Special Topic of Australian Tax Law

VerifiedAdded on 2023/06/03

|12

|2288

|344

AI Summary

This article discusses the Fringe Benefit Tax liability of Montgomery’s Pty Ltd and the taxable value of fringe benefits for the BMW X provided by Montgomery’s Pty Ltd to its new marketing director. It also explains the FBT liability for providing foods to the employees who are living away from home and more. The article cites relevant sections of the Fringe Benefits Tax Assessment Act 1986 and provides examples to illustrate the application of the rules. The article concludes by stating that business expenditures are not subjected to FBT and only the non-monetary benefits which are not subjected to ITAA and not business-related expenditures are liable to FBT as per the FBTAA.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: SPECIAL TOPIC OF AUSTRALIAN TAX LAW

Special Topic of Australian Tax Law

Name of the Student:

Name of the University:

Authors Note:

Special Topic of Australian Tax Law

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1SPECIAL TOPIC OF AUSTRALIAN TAX LAW

Contents

Sales manager:.................................................................................................................................2

New marketing director:..................................................................................................................6

Benefits to general Staffs:................................................................................................................8

References:....................................................................................................................................10

Contents

Sales manager:.................................................................................................................................2

New marketing director:..................................................................................................................6

Benefits to general Staffs:................................................................................................................8

References:....................................................................................................................................10

2SPECIAL TOPIC OF AUSTRALIAN TAX LAW

Sales manager:

Issue:

Determining the Fringe Benefit Tax liability of Montgomery’s Pty Ltd is the main topic of

discussion here.

Rules:

Often employers provide non-monetary benefits to their employee in addition to the salary and

other monetary benefits to motivate them to work efficiently for the organizations. Such non-

monetary benefits are not taxable in the hands of the employee rather the employers are required

to pay Fringe Benefit Tax on such non-monetary benefits. Taking into consideration the

provisions of Fringe Benefits Tax Assessment Act 1986 (FBTAA) the practical scenarios shall

be elaborated in this document1. Division 2 of Part III of FBTAA specifies that an employer is

liable to pay Fringe Benefit Tax (FBT) for making available the car owned or leased by the

employer for the personal use of the employee.

Application:

(a) Cash salary of $125000 is a taxable income of Brad Cruise and he will be liable to pay income

tax on such salary as per Income Tax Assessment Act 1997 (ITAA). Thus, the amount of salary is

not subjected to Fringe benefit tax (FBT).

(b) Superannuation contribution both by the employer as well as employee is not subjected to FBT.

1 Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits tax

a barrier to active commuting in Australia? 1." eJournal of Tax Research 13, no. 3 (2015): 819.

Sales manager:

Issue:

Determining the Fringe Benefit Tax liability of Montgomery’s Pty Ltd is the main topic of

discussion here.

Rules:

Often employers provide non-monetary benefits to their employee in addition to the salary and

other monetary benefits to motivate them to work efficiently for the organizations. Such non-

monetary benefits are not taxable in the hands of the employee rather the employers are required

to pay Fringe Benefit Tax on such non-monetary benefits. Taking into consideration the

provisions of Fringe Benefits Tax Assessment Act 1986 (FBTAA) the practical scenarios shall

be elaborated in this document1. Division 2 of Part III of FBTAA specifies that an employer is

liable to pay Fringe Benefit Tax (FBT) for making available the car owned or leased by the

employer for the personal use of the employee.

Application:

(a) Cash salary of $125000 is a taxable income of Brad Cruise and he will be liable to pay income

tax on such salary as per Income Tax Assessment Act 1997 (ITAA). Thus, the amount of salary is

not subjected to Fringe benefit tax (FBT).

(b) Superannuation contribution both by the employer as well as employee is not subjected to FBT.

1 Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits tax

a barrier to active commuting in Australia? 1." eJournal of Tax Research 13, no. 3 (2015): 819.

