Discussion Regarding Audit Risks of API

Added on 2023-03-17

15 Pages3872 Words98 Views

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Author’s Note

Auditing

Name of the Student:

Name of the University:

Author’s Note

1

AUDITING

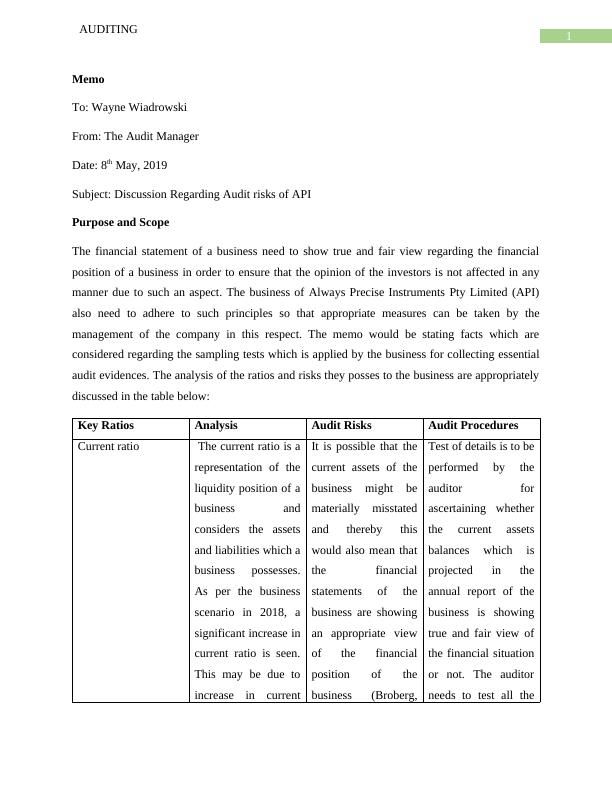

Memo

To: Wayne Wiadrowski

From: The Audit Manager

Date: 8th May, 2019

Subject: Discussion Regarding Audit risks of API

Purpose and Scope

The financial statement of a business need to show true and fair view regarding the financial

position of a business in order to ensure that the opinion of the investors is not affected in any

manner due to such an aspect. The business of Always Precise Instruments Pty Limited (API)

also need to adhere to such principles so that appropriate measures can be taken by the

management of the company in this respect. The memo would be stating facts which are

considered regarding the sampling tests which is applied by the business for collecting essential

audit evidences. The analysis of the ratios and risks they posses to the business are appropriately

discussed in the table below:

Key Ratios Analysis Audit Risks Audit Procedures

Current ratio The current ratio is a

representation of the

liquidity position of a

business and

considers the assets

and liabilities which a

business possesses.

As per the business

scenario in 2018, a

significant increase in

current ratio is seen.

This may be due to

increase in current

It is possible that the

current assets of the

business might be

materially misstated

and thereby this

would also mean that

the financial

statements of the

business are showing

an appropriate view

of the financial

position of the

business (Broberg,

Test of details is to be

performed by the

auditor for

ascertaining whether

the current assets

balances which is

projected in the

annual report of the

business is showing

true and fair view of

the financial situation

or not. The auditor

needs to test all the

AUDITING

Memo

To: Wayne Wiadrowski

From: The Audit Manager

Date: 8th May, 2019

Subject: Discussion Regarding Audit risks of API

Purpose and Scope

The financial statement of a business need to show true and fair view regarding the financial

position of a business in order to ensure that the opinion of the investors is not affected in any

manner due to such an aspect. The business of Always Precise Instruments Pty Limited (API)

also need to adhere to such principles so that appropriate measures can be taken by the

management of the company in this respect. The memo would be stating facts which are

considered regarding the sampling tests which is applied by the business for collecting essential

audit evidences. The analysis of the ratios and risks they posses to the business are appropriately

discussed in the table below:

Key Ratios Analysis Audit Risks Audit Procedures

Current ratio The current ratio is a

representation of the

liquidity position of a

business and

considers the assets

and liabilities which a

business possesses.

As per the business

scenario in 2018, a

significant increase in

current ratio is seen.

This may be due to

increase in current

It is possible that the

current assets of the

business might be

materially misstated

and thereby this

would also mean that

the financial

statements of the

business are showing

an appropriate view

of the financial

position of the

business (Broberg,

Test of details is to be

performed by the

auditor for

ascertaining whether

the current assets

balances which is

projected in the

annual report of the

business is showing

true and fair view of

the financial situation

or not. The auditor

needs to test all the

2

AUDITING

assets of the business

in relation to current

liabilities of the

business.

