Audit Planning and Analytical Procedures for Westpac

VerifiedAdded on 2019/11/08

|12

|2651

|311

Report

AI Summary

The assignment discusses the audit planning process of Westpac, a leading Australian bank. The company faces various risks, including actual or potential claims, business risks, and information technology assimilation risks. To mitigate these risks, auditors perform analytical procedures to identify potential risk areas and plan other audit procedures accordingly. The analysis reveals that while Westpac's liquidity position has improved, its debt-to-equity ratio has increased, indicating an unfavourable solvency condition. Furthermore, the company's profitability has declined, suggesting undesirable financial health. Ultimately, the study highlights the importance of audit testing in analyzing and detecting issues affecting a company's financial health.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDITING AND ASSURANCE

Auditing and Assurance

University Name

Student Name

Authors’ Note

Auditing and Assurance

University Name

Student Name

Authors’ Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2AUDITING AND ASSURANCE

Executive Summary

The current study elucidates in detail about audit planning taking into consideration the

operations of one of the major banks of Australia (Westpac). The current segment analyses

banking industry and the operations of the company Westpac operates. This study also

presents the different steps involved in audit planning of the firm. Thereafter, the study also

detects the risks that might be faced by the company and carries out an analytical procedure

using key financial ratio.

Executive Summary

The current study elucidates in detail about audit planning taking into consideration the

operations of one of the major banks of Australia (Westpac). The current segment analyses

banking industry and the operations of the company Westpac operates. This study also

presents the different steps involved in audit planning of the firm. Thereafter, the study also

detects the risks that might be faced by the company and carries out an analytical procedure

using key financial ratio.

3AUDITING AND ASSURANCE

Table of Contents

Introduction................................................................................................................................4

Acceptance of the client and Planning of Audit.........................................................................4

Analysis of the business of the client.........................................................................................5

Analysis of the business risk of the client..................................................................................7

Performing analytical procedures..............................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

Table of Contents

Introduction................................................................................................................................4

Acceptance of the client and Planning of Audit.........................................................................4

Analysis of the business of the client.........................................................................................5

Analysis of the business risk of the client..................................................................................7

Performing analytical procedures..............................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

4AUDITING AND ASSURANCE

Introduction

The current report elucidates in detail the audit planning with special orientation to the

operations of the firm Westpac. The current segment analyses the industry that is the banking

industry in which the company Westpac operates and evaluates the operations of company.

This study conducts an industry analysis and company analysis and audit planning of the

firm. Thereafter, the study also detects the risks that might be faced by the company and

carries out an analytical procedure.

Acceptance of the client and Planning of Audit

The current report illustratively elucidates the sequential procedures for planning for carrying

out audit of the firm. The present segment explains the successive steps that can be adopted

for undertaking the planning of audit in the company Westpac. Audit planning thereby

involves the following steps:

- Discussions with the client

- Review of documentation of audit of Westpac

- Analysis of financial assertions of the company Westpac

- Analysis of interim pecuniary assertions of the company Westpac

- Identification and consultation with diverse non-audit personnel of specifically the

accounting corporation (Arens et al., 2012).

- Staffing required for the purpose of audit of the firm Westpac

- Timing of different procedures of audit (Eilifsen et al., 2013).

- Outside help essentially needs to be determined counting the utilization of a particular

specialist as necessary and determination of the nature and extent of involvement of

the internal assessors of the specific client (William Jr et al., 2016).

Introduction

The current report elucidates in detail the audit planning with special orientation to the

operations of the firm Westpac. The current segment analyses the industry that is the banking

industry in which the company Westpac operates and evaluates the operations of company.

This study conducts an industry analysis and company analysis and audit planning of the

firm. Thereafter, the study also detects the risks that might be faced by the company and

carries out an analytical procedure.

Acceptance of the client and Planning of Audit

The current report illustratively elucidates the sequential procedures for planning for carrying

out audit of the firm. The present segment explains the successive steps that can be adopted

for undertaking the planning of audit in the company Westpac. Audit planning thereby

involves the following steps:

- Discussions with the client

- Review of documentation of audit of Westpac

- Analysis of financial assertions of the company Westpac

- Analysis of interim pecuniary assertions of the company Westpac

- Identification and consultation with diverse non-audit personnel of specifically the

accounting corporation (Arens et al., 2012).

