CQUniversity Auditing and Ethics Report: CSL Limited Analysis 2019

VerifiedAdded on 2022/09/05

|15

|2884

|22

Report

AI Summary

This report provides a comprehensive analysis of auditing and ethics principles applied to CSL Limited's financial statements. It begins by examining the concept of materiality, including its calculation and impact on audit risk, using CSL Limited's 2019 financial data. The report then delves into significant audit areas like contingencies and provisions, outlining the audit procedures required. A preliminary analytical review is conducted, calculating and interpreting key ratios such as liquidity, leverage, and profitability ratios. The report further analyzes CSL Limited's statement of cash flow and concludes with a review of the auditor's report, highlighting the unmodified opinion and any potential going concern issues. The analysis incorporates relevant Australian Auditing Standards (ASA) and accounting principles to provide a detailed understanding of the audit process.

Running head: AUDITING AND ETHICS

Auditing and ethics

Name of the student

Name of the university

Student ID

Author note

Auditing and ethics

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHICS

Table of Contents

Introduction......................................................................................................................................2

Section 1..........................................................................................................................................2

Materiality level...........................................................................................................................2

Significant amount for audit........................................................................................................4

Section 2..........................................................................................................................................6

Preliminary analytical review......................................................................................................6

Key ratio computation of CS Limited.........................................................................................7

Section 3........................................................................................................................................10

Statement of cash flow...............................................................................................................10

Audit report................................................................................................................................10

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................2

Section 1..........................................................................................................................................2

Materiality level...........................................................................................................................2

Significant amount for audit........................................................................................................4

Section 2..........................................................................................................................................6

Preliminary analytical review......................................................................................................6

Key ratio computation of CS Limited.........................................................................................7

Section 3........................................................................................................................................10

Statement of cash flow...............................................................................................................10

Audit report................................................................................................................................10

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

2AUDITING AND ETHICS

Introduction

In accordance with ASA 320 materiality is the misstatements that includes omissions and

are accounted for as material if the same in association with other or individually are likely to

have its influence on the economic decision taken by the users based on the annual report.

Judgments regarding the concept materiality are made depended on the contiguous

circumstances and are impacted by the nature or the size of misstatements or by both size as well

as nature (Eilifsen & Messier Jr, 2014). Major purpose of the task is to focus on the materiality

concept and analysing the financial report of ASX listed entity CSL Limited to estimate the

amount of materiality. Further the task will prepare the preliminary analytical review in

association with the information provided by the entity. In addition the report will go through the

cash flow statement and auditors report of CSL Limited for extracting various information.

Section 1

Materiality level

In accordance with AUS 202 objectives as well as general principles that administrates

the financial report audit is to allow the auditor in expressing the opinion in context of whether

the annual statement has been prepared in conformity with the framework of financial reporting

in all the material aspects. Relationship among materiality and audit risk indicates that with

higher level of risk level of materiality becomes lower. Thus, the auditor shall take into

consideration the association among audit risk and materiality while determining the nature,

timing and extent of audit procedure (Louwers et al., 2015).

Introduction

In accordance with ASA 320 materiality is the misstatements that includes omissions and

are accounted for as material if the same in association with other or individually are likely to

have its influence on the economic decision taken by the users based on the annual report.

Judgments regarding the concept materiality are made depended on the contiguous

circumstances and are impacted by the nature or the size of misstatements or by both size as well

as nature (Eilifsen & Messier Jr, 2014). Major purpose of the task is to focus on the materiality

concept and analysing the financial report of ASX listed entity CSL Limited to estimate the

amount of materiality. Further the task will prepare the preliminary analytical review in

association with the information provided by the entity. In addition the report will go through the

cash flow statement and auditors report of CSL Limited for extracting various information.

Section 1

Materiality level

In accordance with AUS 202 objectives as well as general principles that administrates

the financial report audit is to allow the auditor in expressing the opinion in context of whether

the annual statement has been prepared in conformity with the framework of financial reporting

in all the material aspects. Relationship among materiality and audit risk indicates that with

higher level of risk level of materiality becomes lower. Thus, the auditor shall take into

consideration the association among audit risk and materiality while determining the nature,

timing and extent of audit procedure (Louwers et al., 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHICS

Planning materiality is setting of the amount for misstatement by auditors at the stage of

planning dependent on the materiality in the annual statement. It is used by the auditor for

evaluating the impact of misstatement in aggregate or individually in context of the financial

statement. Once the materiality in annual statement is acknowledged as well as assessed by the

auditor, the auditor establishes the performance materiality that is the tolerable misstatement.

