Addressing Specific Audit Situations in Auditing and Assurance in Australia

VerifiedAdded on 2022/12/27

|16

|4293

|49

AI Summary

This memo discusses the identification of potential audit risks and the corresponding audit procedures to address them in the context of auditing and assurance in Australia. It also highlights the weaknesses in the internal control system and suggests audit procedures to mitigate these risks. The memo focuses on specific financial ratios and their analysis, such as current ratio, quick assets ratio, return on equity, return on assets, gross margin, marketing expenses, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDITING AND ASSURANCE IN AUSTRALIA

Auditing and Assurance in Australia

Name of the Student

Name of the University

Author’s Note

Auditing and Assurance in Australia

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1AUDITING AND ASSURANCE IN AUSTRALIA

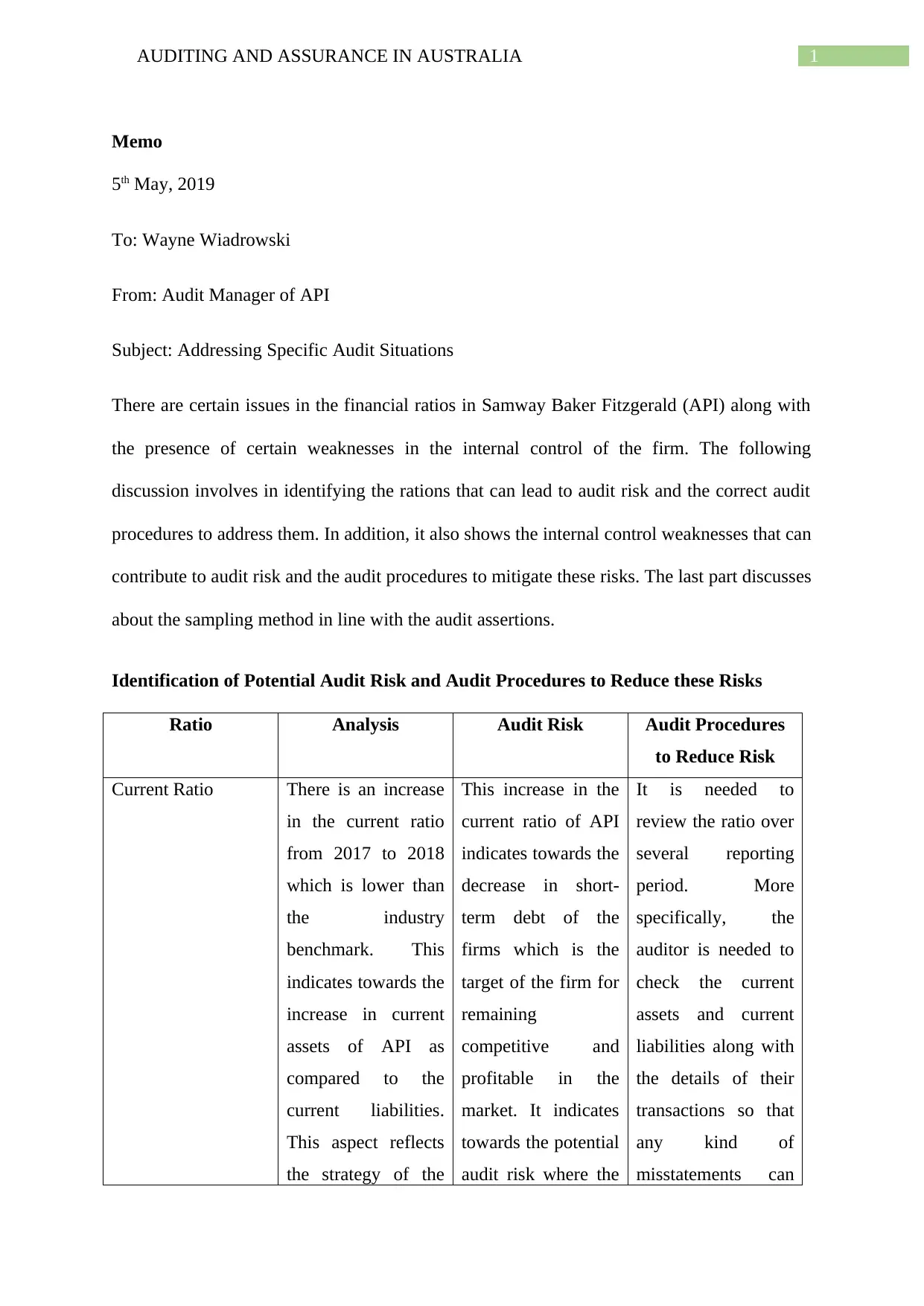

Memo

5th May, 2019

To: Wayne Wiadrowski

From: Audit Manager of API

Subject: Addressing Specific Audit Situations

There are certain issues in the financial ratios in Samway Baker Fitzgerald (API) along with

the presence of certain weaknesses in the internal control of the firm. The following

discussion involves in identifying the rations that can lead to audit risk and the correct audit

procedures to address them. In addition, it also shows the internal control weaknesses that can

contribute to audit risk and the audit procedures to mitigate these risks. The last part discusses

about the sampling method in line with the audit assertions.

Identification of Potential Audit Risk and Audit Procedures to Reduce these Risks

Ratio Analysis Audit Risk Audit Procedures

to Reduce Risk

Current Ratio There is an increase

in the current ratio

from 2017 to 2018

which is lower than

the industry

benchmark. This

indicates towards the

increase in current

assets of API as

compared to the

current liabilities.

This aspect reflects

the strategy of the

This increase in the

current ratio of API

indicates towards the

decrease in short-

term debt of the

firms which is the

target of the firm for

remaining

competitive and

profitable in the

market. It indicates

towards the potential

audit risk where the

It is needed to

review the ratio over

several reporting

period. More

specifically, the

auditor is needed to

check the current

assets and current

liabilities along with

the details of their

transactions so that

any kind of

misstatements can

Memo

5th May, 2019

To: Wayne Wiadrowski

From: Audit Manager of API

Subject: Addressing Specific Audit Situations

There are certain issues in the financial ratios in Samway Baker Fitzgerald (API) along with

the presence of certain weaknesses in the internal control of the firm. The following

discussion involves in identifying the rations that can lead to audit risk and the correct audit

procedures to address them. In addition, it also shows the internal control weaknesses that can

contribute to audit risk and the audit procedures to mitigate these risks. The last part discusses

about the sampling method in line with the audit assertions.

Identification of Potential Audit Risk and Audit Procedures to Reduce these Risks

Ratio Analysis Audit Risk Audit Procedures

to Reduce Risk

Current Ratio There is an increase

in the current ratio

from 2017 to 2018

which is lower than

the industry

benchmark. This

indicates towards the

increase in current

assets of API as

compared to the

current liabilities.

