THE AUSTRALIAN TAXATION LAW

VerifiedAdded on 2022/09/03

|12

|2731

|17

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: AUSTRALIAN TAXATION LAW

Australian Taxation Law

Name of the Student:

Name of the University:

Author Note:

Australian Taxation Law

Name of the Student:

Name of the University:

Author Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

AUSTRALIAN TAXATION LAW

Table of Contents

Answer to question 1...........................................................................................................2

Answer to question 2...........................................................................................................6

Reference list.......................................................................................................................9

AUSTRALIAN TAXATION LAW

Table of Contents

Answer to question 1...........................................................................................................2

Answer to question 2...........................................................................................................6

Reference list.......................................................................................................................9

2

AUSTRALIAN TAXATION LAW

Answer to question 1

From the sale of capital asset when any profit or loss arises, it is known as the capital

gain or capital loss. With the rise of capital gain, taxpayer has to pay tax which is known as

capital gain tax. It can be a short-term or long-term gain or loss. It is usually the difference

between the cost paid and the cost of sell. Both capital gain and losses is need to be reported in

the income tax return and if any gain is arise then tax on it has to be paid. When capital gain

arises it is added to the assessable income to make the taxable income. If capital loss arises then

the taxpayer cannot claim it against any other income but it can used to reduce the capital gain.

All assets, which are acquired before the tax on capital gain started which is 20th September

1985, are exempted from the capital gain tax (Grudnoff 2015).

Issues: Sophia sales some of her capital assets in the financial year 2018 which consist of a

block of land, shares, stamps and a piano. The block of land which was purchased by Sophia in

1991 as an investment and made some expenses to purchase the land. She also took bank loon

for the purpose of purchase. Before selling the property she had made some expenses to make

the land sellable. Shares of ABC co. that was purchased by Sophia in 1993 is sold by paying 1

percent brokerage. Then Sophia’s stamp collection has been sold in an auction which she has

brought in 2018 after paying certain amount of auction fees. She also sold a guitar which she has

brought in 2003.

Law: Capital gain tax is applicable on all the capital assets which includes real estate, shares,

investments, crypto currencies, goodwill, collectable items, foreign currency and personal assets

of certain values (Evans, Minas and Lim 2015). Capital gain tax is applicable to all the Australian

resident assets which is situated anywhere in the world and for the Norfolk Island resident capital

AUSTRALIAN TAXATION LAW

Answer to question 1

From the sale of capital asset when any profit or loss arises, it is known as the capital

gain or capital loss. With the rise of capital gain, taxpayer has to pay tax which is known as

capital gain tax. It can be a short-term or long-term gain or loss. It is usually the difference

between the cost paid and the cost of sell. Both capital gain and losses is need to be reported in

the income tax return and if any gain is arise then tax on it has to be paid. When capital gain

arises it is added to the assessable income to make the taxable income. If capital loss arises then

the taxpayer cannot claim it against any other income but it can used to reduce the capital gain.

All assets, which are acquired before the tax on capital gain started which is 20th September

1985, are exempted from the capital gain tax (Grudnoff 2015).

Issues: Sophia sales some of her capital assets in the financial year 2018 which consist of a

block of land, shares, stamps and a piano. The block of land which was purchased by Sophia in

1991 as an investment and made some expenses to purchase the land. She also took bank loon

for the purpose of purchase. Before selling the property she had made some expenses to make

the land sellable. Shares of ABC co. that was purchased by Sophia in 1993 is sold by paying 1

percent brokerage. Then Sophia’s stamp collection has been sold in an auction which she has

brought in 2018 after paying certain amount of auction fees. She also sold a guitar which she has

brought in 2003.

Law: Capital gain tax is applicable on all the capital assets which includes real estate, shares,

investments, crypto currencies, goodwill, collectable items, foreign currency and personal assets

of certain values (Evans, Minas and Lim 2015). Capital gain tax is applicable to all the Australian

resident assets which is situated anywhere in the world and for the Norfolk Island resident capital

3

AUSTRALIAN TAXATION LAW

gain tax is applicable if the asset is purchased from 23rd October 2015. Capital gain tax is also

applicable to the foreign resident if the capital gain has been arise from the sale of Australian

taxable property. Capital gain or loss for an asset is need to be reported in the tax return of the

year when the taxpayer enters into the contract to sell the investment property rather than when

the asset is originally disposed off (Burkhauser, Hahn and Wilkins 2015). However, some of the

capital assets are exempted from the capital gain tax which are as follows:

Personal assets which includes residential property, car and personnel furniture.

