HA3042 Taxation Law Assignment: FBT, Capital Gains, and Tax Liability

VerifiedAdded on 2023/03/23

|8

|2586

|47

Homework Assignment

AI Summary

This assignment solution addresses two key areas of Australian taxation law: Fringe Benefit Tax (FBT) and Capital Gains Tax (CGT). Question 1 focuses on calculating Spiceco Pty Ltd's FBT liability for a car fringe benefit provided to Lucinda for the 2018/19 FBT year, including depreciation, operating costs, and taxable value calculations, culminating in the determination of the FBT liability. Question 2 delves into Daniel's capital gains and losses from the disposal of various assets, including a house (main residence exemption), a painting (collectible), a luxury yacht (personal use asset), and shares. The analysis includes determining the net capital gains or losses, applying relevant CGT rules, and discussing tax implications, including the discount method and loss carry-forward provisions. The solution demonstrates a comprehensive understanding of relevant tax legislation and its application to specific scenarios.

TAXATION LAW

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

The focus is to compute the Fringe Benefit Tax (FBT) liability for employer Spiceco

Pty Ltd with respect to the provided car fringe benefit to Lucinda. Further, the FBT

liability would be determined for Spiceco Pty Ltd for FBT year 2018/19.

Calculation of depreciation

The depreciation of the car would be determined through the following formula stated

in “s. 11-1, Fringe Benefit Tax Assessment Act 1986” (Krever, 2017).

Depreciation= ABC

D

Where,

A = (a) When car is purchased by person; Car value at the beginning of tax year –

depreciated value of car at that moment

(b) In any other case;Cost price of car

B = Amount worked for person and for car computed through subsection 1AA

C = Car usage days for fringe benefit tax year for employee

D = Total days in fringe benefit tax year

It is noteworthy that an effective car life is assumed as 8 years and the diminishing

depreciation is considered as 25% per annum. Spiceco Pty Ltd has provided car to

Lucinda on April 1, 2018 which represented that variable C and D would be 365 days

only. The variable A would be same as $18,000 i.e. cost of car and B would be 0.25.

Depreciation of car for FY 218 /19= ABC

D = 18000∗0.25∗365

365 =$ 4500

Calculation of interest

Depreciation= ABC

D

All the above shown variables would be same as earlier except variable B. Here, the

B represent the statutory rate of interest of car for the given FBT year. According to

TD2018/2, the applicable interest rate would be 5.20% (Barkoczy, 2018).

Depreciation of car for FY 2018 /19= ABC

D = 18000∗5.2 %∗365

365 =$ 936

Operating costs

Operating costs of car for FY 2018/19 is computed through ss. 10-3 FBTAA 1986

and is shown below.

Repairs cost $3300

Insurance cost $2200

Fuel cost $990

Depreciation amount $4500

2

The focus is to compute the Fringe Benefit Tax (FBT) liability for employer Spiceco

Pty Ltd with respect to the provided car fringe benefit to Lucinda. Further, the FBT

liability would be determined for Spiceco Pty Ltd for FBT year 2018/19.

Calculation of depreciation

The depreciation of the car would be determined through the following formula stated

in “s. 11-1, Fringe Benefit Tax Assessment Act 1986” (Krever, 2017).

Depreciation= ABC

D

Where,

A = (a) When car is purchased by person; Car value at the beginning of tax year –

depreciated value of car at that moment

(b) In any other case;Cost price of car

B = Amount worked for person and for car computed through subsection 1AA

C = Car usage days for fringe benefit tax year for employee

D = Total days in fringe benefit tax year

It is noteworthy that an effective car life is assumed as 8 years and the diminishing

depreciation is considered as 25% per annum. Spiceco Pty Ltd has provided car to

Lucinda on April 1, 2018 which represented that variable C and D would be 365 days

only. The variable A would be same as $18,000 i.e. cost of car and B would be 0.25.

Depreciation of car for FY 218 /19= ABC

D = 18000∗0.25∗365

365 =$ 4500

Calculation of interest

Depreciation= ABC

D

All the above shown variables would be same as earlier except variable B. Here, the

B represent the statutory rate of interest of car for the given FBT year. According to

TD2018/2, the applicable interest rate would be 5.20% (Barkoczy, 2018).