This aspect reflects

the strategy of the

This increase in the

current ratio of API

indicates towards the

decrease in short-

term debt of the

firms which is the

target of the firm for

remaining

competitive and

profitable in the

market. It indicates

towards the potential

audit risk where the

It is needed to

review the ratio over

several reporting

period. More

specifically, the

auditor is needed to

check the current

assets and current

liabilities along with

the details of their

transactions so that

any kind of

misstatements can

2AUDITING AND ASSURANCE IN AUSTRALIA

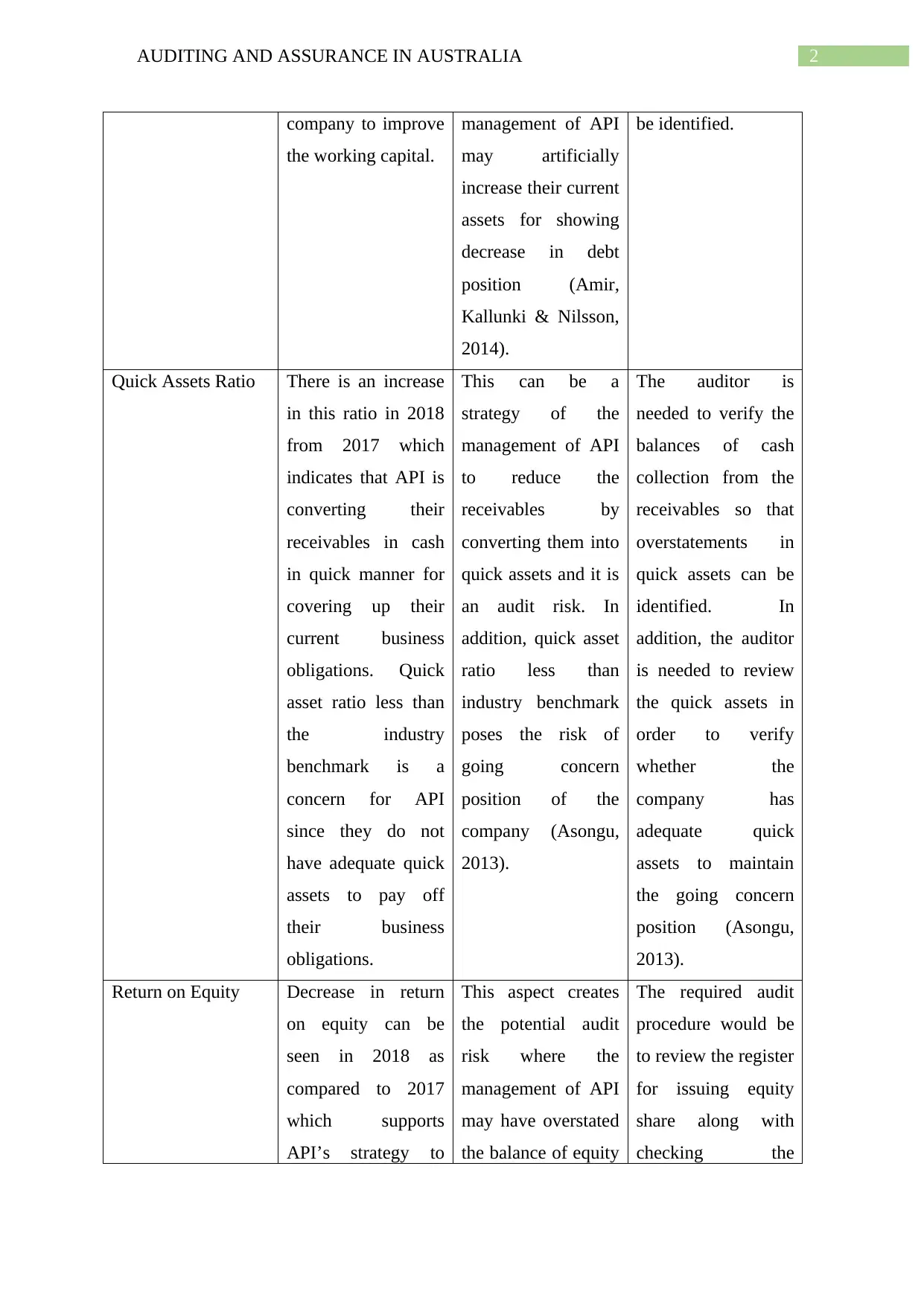

company to improve

the working capital.

management of API

may artificially

increase their current

assets for showing

decrease in debt

position (Amir,

Kallunki & Nilsson,

2014).

be identified.

Quick Assets Ratio There is an increase

in this ratio in 2018

from 2017 which

indicates that API is

converting their

receivables in cash

in quick manner for

covering up their

current business

obligations. Quick

asset ratio less than

the industry

benchmark is a

concern for API

since they do not

have adequate quick

assets to pay off

their business

obligations.

This can be a

strategy of the

management of API

to reduce the

receivables by

converting them into

quick assets and it is

an audit risk. In

addition, quick asset

ratio less than

industry benchmark

poses the risk of

going concern

position of the

company (Asongu,

2013).

The auditor is

needed to verify the

balances of cash

collection from the

receivables so that

overstatements in

quick assets can be

identified. In

addition, the auditor

is needed to review

the quick assets in

order to verify

whether the

company has

adequate quick

assets to maintain

the going concern

position (Asongu,

2013).

Return on Equity Decrease in return

on equity can be

seen in 2018 as

compared to 2017

which supports

API’s strategy to

This aspect creates

the potential audit

risk where the

management of API

may have overstated

the balance of equity

The required audit

procedure would be

to review the register

for issuing equity

share along with

checking the

company to improve

the working capital.

management of API

may artificially

increase their current

assets for showing

decrease in debt

position (Amir,

Kallunki & Nilsson,

2014).

be identified.

Quick Assets Ratio There is an increase

in this ratio in 2018

from 2017 which

indicates that API is

converting their

receivables in cash

in quick manner for

covering up their

current business

obligations. Quick

asset ratio less than

the industry

benchmark is a

concern for API

since they do not

have adequate quick

assets to pay off

their business

obligations.

This can be a

strategy of the

management of API

to reduce the

receivables by

converting them into

quick assets and it is

an audit risk. In

addition, quick asset

ratio less than

industry benchmark

poses the risk of

going concern

position of the

company (Asongu,

2013).

The auditor is

needed to verify the

balances of cash

collection from the

receivables so that

overstatements in

quick assets can be

identified. In

addition, the auditor

is needed to review

the quick assets in

order to verify

whether the

company has

adequate quick

assets to maintain

the going concern

position (Asongu,

2013).

Return on Equity Decrease in return

on equity can be

seen in 2018 as

compared to 2017

which supports

API’s strategy to

This aspect creates

the potential audit

risk where the

management of API

may have overstated

the balance of equity

The required audit

procedure would be

to review the register

for issuing equity

share along with

checking the

3AUDITING AND ASSURANCE IN AUSTRALIA

reduce debts for

staying competitive.

It indicates towards

the decrease in debts

of the company due

to the increase in

equity share capital.

capital so that total

debts can be

decreased in the

books.

resolution of the

Board of API in

order to ensure

whether there is any

overstatement on the

equity share capital

of the company or

not (Freedman &

Nutting, 2015).

Return on Total

Assets

It can be seen that

there is decrease in

this ration in 2018

from 2017. It

indicates that the

total assets of the

company have

increased due to the

decrease in profit. It

is also lower than

the industry

benchmark.

This can lead to

potential audit risk

where the

management of API

may have

understated the

profit as a part of

their strategy to

remain competitive

in the market. This

has led to the

increase in total

assets of the firm

(Ghosh & Tang,

2015).

The appropriate

audit procedure in

this case would be to

test the vouchers as

well receipts of the

purchase and sale of

assets with the aim

to determine

whether there is

actual increase in the

profit in the current

year. This would

also help in

determining the

understatement of

profit.

Gross Margin Major decrease in

gross margin can be

seen in 2018 from

2017. This gross

margin of API is

also lower than the

industry benchmark.

Decrease in sales

This can lead to the

audit risk of

understatement in

sales as well as

overstatement of

expenses for

showing less gross

profit margin. The

The main audit

procedure for the

auditor would be to

review the sales

balance of API at the

end of 201 along

with checking the

sales vouchers and

reduce debts for

staying competitive.

It indicates towards

the decrease in debts

of the company due

to the increase in

equity share capital.

capital so that total

debts can be

decreased in the

books.

resolution of the

Board of API in

order to ensure

whether there is any

overstatement on the

equity share capital

of the company or

not (Freedman &

Nutting, 2015).

Return on Total

Assets

It can be seen that

there is decrease in

this ration in 2018

from 2017. It

indicates that the

total assets of the

company have

increased due to the

decrease in profit. It

is also lower than

the industry

benchmark.