Depreciable assets which is solely used for the taxable purpose

Assets which are acquired before 20th September 1985

Personnel assets which is acquired with the amount less than $10000

Collectable items whose value is less than $500

Motor vehicle that is designed to carry goods of less than 1 ton and nine passengers

Taxpayer need to keep record of all his capital assets and maintain all the transaction related to it

in order to calculate the capital gain tax. Purchase price and the selling price is an essential data

which is needed to calculate the capital gain or loss. Purchase price of the asset includes all the

cost which is paid for the asset during its buying and selling. Once the purchase price is

determined then few methods are used to calculate the capital gain tax. These are the three

method which is used to calculating capital gain:

1. Discounting method – This method is applicable when the taxpayer holds the asset for

more than 12 month. Under this method, capital gain is calculated by reducing the entire

cost and 50 percent discount from the selling price (Blunden, H., 2016). This method is

applicable only for the individual who did not choose the indexation method, but non-

AUSTRALIAN TAXATION LAW

gain tax is applicable if the asset is purchased from 23rd October 2015. Capital gain tax is also

applicable to the foreign resident if the capital gain has been arise from the sale of Australian

taxable property. Capital gain or loss for an asset is need to be reported in the tax return of the

year when the taxpayer enters into the contract to sell the investment property rather than when

the asset is originally disposed off (Burkhauser, Hahn and Wilkins 2015). However, some of the

capital assets are exempted from the capital gain tax which are as follows:

Personal assets which includes residential property, car and personnel furniture.

Depreciable assets which is solely used for the taxable purpose

Assets which are acquired before 20th September 1985

Personnel assets which is acquired with the amount less than $10000

Collectable items whose value is less than $500

Motor vehicle that is designed to carry goods of less than 1 ton and nine passengers

Taxpayer need to keep record of all his capital assets and maintain all the transaction related to it

in order to calculate the capital gain tax. Purchase price and the selling price is an essential data

which is needed to calculate the capital gain or loss. Purchase price of the asset includes all the

cost which is paid for the asset during its buying and selling. Once the purchase price is

determined then few methods are used to calculate the capital gain tax. These are the three

method which is used to calculating capital gain:

1. Discounting method – This method is applicable when the taxpayer holds the asset for

more than 12 month. Under this method, capital gain is calculated by reducing the entire

cost and 50 percent discount from the selling price (Blunden, H., 2016). This method is

applicable only for the individual who did not choose the indexation method, but non-

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

AUSTRALIAN TAXATION LAW

resident can also apply for this after removing the discount rule. Companies cannot avail

this discount method as they pays 30 percent tax on the net capital gain.

2. Indexation method – This method is eligible when the asset is held for more than 12

month or the asset has been acquired before 21st September 1999. This method helps to

increase the cost base of the asset by applying the price index method. It is calculated by

deducting the index cost from the sale price to get the capital gain. This method is

applicable for company and also individual if they fulfill the condition (Minas, Lim and

Evans 2018).

3. Others method – This method is applicable when the asset is held for less than 12 month

and it is the simplest method of all other method of calculating capital gain. It is

calculated by deducting the cost from the sale price.

Application: Sofia block of land is eligible for the capital gain as it fulfills all the requirement.

Purchase price consist of interest on borrowing, council rate, insurance and legal disputes as it

make the total cost of purchase. Then all eligible capital cost are deducted which includes stamp

duty, advertising charges, legal fees and other expense which is required to make the land

saleable. Then the eligible discount at the rate of 50 percent is deducted as the asset is hold by

Sophia for more than 12 month and she is an Australian resident. From the sale of shares Sophia

earned the capital gain which is not form the part of capital gain tax as it was purchased in 1983.

From the sale of stamps and guitar, Sophia has incurred capital loss which is need to be adjusted

with the other capital gain items.

Conclusion: Sophia is an Australian resident made capital gain which is eligible for capital gain.

Capital losses which are incurred from the sale of stamps and Guitar are reduced with the capital

gain earned from the sale of land. While the sale of shares is ineligible for the capital gain tax

AUSTRALIAN TAXATION LAW

resident can also apply for this after removing the discount rule. Companies cannot avail

this discount method as they pays 30 percent tax on the net capital gain.

2. Indexation method – This method is eligible when the asset is held for more than 12

month or the asset has been acquired before 21st September 1999. This method helps to

increase the cost base of the asset by applying the price index method. It is calculated by

deducting the index cost from the sale price to get the capital gain. This method is

applicable for company and also individual if they fulfill the condition (Minas, Lim and

Evans 2018).

3. Others method – This method is applicable when the asset is held for less than 12 month

and it is the simplest method of all other method of calculating capital gain. It is

calculated by deducting the cost from the sale price.

Application: Sofia block of land is eligible for the capital gain as it fulfills all the requirement.

Purchase price consist of interest on borrowing, council rate, insurance and legal disputes as it

make the total cost of purchase. Then all eligible capital cost are deducted which includes stamp

duty, advertising charges, legal fees and other expense which is required to make the land

saleable. Then the eligible discount at the rate of 50 percent is deducted as the asset is hold by

Sophia for more than 12 month and she is an Australian resident. From the sale of shares Sophia

earned the capital gain which is not form the part of capital gain tax as it was purchased in 1983.

From the sale of stamps and guitar, Sophia has incurred capital loss which is need to be adjusted

with the other capital gain items.

Conclusion: Sophia is an Australian resident made capital gain which is eligible for capital gain.

