Auditing and Assurance services at API

VerifiedAdded on 2023/03/21

|13

|3558

|100

AI Summary

This document provides an analysis of the financial ratios of Always Precise Instruments Pty Limited (API) to identify potential audit risks. It also suggests audit procedures that can be undertaken to reduce the audit risk. The document discusses various ratios such as current ratio, quick asset ratio, return on equity, return on total assets, gross margin, marketing expense ratio, admin expenses/sales ratio, times interest earned, days in inventory, days in accounts receivable, and debt to equity ratio. It also highlights internal control weaknesses in the inventory system and suggests audit procedures to reduce the risk.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Auditing and Assurance services at API 1

AUDITING AND ASSURANCE SERVICES AT API

by [Your Name]

Course

Professor’s Name

Name of Your Institution

Location of Institution

Date

AUDITING AND ASSURANCE SERVICES AT API

by [Your Name]

Course

Professor’s Name

Name of Your Institution

Location of Institution

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Auditing and Assurance services at API 2

Auditing of Always Precise Instruments Pty Limited

Question 1 8%

Analysis of Always Precise Instruments Pty Limited (API) ratios to identify potential

audit risks and identifying audit procedures that could be undertaken to reduce the audit risk.

TO: WAYNE WIADROSKI, SENIOR AUDITOR

FROM: AUDIT MANAGER

DATE: 12TH MAY 2019

Always Precise Instruments Pty Limited (API),

SUBJECT: AUDITING OF ALWAYS PRECISE INSTRUMENTS PTY LIMITED (API)

I have checked the financial statements and the underlying books of account for Always

Precise Instruments Pty Limited (API) for the financial year ending 31st December 2018 and I

have come up with the following analysis. I have arrived at these analyses by comparing the

financial performance for the company reported in the financial period ending 31st December

2018 against the budget, the previous year's performance and the industry benchmark. From the

analysis, I have realized that there are a number of audit issues that need to be examined during

the audit. These issues are summarized in the tables below. They include analysis of the financial

ratios to establish the audit risks associated which each type of ratio, assessing the internal

control weaknesses in the inventory system for the company and the potential audit risks that are

posed by the weaknesses and the Internal control weaknesses in the inventory system for API

company and potential audit risks posed and test counts for year-end stocks that needs to be done

through audit sampling to test the completeness and existence assertions.

Auditing of Always Precise Instruments Pty Limited

Question 1 8%

Analysis of Always Precise Instruments Pty Limited (API) ratios to identify potential

audit risks and identifying audit procedures that could be undertaken to reduce the audit risk.

TO: WAYNE WIADROSKI, SENIOR AUDITOR

FROM: AUDIT MANAGER

DATE: 12TH MAY 2019

Always Precise Instruments Pty Limited (API),

SUBJECT: AUDITING OF ALWAYS PRECISE INSTRUMENTS PTY LIMITED (API)

I have checked the financial statements and the underlying books of account for Always

Precise Instruments Pty Limited (API) for the financial year ending 31st December 2018 and I

have come up with the following analysis. I have arrived at these analyses by comparing the

financial performance for the company reported in the financial period ending 31st December

2018 against the budget, the previous year's performance and the industry benchmark. From the

analysis, I have realized that there are a number of audit issues that need to be examined during

the audit. These issues are summarized in the tables below. They include analysis of the financial

ratios to establish the audit risks associated which each type of ratio, assessing the internal

control weaknesses in the inventory system for the company and the potential audit risks that are

posed by the weaknesses and the Internal control weaknesses in the inventory system for API

company and potential audit risks posed and test counts for year-end stocks that needs to be done

through audit sampling to test the completeness and existence assertions.

Auditing and Assurance services at API 3

Ratio Analysis Audit risk Audit procedure to Reduce risk

The current ratio of

1.64

The current ratio for API has

increased slightly from 1.54 in

2017 to 1.64. This increase can

be due to the build-up in the

inventory. Although the current

ratio is slightly below the

industry benchmark of 1.84, it

is a bit higher than the budget.

Additional audit attention is

required here because there

might have been potential

manipulation of the current

assets so as to boost the current

ratio. It is also possible that

there might be an

overstatement of receivables

and inventory either following

a change in the accounting

method for inventory from

FIFO to average cost method

or to LIFO, which is likely to

have contributed to part of the

increase in the value of

inventory.

Control Risks Recalculate the accounts

receivables balances and inventory

turnover ratio to ensure that it is

reasonable compared with the

industry benchmark and the

previous year.

Gather sufficient., reliable and

appropriate audit evidence to

ensure that the true value of the

accounts receivable and inventory

has been reported.

Assess also whether all short terms

liabilities have been reported and

at the correct amounts.