This can lead to

potential audit risk

where the

management of API

may have

understated the

profit as a part of

their strategy to

remain competitive

in the market. This

has led to the

increase in total

assets of the firm

(Ghosh & Tang,

2015).

The appropriate

audit procedure in

this case would be to

test the vouchers as

well receipts of the

purchase and sale of

assets with the aim

to determine

whether there is

actual increase in the

profit in the current

year. This would

also help in

determining the

understatement of

profit.

Gross Margin Major decrease in

gross margin can be

seen in 2018 from

2017. This gross

margin of API is

also lower than the

industry benchmark.

Decrease in sales

This can lead to the

audit risk of

understatement in

sales as well as

overstatement of

expenses for

showing less gross

profit margin. The

The main audit

procedure for the

auditor would be to

review the sales

balance of API at the

end of 201 along

with checking the

sales vouchers and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4AUDITING AND ASSURANCE IN AUSTRALIA

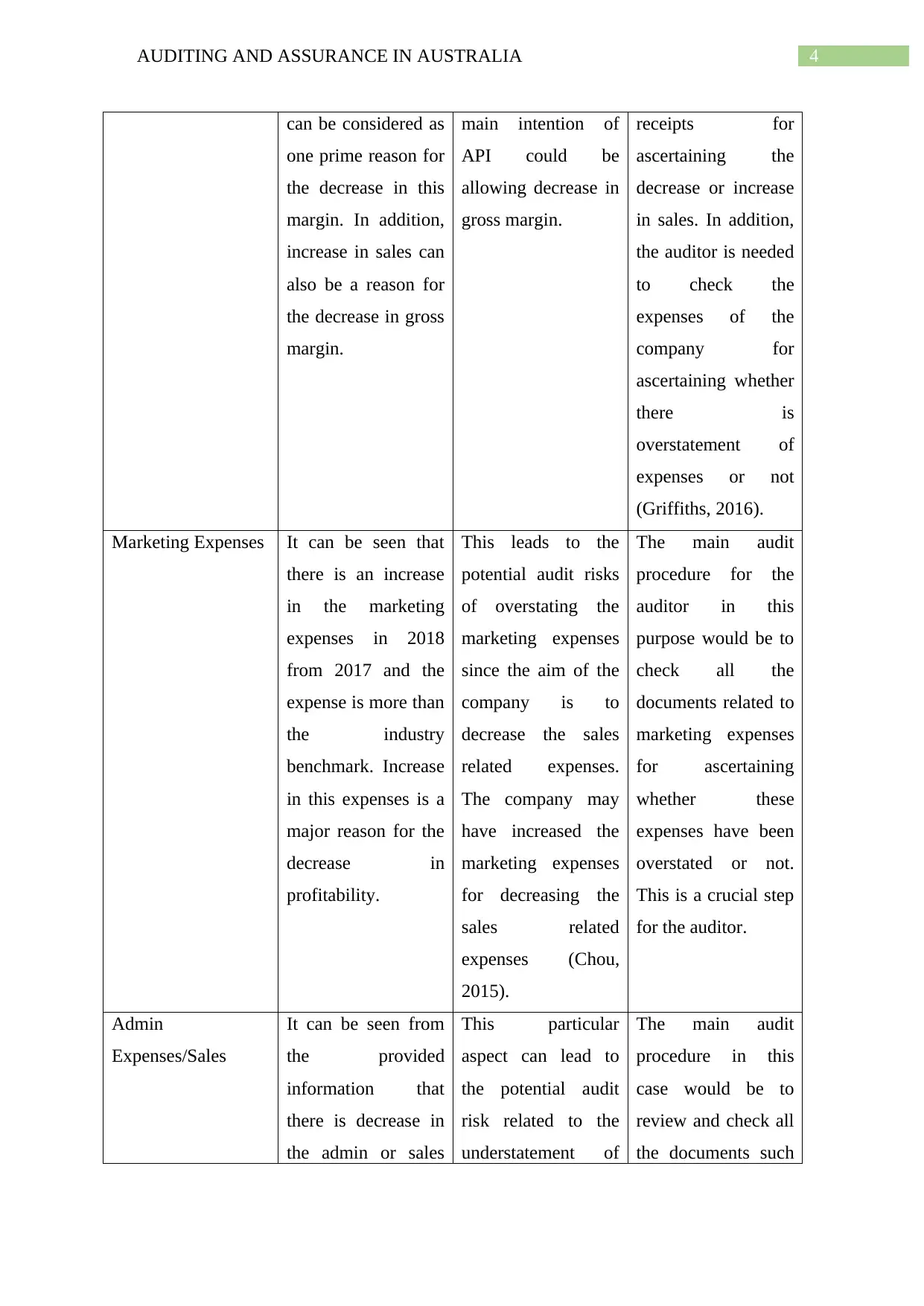

can be considered as

one prime reason for

the decrease in this

margin. In addition,

increase in sales can

also be a reason for

the decrease in gross

margin.

main intention of

API could be

allowing decrease in

gross margin.

receipts for

ascertaining the

decrease or increase

in sales. In addition,

the auditor is needed

to check the

expenses of the

company for

ascertaining whether

there is

overstatement of

expenses or not

(Griffiths, 2016).

Marketing Expenses It can be seen that

there is an increase

in the marketing

expenses in 2018

from 2017 and the

expense is more than

the industry

benchmark. Increase

in this expenses is a

major reason for the

decrease in

profitability.

This leads to the

potential audit risks

of overstating the

marketing expenses

since the aim of the

company is to

decrease the sales

related expenses.

The company may

have increased the

marketing expenses

for decreasing the

sales related

expenses (Chou,

2015).

The main audit

procedure for the

auditor in this

purpose would be to

check all the

documents related to

marketing expenses

for ascertaining

whether these

expenses have been

overstated or not.

This is a crucial step

for the auditor.

Admin

Expenses/Sales

It can be seen from

the provided

information that

there is decrease in

the admin or sales

This particular

aspect can lead to

the potential audit

risk related to the

understatement of

The main audit

procedure in this

case would be to

review and check all

the documents such

can be considered as

one prime reason for

the decrease in this

margin. In addition,

increase in sales can

also be a reason for

the decrease in gross

margin.

main intention of

API could be

allowing decrease in

gross margin.

receipts for

ascertaining the

decrease or increase

in sales. In addition,

the auditor is needed

to check the

expenses of the

company for

ascertaining whether

there is

overstatement of

expenses or not

(Griffiths, 2016).

Marketing Expenses It can be seen that

there is an increase

in the marketing

expenses in 2018

from 2017 and the

expense is more than

the industry

benchmark. Increase

in this expenses is a

major reason for the

decrease in

profitability.

This leads to the

potential audit risks

of overstating the

marketing expenses

since the aim of the

company is to

decrease the sales

related expenses.

The company may

have increased the

marketing expenses

for decreasing the

sales related

expenses (Chou,

2015).

The main audit

procedure for the

auditor in this

purpose would be to

check all the

documents related to

marketing expenses

for ascertaining

whether these

expenses have been

overstated or not.

This is a crucial step

for the auditor.

Admin

Expenses/Sales

It can be seen from

the provided

information that

there is decrease in

the admin or sales

This particular

aspect can lead to

the potential audit

risk related to the

understatement of

The main audit

procedure in this

case would be to

review and check all

the documents such

5AUDITING AND ASSURANCE IN AUSTRALIA

expenses of API

from 2017 to 2018

and the company has

been able in

achieving the

budgeted figure for

this. This is in line

with the strategy of

the company of cost

cutting.

administrative and

sales expense due to

the cost cutting

strategy of the

company.

as vouchers and

receipts related to

the administrative

and sales expenses

in order to ascertain

the fact that whether

there is any

understatement of

these expenses or

not. This is a crucial

audit procedure that

is related to

company’s

profitability

(Knechel & Salterio,

2016).

