Berkshire Instruments: WACC Calculation and Analysis

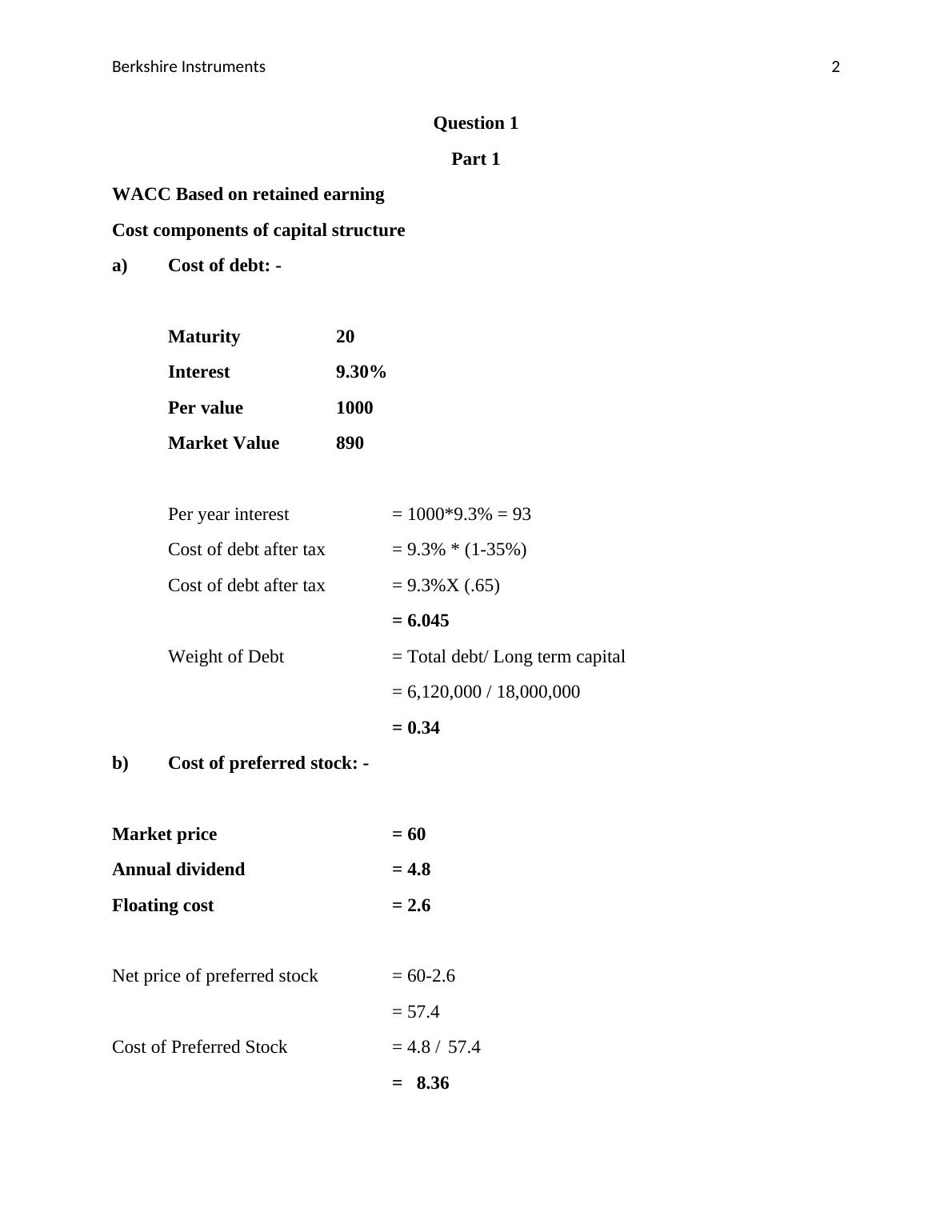

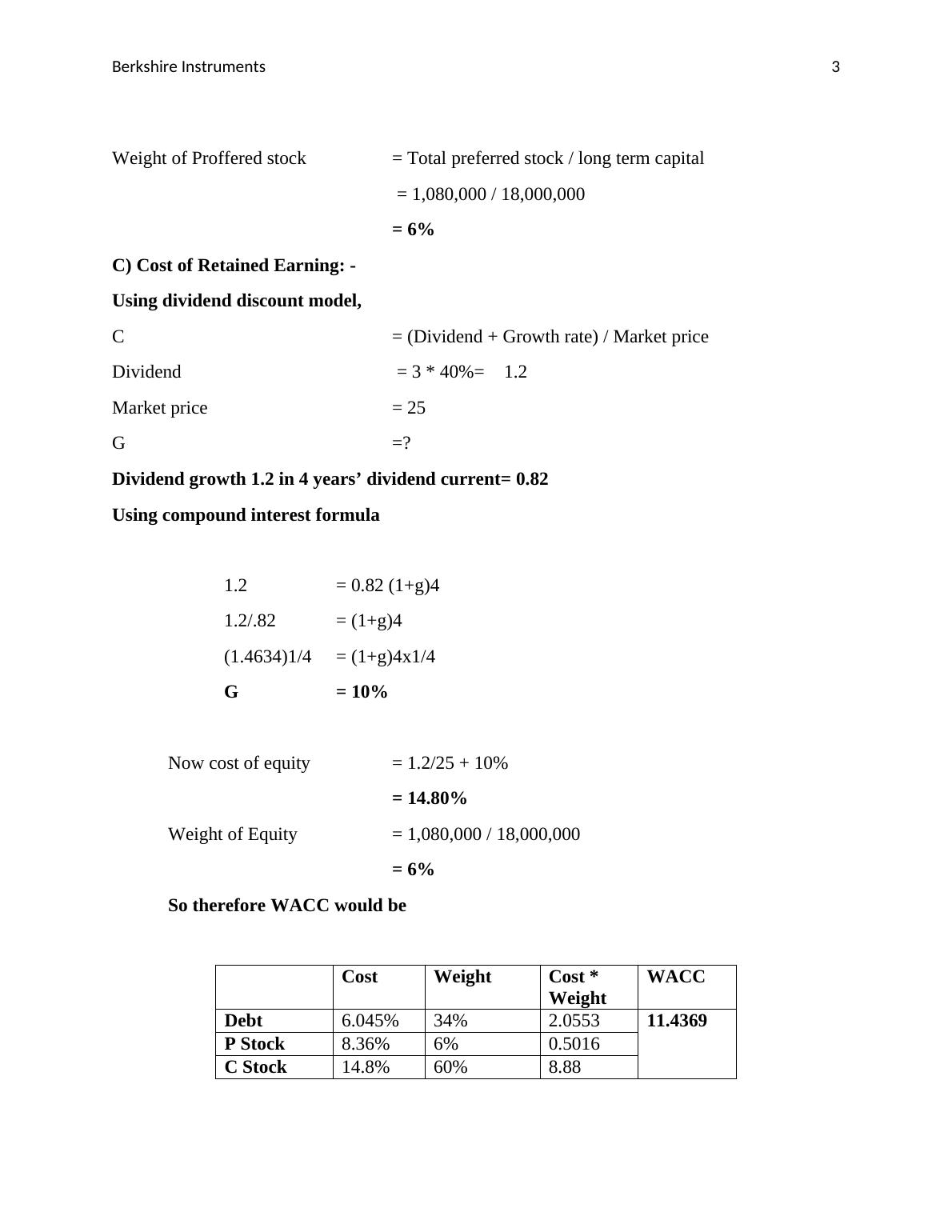

Al Hansen, the vice president of finance at Berkshire Instruments, is tasked with determining the firm's cost of capital. He examines the current balance sheet and past costs of debt and preferred stock. However, his investment banker advises him to focus on the current cost of funds instead of historical costs.

7 Pages791 Words97 Views

Added on 2023-03-23

About This Document

This document provides a step-by-step guide on calculating the weighted average cost of capital (WACC) for Berkshire Instruments using both the retained earnings and new equity methods. It explains the significance of WACC in determining the cost of financing and making investment decisions. The document also includes a comparison of the two methods and suggests the preferred option based on lower cost.

Berkshire Instruments: WACC Calculation and Analysis

Al Hansen, the vice president of finance at Berkshire Instruments, is tasked with determining the firm's cost of capital. He examines the current balance sheet and past costs of debt and preferred stock. However, his investment banker advises him to focus on the current cost of funds instead of historical costs.

Added on 2023-03-23

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Financial Management & Int Finance Study

|5

|935

|58

Weighted Average Cost of Capital

|14

|3759

|61

Assignment on Financial Management1

|11

|1661

|14

Calculation of Net Present Value and Intrinsic Value of Walmart Inc. and Sysco Corp

|19

|3990

|288

Calculating WACC for Kapusa plc - Corporate Finance Question

|5

|545

|368

Managing Finance: Analysis of Amaysim and Telstra Stocks, WACC, Dividend Policy and Share Purchase

|12

|2467

|69