ACC3001 Auditing: Risk Assessment in Audit Planning for Southern Cross

VerifiedAdded on 2023/04/03

|14

|2518

|148

Report

AI Summary

This report provides an assessment of audit risks in the planning phase of an audit engagement, focusing on Southern Cross Media Group Limited, an ASX-listed media company. It identifies key risk factors such as impairment of intangibles and investments, financial market risks (interest rate, liquidity, and cash flow), and employee share entitlements. The report analyzes the company's financial performance, including declining revenue and EBITDA, and questions the board's decision to maintain dividends. It also emphasizes the importance of technology and cybersecurity risks, highlighting material risks disclosed by the company and the need for auditors to understand the business complexities and internal policies. The report concludes by stressing the importance of reviewing financial reports to identify potential risk areas and plan audit procedures accordingly. Desklib offers a variety of solved assignments and past papers for students.

AUDITING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

Executive Summary

The report aims at assessing and evaluating the risk factors in the process of planning the

audit engagement from the viewpoint of the auditor. For this analysis, we have selected a

company listed in the ASX namely Southern Cross Media Group Limited. The company is a

pioneer in media companies in Australia which deals in free-to-air commercial radio,

television and online services all over Australia. The company has various broadcast channels

and media platforms including online and mobile platforms and thus operates in a very

competitive environment.

2

Executive Summary

The report aims at assessing and evaluating the risk factors in the process of planning the

audit engagement from the viewpoint of the auditor. For this analysis, we have selected a

company listed in the ASX namely Southern Cross Media Group Limited. The company is a

pioneer in media companies in Australia which deals in free-to-air commercial radio,

television and online services all over Australia. The company has various broadcast channels

and media platforms including online and mobile platforms and thus operates in a very

competitive environment.

2

Audit

Contents

Introduction...........................................................................................................................................2

Audit Planning.......................................................................................................................................2

Impairment of Intangibles and Investments-.................................................................................2

Financial Market Risks...................................................................................................................3

Employee share entitlements........................................................................................................4

Key Parameters.....................................................................................................................................5

Technology & its use:.....................................................................................................................6

Material risks.................................................................................................................................7

Financial factors:...................................................................................................................................8

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

3

Contents

Introduction...........................................................................................................................................2

Audit Planning.......................................................................................................................................2

Impairment of Intangibles and Investments-.................................................................................2

Financial Market Risks...................................................................................................................3

Employee share entitlements........................................................................................................4

Key Parameters.....................................................................................................................................5

Technology & its use:.....................................................................................................................6

Material risks.................................................................................................................................7

Financial factors:...................................................................................................................................8

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

Introduction

In planning an Audit procedure, every auditor is at risk that the financial statements on which

he is providing his opinion might be materially misstated or have omitted financial

statements. This risk is called audit risk. There are various factors that contribute to audit risk.

One of such factors is business risk despite the difference in nature of both the risks, as

business risk is related to the company and its stakeholders, unlike audit risk. But the

detection of audit risks can be done by detecting the inherent business risks also (Livne,

2015). We shall analyze the Annual Report of the company Southern Cross Media Group

Limited for the year ended 30th June 2018 for assessing the audit risks at the planning stage.

The Audit risk is composed of Inherent risks, control risks, and detection risks. Inherent risk

is the risk that is created by an error or omission due to reasons other than the control failure.

When the transactions are complex, the case of inherent risk is likely to occur. On the other

hand, the control risk can be defined as the probability that material misstatement will happen

in the financial statements due to the system control failure utilized by the business.

The detection risk can be defined as the possibility that the auditor will fail to trace the

material misstatement that is present in the financial statement. For detection of such risk it

is important that the auditor should make use of the audit procedures.

The Audit planning can be performed in the following manner:

Performance of the initial audit planning

Understanding the business of Southern group and the industry in which it performs

Assessment of the risk of business

Understanding the internal control together with the control risk

Gathering information to evaluate fraud

The detailed audit planning is defined in the further part of the report and deals

exclusively for Southern Cross Media Group Limited

Audit planning

As studied from the Annual Report of Southern Cross Media Group Limited for the year

ended 30th June 2018, following are some of the risk factors that an auditor needs to consider

while planning the audit engagement:

4

Introduction

In planning an Audit procedure, every auditor is at risk that the financial statements on which

he is providing his opinion might be materially misstated or have omitted financial

statements. This risk is called audit risk. There are various factors that contribute to audit risk.

One of such factors is business risk despite the difference in nature of both the risks, as

business risk is related to the company and its stakeholders, unlike audit risk. But the

detection of audit risks can be done by detecting the inherent business risks also (Livne,

2015). We shall analyze the Annual Report of the company Southern Cross Media Group

Limited for the year ended 30th June 2018 for assessing the audit risks at the planning stage.