Quick asset ratio of

0.91

The quick asset ratio of 0.91

recorded in 2018 is an increase

of 0.04 from 2017 and it is

slightly below the industry

benchmark of 1.1. This

, therefore, needs to be

counterchecked as any

variance could indicate that the

company can experience

problems with paying its

creditors and hence a potential

sign of going-concern. In any

case, the ratio might actually

be worse if there was a

possible overstatement of

receivables as has been

suspected above. In this case,

therefore, more audit attention

should be given to the cash

flows of the company.

Detection risks Trace all sales receipts and other

banking’s to identify whether they

‘are recorded correctly in the

books. Look at details including

the amounts, in particular, dollar

amounts, descriptions and

document dates are recorded

correctly and in an organized

manner.

Ratio Analysis Audit risk Audit procedure to Reduce risk

The current ratio of

1.64

The current ratio for API has

increased slightly from 1.54 in

2017 to 1.64. This increase can

be due to the build-up in the

inventory. Although the current

ratio is slightly below the

industry benchmark of 1.84, it

is a bit higher than the budget.

Additional audit attention is

required here because there

might have been potential

manipulation of the current

assets so as to boost the current

ratio. It is also possible that

there might be an

overstatement of receivables

and inventory either following

a change in the accounting

method for inventory from

FIFO to average cost method

or to LIFO, which is likely to

have contributed to part of the

increase in the value of

inventory.

Control Risks Recalculate the accounts

receivables balances and inventory

turnover ratio to ensure that it is

reasonable compared with the

industry benchmark and the

previous year.

Gather sufficient., reliable and

appropriate audit evidence to

ensure that the true value of the

accounts receivable and inventory

has been reported.

Assess also whether all short terms

liabilities have been reported and

at the correct amounts.

Quick asset ratio of

0.91

The quick asset ratio of 0.91

recorded in 2018 is an increase

of 0.04 from 2017 and it is

slightly below the industry

benchmark of 1.1. This

, therefore, needs to be

counterchecked as any

variance could indicate that the

company can experience

problems with paying its

creditors and hence a potential

sign of going-concern. In any

case, the ratio might actually

be worse if there was a

possible overstatement of

receivables as has been

suspected above. In this case,

therefore, more audit attention

should be given to the cash

flows of the company.

Detection risks Trace all sales receipts and other

banking’s to identify whether they

‘are recorded correctly in the

books. Look at details including

the amounts, in particular, dollar

amounts, descriptions and

document dates are recorded

correctly and in an organized

manner.

Auditing and Assurance services at API 4

Return on equity:

14.7%

The return on equity for API

reduced from 16.6% in 2017to

14.7% in 2018. This is way

below the budget of 18.4% and

the industry benchmark of

17.3%. The decrease in the

return on equity is attributed to

the reduction in the gross

margin and an increase in debt

to equity ratio. This means that

the company’s reliance on debt

increased in 2018 as depicted

by the debt to equity ratio.

Detection risks Assuming that the reduction in

return on equity is attributed to a

decline in gross profit for the

company, it would be worth

investigating and evaluating what

the borrowings did in 2018 by the

company was meant for. Check

the loans balances to verify if there

are loans that are not being repaid.

Verify that there are proper

records for authorization before

loans are borrowed.

Return on total

assets:12.5 %

The return on total assets

reduced from 14.9% in 2017 to

12.5 % in 2018 which is also

below the budget and industry

benchmark which are at 16.0%

and 16.3 % respectively. The

decrease in return on equity is

due to the decrease in gross

margin. However, attention

should be given on how the

assets were valued and

recognized in the books

(whether they conform to

International Accounting

Standards, IAS)

Inherent risks Examine the documentation that

records the assets purchased and

revaluation(depreciation) of the

existing assets. Recalculate the

accounts of property plant and

equipment to ensure they are

accurate and reasonable as

compared with the previous

period. Check the underlying

books that support the purchasing

of more assets during the year.

Gross margin of 6.5

%

The gross margin for the

company reduced from 10.3%

in 2017 to 6.5% in 2018. This

is below the budget provision

and industry benchmarks. A

reduction in gross profit means

that there is a possibility for

some inventory being obsolete

due to slow sales. It could also

mean that some of the stock

could be sold by discount due

to avoid obsolescence.

Inherent risks Examination and verification of

the significance of fixed assets

additions and/ or investments in

generation of additional income

and consequently profit.

Marketing expense

4.4 %

The marketing expense ratio

for API in 2018 was at 4.4 %

an increase of 0.6% from 3.8%

in 2017. The ratio is above the

budget provision and industry

benchmarks set at 3.6% and

Control risks Scrutinize the marketing expense

accounts in the books to establish

if there are amounts that should

have been capitalized or

reclassified as developments costs

in the trial balance. Countercheck

Return on equity:

14.7%

The return on equity for API

reduced from 16.6% in 2017to

14.7% in 2018. This is way

below the budget of 18.4% and

the industry benchmark of

17.3%. The decrease in the

return on equity is attributed to

the reduction in the gross

margin and an increase in debt

to equity ratio. This means that

the company’s reliance on debt

increased in 2018 as depicted

by the debt to equity ratio.