However, while establishing the level of materiality the auditor considers various factors

including the level of reliance that can be placed on the information provided by the management

and other factors if any that may signify any deviation from normal activities of the entity

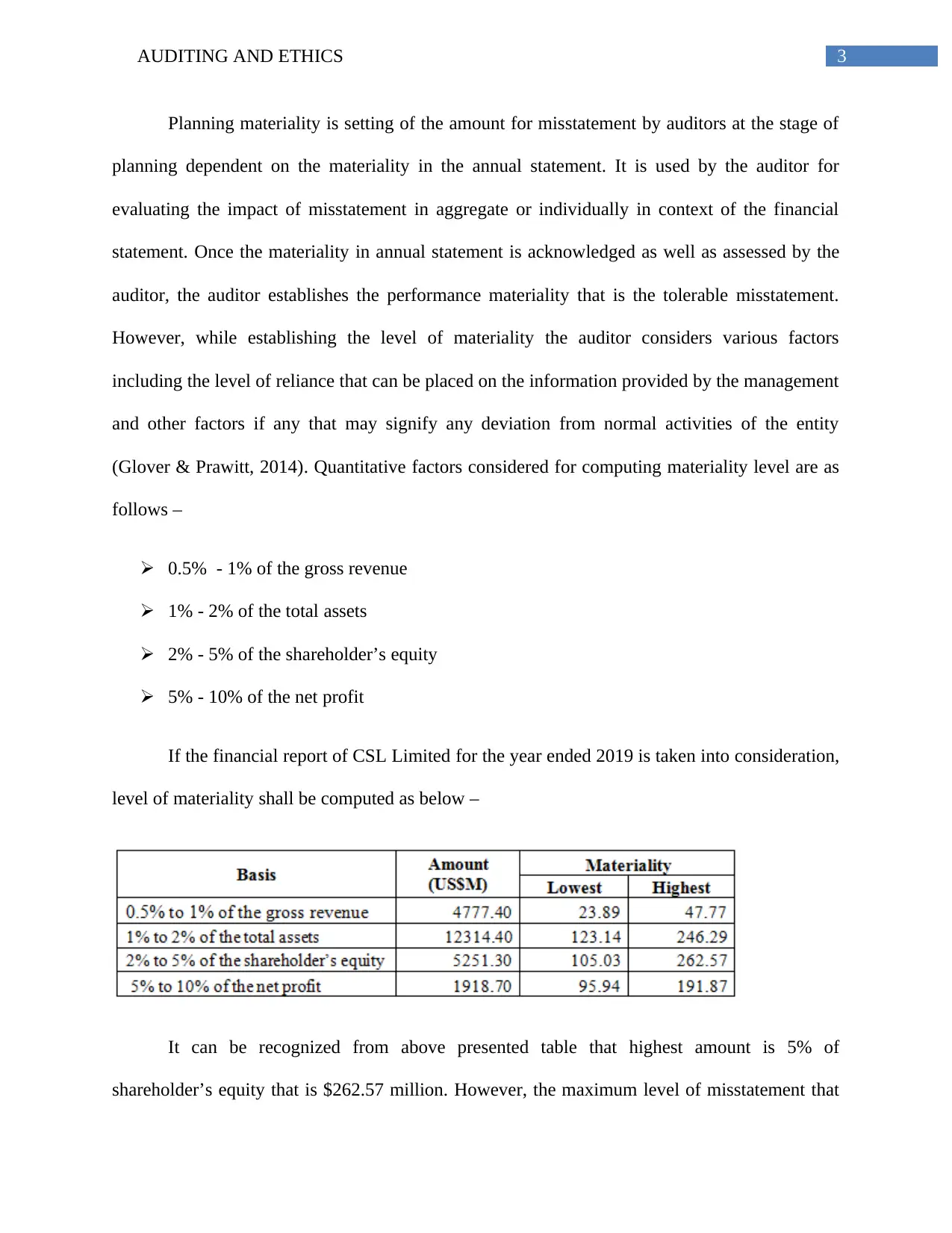

(Glover & Prawitt, 2014). Quantitative factors considered for computing materiality level are as