3SPECIAL TOPIC OF AUSTRALIAN TAX LAW

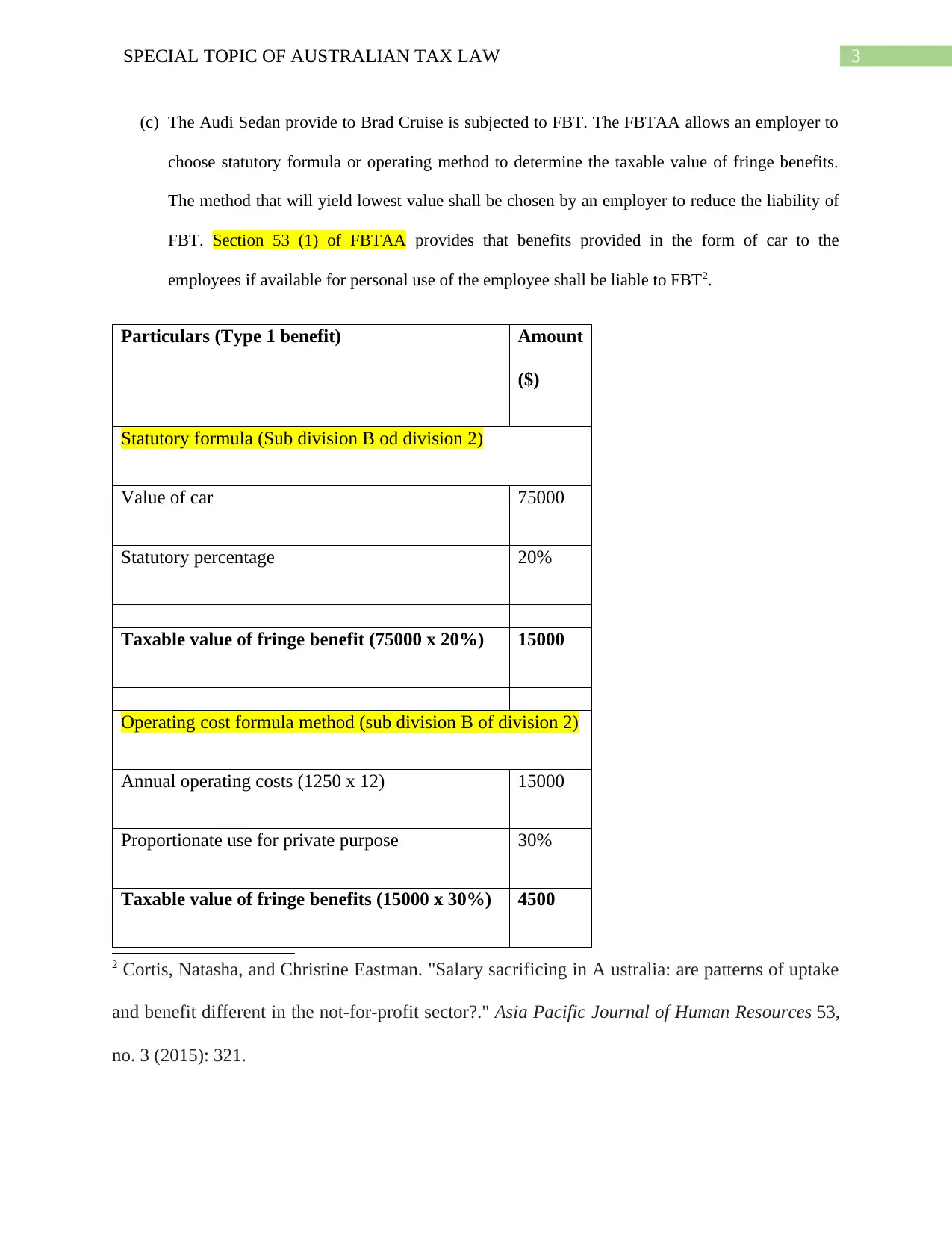

(c) The Audi Sedan provide to Brad Cruise is subjected to FBT. The FBTAA allows an employer to

choose statutory formula or operating method to determine the taxable value of fringe benefits.

The method that will yield lowest value shall be chosen by an employer to reduce the liability of

FBT. Section 53 (1) of FBTAA provides that benefits provided in the form of car to the

employees if available for personal use of the employee shall be liable to FBT2.

Particulars (Type 1 benefit) Amount

($)

Statutory formula (Sub division B od division 2)

Value of car 75000

Statutory percentage 20%

Taxable value of fringe benefit (75000 x 20%) 15000

Operating cost formula method (sub division B of division 2)

Annual operating costs (1250 x 12) 15000

Proportionate use for private purpose 30%

Taxable value of fringe benefits (15000 x 30%) 4500

2 Cortis, Natasha, and Christine Eastman. "Salary sacrificing in A ustralia: are patterns of uptake

and benefit different in the not‐for‐profit sector?." Asia Pacific Journal of Human Resources 53,

no. 3 (2015): 321.

(c) The Audi Sedan provide to Brad Cruise is subjected to FBT. The FBTAA allows an employer to

choose statutory formula or operating method to determine the taxable value of fringe benefits.

The method that will yield lowest value shall be chosen by an employer to reduce the liability of

FBT. Section 53 (1) of FBTAA provides that benefits provided in the form of car to the

employees if available for personal use of the employee shall be liable to FBT2.

Particulars (Type 1 benefit) Amount

($)

Statutory formula (Sub division B od division 2)

Value of car 75000

Statutory percentage 20%

Taxable value of fringe benefit (75000 x 20%) 15000

Operating cost formula method (sub division B of division 2)

Annual operating costs (1250 x 12) 15000

Proportionate use for private purpose 30%

Taxable value of fringe benefits (15000 x 30%) 4500

2 Cortis, Natasha, and Christine Eastman. "Salary sacrificing in A ustralia: are patterns of uptake

and benefit different in the not‐for‐profit sector?." Asia Pacific Journal of Human Resources 53,

no. 3 (2015): 321.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4SPECIAL TOPIC OF AUSTRALIAN TAX LAW