Capital losses which are incurred from the sale of stamps and Guitar are reduced with the capital

gain earned from the sale of land. While the sale of shares is ineligible for the capital gain tax

5

AUSTRALIAN TAXATION LAW

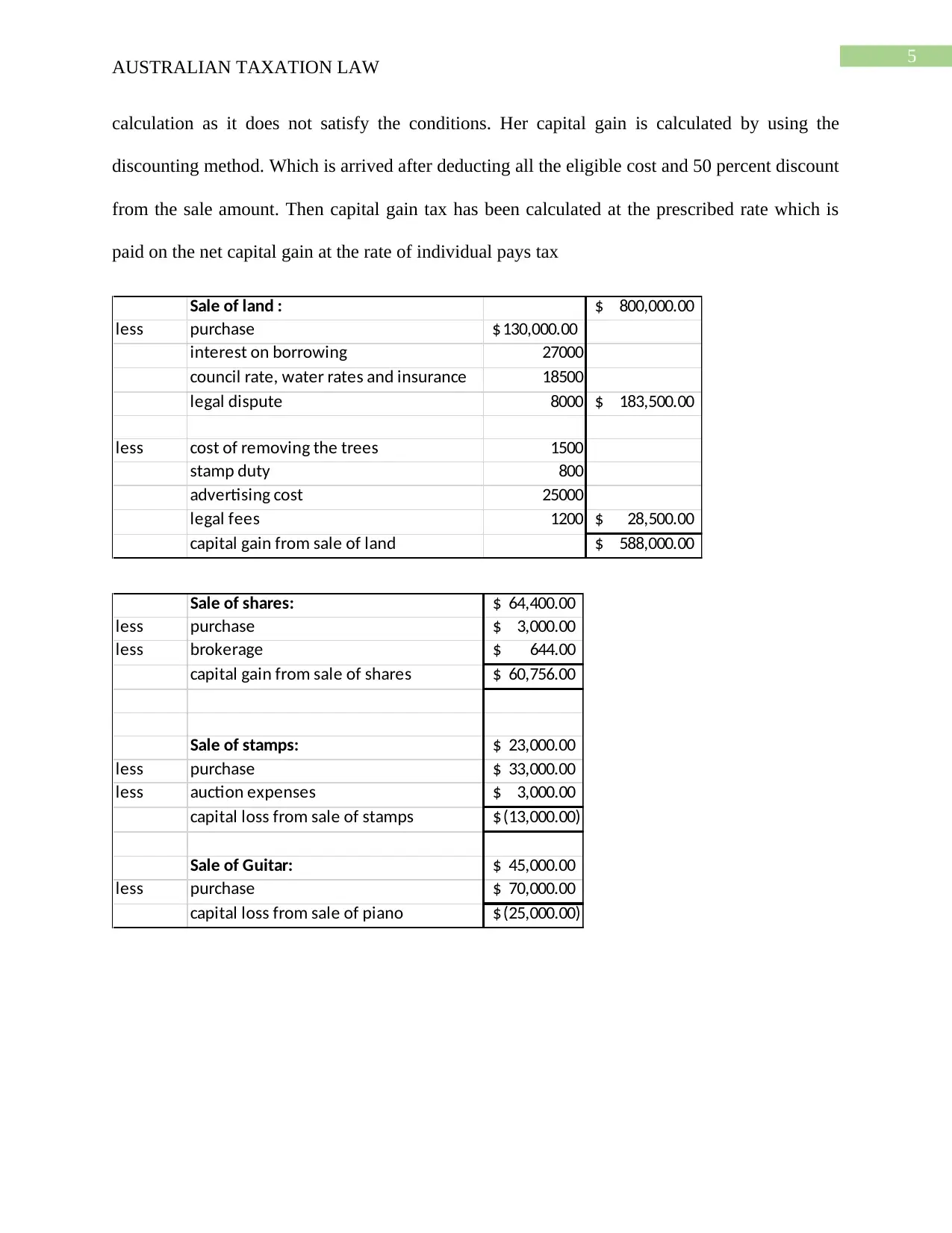

calculation as it does not satisfy the conditions. Her capital gain is calculated by using the

discounting method. Which is arrived after deducting all the eligible cost and 50 percent discount

from the sale amount. Then capital gain tax has been calculated at the prescribed rate which is

paid on the net capital gain at the rate of individual pays tax

Sale of land : 800,000.00$

less purchase 130,000.00$

interest on borrowing 27000

council rate, water rates and insurance 18500

legal dispute 8000 183,500.00$

less cost of removing the trees 1500

stamp duty 800

advertising cost 25000

legal fees 1200 28,500.00$

capital gain from sale of land 588,000.00$

Sale of shares: 64,400.00$

less purchase 3,000.00$

less brokerage 644.00$

capital gain from sale of shares 60,756.00$

Sale of stamps: 23,000.00$

less purchase 33,000.00$

less auction expenses 3,000.00$

capital loss from sale of stamps (13,000.00)$

Sale of Guitar: 45,000.00$

less purchase 70,000.00$

capital loss from sale of piano (25,000.00)$

AUSTRALIAN TAXATION LAW

calculation as it does not satisfy the conditions. Her capital gain is calculated by using the

discounting method. Which is arrived after deducting all the eligible cost and 50 percent discount

from the sale amount. Then capital gain tax has been calculated at the prescribed rate which is

