BFM102B - Valuation of Investments 1: Comprehensive Assignment

VerifiedAdded on 2022/12/22

|11

|3031

|2

Homework Assignment

AI Summary

This document presents a comprehensive solution to a BFM102B Valuation of Investments assignment. It begins by explaining the marking-to-market process for futures contracts and then proceeds to calculate forward prices, considering dividend yields and risk-free rates. The solution also explores various options strategies, including stop-loss orders, hedging techniques, and the valuation of call options. Furthermore, it delves into the concepts of knock-in options, barrier options, and their valuation. The assignment includes calculations for portfolio deltas, gammas, and vegas, and concludes with an analysis of bull and bear spreads using call and put options. Finally, it discusses the assumptions underlying the Black-Scholes model and their impact on option pricing, providing a thorough understanding of investment valuation principles.

BFM102B - Valuation of Investments

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

BFM102B - Valuation of Investments.............................................................................................1

Contents...........................................................................................................................................2

QUESTION 1...................................................................................................................................3

(a) Describe the marking-to-market process for futures contracts:.............................................3

(b)................................................................................................................................................3

(c)................................................................................................................................................4

QUESTION 2...................................................................................................................................5

(a)................................................................................................................................................5

(b)................................................................................................................................................6

(c)................................................................................................................................................7

(d)................................................................................................................................................8

Question 3........................................................................................................................................9

References......................................................................................................................................11

2

BFM102B - Valuation of Investments.............................................................................................1

Contents...........................................................................................................................................2

QUESTION 1...................................................................................................................................3

(a) Describe the marking-to-market process for futures contracts:.............................................3

(b)................................................................................................................................................3

(c)................................................................................................................................................4

QUESTION 2...................................................................................................................................5

(a)................................................................................................................................................5

(b)................................................................................................................................................6

(c)................................................................................................................................................7

(d)................................................................................................................................................8

Question 3........................................................................................................................................9

References......................................................................................................................................11

2

QUESTION 1

(a) Describe the marking-to-market process for futures contracts:

Gains as well as losses settled on every trading day, which is one of most significant aspects of

futures contracts/transactions. Mark to Market settlement is the term for this method. This

implies that contract's value has been adjusted to reflect its actual market value. The

exchanges will receive this MTM margins from loss-bearing party as well as pay this to gain-

eligible recipient party with support of brokers or clearing houses (Raimbourg and Zimmermann,

2018).

MTM stands for mark to market, as well as this is a way of determining fair value of

accounts which vary over period, like assets and liabilities. The objective of marks to market

would provide a practical assessment of a business's or organization's current financial position

based on existing market conditions. Depending on what the business could expect in return

for asset under present industry conditions marks to market will provide a more reliable figure

for current value of company's assets.

MTM cannot accurately reflect asset's true value in orderly market throughout adverse or

unpredictable times. Marks to market is in comparison to historical costs accounting that

keeps asset's value at its purchasing price. Transactions for futures contract being marked to

market on regular in futures trading. Between long and short-positions, profits and losses are

measured (Thirumagal and SURESH, 2019).

Marks to market is accounting concept that refers to the process of changing the valuation

of asset to represent its existing market value. MV of an asset is measured by the amount a

business would receive if it were sold at a certain period. A corporation 's balance sheet should

represent current market value of such accounts at end of fiscal period. Other accounts can keep

their historical expense, which is asset's initial purchasing price.

(b).

(i).

Risk-free rate = 2% p.a.

Dividend yield = 6% per annum

3 Month forward price = F0 = S0 e(r–q )T

= 1250 * e.04*(3/12)

3

(a) Describe the marking-to-market process for futures contracts:

Gains as well as losses settled on every trading day, which is one of most significant aspects of

futures contracts/transactions. Mark to Market settlement is the term for this method. This

implies that contract's value has been adjusted to reflect its actual market value. The

exchanges will receive this MTM margins from loss-bearing party as well as pay this to gain-

eligible recipient party with support of brokers or clearing houses (Raimbourg and Zimmermann,

2018).

MTM stands for mark to market, as well as this is a way of determining fair value of

accounts which vary over period, like assets and liabilities. The objective of marks to market

would provide a practical assessment of a business's or organization's current financial position

based on existing market conditions. Depending on what the business could expect in return

for asset under present industry conditions marks to market will provide a more reliable figure

for current value of company's assets.

MTM cannot accurately reflect asset's true value in orderly market throughout adverse or

unpredictable times. Marks to market is in comparison to historical costs accounting that

keeps asset's value at its purchasing price. Transactions for futures contract being marked to

market on regular in futures trading. Between long and short-positions, profits and losses are

measured (Thirumagal and SURESH, 2019).