follows –

0.5% - 1% of the gross revenue

1% - 2% of the total assets

2% - 5% of the shareholder’s equity

5% - 10% of the net profit

If the financial report of CSL Limited for the year ended 2019 is taken into consideration,

level of materiality shall be computed as below –

It can be recognized from above presented table that highest amount is 5% of

shareholder’s equity that is $262.57 million. However, the maximum level of misstatement that

Planning materiality is setting of the amount for misstatement by auditors at the stage of

planning dependent on the materiality in the annual statement. It is used by the auditor for

evaluating the impact of misstatement in aggregate or individually in context of the financial

statement. Once the materiality in annual statement is acknowledged as well as assessed by the

auditor, the auditor establishes the performance materiality that is the tolerable misstatement.

However, while establishing the level of materiality the auditor considers various factors

including the level of reliance that can be placed on the information provided by the management

and other factors if any that may signify any deviation from normal activities of the entity

(Glover & Prawitt, 2014). Quantitative factors considered for computing materiality level are as

follows –

0.5% - 1% of the gross revenue

1% - 2% of the total assets

2% - 5% of the shareholder’s equity

5% - 10% of the net profit

If the financial report of CSL Limited for the year ended 2019 is taken into consideration,

level of materiality shall be computed as below –

It can be recognized from above presented table that highest amount is 5% of

shareholder’s equity that is $262.57 million. However, the maximum level of misstatement that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHICS

can be tolerated is assumed to be 50% to 75% of highest amount for material misstatement. Thus

the tolerable amount for material misstatement will be $262.57 * 75% = $196.92 million. It can

be identified that the computed amount for tolerable misstatement is quite high and hence the

level of audit risk is expected to be lower in context of the financial report for the year ended

2018. The auditor of CSL Limited for the period under concern has stated that the entity’s

financial report is offering true and fair view in context of its financial performance as well as

financial position (Arens et al., 2016)

Significant amount for audit

Looking into the financial report of CSL Limited for the year 2018 below mentioned

items are considered to be noteworthy for the purpose of audit –

Contingencies –the entity is involved in the litigation in ordinary business course that includes

litigation on account of breach of contract claims. In some of the cases, the entity recognized

legal provision that is expected to be utilized in case any settlement is required. In addition, the

entity is subject to few patent infringements action those are brought in by the competitors. The

entity is highly confident in context of intellectual property status those are the product for more

than the decade as a result of innovative research by the entity (Byrnes et al., 2015). However,

the entity is defending the claims vigorously. Procedure of audit for the contingencies will be as

follows –

Analysing the event’s probability – auditor is required to project the likelihood of taking

place of the event. This likelihood can be of different level such as probable, remote or

reasonably probable. In addition the auditor is required to enquire that whether the entity

can be tolerated is assumed to be 50% to 75% of highest amount for material misstatement. Thus

the tolerable amount for material misstatement will be $262.57 * 75% = $196.92 million. It can

be identified that the computed amount for tolerable misstatement is quite high and hence the

level of audit risk is expected to be lower in context of the financial report for the year ended

2018. The auditor of CSL Limited for the period under concern has stated that the entity’s

financial report is offering true and fair view in context of its financial performance as well as

financial position (Arens et al., 2016)

Significant amount for audit

Looking into the financial report of CSL Limited for the year 2018 below mentioned

items are considered to be noteworthy for the purpose of audit –

Contingencies –the entity is involved in the litigation in ordinary business course that includes

litigation on account of breach of contract claims. In some of the cases, the entity recognized

legal provision that is expected to be utilized in case any settlement is required. In addition, the

entity is subject to few patent infringements action those are brought in by the competitors. The

entity is highly confident in context of intellectual property status those are the product for more

than the decade as a result of innovative research by the entity (Byrnes et al., 2015). However,

the entity is defending the claims vigorously. Procedure of audit for the contingencies will be as

follows –

Analysing the event’s probability – auditor is required to project the likelihood of taking

place of the event. This likelihood can be of different level such as probable, remote or

reasonably probable. In addition the auditor is required to enquire that whether the entity

5AUDITING AND ETHICS

has provided required disclosures or footnotes in context of the possible or reasonably

possible contingent liabilities (Ruhnke, Pronobis & Michel, 2014).

