Financial Analysis for Investment Decisions

VerifiedAdded on 2020/06/03

|12

|1867

|226

AI Summary

This assignment delves into financial analysis techniques used for making informed investment decisions. It focuses on Net Present Value (NPV) and Internal Rate of Return (IRR), explaining how to calculate and interpret these metrics. Students will analyze cash flow projections for two projects and rank them based on NPV and IRR, comparing the results and identifying potential conflicts. The assignment emphasizes the importance of effective project scheduling and budgeting in maximizing business value.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Project Scheduling and

Budgeting Part 2

Budgeting Part 2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1 Measurements for the Net cash flow, internal rate of returns, NPV ad Discount factor for

both the project............................................................................................................................1

2 comparing the NPV with IRR and suggestions to start operating spaceship or not................6

3 Determining the limitations of NPV and IRR as well as ranking the projects........................7

4 Presenting the column and charts.............................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

1 Measurements for the Net cash flow, internal rate of returns, NPV ad Discount factor for

both the project............................................................................................................................1

2 comparing the NPV with IRR and suggestions to start operating spaceship or not................6

3 Determining the limitations of NPV and IRR as well as ranking the projects........................7

4 Presenting the column and charts.............................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Project scheduling and budgeting is significant in the development of an effective project

plan that renders a guidance in executing each and every step of the business. There are further

some other features added to bring effectiveness in the plan such as resources and timescales

(Kerzner, 2013). These section of the project covers the details of overall requirements for the

undertaken project work along with deadlines in which these tasks will be accomplished based

on their priorities. The present report is focused on the calculations of different financial terms

such as net cash flow, internal rate of return, etc. for an undertaken project. Also, advantages and

limitation of NPV and IRR will be discussed in the present report.

The project that is central to the whole work is development of the Death Star ( a gigantic

space ship which can be able to destroy entire planets) by Galactic Empire organisation. The

scheduling and budgeting is performed for the construction of mentioned ship.

1 Measurements for the Net cash flow, internal rate of returns, NPV ad Discount factor for both

the project

In terms of planning the implication as well as investments in the projects there will be

need to make the adequate analysis as well as determining the profitability of such projects.

Hence, Galactic Empire has planned two projects such as A and B which are belongs to the 20

years of investments (Potes and et.al., 2017). Therefore, there will be need to analyse the net

cash flow, IRR and NPV which will help in making the appropriate and accurate decisions by the

managers.

Net cash flow:

In accordance with determining the net cash flow of the business there will be need to

analyse and record all the cash and cash equivalent transactions (Van Heerden and Van

Rensburg, 2016). Therefore, there will be analysis based on Project A and Project B which are

need to be analysed as follows:

Project A:

Particul

ars

Initia

l

inves

1

ye

ar

2

ye

ar

3

ye

ar

4

ye

ar

5

ye

ar

6

ye

ar

7

ye

ar

8

ye

ar

9

ye

ar

10

ye

ar

11

ye

ar

12

ye

ar

13

ye

ar

14

ye

ar

15

ye

ar

16

ye

ar

17

ye

ar

18

ye

ar

19

ye

ar

20

ye

ar

1

Project scheduling and budgeting is significant in the development of an effective project

plan that renders a guidance in executing each and every step of the business. There are further

some other features added to bring effectiveness in the plan such as resources and timescales

(Kerzner, 2013). These section of the project covers the details of overall requirements for the

undertaken project work along with deadlines in which these tasks will be accomplished based

on their priorities. The present report is focused on the calculations of different financial terms

such as net cash flow, internal rate of return, etc. for an undertaken project. Also, advantages and

limitation of NPV and IRR will be discussed in the present report.

The project that is central to the whole work is development of the Death Star ( a gigantic

space ship which can be able to destroy entire planets) by Galactic Empire organisation. The

scheduling and budgeting is performed for the construction of mentioned ship.

1 Measurements for the Net cash flow, internal rate of returns, NPV ad Discount factor for both

the project

In terms of planning the implication as well as investments in the projects there will be

need to make the adequate analysis as well as determining the profitability of such projects.

Hence, Galactic Empire has planned two projects such as A and B which are belongs to the 20

years of investments (Potes and et.al., 2017). Therefore, there will be need to analyse the net

cash flow, IRR and NPV which will help in making the appropriate and accurate decisions by the

managers.