The Audit risk is composed of Inherent risks, control risks, and detection risks. Inherent risk

is the risk that is created by an error or omission due to reasons other than the control failure.

When the transactions are complex, the case of inherent risk is likely to occur. On the other

hand, the control risk can be defined as the probability that material misstatement will happen

in the financial statements due to the system control failure utilized by the business.

The detection risk can be defined as the possibility that the auditor will fail to trace the

material misstatement that is present in the financial statement. For detection of such risk it

is important that the auditor should make use of the audit procedures.

The Audit planning can be performed in the following manner:

Performance of the initial audit planning

Understanding the business of Southern group and the industry in which it performs

Assessment of the risk of business

Understanding the internal control together with the control risk

Gathering information to evaluate fraud

The detailed audit planning is defined in the further part of the report and deals

exclusively for Southern Cross Media Group Limited

Audit planning

As studied from the Annual Report of Southern Cross Media Group Limited for the year

ended 30th June 2018, following are some of the risk factors that an auditor needs to consider

while planning the audit engagement:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

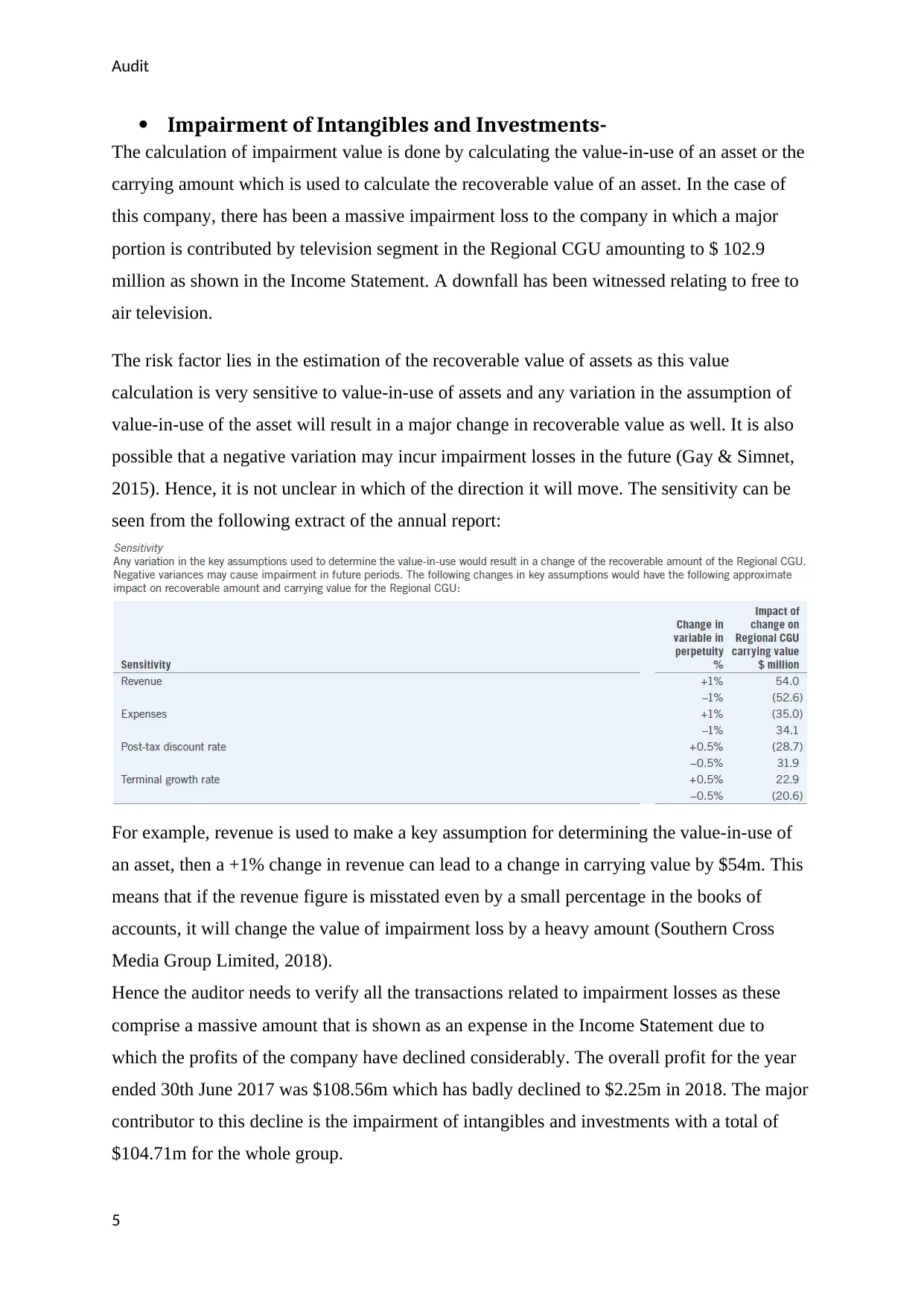

Impairment of Intangibles and Investments-

The calculation of impairment value is done by calculating the value-in-use of an asset or the