Considering likely events – the auditors are required to look into contingent liabilities

under probable or likely segment as the same shall be accounted with special treatment.

In case it is found that the contingent liability is likely, amount for which is not able to

be forecasted, same liability is required to be only disclosed through notes. However, in

case the likelihood of liabilities is certain and the value for the same can be forecasted, it

requires particular journal entry to be passed. Under such circumstances, the auditor

shall ensure that the entity passed both debit as well as credit entry for the likely as well

as measurable amount of contingent liability, if any (Coetzee & Lubbe, 2014).

Provisions – CSL Limited reports provisions while all the below mentioned criteria fulfilled –

It is likely that the entity is required make payment through outflow of the economic

resources for resolve obligation

It has constructive or current obligation on account of past event or past transaction

Amount of the obligation can be forecasted reliably

Provision that is reported by the entity is the best forecast by the management for the

expenses required for resolving the obligation. It is determined through discounting likely future

cash flow required for resolving the obligation at pre-tax discount rate (Wali, 2015). Producer for

the provisions those shall be followed by the auditor must include –

Auditor must assure that all the provisions are passed through charging the same in

profit and loss account.

The auditor shall ensure that amount reserved as provision is sufficient

has provided required disclosures or footnotes in context of the possible or reasonably

possible contingent liabilities (Ruhnke, Pronobis & Michel, 2014).

Considering likely events – the auditors are required to look into contingent liabilities

under probable or likely segment as the same shall be accounted with special treatment.

In case it is found that the contingent liability is likely, amount for which is not able to

be forecasted, same liability is required to be only disclosed through notes. However, in

case the likelihood of liabilities is certain and the value for the same can be forecasted, it

requires particular journal entry to be passed. Under such circumstances, the auditor

shall ensure that the entity passed both debit as well as credit entry for the likely as well

as measurable amount of contingent liability, if any (Coetzee & Lubbe, 2014).

Provisions – CSL Limited reports provisions while all the below mentioned criteria fulfilled –

It is likely that the entity is required make payment through outflow of the economic

resources for resolve obligation

It has constructive or current obligation on account of past event or past transaction

Amount of the obligation can be forecasted reliably

Provision that is reported by the entity is the best forecast by the management for the

expenses required for resolving the obligation. It is determined through discounting likely future

cash flow required for resolving the obligation at pre-tax discount rate (Wali, 2015). Producer for

the provisions those shall be followed by the auditor must include –

Auditor must assure that all the provisions are passed through charging the same in

profit and loss account.

The auditor shall ensure that amount reserved as provision is sufficient

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHICS

Auditor shall further verify that the amount used only for the purpose for which they

were originally created.

The auditor shall also verify that the disclosure for all the provisions have been provided

by the entity in the financial report.

Section 2

Preliminary analytical review

It involves analytical procedure as well as inquiry procedure of management those are

applied under the audit planning stage. Auditors shall carry out the procedure for risk assessment

that includes observation as well as inspection procedure those are primarily focussed on gaining

understanding of the organisation’s internal control in addition to significant agreements or

contracts fundamentals to the entity (Jans, Alles & Vasarhelyi, 2014).

Auditor shall further verify that the amount used only for the purpose for which they

were originally created.

The auditor shall also verify that the disclosure for all the provisions have been provided

by the entity in the financial report.