Net cash flow:

In accordance with determining the net cash flow of the business there will be need to

analyse and record all the cash and cash equivalent transactions (Van Heerden and Van

Rensburg, 2016). Therefore, there will be analysis based on Project A and Project B which are

need to be analysed as follows:

Project A:

Particul

ars

Initia

l

inves

1

ye

ar

2

ye

ar

3

ye

ar

4

ye

ar

5

ye

ar

6

ye

ar

7

ye

ar

8

ye

ar

9

ye

ar

10

ye

ar

11

ye

ar

12

ye

ar

13

ye

ar

14

ye

ar

15

ye

ar

16

ye

ar

17

ye

ar

18

ye

ar

19

ye

ar

20

ye

ar

1

tmen

t

Capital

costs 1000

50

0

50

0

50

0

50

0

50

0

25

0

25

0

25

0

25

0

25

0

25

0

Operatin

g cost

10

0

10

0

10

0

10

0

10

0

10

0

10

0

10

0

10

0

10

0

Operati

ng

income

Commer

cial

revenues

40

0

40

0

40

0

40

0

40

0

80

0

80

0

80

0

80

0

80

0

Docking

fees

10

00

12

50

15

62.

5

19

53.

12

5

24

41.

40

62

5

30

51.

75

78

12

5

38

14.

69

72

65

62

5

47

68.

37

15

82

03

13

59

60.

46

44

77

53

91

74

50.

58

05

96

92

38

Net cash

flow 1000

50

0

50

0

50

0

50

0

50

0

25

0

25

0

25

0

25

0

25

0

17

50

17

50

20

62.

5

24

53.

12

5

29

41.

40

62

5

39

51.

75

78

12

5

47

14.

69

72

65

62

5

56

68.

37

15

82

03

13

68

60.

46

44

77

53

91

83

50.

58

05

96

92

38

Project B:

Particul

ars

Initi

al

1

ye

2

ye

3

ye

4

ye

5

ye

6

ye

7

ye

8

ye

9

ye

10

ye

11

ye

12

ye

13

ye

14

ye

15

ye

16

ye

17

ye

18

ye

19

ye

20

ye

2

t

Capital

costs 1000

50

0

50

0

50

0

50

0

50

0

25

0

25

0

25

0

25

0

25

0

25

0

Operatin

g cost

10

0

10

0

10

0

10

0

10

0

10

0

10

0

10

0

10

0

10

0

Operati

ng

income

Commer

cial

revenues

40

0

40

0

40

0

40

0

40

0

80

0

80

0

80

0

80

0

80

0

Docking

fees

10

00

12

50

15

62.

5

19

53.

12

5

24

41.

40

62

5

30

51.

75

78

12

5

38

14.

69

72

65

62

5

47

68.

37

15

82

03

13

59

60.

46

44

77

53

91

74

50.

58

05

96

92

38

Net cash

flow 1000

50

0

50

0

50

0

50

0

50

0

25

0

25

0

25

0

25

0

25

0

17

50

17

50

20

62.

5

24

53.

12

5

29

41.

40

62

5

39

51.

75

78

12

5

47

14.

69

72

65

62

5

56

68.

37

15

82

03

13

68

60.

46

44

77

53

91

83

50.

58

05

96

92

38

Project B:

Particul

ars

Initi

al

1

ye

2

ye

3

ye

4

ye

5

ye

6

ye

7

ye

8

ye

9

ye

10

ye

11

ye

12

ye

13

ye

14

ye

15

ye

16

ye

17

ye

18

ye

19

ye

20

ye

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

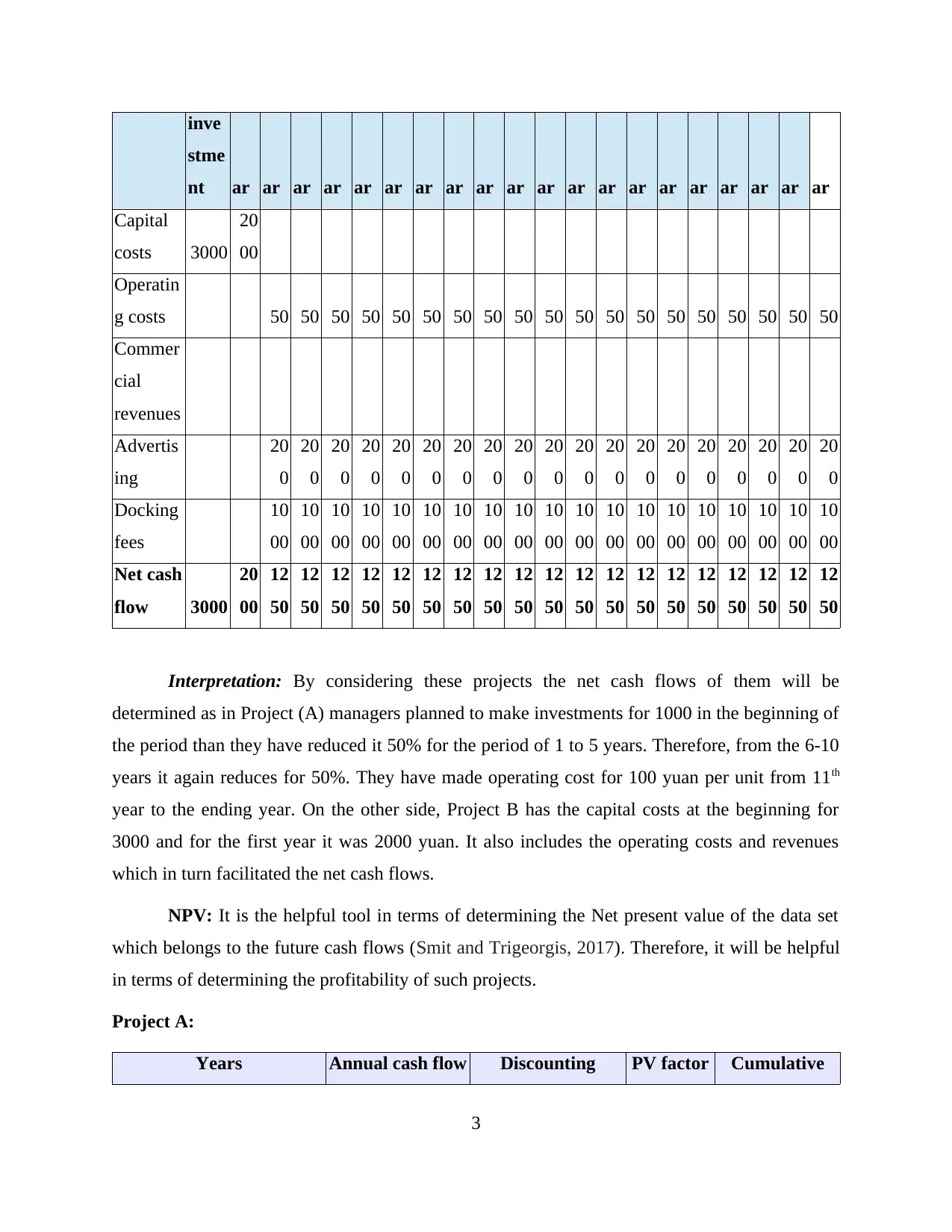

inve

stme

nt ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar

Capital

costs 3000

20

00

Operatin

g costs 50 50 50 50 50 50 50 50 50 50 50 50 50 50 50 50 50 50 50

Commer

cial

revenues

Advertis

ing

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

Docking

fees

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

Net cash

flow 3000

20

00

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