- Staffing required for the purpose of audit of the firm Westpac

- Timing of different procedures of audit (Eilifsen et al., 2013).

- Outside help essentially needs to be determined counting the utilization of a particular

specialist as necessary and determination of the nature and extent of involvement of

the internal assessors of the specific client (William Jr et al., 2016).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5AUDITING AND ASSURANCE

- Pronouncements on different accounting principles as well as audit guidelines that

need to be read and assessed (Louwers et al., 2015). This can help in the process of

development of specifically complete audit programs aptly fitting the exclusive

requirements of the business of the client as well as industry (Simnett et al., 2016).

- Scheduling with the client is required to coordinate actions. For example, schedule

prepared by client necessarily need to be ready at the time when the assessor is

anticipated to assess them (Arens et al., 2016). The client has the need to be informed

regarding the dates at which they can be prohibited from accessing bank safe deposits

in order to make certain that the integrity of different counts of security that is

specifically held at banks (Arens et al., 2016).

Analysis of the business of the client

Westpac Banking Corporation is the presently the client of the accounting firm NY. Westpac

Banking Corporation also referred to as Westpac is essentially one of the big four Australian

banks as well as financial service provider that is headquartered in Sydney. Westpac operates

through four different core business divisions that include Consumer Bank, Business as well

as Commercial Bank, Westpac Institutional Bank along with Westpac New Zealand as well

as the BT Financial Group. Essentially, consumer bank is accountable for necessarily sales

as well as service of approximately 9 million consumers across the nation Australia and aids

them in the regular banking needs of the consumers. Again, business bank division is

accountable for both sales as well as service of diverse small along with medium sized

enterprises, different commercial along with the agribusinesses in Australia together with the

asset and tools/instruments finance and functions under the corporation Westpac. Particularly,

BT Financial Group is essentially the wealth management division of the corporation

Westpac Group that subsequent to the merger with the business entity St. George Bank

- Pronouncements on different accounting principles as well as audit guidelines that

need to be read and assessed (Louwers et al., 2015). This can help in the process of

development of specifically complete audit programs aptly fitting the exclusive

requirements of the business of the client as well as industry (Simnett et al., 2016).

- Scheduling with the client is required to coordinate actions. For example, schedule

prepared by client necessarily need to be ready at the time when the assessor is

anticipated to assess them (Arens et al., 2016). The client has the need to be informed

regarding the dates at which they can be prohibited from accessing bank safe deposits

in order to make certain that the integrity of different counts of security that is

specifically held at banks (Arens et al., 2016).

Analysis of the business of the client

Westpac Banking Corporation is the presently the client of the accounting firm NY. Westpac

Banking Corporation also referred to as Westpac is essentially one of the big four Australian

banks as well as financial service provider that is headquartered in Sydney. Westpac operates

through four different core business divisions that include Consumer Bank, Business as well

as Commercial Bank, Westpac Institutional Bank along with Westpac New Zealand as well

as the BT Financial Group. Essentially, consumer bank is accountable for necessarily sales

as well as service of approximately 9 million consumers across the nation Australia and aids

them in the regular banking needs of the consumers. Again, business bank division is

accountable for both sales as well as service of diverse small along with medium sized

enterprises, different commercial along with the agribusinesses in Australia together with the

asset and tools/instruments finance and functions under the corporation Westpac. Particularly,

BT Financial Group is essentially the wealth management division of the corporation

Westpac Group that subsequent to the merger with the business entity St. George Bank

6AUDITING AND ASSURANCE

Limited also takes into account the wealth division of the firm St. George. Furthermore, the

Westpac Institutional Bank also offers a wide range of financial services to different

commercial, corporate, institutional as well as government clientele.

Analysis of the banking industry

The financial results of the majority of the Australian banks emphasizes the fact that the

growth in earnings of the companies are slowing down, representing the influence of

enhanced regulatory needs and a downcast domestic economy. However, specific margins

have continuously decreased across diverse majors in spite of asset re-pricing and enhanced

financing from different customer deposits, stressing all the difficulties of the present low rate

of interest as well as deposits of customers. The economic outlook in this case remains

difficult and the majors continue to stress on the capital efficacy, overall productivity and

added refinement of different business models. Unceasingly challenging conditions of

market, increasing regulatory capital, enhancing loan impairments as well as margin

compression exert downward pressure on the returns of the industry (Arens et al., 2016).

