CQUniversity Auditing and Ethics Report: Amcor Plc Audit Analysis

VerifiedAdded on 2022/09/01

|12

|2828

|37

Report

AI Summary

This report analyzes the audit of Amcor Plc, a listed company, focusing on materiality, analytical review, and audit procedures. The report begins by discussing materiality, including benchmark selection and percentage determination, and calculates the materiality level for Amcor Plc. It then reviews draft notes and disclosures, highlighting contingencies and legal proceedings that require audit consideration. The report continues with a preliminary analytical review, examining operating profit margin, net profit margin, current ratio, quick ratio, accounts receivable turnover ratio, debt to equity ratio, and debt ratio, identifying trends and potential areas of concern. The analysis extends to the statement of cash flows, reviewing operating, financing, and investing activities, and assessing the risk of going concern. Finally, the report reviews the audit report, discussing the unqualified opinion issued by PricewaterhouseCoopers and concluding on the fairness of the financial statements.

Running head: AUDITING AND ETHICS

Auditing and Ethics

Name of the Student

Name of the University

Author’s Note

Auditing and Ethics

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHICS

Table of Contents

Introduction................................................................................................................................2

Section 1.....................................................................................................................................2

Materiality..............................................................................................................................2

Review of Draft Notes and Disclosures.................................................................................4

Section 2.....................................................................................................................................5

Section 3.....................................................................................................................................7

Statement of Cash Flows Review..........................................................................................7

Audit Report Review..............................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Section 1.....................................................................................................................................2

Materiality..............................................................................................................................2

Review of Draft Notes and Disclosures.................................................................................4

Section 2.....................................................................................................................................5

Section 3.....................................................................................................................................7

Statement of Cash Flows Review..........................................................................................7

Audit Report Review..............................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

2AUDITING AND ETHICS

Introduction

It is the responsibility of the auditors to account for the required aspects at the time to

carry out the required audit procedures. Ascertaining the materiality level is one of these

aspects where the auditors are required to consider the required aspects associated with the

ascertainment of audit materiality. In addition, the auditors are responsible for reviewing

different drafts and disclosures of the company’s financial statements for identifying the areas

with major audit attention. They are required to undertake the necessary preliminary

analytical review of the financial statements for the identification of the risk areas. They are

also responsible for assessing the risk of going concern of the clients by taking into account

the required factors (Wigunani, 2016). There are three part of this report. The first part

discusses about audit materiality and review of drafts as well as notes of Amcor Plc. The

second part undertakes the preliminary analytical review of the financial reports of Amcor

Plc. The last part discusses about cash flow, going concern and audit report of the same

company.

Section 1

Materiality

According to ASA 320, Paragraph 2, in auditing, materiality can be considered as the

misstatements that include individual or aggregate omission that can reasonably influence the

decision of the users of the financial information on the basis of the financial statements. The

auditors are required to make the materiality related judgments by considering the

surrounding condition; and the nature and size of the material misstatements affect the audit

judgements (auasb.gov.au, 2019). In auditing, materiality level is determined through three

stages.

Introduction

It is the responsibility of the auditors to account for the required aspects at the time to

carry out the required audit procedures. Ascertaining the materiality level is one of these

aspects where the auditors are required to consider the required aspects associated with the

ascertainment of audit materiality. In addition, the auditors are responsible for reviewing

different drafts and disclosures of the company’s financial statements for identifying the areas

with major audit attention. They are required to undertake the necessary preliminary

analytical review of the financial statements for the identification of the risk areas. They are

also responsible for assessing the risk of going concern of the clients by taking into account

the required factors (Wigunani, 2016). There are three part of this report. The first part

discusses about audit materiality and review of drafts as well as notes of Amcor Plc. The

second part undertakes the preliminary analytical review of the financial reports of Amcor

Plc. The last part discusses about cash flow, going concern and audit report of the same

company.

Section 1

Materiality

According to ASA 320, Paragraph 2, in auditing, materiality can be considered as the

misstatements that include individual or aggregate omission that can reasonably influence the

decision of the users of the financial information on the basis of the financial statements. The

auditors are required to make the materiality related judgments by considering the

surrounding condition; and the nature and size of the material misstatements affect the audit

judgements (auasb.gov.au, 2019). In auditing, materiality level is determined through three

stages.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHICS

Stage 1 – Selection of the appropriate and applicable benchmark is vital in the ascertainment

of level of materiality. The selection of the correct benchmark is largely dependent on the

consideration of the industry in which Amcor Plc operates and its nature. There are many

benchmarks utilized by the auditors in materiality determination process such as earnings

before tax, total revenue, total assets, gross profit and others (Jacoby & Levy, 2016). 2019

Annual Report of Amcor Plc shows $604.1 million as the income from continuous operations

before income taxes; and this is earnings before tax. This would be the benchmark for

materiality determination of Amcor Plc.

Stage 2 – Selection of the appropriate and applicable percentage is also vital in the

materiality determination process and correct quantitative threshold must be selected as

guidance to ascertain the materiality level. AASB 1031 Materiality prescribes two

quantitative thresholds for the determination of materiality. They are as follows:

a) An amount which is greater than or equal to 10% of the certain benchmark may be

considered as material; and

b) An amount which is less than or equal to 5% of the preferred benchmark may be

considered as material (aasb.gov.au, 2019).