Interpretation: By considering these projects the net cash flows of them will be

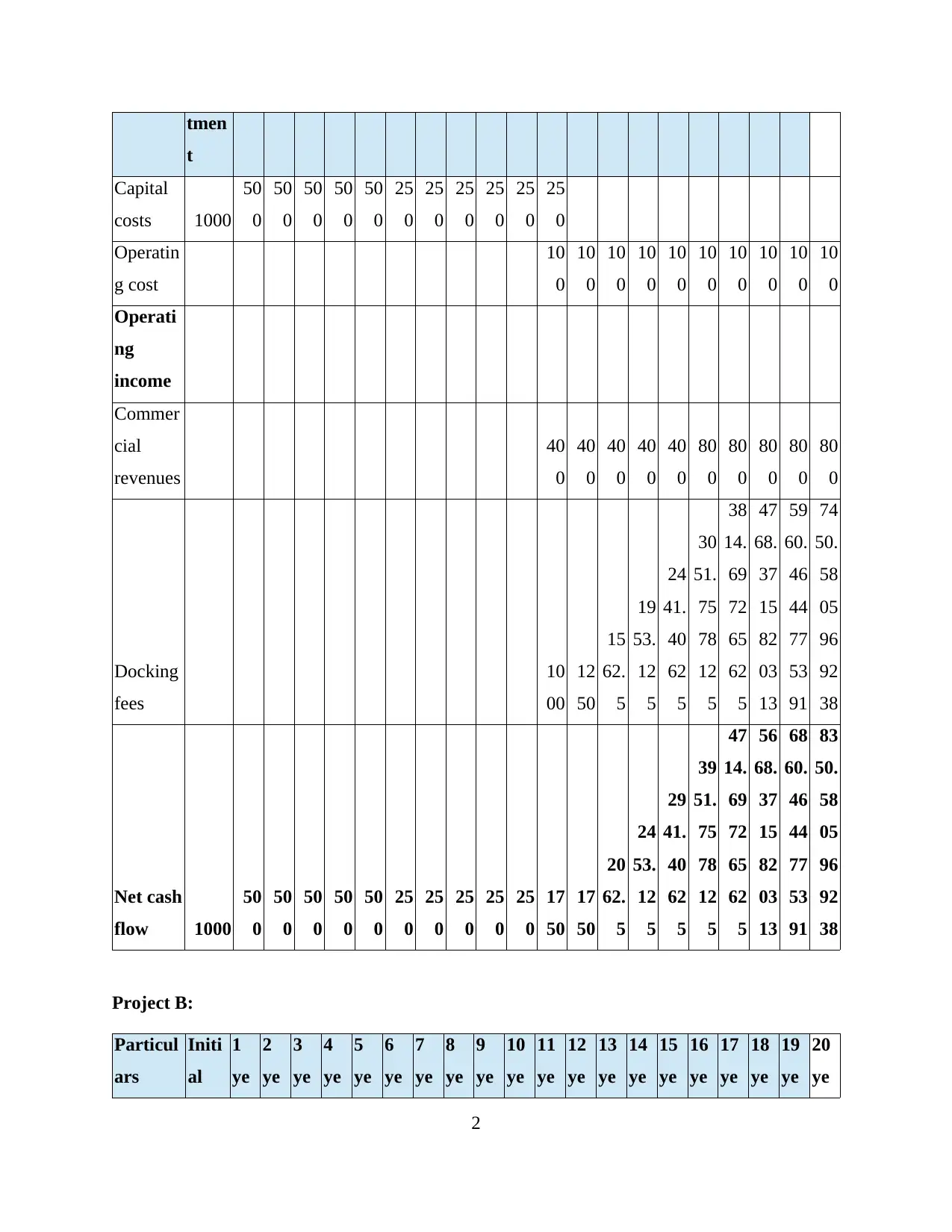

determined as in Project (A) managers planned to make investments for 1000 in the beginning of

the period than they have reduced it 50% for the period of 1 to 5 years. Therefore, from the 6-10

years it again reduces for 50%. They have made operating cost for 100 yuan per unit from 11th

year to the ending year. On the other side, Project B has the capital costs at the beginning for

3000 and for the first year it was 2000 yuan. It also includes the operating costs and revenues

which in turn facilitated the net cash flows.