paid on the net capital gain at the rate of individual pays tax

Sale of land : 800,000.00$

less purchase 130,000.00$

interest on borrowing 27000

council rate, water rates and insurance 18500

legal dispute 8000 183,500.00$

less cost of removing the trees 1500

stamp duty 800

advertising cost 25000

legal fees 1200 28,500.00$

capital gain from sale of land 588,000.00$

Sale of shares: 64,400.00$

less purchase 3,000.00$

less brokerage 644.00$

capital gain from sale of shares 60,756.00$

Sale of stamps: 23,000.00$

less purchase 33,000.00$

less auction expenses 3,000.00$

capital loss from sale of stamps (13,000.00)$

Sale of Guitar: 45,000.00$

less purchase 70,000.00$

capital loss from sale of piano (25,000.00)$

6

AUSTRALIAN TAXATION LAW

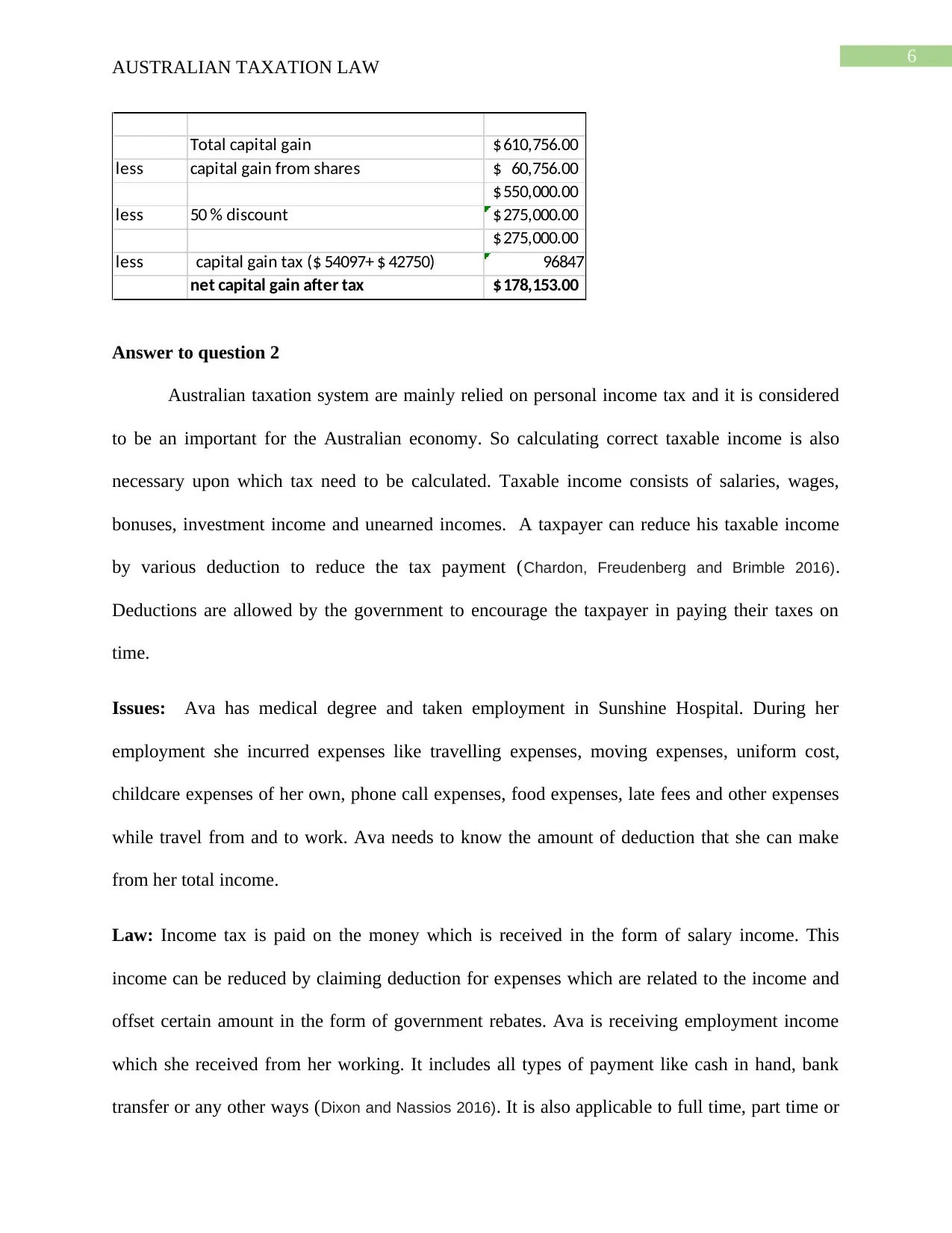

Total capital gain 610,756.00$

less capital gain from shares 60,756.00$

550,000.00$

less 50 % discount 275,000.00$

275,000.00$

less capital gain tax ($ 54097+ $ 42750) 96847

net capital gain after tax 178,153.00$

Answer to question 2

Australian taxation system are mainly relied on personal income tax and it is considered

to be an important for the Australian economy. So calculating correct taxable income is also

necessary upon which tax need to be calculated. Taxable income consists of salaries, wages,

bonuses, investment income and unearned incomes. A taxpayer can reduce his taxable income

by various deduction to reduce the tax payment (Chardon, Freudenberg and Brimble 2016).