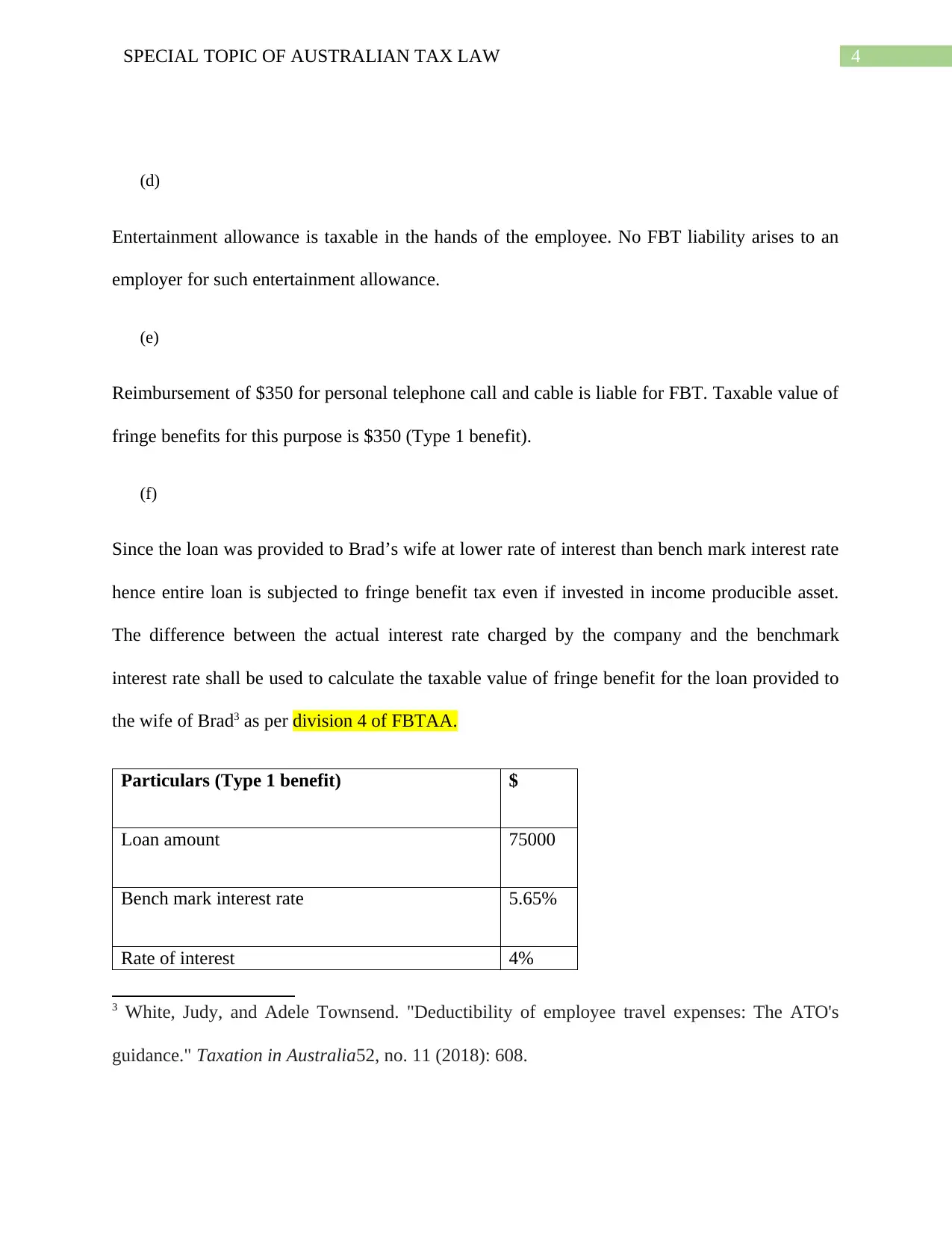

(d)

Entertainment allowance is taxable in the hands of the employee. No FBT liability arises to an

employer for such entertainment allowance.

(e)

Reimbursement of $350 for personal telephone call and cable is liable for FBT. Taxable value of

fringe benefits for this purpose is $350 (Type 1 benefit).

(f)

Since the loan was provided to Brad’s wife at lower rate of interest than bench mark interest rate

hence entire loan is subjected to fringe benefit tax even if invested in income producible asset.

The difference between the actual interest rate charged by the company and the benchmark

interest rate shall be used to calculate the taxable value of fringe benefit for the loan provided to

the wife of Brad3 as per division 4 of FBTAA.

Particulars (Type 1 benefit) $

Loan amount 75000

Bench mark interest rate 5.65%

Rate of interest 4%

3 White, Judy, and Adele Townsend. "Deductibility of employee travel expenses: The ATO's

guidance." Taxation in Australia52, no. 11 (2018): 608.

(d)

Entertainment allowance is taxable in the hands of the employee. No FBT liability arises to an

employer for such entertainment allowance.

(e)

Reimbursement of $350 for personal telephone call and cable is liable for FBT. Taxable value of

fringe benefits for this purpose is $350 (Type 1 benefit).

(f)

Since the loan was provided to Brad’s wife at lower rate of interest than bench mark interest rate

hence entire loan is subjected to fringe benefit tax even if invested in income producible asset.

The difference between the actual interest rate charged by the company and the benchmark

interest rate shall be used to calculate the taxable value of fringe benefit for the loan provided to

the wife of Brad3 as per division 4 of FBTAA.