Jointly, the majors operating in the banking industry of Australia declared a cash profit

enumerated after tax of approximately $29.6 billion during the financial year 2016 that is

necessarily down by around 2.5% recorded during 2015. The decrease in earnings mainly

owes to decrease in net margin of interest, flatter non interest earning, increase in loan

impairment alterations and greater cost of operations. In particular, these facets are also

apparent from the decrease in the specific statutory net gains from continued operations of

approximately $2.6 billion to nearly $28.8 billion. The challenging outlook for different

majors is essentially set to continuously driven by poor growth in revenue, erosion of margin,

enhanced charges of impairment, greater downward pressure on particularly return on equity

as well as earnings per share. Consequently, the ability of the majors to detect cost eliminate

Limited also takes into account the wealth division of the firm St. George. Furthermore, the

Westpac Institutional Bank also offers a wide range of financial services to different

commercial, corporate, institutional as well as government clientele.

Analysis of the banking industry

The financial results of the majority of the Australian banks emphasizes the fact that the

growth in earnings of the companies are slowing down, representing the influence of

enhanced regulatory needs and a downcast domestic economy. However, specific margins

have continuously decreased across diverse majors in spite of asset re-pricing and enhanced

financing from different customer deposits, stressing all the difficulties of the present low rate

of interest as well as deposits of customers. The economic outlook in this case remains

difficult and the majors continue to stress on the capital efficacy, overall productivity and

added refinement of different business models. Unceasingly challenging conditions of

market, increasing regulatory capital, enhancing loan impairments as well as margin

compression exert downward pressure on the returns of the industry (Arens et al., 2016).

Jointly, the majors operating in the banking industry of Australia declared a cash profit

enumerated after tax of approximately $29.6 billion during the financial year 2016 that is

necessarily down by around 2.5% recorded during 2015. The decrease in earnings mainly

owes to decrease in net margin of interest, flatter non interest earning, increase in loan

impairment alterations and greater cost of operations. In particular, these facets are also

apparent from the decrease in the specific statutory net gains from continued operations of

approximately $2.6 billion to nearly $28.8 billion. The challenging outlook for different

majors is essentially set to continuously driven by poor growth in revenue, erosion of margin,

enhanced charges of impairment, greater downward pressure on particularly return on equity

as well as earnings per share. Consequently, the ability of the majors to detect cost eliminate

7AUDITING AND ASSURANCE

chances that can be realised specifically in the short and medium terms without

compromising with the prospects of the growth of the revenue.

Analysis of the business risk of the client

Analysis of the operations of the business Westpac Banking helps in understanding the

exposure to diverse business risks. Varying nature as well as scope of business operations

also poses business risks. Essentially, Westpac has a diverse mix of specific financial market

trading business to particularly St. George along with the important operations in institutional

banking, underwriting along with general insurance all of these expose the shareholders of

the firm St. George to diverse risks than normally they are exposed to (Westpac - Personal,

Business and Corporate Banking, 2017).

In essence, St, George has no exposure to the market of New Zealand. In essentially, Westpac

generates around 15% to 20% of the profit enumerated after tax from the business operations

of the company in New Zealand (Westpac - Personal, Business and Corporate Banking,

2017). However, St. George has not got any kind of exposure to the market of New Zealand.

In this case, it can be mentioned that the nation New Zealand is encountering slowdown in

terms of growth of economy due to the outcome of the slowdown of the housing market,

drought, higher rate of interest and increasing inflation that have eroded the overall consumer

as well as business confidence (Westpac - Personal, Business and Corporate Banking, 2017).

Essentially, these kinds of conditions can probably lead to low earnings and enhanced bad

debts from specifically New Zealand wing of Westpac.