Deductions are allowed by the government to encourage the taxpayer in paying their taxes on

time.

Issues: Ava has medical degree and taken employment in Sunshine Hospital. During her

employment she incurred expenses like travelling expenses, moving expenses, uniform cost,

childcare expenses of her own, phone call expenses, food expenses, late fees and other expenses

while travel from and to work. Ava needs to know the amount of deduction that she can make

from her total income.

Law: Income tax is paid on the money which is received in the form of salary income. This

income can be reduced by claiming deduction for expenses which are related to the income and

offset certain amount in the form of government rebates. Ava is receiving employment income

which she received from her working. It includes all types of payment like cash in hand, bank

transfer or any other ways (Dixon and Nassios 2016). It is also applicable to full time, part time or

AUSTRALIAN TAXATION LAW

Total capital gain 610,756.00$

less capital gain from shares 60,756.00$

550,000.00$

less 50 % discount 275,000.00$

275,000.00$

less capital gain tax ($ 54097+ $ 42750) 96847

net capital gain after tax 178,153.00$

Answer to question 2

Australian taxation system are mainly relied on personal income tax and it is considered

to be an important for the Australian economy. So calculating correct taxable income is also

necessary upon which tax need to be calculated. Taxable income consists of salaries, wages,

bonuses, investment income and unearned incomes. A taxpayer can reduce his taxable income

by various deduction to reduce the tax payment (Chardon, Freudenberg and Brimble 2016).

Deductions are allowed by the government to encourage the taxpayer in paying their taxes on

time.

Issues: Ava has medical degree and taken employment in Sunshine Hospital. During her

employment she incurred expenses like travelling expenses, moving expenses, uniform cost,

childcare expenses of her own, phone call expenses, food expenses, late fees and other expenses

while travel from and to work. Ava needs to know the amount of deduction that she can make

from her total income.

Law: Income tax is paid on the money which is received in the form of salary income. This

income can be reduced by claiming deduction for expenses which are related to the income and

offset certain amount in the form of government rebates. Ava is receiving employment income

which she received from her working. It includes all types of payment like cash in hand, bank

transfer or any other ways (Dixon and Nassios 2016). It is also applicable to full time, part time or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUSTRALIAN TAXATION LAW

casual jobs as the basic condition is the employment income which must be included in the tax

return. According to the income tax incomes which is needed to be declared in the income

statement as income are employment salary or wages, pensions, annuities, investment income,

trust income, foreign income and some other incomes.

While computing taxable income taxpayer can claim the deduction for the expenses

which are directly related to the income earned. The condition for claiming deduction which is

work related is that the money must be spent by the taxpayer himself and it must not be

reimbursed by the employer, expenses must be directly related to the income earned by the

taxpayer and there must be some record to prove the expenses made by the taxpayer. If the

expense is related to both work and personnel purpose than the deduction is allowed for the

expenses which is related to the work. Deduction like vehicle expenses, clothing expenses,

travelling expenses, home or office expenses, education of self expenses and work related

expenses could be claimed as expenses which is directly related to the work. If the taxpayer has

not received any income until the next financial year but he incurred some expenses in the

current year then the taxpayer can avail the benefit of claiming the deduction in the next financial

year for the expenses incurred in the current year. Employing someone to assist in the taxpayer

employment can be claimed as expenses by the taxpayer as work related expenses (Datt and

Keating 2018). Some tax offsets which can be directly reduced from the taxable amount like

health insurance, any government benefit, low-income earner, income tests, any medical

expenses and any other tax offset.

Application: Ava traveling expenses to sunshine hospital for the job interview is not deductible

as it is related to personal expenses. Relocation expenses is not related to the income earned and

it is a private income so it cannot be claimed as deduction. Payment for the white uniform which

AUSTRALIAN TAXATION LAW

casual jobs as the basic condition is the employment income which must be included in the tax

return. According to the income tax incomes which is needed to be declared in the income

statement as income are employment salary or wages, pensions, annuities, investment income,

trust income, foreign income and some other incomes.

While computing taxable income taxpayer can claim the deduction for the expenses

which are directly related to the income earned. The condition for claiming deduction which is

work related is that the money must be spent by the taxpayer himself and it must not be

reimbursed by the employer, expenses must be directly related to the income earned by the

taxpayer and there must be some record to prove the expenses made by the taxpayer. If the

expense is related to both work and personnel purpose than the deduction is allowed for the

expenses which is related to the work. Deduction like vehicle expenses, clothing expenses,

travelling expenses, home or office expenses, education of self expenses and work related

expenses could be claimed as expenses which is directly related to the work. If the taxpayer has

not received any income until the next financial year but he incurred some expenses in the

current year then the taxpayer can avail the benefit of claiming the deduction in the next financial

year for the expenses incurred in the current year. Employing someone to assist in the taxpayer

employment can be claimed as expenses by the taxpayer as work related expenses (Datt and

Keating 2018). Some tax offsets which can be directly reduced from the taxable amount like

health insurance, any government benefit, low-income earner, income tests, any medical

expenses and any other tax offset.