Apart from these quantitative thresholds, professional judgement of the auditor and the

entity’s characteristic also matter in the materiality determination process. In case of Amcor

Plc, 5% would be considered as the relevant percentage.

Stage 3 – It is now needed to calculate the materiality level for the 2019 audit of Amcor Plc

after choosing the relevant benchmark and percentage and then justification needs to be

provided. The calculation is shown below:

Materiality Level = Earnings before Tax × 5%

= $604.1 million × 5%

Stage 1 – Selection of the appropriate and applicable benchmark is vital in the ascertainment

of level of materiality. The selection of the correct benchmark is largely dependent on the

consideration of the industry in which Amcor Plc operates and its nature. There are many

benchmarks utilized by the auditors in materiality determination process such as earnings

before tax, total revenue, total assets, gross profit and others (Jacoby & Levy, 2016). 2019

Annual Report of Amcor Plc shows $604.1 million as the income from continuous operations

before income taxes; and this is earnings before tax. This would be the benchmark for

materiality determination of Amcor Plc.

Stage 2 – Selection of the appropriate and applicable percentage is also vital in the

materiality determination process and correct quantitative threshold must be selected as

guidance to ascertain the materiality level. AASB 1031 Materiality prescribes two

quantitative thresholds for the determination of materiality. They are as follows:

a) An amount which is greater than or equal to 10% of the certain benchmark may be

considered as material; and

b) An amount which is less than or equal to 5% of the preferred benchmark may be

considered as material (aasb.gov.au, 2019).

Apart from these quantitative thresholds, professional judgement of the auditor and the

entity’s characteristic also matter in the materiality determination process. In case of Amcor

Plc, 5% would be considered as the relevant percentage.

Stage 3 – It is now needed to calculate the materiality level for the 2019 audit of Amcor Plc

after choosing the relevant benchmark and percentage and then justification needs to be

provided. The calculation is shown below:

Materiality Level = Earnings before Tax × 5%

= $604.1 million × 5%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHICS

= $30.21 million (Approximately)

Earnings before tax is selected as this is the most commonly used performance metric

and mostly accepted benchmark in the industry in which Amcor Plc operates 5% is selected

based on professional judgment since this is in the range of usually established quantitative

measure of materiality (Jacoby & Levy, 2016).

Review of Draft Notes and Disclosures

Contingencies – Under the customary local regulations in Brazil, the Brazilian subsidiaries

of Amcor Plc may require to post other collateral or cash in case there is a challenge to any

administrative examination process to the Brazilian court system. At June 30, 2019 and 2018,

an accrual of $16.4 million and $15.1 million has been recorded by the company in the non-

current liabilities and this has led to a possibly loss exposure of the accrual $23.7 million and

$22.7 million respectively. Since, there is many uncertainties involved in the litigation

process, there can be mismatch between the ultimate outcomes of these matters with the

company’s assessment (assets.ctfassets.net, 2019). This matter is significant for the audit of

2019 since this can materially misstate the financial reports of Amcor Plc. The required audit

procedure is to evaluate the likelihood that the events will occur. The probability can be

remote, realistically possible or probable. In case the likelihood is probable, appropriate

accounting treatment would be required to adopt (Herda & Lavelle, 2014).

Legal Proceedings –Amcor Plc has been involved in a legal proceeding associated with the

transaction between them and Bemis; and this is related to the payment of fair value of the

funds of two shareholders. Amcor Plc has not disclosed any assessment on this matter and

this requires audit consideration (assets.ctfassets.net, 2019). It is required to assess the

likelihood of the occurrence of the legal proceedings so that appropriate action can be taken

(Herda & Lavelle, 2014).

= $30.21 million (Approximately)

Earnings before tax is selected as this is the most commonly used performance metric

and mostly accepted benchmark in the industry in which Amcor Plc operates 5% is selected

based on professional judgment since this is in the range of usually established quantitative

measure of materiality (Jacoby & Levy, 2016).

Review of Draft Notes and Disclosures

Contingencies – Under the customary local regulations in Brazil, the Brazilian subsidiaries

of Amcor Plc may require to post other collateral or cash in case there is a challenge to any

administrative examination process to the Brazilian court system. At June 30, 2019 and 2018,

an accrual of $16.4 million and $15.1 million has been recorded by the company in the non-

current liabilities and this has led to a possibly loss exposure of the accrual $23.7 million and

$22.7 million respectively. Since, there is many uncertainties involved in the litigation

process, there can be mismatch between the ultimate outcomes of these matters with the

company’s assessment (assets.ctfassets.net, 2019). This matter is significant for the audit of

2019 since this can materially misstate the financial reports of Amcor Plc. The required audit

procedure is to evaluate the likelihood that the events will occur. The probability can be

remote, realistically possible or probable. In case the likelihood is probable, appropriate

accounting treatment would be required to adopt (Herda & Lavelle, 2014).

Legal Proceedings –Amcor Plc has been involved in a legal proceeding associated with the

transaction between them and Bemis; and this is related to the payment of fair value of the

funds of two shareholders. Amcor Plc has not disclosed any assessment on this matter and

this requires audit consideration (assets.ctfassets.net, 2019). It is required to assess the

likelihood of the occurrence of the legal proceedings so that appropriate action can be taken

(Herda & Lavelle, 2014).