carrying amount which is used to calculate the recoverable value of an asset. In the case of

this company, there has been a massive impairment loss to the company in which a major

portion is contributed by television segment in the Regional CGU amounting to $ 102.9

million as shown in the Income Statement. A downfall has been witnessed relating to free to

air television.

The risk factor lies in the estimation of the recoverable value of assets as this value

calculation is very sensitive to value-in-use of assets and any variation in the assumption of

value-in-use of the asset will result in a major change in recoverable value as well. It is also

possible that a negative variation may incur impairment losses in the future (Gay & Simnet,

2015). Hence, it is not unclear in which of the direction it will move. The sensitivity can be

seen from the following extract of the annual report:

For example, revenue is used to make a key assumption for determining the value-in-use of

an asset, then a +1% change in revenue can lead to a change in carrying value by $54m. This

means that if the revenue figure is misstated even by a small percentage in the books of

accounts, it will change the value of impairment loss by a heavy amount (Southern Cross

Media Group Limited, 2018).

Hence the auditor needs to verify all the transactions related to impairment losses as these

comprise a massive amount that is shown as an expense in the Income Statement due to

which the profits of the company have declined considerably. The overall profit for the year

ended 30th June 2017 was $108.56m which has badly declined to $2.25m in 2018. The major

contributor to this decline is the impairment of intangibles and investments with a total of

$104.71m for the whole group.

5

Impairment of Intangibles and Investments-

The calculation of impairment value is done by calculating the value-in-use of an asset or the

carrying amount which is used to calculate the recoverable value of an asset. In the case of

this company, there has been a massive impairment loss to the company in which a major

portion is contributed by television segment in the Regional CGU amounting to $ 102.9

million as shown in the Income Statement. A downfall has been witnessed relating to free to

air television.

The risk factor lies in the estimation of the recoverable value of assets as this value

calculation is very sensitive to value-in-use of assets and any variation in the assumption of

value-in-use of the asset will result in a major change in recoverable value as well. It is also

possible that a negative variation may incur impairment losses in the future (Gay & Simnet,

2015). Hence, it is not unclear in which of the direction it will move. The sensitivity can be

seen from the following extract of the annual report:

For example, revenue is used to make a key assumption for determining the value-in-use of

an asset, then a +1% change in revenue can lead to a change in carrying value by $54m. This

means that if the revenue figure is misstated even by a small percentage in the books of

accounts, it will change the value of impairment loss by a heavy amount (Southern Cross

Media Group Limited, 2018).

Hence the auditor needs to verify all the transactions related to impairment losses as these

comprise a massive amount that is shown as an expense in the Income Statement due to

which the profits of the company have declined considerably. The overall profit for the year

ended 30th June 2017 was $108.56m which has badly declined to $2.25m in 2018. The major

contributor to this decline is the impairment of intangibles and investments with a total of

$104.71m for the whole group.

5

Audit

Financial Market Risks

There are three kinds of risk that the company is prone to- interest rate risk, liquidity risk &

cash flow interest rate risk. The most important risk that the company seeks to minimize

throughout the year is the interest rate risk as it has major influence on the company’s

financial performance (Roach, 2010).

An interest rate risk projects that risk that the company may not be able to fulfill its interest

rate commitments if the market interest rates move in an adverse way (Baldwin, 2010). The

company takes borrowings of long term at variable interest rates and hence exposes itself to a

interest rate risk that is linked to cash flow as well. When the interest rates are variable there

is a strong exposure to risk because the market situation is always filled with fluctuations that

might hamper the scenario (Melville, 2013).

The main risk factor to be kept in mind here is that the company does not have any fixed

formal policy for fixing its borrowing interest rates. It manages the interest rate risk by

utilizing the variable to fixed rate of interest swaps through which the interest rate on

borrowing can be converted from variable rates to fixed rates (Niemi & Sundgren, 2012). The

borrowing is done by the group at rates of variable nature and then swaps the same into fixed

rates. The company makes contracts with other parties so that difference can be exchanged

between the fixed and variable interest amounts on the basis of principal amounts that is

notional. For instance the group took an interest rate swap of $100 million through which it

can receive variable interest rate but the group will be subjected to pay average fixed rate of

2.25% with effect from January 2018. Now here the variable rates may be lower than payable

(Southern Cross Media Group Limited, 2018)

Fixed rates or it may be higher than this rate.