Application: Ava traveling expenses to sunshine hospital for the job interview is not deductible

as it is related to personal expenses. Relocation expenses is not related to the income earned and

it is a private income so it cannot be claimed as deduction. Payment for the white uniform which

8

AUSTRALIAN TAXATION LAW

is compulsory for doctor to wear at work is a claimable deduction for Ava as it is not born by the

employer. Ava expenses as childcare for her daughter cannot be claimed as deduction as it is a

private related expenses. Ava phone call expenses from her home to the hospital to check on the

patient is a claimable deduction if its cost is not born by the employer and Ava must have records

to support the claims. Ava purchased food items from the hospital café during her shift hour

cannot be claimed as deduction as deduction is allowed for overtime meals. She paid late fines

for running late at work cannot be claimed as deduction. Ava cannot claim for deduction in

traveling expenses to and from work as it is considered as private travel. But in some case

deduction can be claimed for travel expenses to and from work.

Conclusion: Earning income as a medical professional or specialist by Ava is need to be

declared as income in the tax return which includes salary, wages, bonus and all allowances. She

can also claim for the deduction which is directly related to her work and the amount must not

have been reimbursed. Ava can claim for deduction only for the uniform expenses and phone call

expenses from her total income as they are related to the income earned by Ava. Other expenses

like relocation expenses and traveling expense for interview is private related so it cannot be

claimed for deduction. Her child care expenses is also private related so it cannot be allowed for

deduction. Food expenses during shift hour is not allowed as deduction but if the food expenses

has been incurred after the shift hour then it can be claimed as deduction. Late fine is considered

as private as expenses as it occurred due to own reasons so it cannot be claimed. Traveling from

and to work is considered as private expenses making it as non-deductible expenses. So Ava can

claim for only $400 as deduction from her total income.

AUSTRALIAN TAXATION LAW

is compulsory for doctor to wear at work is a claimable deduction for Ava as it is not born by the

employer. Ava expenses as childcare for her daughter cannot be claimed as deduction as it is a

private related expenses. Ava phone call expenses from her home to the hospital to check on the

patient is a claimable deduction if its cost is not born by the employer and Ava must have records

to support the claims. Ava purchased food items from the hospital café during her shift hour

cannot be claimed as deduction as deduction is allowed for overtime meals. She paid late fines

for running late at work cannot be claimed as deduction. Ava cannot claim for deduction in

traveling expenses to and from work as it is considered as private travel. But in some case

deduction can be claimed for travel expenses to and from work.

Conclusion: Earning income as a medical professional or specialist by Ava is need to be

declared as income in the tax return which includes salary, wages, bonus and all allowances. She

can also claim for the deduction which is directly related to her work and the amount must not

have been reimbursed. Ava can claim for deduction only for the uniform expenses and phone call

expenses from her total income as they are related to the income earned by Ava. Other expenses

like relocation expenses and traveling expense for interview is private related so it cannot be

claimed for deduction. Her child care expenses is also private related so it cannot be allowed for

deduction. Food expenses during shift hour is not allowed as deduction but if the food expenses

has been incurred after the shift hour then it can be claimed as deduction. Late fine is considered

as private as expenses as it occurred due to own reasons so it cannot be claimed. Traveling from

and to work is considered as private expenses making it as non-deductible expenses. So Ava can

claim for only $400 as deduction from her total income.