5AUDITING AND ETHICS

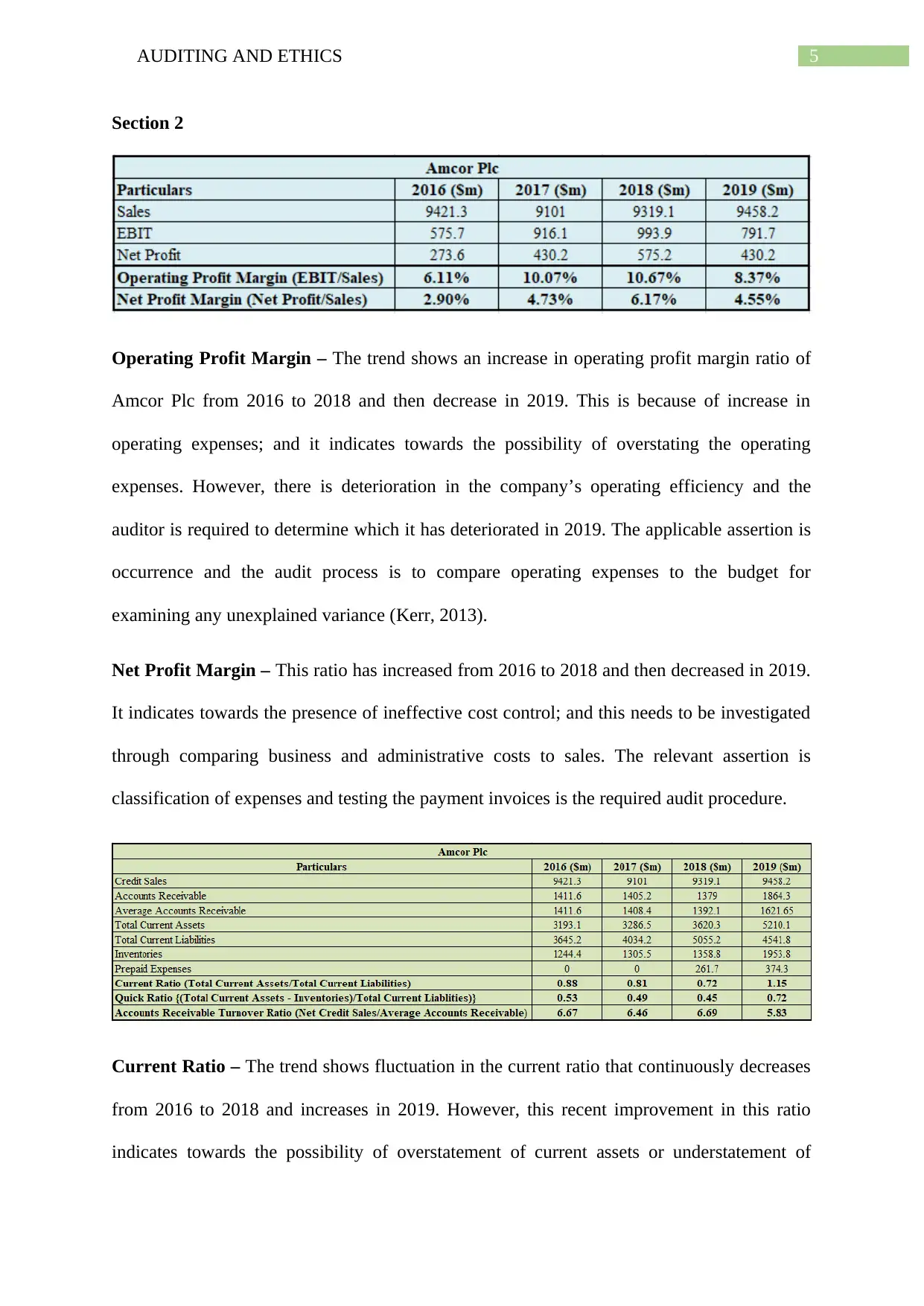

Section 2

Operating Profit Margin – The trend shows an increase in operating profit margin ratio of

Amcor Plc from 2016 to 2018 and then decrease in 2019. This is because of increase in

operating expenses; and it indicates towards the possibility of overstating the operating

expenses. However, there is deterioration in the company’s operating efficiency and the

auditor is required to determine which it has deteriorated in 2019. The applicable assertion is

occurrence and the audit process is to compare operating expenses to the budget for

examining any unexplained variance (Kerr, 2013).

Net Profit Margin – This ratio has increased from 2016 to 2018 and then decreased in 2019.

It indicates towards the presence of ineffective cost control; and this needs to be investigated

through comparing business and administrative costs to sales. The relevant assertion is

classification of expenses and testing the payment invoices is the required audit procedure.