Hence the auditor needs to consider these factors while auditing the derivative financial

instruments related matters where there is interest rate risk prevalent.

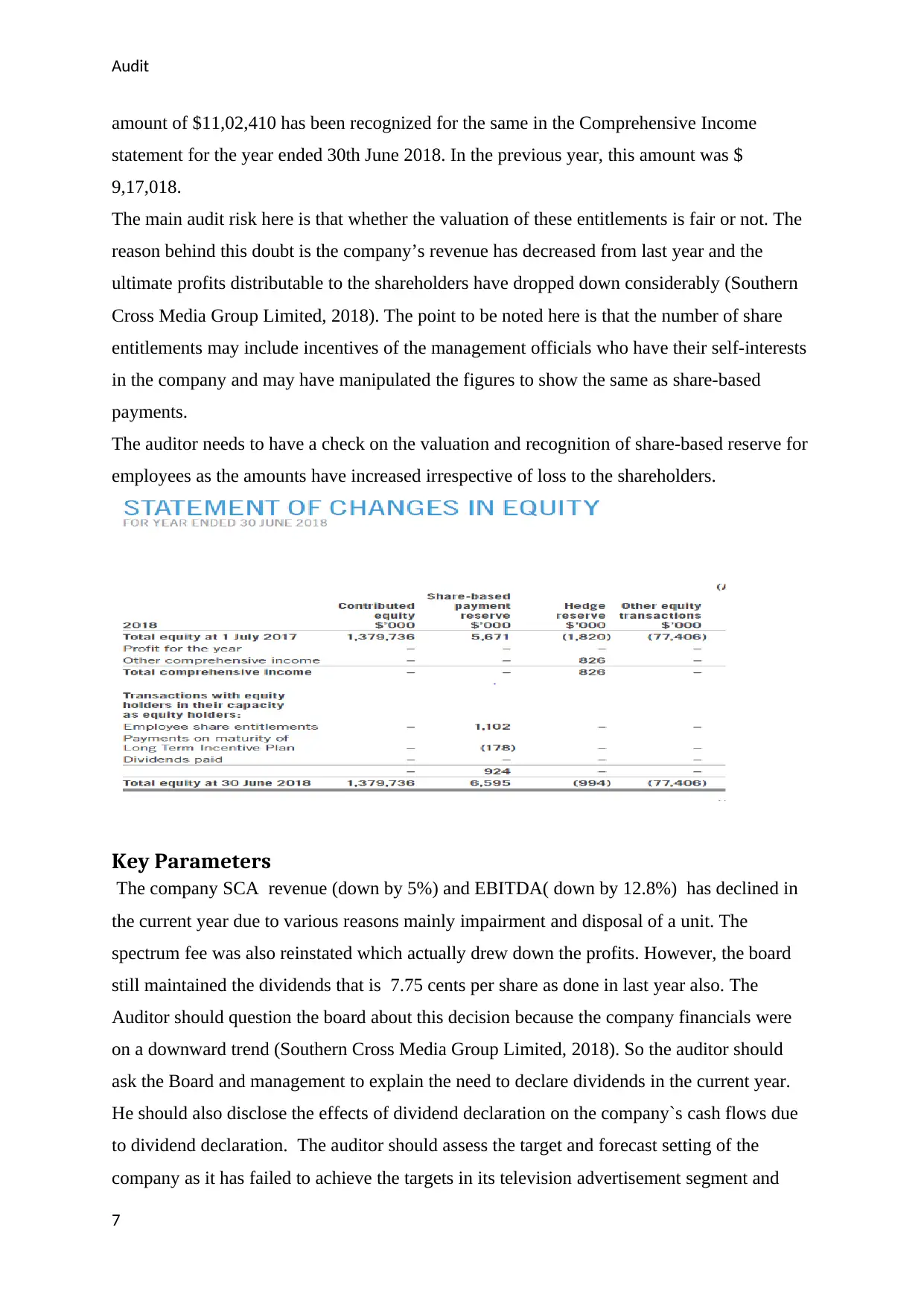

Employee share entitlements

The employees have issued shares in lieu of no consideration with respect to the rights of

performance offered under LTIP, for utilization of share-based payments will be done and

where the fair value of the future estimated shares is recognized. For the current year, an

6

Financial Market Risks

There are three kinds of risk that the company is prone to- interest rate risk, liquidity risk &

cash flow interest rate risk. The most important risk that the company seeks to minimize

throughout the year is the interest rate risk as it has major influence on the company’s

financial performance (Roach, 2010).