Section 2

Preliminary analytical review

It involves analytical procedure as well as inquiry procedure of management those are

applied under the audit planning stage. Auditors shall carry out the procedure for risk assessment

that includes observation as well as inspection procedure those are primarily focussed on gaining

understanding of the organisation’s internal control in addition to significant agreements or

contracts fundamentals to the entity (Jans, Alles & Vasarhelyi, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHICS

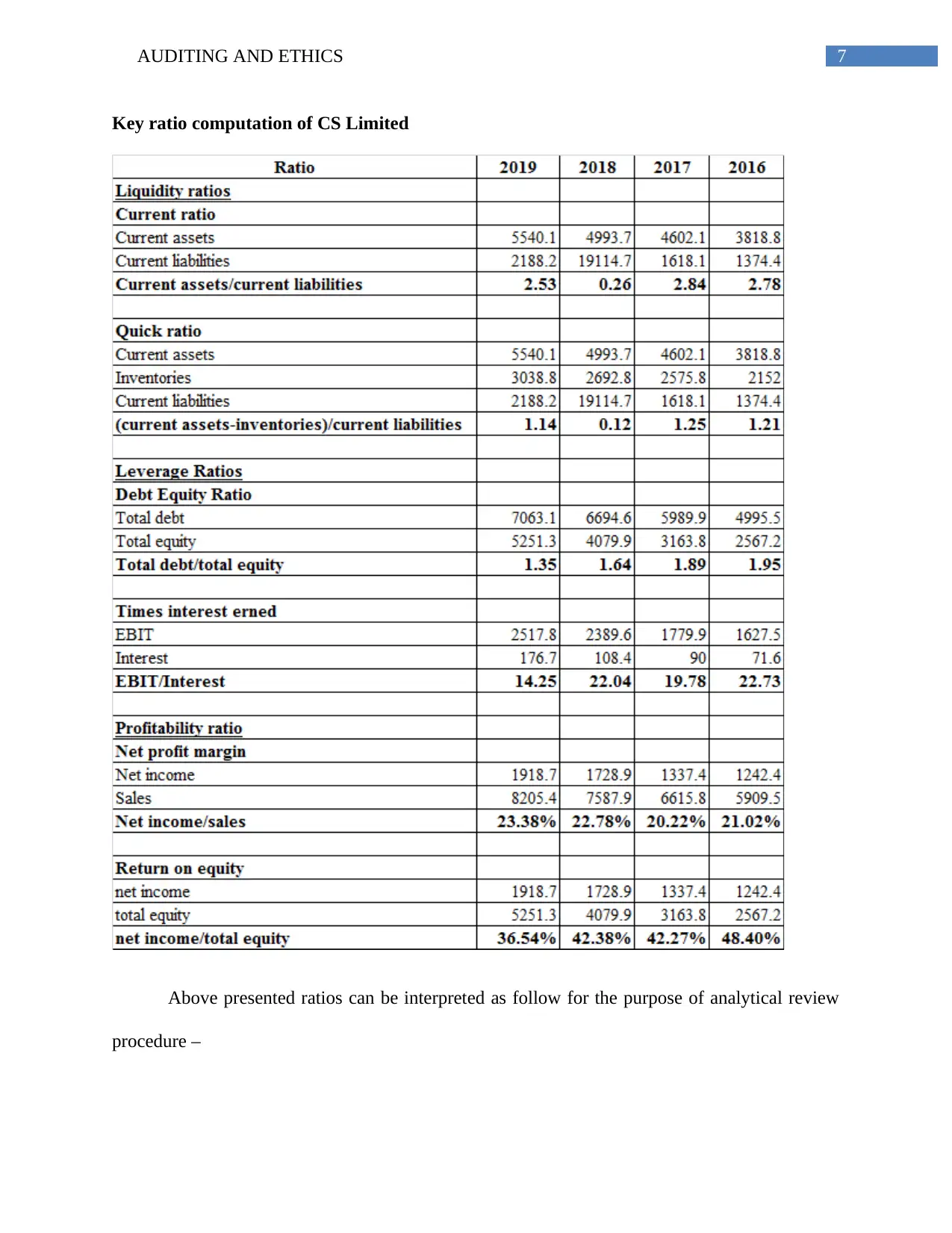

Key ratio computation of CS Limited

Above presented ratios can be interpreted as follow for the purpose of analytical review

procedure –

Key ratio computation of CS Limited

Above presented ratios can be interpreted as follow for the purpose of analytical review