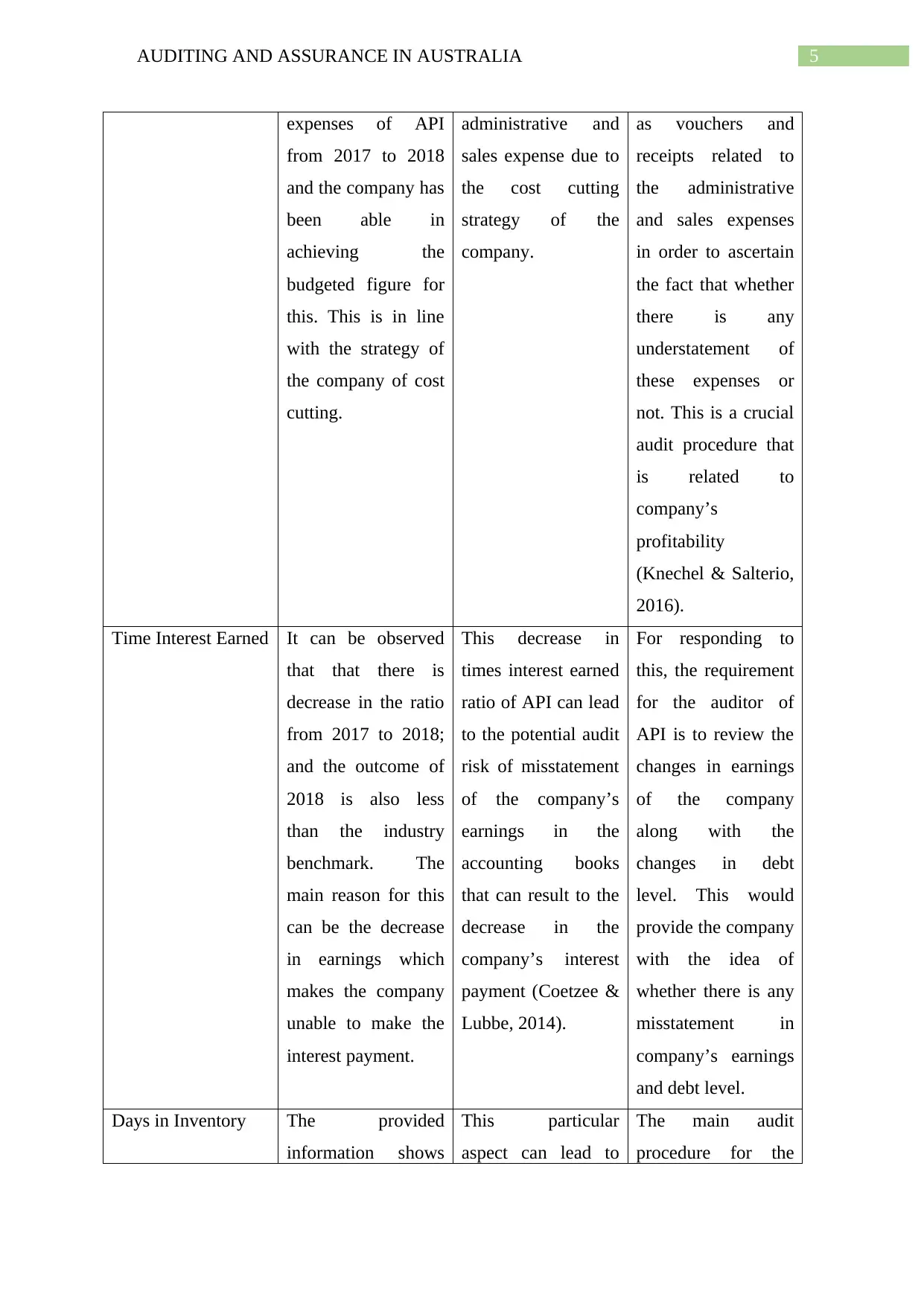

Time Interest Earned It can be observed

that that there is

decrease in the ratio

from 2017 to 2018;

and the outcome of

2018 is also less

than the industry

benchmark. The

main reason for this

can be the decrease

in earnings which

makes the company

unable to make the

interest payment.

This decrease in

times interest earned

ratio of API can lead

to the potential audit

risk of misstatement

of the company’s

earnings in the

accounting books

that can result to the

decrease in the

company’s interest

payment (Coetzee &

Lubbe, 2014).

For responding to

this, the requirement

for the auditor of

API is to review the

changes in earnings

of the company

along with the

changes in debt

level. This would

provide the company

with the idea of

whether there is any

misstatement in

company’s earnings

and debt level.

Days in Inventory The provided

information shows

This particular

aspect can lead to

The main audit

procedure for the

expenses of API

from 2017 to 2018

and the company has

been able in

achieving the

budgeted figure for

this. This is in line

with the strategy of

the company of cost

cutting.

administrative and

sales expense due to

the cost cutting

strategy of the

company.

as vouchers and

receipts related to

the administrative

and sales expenses

in order to ascertain

the fact that whether

there is any

understatement of

these expenses or

not. This is a crucial

audit procedure that

is related to

company’s

profitability

(Knechel & Salterio,

2016).

Time Interest Earned It can be observed

that that there is

decrease in the ratio

from 2017 to 2018;

and the outcome of

2018 is also less

than the industry

benchmark. The

main reason for this

can be the decrease

in earnings which

makes the company

unable to make the

interest payment.

This decrease in

times interest earned

ratio of API can lead

to the potential audit

risk of misstatement

of the company’s

earnings in the

accounting books

that can result to the

decrease in the

company’s interest

payment (Coetzee &

Lubbe, 2014).

For responding to

this, the requirement

for the auditor of

API is to review the

changes in earnings

of the company

along with the

changes in debt

level. This would

provide the company

with the idea of

whether there is any

misstatement in

company’s earnings

and debt level.