An interest rate risk projects that risk that the company may not be able to fulfill its interest

rate commitments if the market interest rates move in an adverse way (Baldwin, 2010). The

company takes borrowings of long term at variable interest rates and hence exposes itself to a

interest rate risk that is linked to cash flow as well. When the interest rates are variable there

is a strong exposure to risk because the market situation is always filled with fluctuations that

might hamper the scenario (Melville, 2013).

The main risk factor to be kept in mind here is that the company does not have any fixed

formal policy for fixing its borrowing interest rates. It manages the interest rate risk by

utilizing the variable to fixed rate of interest swaps through which the interest rate on

borrowing can be converted from variable rates to fixed rates (Niemi & Sundgren, 2012). The

borrowing is done by the group at rates of variable nature and then swaps the same into fixed

rates. The company makes contracts with other parties so that difference can be exchanged

between the fixed and variable interest amounts on the basis of principal amounts that is

notional. For instance the group took an interest rate swap of $100 million through which it

can receive variable interest rate but the group will be subjected to pay average fixed rate of

2.25% with effect from January 2018. Now here the variable rates may be lower than payable

(Southern Cross Media Group Limited, 2018)

Fixed rates or it may be higher than this rate.

Hence the auditor needs to consider these factors while auditing the derivative financial

instruments related matters where there is interest rate risk prevalent.

Employee share entitlements

The employees have issued shares in lieu of no consideration with respect to the rights of

performance offered under LTIP, for utilization of share-based payments will be done and

where the fair value of the future estimated shares is recognized. For the current year, an

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

amount of $11,02,410 has been recognized for the same in the Comprehensive Income

statement for the year ended 30th June 2018. In the previous year, this amount was $

9,17,018.

The main audit risk here is that whether the valuation of these entitlements is fair or not. The

reason behind this doubt is the company’s revenue has decreased from last year and the

ultimate profits distributable to the shareholders have dropped down considerably (Southern

Cross Media Group Limited, 2018). The point to be noted here is that the number of share

entitlements may include incentives of the management officials who have their self-interests

in the company and may have manipulated the figures to show the same as share-based

payments.

The auditor needs to have a check on the valuation and recognition of share-based reserve for

employees as the amounts have increased irrespective of loss to the shareholders.

Key Parameters

The company SCA revenue (down by 5%) and EBITDA( down by 12.8%) has declined in

the current year due to various reasons mainly impairment and disposal of a unit. The

spectrum fee was also reinstated which actually drew down the profits. However, the board

still maintained the dividends that is 7.75 cents per share as done in last year also. The

Auditor should question the board about this decision because the company financials were

on a downward trend (Southern Cross Media Group Limited, 2018). So the auditor should

ask the Board and management to explain the need to declare dividends in the current year.

He should also disclose the effects of dividend declaration on the company`s cash flows due

to dividend declaration. The auditor should assess the target and forecast setting of the

company as it has failed to achieve the targets in its television advertisement segment and

7

amount of $11,02,410 has been recognized for the same in the Comprehensive Income

statement for the year ended 30th June 2018. In the previous year, this amount was $

9,17,018.

The main audit risk here is that whether the valuation of these entitlements is fair or not. The

reason behind this doubt is the company’s revenue has decreased from last year and the

ultimate profits distributable to the shareholders have dropped down considerably (Southern

Cross Media Group Limited, 2018). The point to be noted here is that the number of share

entitlements may include incentives of the management officials who have their self-interests

in the company and may have manipulated the figures to show the same as share-based

payments.

The auditor needs to have a check on the valuation and recognition of share-based reserve for

employees as the amounts have increased irrespective of loss to the shareholders.

Key Parameters

The company SCA revenue (down by 5%) and EBITDA( down by 12.8%) has declined in

the current year due to various reasons mainly impairment and disposal of a unit. The

spectrum fee was also reinstated which actually drew down the profits. However, the board

still maintained the dividends that is 7.75 cents per share as done in last year also. The

Auditor should question the board about this decision because the company financials were

on a downward trend (Southern Cross Media Group Limited, 2018). So the auditor should

ask the Board and management to explain the need to declare dividends in the current year.

He should also disclose the effects of dividend declaration on the company`s cash flows due

to dividend declaration. The auditor should assess the target and forecast setting of the

company as it has failed to achieve the targets in its television advertisement segment and

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

metro radio business (Arnold, 2010). The internal audit team needs to be cross-questioned

and the auditor needs to check whether the internal auditor has shown and discussed the

downward trends of sales and profits in his Internal Audit reports (Matthew, 2015).