procedure –

8AUDITING AND ETHICS

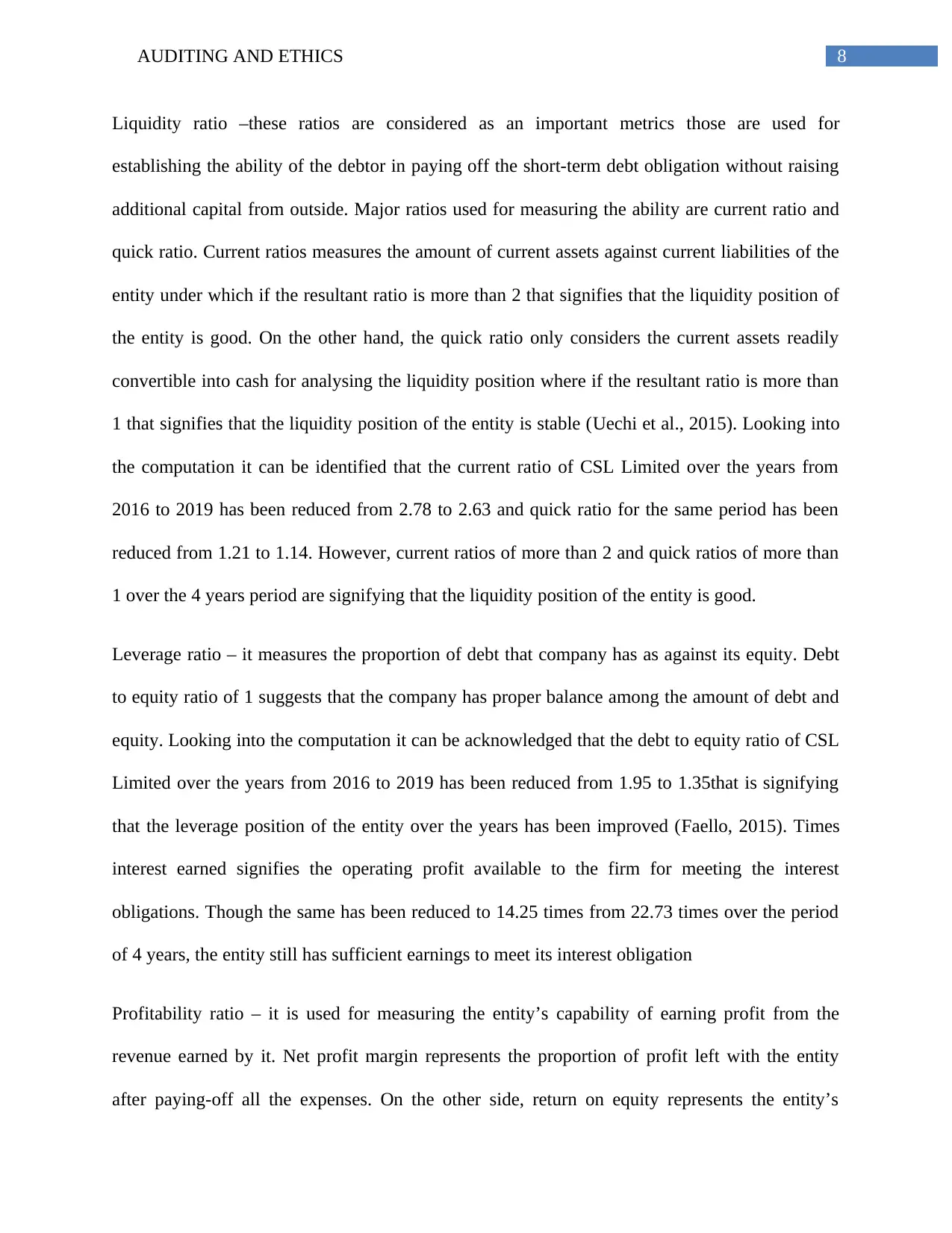

Liquidity ratio –these ratios are considered as an important metrics those are used for

establishing the ability of the debtor in paying off the short-term debt obligation without raising

additional capital from outside. Major ratios used for measuring the ability are current ratio and

quick ratio. Current ratios measures the amount of current assets against current liabilities of the

entity under which if the resultant ratio is more than 2 that signifies that the liquidity position of

the entity is good. On the other hand, the quick ratio only considers the current assets readily

convertible into cash for analysing the liquidity position where if the resultant ratio is more than

1 that signifies that the liquidity position of the entity is stable (Uechi et al., 2015). Looking into

the computation it can be identified that the current ratio of CSL Limited over the years from

2016 to 2019 has been reduced from 2.78 to 2.63 and quick ratio for the same period has been

reduced from 1.21 to 1.14. However, current ratios of more than 2 and quick ratios of more than

1 over the 4 years period are signifying that the liquidity position of the entity is good.