Detection risks Assuming that the reduction in

return on equity is attributed to a

decline in gross profit for the

company, it would be worth

investigating and evaluating what

the borrowings did in 2018 by the

company was meant for. Check

the loans balances to verify if there

are loans that are not being repaid.

Verify that there are proper

records for authorization before

loans are borrowed.

Return on total

assets:12.5 %

The return on total assets

reduced from 14.9% in 2017 to

12.5 % in 2018 which is also

below the budget and industry

benchmark which are at 16.0%

and 16.3 % respectively. The

decrease in return on equity is

due to the decrease in gross

margin. However, attention

should be given on how the

assets were valued and

recognized in the books

(whether they conform to

International Accounting

Standards, IAS)

Inherent risks Examine the documentation that

records the assets purchased and

revaluation(depreciation) of the

existing assets. Recalculate the

accounts of property plant and

equipment to ensure they are

accurate and reasonable as

compared with the previous

period. Check the underlying

books that support the purchasing

of more assets during the year.

Gross margin of 6.5

%

The gross margin for the

company reduced from 10.3%

in 2017 to 6.5% in 2018. This

is below the budget provision

and industry benchmarks. A

reduction in gross profit means

that there is a possibility for

some inventory being obsolete

due to slow sales. It could also

mean that some of the stock

could be sold by discount due

to avoid obsolescence.

Inherent risks Examination and verification of

the significance of fixed assets

additions and/ or investments in

generation of additional income

and consequently profit.

Marketing expense

4.4 %

The marketing expense ratio

for API in 2018 was at 4.4 %

an increase of 0.6% from 3.8%

in 2017. The ratio is above the

budget provision and industry

benchmarks set at 3.6% and

Control risks Scrutinize the marketing expense

accounts in the books to establish

if there are amounts that should

have been capitalized or

reclassified as developments costs

in the trial balance. Countercheck

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Auditing and Assurance services at API 5

4.0% respectively. Audit

attention is required to

establish the reason for an

increase in marketing expenses

despite the decline in sales

amounts and consequently the

gross profit.

if all the expenses classified as

marketing expenses related to the

direct promotion of the core

products of the company.

Scrutinize to establish if there

were any unnecessary marketing

expenses not directly related to

marketing of the company’s

products.

Admin

expenses/sales 3.4 %

The admin expenses to sales

ratio for API company in 2018

was 3.4% which is at par with

the budget but slightly less

than the ratio for 2017. The

ratio is also below the industry

standard which is set at 3.8%.

There is no serious audit

concern for this but attention

should be placed on how the

expenses were classified.

Detection risks Examine the expense control

accounts and verify the procedures

that are taken before an expense is

incurred (paid) and the control

measures set to bar unnecessary

expenditure. This will help to

determine if the admin expense

figures arrived and recorded in the

trial balance are relevant and

accurate

Times interest earned

3.6

The time's interest earned for

API reduced from 4.6 in 2017

to 3.6 in 2018. This is against

the budget provision set at 6.3

and industry benchmark at 4.2.

A reducing times interest

earned that the ability of the

company to cover its interest

charges based from gross

income is decreasing. Audit

attention is required to

establish if the company will

be able to meet its interest

portfolio in the near future.

Control risks Countercheck how much the

company is required to repay in

terms of interest on loan,

overdrafts, bonds and other

contractual debt to establish

whether the times on interest

earned ratio is showing a true and

fair value of the company’s state

of affairs.

Days in inventory:

34.9

Days in inventory increased

from 32.9 in 2017 to 34.9 in

2018. This is below the budget

line set at 32.3 and industry

benchmark at 31.8. An increase

in the days in inventory means

that the company’s stock is

moving slowly. Audit attention

is required to establish why the

stocks are taking too long to

clear.

Detection risks The audit needs to examine the

reasons for slow-moving

inventory. Given that the days in

accounts receivable has increased,

sales should be moving faster due

to more lenient credit terms.

Documentation of all discount

sales made should be

counterchecked to establish if the

slow-moving inventories were

cleared at discounted prices.

4.0% respectively. Audit

attention is required to

establish the reason for an

increase in marketing expenses

despite the decline in sales

amounts and consequently the

gross profit.

if all the expenses classified as

marketing expenses related to the

direct promotion of the core

products of the company.

Scrutinize to establish if there

were any unnecessary marketing

expenses not directly related to

marketing of the company’s

products.

Admin

expenses/sales 3.4 %

The admin expenses to sales

ratio for API company in 2018

was 3.4% which is at par with

the budget but slightly less

than the ratio for 2017. The

ratio is also below the industry

standard which is set at 3.8%.

There is no serious audit

concern for this but attention

should be placed on how the

expenses were classified.