Technology & its use:

The company is widely spread in Australia and its business is dependent heavily on the use of

the latest technology. Be it TV, audio or radio entertainment, the company has its footprints

in all the areas (Southern Cross Media Group Limited, 2018). It is a consumer-centric

company whose only success parameter is customer satisfaction. The technology plays a

major reason for reaching its customers. The Auditor should clearly understand the use of

8

metro radio business (Arnold, 2010). The internal audit team needs to be cross-questioned

and the auditor needs to check whether the internal auditor has shown and discussed the

downward trends of sales and profits in his Internal Audit reports (Matthew, 2015).

Technology & its use:

The company is widely spread in Australia and its business is dependent heavily on the use of

the latest technology. Be it TV, audio or radio entertainment, the company has its footprints

in all the areas (Southern Cross Media Group Limited, 2018). It is a consumer-centric

company whose only success parameter is customer satisfaction. The technology plays a

major reason for reaching its customers. The Auditor should clearly understand the use of

8

Audit

technology and effects in case of any failure on the business operations before accepting the

audit engagement. The Auditor should plan his audit program in a way that he can understand

the effects of connectivity failure and try to disclose the contingent Loss and reputation Loss

to the company.

The company has built a strong network and also employed the best workforce to manage

traffic and connectivity. The company is regularly expanding his business and acquiring

network assets and connecting them with each other via cable lines and satellites etc. There

always remains a risk of hacking and compromise of security which may seriously affect the

company business. Hence Audit planning should be done after keeping this in mind. Below is

an excerpt of CEO of the company.

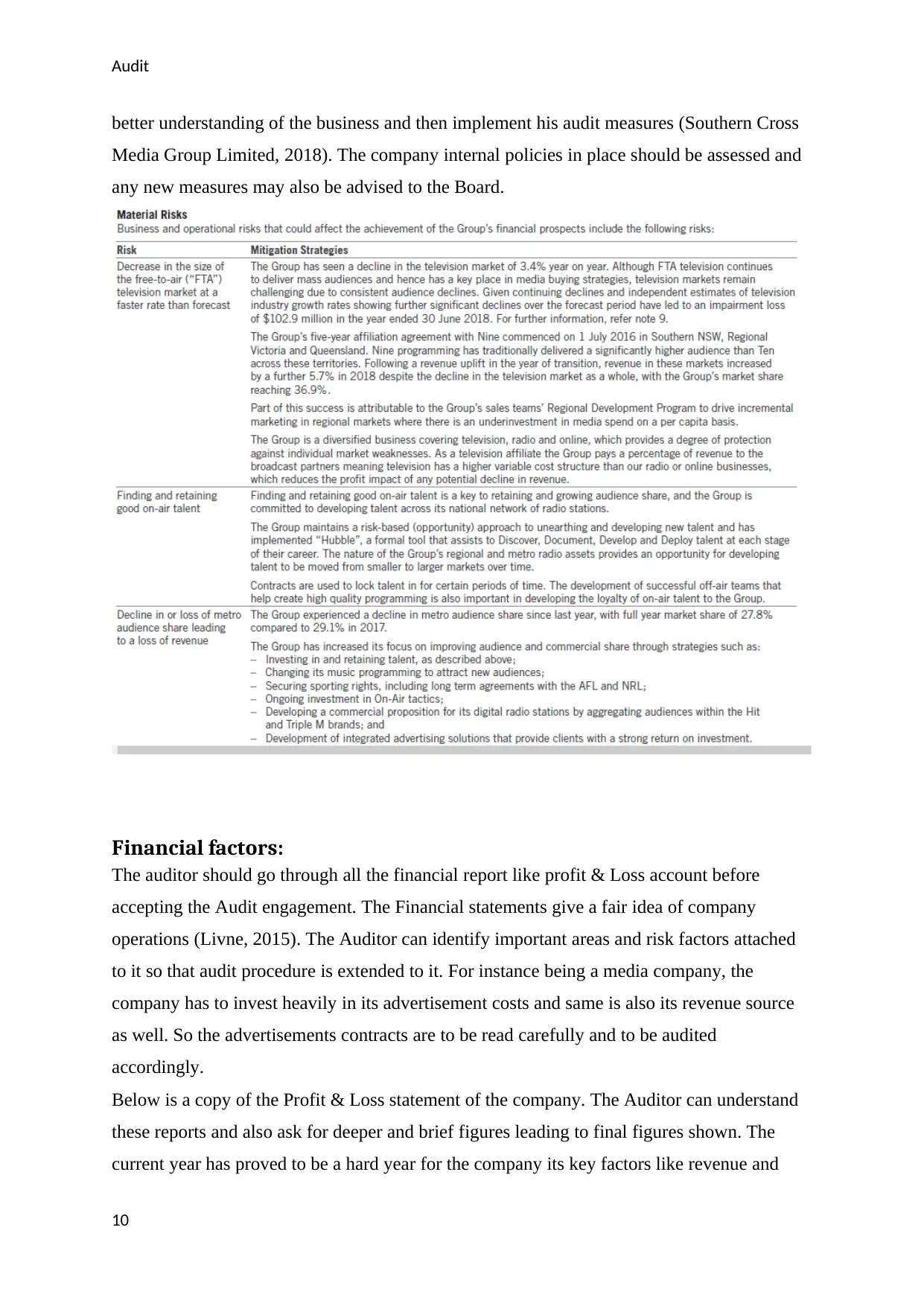

Material risks

The company has also revealed some of its material risks which are of paramount importance