Marks to market is accounting concept that refers to the process of changing the valuation

of asset to represent its existing market value. MV of an asset is measured by the amount a

business would receive if it were sold at a certain period. A corporation 's balance sheet should

represent current market value of such accounts at end of fiscal period. Other accounts can keep

their historical expense, which is asset's initial purchasing price.

(b).

(i).

Risk-free rate = 2% p.a.

Dividend yield = 6% per annum

3 Month forward price = F0 = S0 e(r–q )T

= 1250 * e.04*(3/12)

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 1250 * e.04*(1/4)

= 1250 * e.01

= 1250 * 1.010050

= 1,262.56

(ii).

Dividend in 2 months = $5

Three-month forward Share Price = 26 + 5/2 * 3 = 33.5

(iii).

Current spot price = 1.25

Risk-free rate = 1%

Three-month forward price = 1.25.e.01*(90/360)

= 1.25 * 1.002503

= 1.253128

(c).

Strike price = $115

Risk-free rate = 5% per annum

Stock price = $120

Four-month Forward rate = $120. e.05*(4/12)

= $120 * 1.0168063

= 122.0167

(d).

No, it’s never be a smart option to exercise American option early, particularly if it's stock that

doesn't pay dividends. Let's take look at why this is situation. The alternative has both intrinsic

and temporal significance. Option's intrinsic value being always higher than zero. Furthermore,

since money has time value, one would like to avoid paying strike price by practicing it as

longer as possible. One could put the money to good use by earning interest. So, if the option has

a favourable intrinsic value including positive time value, one can sell it instead of exercise it

early. That's also valid for stock that does not pay dividends (Zanger, 2018).

4

= 1250 * e.01

= 1250 * 1.010050

= 1,262.56

(ii).

Dividend in 2 months = $5

Three-month forward Share Price = 26 + 5/2 * 3 = 33.5

(iii).

Current spot price = 1.25

Risk-free rate = 1%

Three-month forward price = 1.25.e.01*(90/360)

= 1.25 * 1.002503

= 1.253128

(c).

Strike price = $115

Risk-free rate = 5% per annum

Stock price = $120

Four-month Forward rate = $120. e.05*(4/12)

= $120 * 1.0168063

= 122.0167

(d).

No, it’s never be a smart option to exercise American option early, particularly if it's stock that

doesn't pay dividends. Let's take look at why this is situation. The alternative has both intrinsic

and temporal significance. Option's intrinsic value being always higher than zero. Furthermore,

since money has time value, one would like to avoid paying strike price by practicing it as

longer as possible. One could put the money to good use by earning interest. So, if the option has

a favourable intrinsic value including positive time value, one can sell it instead of exercise it

early. That's also valid for stock that does not pay dividends (Zanger, 2018).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 2

(a).

Stop-loss strategy:

Stop-loss strategy being used to determine when an investor can sell stock or security. That's a

stopping order with a listed price that's lower than current market price which is intended to be

selling. Stop-losses are mostly employed to protect traders' longer positions when hedging

(Ciorciari, 2019).

Hedging:

Regulating or reducing risks is what hedging is all about. Hedge is term for investment strategy

that uses another investment to hedge future gains and losses.

Out-of-the-money call options:

If strike price of call option is higher than market price of underlying asset/security, option is

said to be out-of-the-money. That means that investor has the option to buy security at a greater

price than market price, as long as the difference isn't too big. Time value determines price of

out-of-money call options (Haaland, Wright, Tufto and Ratikainen, 2019).

Call options:

Call option offers option holder's right to buy a security at set price if the buyer expects stock

prices would increase.

Suppose the strike price is 10.00. Option writer targets to fully covered if options are in

money as well as naked if this is out-of-money. Option writer tries to accomplish this by

purchasing assets underlying option as early as asset price hits 10.00 from underneath and selling

when asset price crosses 10.00 through above. The problem with this strategy is that this believes

that if asset price increases from 9.99 to then, it can move to higher price. (In reality, it's possible

that the next jump will be 9.99.) It is therefore assumed that if asset price rises from 10.01 to

ten, next move would be under 10.00. Buying at 10.01 as well as selling at the 9.99 is how the

scheme operates. It is, though, a poor hedging. Trading strategy's expense is negligible if asset

price never exceeds $10,000, but it can be very high if this does so often. A strong hedge

has property of having an expense that is still very close to option's value (Jia and Chen, 2020).

5

(a).