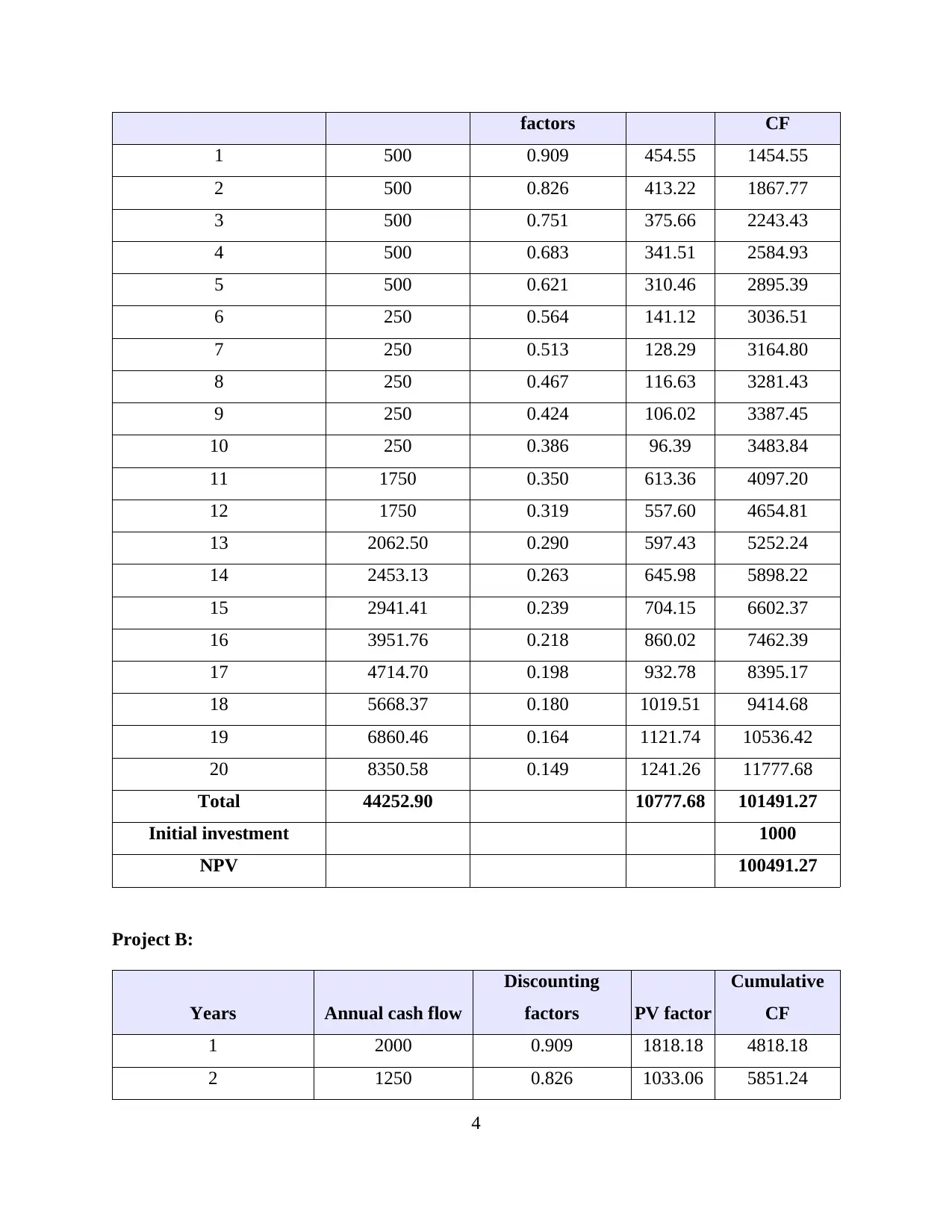

NPV: It is the helpful tool in terms of determining the Net present value of the data set

which belongs to the future cash flows (Smit and Trigeorgis, 2017). Therefore, it will be helpful

in terms of determining the profitability of such projects.

Project A:

Years Annual cash flow Discounting PV factor Cumulative

3

stme

nt ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar ar

Capital

costs 3000

20

00

Operatin

g costs 50 50 50 50 50 50 50 50 50 50 50 50 50 50 50 50 50 50 50

Commer

cial

revenues

Advertis

ing

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

Docking

fees

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

10

00

Net cash

flow 3000

20

00

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

12

50

Interpretation: By considering these projects the net cash flows of them will be

determined as in Project (A) managers planned to make investments for 1000 in the beginning of

the period than they have reduced it 50% for the period of 1 to 5 years. Therefore, from the 6-10

years it again reduces for 50%. They have made operating cost for 100 yuan per unit from 11th

year to the ending year. On the other side, Project B has the capital costs at the beginning for

3000 and for the first year it was 2000 yuan. It also includes the operating costs and revenues

which in turn facilitated the net cash flows.