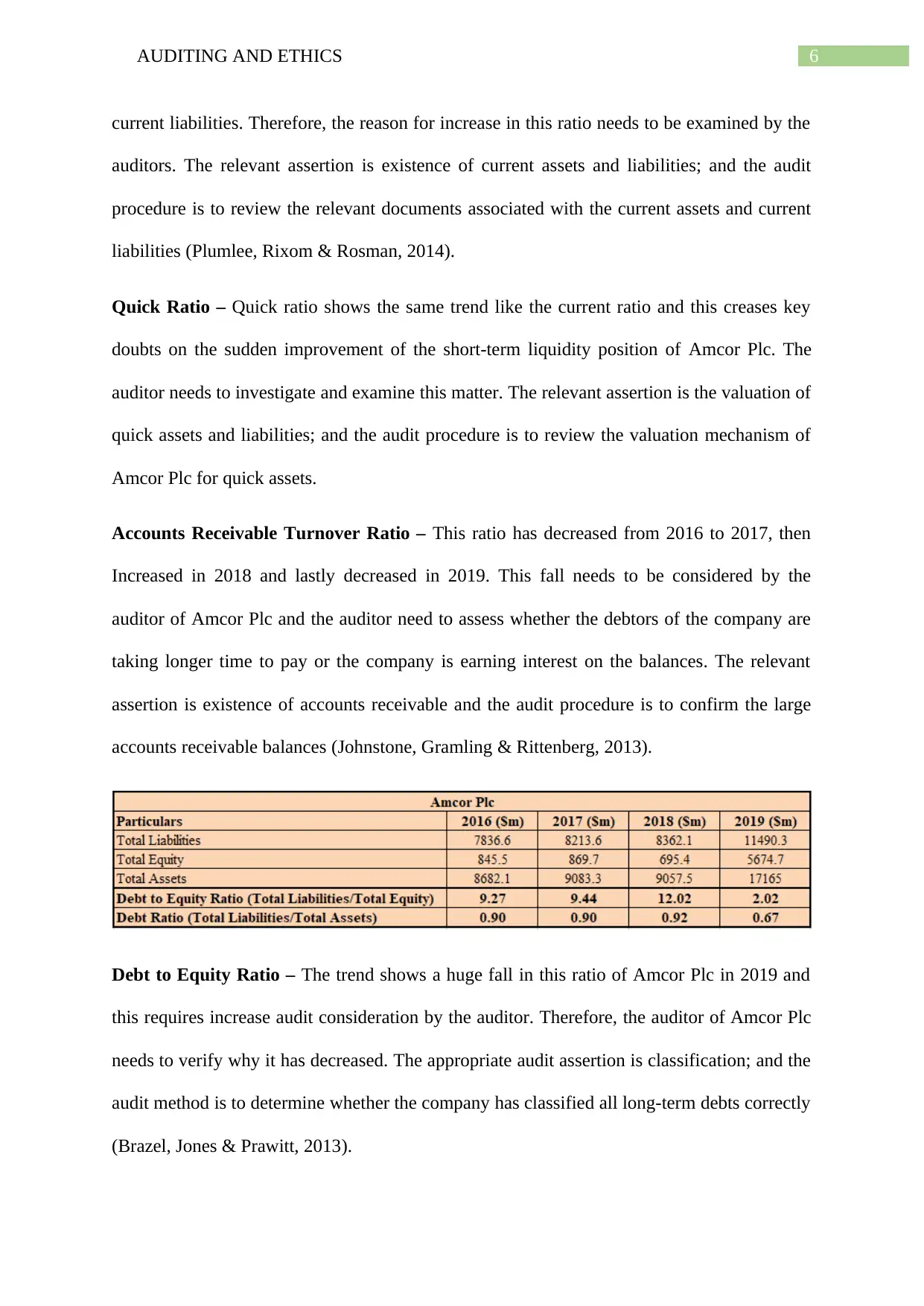

Current Ratio – The trend shows fluctuation in the current ratio that continuously decreases

from 2016 to 2018 and increases in 2019. However, this recent improvement in this ratio

indicates towards the possibility of overstatement of current assets or understatement of

Section 2

Operating Profit Margin – The trend shows an increase in operating profit margin ratio of

Amcor Plc from 2016 to 2018 and then decrease in 2019. This is because of increase in

operating expenses; and it indicates towards the possibility of overstating the operating

expenses. However, there is deterioration in the company’s operating efficiency and the

auditor is required to determine which it has deteriorated in 2019. The applicable assertion is

occurrence and the audit process is to compare operating expenses to the budget for

examining any unexplained variance (Kerr, 2013).

Net Profit Margin – This ratio has increased from 2016 to 2018 and then decreased in 2019.

It indicates towards the presence of ineffective cost control; and this needs to be investigated

through comparing business and administrative costs to sales. The relevant assertion is

classification of expenses and testing the payment invoices is the required audit procedure.

Current Ratio – The trend shows fluctuation in the current ratio that continuously decreases

from 2016 to 2018 and increases in 2019. However, this recent improvement in this ratio

indicates towards the possibility of overstatement of current assets or understatement of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHICS

current liabilities. Therefore, the reason for increase in this ratio needs to be examined by the

auditors. The relevant assertion is existence of current assets and liabilities; and the audit

procedure is to review the relevant documents associated with the current assets and current

liabilities (Plumlee, Rixom & Rosman, 2014).

Quick Ratio – Quick ratio shows the same trend like the current ratio and this creases key

doubts on the sudden improvement of the short-term liquidity position of Amcor Plc. The

auditor needs to investigate and examine this matter. The relevant assertion is the valuation of

quick assets and liabilities; and the audit procedure is to review the valuation mechanism of

Amcor Plc for quick assets.