Stop-loss strategy:

Stop-loss strategy being used to determine when an investor can sell stock or security. That's a

stopping order with a listed price that's lower than current market price which is intended to be

selling. Stop-losses are mostly employed to protect traders' longer positions when hedging

(Ciorciari, 2019).

Hedging:

Regulating or reducing risks is what hedging is all about. Hedge is term for investment strategy

that uses another investment to hedge future gains and losses.

Out-of-the-money call options:

If strike price of call option is higher than market price of underlying asset/security, option is

said to be out-of-the-money. That means that investor has the option to buy security at a greater

price than market price, as long as the difference isn't too big. Time value determines price of

out-of-money call options (Haaland, Wright, Tufto and Ratikainen, 2019).

Call options:

Call option offers option holder's right to buy a security at set price if the buyer expects stock

prices would increase.

Suppose the strike price is 10.00. Option writer targets to fully covered if options are in

money as well as naked if this is out-of-money. Option writer tries to accomplish this by

purchasing assets underlying option as early as asset price hits 10.00 from underneath and selling

when asset price crosses 10.00 through above. The problem with this strategy is that this believes

that if asset price increases from 9.99 to then, it can move to higher price. (In reality, it's possible

that the next jump will be 9.99.) It is therefore assumed that if asset price rises from 10.01 to

ten, next move would be under 10.00. Buying at 10.01 as well as selling at the 9.99 is how the

scheme operates. It is, though, a poor hedging. Trading strategy's expense is negligible if asset

price never exceeds $10,000, but it can be very high if this does so often. A strong hedge

has property of having an expense that is still very close to option's value (Jia and Chen, 2020).