Days in Inventory The provided

information shows

This particular

aspect can lead to

The main audit

procedure for the

6AUDITING AND ASSURANCE IN AUSTRALIA

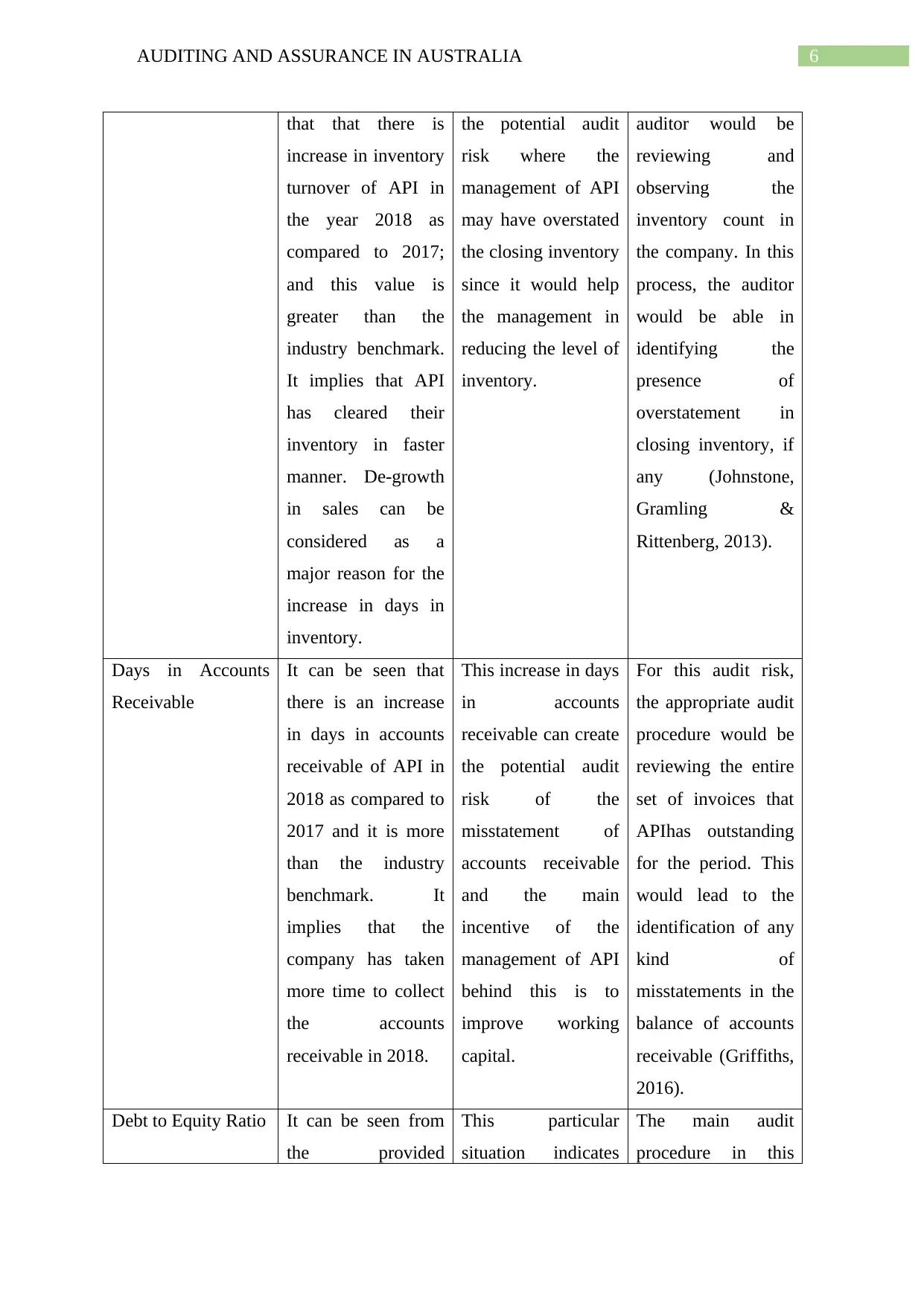

that that there is

increase in inventory

turnover of API in

the year 2018 as

compared to 2017;

and this value is

greater than the

industry benchmark.

It implies that API

has cleared their

inventory in faster

manner. De-growth

in sales can be

considered as a

major reason for the

increase in days in

inventory.

the potential audit

risk where the

management of API

may have overstated

the closing inventory

since it would help

the management in

reducing the level of

inventory.

auditor would be

reviewing and

observing the

inventory count in

the company. In this

process, the auditor

would be able in

identifying the

presence of

overstatement in

closing inventory, if

any (Johnstone,

Gramling &

Rittenberg, 2013).

Days in Accounts

Receivable

It can be seen that

there is an increase

in days in accounts

receivable of API in

2018 as compared to

2017 and it is more

than the industry

benchmark. It

implies that the

company has taken

more time to collect

the accounts

receivable in 2018.

This increase in days

in accounts

receivable can create

the potential audit

risk of the

misstatement of

accounts receivable

and the main

incentive of the

management of API

behind this is to

improve working

capital.

For this audit risk,

the appropriate audit

procedure would be

reviewing the entire

set of invoices that

APIhas outstanding

for the period. This

would lead to the

identification of any

kind of

misstatements in the

balance of accounts

receivable (Griffiths,

2016).

Debt to Equity Ratio It can be seen from

the provided

This particular

situation indicates

The main audit

procedure in this

that that there is

increase in inventory

turnover of API in

the year 2018 as

compared to 2017;

and this value is

greater than the

industry benchmark.

It implies that API

has cleared their

inventory in faster

manner. De-growth

in sales can be

considered as a

major reason for the

increase in days in

inventory.

the potential audit

risk where the

management of API

may have overstated

the closing inventory

since it would help

the management in

reducing the level of

inventory.

auditor would be

reviewing and

observing the

inventory count in

the company. In this

process, the auditor

would be able in

identifying the

presence of

overstatement in

closing inventory, if

any (Johnstone,

Gramling &

Rittenberg, 2013).

Days in Accounts

Receivable

It can be seen that

there is an increase

in days in accounts

receivable of API in

2018 as compared to

2017 and it is more

than the industry

benchmark. It

implies that the

company has taken

more time to collect

the accounts

receivable in 2018.

This increase in days

in accounts

receivable can create

the potential audit

risk of the

misstatement of

accounts receivable

and the main

incentive of the

management of API

behind this is to

improve working

capital.

For this audit risk,

the appropriate audit

procedure would be

reviewing the entire

set of invoices that

APIhas outstanding

for the period. This

would lead to the

identification of any

kind of

misstatements in the

balance of accounts

receivable (Griffiths,

2016).

Debt to Equity Ratio It can be seen from

the provided

This particular

situation indicates

The main audit

procedure in this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE IN AUSTRALIA

information that

there is increase in

the debt-to-equity

ratio of API in 2018

as compared to 2017

and it is more than

the industry

benchmark. This

increase implies that

the company has

increased equity

share capital as

compared to the debt

capital due to the

company’s strategy

to decrease the level

of debt.

towards the presence

of a potential audit

risk of overstatement

of equity share

capital so that

decreased level of

debt can be shown.

This would lead to

drop in debt level for

ensuring the

presence of healthy

cash flows.

case would be

checking the register

of share issue and

Board’s resolution

related to issue of

share. Moreover, the

auditor is needed to

review the necessary

documents for

verifying the level of

debts for

ascertaining the

misstatements in

share capital and

debts (Guénin-

Paracini, Malsch &

Paillé, 2014).

Internal Control Weaknesses and Audit Procedures

Internal Control Weakness Audit Risk Audit Procedures

API’s account clerk has both

the responsibility of filling

the purchase order as well as

the second copy if GRN.

This weakness can lead to

the audit risk where there

will be major implications

on the purchase orders. This

can lead to over or under

orders of the raw materials

(Feng et al., 2014).

The audit procedure would

be to ensure the presence of

specific approval authority

that will be authorized for

reviewing the purchase

order related transactions

and it would add a layer of

responsibility to the

purchase order transactions.

The production controller is

responsible for filling the

production orders and his

copy is used for matching

the production order.

This weakness can lead to

the audit risk of

misstatements in production

orders and it will not be

possible to identify this

The appropriate audit

procedure in this situation

would be to ensure the

presence of approval

authority for the purposes of

information that

there is increase in

the debt-to-equity

ratio of API in 2018

as compared to 2017

and it is more than

the industry

benchmark. This

increase implies that

the company has

increased equity

share capital as

compared to the debt

capital due to the

company’s strategy

to decrease the level

of debt.

towards the presence

of a potential audit

risk of overstatement

of equity share

capital so that

decreased level of

debt can be shown.

This would lead to

drop in debt level for

ensuring the

presence of healthy

cash flows.

case would be

checking the register

of share issue and

Board’s resolution

related to issue of

share. Moreover, the

auditor is needed to

review the necessary

documents for

verifying the level of

debts for

ascertaining the

misstatements in

share capital and

debts (Guénin-

Paracini, Malsch &

Paillé, 2014).

Internal Control Weaknesses and Audit Procedures

Internal Control Weakness Audit Risk Audit Procedures

API’s account clerk has both

the responsibility of filling

the purchase order as well as

the second copy if GRN.

This weakness can lead to

the audit risk where there

will be major implications

on the purchase orders. This

can lead to over or under

orders of the raw materials

(Feng et al., 2014).

The audit procedure would

be to ensure the presence of

specific approval authority

that will be authorized for

reviewing the purchase

order related transactions

and it would add a layer of

responsibility to the

purchase order transactions.

The production controller is

responsible for filling the

production orders and his

copy is used for matching

the production order.