Detection risks Examine the expense control

accounts and verify the procedures

that are taken before an expense is

incurred (paid) and the control

measures set to bar unnecessary

expenditure. This will help to

determine if the admin expense

figures arrived and recorded in the

trial balance are relevant and

accurate

Times interest earned

3.6

The time's interest earned for

API reduced from 4.6 in 2017

to 3.6 in 2018. This is against

the budget provision set at 6.3

and industry benchmark at 4.2.

A reducing times interest

earned that the ability of the

company to cover its interest

charges based from gross

income is decreasing. Audit

attention is required to

establish if the company will

be able to meet its interest

portfolio in the near future.

Control risks Countercheck how much the

company is required to repay in

terms of interest on loan,

overdrafts, bonds and other

contractual debt to establish

whether the times on interest

earned ratio is showing a true and

fair value of the company’s state

of affairs.

Days in inventory:

34.9

Days in inventory increased

from 32.9 in 2017 to 34.9 in

2018. This is below the budget

line set at 32.3 and industry

benchmark at 31.8. An increase

in the days in inventory means

that the company’s stock is

moving slowly. Audit attention

is required to establish why the

stocks are taking too long to

clear.

Detection risks The audit needs to examine the

reasons for slow-moving

inventory. Given that the days in

accounts receivable has increased,

sales should be moving faster due

to more lenient credit terms.

Documentation of all discount

sales made should be

counterchecked to establish if the

slow-moving inventories were

cleared at discounted prices.

Auditing and Assurance services at API 6

Days in accounts

receivable: 53.0

The ratio has increased over

the two years from 51.5 in

2017 to 53.0 in 2018. This is

way above the budget and the

industry benchmark which

were set at 49.8 and 46.9

respectively. An increase in the

days in inventory means there

could be increasing leniency in

terms of credit policy in a bid

to generate more sales.

Audit attention is required as

lenient credit terms may have a

subsequent effect on the

collectability of accounts

receivable.

Control risks Checking the documentation for

terms of sales, the authorization of

credit to credit customers,

counterchecking if the credit

policy for the company is adhered

to by selecting a sample of debtors

accounts checking their credit

balance in reference to their limit

and credit terms.

Debt to equity

ratio:0.61

The debt to equity ratio for API

increased 0.52 in 2017 to 0.61

in 2018. This is against the

budget which was set at 0.43

and the industry benchmark. A

higher debt ratio means that the

company’s reliance on debt as

compared with equity is

increasing.

Assuming that much of the

borrowings in the earlier years

were used to purchase assets

and boost production, it would

be worth examining what the

recent borrowings were meant

for.

Detection risks Examining the reason for

increased borrowings and the

company’s increasing dependence

on debt. Documentation for

borrowings needs to be

counterchecked to assess the

ability of the company ability to

repay the debt.

Question 2 8%

Days in accounts

receivable: 53.0

The ratio has increased over

the two years from 51.5 in

2017 to 53.0 in 2018. This is

way above the budget and the

industry benchmark which

were set at 49.8 and 46.9

respectively. An increase in the

days in inventory means there

could be increasing leniency in

terms of credit policy in a bid

to generate more sales.

Audit attention is required as

lenient credit terms may have a

subsequent effect on the

collectability of accounts

receivable.

Control risks Checking the documentation for

terms of sales, the authorization of

credit to credit customers,

counterchecking if the credit

policy for the company is adhered

to by selecting a sample of debtors

accounts checking their credit

balance in reference to their limit

and credit terms.

Debt to equity

ratio:0.61

The debt to equity ratio for API

increased 0.52 in 2017 to 0.61

in 2018. This is against the

budget which was set at 0.43

and the industry benchmark. A

higher debt ratio means that the

company’s reliance on debt as

compared with equity is

increasing.

Assuming that much of the

borrowings in the earlier years

were used to purchase assets

and boost production, it would

be worth examining what the

recent borrowings were meant

for.

Detection risks Examining the reason for

increased borrowings and the

company’s increasing dependence

on debt. Documentation for

borrowings needs to be

counterchecked to assess the

ability of the company ability to

repay the debt.

