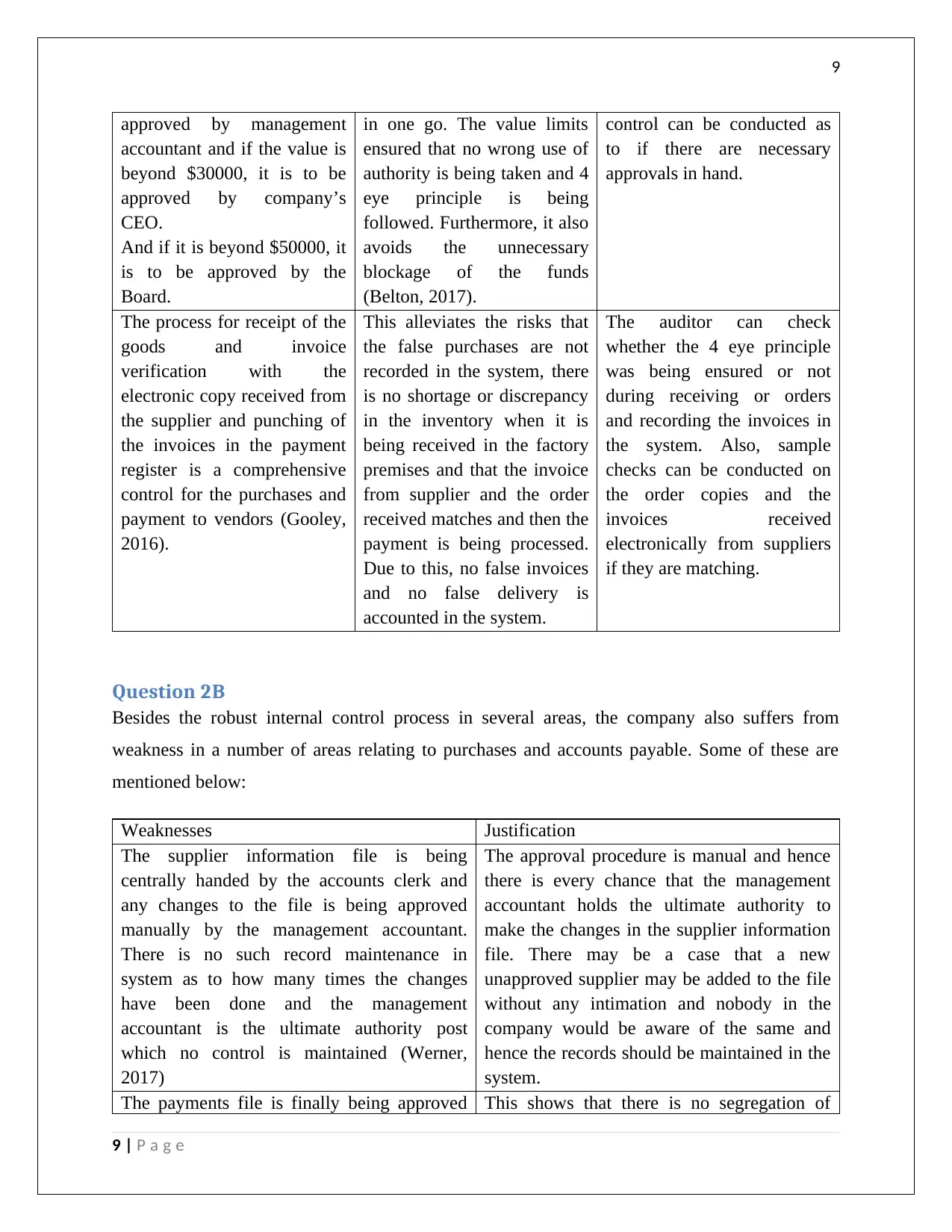

The process for receipt of the

goods and invoice

verification with the

electronic copy received from

the supplier and punching of

the invoices in the payment

register is a comprehensive

control for the purchases and

payment to vendors (Gooley,

2016).

This alleviates the risks that

the false purchases are not

recorded in the system, there

is no shortage or discrepancy

in the inventory when it is

being received in the factory

premises and that the invoice

from supplier and the order

received matches and then the

payment is being processed.

Due to this, no false invoices

and no false delivery is

accounted in the system.

The auditor can check

whether the 4 eye principle

was being ensured or not

during receiving or orders

and recording the invoices in

the system. Also, sample

checks can be conducted on

the order copies and the

invoices received

electronically from suppliers

if they are matching.

Question 2B

Besides the robust internal control process in several areas, the company also suffers from

weakness in a number of areas relating to purchases and accounts payable. Some of these are

mentioned below:

Weaknesses Justification

The supplier information file is being

centrally handed by the accounts clerk and

any changes to the file is being approved

manually by the management accountant.

There is no such record maintenance in

system as to how many times the changes

have been done and the management

accountant is the ultimate authority post

which no control is maintained (Werner,

2017)

The approval procedure is manual and hence

there is every chance that the management

accountant holds the ultimate authority to

make the changes in the supplier information

file. There may be a case that a new

unapproved supplier may be added to the file

without any intimation and nobody in the

company would be aware of the same and

hence the records should be maintained in the

system.

The payments file is finally being approved This shows that there is no segregation of

9 | P a g e

approved by management

accountant and if the value is

beyond $30000, it is to be

approved by company’s

CEO.

And if it is beyond $50000, it

is to be approved by the

Board.

in one go. The value limits

ensured that no wrong use of

authority is being taken and 4

eye principle is being

followed. Furthermore, it also

avoids the unnecessary

blockage of the funds

(Belton, 2017).

control can be conducted as

to if there are necessary

approvals in hand.