Leverage ratio – it measures the proportion of debt that company has as against its equity. Debt

to equity ratio of 1 suggests that the company has proper balance among the amount of debt and

equity. Looking into the computation it can be acknowledged that the debt to equity ratio of CSL

Limited over the years from 2016 to 2019 has been reduced from 1.95 to 1.35that is signifying

that the leverage position of the entity over the years has been improved (Faello, 2015). Times

interest earned signifies the operating profit available to the firm for meeting the interest

obligations. Though the same has been reduced to 14.25 times from 22.73 times over the period

of 4 years, the entity still has sufficient earnings to meet its interest obligation

Profitability ratio – it is used for measuring the entity’s capability of earning profit from the

revenue earned by it. Net profit margin represents the proportion of profit left with the entity

after paying-off all the expenses. On the other side, return on equity represents the entity’s

Liquidity ratio –these ratios are considered as an important metrics those are used for

establishing the ability of the debtor in paying off the short-term debt obligation without raising

additional capital from outside. Major ratios used for measuring the ability are current ratio and

quick ratio. Current ratios measures the amount of current assets against current liabilities of the

entity under which if the resultant ratio is more than 2 that signifies that the liquidity position of

the entity is good. On the other hand, the quick ratio only considers the current assets readily

convertible into cash for analysing the liquidity position where if the resultant ratio is more than

1 that signifies that the liquidity position of the entity is stable (Uechi et al., 2015). Looking into

the computation it can be identified that the current ratio of CSL Limited over the years from

2016 to 2019 has been reduced from 2.78 to 2.63 and quick ratio for the same period has been

reduced from 1.21 to 1.14. However, current ratios of more than 2 and quick ratios of more than

1 over the 4 years period are signifying that the liquidity position of the entity is good.

Leverage ratio – it measures the proportion of debt that company has as against its equity. Debt

to equity ratio of 1 suggests that the company has proper balance among the amount of debt and

equity. Looking into the computation it can be acknowledged that the debt to equity ratio of CSL

Limited over the years from 2016 to 2019 has been reduced from 1.95 to 1.35that is signifying

that the leverage position of the entity over the years has been improved (Faello, 2015). Times

interest earned signifies the operating profit available to the firm for meeting the interest

obligations. Though the same has been reduced to 14.25 times from 22.73 times over the period

of 4 years, the entity still has sufficient earnings to meet its interest obligation

Profitability ratio – it is used for measuring the entity’s capability of earning profit from the

revenue earned by it. Net profit margin represents the proportion of profit left with the entity

after paying-off all the expenses. On the other side, return on equity represents the entity’s

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHICS

capability to create earnings from shareholder’s investment (Dokas, Giokas & Tsamis, 2014).

Looking into the computation it can be identified that the current ratio of CSL Limited over the

years from 2016 to 2019 has went up from 21.02% to 23.38% and ROE for the same period has

been reduced from 48.40% to 36.54%.

Looking into the entity’s entire financial performance for the period covering last 4 years

areas which shall be analytically reviewed are –

Cash – this item is considered as material on account of its most liquid nature. Major

assertion associated with cash are – (i) existence that is all the cash balance reported are

actually exist on balance sheet date (ii) completeness that is all the transaction associated

with cash have been reported in the books. While auditing, cash balance shall be

reconciled with bank records and all the ash related records shall be verified with

associated documents (Kharisova & Kozlova, 2014).

Interest bearing liabilities – it has been found that this item involved largest amount under

long term liabilities. Major assertion associated with interest bearing liabilities are – (i)

cut-off that is liabilities related to the current period only has been reported (ii) existence

that is all the interest bearing liabilities reported are actually exist on balance sheet date.