Again, large bad debts also pose business risks to the operations of Westpac. In particular,

Westpac also declared that it does not have the identical level of exposure to the specific

kinds of loans that have compelled both NAB as well as ANZ to declare enhancement in the

overall provisions as well as write downs for the period ending on Sept 2008 (Westpac -

chances that can be realised specifically in the short and medium terms without

compromising with the prospects of the growth of the revenue.

Analysis of the business risk of the client

Analysis of the operations of the business Westpac Banking helps in understanding the

exposure to diverse business risks. Varying nature as well as scope of business operations

also poses business risks. Essentially, Westpac has a diverse mix of specific financial market

trading business to particularly St. George along with the important operations in institutional

banking, underwriting along with general insurance all of these expose the shareholders of

the firm St. George to diverse risks than normally they are exposed to (Westpac - Personal,

Business and Corporate Banking, 2017).

In essence, St, George has no exposure to the market of New Zealand. In essentially, Westpac

generates around 15% to 20% of the profit enumerated after tax from the business operations

of the company in New Zealand (Westpac - Personal, Business and Corporate Banking,

2017). However, St. George has not got any kind of exposure to the market of New Zealand.

In this case, it can be mentioned that the nation New Zealand is encountering slowdown in

terms of growth of economy due to the outcome of the slowdown of the housing market,

drought, higher rate of interest and increasing inflation that have eroded the overall consumer

as well as business confidence (Westpac - Personal, Business and Corporate Banking, 2017).

Essentially, these kinds of conditions can probably lead to low earnings and enhanced bad

debts from specifically New Zealand wing of Westpac.

Again, large bad debts also pose business risks to the operations of Westpac. In particular,

Westpac also declared that it does not have the identical level of exposure to the specific

kinds of loans that have compelled both NAB as well as ANZ to declare enhancement in the

overall provisions as well as write downs for the period ending on Sept 2008 (Westpac -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8AUDITING AND ASSURANCE

Personal, Business and Corporate Banking, 2017). The company also have small

collateralised obligations of debt, however, management of the firm has publicly declared

that this specific portfolio has witnessed no significant measurable influence on earnings.

Nevertheless, all banking corporations are essentially exposed to different degrees of rising

level of bad debt and this firm Westpac also have exposure to the weak commercial property

as well as markets of New Zealand (Westpac - Personal, Business and Corporate Banking,

2017). Contrarily,rating organization Standard & Poor’s also substantiated the AA rating of

Westpac after analysis of the probable credit loss during the short to the medium period of

time.

The company Westpac also faces business risk in the making huge investments for the

process of reviewing the legacy information system. Essentially, this might possibly add to

the overall level of complexity and risk to the procedure of assimilation (Westpac - Personal,

Business and Corporate Banking, 2017).

In addition to this, association with the third parties of the corporation that is within RAMS

businesses as well as BTIM (by means of license contracts) generate added risks since poor

level of performance or else termination of specific agreements of franchise might influence

the revenue adversely and cause damage to the brand.

The corporation Westpac also faces contingent liability risk. This is because the corporation

Westpac is engaged in a number of actual or else potential claims as well as proceedings in

diverse ordinary processes of business (counting tax liabilities) that are not determined and

for that no specific provision is there in the balance sheet (Westpac - Personal, Business and

Corporate Banking, 2017).

There are also certain unavoidable business risks faced by the firm Westpac. Westpac is

necessarily subject to specific disclosure requirements of particularly ASX and compliance

Personal, Business and Corporate Banking, 2017). The company also have small

collateralised obligations of debt, however, management of the firm has publicly declared

that this specific portfolio has witnessed no significant measurable influence on earnings.

Nevertheless, all banking corporations are essentially exposed to different degrees of rising

level of bad debt and this firm Westpac also have exposure to the weak commercial property

as well as markets of New Zealand (Westpac - Personal, Business and Corporate Banking,

2017). Contrarily,rating organization Standard & Poor’s also substantiated the AA rating of

Westpac after analysis of the probable credit loss during the short to the medium period of

time.

The company Westpac also faces business risk in the making huge investments for the

process of reviewing the legacy information system. Essentially, this might possibly add to

the overall level of complexity and risk to the procedure of assimilation (Westpac - Personal,

Business and Corporate Banking, 2017).

