THE AUDITING AND ETHICS

Added on 2022-08-29

14 Pages2834 Words19 Views

Running head: AUDITING AND ETHICS

Auditing and Ethics

Name of the Student

Name of the University

Author’s Note

Auditing and Ethics

Name of the Student

Name of the University

Author’s Note

1AUDITING AND ETHICS

Table of Contents

Introduction......................................................................................................................................2

Section 1..........................................................................................................................................2

Requirement 1.1...........................................................................................................................2

Requirement 1.2...........................................................................................................................4

Section 2..........................................................................................................................................4

Section 3..........................................................................................................................................7

Requirement 3.1...........................................................................................................................7

Requirement 3.2...........................................................................................................................9

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................2

Section 1..........................................................................................................................................2

Requirement 1.1...........................................................................................................................2

Requirement 1.2...........................................................................................................................4

Section 2..........................................................................................................................................4

Section 3..........................................................................................................................................7

Requirement 3.1...........................................................................................................................7

Requirement 3.2...........................................................................................................................9

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

2AUDITING AND ETHICS

Introduction

There are different aspects of auditing and the responsibility of the auditors is to properly

carry out the audit procedures by considering all these aspects. Calculation of the materiality

level is one crucial aspect where the auditors are responsible for determining the appropriate

threshold for recognizing the areas of material misstatements in client’s accounting books. This

is a crucial step as the outcome of the whole audit largely depends on the determination of

materiality level. After this step, the auditors are responsible for carrying out the required

preliminary analytical review of the financial information of the client and analysis of certain

ratios is a major procedure under this. This helps the auditors in identifying the areas of risk in

the client’s financial reports. Moreover, assessment of the cash flows statement of the client is

required by the auditors for assessing the going concern risk of the client. This report is based on

Goodman Group Limited. First section discusses about materiality level determination, second

section shows the preliminary analytical review and the last section analyses the cash flow

statement and audit report of the chosen company.

Section 1

Requirement 1.1

Materiality is a key concept used in auditing which is used by the auditors for

recognizing material misstatements in financial reports. It is mentioned in ASA 32, Paragraph 2

that the auditors consider misstatements in financial reports as material if the decisions of the

users are affected by this. Different factors are required to be considered by the auditors for

determining the level of materiality (auasb.gov.au, 2020).

Introduction

There are different aspects of auditing and the responsibility of the auditors is to properly

carry out the audit procedures by considering all these aspects. Calculation of the materiality

level is one crucial aspect where the auditors are responsible for determining the appropriate

threshold for recognizing the areas of material misstatements in client’s accounting books. This

is a crucial step as the outcome of the whole audit largely depends on the determination of

materiality level. After this step, the auditors are responsible for carrying out the required

preliminary analytical review of the financial information of the client and analysis of certain

ratios is a major procedure under this. This helps the auditors in identifying the areas of risk in

the client’s financial reports. Moreover, assessment of the cash flows statement of the client is

required by the auditors for assessing the going concern risk of the client. This report is based on

Goodman Group Limited. First section discusses about materiality level determination, second

section shows the preliminary analytical review and the last section analyses the cash flow

statement and audit report of the chosen company.

Section 1

Requirement 1.1

Materiality is a key concept used in auditing which is used by the auditors for

recognizing material misstatements in financial reports. It is mentioned in ASA 32, Paragraph 2

that the auditors consider misstatements in financial reports as material if the decisions of the

users are affected by this. Different factors are required to be considered by the auditors for

determining the level of materiality (auasb.gov.au, 2020).