9

AUSTRALIAN TAXATION LAW

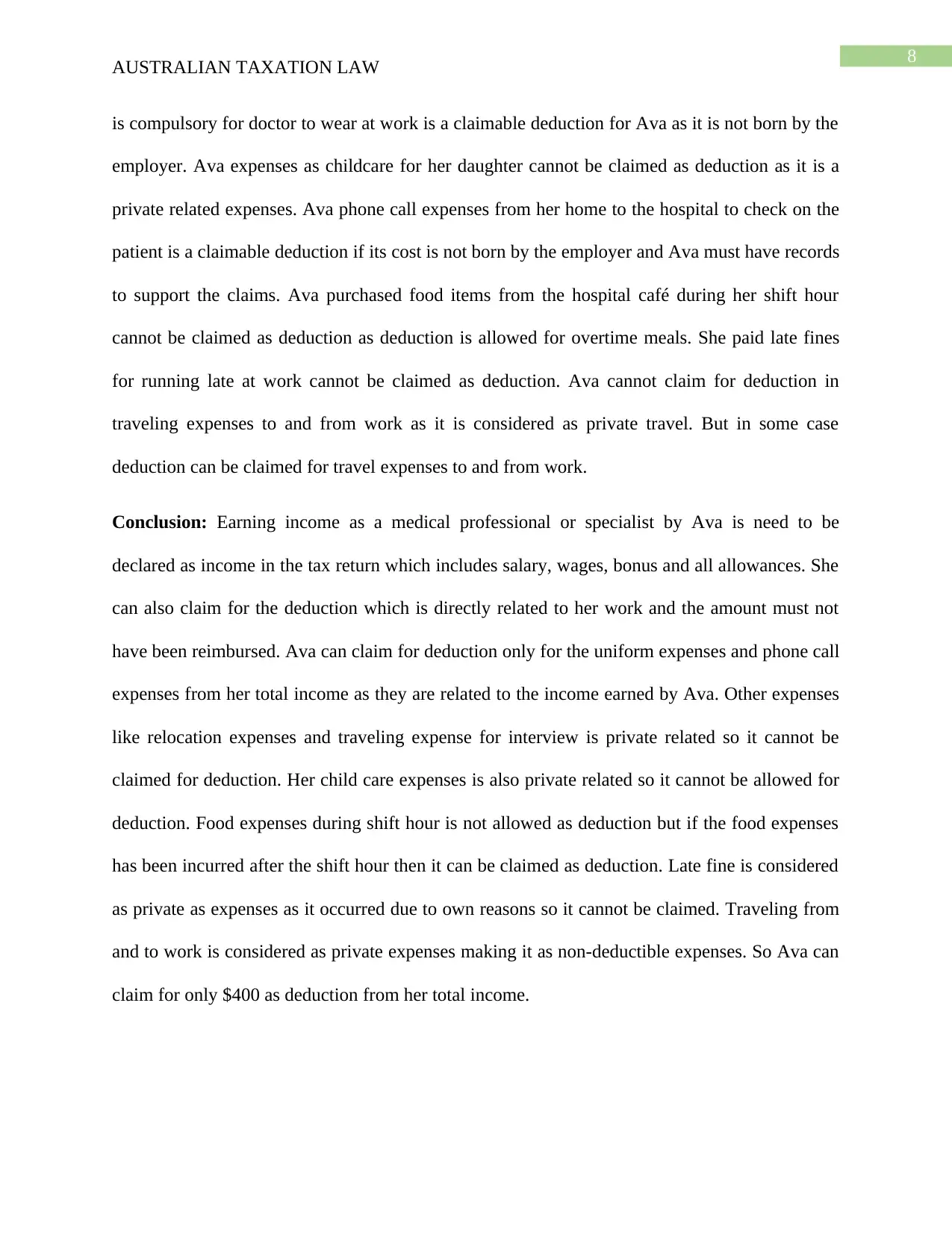

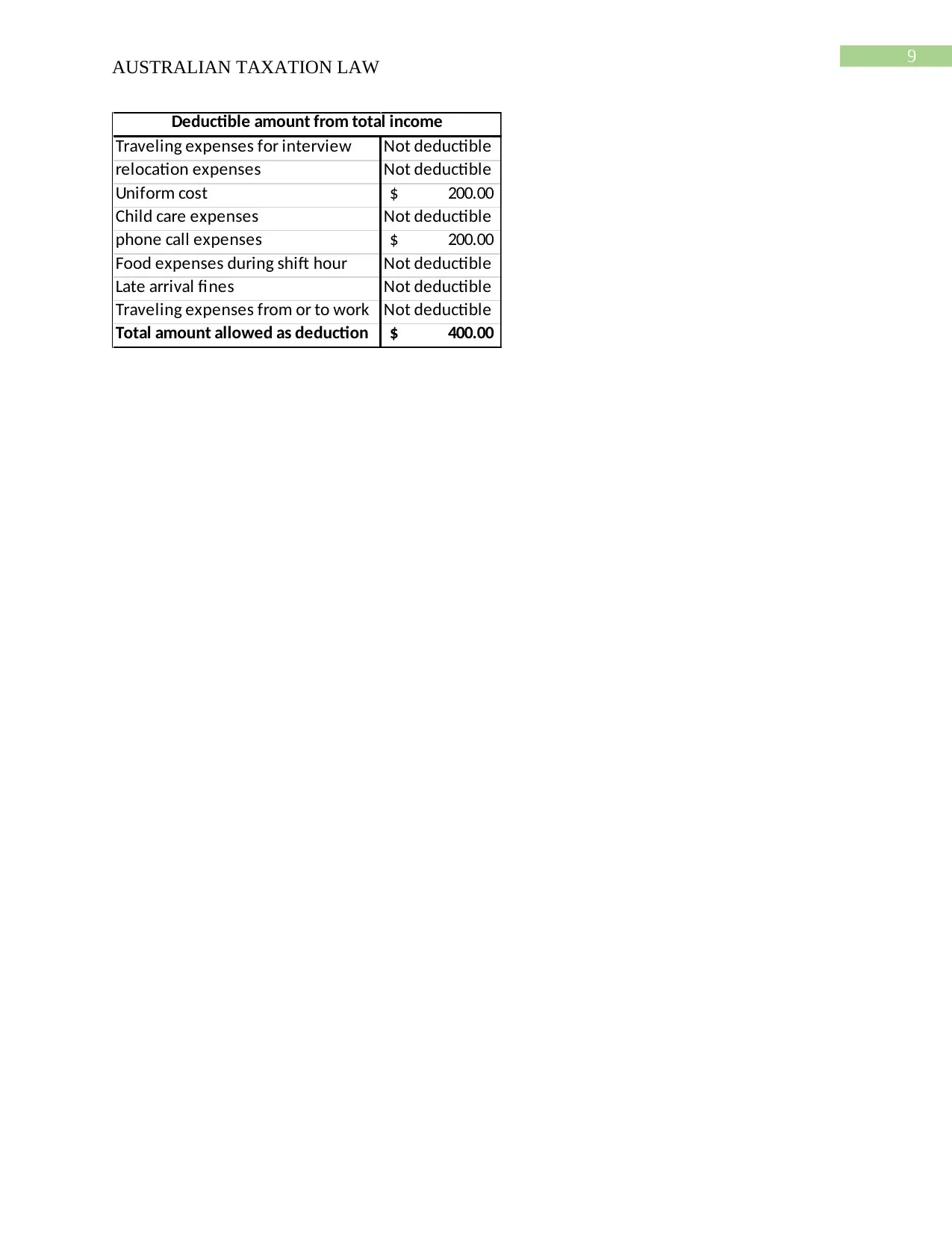

Traveling expenses for interview Not deductible

relocation expenses Not deductible

Uniform cost 200.00$

Child care expenses Not deductible

phone call expenses 200.00$

Food expenses during shift hour Not deductible

Late arrival fines Not deductible

Traveling expenses from or to work Not deductible

Total amount allowed as deduction 400.00$

Deductible amount from total income

AUSTRALIAN TAXATION LAW

Traveling expenses for interview Not deductible

relocation expenses Not deductible

Uniform cost 200.00$

Child care expenses Not deductible

phone call expenses 200.00$

Food expenses during shift hour Not deductible

Late arrival fines Not deductible

Traveling expenses from or to work Not deductible

Total amount allowed as deduction 400.00$

Deductible amount from total income

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

AUSTRALIAN TAXATION LAW

Reference list

Blunden, H., 2016. Discourses around negative gearing of investment properties in

Australia. Housing Studies, 31(3), pp.340-357.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Datt, K.H. and Keating, M., 2018, April. The Commissioner’s obligation to make compensating

adjustments for income tax and GST in Australia and New Zealand. In Australian Tax

Forum (Vol. 33, No. 3).

Dixon, J. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in Australia.

Centre of Policy Studies (CoPS), Victoria University.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An alternative

way forward. Austl. Tax F., 30, p.735.

Grudnoff, M., 2015. Top gears: how negative gearing and the capital gains tax discount benefit

the top 10 per cent and drive up house prices.

Hasseldine, J. and Fatemi, D., 2018. Tax practitioner judgements and client advocacy: the

blurred boundary between capital gains vs. ordinary income. eJTR, 16, p.303.

AUSTRALIAN TAXATION LAW

Reference list

Blunden, H., 2016. Discourses around negative gearing of investment properties in

Australia. Housing Studies, 31(3), pp.340-357.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Datt, K.H. and Keating, M., 2018, April. The Commissioner’s obligation to make compensating

adjustments for income tax and GST in Australia and New Zealand. In Australian Tax

Forum (Vol. 33, No. 3).

Dixon, J. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in Australia.