5

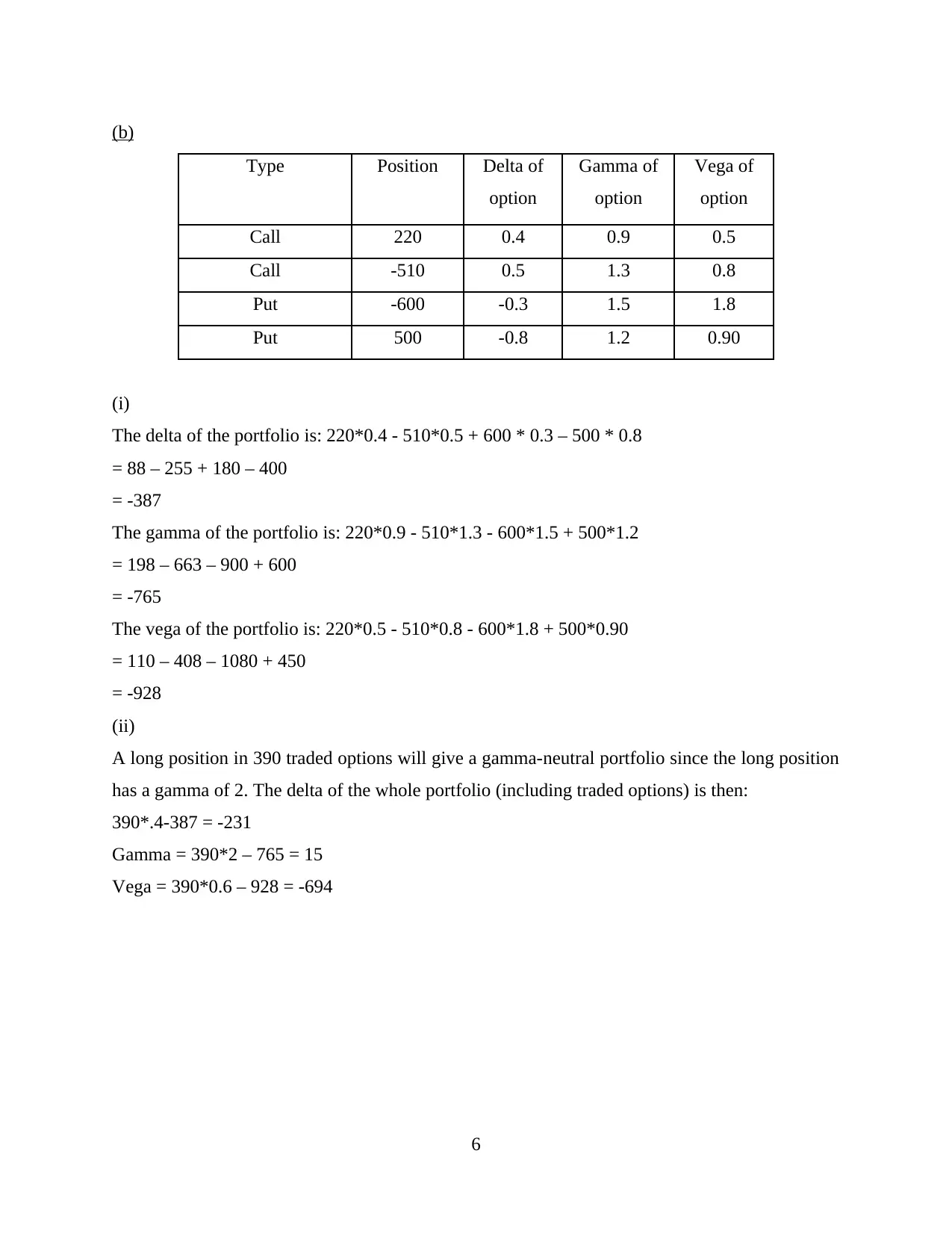

(b)

Type Position Delta of

option

Gamma of

option

Vega of

option

Call 220 0.4 0.9 0.5

Call -510 0.5 1.3 0.8

Put -600 -0.3 1.5 1.8

Put 500 -0.8 1.2 0.90

(i)

The delta of the portfolio is: 220*0.4 - 510*0.5 + 600 * 0.3 – 500 * 0.8

= 88 – 255 + 180 – 400

= -387

The gamma of the portfolio is: 220*0.9 - 510*1.3 - 600*1.5 + 500*1.2

= 198 – 663 – 900 + 600

= -765

The vega of the portfolio is: 220*0.5 - 510*0.8 - 600*1.8 + 500*0.90

= 110 – 408 – 1080 + 450

= -928

(ii)

A long position in 390 traded options will give a gamma-neutral portfolio since the long position

has a gamma of 2. The delta of the whole portfolio (including traded options) is then:

390*.4-387 = -231

Gamma = 390*2 – 765 = 15

Vega = 390*0.6 – 928 = -694

6

Type Position Delta of

option

Gamma of

option

Vega of

option

Call 220 0.4 0.9 0.5

Call -510 0.5 1.3 0.8

Put -600 -0.3 1.5 1.8

Put 500 -0.8 1.2 0.90

(i)

The delta of the portfolio is: 220*0.4 - 510*0.5 + 600 * 0.3 – 500 * 0.8

= 88 – 255 + 180 – 400

= -387

The gamma of the portfolio is: 220*0.9 - 510*1.3 - 600*1.5 + 500*1.2

= 198 – 663 – 900 + 600

= -765

The vega of the portfolio is: 220*0.5 - 510*0.8 - 600*1.8 + 500*0.90

= 110 – 408 – 1080 + 450

= -928

(ii)

A long position in 390 traded options will give a gamma-neutral portfolio since the long position

has a gamma of 2. The delta of the whole portfolio (including traded options) is then:

390*.4-387 = -231

Gamma = 390*2 – 765 = 15

Vega = 390*0.6 – 928 = -694

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(c).

A knock-in choice is latent option-contract as it only becomes active (or "knocks in") after

a certain cost level is achieved prior to expire. Knock-ins may be characterized either as a back

or an optional kind of obstacle. A barrier choice is a form of insurance wherein the compensation

is contingent on the value of the portfolio or whether it reaches a certain threshold. A barrier

choice is a form of insurance wherein the payoff is based mostly on value of the portfolio or even

if it reaches a certain cost over a certain time frame. Knock-in options are among 2 kinds of

barrier choices, with turn opportunities being another. A knock-in investor can purchase which is

only available if a certain cost is achieved. As a result, if the pricing has never been agreed

upon, the agreement ceases to exist. The knock-in alternative, on the other hand, is activated

when the asset value crosses a certain threshold. A knock-in choice arises only when the

underlying asset hits a boundary, whereas a knock-out choice begins to occur whenever the

underlying asset hits an obstacle. Barrier alternatives have cheaper insurance than vanilla

choices, owing to the increased risk of the choice being useless. Unless the fundamental is very

likely to strike the boundary, a seller might opt for the less expensive (in comparison to a similar

vanilla) barrier choice (Miura, Quadros, Gurumurthy and Ohtsuka, 2018).

Suspect a down-and-in call options with such a hurdle cost of $90 as well as a current

value of $100 is bought. The underlying asset is holding steady at $110, as well as the option has

a three-month expiration date. The alternative is created and will become a vanilla choice with

such a market price of $100 unless the volatility of the bond security hits $90. After that, even if

the asset value is traded beneath $90, the choice manager has the authority to acquire this at the

market price of $100. The alternative value is determined by this right which provide better

understanding of profit for the company. Even though the price of a security rises back below

$90, the option contract stays active until about the expiry date. The bottom expiration date

useless unless the asset value doesn't really fall far below intermediary price throughout the

contract terms life. The fact that the barrier has been breached does not guarantee a profit mostly

on trade so because fundamental must remain beneath $100, because after obstacle has been

triggered) in attempt for the alternative to be useful.