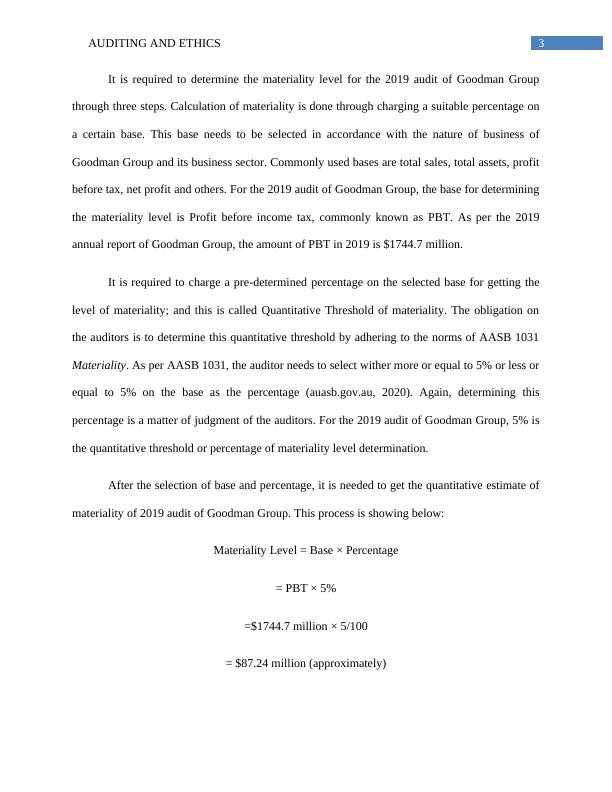

3AUDITING AND ETHICS

It is required to determine the materiality level for the 2019 audit of Goodman Group

through three steps. Calculation of materiality is done through charging a suitable percentage on

a certain base. This base needs to be selected in accordance with the nature of business of

Goodman Group and its business sector. Commonly used bases are total sales, total assets, profit

before tax, net profit and others. For the 2019 audit of Goodman Group, the base for determining

the materiality level is Profit before income tax, commonly known as PBT. As per the 2019

annual report of Goodman Group, the amount of PBT in 2019 is $1744.7 million.

It is required to charge a pre-determined percentage on the selected base for getting the

level of materiality; and this is called Quantitative Threshold of materiality. The obligation on

the auditors is to determine this quantitative threshold by adhering to the norms of AASB 1031

Materiality. As per AASB 1031, the auditor needs to select wither more or equal to 5% or less or

equal to 5% on the base as the percentage (auasb.gov.au, 2020). Again, determining this

percentage is a matter of judgment of the auditors. For the 2019 audit of Goodman Group, 5% is

the quantitative threshold or percentage of materiality level determination.

After the selection of base and percentage, it is needed to get the quantitative estimate of

materiality of 2019 audit of Goodman Group. This process is showing below:

Materiality Level = Base × Percentage

= PBT × 5%

=$1744.7 million × 5/100

= $87.24 million (approximately)

It is required to determine the materiality level for the 2019 audit of Goodman Group

through three steps. Calculation of materiality is done through charging a suitable percentage on

a certain base. This base needs to be selected in accordance with the nature of business of

Goodman Group and its business sector. Commonly used bases are total sales, total assets, profit

before tax, net profit and others. For the 2019 audit of Goodman Group, the base for determining

the materiality level is Profit before income tax, commonly known as PBT. As per the 2019

annual report of Goodman Group, the amount of PBT in 2019 is $1744.7 million.

It is required to charge a pre-determined percentage on the selected base for getting the

level of materiality; and this is called Quantitative Threshold of materiality. The obligation on

the auditors is to determine this quantitative threshold by adhering to the norms of AASB 1031

Materiality. As per AASB 1031, the auditor needs to select wither more or equal to 5% or less or

equal to 5% on the base as the percentage (auasb.gov.au, 2020). Again, determining this

percentage is a matter of judgment of the auditors. For the 2019 audit of Goodman Group, 5% is

the quantitative threshold or percentage of materiality level determination.

After the selection of base and percentage, it is needed to get the quantitative estimate of

materiality of 2019 audit of Goodman Group. This process is showing below:

Materiality Level = Base × Percentage

= PBT × 5%

=$1744.7 million × 5/100

= $87.24 million (approximately)

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Auditing and Ethics | Reportlg...

|12

|2828

|37

Auditing and Ethiclg...

|11

|2932

|84

Auditing and Ethics Assignment Samplelg...

|16

|3106

|44

Auditing and Ethical Practiceslg...

|10

|2096

|54

Auditing and Ethicslg...

|13

|3472

|93

AUDITING AND ETHIC DISCUSSION 2022lg...

|13

|3014

|37