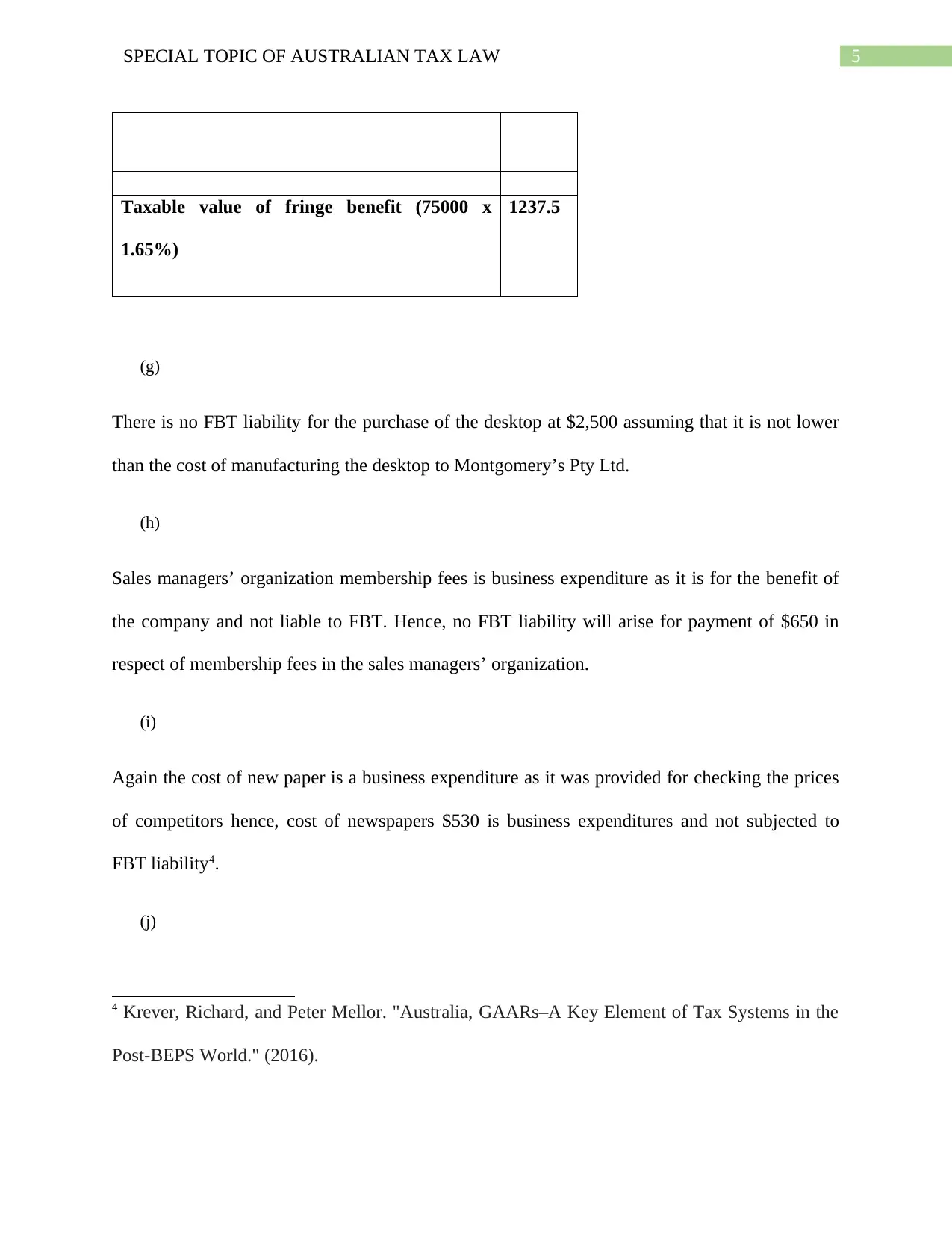

Particulars (Type 1 benefit) $

Loan amount 75000

Bench mark interest rate 5.65%

Rate of interest 4%

3 White, Judy, and Adele Townsend. "Deductibility of employee travel expenses: The ATO's

guidance." Taxation in Australia52, no. 11 (2018): 608.

5SPECIAL TOPIC OF AUSTRALIAN TAX LAW

Taxable value of fringe benefit (75000 x

1.65%)

1237.5

(g)

There is no FBT liability for the purchase of the desktop at $2,500 assuming that it is not lower

than the cost of manufacturing the desktop to Montgomery’s Pty Ltd.

(h)

Sales managers’ organization membership fees is business expenditure as it is for the benefit of

the company and not liable to FBT. Hence, no FBT liability will arise for payment of $650 in

respect of membership fees in the sales managers’ organization.

(i)

Again the cost of new paper is a business expenditure as it was provided for checking the prices

of competitors hence, cost of newspapers $530 is business expenditures and not subjected to

FBT liability4.

(j)

4 Krever, Richard, and Peter Mellor. "Australia, GAARs–A Key Element of Tax Systems in the

Post-BEPS World." (2016).

Taxable value of fringe benefit (75000 x

1.65%)

1237.5

(g)

There is no FBT liability for the purchase of the desktop at $2,500 assuming that it is not lower

than the cost of manufacturing the desktop to Montgomery’s Pty Ltd.

(h)

Sales managers’ organization membership fees is business expenditure as it is for the benefit of

the company and not liable to FBT. Hence, no FBT liability will arise for payment of $650 in

respect of membership fees in the sales managers’ organization.