Depreciation of car for FY 2018 /19= ABC

D = 18000∗5.2 %∗365

365 =$ 936

Operating costs

Operating costs of car for FY 2018/19 is computed through ss. 10-3 FBTAA 1986

and is shown below.

Repairs cost $3300

Insurance cost $2200

Fuel cost $990

Depreciation amount $4500

2

Interest amount $936

Operating cost = 3300+2200+990+4500+936

= $11,926

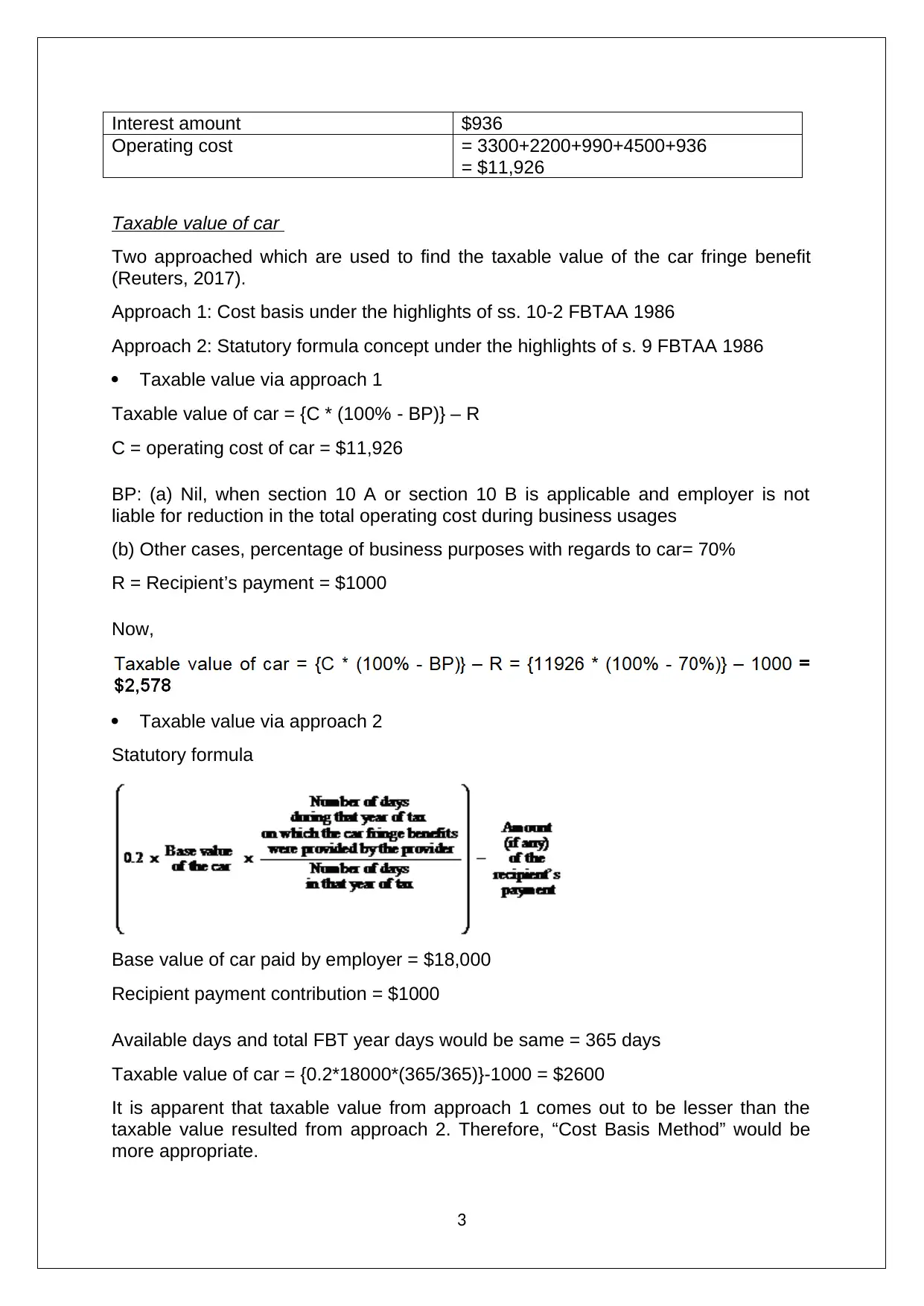

Taxable value of car

Two approached which are used to find the taxable value of the car fringe benefit

(Reuters, 2017).