In addition to this, association with the third parties of the corporation that is within RAMS

businesses as well as BTIM (by means of license contracts) generate added risks since poor

level of performance or else termination of specific agreements of franchise might influence

the revenue adversely and cause damage to the brand.

The corporation Westpac also faces contingent liability risk. This is because the corporation

Westpac is engaged in a number of actual or else potential claims as well as proceedings in

diverse ordinary processes of business (counting tax liabilities) that are not determined and

for that no specific provision is there in the balance sheet (Westpac - Personal, Business and

Corporate Banking, 2017).

There are also certain unavoidable business risks faced by the firm Westpac. Westpac is

necessarily subject to specific disclosure requirements of particularly ASX and compliance

9AUDITING AND ASSURANCE

with the requirements poses risk to the business. Additionally, the assimilation of the system

of information technology of both St. George and the company Westpac is also considered to

be very intricate and risky and require considerable investment of both time as well as

resources (Westpac - Personal, Business and Corporate Banking, 2017). Considerable amount

of risk also remains in using two brand strategies that is essentially being attempted on a scale

that is much larger than what is has been in other dealing.

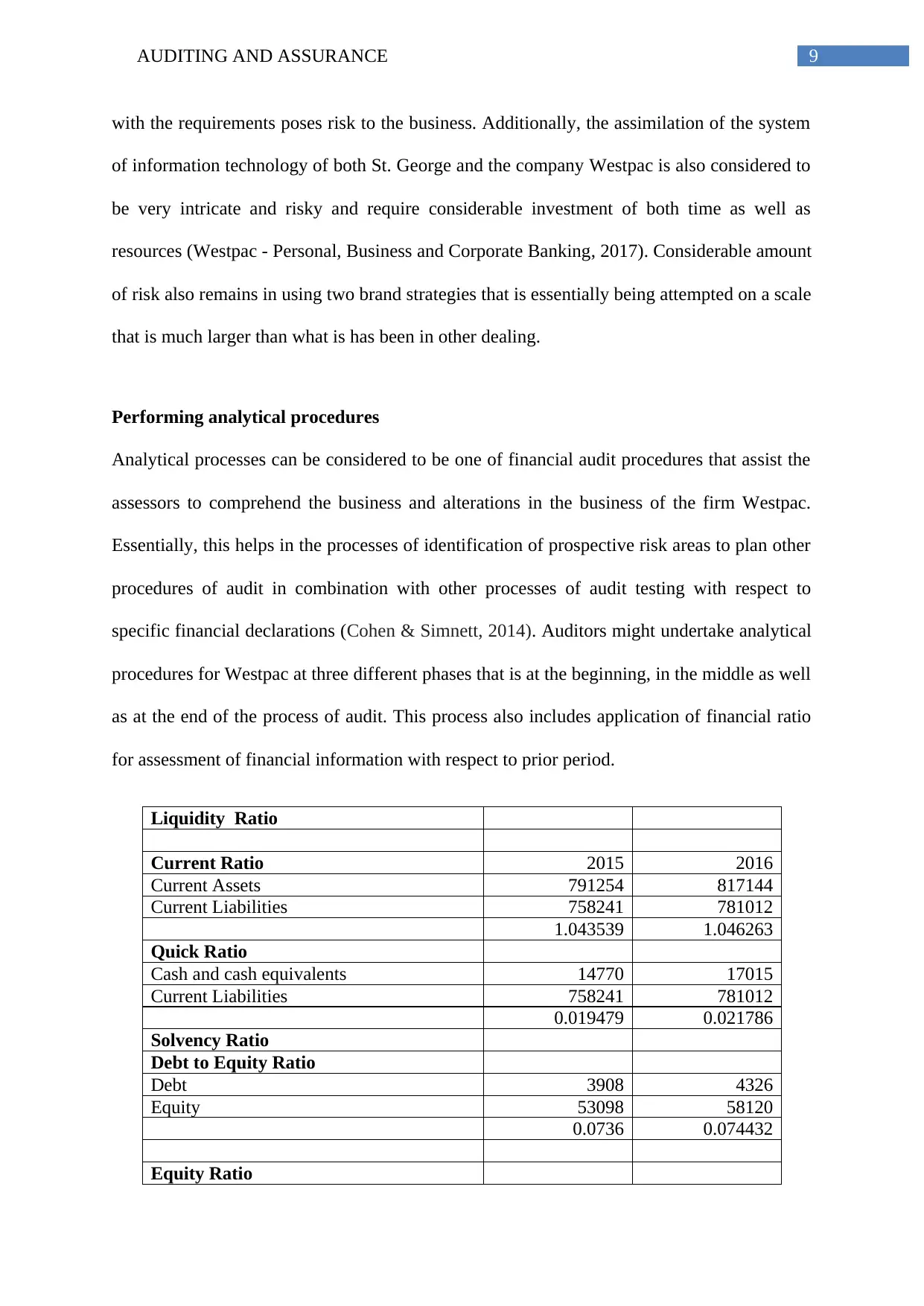

Performing analytical procedures

Analytical processes can be considered to be one of financial audit procedures that assist the

assessors to comprehend the business and alterations in the business of the firm Westpac.

Essentially, this helps in the processes of identification of prospective risk areas to plan other

procedures of audit in combination with other processes of audit testing with respect to