(i)

Again the cost of new paper is a business expenditure as it was provided for checking the prices

of competitors hence, cost of newspapers $530 is business expenditures and not subjected to

FBT liability4.

(j)

4 Krever, Richard, and Peter Mellor. "Australia, GAARs–A Key Element of Tax Systems in the

Post-BEPS World." (2016).

6SPECIAL TOPIC OF AUSTRALIAN TAX LAW

Gift of $280 via visa card prepaid is liable to be taxed for fringe benefits purpose (Type 2

benefit).

(k)

Since, the chemist shop was almost 90% way to the home hence the travelling cost of $96 is not

subjected to FBT liability.

(l)

Since the nearest car parking facility is situated 2 kilometres away hence, no FBT liability will

arise for the car parking facility provided to Brad. Chapter 16 of FBTAA provides that only

when the car parking facility is within 1 kilometres radius from the factory or office premises

that the liability to FBT arise5. Division 10A of the act provides that only in case certain

conditions are fulfilled then the free car parking facilities to employees will not be considered for

FBT purpose.

Conclusion:

It is clear from the above that the business expenditures are not subjected to FBT and only the

non-monetary benefits which are not subjected to ITAA and not business related expenditures

are liable to FBT as per the FBTAA.

New marketing director:

Issue:

5 Soled, Jay A., and Kathleen DeLaney Thomas. "Revisiting the Taxation of Fringe

Benefits." Wash. L. Rev. 91 (2016): 761.

Gift of $280 via visa card prepaid is liable to be taxed for fringe benefits purpose (Type 2

benefit).

(k)

Since, the chemist shop was almost 90% way to the home hence the travelling cost of $96 is not

subjected to FBT liability.

(l)

Since the nearest car parking facility is situated 2 kilometres away hence, no FBT liability will

arise for the car parking facility provided to Brad. Chapter 16 of FBTAA provides that only

when the car parking facility is within 1 kilometres radius from the factory or office premises

that the liability to FBT arise5. Division 10A of the act provides that only in case certain

conditions are fulfilled then the free car parking facilities to employees will not be considered for

FBT purpose.

Conclusion:

It is clear from the above that the business expenditures are not subjected to FBT and only the

non-monetary benefits which are not subjected to ITAA and not business related expenditures

are liable to FBT as per the FBTAA.

New marketing director:

Issue:

5 Soled, Jay A., and Kathleen DeLaney Thomas. "Revisiting the Taxation of Fringe

Benefits." Wash. L. Rev. 91 (2016): 761.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7SPECIAL TOPIC OF AUSTRALIAN TAX LAW