Approach 1: Cost basis under the highlights of ss. 10-2 FBTAA 1986

Approach 2: Statutory formula concept under the highlights of s. 9 FBTAA 1986

Taxable value via approach 1

Taxable value of car = {C * (100% - BP)} – R

C = operating cost of car = $11,926

BP: (a) Nil, when section 10 A or section 10 B is applicable and employer is not

liable for reduction in the total operating cost during business usages

(b) Other cases, percentage of business purposes with regards to car= 70%

R = Recipient’s payment = $1000

Now,

Taxable value via approach 2

Statutory formula

Base value of car paid by employer = $18,000

Recipient payment contribution = $1000

Available days and total FBT year days would be same = 365 days

Taxable value of car = {0.2*18000*(365/365)}-1000 = $2600

It is apparent that taxable value from approach 1 comes out to be lesser than the

taxable value resulted from approach 2. Therefore, “Cost Basis Method” would be

more appropriate.

3

Operating cost = 3300+2200+990+4500+936

= $11,926

Taxable value of car

Two approached which are used to find the taxable value of the car fringe benefit

(Reuters, 2017).

Approach 1: Cost basis under the highlights of ss. 10-2 FBTAA 1986

Approach 2: Statutory formula concept under the highlights of s. 9 FBTAA 1986

Taxable value via approach 1

Taxable value of car = {C * (100% - BP)} – R

C = operating cost of car = $11,926

BP: (a) Nil, when section 10 A or section 10 B is applicable and employer is not

liable for reduction in the total operating cost during business usages

(b) Other cases, percentage of business purposes with regards to car= 70%

R = Recipient’s payment = $1000

Now,

Taxable value via approach 2

Statutory formula

Base value of car paid by employer = $18,000

Recipient payment contribution = $1000

Available days and total FBT year days would be same = 365 days

Taxable value of car = {0.2*18000*(365/365)}-1000 = $2600

It is apparent that taxable value from approach 1 comes out to be lesser than the

taxable value resulted from approach 2. Therefore, “Cost Basis Method” would be

more appropriate.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FBT liability

Grossed up taxable value will be determined by multiplying the taxable value of car

with the respective value of gross up factor. GST is applicable on the car and it

categorised as type 1 good and hence, the gross up factor for car for FY 2018/19 will

be 2.0802 (ATO, 2019).

Grossed up taxable value = Taxable value of car * Gross up factor

Grossed up taxable value = 2578*2.0802 =$5362.34

The computed grossed up taxable value then multiplies with the applicable FBT rate

in order to get the net FBT liability for car fringe benefits for employer (Deutsch et.

al., 2016).

The FBT rate for FY 2018/19 comes out to be 47% and thus (ATO, 2019),

FBT liability = Grossed up taxable value * FBT rate = 5362.34*47% = $2520.3

Hence, Spiceco Pty Ltd has a net FBT liability of $2520.3 for car fringe benefits

extended to employee Lucinda.

Question 2

(a) The main focus is to determine the net capital gains or capital losses from the

disposal of the capital assets which Daniel has sold in the FY 2018/19 in the

process of deriving capital for his fund. The objective here is to analyse each of

the transaction of sale for the asset so as to find the net capital gains/losses

under the highlights of relevant statutory law.

Transaction 1: Disposal of house

The key aspect in regards to disposal of the house is to determine whether it is the

main residence of the taxpayer or not. This is because if the taxpayer has disposed

his main residence then Sub-division 118-B would be applied and main residence

exemption would be enforceable due to which no CGT implication would be raised

on the capital gains derived from disposal. Also, it is noteworthy the residence must

not be used for deriving assessable income for taxpayer and the residence must be

the main residential place of taxpayer during the complete period of ownership

(Coleman,2016).