Accounts Receivable Turnover Ratio – This ratio has decreased from 2016 to 2017, then

Increased in 2018 and lastly decreased in 2019. This fall needs to be considered by the

auditor of Amcor Plc and the auditor need to assess whether the debtors of the company are

taking longer time to pay or the company is earning interest on the balances. The relevant

assertion is existence of accounts receivable and the audit procedure is to confirm the large

accounts receivable balances (Johnstone, Gramling & Rittenberg, 2013).

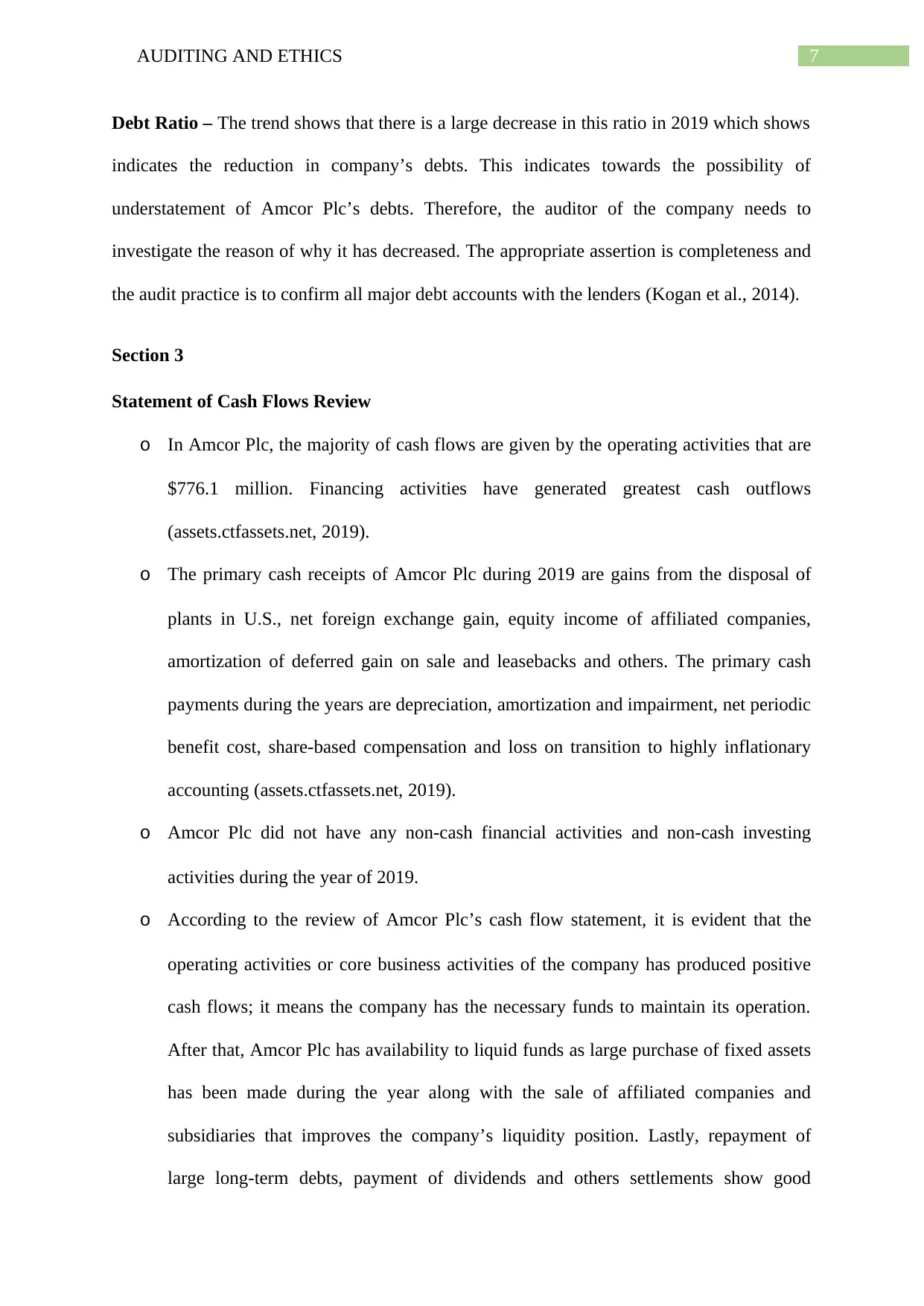

Debt to Equity Ratio – The trend shows a huge fall in this ratio of Amcor Plc in 2019 and

this requires increase audit consideration by the auditor. Therefore, the auditor of Amcor Plc

needs to verify why it has decreased. The appropriate audit assertion is classification; and the

audit method is to determine whether the company has classified all long-term debts correctly

(Brazel, Jones & Prawitt, 2013).

current liabilities. Therefore, the reason for increase in this ratio needs to be examined by the

auditors. The relevant assertion is existence of current assets and liabilities; and the audit

procedure is to review the relevant documents associated with the current assets and current

liabilities (Plumlee, Rixom & Rosman, 2014).

Quick Ratio – Quick ratio shows the same trend like the current ratio and this creases key

doubts on the sudden improvement of the short-term liquidity position of Amcor Plc. The

auditor needs to investigate and examine this matter. The relevant assertion is the valuation of

quick assets and liabilities; and the audit procedure is to review the valuation mechanism of

Amcor Plc for quick assets.