Question 2 8%

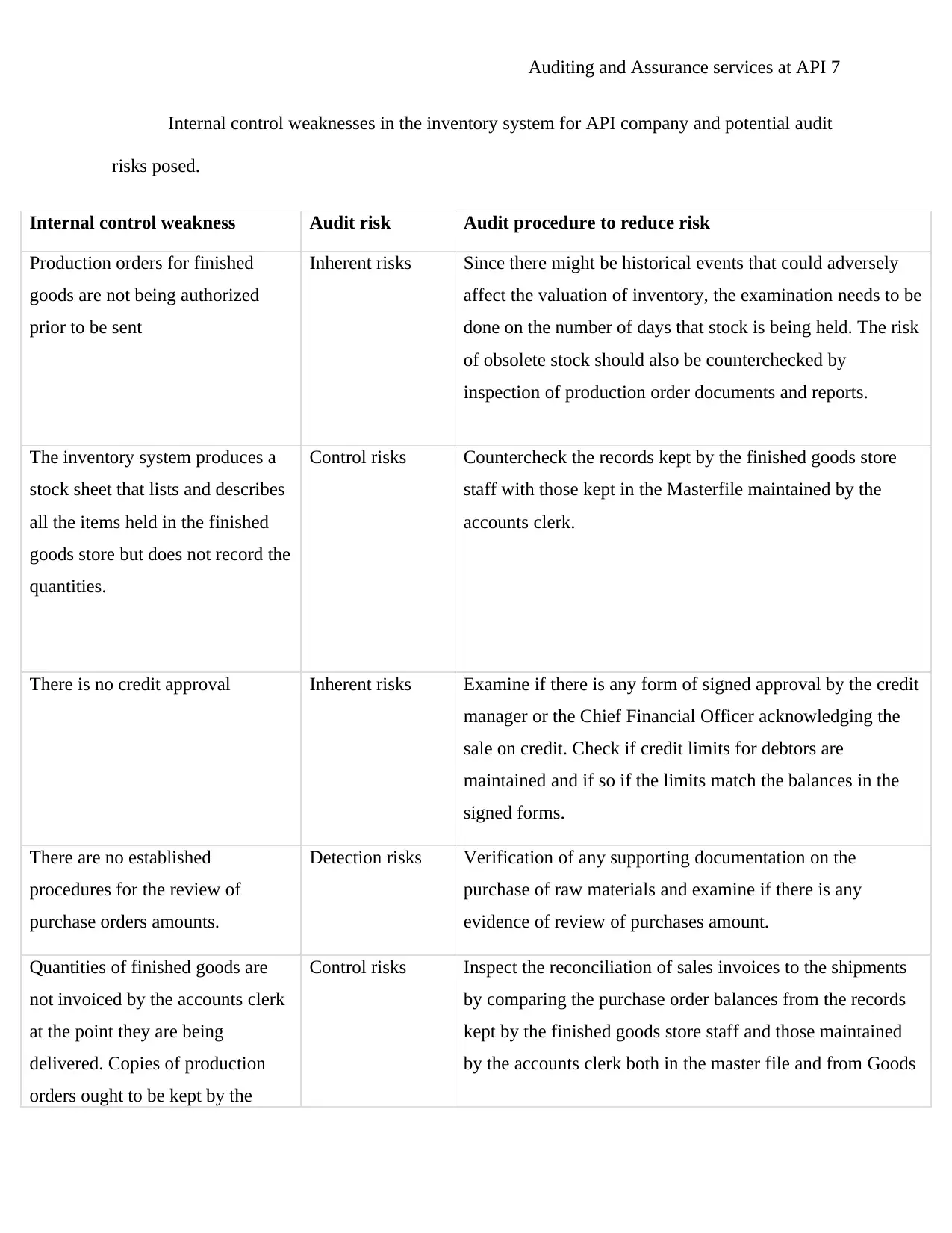

Auditing and Assurance services at API 7

Internal control weaknesses in the inventory system for API company and potential audit

risks posed.

Internal control weakness Audit risk Audit procedure to reduce risk

Production orders for finished

goods are not being authorized

prior to be sent

Inherent risks Since there might be historical events that could adversely

affect the valuation of inventory, the examination needs to be

done on the number of days that stock is being held. The risk

of obsolete stock should also be counterchecked by

inspection of production order documents and reports.

The inventory system produces a

stock sheet that lists and describes

all the items held in the finished

goods store but does not record the

quantities.

Control risks Countercheck the records kept by the finished goods store

staff with those kept in the Masterfile maintained by the

accounts clerk.

There is no credit approval Inherent risks Examine if there is any form of signed approval by the credit

manager or the Chief Financial Officer acknowledging the

sale on credit. Check if credit limits for debtors are

maintained and if so if the limits match the balances in the

signed forms.

There are no established

procedures for the review of

purchase orders amounts.

Detection risks Verification of any supporting documentation on the

purchase of raw materials and examine if there is any

evidence of review of purchases amount.

Quantities of finished goods are

not invoiced by the accounts clerk

at the point they are being

delivered. Copies of production

orders ought to be kept by the

Control risks Inspect the reconciliation of sales invoices to the shipments

by comparing the purchase order balances from the records

kept by the finished goods store staff and those maintained

by the accounts clerk both in the master file and from Goods

Internal control weaknesses in the inventory system for API company and potential audit

risks posed.

Internal control weakness Audit risk Audit procedure to reduce risk

Production orders for finished

goods are not being authorized

prior to be sent

Inherent risks Since there might be historical events that could adversely

affect the valuation of inventory, the examination needs to be

done on the number of days that stock is being held. The risk

of obsolete stock should also be counterchecked by

inspection of production order documents and reports.

The inventory system produces a

stock sheet that lists and describes

all the items held in the finished

goods store but does not record the

quantities.

Control risks Countercheck the records kept by the finished goods store

staff with those kept in the Masterfile maintained by the

accounts clerk.