In present scenario, Daniel’s main residence is the house located in Doncaster for

the entire period of ownership (30 years). Further, there is no evidence which reflects

that he has used the main residence for assessable income generation and

therefore, it would be fair to say that the house is the main residence of Daniel.

Hence, the capital gains derived from the sale of main residence would not be taxed.

Thereby, the advance payment of $85000 will be realised and the capital gains

derived from the house would not be taxable under main residence exemption

available under Sub-division 118-B.

Transaction 2: Disposal of painting

4

Grossed up taxable value will be determined by multiplying the taxable value of car

with the respective value of gross up factor. GST is applicable on the car and it

categorised as type 1 good and hence, the gross up factor for car for FY 2018/19 will

be 2.0802 (ATO, 2019).

Grossed up taxable value = Taxable value of car * Gross up factor

Grossed up taxable value = 2578*2.0802 =$5362.34

The computed grossed up taxable value then multiplies with the applicable FBT rate

in order to get the net FBT liability for car fringe benefits for employer (Deutsch et.

al., 2016).

The FBT rate for FY 2018/19 comes out to be 47% and thus (ATO, 2019),

FBT liability = Grossed up taxable value * FBT rate = 5362.34*47% = $2520.3

Hence, Spiceco Pty Ltd has a net FBT liability of $2520.3 for car fringe benefits

extended to employee Lucinda.

Question 2

(a) The main focus is to determine the net capital gains or capital losses from the

disposal of the capital assets which Daniel has sold in the FY 2018/19 in the

process of deriving capital for his fund. The objective here is to analyse each of

the transaction of sale for the asset so as to find the net capital gains/losses

under the highlights of relevant statutory law.

Transaction 1: Disposal of house

The key aspect in regards to disposal of the house is to determine whether it is the

main residence of the taxpayer or not. This is because if the taxpayer has disposed

his main residence then Sub-division 118-B would be applied and main residence

exemption would be enforceable due to which no CGT implication would be raised

on the capital gains derived from disposal. Also, it is noteworthy the residence must

not be used for deriving assessable income for taxpayer and the residence must be

the main residential place of taxpayer during the complete period of ownership

(Coleman,2016).

In present scenario, Daniel’s main residence is the house located in Doncaster for

the entire period of ownership (30 years). Further, there is no evidence which reflects

that he has used the main residence for assessable income generation and

therefore, it would be fair to say that the house is the main residence of Daniel.

Hence, the capital gains derived from the sale of main residence would not be taxed.

Thereby, the advance payment of $85000 will be realised and the capital gains

derived from the house would not be taxable under main residence exemption

available under Sub-division 118-B.

Transaction 2: Disposal of painting

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Paintings are categorised as collectibles as highlighted in ss. 108-10(15) ITAA 1997

and the disposal of collectibles is considered as A1 CGT event as indicated in ss.

104(5) ITAA 1997.This leads to CGT implication on the derived capital gains/losses.

The statutory formula stated in ss. 104(10) ITAA 1997 would be taken into

consideration in order to find the net capital gains/losses from the sale of a collectible

(Barkocy, 2018). The formula states that net capital gains/losses will be determined

after subtracting the cost of the asset from received sale proceeds. However, it is

noteworthy that CGT liability would be levied only when the collectible has been

purchased for more than $500 (Coleman, 2016)p..In this regard, the main aspect is

to check whether the disposed asset belongs to the pre-CGT asset category or not.

It is because CGT will not be levied on taxpayer when he disposed a pre-CGT asset.

Any capital asset of taxpayer which has been bought before the period of September

20, 1985 will be designated as pre-CGT asset as per s.149(10) ITAA 1997 (Austlii,

2019a).

Here, Daniel has purchased painting on September 20, 1985 which means it would

not be categorised as pre-CGT asset. The proceeds received from sale are

$125,000 and cost of purchase is $15,000. The capital gains received from disposal

of painting ($125000 -$15000) = $110,000

Discount method (Division 15 ITAA 1997) would be used for reducing the CGT

liability because painting is a long-term asset (holding periodis more than a year) of

Daniel (Woellner, 2014).