While auditing, the auditor shall verify all the documents related to the same along with

the amount, interest rate, lender’s name and repayment schedule (Leung et al., 2014).

Section 3

Statement of cash flow

Operating activities provided the majority of cash inflows amounting to $1644.4 million

and investing activities had greatest cash outflows amounting to $1287.3 million

capability to create earnings from shareholder’s investment (Dokas, Giokas & Tsamis, 2014).

Looking into the computation it can be identified that the current ratio of CSL Limited over the

years from 2016 to 2019 has went up from 21.02% to 23.38% and ROE for the same period has

been reduced from 48.40% to 36.54%.

Looking into the entity’s entire financial performance for the period covering last 4 years

areas which shall be analytically reviewed are –

Cash – this item is considered as material on account of its most liquid nature. Major

assertion associated with cash are – (i) existence that is all the cash balance reported are

actually exist on balance sheet date (ii) completeness that is all the transaction associated

with cash have been reported in the books. While auditing, cash balance shall be

reconciled with bank records and all the ash related records shall be verified with

associated documents (Kharisova & Kozlova, 2014).

Interest bearing liabilities – it has been found that this item involved largest amount under

long term liabilities. Major assertion associated with interest bearing liabilities are – (i)

cut-off that is liabilities related to the current period only has been reported (ii) existence

that is all the interest bearing liabilities reported are actually exist on balance sheet date.

While auditing, the auditor shall verify all the documents related to the same along with

the amount, interest rate, lender’s name and repayment schedule (Leung et al., 2014).

Section 3

Statement of cash flow

Operating activities provided the majority of cash inflows amounting to $1644.4 million

and investing activities had greatest cash outflows amounting to $1287.3 million

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHICS

Primary cash receipts were receipts from customers amounting to 8603.2 million and

primary cash payments were towards suppliers and employees amounting to $6304.5

million (Annual Reports, 2020).

Major non-cash financial and investing activity was variations in the exchange rate on

account of foreign cash as well as cash equivalents

Cash from operating activities reduced from $1902.1 million to $1644.4 million over

2018 to 2019. Further the closing cash balance over the same period reduced from $812.7

million to $657.8 million. These indicate going concern issue for the entity. Hence, the

auditor must verify the receipts of this year against preceding year and verify the reason

of difference (CSL Limited, 2020).

Audit report

Auditors Ernst & Young expressed unmodified opinion. However, the following matters

have been recognised as key audit matter –

Valuation and existence of inventories

Complexities of tax (Annual Reports, 2020).

Conclusion

It is determined from above discussion that materiality shall be determined by the auditor

while the nature, timing and extent of audit is determined by them along with the audit procedure

and evaluating effect of the misstatement. Looking into financial overview of CSL Limited it is

observed that cash and interest bearing liabilities shall be reviewed analytically. Further, the cash

flow statement is signifying that there is going concern issue in the entity that shall be taken into

consideration while carrying out the audit.

Primary cash receipts were receipts from customers amounting to 8603.2 million and

primary cash payments were towards suppliers and employees amounting to $6304.5

million (Annual Reports, 2020).

Major non-cash financial and investing activity was variations in the exchange rate on

account of foreign cash as well as cash equivalents

Cash from operating activities reduced from $1902.1 million to $1644.4 million over

2018 to 2019. Further the closing cash balance over the same period reduced from $812.7

million to $657.8 million. These indicate going concern issue for the entity. Hence, the

auditor must verify the receipts of this year against preceding year and verify the reason

of difference (CSL Limited, 2020).

Audit report

Auditors Ernst & Young expressed unmodified opinion. However, the following matters

have been recognised as key audit matter –

Valuation and existence of inventories

Complexities of tax (Annual Reports, 2020).

Conclusion

It is determined from above discussion that materiality shall be determined by the auditor

while the nature, timing and extent of audit is determined by them along with the audit procedure

and evaluating effect of the misstatement. Looking into financial overview of CSL Limited it is

observed that cash and interest bearing liabilities shall be reviewed analytically. Further, the cash

flow statement is signifying that there is going concern issue in the entity that shall be taken into

consideration while carrying out the audit.

11AUDITING AND ETHICS

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.