Umans & Gerlofstig,

2013).

relevant documents

which are associated

with payment of

current liabilities and

ensure that both

current assets and

current liabilities of

the business are

appropriately valued.

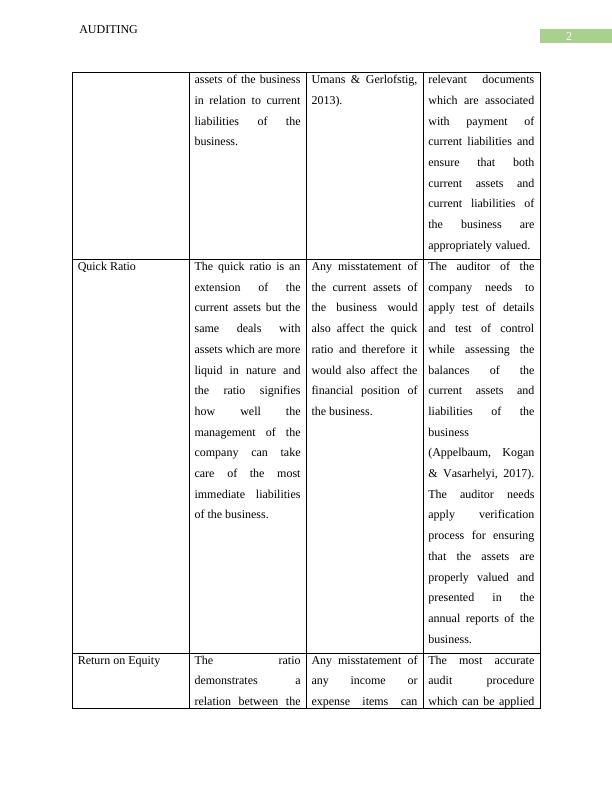

Quick Ratio The quick ratio is an

extension of the

current assets but the

same deals with

assets which are more

liquid in nature and

the ratio signifies

how well the

management of the

company can take

care of the most

immediate liabilities

of the business.

Any misstatement of

the current assets of

the business would

also affect the quick

ratio and therefore it

would also affect the

financial position of

the business.

The auditor of the

company needs to

apply test of details

and test of control

while assessing the

balances of the

current assets and

liabilities of the

business

(Appelbaum, Kogan

& Vasarhelyi, 2017).

The auditor needs

apply verification

process for ensuring

that the assets are

properly valued and

presented in the

annual reports of the

business.

Return on Equity The ratio

demonstrates a

relation between the

Any misstatement of

any income or

expense items can

The most accurate

audit procedure

which can be applied

AUDITING

assets of the business

in relation to current

liabilities of the

business.

Umans & Gerlofstig,

2013).

relevant documents

which are associated

with payment of

current liabilities and

ensure that both

current assets and

current liabilities of

the business are

appropriately valued.

Quick Ratio The quick ratio is an

extension of the

current assets but the

same deals with

assets which are more

liquid in nature and

the ratio signifies

how well the

management of the

company can take

care of the most

immediate liabilities

of the business.

Any misstatement of

the current assets of

the business would

also affect the quick

ratio and therefore it

would also affect the

financial position of

the business.

The auditor of the

company needs to

apply test of details

and test of control

while assessing the

balances of the

current assets and

liabilities of the

business

(Appelbaum, Kogan

& Vasarhelyi, 2017).

The auditor needs

apply verification

process for ensuring

that the assets are

properly valued and

presented in the

annual reports of the

business.