Accounts Receivable Turnover Ratio – This ratio has decreased from 2016 to 2017, then

Increased in 2018 and lastly decreased in 2019. This fall needs to be considered by the

auditor of Amcor Plc and the auditor need to assess whether the debtors of the company are

taking longer time to pay or the company is earning interest on the balances. The relevant

assertion is existence of accounts receivable and the audit procedure is to confirm the large

accounts receivable balances (Johnstone, Gramling & Rittenberg, 2013).

Debt to Equity Ratio – The trend shows a huge fall in this ratio of Amcor Plc in 2019 and

this requires increase audit consideration by the auditor. Therefore, the auditor of Amcor Plc

needs to verify why it has decreased. The appropriate audit assertion is classification; and the

audit method is to determine whether the company has classified all long-term debts correctly

(Brazel, Jones & Prawitt, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHICS

Debt Ratio – The trend shows that there is a large decrease in this ratio in 2019 which shows

indicates the reduction in company’s debts. This indicates towards the possibility of

understatement of Amcor Plc’s debts. Therefore, the auditor of the company needs to

investigate the reason of why it has decreased. The appropriate assertion is completeness and

the audit practice is to confirm all major debt accounts with the lenders (Kogan et al., 2014).

Section 3

Statement of Cash Flows Review

o In Amcor Plc, the majority of cash flows are given by the operating activities that are

$776.1 million. Financing activities have generated greatest cash outflows

(assets.ctfassets.net, 2019).

o The primary cash receipts of Amcor Plc during 2019 are gains from the disposal of

plants in U.S., net foreign exchange gain, equity income of affiliated companies,

amortization of deferred gain on sale and leasebacks and others. The primary cash

payments during the years are depreciation, amortization and impairment, net periodic

benefit cost, share-based compensation and loss on transition to highly inflationary

accounting (assets.ctfassets.net, 2019).

o Amcor Plc did not have any non-cash financial activities and non-cash investing

activities during the year of 2019.

o According to the review of Amcor Plc’s cash flow statement, it is evident that the

operating activities or core business activities of the company has produced positive

cash flows; it means the company has the necessary funds to maintain its operation.

After that, Amcor Plc has availability to liquid funds as large purchase of fixed assets

has been made during the year along with the sale of affiliated companies and

subsidiaries that improves the company’s liquidity position. Lastly, repayment of

large long-term debts, payment of dividends and others settlements show good

Debt Ratio – The trend shows that there is a large decrease in this ratio in 2019 which shows

indicates the reduction in company’s debts. This indicates towards the possibility of

understatement of Amcor Plc’s debts. Therefore, the auditor of the company needs to

investigate the reason of why it has decreased. The appropriate assertion is completeness and

the audit practice is to confirm all major debt accounts with the lenders (Kogan et al., 2014).

Section 3

Statement of Cash Flows Review

o In Amcor Plc, the majority of cash flows are given by the operating activities that are

$776.1 million. Financing activities have generated greatest cash outflows

(assets.ctfassets.net, 2019).

o The primary cash receipts of Amcor Plc during 2019 are gains from the disposal of

plants in U.S., net foreign exchange gain, equity income of affiliated companies,

amortization of deferred gain on sale and leasebacks and others. The primary cash

payments during the years are depreciation, amortization and impairment, net periodic

benefit cost, share-based compensation and loss on transition to highly inflationary

accounting (assets.ctfassets.net, 2019).

o Amcor Plc did not have any non-cash financial activities and non-cash investing

activities during the year of 2019.

o According to the review of Amcor Plc’s cash flow statement, it is evident that the

operating activities or core business activities of the company has produced positive

cash flows; it means the company has the necessary funds to maintain its operation.

After that, Amcor Plc has availability to liquid funds as large purchase of fixed assets

has been made during the year along with the sale of affiliated companies and

subsidiaries that improves the company’s liquidity position. Lastly, repayment of

large long-term debts, payment of dividends and others settlements show good

8AUDITING AND ETHICS

financial condition of Amcor Plc. All these aspects eliminate the risk of going concern

that is to wind up the operations in the coming years (Hapsoro & Suryanto, 2017).

However, in case there is any risk related to going concern, the auditors are required

to undertake the following audit procedures to address them:

1. Requesting the company’s management for the assessment of the going

concern status of the company.

2. Evaluating the plan of the management associated with the going concern

assessment with regard to the probability of implementing the management’s

plan and mitigating the events that raise the going concern doubt.

3. Determining whether the company has accurately disclosed any material

uncertainty in the financial statements (cpaaustralia.com.au, 2019).

Audit Report Review

It has been mentioned by the auditors of Amcor Plc that is PricewaterhouseCoopers

that the company’s all the consolidated financial statements has presented the firm’s financial

position, results of its operations and cash flow in the most fair manner by maintaining its

compliance with the generally accepted accounting principles in the United States of

America. Apart from this, the auditors of Amcor Plc has not disclosed about any kind of

issues in the audit report of 2019 (assets.ctfassets.net, 2019). It indicates towards the issue of

unqualified audit opinion or unmodified audit opinion. Unqualified or unmodified audit

opinion is issued when the financial statements of a company provide true and fair view of

the company’s financial performance and standing and required accounting standards have

been adopted for the preparation of the financial statements (Samudera, 2017). Since the

presence of all these aspects can be seen in Amcor Plc, providing unqualified or unmodified

audit opinion is justified.

financial condition of Amcor Plc. All these aspects eliminate the risk of going concern

that is to wind up the operations in the coming years (Hapsoro & Suryanto, 2017).