Transaction 3: Disposal of luxury yacht

When the taxpayer disposes his/her personal use asset then some special type of

rules would be used to find the net capital gains or losses. The CGT would be levied

on the capital gains derived from the disposal of personal use asset only when it has

been purchased for more than $10,000. It is essential to note that no CGT

implication would arise when there are capital losses incurred from the disposal of

personal use asset under the highlights of ss. 108-20(1) ITAA 1997. In other words,

the capital loss would be ignored for CGT purpose (Reuters, 2017).

In present case, Daniel has luxury yacht which he has purchased for $1100,000 for

personal usage. There are no facts given which represent that Daniel has used it for

business purposes and thus, it would be categorised as personal use asset only

under ss. 108 – 20(2) ITAA 1997. The statutory formula stated in ss. 104(10) ITAA

1997 would be taken into consideration in order to find the net capital gains/losses

from the sale of a collectible. The formula states that net capital gains/losses will be

determined after subtracting the cost of the asset from received sale proceeds.

Danial has received a net income of $60,000 from disposal and the cost base of

yacht is $110,000. It is apparent that cost bae is higher than the net income which

implies that Daniel has a net capital loss from the disposal of yacht that would be

ignored and no CGT liability would be imposed

Transaction 3: Disposal of shares

Share is also categorised as a capital asset and transaction of disposal of shares is

termed as A1 CGT event under ss. 104-5 ITAA 1997. Cost base of asset and sale

proceeds would be used to find the net capital gains or losses as described in ss.

104-10 ITAA 1997 (Austlii, 2019b).

5

and the disposal of collectibles is considered as A1 CGT event as indicated in ss.

104(5) ITAA 1997.This leads to CGT implication on the derived capital gains/losses.

The statutory formula stated in ss. 104(10) ITAA 1997 would be taken into

consideration in order to find the net capital gains/losses from the sale of a collectible

(Barkocy, 2018). The formula states that net capital gains/losses will be determined

after subtracting the cost of the asset from received sale proceeds. However, it is

noteworthy that CGT liability would be levied only when the collectible has been

purchased for more than $500 (Coleman, 2016)p..In this regard, the main aspect is

to check whether the disposed asset belongs to the pre-CGT asset category or not.

It is because CGT will not be levied on taxpayer when he disposed a pre-CGT asset.

Any capital asset of taxpayer which has been bought before the period of September

20, 1985 will be designated as pre-CGT asset as per s.149(10) ITAA 1997 (Austlii,

2019a).

Here, Daniel has purchased painting on September 20, 1985 which means it would

not be categorised as pre-CGT asset. The proceeds received from sale are

$125,000 and cost of purchase is $15,000. The capital gains received from disposal

of painting ($125000 -$15000) = $110,000

Discount method (Division 15 ITAA 1997) would be used for reducing the CGT

liability because painting is a long-term asset (holding periodis more than a year) of

Daniel (Woellner, 2014).

Transaction 3: Disposal of luxury yacht

When the taxpayer disposes his/her personal use asset then some special type of

rules would be used to find the net capital gains or losses. The CGT would be levied

on the capital gains derived from the disposal of personal use asset only when it has

been purchased for more than $10,000. It is essential to note that no CGT

implication would arise when there are capital losses incurred from the disposal of

personal use asset under the highlights of ss. 108-20(1) ITAA 1997. In other words,

the capital loss would be ignored for CGT purpose (Reuters, 2017).

In present case, Daniel has luxury yacht which he has purchased for $1100,000 for

personal usage. There are no facts given which represent that Daniel has used it for

business purposes and thus, it would be categorised as personal use asset only

under ss. 108 – 20(2) ITAA 1997. The statutory formula stated in ss. 104(10) ITAA

1997 would be taken into consideration in order to find the net capital gains/losses

from the sale of a collectible. The formula states that net capital gains/losses will be

determined after subtracting the cost of the asset from received sale proceeds.