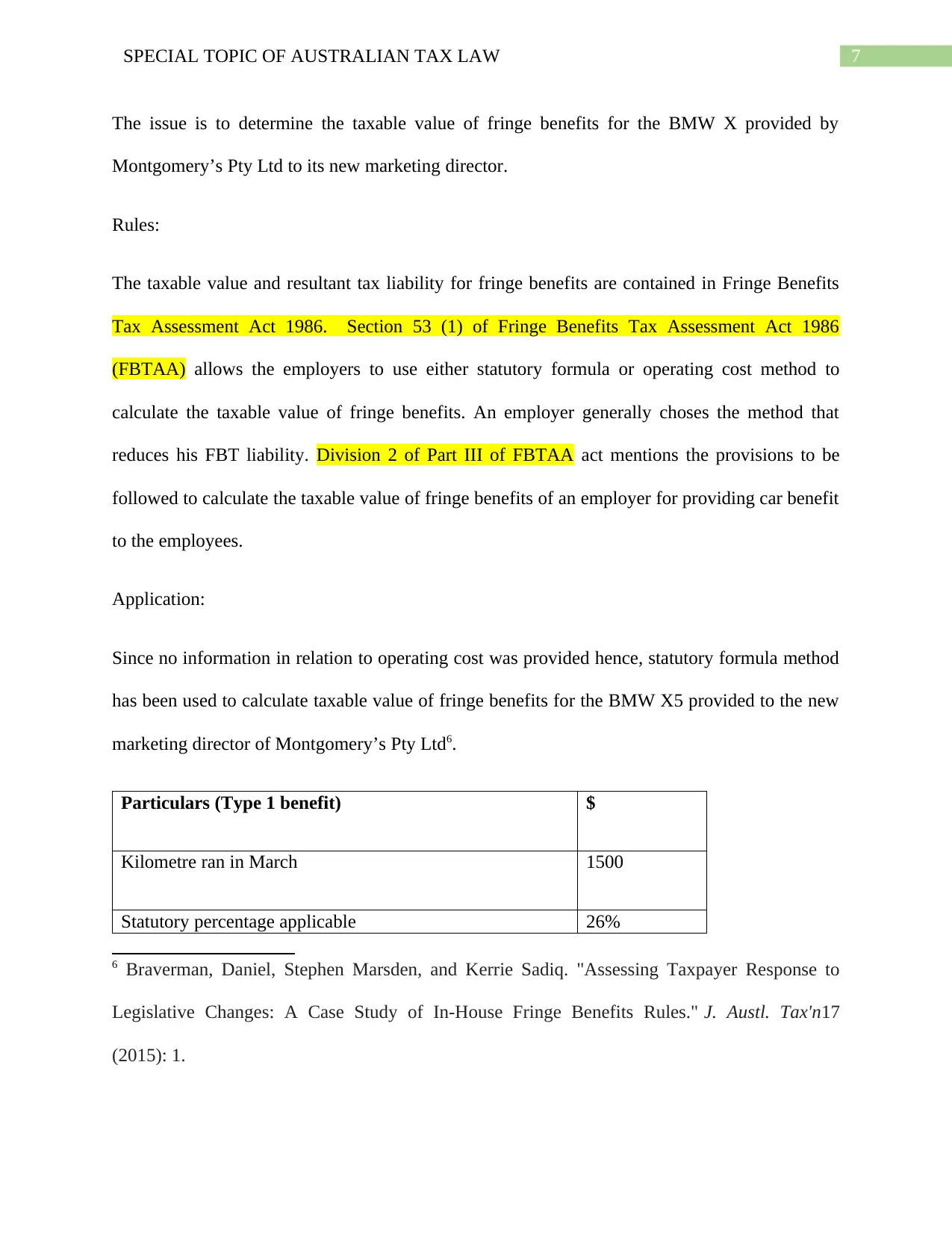

The issue is to determine the taxable value of fringe benefits for the BMW X provided by

Montgomery’s Pty Ltd to its new marketing director.

Rules:

The taxable value and resultant tax liability for fringe benefits are contained in Fringe Benefits

Tax Assessment Act 1986. Section 53 (1) of Fringe Benefits Tax Assessment Act 1986

(FBTAA) allows the employers to use either statutory formula or operating cost method to

calculate the taxable value of fringe benefits. An employer generally choses the method that

reduces his FBT liability. Division 2 of Part III of FBTAA act mentions the provisions to be

followed to calculate the taxable value of fringe benefits of an employer for providing car benefit

to the employees.

Application:

Since no information in relation to operating cost was provided hence, statutory formula method

has been used to calculate taxable value of fringe benefits for the BMW X5 provided to the new

marketing director of Montgomery’s Pty Ltd6.

Particulars (Type 1 benefit) $

Kilometre ran in March 1500

Statutory percentage applicable 26%

6 Braverman, Daniel, Stephen Marsden, and Kerrie Sadiq. "Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules." J. Austl. Tax'n17

(2015): 1.

The issue is to determine the taxable value of fringe benefits for the BMW X provided by

Montgomery’s Pty Ltd to its new marketing director.

Rules:

The taxable value and resultant tax liability for fringe benefits are contained in Fringe Benefits

Tax Assessment Act 1986. Section 53 (1) of Fringe Benefits Tax Assessment Act 1986

(FBTAA) allows the employers to use either statutory formula or operating cost method to

calculate the taxable value of fringe benefits. An employer generally choses the method that

reduces his FBT liability. Division 2 of Part III of FBTAA act mentions the provisions to be

followed to calculate the taxable value of fringe benefits of an employer for providing car benefit

to the employees.

Application:

Since no information in relation to operating cost was provided hence, statutory formula method

has been used to calculate taxable value of fringe benefits for the BMW X5 provided to the new

marketing director of Montgomery’s Pty Ltd6.

Particulars (Type 1 benefit) $

Kilometre ran in March 1500

Statutory percentage applicable 26%

6 Braverman, Daniel, Stephen Marsden, and Kerrie Sadiq. "Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules." J. Austl. Tax'n17

(2015): 1.