There is no credit approval Inherent risks Examine if there is any form of signed approval by the credit

manager or the Chief Financial Officer acknowledging the

sale on credit. Check if credit limits for debtors are

maintained and if so if the limits match the balances in the

signed forms.

There are no established

procedures for the review of

purchase orders amounts.

Detection risks Verification of any supporting documentation on the

purchase of raw materials and examine if there is any

evidence of review of purchases amount.

Quantities of finished goods are

not invoiced by the accounts clerk

at the point they are being

delivered. Copies of production

orders ought to be kept by the

Control risks Inspect the reconciliation of sales invoices to the shipments

by comparing the purchase order balances from the records

kept by the finished goods store staff and those maintained

by the accounts clerk both in the master file and from Goods

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing and Assurance services at API 8

accounts clerk and reconciled with

quantities in the Goods Received

Note produced by the suppliers.

Received Notes.

Supplier statements are not being

e-mailed monthly to customers to

facilitate queries and follow up of

payments. This could be the

reason for the increase in the days

in accounts receivable. The system

should be designed to

automatically sent statements to

the suppliers to assist them in their

reconciliation and also enable

them to know the amounts of their

debts.

Inherent risks The audit should check whether the debtors account balances

are correct and are reconciled every month to ensure that

suppliers are aware of the amounts they are supposed to pay.

The evaluation also needs to be done to assess whether

suppliers get access to their statements to assist them to settle

their debts.

No segregation of duties. The

accounts clerk has the rights to

effect Masterfile amendments.

This means that the same person is

tasked with receiving sales

invoices, entering them into the

system, checking the correctness

of purchase invoices and payment

of suppliers.

Inherent risks The audit needs to observe and confirm how the functions to

do with receiving, entering and payment of suppliers are

performed by the accounts clerk. It is not ideal for the same

person to check, pay and approve the same process.

accounts clerk and reconciled with

quantities in the Goods Received

Note produced by the suppliers.

Received Notes.

Supplier statements are not being

e-mailed monthly to customers to

facilitate queries and follow up of

payments. This could be the

reason for the increase in the days

in accounts receivable. The system

should be designed to

automatically sent statements to

the suppliers to assist them in their

reconciliation and also enable

them to know the amounts of their

debts.

Inherent risks The audit should check whether the debtors account balances

are correct and are reconciled every month to ensure that

suppliers are aware of the amounts they are supposed to pay.

The evaluation also needs to be done to assess whether

suppliers get access to their statements to assist them to settle

their debts.

No segregation of duties. The

accounts clerk has the rights to

effect Masterfile amendments.

This means that the same person is

tasked with receiving sales

invoices, entering them into the

system, checking the correctness

of purchase invoices and payment

of suppliers.

Inherent risks The audit needs to observe and confirm how the functions to

do with receiving, entering and payment of suppliers are

performed by the accounts clerk. It is not ideal for the same

person to check, pay and approve the same process.

Auditing and Assurance services at API 9

There are no physical requisitions

forms from the production

departments to accompany the

automatic system generated

purchase orders which means that

if there is a system disorder,

ordering of raw materials can be

delayed

Control risks Pick a sample of purchase orders filed in the production

department and compare with the purchase requisitions made

by the company filed in the master file to ensure that the

corresponding purchases are correct.

The lack of hard copy

documentation of sales.

Detection risks The audit needs to check the automatic controls of the

system to verify that all the posting of sales is done

appropriately to the right accounts. In this case, Computer

Assisted Auditing Techniques (CAAT's) needs to be used.

Purchase requisition being done by

the purchasing department instead

of being done by the department

that requires the raw material. The

procedure of having the store

department issuing voluntary

requisitions should not be the case

as this can result in the ordering of

unwanted stock, therefore,

reducing the cash flow of the

company.

Inherent risks Examination of purchase requisition sheets to establish if

indeed the purchased raw materials were as a result of

demand by the relevant department or not. The system

should be checked if it is efficient in terms of raising

production orders when finished goods fall below the set

benchmark.

There are no physical requisitions

forms from the production

departments to accompany the

automatic system generated

purchase orders which means that

if there is a system disorder,

ordering of raw materials can be

delayed

Control risks Pick a sample of purchase orders filed in the production

department and compare with the purchase requisitions made

by the company filed in the master file to ensure that the

corresponding purchases are correct.

The lack of hard copy

documentation of sales.

Detection risks The audit needs to check the automatic controls of the

system to verify that all the posting of sales is done

appropriately to the right accounts. In this case, Computer

Assisted Auditing Techniques (CAAT's) needs to be used.

Purchase requisition being done by

the purchasing department instead

of being done by the department

that requires the raw material. The

procedure of having the store

department issuing voluntary

requisitions should not be the case

as this can result in the ordering of

unwanted stock, therefore,

reducing the cash flow of the

company.