A back option, unlike an away option, only exists if the underlying crosses a barriers cost

that is greater than the current underlying's pricing. Presume a dealer buys one more a go call

option through an underlying value that is currently traded at $40 per percentage. The market

7

A knock-in choice is latent option-contract as it only becomes active (or "knocks in") after

a certain cost level is achieved prior to expire. Knock-ins may be characterized either as a back

or an optional kind of obstacle. A barrier choice is a form of insurance wherein the compensation

is contingent on the value of the portfolio or whether it reaches a certain threshold. A barrier

choice is a form of insurance wherein the payoff is based mostly on value of the portfolio or even

if it reaches a certain cost over a certain time frame. Knock-in options are among 2 kinds of

barrier choices, with turn opportunities being another. A knock-in investor can purchase which is

only available if a certain cost is achieved. As a result, if the pricing has never been agreed

upon, the agreement ceases to exist. The knock-in alternative, on the other hand, is activated

when the asset value crosses a certain threshold. A knock-in choice arises only when the

underlying asset hits a boundary, whereas a knock-out choice begins to occur whenever the

underlying asset hits an obstacle. Barrier alternatives have cheaper insurance than vanilla

choices, owing to the increased risk of the choice being useless. Unless the fundamental is very

likely to strike the boundary, a seller might opt for the less expensive (in comparison to a similar

vanilla) barrier choice (Miura, Quadros, Gurumurthy and Ohtsuka, 2018).

Suspect a down-and-in call options with such a hurdle cost of $90 as well as a current

value of $100 is bought. The underlying asset is holding steady at $110, as well as the option has

a three-month expiration date. The alternative is created and will become a vanilla choice with

such a market price of $100 unless the volatility of the bond security hits $90. After that, even if

the asset value is traded beneath $90, the choice manager has the authority to acquire this at the

market price of $100. The alternative value is determined by this right which provide better

understanding of profit for the company. Even though the price of a security rises back below

$90, the option contract stays active until about the expiry date. The bottom expiration date

useless unless the asset value doesn't really fall far below intermediary price throughout the

contract terms life. The fact that the barrier has been breached does not guarantee a profit mostly

on trade so because fundamental must remain beneath $100, because after obstacle has been

triggered) in attempt for the alternative to be useful.

A back option, unlike an away option, only exists if the underlying crosses a barriers cost

that is greater than the current underlying's pricing. Presume a dealer buys one more a go call

option through an underlying value that is currently traded at $40 per percentage. The market

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

price including its out of call option contract is $50, with a hurdle of $55. The strike price of both

the back call futures contracts is $50, with a hurdle of $55. The choice deal ends worthless if the

asset value doesn't really exceed $55 within the duration of the agreement. The covered call will

become active and the investor would have been in the cash if the average investor rose to $55 or

higher (Golbabai, Nikan and Nikazad, 2019).