Centre of Policy Studies (CoPS), Victoria University.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An alternative

way forward. Austl. Tax F., 30, p.735.

Grudnoff, M., 2015. Top gears: how negative gearing and the capital gains tax discount benefit

the top 10 per cent and drive up house prices.

Hasseldine, J. and Fatemi, D., 2018. Tax practitioner judgements and client advocacy: the

blurred boundary between capital gains vs. ordinary income. eJTR, 16, p.303.

11

AUSTRALIAN TAXATION LAW

Mahar, F., 2016. The distortive effects of the capital gains tax regime. Tax Specialist, 20(1),

p.16.

Maleki, B., Sameti, M., Sameti, M. and Ranjbar, H., 2017. The Effect of Capital Gain Tax on

Capital Formation, Financial Development and Economic Growth. Journal of Economic &

Management Perspectives, 11(4), pp.1365-1376.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on capital gains

realisations: evidence from Australia. In Australian Tax Forum (Vol. 33, No. 4).

Mintz, J., Bazel, P., Chen, D. and Crisan, D., 2017. With global company tax reform in the air,

will Australia finally respond?. Minerals Council of Australia, Melbourne, Australia, March.

Warren, N., 2016. E-filing and compliance risk: Evidence from Australian personal income tax

deductions. Austl. Tax F., 31, p.577.

Wilkins, R., 2015. Measuring income inequality in Australia. Australian Economic

Review, 48(1), pp.93-102.

AUSTRALIAN TAXATION LAW

Mahar, F., 2016. The distortive effects of the capital gains tax regime. Tax Specialist, 20(1),

p.16.

Maleki, B., Sameti, M., Sameti, M. and Ranjbar, H., 2017. The Effect of Capital Gain Tax on

Capital Formation, Financial Development and Economic Growth. Journal of Economic &

Management Perspectives, 11(4), pp.1365-1376.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on capital gains

realisations: evidence from Australia. In Australian Tax Forum (Vol. 33, No. 4).

Mintz, J., Bazel, P., Chen, D. and Crisan, D., 2017. With global company tax reform in the air,

will Australia finally respond?. Minerals Council of Australia, Melbourne, Australia, March.

Warren, N., 2016. E-filing and compliance risk: Evidence from Australian personal income tax

deductions. Austl. Tax F., 31, p.577.

Wilkins, R., 2015. Measuring income inequality in Australia. Australian Economic

Review, 48(1), pp.93-102.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.