This weakness can lead to

the audit risk of

misstatements in production

orders and it will not be

possible to identify this

The appropriate audit

procedure in this situation

would be to ensure the

presence of approval

authority for the purposes of

8AUDITING AND ASSURANCE IN AUSTRALIA

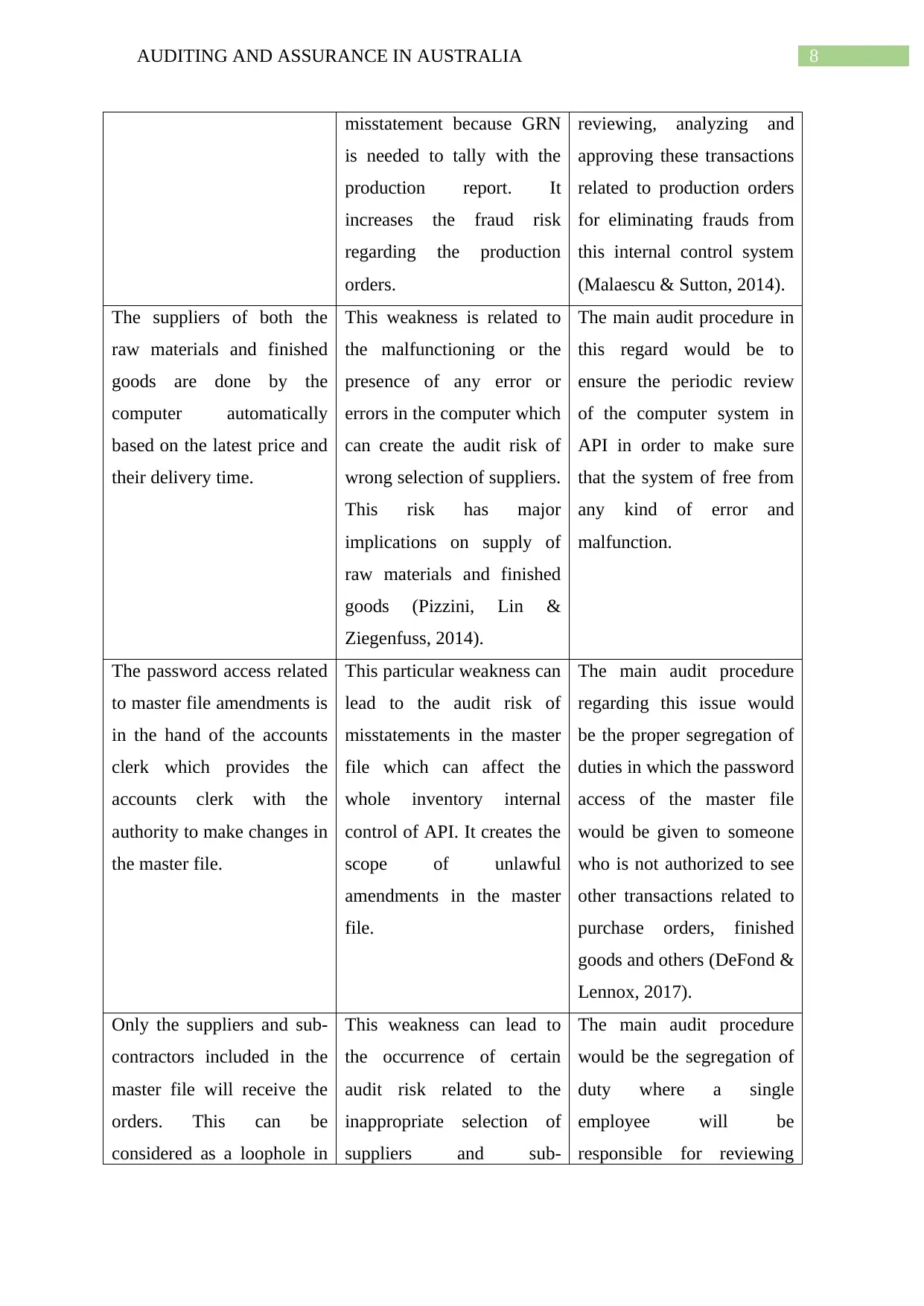

misstatement because GRN

is needed to tally with the

production report. It

increases the fraud risk

regarding the production

orders.

reviewing, analyzing and

approving these transactions

related to production orders

for eliminating frauds from

this internal control system

(Malaescu & Sutton, 2014).

The suppliers of both the

raw materials and finished

goods are done by the

computer automatically

based on the latest price and

their delivery time.

This weakness is related to

the malfunctioning or the

presence of any error or

errors in the computer which

can create the audit risk of

wrong selection of suppliers.

This risk has major

implications on supply of

raw materials and finished

goods (Pizzini, Lin &

Ziegenfuss, 2014).

The main audit procedure in

this regard would be to

ensure the periodic review

of the computer system in

API in order to make sure

that the system of free from

any kind of error and

malfunction.

The password access related

to master file amendments is

in the hand of the accounts

clerk which provides the

accounts clerk with the

authority to make changes in

the master file.

This particular weakness can

lead to the audit risk of

misstatements in the master

file which can affect the

whole inventory internal

control of API. It creates the

scope of unlawful

amendments in the master

file.

The main audit procedure

regarding this issue would

be the proper segregation of

duties in which the password

access of the master file

would be given to someone

who is not authorized to see

other transactions related to

purchase orders, finished

goods and others (DeFond &

Lennox, 2017).

Only the suppliers and sub-

contractors included in the

master file will receive the

orders. This can be

considered as a loophole in

This weakness can lead to

the occurrence of certain

audit risk related to the

inappropriate selection of

suppliers and sub-

The main audit procedure

would be the segregation of

duty where a single

employee will be

responsible for reviewing

misstatement because GRN

is needed to tally with the

production report. It

increases the fraud risk

regarding the production

orders.

reviewing, analyzing and

approving these transactions

related to production orders

for eliminating frauds from

this internal control system

(Malaescu & Sutton, 2014).

The suppliers of both the

raw materials and finished

goods are done by the

computer automatically

based on the latest price and

their delivery time.

This weakness is related to

the malfunctioning or the

presence of any error or

errors in the computer which

can create the audit risk of

wrong selection of suppliers.

This risk has major

implications on supply of

raw materials and finished

goods (Pizzini, Lin &

Ziegenfuss, 2014).

The main audit procedure in

this regard would be to

ensure the periodic review

of the computer system in

API in order to make sure

that the system of free from

any kind of error and

malfunction.

The password access related

to master file amendments is

in the hand of the accounts

clerk which provides the

accounts clerk with the

authority to make changes in

the master file.

This particular weakness can

lead to the audit risk of

misstatements in the master

file which can affect the

whole inventory internal

control of API. It creates the

scope of unlawful

amendments in the master

file.

The main audit procedure

regarding this issue would

be the proper segregation of

duties in which the password

access of the master file

would be given to someone

who is not authorized to see

other transactions related to

purchase orders, finished

goods and others (DeFond &

Lennox, 2017).

Only the suppliers and sub-

contractors included in the

master file will receive the

orders. This can be

considered as a loophole in

This weakness can lead to

the occurrence of certain

audit risk related to the

inappropriate selection of

suppliers and sub-

The main audit procedure

would be the segregation of

duty where a single

employee will be

responsible for reviewing

9AUDITING AND ASSURANCE IN AUSTRALIA

the internal control

regarding inventory.

contractors. This is because

the personnel have access to

the master file and other

transactions like purchase

orders can intentionally

change the names of

suppliers and sub-

contractors (Mat Zain,

Zaman & Mohamed, 2015).

the master file in order to

prevent the intentionally

wrong amendments in the

master file.

The right to bring changes in

the master file in the

transactions of finished

goods and raw materials is

in the hands of the

production controller which

is a weakness in the

inventory internal control.

This weakness can lead to

the misstatements in the

master file in the absence of

any procedure for reviewing

the changes that the

production controller has

made except the amendment

form.