Return on Equity The ratio

demonstrates a

relation between the

Any misstatement of

any income or

expense items can

The most accurate

audit procedure

which can be applied

3

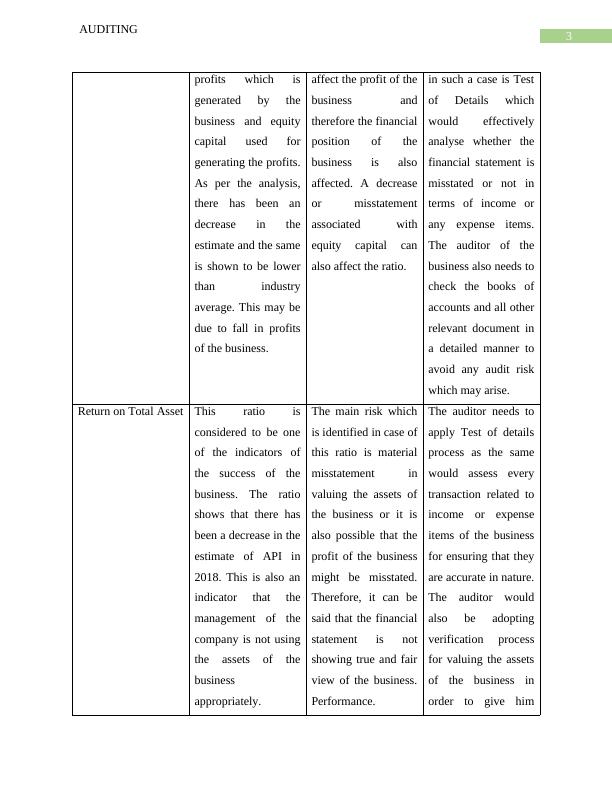

AUDITING

profits which is

generated by the

business and equity

capital used for

generating the profits.

As per the analysis,

there has been an

decrease in the

estimate and the same

is shown to be lower

than industry

average. This may be

due to fall in profits

of the business.

affect the profit of the

business and

therefore the financial

position of the

business is also

affected. A decrease

or misstatement

associated with

equity capital can

also affect the ratio.

in such a case is Test

of Details which

would effectively

analyse whether the

financial statement is

misstated or not in

terms of income or

any expense items.

The auditor of the

business also needs to

check the books of

accounts and all other

relevant document in

a detailed manner to

avoid any audit risk

which may arise.

Return on Total Asset This ratio is

considered to be one

of the indicators of

the success of the

business. The ratio

shows that there has

been a decrease in the

estimate of API in

2018. This is also an

indicator that the

management of the

company is not using

the assets of the

business

appropriately.

The main risk which

is identified in case of

this ratio is material

misstatement in

valuing the assets of

the business or it is

also possible that the

profit of the business

might be misstated.

Therefore, it can be

said that the financial

statement is not

showing true and fair

view of the business.

Performance.

The auditor needs to

apply Test of details

process as the same

would assess every

transaction related to

income or expense

items of the business

for ensuring that they

are accurate in nature.

The auditor would

also be adopting

verification process

for valuing the assets

of the business in

order to give him

AUDITING

profits which is

generated by the

business and equity

capital used for

generating the profits.

As per the analysis,

there has been an

decrease in the

estimate and the same

is shown to be lower

than industry

average. This may be

due to fall in profits

of the business.

affect the profit of the

business and

therefore the financial

position of the

business is also

affected. A decrease

or misstatement

associated with

equity capital can

also affect the ratio.

in such a case is Test

of Details which

would effectively

analyse whether the

financial statement is

misstated or not in

terms of income or

any expense items.

The auditor of the

business also needs to

check the books of

accounts and all other

relevant document in

a detailed manner to

avoid any audit risk

which may arise.

Return on Total Asset This ratio is

considered to be one

of the indicators of

the success of the

business. The ratio

shows that there has

been a decrease in the

estimate of API in

2018. This is also an

indicator that the

management of the

company is not using

the assets of the

business

appropriately.

The main risk which

is identified in case of

this ratio is material

misstatement in

valuing the assets of

the business or it is

also possible that the

profit of the business

might be misstated.

Therefore, it can be

said that the financial

statement is not

showing true and fair

view of the business.

Performance.

The auditor needs to

apply Test of details

process as the same

would assess every

transaction related to

income or expense

items of the business

for ensuring that they

are accurate in nature.

The auditor would

also be adopting

verification process

for valuing the assets

of the business in

order to give him

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Weaknesses in Inventory Internal Control, Audit Risk and Procedureslg...

|15

|3868

|48

Audit Risks of API: A Memolg...

|13

|3341

|63

Auditing and Assurancelg...

|12

|4263

|52

Weakness in Inventory Internal Control, Audit Risk and Procedureslg...

|15

|3701

|33

Audit and Assurancelg...

|15

|3782

|81

Audit Risks from Ratios and Internal Control and Sampling Method of APIlg...

|15

|4289

|34