specific financial declarations (Cohen & Simnett, 2014). Auditors might undertake analytical

procedures for Westpac at three different phases that is at the beginning, in the middle as well

as at the end of the process of audit. This process also includes application of financial ratio

for assessment of financial information with respect to prior period.

Liquidity Ratio

Current Ratio 2015 2016

Current Assets 791254 817144

Current Liabilities 758241 781012

1.043539 1.046263

Quick Ratio

Cash and cash equivalents 14770 17015

Current Liabilities 758241 781012

0.019479 0.021786

Solvency Ratio

Debt to Equity Ratio

Debt 3908 4326

Equity 53098 58120

0.0736 0.074432

Equity Ratio

with the requirements poses risk to the business. Additionally, the assimilation of the system

of information technology of both St. George and the company Westpac is also considered to

be very intricate and risky and require considerable investment of both time as well as

resources (Westpac - Personal, Business and Corporate Banking, 2017). Considerable amount

of risk also remains in using two brand strategies that is essentially being attempted on a scale

that is much larger than what is has been in other dealing.

Performing analytical procedures

Analytical processes can be considered to be one of financial audit procedures that assist the

assessors to comprehend the business and alterations in the business of the firm Westpac.

Essentially, this helps in the processes of identification of prospective risk areas to plan other

procedures of audit in combination with other processes of audit testing with respect to

specific financial declarations (Cohen & Simnett, 2014). Auditors might undertake analytical

procedures for Westpac at three different phases that is at the beginning, in the middle as well

as at the end of the process of audit. This process also includes application of financial ratio

for assessment of financial information with respect to prior period.