However, in case there is any risk related to going concern, the auditors are required

to undertake the following audit procedures to address them:

1. Requesting the company’s management for the assessment of the going

concern status of the company.

2. Evaluating the plan of the management associated with the going concern

assessment with regard to the probability of implementing the management’s

plan and mitigating the events that raise the going concern doubt.

3. Determining whether the company has accurately disclosed any material

uncertainty in the financial statements (cpaaustralia.com.au, 2019).

Audit Report Review

It has been mentioned by the auditors of Amcor Plc that is PricewaterhouseCoopers

that the company’s all the consolidated financial statements has presented the firm’s financial

position, results of its operations and cash flow in the most fair manner by maintaining its

compliance with the generally accepted accounting principles in the United States of

America. Apart from this, the auditors of Amcor Plc has not disclosed about any kind of

issues in the audit report of 2019 (assets.ctfassets.net, 2019). It indicates towards the issue of

unqualified audit opinion or unmodified audit opinion. Unqualified or unmodified audit

opinion is issued when the financial statements of a company provide true and fair view of

the company’s financial performance and standing and required accounting standards have

been adopted for the preparation of the financial statements (Samudera, 2017). Since the

presence of all these aspects can be seen in Amcor Plc, providing unqualified or unmodified

audit opinion is justified.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHICS

There is not any additional paragraph indicating any audit issue in the financial

statements of Amcor Plc.

Conclusion

The analysis shows that the level of materiality is determined through three stage

which are the determination of benchmark, determination of percentage and calculation of

materiality with proper rationale. Analysis of ratio is a key tool used in preliminary analytical

review; and this ratio analysis shows the auditors of Amcor Plc with the areas that required

additional attention and audit procedures; such as sudden decrease in profitability ratios,

decrease in level of debts and others. Review of the cash flows statements of Amcor Plc

shows that there is not any going concern risk in Amcor Plc as the company has good

financial performance with adequate liquid funds and good debt position. The auditors have

issued unqualified or unmodified audit opinion to Amcor Plc as there is not any audit issue in

the company’s financial reports.

There is not any additional paragraph indicating any audit issue in the financial

statements of Amcor Plc.

Conclusion

The analysis shows that the level of materiality is determined through three stage

which are the determination of benchmark, determination of percentage and calculation of

materiality with proper rationale. Analysis of ratio is a key tool used in preliminary analytical

review; and this ratio analysis shows the auditors of Amcor Plc with the areas that required

additional attention and audit procedures; such as sudden decrease in profitability ratios,

decrease in level of debts and others. Review of the cash flows statements of Amcor Plc

shows that there is not any going concern risk in Amcor Plc as the company has good

financial performance with adequate liquid funds and good debt position. The auditors have

issued unqualified or unmodified audit opinion to Amcor Plc as there is not any audit issue in

the company’s financial reports.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHICS

References

Aasb.gov.au. (2019). Materiality. Retrieved 31 December 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB1031_07-

04_COMPdec09_01-11.pdf

Assets.ctfassets.net. (2019). 2019 Annual Report. Retrieved 31 December 2019, from

https://assets.ctfassets.net/f7tuyt85vtoa/3TpBK6DXV7IBiEBbQ8g40Q/cedfc2f34b98

40bd503c6475108f6b79/Amcor-Annual-Report-10-K-2019.pdf

Assets.ctfassets.net. (2019). Annual Report 2017. Retrieved 31 December 2019, from

https://assets.ctfassets.net/f7tuyt85vtoa/2ckiIO9GXymIqu6qi8Oo4s/6a9b62ee553e2af

1e354e042c6055d8a/Amcor_Annual_Report_2017.pdf

Assets.ctfassets.net. (2019). Annual Report 2018. Retrieved 31 December 2019, from

https://assets.ctfassets.net/f7tuyt85vtoa/Ry9ogH9cQemqGA800oiGE/cbcc6bef0d76b7

9be2a227dfc13a7e87/Amcor_Annual_Report_2018.PDF

Auasb.gov.au. (2019). Auditing Standard ASA 320 Materiality in Planning and Performing

an Audit. Retrieved 31 December 2019, from

https://www.auasb.gov.au/admin/file/content102/c3/ASA_320_Compiled_2015.pdf

Brazel, J. F., Jones, K. L., & Prawitt, D. F. (2013). Auditors' reactions to inconsistencies

between financial and nonfinancial measures: The interactive effects of fraud risk

assessment and a decision prompt. Behavioral Research in Accounting, 26(1), 131-

156.