The process for receipt of the

goods and invoice

verification with the

electronic copy received from

the supplier and punching of

the invoices in the payment

register is a comprehensive

control for the purchases and

payment to vendors (Gooley,

2016).

This alleviates the risks that

the false purchases are not

recorded in the system, there

is no shortage or discrepancy

in the inventory when it is

being received in the factory

premises and that the invoice

from supplier and the order

received matches and then the

payment is being processed.

Due to this, no false invoices

and no false delivery is

accounted in the system.

The auditor can check

whether the 4 eye principle

was being ensured or not

during receiving or orders

and recording the invoices in

the system. Also, sample

checks can be conducted on

the order copies and the

invoices received

electronically from suppliers

if they are matching.

Question 2B

Besides the robust internal control process in several areas, the company also suffers from

weakness in a number of areas relating to purchases and accounts payable. Some of these are

mentioned below:

Weaknesses Justification

The supplier information file is being

centrally handed by the accounts clerk and

any changes to the file is being approved

manually by the management accountant.

There is no such record maintenance in

system as to how many times the changes

have been done and the management

accountant is the ultimate authority post

which no control is maintained (Werner,

2017)

The approval procedure is manual and hence

there is every chance that the management

accountant holds the ultimate authority to

make the changes in the supplier information

file. There may be a case that a new

unapproved supplier may be added to the file

without any intimation and nobody in the

company would be aware of the same and

hence the records should be maintained in the

system.

The payments file is finally being approved This shows that there is no segregation of

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

by the management accountant once in a

week and then he only uploads the ABA file

in the bank portal for the payment.

duties and the company may fall into situation

where the management accountant may also

approve for the unauthorised and unchecked

payments and upload the same in the bank

portal for the payment. The company might

suffer a loss on account of this. Therefore,

there should be proper internal control and 4

eye principle being followed here

(Heminway, 2017).

With regards to the payment of the service as

well as supplier invoices, as soon as the

invoice is being punched in the payments file

and approved by management accountant, it is

being recorded as paid in the accounting

system without proper acknowledgement

system or procedure. This can lead to serious

reconciliation issues in the future with the

creditors.

To avoid the reconciliation issues with the

creditors in the future, the company should

ensure that the acknowledgement is generated

form the bank side and is also captured in the

payments file and is also properly accounted

in the accounting system. Also, the balance

confirmation from the creditors and the

vendors should be asked on a monthly basis

(Trieu, 2017).

There is no control om when the next

purchases of the wine, grape or beef should be

made by the section managers. There should

be a limit on the stock which when reached,

only then the next order should be made

(Linden & Freeman, 2017).

In case this control is not being maintained or

implemented, then the section managers can

send the purchase requisition for any and

every quantity and it would be difficult for the

company to maintain and monitor the stock

levels and thus it can end up having excess

stocks.

10 | P a g e

by the management accountant once in a

week and then he only uploads the ABA file

in the bank portal for the payment.

duties and the company may fall into situation

where the management accountant may also

approve for the unauthorised and unchecked

payments and upload the same in the bank

portal for the payment. The company might

suffer a loss on account of this. Therefore,

there should be proper internal control and 4

eye principle being followed here

(Heminway, 2017).

With regards to the payment of the service as

well as supplier invoices, as soon as the

invoice is being punched in the payments file

and approved by management accountant, it is

being recorded as paid in the accounting

system without proper acknowledgement

system or procedure. This can lead to serious

reconciliation issues in the future with the

creditors.

To avoid the reconciliation issues with the

creditors in the future, the company should

ensure that the acknowledgement is generated

form the bank side and is also captured in the

payments file and is also properly accounted

in the accounting system. Also, the balance

confirmation from the creditors and the

vendors should be asked on a monthly basis

(Trieu, 2017).

There is no control om when the next

purchases of the wine, grape or beef should be

made by the section managers. There should

be a limit on the stock which when reached,

only then the next order should be made

(Linden & Freeman, 2017).

In case this control is not being maintained or

implemented, then the section managers can

send the purchase requisition for any and

every quantity and it would be difficult for the

company to maintain and monitor the stock

levels and thus it can end up having excess

stocks.

10 | P a g e

11

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Bizfluent. (2017). Advantages & Disadvantages of Internal Control. Retrieved december 07, 2017, from

https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Chron. (2017). five-common-features-internal-control-system-business. Retrieved december 07, 2017,

from http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. Retrieved from https://doi.org/10.1080/00014788.2017.1299620

Gooley, J. (2016). Principles of Australian Contract Law. Australia: Lexis Nexis.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 1-35.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Saeidi, F. (2012). Audit expectations gap and corporate fraud: Empirical evidence from Iran. African

Journal of Business Management, 6(23), 7031-41. Retrieved from search.proquest.com

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

11 | P a g e

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Bizfluent. (2017). Advantages & Disadvantages of Internal Control. Retrieved december 07, 2017, from

https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Chron. (2017). five-common-features-internal-control-system-business. Retrieved december 07, 2017,

from http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. Retrieved from https://doi.org/10.1080/00014788.2017.1299620

Gooley, J. (2016). Principles of Australian Contract Law. Australia: Lexis Nexis.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 1-35.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), 353-379. Retrieved from https://doi.org/10.1017/beq.2017.1

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Saeidi, F. (2012). Audit expectations gap and corporate fraud: Empirical evidence from Iran. African

Journal of Business Management, 6(23), 7031-41. Retrieved from search.proquest.com

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.