Inherent risks Examination of purchase requisition sheets to establish if

indeed the purchased raw materials were as a result of

demand by the relevant department or not. The system

should be checked if it is efficient in terms of raising

production orders when finished goods fall below the set

benchmark.

Auditing and Assurance services at API 10

Question 3 4%

API test counts of year-end stocks through sampling to test the existence and

completeness assertions.

Assertion Which population? Sample selection method Justification for the sample selection method

Completeness Purchase

orders (raw

materials)

Suppliers’

invoices

Finished

goods stock

Statistical method

Non-statistical

method

Statistical Method

The statistical method of sampling is applicable

here as the accounting of the numerical figures

and sequence of the purchase order reports need

to be reviewed here.

The non-statistical method is appropriate here

because judgment can be used to assess the

evidence for the numerical sequence created by

the system in the numbering of invoices.

This method is appropriate as it helps the audit to

compare the goods received by the store's

department after counterchecking for any

damage or substandard quality with those kept

by the purchasing department or the accounts

clerk. Assessment should also be done to

establish if the goods supplied are vouched to the

supplier in reference to goods type and quantity.

Existence Purchase

orders

Variable sampling Variable sampling is required here to verify that

there is a documentary trail of evidence to

support all the purchases made. This sampling is

intended to evaluate whether there is physical

evidence of order forms and whether it has

signatures showing approval.

Question 3 4%

API test counts of year-end stocks through sampling to test the existence and

completeness assertions.

Assertion Which population? Sample selection method Justification for the sample selection method

Completeness Purchase

orders (raw

materials)

Suppliers’

invoices

Finished

goods stock

Statistical method

Non-statistical

method

Statistical Method

The statistical method of sampling is applicable

here as the accounting of the numerical figures

and sequence of the purchase order reports need

to be reviewed here.

The non-statistical method is appropriate here

because judgment can be used to assess the

evidence for the numerical sequence created by

the system in the numbering of invoices.

This method is appropriate as it helps the audit to

compare the goods received by the store's

department after counterchecking for any

damage or substandard quality with those kept

by the purchasing department or the accounts

clerk. Assessment should also be done to

establish if the goods supplied are vouched to the

supplier in reference to goods type and quantity.

Existence Purchase

orders

Variable sampling Variable sampling is required here to verify that

there is a documentary trail of evidence to

support all the purchases made. This sampling is

intended to evaluate whether there is physical

evidence of order forms and whether it has

signatures showing approval.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Auditing and Assurance services at API 11

Suppliers

Invoices

Finished goods

stock

Attributive

sampling

Variable sampling

This method is appropriate as it enables the audit

to check to estimate the existence and occurrence

of the supplier's invoice numbers both in the

system and in hard copy. This assists to establish

the proportion of accuracy for the existence of

suppliers invoices as a point of interest.

The variable sampling method is appropriate

here as it can be used to verify the existence of

finished goods physically present in the finished

goods store. This method also can help the audit

to establish if the finished goods physically

presented in the store are matching those in the

system.

Suppliers

Invoices

Finished goods

stock

Attributive

sampling

Variable sampling

This method is appropriate as it enables the audit

to check to estimate the existence and occurrence

of the supplier's invoice numbers both in the

system and in hard copy. This assists to establish

the proportion of accuracy for the existence of

suppliers invoices as a point of interest.

The variable sampling method is appropriate

here as it can be used to verify the existence of

finished goods physically present in the finished

goods store. This method also can help the audit

to establish if the finished goods physically

presented in the store are matching those in the

system.

Auditing and Assurance services at API 12

References

Auasb.gov.au. (2019). Auditing and Assurance Standards Board (AUASB) - Home. [online]

Available at: https://www.auasb.gov.au/ [Accessed 12 May 2019].

Bell Partners. (2019). Auditing and Assurance Services in Australia | Bell Partners. [online]

Available at: https://www.bellpartners.com/services/audit-and-assurance/ [Accessed 12

May 2019].

Botica Redmayne, N. (2012). Essentials of Auditing, Assurance Services & Ethics in Australia:

An Integrated Approach20121Essentials of Auditing, Assurance Services & Ethics in

Australia: An Integrated Approach. Massey: Massey University 1st ed. Journal of

Accounting & Organizational Change, 8(1), pp.120-122.

Channuntapipat, C., Samsonova-Taddei, A. and Turley, S. (2019). Exploring diversity in the

sustainability assurance practice. Accounting, Auditing & Accountability Journal.

Cpaaustralia.com.au. (2019). [online] Available at:

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/professional-

resources/auditing-assurance/guide-understanding-audit-assurance.pdf [Accessed 12 May

2019].

Gay, G. and Simnett, R. (2018). Auditing and assurance services in Australia. North Ryde,

N.S.W: McGraw-Hill Education (Australia).

Google Books. (2019). Auditing and Assurance Services in Australia. [online] Available at:

https://books.google.com/books/about/Auditing_and_Assurance_Services_in_Austr.html

?id=LA4juAAACAAJ [Accessed 12 May 2019].