Cpaaustralia.com.au. (2019). A GUIDE TO UNDERSTANDING AUDITING AND

ASSURANCE: AUSTRALIAN LISTED COMPANIES NOVEMBER 2019. Retrieved

31 December 2019, from

References

Aasb.gov.au. (2019). Materiality. Retrieved 31 December 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB1031_07-

04_COMPdec09_01-11.pdf

Assets.ctfassets.net. (2019). 2019 Annual Report. Retrieved 31 December 2019, from

https://assets.ctfassets.net/f7tuyt85vtoa/3TpBK6DXV7IBiEBbQ8g40Q/cedfc2f34b98

40bd503c6475108f6b79/Amcor-Annual-Report-10-K-2019.pdf

Assets.ctfassets.net. (2019). Annual Report 2017. Retrieved 31 December 2019, from

https://assets.ctfassets.net/f7tuyt85vtoa/2ckiIO9GXymIqu6qi8Oo4s/6a9b62ee553e2af

1e354e042c6055d8a/Amcor_Annual_Report_2017.pdf

Assets.ctfassets.net. (2019). Annual Report 2018. Retrieved 31 December 2019, from

https://assets.ctfassets.net/f7tuyt85vtoa/Ry9ogH9cQemqGA800oiGE/cbcc6bef0d76b7

9be2a227dfc13a7e87/Amcor_Annual_Report_2018.PDF

Auasb.gov.au. (2019). Auditing Standard ASA 320 Materiality in Planning and Performing

an Audit. Retrieved 31 December 2019, from

https://www.auasb.gov.au/admin/file/content102/c3/ASA_320_Compiled_2015.pdf

Brazel, J. F., Jones, K. L., & Prawitt, D. F. (2013). Auditors' reactions to inconsistencies

between financial and nonfinancial measures: The interactive effects of fraud risk

assessment and a decision prompt. Behavioral Research in Accounting, 26(1), 131-

156.

Cpaaustralia.com.au. (2019). A GUIDE TO UNDERSTANDING AUDITING AND

ASSURANCE: AUSTRALIAN LISTED COMPANIES NOVEMBER 2019. Retrieved

31 December 2019, from

11AUDITING AND ETHICS

https://www.cpaaustralia.com.au/~/media/Corporate/AllFiles/Document/professional-

resources/auditing-assurance/guide-understanding-audit-assurance.pdf

Hapsoro, D., & Suryanto, T. (2017). Consequences of going concern opinion for financial

reports of business firms and capital markets with auditor reputation as a moderation

variable: an experimental study. European Research Studies, 20(2), 197.

Herda, D. N., & Lavelle, J. J. (2014). Auditing subsequent events: Perspectives from the

field. Current Issues in Auditing, 8(2), A10-A24.

Jacoby, J., & Levy, H. B. (2016). The materiality mystery. The CPA Journal, 86(7), 14.

Johnstone, K., Gramling, A., & Rittenberg, L. E. (2013). Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Kerr, D. S. (2013). Fraud-risk factors and audit planning: The effects of auditor rank. Journal

of Forensic & Investigative Accounting, 5(2), 48-76.

Kogan, A., Alles, M. G., Vasarhelyi, M. A., & Wu, J. (2014). Design and evaluation of a

continuous data level auditing system. Auditing: A Journal of Practice &

Theory, 33(4), 221-245.

Plumlee, R. D., Rixom, B. A., & Rosman, A. J. (2014). Training auditors to perform

analytical procedures using metacognitive skills. The Accounting Review, 90(1), 351-

369.

Samudera, M. B. (2017). Does Modified Audit Opinion Matter to Investors? Evidence from

Indonesia.

Wigunani, T. L. (2016). HOW DO INDEPENDENT AUDITORS DETECT FRAUDULENT

FINANCIAL STATEMENTS?. Asia Pacific Fraud Journal, 1(2), 301-315.

https://www.cpaaustralia.com.au/~/media/Corporate/AllFiles/Document/professional-

resources/auditing-assurance/guide-understanding-audit-assurance.pdf

Hapsoro, D., & Suryanto, T. (2017). Consequences of going concern opinion for financial

reports of business firms and capital markets with auditor reputation as a moderation

variable: an experimental study. European Research Studies, 20(2), 197.

Herda, D. N., & Lavelle, J. J. (2014). Auditing subsequent events: Perspectives from the

field. Current Issues in Auditing, 8(2), A10-A24.

Jacoby, J., & Levy, H. B. (2016). The materiality mystery. The CPA Journal, 86(7), 14.

Johnstone, K., Gramling, A., & Rittenberg, L. E. (2013). Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Kerr, D. S. (2013). Fraud-risk factors and audit planning: The effects of auditor rank. Journal

of Forensic & Investigative Accounting, 5(2), 48-76.

Kogan, A., Alles, M. G., Vasarhelyi, M. A., & Wu, J. (2014). Design and evaluation of a

continuous data level auditing system. Auditing: A Journal of Practice &

Theory, 33(4), 221-245.

Plumlee, R. D., Rixom, B. A., & Rosman, A. J. (2014). Training auditors to perform

analytical procedures using metacognitive skills. The Accounting Review, 90(1), 351-

369.

Samudera, M. B. (2017). Does Modified Audit Opinion Matter to Investors? Evidence from

Indonesia.

Wigunani, T. L. (2016). HOW DO INDEPENDENT AUDITORS DETECT FRAUDULENT

FINANCIAL STATEMENTS?. Asia Pacific Fraud Journal, 1(2), 301-315.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.