Liquidity Ratio

Current Ratio 2015 2016

Current Assets 791254 817144

Current Liabilities 758241 781012

1.043539 1.046263

Quick Ratio

Cash and cash equivalents 14770 17015

Current Liabilities 758241 781012

0.019479 0.021786

Solvency Ratio

Debt to Equity Ratio

Debt 3908 4326

Equity 53098 58120

0.0736 0.074432

Equity Ratio

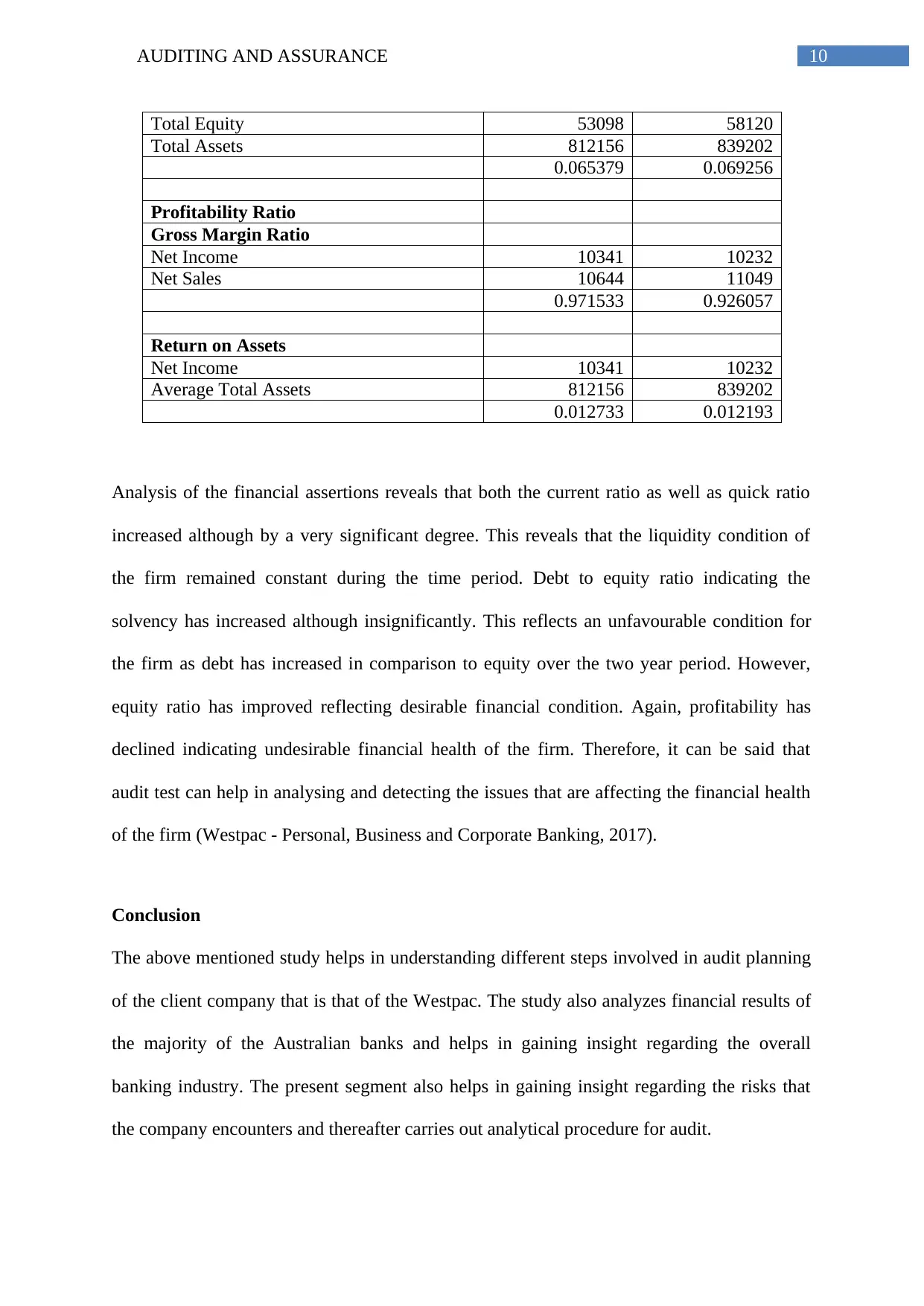

10AUDITING AND ASSURANCE

Total Equity 53098 58120

Total Assets 812156 839202

0.065379 0.069256

Profitability Ratio

Gross Margin Ratio

Net Income 10341 10232

Net Sales 10644 11049

0.971533 0.926057

Return on Assets

Net Income 10341 10232

Average Total Assets 812156 839202

0.012733 0.012193

Analysis of the financial assertions reveals that both the current ratio as well as quick ratio

increased although by a very significant degree. This reveals that the liquidity condition of

the firm remained constant during the time period. Debt to equity ratio indicating the

solvency has increased although insignificantly. This reflects an unfavourable condition for

the firm as debt has increased in comparison to equity over the two year period. However,

equity ratio has improved reflecting desirable financial condition. Again, profitability has

declined indicating undesirable financial health of the firm. Therefore, it can be said that

audit test can help in analysing and detecting the issues that are affecting the financial health

of the firm (Westpac - Personal, Business and Corporate Banking, 2017).

Conclusion

The above mentioned study helps in understanding different steps involved in audit planning

of the client company that is that of the Westpac. The study also analyzes financial results of

the majority of the Australian banks and helps in gaining insight regarding the overall

banking industry. The present segment also helps in gaining insight regarding the risks that

the company encounters and thereafter carries out analytical procedure for audit.