The appropriate audit

procedure regarding this

issue would be to deter the

production controller from

bringing changes in the

master file and to ensure the

presence of an employee

who will be responsible for

this (Clinton, Pinello &

Skaife, 2014).

The ability of the inventory

system for producing a

complete stock listing in the

presence of the above-

discussed inventory control

weaknesses.

This weakness can lead to

the audit risk of

misstatements in the

complete stock listing due to

the presence of the issues

like illegal amendments in

master file and others (Sun,

2016).

The main audit process in

this case would be

conducting periodic

reconciliation of the whole

accounting system so that

the weaknesses in the

inventory internal control

can be identified and correct

stock listing can be

produced.

The stock sheet reports do

not include the quantities of

the stocks since the count

teams complete this. The

This aspect can lead to the

audit risk of non-detection

wrong inventory count by

the count teams which can

The appropriate audit step

regarding this issue would

be to ensure observing and

reviewing the inventory

the internal control

regarding inventory.

contractors. This is because

the personnel have access to

the master file and other

transactions like purchase

orders can intentionally

change the names of

suppliers and sub-

contractors (Mat Zain,

Zaman & Mohamed, 2015).

the master file in order to

prevent the intentionally

wrong amendments in the

master file.

The right to bring changes in

the master file in the

transactions of finished

goods and raw materials is

in the hands of the

production controller which

is a weakness in the

inventory internal control.

This weakness can lead to

the misstatements in the

master file in the absence of

any procedure for reviewing

the changes that the

production controller has

made except the amendment

form.

The appropriate audit

procedure regarding this

issue would be to deter the

production controller from

bringing changes in the

master file and to ensure the

presence of an employee

who will be responsible for

this (Clinton, Pinello &

Skaife, 2014).

The ability of the inventory

system for producing a

complete stock listing in the

presence of the above-

discussed inventory control

weaknesses.

This weakness can lead to

the audit risk of

misstatements in the

complete stock listing due to

the presence of the issues

like illegal amendments in

master file and others (Sun,

2016).

The main audit process in

this case would be

conducting periodic

reconciliation of the whole

accounting system so that

the weaknesses in the

inventory internal control

can be identified and correct

stock listing can be

produced.

The stock sheet reports do

not include the quantities of

the stocks since the count

teams complete this. The

This aspect can lead to the

audit risk of non-detection

wrong inventory count by

the count teams which can

The appropriate audit step

regarding this issue would

be to ensure observing and

reviewing the inventory

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10AUDITING AND ASSURANCE IN AUSTRALIA

absence of quantity is a

weakness in the whole

inventory control system.

affect the stock sheet report. counting process. If

necessary, re-performing the

inventory count process

needs to be done for

ensuring the elimination of

inappropriateness in the

inventory counting process

(Daniela & Attila, 2013).

Selection of Samples for Undertaking Testing

Assertion Which Population? Sample Selection

Method

Justification for the

Sample Selection

Method

Existence This particular assertion

of existence assists the

auditors in testing if the

transactions related to

inventory actually occur

or not (Titera, 2013).

Thus, in order to address

this assertion, Wayne

needs to select the

sample from the

inventory purchase with

the aim to vouch them to

purchase requisitions as

well as receiving reports.

Vouching refers to

consider a recorded

amount and track it back

to the supporting

document.

In order to select the

sample from the

inventory purchase,

Wayne needs to select

the method of random

sampling. Under this

method, Wayne will

be required to select a

random sample of

inventory purchase

stock takes generated

by the inventory

system from a random

number table with the

presence of document

numbers (Christensen,

Elder, & Glover,

2014).

The main reason

behind the selection of

random sampling is

that this sample

selection method

ensure that the all the

items under the

selected population get

an equal chance of

selection through the

use of random number

tables on random

number generators.

This will provide

Wayne with ease of

use along with

accuracy in

representation. At the

same time, there is no

absence of quantity is a

weakness in the whole

inventory control system.

affect the stock sheet report. counting process. If

necessary, re-performing the

inventory count process

needs to be done for

ensuring the elimination of

inappropriateness in the

inventory counting process

(Daniela & Attila, 2013).

Selection of Samples for Undertaking Testing

Assertion Which Population? Sample Selection

Method

Justification for the

Sample Selection

Method

Existence This particular assertion

of existence assists the

auditors in testing if the

transactions related to

inventory actually occur

or not (Titera, 2013).

Thus, in order to address

this assertion, Wayne

needs to select the

sample from the

inventory purchase with

the aim to vouch them to

purchase requisitions as

well as receiving reports.

Vouching refers to

consider a recorded

amount and track it back

to the supporting

document.

In order to select the

sample from the

inventory purchase,

Wayne needs to select

the method of random

sampling. Under this

method, Wayne will

be required to select a

random sample of

inventory purchase

stock takes generated

by the inventory

system from a random

number table with the

presence of document

numbers (Christensen,

Elder, & Glover,

2014).

The main reason

behind the selection of

random sampling is

that this sample

selection method

ensure that the all the

items under the

selected population get

an equal chance of

selection through the

use of random number

tables on random

number generators.

This will provide

Wayne with ease of

use along with

accuracy in

representation. At the

same time, there is no

11AUDITING AND ASSURANCE IN AUSTRALIA

easier sampling

method than random

sampling that helps in

extracting large

population. In the

presence of all these

reasons, Wayne needs

to consider random

sampling method for

the examination of the

assertion of

completeness (Durney,

Elder & Glover, 2013).

Completeness This assertion deals with

whether all transactions

and accounts are

included that should be

presented in the financial

statements (Byrnes et al.,

2018). This assertion

deals with the biggest

risk that is inventory

understatement. With the

aim to test this particular

assertion, it is needed for

Wayne to take sample

from the inventory

receiving reports to the

inventory records with

the aim to make it sure

that these two reports

match.

With the aim to select

the sample from the

inventory receiving

reports, it is needed

for Wayne to select

systematic sample

selection method.

Under this method,

Wayne will be needed

to determine a uniform

interval through

dividing the number of

physical units in the

population by the

same size and then, it

needs to be rounded

up (Elder et al., 2013).

It needs to be

mentioned that the

main reason behind

selecting systematic

sampling method is

that this method adds

simplicity in the whole

auditing method. With

the help of this sample,

Wayne will be assured

on the fact that the

whole population will

be evenly samples

which is needed for the

examination of this

particular assertion. In

addition, the auditor

can ensure more

randomness in this

systematic sample

easier sampling

method than random

sampling that helps in

extracting large

population. In the

presence of all these

reasons, Wayne needs

to consider random

sampling method for

the examination of the

assertion of

completeness (Durney,

Elder & Glover, 2013).

Completeness This assertion deals with

whether all transactions

and accounts are

included that should be

presented in the financial

statements (Byrnes et al.,

2018). This assertion

deals with the biggest

risk that is inventory

understatement. With the

aim to test this particular

assertion, it is needed for

Wayne to take sample

from the inventory

receiving reports to the

inventory records with

the aim to make it sure

that these two reports

match.

With the aim to select

the sample from the

inventory receiving

reports, it is needed

for Wayne to select

systematic sample

selection method.

Under this method,

Wayne will be needed

to determine a uniform

interval through

dividing the number of

physical units in the

population by the

same size and then, it

needs to be rounded

up (Elder et al., 2013).

It needs to be

mentioned that the

main reason behind

selecting systematic

sampling method is

that this method adds

simplicity in the whole

auditing method. With

the help of this sample,

Wayne will be assured

on the fact that the

whole population will

be evenly samples

which is needed for the

examination of this

particular assertion. In

addition, the auditor

can ensure more

randomness in this

systematic sample

12AUDITING AND ASSURANCE IN AUSTRALIA

through the re-

computation of interval

each time with the use

of a random number

table. The presence of

these aspects is the

main reason behind the

selection of this

sampling method

(Lingard & Sellar,

2013).

through the re-

computation of interval

each time with the use

of a random number

table. The presence of

these aspects is the

main reason behind the

selection of this

sampling method

(Lingard & Sellar,

2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13AUDITING AND ASSURANCE IN AUSTRALIA

References

Amir, E., Kallunki, J. P., & Nilsson, H. (2014). The association between individual audit

partners’ risk preferences and the composition of their client portfolios. Review of

Accounting Studies, 19(1), 103-133.