8SPECIAL TOPIC OF AUSTRALIAN TAX LAW

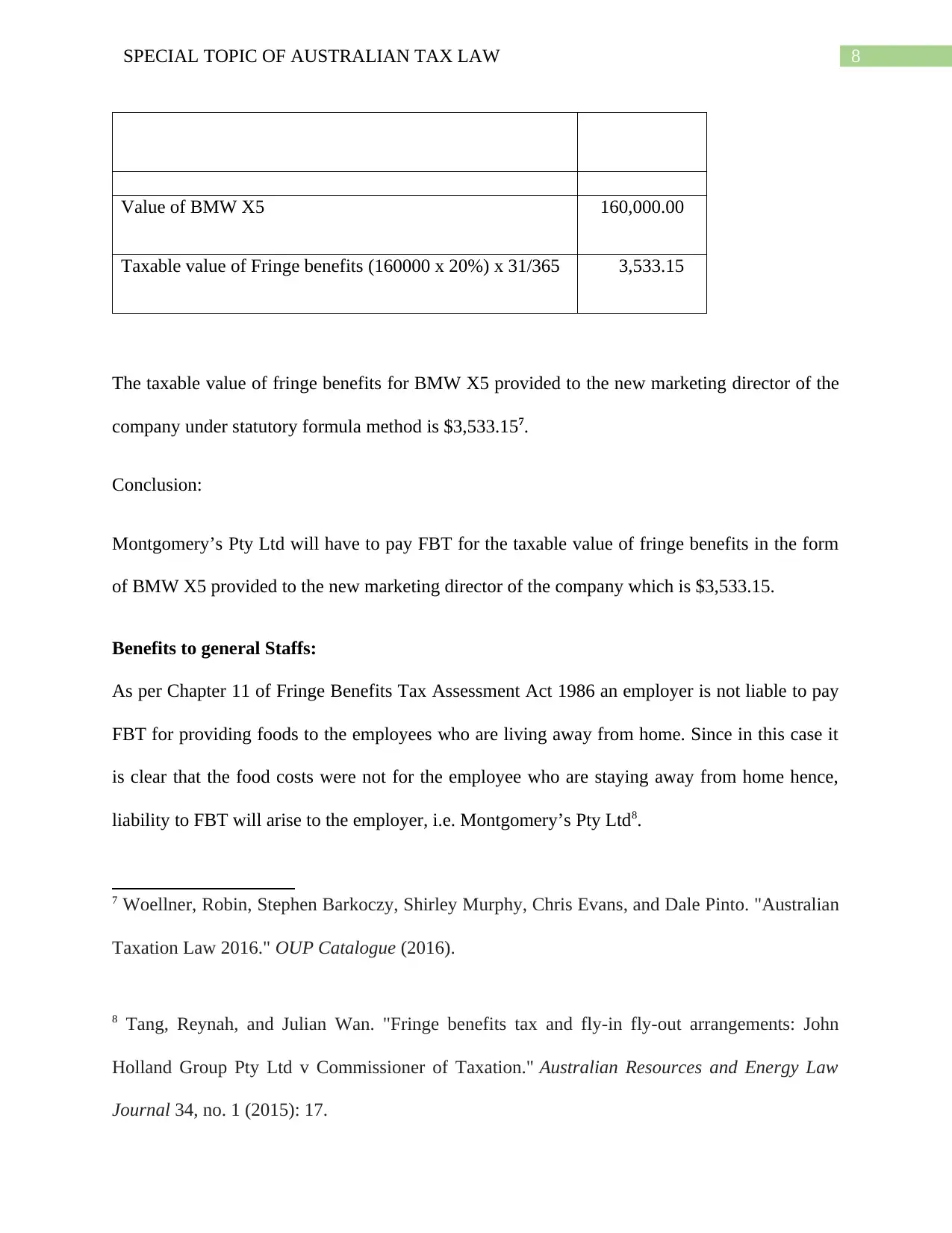

Value of BMW X5 160,000.00

Taxable value of Fringe benefits (160000 x 20%) x 31/365 3,533.15

The taxable value of fringe benefits for BMW X5 provided to the new marketing director of the

company under statutory formula method is $3,533.157.

Conclusion:

Montgomery’s Pty Ltd will have to pay FBT for the taxable value of fringe benefits in the form

of BMW X5 provided to the new marketing director of the company which is $3,533.15.

Benefits to general Staffs:

As per Chapter 11 of Fringe Benefits Tax Assessment Act 1986 an employer is not liable to pay

FBT for providing foods to the employees who are living away from home. Since in this case it

is clear that the food costs were not for the employee who are staying away from home hence,

liability to FBT will arise to the employer, i.e. Montgomery’s Pty Ltd8.

7 Woellner, Robin, Stephen Barkoczy, Shirley Murphy, Chris Evans, and Dale Pinto. "Australian

Taxation Law 2016." OUP Catalogue (2016).

8 Tang, Reynah, and Julian Wan. "Fringe benefits tax and fly-in fly-out arrangements: John

Holland Group Pty Ltd v Commissioner of Taxation." Australian Resources and Energy Law

Journal 34, no. 1 (2015): 17.

Value of BMW X5 160,000.00

Taxable value of Fringe benefits (160000 x 20%) x 31/365 3,533.15

The taxable value of fringe benefits for BMW X5 provided to the new marketing director of the

company under statutory formula method is $3,533.157.

Conclusion:

Montgomery’s Pty Ltd will have to pay FBT for the taxable value of fringe benefits in the form

of BMW X5 provided to the new marketing director of the company which is $3,533.15.

Benefits to general Staffs:

As per Chapter 11 of Fringe Benefits Tax Assessment Act 1986 an employer is not liable to pay

FBT for providing foods to the employees who are living away from home. Since in this case it

is clear that the food costs were not for the employee who are staying away from home hence,

liability to FBT will arise to the employer, i.e. Montgomery’s Pty Ltd8.

7 Woellner, Robin, Stephen Barkoczy, Shirley Murphy, Chris Evans, and Dale Pinto. "Australian

Taxation Law 2016." OUP Catalogue (2016).

8 Tang, Reynah, and Julian Wan. "Fringe benefits tax and fly-in fly-out arrangements: John

Holland Group Pty Ltd v Commissioner of Taxation." Australian Resources and Energy Law

Journal 34, no. 1 (2015): 17.

9SPECIAL TOPIC OF AUSTRALIAN TAX LAW

Hence, the food cost of $5,600 for fresh fruits to staffs will be considered as fringe benefits and

accordingly, shall be liable to FBT as per division 9A of the act outlining meal entertainment.

The cost of party to the extent related to the clients and their spouses will not be subjected to

FBT. However, the cost of employee and their spouses will be considered for the purpose of

FBT. Hence, the entertainment cost of 10 staffs and their spouses combining to $3,000 (20 x

150) is taxable value of fringe benefits (Type 1 benefit) for the purpose to calculate the FBT

liability of the company is respect of the Christmas party held by the company.

