ACC621 Auditing Practice Report: Materiality and Fraud Risks

VerifiedAdded on 2023/06/08

|15

|2181

|447

Report

AI Summary

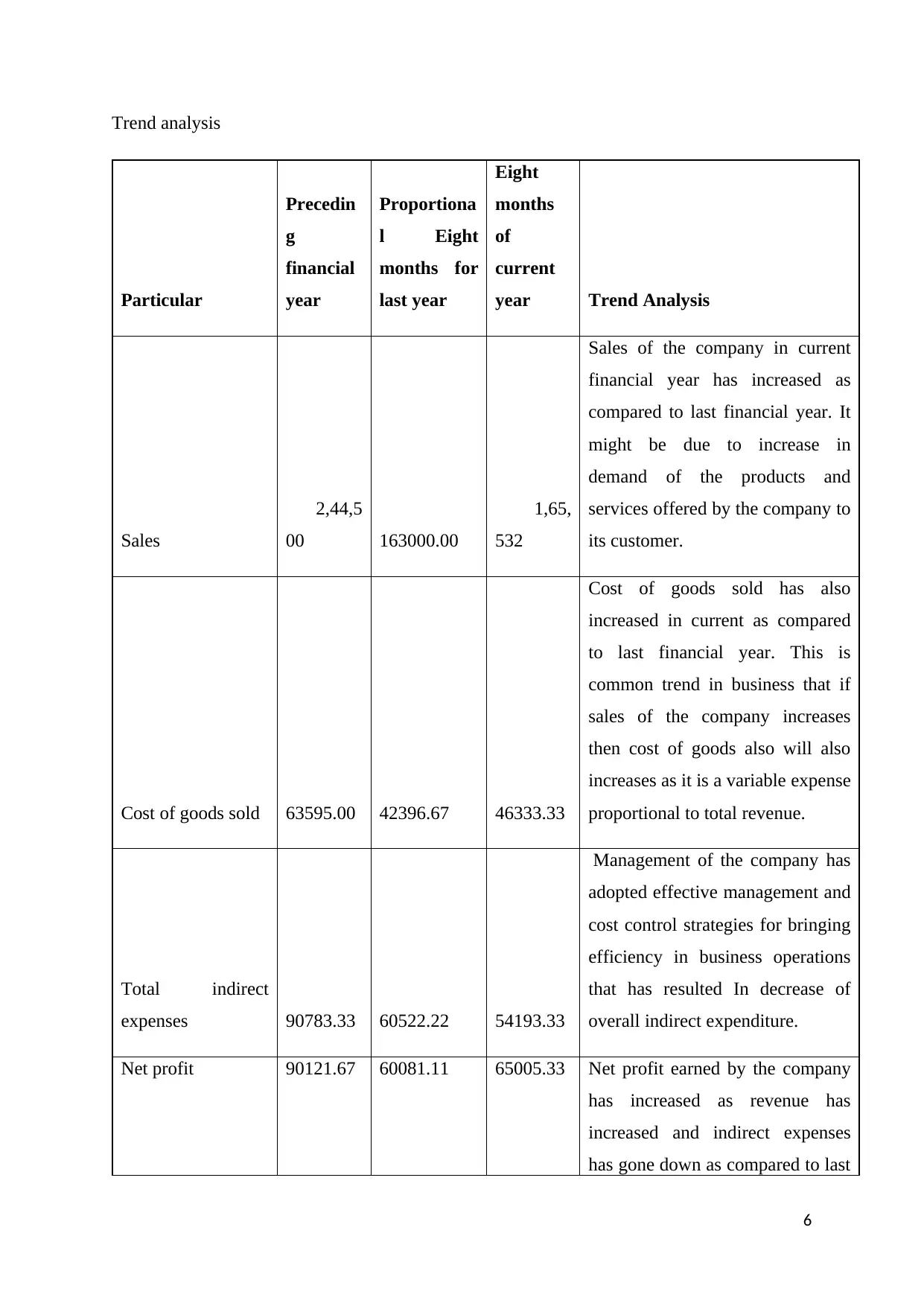

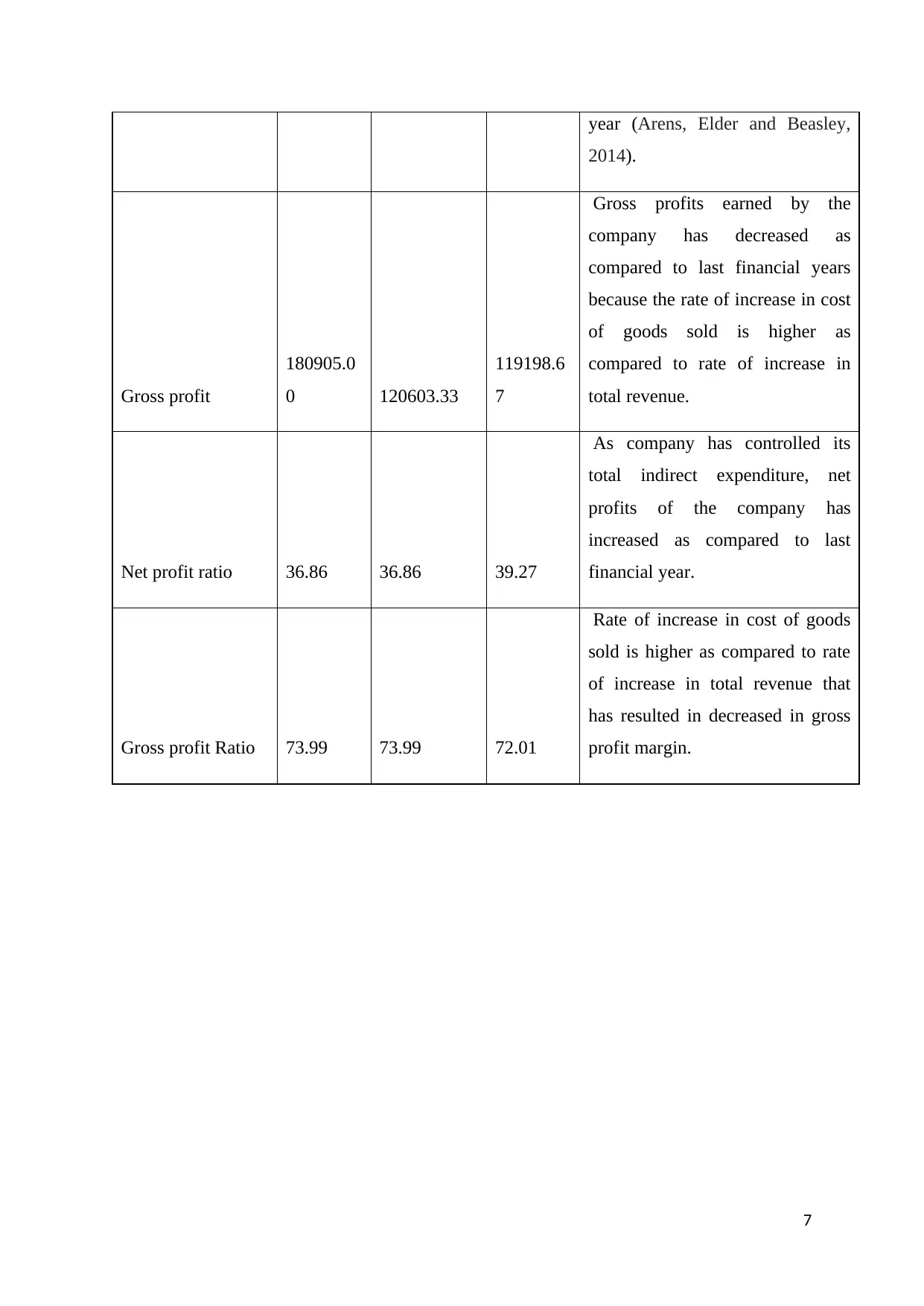

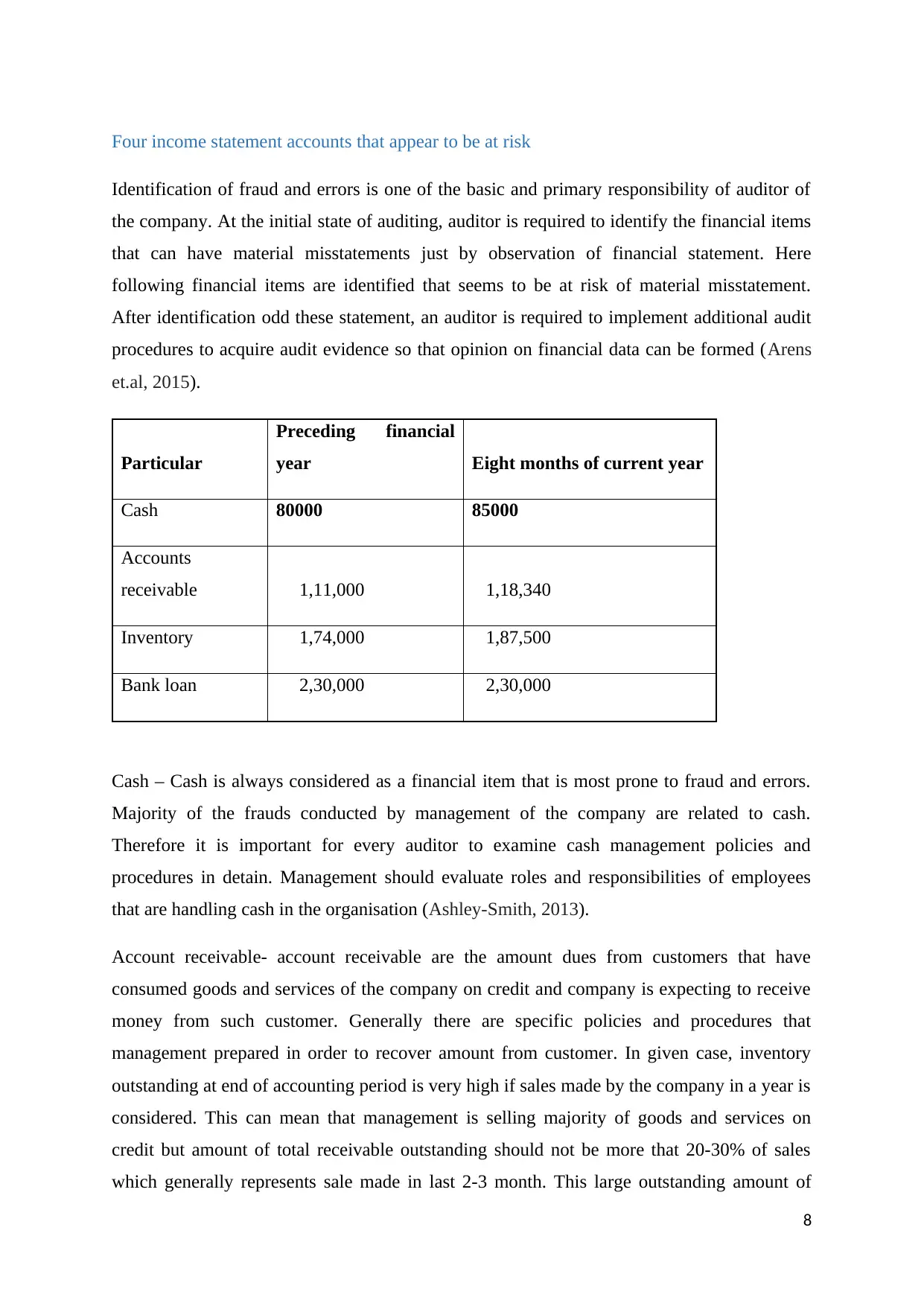

This report provides a comprehensive analysis of auditing practices, focusing on the audit of Chamoisee Enterprises. The report begins by addressing the concept of materiality in financial reporting, explaining its significance and how auditors determine materiality thresholds. It then examines the financial statements of Chamoisee Enterprises, including trend analysis of key accounts like sales, cost of goods sold, and net profit. The report identifies potential risks of material misstatement in accounts such as cash, accounts receivable, inventory, and bank loans, and proposes specific audit procedures to address these risks. Furthermore, the report discusses the importance of fraud risk assessment and highlights the limitations of the audit partner's initial assessment. Finally, the report concludes by summarizing the key findings and recommendations, emphasizing the importance of thorough audit procedures and a comprehensive understanding of financial statement analysis.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.