Danial has received a net income of $60,000 from disposal and the cost base of

yacht is $110,000. It is apparent that cost bae is higher than the net income which

implies that Daniel has a net capital loss from the disposal of yacht that would be

ignored and no CGT liability would be imposed

Transaction 3: Disposal of shares

Share is also categorised as a capital asset and transaction of disposal of shares is

termed as A1 CGT event under ss. 104-5 ITAA 1997. Cost base of asset and sale

proceeds would be used to find the net capital gains or losses as described in ss.

104-10 ITAA 1997 (Austlii, 2019b).

5

Cost base of the assets comprises five main elements which needs to be determined

in regards to find the net cost base of asset under s. 110-25(2) ITAA 1997 (Deutsch

et.al., 2016).

Purchase cost of asset

Incidental cost incurred in selling or buying of the asset

Cost incurred in relation to maintain the asset ownership

Capital expenses incurred so as to improve the economic asset value

Capital expenses incurred in relation to maintain the legal title of the asset

Daniel has purchased the shares of BHP for $75,000 and has disposed the shares

for $80,000. The transaction of shares disposal is termed as A1 CGT event and thus,

the net capital gains/losses would be determined as shown below.

Incidental cost = Stamp duty + Brokerage amount = 250+750 = $1000

Purchasing cost = $75,000

Cost related to the share ownership = Interest cost = $5000

Cost base of asset = Incidental cost+Purchasing cost+ cost related to the share

ownership = 75000 +1000 +5000 = $81,000

Proceeds resulted from sale of shares = $80,000

Capital gains = 80000-81000 = -$1,000

Capital gains = -$1,000

Daniel has a net capital loss of $1000 from the sale of shares.

Net Capital Gains/Loses for FY2018/19 for Daniel

Capital gains (Painting) = $110,000

Capital loss (BHP Shares) = -$1000

Previous year loss (AZJ Share sale FY2017/18) = $10,000

Net Capital Gains = 110000 – 1000 – 10000 = $99,000

Daniel has a net capital gains of $99,000 for the transactions incurred during FY

2018/19. The assets were long term assets which indicates that 50% discount would

be available on the capital gains.

Taxable Capital Gains FY 2018/19 = 50% of Net Capital Gains = 50% * 99000

=$44,500

(b) With regards to capital gains made by Daniel, CGT would be payable to the ATO

which would attract the marginal tax rate based on the other assessable income

that Daniel has. Also, it is noteworthy that in case of capital gains, methods such

as cost indexation and discount method can be availed which would help in

lowering the amount of taxable capital gains. The application of discount method

available under Division 15 has been highlighted in part (a) (Barkoczy, 2018).

(c) If there is capital loss derived for the concerned financial year, then it is essential

that the same is carried forward to the future where it can be used to offset any

capital gains which are derived. Capital losses cannot be adjusted against

6

in regards to find the net cost base of asset under s. 110-25(2) ITAA 1997 (Deutsch

et.al., 2016).

Purchase cost of asset

Incidental cost incurred in selling or buying of the asset

Cost incurred in relation to maintain the asset ownership

Capital expenses incurred so as to improve the economic asset value

Capital expenses incurred in relation to maintain the legal title of the asset

Daniel has purchased the shares of BHP for $75,000 and has disposed the shares

for $80,000. The transaction of shares disposal is termed as A1 CGT event and thus,

the net capital gains/losses would be determined as shown below.

Incidental cost = Stamp duty + Brokerage amount = 250+750 = $1000

Purchasing cost = $75,000

Cost related to the share ownership = Interest cost = $5000

Cost base of asset = Incidental cost+Purchasing cost+ cost related to the share

ownership = 75000 +1000 +5000 = $81,000

Proceeds resulted from sale of shares = $80,000

Capital gains = 80000-81000 = -$1,000

Capital gains = -$1,000

Daniel has a net capital loss of $1000 from the sale of shares.

Net Capital Gains/Loses for FY2018/19 for Daniel

Capital gains (Painting) = $110,000

Capital loss (BHP Shares) = -$1000

Previous year loss (AZJ Share sale FY2017/18) = $10,000

Net Capital Gains = 110000 – 1000 – 10000 = $99,000

Daniel has a net capital gains of $99,000 for the transactions incurred during FY

2018/19. The assets were long term assets which indicates that 50% discount would

be available on the capital gains.