which is highlighted below. The auditor will be helped by this and may further extend his

audit planning on these areas as well. The board has also mentioned how to tackle and

mitigate these risks.

The Auditor might not be well versed with the technicalities of the business. The auditor

should fully understand the business procedures and the laws and the regulations binding on

the company (Rezaee & Kedia, 2012). The Auditor can hire any media expert to understand

the complexities of the business like the use of spectrum, Connectivity, Licensing, etc to get a

9

technology and effects in case of any failure on the business operations before accepting the

audit engagement. The Auditor should plan his audit program in a way that he can understand

the effects of connectivity failure and try to disclose the contingent Loss and reputation Loss

to the company.

The company has built a strong network and also employed the best workforce to manage

traffic and connectivity. The company is regularly expanding his business and acquiring

network assets and connecting them with each other via cable lines and satellites etc. There

always remains a risk of hacking and compromise of security which may seriously affect the

company business. Hence Audit planning should be done after keeping this in mind. Below is

an excerpt of CEO of the company.

Material risks

The company has also revealed some of its material risks which are of paramount importance

which is highlighted below. The auditor will be helped by this and may further extend his

audit planning on these areas as well. The board has also mentioned how to tackle and

mitigate these risks.

The Auditor might not be well versed with the technicalities of the business. The auditor

should fully understand the business procedures and the laws and the regulations binding on

the company (Rezaee & Kedia, 2012). The Auditor can hire any media expert to understand

the complexities of the business like the use of spectrum, Connectivity, Licensing, etc to get a

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

better understanding of the business and then implement his audit measures (Southern Cross

Media Group Limited, 2018). The company internal policies in place should be assessed and

any new measures may also be advised to the Board.

Financial factors:

The auditor should go through all the financial report like profit & Loss account before

accepting the Audit engagement. The Financial statements give a fair idea of company

operations (Livne, 2015). The Auditor can identify important areas and risk factors attached

to it so that audit procedure is extended to it. For instance being a media company, the

company has to invest heavily in its advertisement costs and same is also its revenue source

as well. So the advertisements contracts are to be read carefully and to be audited

accordingly.

Below is a copy of the Profit & Loss statement of the company. The Auditor can understand

these reports and also ask for deeper and brief figures leading to final figures shown. The

current year has proved to be a hard year for the company its key factors like revenue and

10

better understanding of the business and then implement his audit measures (Southern Cross

Media Group Limited, 2018). The company internal policies in place should be assessed and

any new measures may also be advised to the Board.

Financial factors:

The auditor should go through all the financial report like profit & Loss account before

accepting the Audit engagement. The Financial statements give a fair idea of company

operations (Livne, 2015). The Auditor can identify important areas and risk factors attached

to it so that audit procedure is extended to it. For instance being a media company, the

company has to invest heavily in its advertisement costs and same is also its revenue source

as well. So the advertisements contracts are to be read carefully and to be audited

accordingly.