Asongu, S. A. (2013). Post-crisis bank liquidity risk management disclosure. Qualitative

research in financial markets, 5(1), 65-84.

Byrnes, P. E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J. D., &

Vasarhelyi, M. (2018). Evolution of Auditing: From the Traditional Approach to the

Future Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297).

Emerald Publishing Limited.

Chou, D. C. (2015). Cloud computing risk and audit issues. Computer Standards &

Interfaces, 42, 137-142.

Christensen, B. E., Elder, R. J., & Glover, S. M. (2014). Behind the numbers: Insights into

large audit firm sampling policies. Accounting Horizons, 29(1), 61-81.

Clinton, S. B., Pinello, A. S., & Skaife, H. A. (2014). The implications of ineffective internal

control and SOX 404 reporting for financial analysts. Journal of Accounting and

Public Policy, 33(4), 303-327.

Coetzee, P., & Lubbe, D. (2014). Improving the efficiency and effectiveness of risk‐based

internal audit engagements. International Journal of Auditing, 18(2), 115-125.

Daniela, P., & Attila, T. (2013). Internal audit versus internal control and coaching. Procedia

Economics and Finance, 6, 694-702.

DeFond, M. L., & Lennox, C. S. (2017). Do PCAOB inspections improve the quality of

internal control audits?. Journal of Accounting Research, 55(3), 591-627.

References

Amir, E., Kallunki, J. P., & Nilsson, H. (2014). The association between individual audit

partners’ risk preferences and the composition of their client portfolios. Review of

Accounting Studies, 19(1), 103-133.

Asongu, S. A. (2013). Post-crisis bank liquidity risk management disclosure. Qualitative

research in financial markets, 5(1), 65-84.

Byrnes, P. E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J. D., &

Vasarhelyi, M. (2018). Evolution of Auditing: From the Traditional Approach to the

Future Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297).

Emerald Publishing Limited.

Chou, D. C. (2015). Cloud computing risk and audit issues. Computer Standards &

Interfaces, 42, 137-142.

Christensen, B. E., Elder, R. J., & Glover, S. M. (2014). Behind the numbers: Insights into

large audit firm sampling policies. Accounting Horizons, 29(1), 61-81.

Clinton, S. B., Pinello, A. S., & Skaife, H. A. (2014). The implications of ineffective internal

control and SOX 404 reporting for financial analysts. Journal of Accounting and

Public Policy, 33(4), 303-327.

Coetzee, P., & Lubbe, D. (2014). Improving the efficiency and effectiveness of risk‐based

internal audit engagements. International Journal of Auditing, 18(2), 115-125.

Daniela, P., & Attila, T. (2013). Internal audit versus internal control and coaching. Procedia

Economics and Finance, 6, 694-702.

DeFond, M. L., & Lennox, C. S. (2017). Do PCAOB inspections improve the quality of

internal control audits?. Journal of Accounting Research, 55(3), 591-627.

14AUDITING AND ASSURANCE IN AUSTRALIA

Durney, M., Elder, R. J., & Glover, S. M. (2013). Field data on accounting error rates and

audit sampling. Auditing: A Journal of Practice & Theory, 33(2), 79-110.

Elder, R. J., Akresh, A. D., Glover, S. M., Higgs, J. L., & Liljegren, J. (2013). Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of

Practice & Theory, 32(sp1), 99-129.

Feng, M., Li, C., McVay, S. E., & Skaife, H. (2014). Does ineffective internal control over

financial reporting affect a firm's operations? Evidence from firms' inventory

management. The Accounting Review, 90(2), 529-557.

Freedman, D. M., & Nutting, M. R. (2015). Equity crowdfunding for investors: A guide to

risks, returns, regulations, funding portals, due diligence, and deal terms. John Wiley

& Sons.

Ghosh, A., & Tang, C. Y. (2015). Auditor resignation and risk factors. Accounting

Horizons, 29(3), 529-549.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Guénin-Paracini, H., Malsch, B., & Paillé, A. M. (2014). Fear and risk in the audit

process. Accounting, Organizations and Society, 39(4), 264-288.

Johnstone, K., Gramling, A., & Rittenberg, L. E. (2013). Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Lingard, B., & Sellar, S. (2013). ‘Catalyst data’: Perverse systemic effects of audit and

accountability in Australian schooling. Journal of Education Policy, 28(5), 634-656.

Durney, M., Elder, R. J., & Glover, S. M. (2013). Field data on accounting error rates and

audit sampling. Auditing: A Journal of Practice & Theory, 33(2), 79-110.

Elder, R. J., Akresh, A. D., Glover, S. M., Higgs, J. L., & Liljegren, J. (2013). Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of

Practice & Theory, 32(sp1), 99-129.

Feng, M., Li, C., McVay, S. E., & Skaife, H. (2014). Does ineffective internal control over

financial reporting affect a firm's operations? Evidence from firms' inventory

management. The Accounting Review, 90(2), 529-557.

Freedman, D. M., & Nutting, M. R. (2015). Equity crowdfunding for investors: A guide to

risks, returns, regulations, funding portals, due diligence, and deal terms. John Wiley

& Sons.

Ghosh, A., & Tang, C. Y. (2015). Auditor resignation and risk factors. Accounting

Horizons, 29(3), 529-549.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Guénin-Paracini, H., Malsch, B., & Paillé, A. M. (2014). Fear and risk in the audit

process. Accounting, Organizations and Society, 39(4), 264-288.

Johnstone, K., Gramling, A., & Rittenberg, L. E. (2013). Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Lingard, B., & Sellar, S. (2013). ‘Catalyst data’: Perverse systemic effects of audit and

accountability in Australian schooling. Journal of Education Policy, 28(5), 634-656.

15AUDITING AND ASSURANCE IN AUSTRALIA

Malaescu, I., & Sutton, S. G. (2014). The reliance of external auditors on internal audit's use

of continuous audit. Journal of Information Systems, 29(1), 95-114.

Mat Zain, M., Zaman, M., & Mohamed, Z. (2015). The effect of internal audit function

quality and internal audit contribution to external audit on audit fees. International

Journal of Auditing, 19(3), 134-147.

Pizzini, M., Lin, S., & Ziegenfuss, D. E. (2014). The impact of internal audit function quality

and contribution on audit delay. Auditing: A Journal of Practice & Theory, 34(1), 25-

58.

Sun, Y. (2016). Internal control weakness disclosure and firm investment. Journal of

Accounting, Auditing & Finance, 31(2), 277-307.

Titera, W. R. (2013). Updating audit standard—Enabling audit data analysis. Journal of

Information Systems, 27(1), 325-331.

Malaescu, I., & Sutton, S. G. (2014). The reliance of external auditors on internal audit's use

of continuous audit. Journal of Information Systems, 29(1), 95-114.

Mat Zain, M., Zaman, M., & Mohamed, Z. (2015). The effect of internal audit function

quality and internal audit contribution to external audit on audit fees. International

Journal of Auditing, 19(3), 134-147.

Pizzini, M., Lin, S., & Ziegenfuss, D. E. (2014). The impact of internal audit function quality

and contribution on audit delay. Auditing: A Journal of Practice & Theory, 34(1), 25-

58.

Sun, Y. (2016). Internal control weakness disclosure and firm investment. Journal of

Accounting, Auditing & Finance, 31(2), 277-307.

Titera, W. R. (2013). Updating audit standard—Enabling audit data analysis. Journal of

Information Systems, 27(1), 325-331.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.