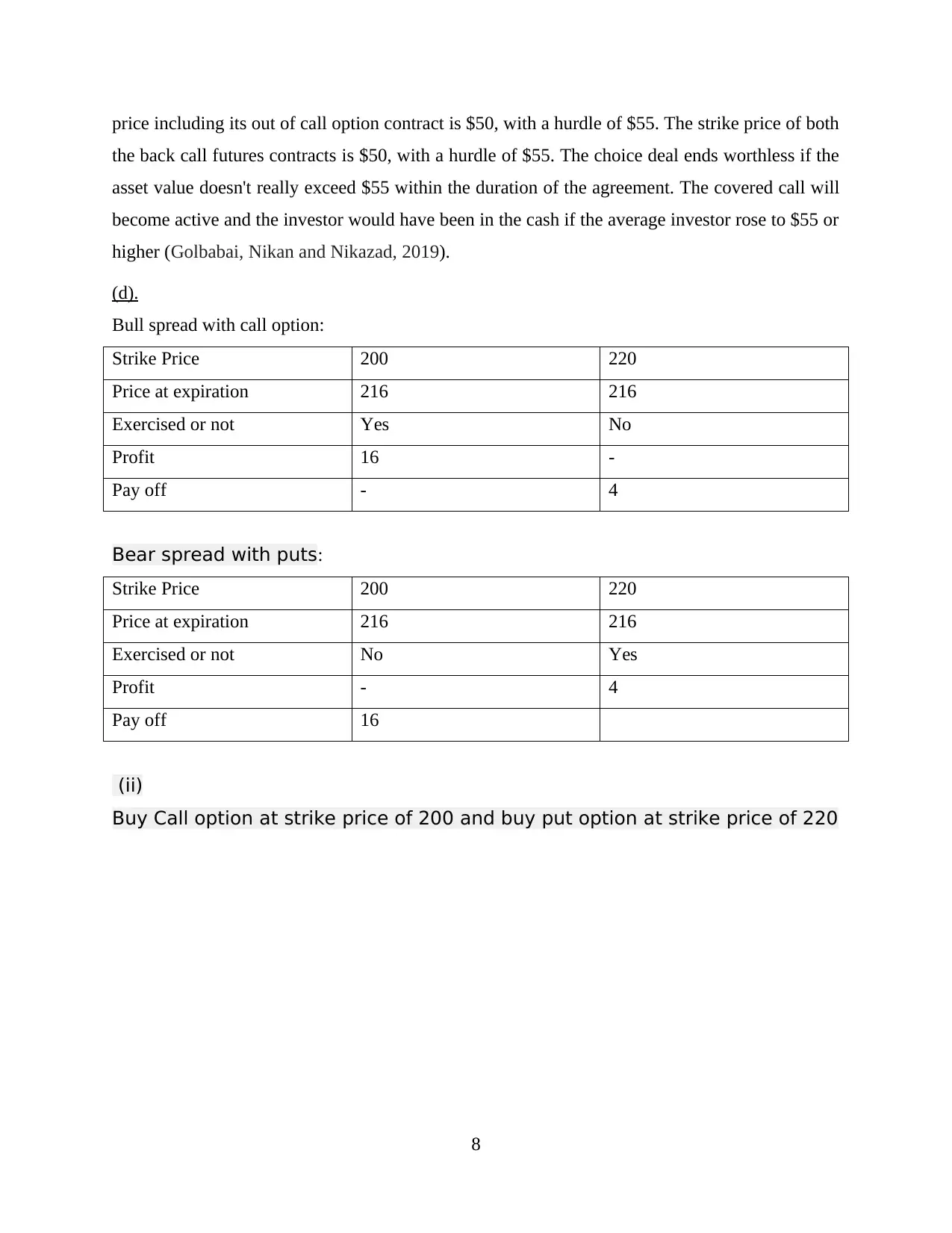

(d).

Bull spread with call option:

Strike Price 200 220

Price at expiration 216 216

Exercised or not Yes No

Profit 16 -

Pay off - 4

Bear spread with puts:

Strike Price 200 220

Price at expiration 216 216

Exercised or not No Yes

Profit - 4

Pay off 16

(ii)

Buy Call option at strike price of 200 and buy put option at strike price of 220

8

the back call futures contracts is $50, with a hurdle of $55. The choice deal ends worthless if the

asset value doesn't really exceed $55 within the duration of the agreement. The covered call will

become active and the investor would have been in the cash if the average investor rose to $55 or

higher (Golbabai, Nikan and Nikazad, 2019).

(d).

Bull spread with call option:

Strike Price 200 220

Price at expiration 216 216

Exercised or not Yes No

Profit 16 -

Pay off - 4

Bear spread with puts:

Strike Price 200 220

Price at expiration 216 216

Exercised or not No Yes

Profit - 4

Pay off 16

(ii)

Buy Call option at strike price of 200 and buy put option at strike price of 220

8

Question 3

Assumptions:

1. Random walk: The first premise, something that might recognize from other economic

projections, is that now the market price cannot be forecast uniformly and seems to be

entirely random. Price performs a so random walk, a moving characteristic often referred

it as Wave function or Brownian in astronomy. The very next movement will be down or

up at a certain moment, so company have no idea where it's going it will be.

2. Constant volatility: Volatility – the general magnitude of the movements, and in other

terms, how large or small movements they can anticipate – is one aspect we may

understand more about company's stock potential developments. Volatility is stable (does

not really change over time) and predictable in the Black-Scholes concept. Of course, in

the actual world, that presumption is extremely difficult (volatility is neither constant nor

known in advance). Simultaneously, volatility is among the model's variables that has the

greatest impact on the output price movement (Al–Zhour, Barfeie, Soleymani and Tohidi,

2019).