The reward of HECS-HELP of $1,825 to each student for achieving highest results in their

tertiary studies is a business strategy of the company to motivate its staffs and employees to

perform better thus, it is to be considered as business expenditure. Hence, no FBT liability will

arise to Montgomery’s Pty Ltd for the above benefits.

The free car parking facility provided by the company to its employees will be subjected to FBT.

Chapter 16 of FBTAA provides that in case the car parking facility is within the business

premises or within 1 kilometre radius then the car parking facility provided by the employer to

its employees shall be subjected to FBT. In this case the taxable value of fringe benefits shall be

calculated by taking into consideration the cheapest car parking fee of $24 per day which has

also increased to $26.60 per day by the end of 31st March, 2018. The taxable value of fringe

benefits for this assuming 260 working day in the FBT year (24 x 260) = $6,240 (Type 1

benefit).

Hence, the food cost of $5,600 for fresh fruits to staffs will be considered as fringe benefits and

accordingly, shall be liable to FBT as per division 9A of the act outlining meal entertainment.

The cost of party to the extent related to the clients and their spouses will not be subjected to

FBT. However, the cost of employee and their spouses will be considered for the purpose of

FBT. Hence, the entertainment cost of 10 staffs and their spouses combining to $3,000 (20 x

150) is taxable value of fringe benefits (Type 1 benefit) for the purpose to calculate the FBT

liability of the company is respect of the Christmas party held by the company.

The reward of HECS-HELP of $1,825 to each student for achieving highest results in their

tertiary studies is a business strategy of the company to motivate its staffs and employees to

perform better thus, it is to be considered as business expenditure. Hence, no FBT liability will

arise to Montgomery’s Pty Ltd for the above benefits.

The free car parking facility provided by the company to its employees will be subjected to FBT.

Chapter 16 of FBTAA provides that in case the car parking facility is within the business

premises or within 1 kilometre radius then the car parking facility provided by the employer to

its employees shall be subjected to FBT. In this case the taxable value of fringe benefits shall be

calculated by taking into consideration the cheapest car parking fee of $24 per day which has

also increased to $26.60 per day by the end of 31st March, 2018. The taxable value of fringe

benefits for this assuming 260 working day in the FBT year (24 x 260) = $6,240 (Type 1

benefit).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10SPECIAL TOPIC OF AUSTRALIAN TAX LAW

References:

Braverman, Daniel, Stephen Marsden, and Kerrie Sadiq. "Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules." J. Austl. Tax'n17 (2015).

Cortis, Natasha, and Christine Eastman. "Salary sacrificing in A ustralia: are patterns of uptake

and benefit different in the not‐for‐profit sector?." Asia Pacific Journal of Human Resources 53,

no. 3 (2015).

Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits tax

a barrier to active commuting in Australia? 1." eJournal of Tax Research 13, no. 3 (2015).

Krever, Richard, and Peter Mellor. "Australia, GAARs–A Key Element of Tax Systems in the

Post-BEPS World." (2016).

Soled, Jay A., and Kathleen DeLaney Thomas. "Revisiting the Taxation of Fringe

Benefits." Wash. L. Rev. 91 (2016).

Tang, Reynah, and Julian Wan. "Fringe benefits tax and fly-in fly-out arrangements: John

Holland Group Pty Ltd v Commissioner of Taxation." Australian Resources and Energy Law

Journal 34, no. 1 (2015).

White, Judy, and Adele Townsend. "Deductibility of employee travel expenses: The ATO's

guidance." Taxation in Australia52, no. 11 (2018).

Woellner, Robin, Stephen Barkoczy, Shirley Murphy, Chris Evans, and Dale Pinto. "Australian

Taxation Law 2016." OUP Catalogue (2016).

References:

Braverman, Daniel, Stephen Marsden, and Kerrie Sadiq. "Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules." J. Austl. Tax'n17 (2015).

Cortis, Natasha, and Christine Eastman. "Salary sacrificing in A ustralia: are patterns of uptake

and benefit different in the not‐for‐profit sector?." Asia Pacific Journal of Human Resources 53,

no. 3 (2015).

Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits tax

a barrier to active commuting in Australia? 1." eJournal of Tax Research 13, no. 3 (2015).

Krever, Richard, and Peter Mellor. "Australia, GAARs–A Key Element of Tax Systems in the

Post-BEPS World." (2016).

Soled, Jay A., and Kathleen DeLaney Thomas. "Revisiting the Taxation of Fringe

Benefits." Wash. L. Rev. 91 (2016).

Tang, Reynah, and Julian Wan. "Fringe benefits tax and fly-in fly-out arrangements: John

Holland Group Pty Ltd v Commissioner of Taxation." Australian Resources and Energy Law

Journal 34, no. 1 (2015).

White, Judy, and Adele Townsend. "Deductibility of employee travel expenses: The ATO's

guidance." Taxation in Australia52, no. 11 (2018).

Woellner, Robin, Stephen Barkoczy, Shirley Murphy, Chris Evans, and Dale Pinto. "Australian

Taxation Law 2016." OUP Catalogue (2016).

11SPECIAL TOPIC OF AUSTRALIAN TAX LAW

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.