Total Equity 53098 58120

Total Assets 812156 839202

0.065379 0.069256

Profitability Ratio

Gross Margin Ratio

Net Income 10341 10232

Net Sales 10644 11049

0.971533 0.926057

Return on Assets

Net Income 10341 10232

Average Total Assets 812156 839202

0.012733 0.012193

Analysis of the financial assertions reveals that both the current ratio as well as quick ratio

increased although by a very significant degree. This reveals that the liquidity condition of

the firm remained constant during the time period. Debt to equity ratio indicating the

solvency has increased although insignificantly. This reflects an unfavourable condition for

the firm as debt has increased in comparison to equity over the two year period. However,

equity ratio has improved reflecting desirable financial condition. Again, profitability has

declined indicating undesirable financial health of the firm. Therefore, it can be said that

audit test can help in analysing and detecting the issues that are affecting the financial health

of the firm (Westpac - Personal, Business and Corporate Banking, 2017).

Conclusion

The above mentioned study helps in understanding different steps involved in audit planning

of the client company that is that of the Westpac. The study also analyzes financial results of

the majority of the Australian banks and helps in gaining insight regarding the overall

banking industry. The present segment also helps in gaining insight regarding the risks that

the company encounters and thereafter carries out analytical procedure for audit.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11AUDITING AND ASSURANCE

References

Arens, A. A., Best, P., Shailer, G., Fiedler, B., Elder, R. J., & Beasley, M. (2016). Auditing

and assurance services in Australia: an integrated approach. Pearson Education

Australia.

Arens, A. A., Elder, R. J., & Beasley, M. S. (2016). Auditing and assurance services: An

integrated approach. Prentice Hall.

Arens, A. A., Elder, R. J., & Mark, B. (2012). Auditing and assurance services: an integrated

approach. Boston: Prentice Hall.

Arens, A. A., Elder, R. J., Beasley, M. S., & Jenkins, G. J. (2016). Essentials of Auditing and

Assurance Services: An Integrated Approach. New Jersey: Prentice Hall.

Cohen, J. R., & Simnett, R. (2014). CSR and assurance services: A research

agenda. Auditing: A Journal of Practice & Theory, 34(1), 59-74.

Eilifsen, A., Messier, W. F., Glover, S. M., & Prawitt, D. F. (2013). Auditing and assurance

services. McGraw-Hill.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Simnett, R., Carson, E., & Vanstraelen, A. (2016). International Archival Auditing and

Assurance Research: Trends, Methodological Issues, and Opportunities. Auditing: A

Journal of Practice & Theory, 35(3), 1-32.

Westpac - Personal, Business and Corporate Banking. (2017). Westpac.com.au. Retrieved 11

September 2017, from http://www.westpac.com.au

References

Arens, A. A., Best, P., Shailer, G., Fiedler, B., Elder, R. J., & Beasley, M. (2016). Auditing

and assurance services in Australia: an integrated approach. Pearson Education

Australia.

Arens, A. A., Elder, R. J., & Beasley, M. S. (2016). Auditing and assurance services: An

integrated approach. Prentice Hall.

Arens, A. A., Elder, R. J., & Mark, B. (2012). Auditing and assurance services: an integrated

approach. Boston: Prentice Hall.

Arens, A. A., Elder, R. J., Beasley, M. S., & Jenkins, G. J. (2016). Essentials of Auditing and

Assurance Services: An Integrated Approach. New Jersey: Prentice Hall.

Cohen, J. R., & Simnett, R. (2014). CSR and assurance services: A research

agenda. Auditing: A Journal of Practice & Theory, 34(1), 59-74.

Eilifsen, A., Messier, W. F., Glover, S. M., & Prawitt, D. F. (2013). Auditing and assurance

services. McGraw-Hill.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Simnett, R., Carson, E., & Vanstraelen, A. (2016). International Archival Auditing and

Assurance Research: Trends, Methodological Issues, and Opportunities. Auditing: A

Journal of Practice & Theory, 35(3), 1-32.

Westpac - Personal, Business and Corporate Banking. (2017). Westpac.com.au. Retrieved 11

September 2017, from http://www.westpac.com.au

12AUDITING AND ASSURANCE

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.