3. Normal distribution of return: Returns mostly on financial investment are traditionally

redistributed as a consequence of the randomness price path (assertion 1 above). The so-

called circular curve depicts the probability of subsequent percent change throughout the

stock's price over even a given timeframe, with smaller price movements close to just the

median having comparatively high probability and also more severe positively or

negatively cost increases being far less probable. When they get closer to the scales, the

percentages eventually decrease significantly. This is because of the connection

connecting distributions and prices, since returns are generally dispersed, prospective

asset values will be residuals are normally allocated at any specific moment in time.

In case if these assumptions are incorrect than option rise will show negative movement due to

which there can be adverse impact over the share price. Stock prices seldom exhibit lognormal

correlations, as Black-Scholes assumes. The distributions of the real world are distorted. As a

result of this disparity, the Black-Scholes model significantly under-priced or overpriced an

alternative. Traders who are acquainted with both the ramifications of the Black-Scholes models

may prefer to buy overvalued or short selling undervalued alternatives, causing them to losses.

To provide the most risk premium, investors must keep a close eye on price trends and market

9

Assumptions:

1. Random walk: The first premise, something that might recognize from other economic

projections, is that now the market price cannot be forecast uniformly and seems to be

entirely random. Price performs a so random walk, a moving characteristic often referred

it as Wave function or Brownian in astronomy. The very next movement will be down or

up at a certain moment, so company have no idea where it's going it will be.

2. Constant volatility: Volatility – the general magnitude of the movements, and in other

terms, how large or small movements they can anticipate – is one aspect we may

understand more about company's stock potential developments. Volatility is stable (does

not really change over time) and predictable in the Black-Scholes concept. Of course, in

the actual world, that presumption is extremely difficult (volatility is neither constant nor

known in advance). Simultaneously, volatility is among the model's variables that has the

greatest impact on the output price movement (Al–Zhour, Barfeie, Soleymani and Tohidi,

2019).

3. Normal distribution of return: Returns mostly on financial investment are traditionally

redistributed as a consequence of the randomness price path (assertion 1 above). The so-

called circular curve depicts the probability of subsequent percent change throughout the

stock's price over even a given timeframe, with smaller price movements close to just the

median having comparatively high probability and also more severe positively or

negatively cost increases being far less probable. When they get closer to the scales, the

percentages eventually decrease significantly. This is because of the connection

connecting distributions and prices, since returns are generally dispersed, prospective

asset values will be residuals are normally allocated at any specific moment in time.

In case if these assumptions are incorrect than option rise will show negative movement due to

which there can be adverse impact over the share price. Stock prices seldom exhibit lognormal

correlations, as Black-Scholes assumes. The distributions of the real world are distorted. As a

result of this disparity, the Black-Scholes model significantly under-priced or overpriced an

alternative. Traders who are acquainted with both the ramifications of the Black-Scholes models

may prefer to buy overvalued or short selling undervalued alternatives, causing them to losses.

To provide the most risk premium, investors must keep a close eye on price trends and market

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

trends as a precautionary measure. Try to buy while volatility remains low (for example, over the

previous duration of the expected option holding period) but sell when it becomes high. In a

nutshell, market prices are believed to be absolute, without any connection to or dependence on

other industry trends or sections. The influence of the 2008–09 financial meltdown attributable to

just the housing market burst resulting in an overall financial meltdown, for instance, could be

counted for within the Black-Scholes modelling (or potentially any simulation theorem). A stock

with such a purchase of $100 as well as a distribution of $5 would drop to $95 on dividends ex-

date if all other variables remain constant. Option vendors take advantage of this opportunity by

selling short call/long futures contracts just before the expiration date and then squaring off the

roles on the expiration date, bringing in earnings. Traders who use Black-Scholes pricing must

be informed of these repercussions using a risk management strategy (De Staelen and Hendy,

2017).

10

previous duration of the expected option holding period) but sell when it becomes high. In a

nutshell, market prices are believed to be absolute, without any connection to or dependence on

other industry trends or sections. The influence of the 2008–09 financial meltdown attributable to

just the housing market burst resulting in an overall financial meltdown, for instance, could be

counted for within the Black-Scholes modelling (or potentially any simulation theorem). A stock

with such a purchase of $100 as well as a distribution of $5 would drop to $95 on dividends ex-

date if all other variables remain constant. Option vendors take advantage of this opportunity by

selling short call/long futures contracts just before the expiration date and then squaring off the

roles on the expiration date, bringing in earnings. Traders who use Black-Scholes pricing must

be informed of these repercussions using a risk management strategy (De Staelen and Hendy,

2017).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and Journals:

Raimbourg, P. and Zimmermann, P., 2018, June. Is Normal Backwardation Normal? Valuing

Financial Futures with a Stochastic, Endogenous Index-Rate Covariance. In Valuing

Financial Futures with a Stochastic, Endogenous Index-Rate Covariance (June 3,

2018). Paris December 2018 Finance Meeting EUROFIDAI-AFFI.