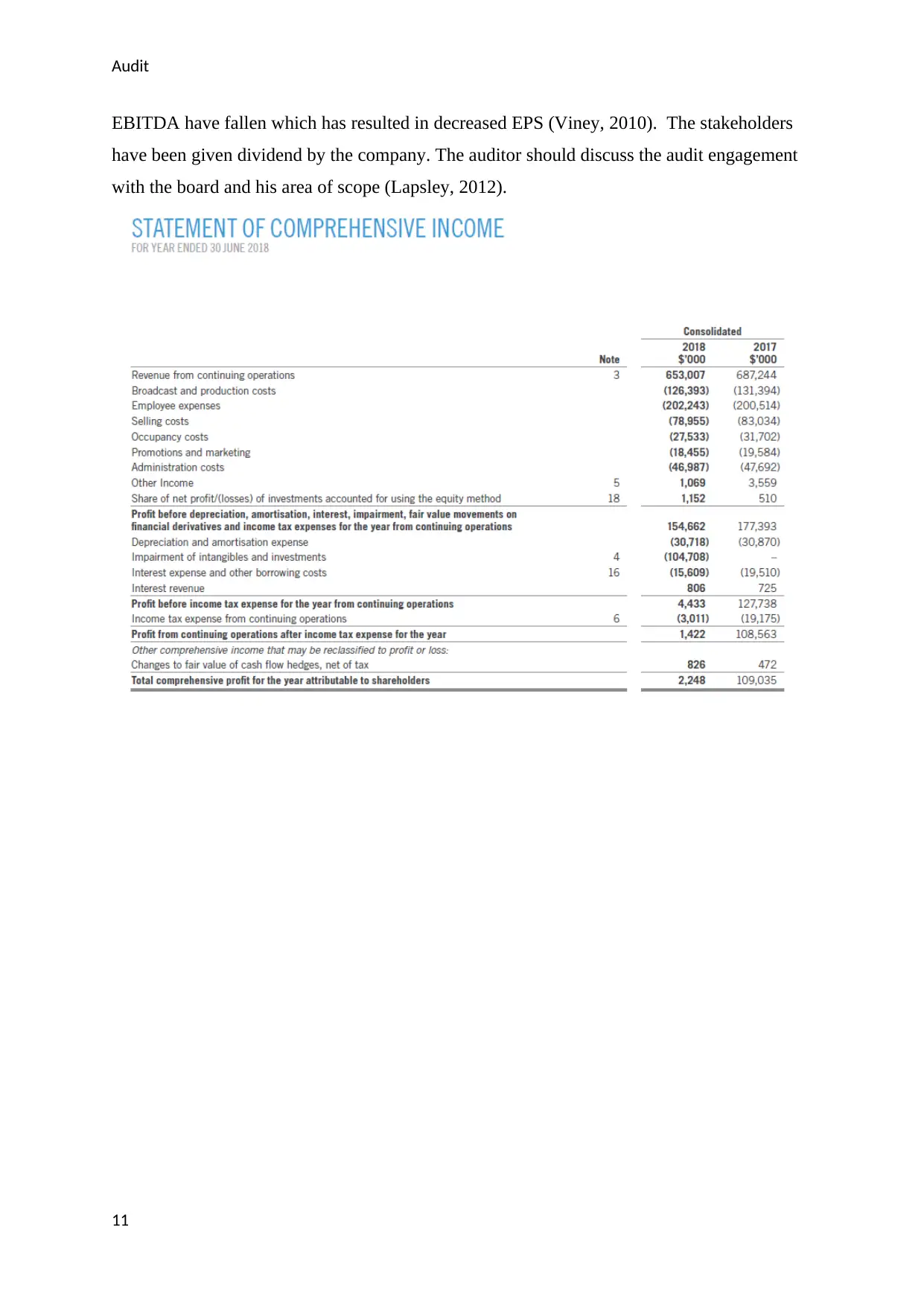

Below is a copy of the Profit & Loss statement of the company. The Auditor can understand

these reports and also ask for deeper and brief figures leading to final figures shown. The

current year has proved to be a hard year for the company its key factors like revenue and

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

EBITDA have fallen which has resulted in decreased EPS (Viney, 2010). The stakeholders

have been given dividend by the company. The auditor should discuss the audit engagement

with the board and his area of scope (Lapsley, 2012).

11

EBITDA have fallen which has resulted in decreased EPS (Viney, 2010). The stakeholders

have been given dividend by the company. The auditor should discuss the audit engagement

with the board and his area of scope (Lapsley, 2012).

11

Audit

Conclusion

The report emphasizes on the main audit risk factors which the company annual report

depicts which the auditor needs to focus on while preparing his audit plan and accepting the

audit engagement. These audit risks if not detected can lead to the unjustified opinion on the

books of accounts by the auditor. Hence these factors are very important from the viewpoint

of an auditor. From the various factors mentioned above and from the annual report, it is clear

that the revenue and the net profits of the company have dropped considerably. Thereby, the

risk factors should be communicated by the auditor to those charged with governance so that

there are no material misstatements in the financial report in the current as well as the

upcoming year. All the relevant disclosures should be made to make the reports transparent

for the user of the financial and non-financial data of the company.

12

Conclusion

The report emphasizes on the main audit risk factors which the company annual report

depicts which the auditor needs to focus on while preparing his audit plan and accepting the

audit engagement. These audit risks if not detected can lead to the unjustified opinion on the

books of accounts by the auditor. Hence these factors are very important from the viewpoint

of an auditor. From the various factors mentioned above and from the annual report, it is clear

that the revenue and the net profits of the company have dropped considerably. Thereby, the

risk factors should be communicated by the auditor to those charged with governance so that

there are no material misstatements in the financial report in the current as well as the

upcoming year. All the relevant disclosures should be made to make the reports transparent

for the user of the financial and non-financial data of the company.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.