References

Auasb.gov.au. (2019). Auditing and Assurance Standards Board (AUASB) - Home. [online]

Available at: https://www.auasb.gov.au/ [Accessed 12 May 2019].

Bell Partners. (2019). Auditing and Assurance Services in Australia | Bell Partners. [online]

Available at: https://www.bellpartners.com/services/audit-and-assurance/ [Accessed 12

May 2019].

Botica Redmayne, N. (2012). Essentials of Auditing, Assurance Services & Ethics in Australia:

An Integrated Approach20121Essentials of Auditing, Assurance Services & Ethics in

Australia: An Integrated Approach. Massey: Massey University 1st ed. Journal of

Accounting & Organizational Change, 8(1), pp.120-122.

Channuntapipat, C., Samsonova-Taddei, A. and Turley, S. (2019). Exploring diversity in the

sustainability assurance practice. Accounting, Auditing & Accountability Journal.

Cpaaustralia.com.au. (2019). [online] Available at:

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/professional-

resources/auditing-assurance/guide-understanding-audit-assurance.pdf [Accessed 12 May

2019].

Gay, G. and Simnett, R. (2018). Auditing and assurance services in Australia. North Ryde,

N.S.W: McGraw-Hill Education (Australia).

Google Books. (2019). Auditing and Assurance Services in Australia. [online] Available at:

https://books.google.com/books/about/Auditing_and_Assurance_Services_in_Austr.html

?id=LA4juAAACAAJ [Accessed 12 May 2019].

Auditing and Assurance services at API 13

Iaasb.org. (2019). The International Auditing and Assurance Standards Board (IAASB). [online]

Available at: https://www.iaasb.org/ [Accessed 12 May 2019].

Imoniana, J. and Perera, L. (2016). The role of IS Auditing in assurance services.

MANAGEMENT CONTROL, (1), pp.17-33.

Maroun, W. (2018). Modifying assurance practices to meet the needs of integrated reporting.

Accounting, Auditing & Accountability Journal, 31(2), pp.400-427.

Mheducation.com.au. (2019). McGraw-Hill Europe, Middle East & Africa. [online] Available at:

https://www.mheducation.com.au/9781760422004-aus-ebook-for-auditing-assurance-

services-in-australia-7th-edition [Accessed 12 May 2019].

PwC. (2019). What is an Audit?. [online] Available at:

https://www.pwc.com.au/assurance/audit.html [Accessed 12 May 2019].

KPMG. (2019). Audit & Assurance. [online] Available at:

https://home.kpmg/au/en/home/services/audit.html [Accessed 12 May 2019].

Services, Arens, A., Elder, R. and Beasley, M. (2019). Auditing and Assurance Services. [online]

Goodreads.com. Available at: https://www.goodreads.com/book/show/20098161-

auditing-and-assurance-services [Accessed 12 May 2019].

Special issue on assurance: a concept in evolution. (2012). Managerial Auditing Journal, 28(1).

Zookal.com. (2019). Auditing and Assurance Services in Australia; ISBN: 9780074717417.

[online] Available at: https://www.zookal.com/auditing-and-assurance-services-in-

australia-9780074717417/ [Accessed 12 May 2019].

Iaasb.org. (2019). The International Auditing and Assurance Standards Board (IAASB). [online]

Available at: https://www.iaasb.org/ [Accessed 12 May 2019].

Imoniana, J. and Perera, L. (2016). The role of IS Auditing in assurance services.

MANAGEMENT CONTROL, (1), pp.17-33.

Maroun, W. (2018). Modifying assurance practices to meet the needs of integrated reporting.

Accounting, Auditing & Accountability Journal, 31(2), pp.400-427.

Mheducation.com.au. (2019). McGraw-Hill Europe, Middle East & Africa. [online] Available at:

https://www.mheducation.com.au/9781760422004-aus-ebook-for-auditing-assurance-

services-in-australia-7th-edition [Accessed 12 May 2019].

PwC. (2019). What is an Audit?. [online] Available at:

https://www.pwc.com.au/assurance/audit.html [Accessed 12 May 2019].

KPMG. (2019). Audit & Assurance. [online] Available at:

https://home.kpmg/au/en/home/services/audit.html [Accessed 12 May 2019].

Services, Arens, A., Elder, R. and Beasley, M. (2019). Auditing and Assurance Services. [online]

Goodreads.com. Available at: https://www.goodreads.com/book/show/20098161-

auditing-and-assurance-services [Accessed 12 May 2019].

Special issue on assurance: a concept in evolution. (2012). Managerial Auditing Journal, 28(1).

Zookal.com. (2019). Auditing and Assurance Services in Australia; ISBN: 9780074717417.

[online] Available at: https://www.zookal.com/auditing-and-assurance-services-in-

australia-9780074717417/ [Accessed 12 May 2019].

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.