Thirumagal, P.G. and SURESH, S., 2019. PAYOFF AND THE IMPACT OF VARIOUS

INVESTMENT ATTRIBUTES ON FREQUENCY OF INVESTMENT IN STOCK

INDEX FUTURES. International Journal of Mechanical and Production Engineering

Research and Development (IJMPERD) Vol, 8, pp.8-15.

Zanger, D.Z., 2018. Convergence of a least‐squares Monte Carlo algorithm for American option

pricing with dependent sample data. Mathematical Finance, 28(1), pp.447-479.

Ciorciari, J.D., 2019. The variable effectiveness of hedging strategies. International Relations of

the Asia-Pacific, 19(3), pp.523-555.

Haaland, T.R., Wright, J., Tufto, J. and Ratikainen, I.I., 2019. Short‐term insurance versus long‐

term bet‐hedging strategies as adaptations to variable environments. Evolution, 73(2),

pp.145-157.

Jia, L. and Chen, W., 2020. Knock-in options of an uncertain stock model with floating interest

rate. Chaos, Solitons & Fractals, 141, p.110324.

Miura, H., Quadros, R.M., Gurumurthy, C.B. and Ohtsuka, M., 2018. Easi-CRISPR for creating

knock-in and conditional knockout mouse models using long ssDNA donors. Nature

protocols, 13(1), p.195.

Golbabai, A., Nikan, O. and Nikazad, T., 2019. Numerical analysis of time fractional Black–

Scholes European option pricing model arising in financial market. Computational and

Applied Mathematics, 38(4), pp.1-24.

Al–Zhour, Z., Barfeie, M., Soleymani, F. and Tohidi, E., 2019. A computational method to price

with transaction costs under the nonlinear Black–Scholes model. Chaos, Solitons &

Fractals, 127, pp.291-301.

De Staelen, R.H. and Hendy, A.S., 2017. Numerically pricing double barrier options in a time-

fractional Black–Scholes model. Computers & Mathematics with Applications, 74(6),

pp.1166-1175.

11

Books and Journals:

Raimbourg, P. and Zimmermann, P., 2018, June. Is Normal Backwardation Normal? Valuing

Financial Futures with a Stochastic, Endogenous Index-Rate Covariance. In Valuing

Financial Futures with a Stochastic, Endogenous Index-Rate Covariance (June 3,

2018). Paris December 2018 Finance Meeting EUROFIDAI-AFFI.

Thirumagal, P.G. and SURESH, S., 2019. PAYOFF AND THE IMPACT OF VARIOUS

INVESTMENT ATTRIBUTES ON FREQUENCY OF INVESTMENT IN STOCK

INDEX FUTURES. International Journal of Mechanical and Production Engineering

Research and Development (IJMPERD) Vol, 8, pp.8-15.

Zanger, D.Z., 2018. Convergence of a least‐squares Monte Carlo algorithm for American option

pricing with dependent sample data. Mathematical Finance, 28(1), pp.447-479.

Ciorciari, J.D., 2019. The variable effectiveness of hedging strategies. International Relations of

the Asia-Pacific, 19(3), pp.523-555.

Haaland, T.R., Wright, J., Tufto, J. and Ratikainen, I.I., 2019. Short‐term insurance versus long‐

term bet‐hedging strategies as adaptations to variable environments. Evolution, 73(2),

pp.145-157.

Jia, L. and Chen, W., 2020. Knock-in options of an uncertain stock model with floating interest

rate. Chaos, Solitons & Fractals, 141, p.110324.

Miura, H., Quadros, R.M., Gurumurthy, C.B. and Ohtsuka, M., 2018. Easi-CRISPR for creating

knock-in and conditional knockout mouse models using long ssDNA donors. Nature

protocols, 13(1), p.195.

Golbabai, A., Nikan, O. and Nikazad, T., 2019. Numerical analysis of time fractional Black–

Scholes European option pricing model arising in financial market. Computational and

Applied Mathematics, 38(4), pp.1-24.

Al–Zhour, Z., Barfeie, M., Soleymani, F. and Tohidi, E., 2019. A computational method to price

with transaction costs under the nonlinear Black–Scholes model. Chaos, Solitons &

Fractals, 127, pp.291-301.

De Staelen, R.H. and Hendy, A.S., 2017. Numerically pricing double barrier options in a time-

fractional Black–Scholes model. Computers & Mathematics with Applications, 74(6),

pp.1166-1175.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.