Taxable Capital Gains FY 2018/19 = 50% of Net Capital Gains = 50% * 99000

=$44,500

(b) With regards to capital gains made by Daniel, CGT would be payable to the ATO

which would attract the marginal tax rate based on the other assessable income

that Daniel has. Also, it is noteworthy that in case of capital gains, methods such

as cost indexation and discount method can be availed which would help in

lowering the amount of taxable capital gains. The application of discount method

available under Division 15 has been highlighted in part (a) (Barkoczy, 2018).

(c) If there is capital loss derived for the concerned financial year, then it is essential

that the same is carried forward to the future where it can be used to offset any

capital gains which are derived. Capital losses cannot be adjusted against

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

revenue receipts either in the current year or in the future years. Further, with

regards to losses for particular asset classes, there are special norms such as

loss on personal use assets to be discarded, collectible based capital losses to

be only adjusted against capital gains derived from sale of collectible assets

(Nethercott, Richardsonand Devos, 2016).

7

regards to losses for particular asset classes, there are special norms such as

loss on personal use assets to be discarded, collectible based capital losses to

be only adjusted against capital gains derived from sale of collectible assets

(Nethercott, Richardsonand Devos, 2016).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

ATO (2019) Fringe benefits tax – rates and thresholds, [online] Available at

https://www.ato.gov.au/Rates/FBT/[Assessed May 25, 2019]

Austlii (2019a) , INCOME TAX ASSESSMENT ACT 1997 - SECT 149.10, [online]

available at http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s149.10.html[Accessed May 26, 2019]

Austlii (2019b) , INCOME TAX ASSESSMENT ACT 1997 - SECT 105.10, [online]

available at http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s105.10.html [Accessed May 26, 2019]

Barkoczy, S. (2018), Foundation of Taxation Law 2018, 9thed.,NorthRyde: CCH

Publications, pp. 231, 320-321

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters

(Professional) Australia, pp. 189

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016), Australian

tax handbook 8th ed., Pymont: Thomson Reuters, pp.189, 345

Nethercott, L., Richardson, G. and Devos, K. (2016), Australian Taxation Study

Manual 2016, 4th ed., Sydney: Oxford University Press, pp. 231, 345

Krever, R. (2017) Australian Taxation Law Cases 2017.2nd ed. Brisbane: THOMSON

LAWBOOK Company, pp. 178, 299-300

Reuters, T. (2017) Australian Tax Legislation (2017).4th ed. Sydney.THOMSON

REUTERS, pp. 189,342-343

Woellner, R (2014), Australian taxation law 2014, 7th ed., North Ryde: CCH Australia,

pp. 187, 267

8

ATO (2019) Fringe benefits tax – rates and thresholds, [online] Available at

https://www.ato.gov.au/Rates/FBT/[Assessed May 25, 2019]

Austlii (2019a) , INCOME TAX ASSESSMENT ACT 1997 - SECT 149.10, [online]

available at http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s149.10.html[Accessed May 26, 2019]

Austlii (2019b) , INCOME TAX ASSESSMENT ACT 1997 - SECT 105.10, [online]

available at http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s105.10.html [Accessed May 26, 2019]

Barkoczy, S. (2018), Foundation of Taxation Law 2018, 9thed.,NorthRyde: CCH

Publications, pp. 231, 320-321

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters

(Professional) Australia, pp. 189

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016), Australian

tax handbook 8th ed., Pymont: Thomson Reuters, pp.189, 345

Nethercott, L., Richardson, G. and Devos, K. (2016), Australian Taxation Study

Manual 2016, 4th ed., Sydney: Oxford University Press, pp. 231, 345

Krever, R. (2017) Australian Taxation Law Cases 2017.2nd ed. Brisbane: THOMSON

LAWBOOK Company, pp. 178, 299-300

Reuters, T. (2017) Australian Tax Legislation (2017).4th ed. Sydney.THOMSON

REUTERS, pp. 189,342-343

Woellner, R (2014), Australian taxation law 2014, 7th ed., North Ryde: CCH Australia,

pp. 187, 267

8

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.