NPV: It is the helpful tool in terms of determining the Net present value of the data set

which belongs to the future cash flows (Smit and Trigeorgis, 2017). Therefore, it will be helpful

in terms of determining the profitability of such projects.

Project A:

Years Annual cash flow Discounting PV factor Cumulative

3

factors CF

1 500 0.909 454.55 1454.55

2 500 0.826 413.22 1867.77

3 500 0.751 375.66 2243.43

4 500 0.683 341.51 2584.93

5 500 0.621 310.46 2895.39

6 250 0.564 141.12 3036.51

7 250 0.513 128.29 3164.80

8 250 0.467 116.63 3281.43

9 250 0.424 106.02 3387.45

10 250 0.386 96.39 3483.84

11 1750 0.350 613.36 4097.20

12 1750 0.319 557.60 4654.81

13 2062.50 0.290 597.43 5252.24

14 2453.13 0.263 645.98 5898.22

15 2941.41 0.239 704.15 6602.37

16 3951.76 0.218 860.02 7462.39

17 4714.70 0.198 932.78 8395.17

18 5668.37 0.180 1019.51 9414.68

19 6860.46 0.164 1121.74 10536.42

20 8350.58 0.149 1241.26 11777.68

Total 44252.90 10777.68 101491.27

Initial investment 1000

NPV 100491.27

Project B:

Years Annual cash flow

Discounting

factors PV factor

Cumulative

CF

1 2000 0.909 1818.18 4818.18

2 1250 0.826 1033.06 5851.24

4

1 500 0.909 454.55 1454.55

2 500 0.826 413.22 1867.77

3 500 0.751 375.66 2243.43

4 500 0.683 341.51 2584.93

5 500 0.621 310.46 2895.39

6 250 0.564 141.12 3036.51

7 250 0.513 128.29 3164.80

8 250 0.467 116.63 3281.43

9 250 0.424 106.02 3387.45

10 250 0.386 96.39 3483.84

11 1750 0.350 613.36 4097.20

12 1750 0.319 557.60 4654.81

13 2062.50 0.290 597.43 5252.24

14 2453.13 0.263 645.98 5898.22

15 2941.41 0.239 704.15 6602.37

16 3951.76 0.218 860.02 7462.39

17 4714.70 0.198 932.78 8395.17

18 5668.37 0.180 1019.51 9414.68

19 6860.46 0.164 1121.74 10536.42

20 8350.58 0.149 1241.26 11777.68

Total 44252.90 10777.68 101491.27

Initial investment 1000

NPV 100491.27

Project B:

Years Annual cash flow

Discounting

factors PV factor

Cumulative

CF

1 2000 0.909 1818.18 4818.18

2 1250 0.826 1033.06 5851.24

4

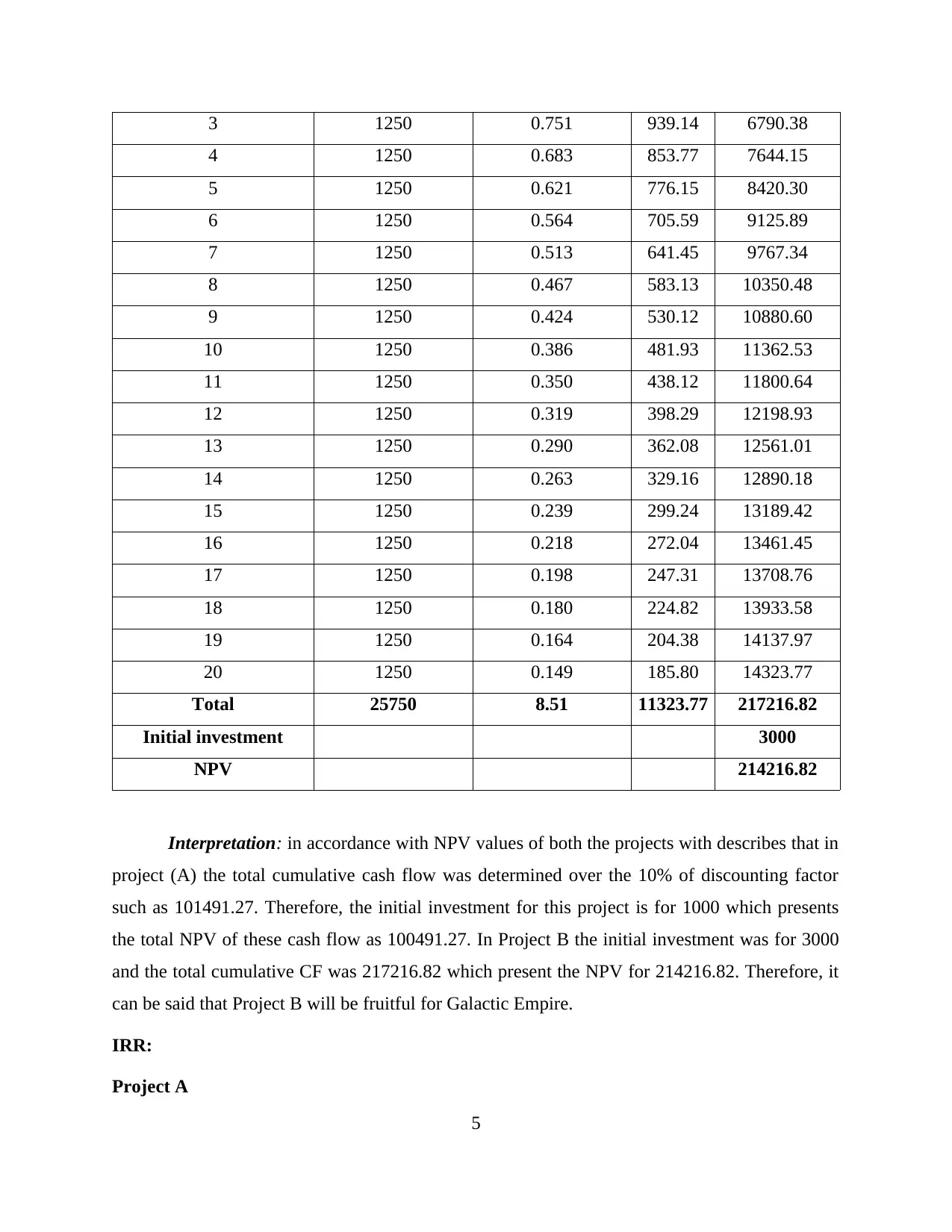

3 1250 0.751 939.14 6790.38

4 1250 0.683 853.77 7644.15

5 1250 0.621 776.15 8420.30

6 1250 0.564 705.59 9125.89

7 1250 0.513 641.45 9767.34

8 1250 0.467 583.13 10350.48

9 1250 0.424 530.12 10880.60

10 1250 0.386 481.93 11362.53

11 1250 0.350 438.12 11800.64

12 1250 0.319 398.29 12198.93

13 1250 0.290 362.08 12561.01

14 1250 0.263 329.16 12890.18

15 1250 0.239 299.24 13189.42

16 1250 0.218 272.04 13461.45

17 1250 0.198 247.31 13708.76

18 1250 0.180 224.82 13933.58

19 1250 0.164 204.38 14137.97

20 1250 0.149 185.80 14323.77

Total 25750 8.51 11323.77 217216.82

Initial investment 3000

NPV 214216.82

Interpretation: in accordance with NPV values of both the projects with describes that in

project (A) the total cumulative cash flow was determined over the 10% of discounting factor

such as 101491.27. Therefore, the initial investment for this project is for 1000 which presents

the total NPV of these cash flow as 100491.27. In Project B the initial investment was for 3000

and the total cumulative CF was 217216.82 which present the NPV for 214216.82. Therefore, it

can be said that Project B will be fruitful for Galactic Empire.

IRR:

Project A

5

4 1250 0.683 853.77 7644.15

5 1250 0.621 776.15 8420.30

6 1250 0.564 705.59 9125.89

7 1250 0.513 641.45 9767.34

8 1250 0.467 583.13 10350.48

9 1250 0.424 530.12 10880.60

10 1250 0.386 481.93 11362.53

11 1250 0.350 438.12 11800.64

12 1250 0.319 398.29 12198.93

13 1250 0.290 362.08 12561.01

14 1250 0.263 329.16 12890.18

15 1250 0.239 299.24 13189.42

16 1250 0.218 272.04 13461.45

17 1250 0.198 247.31 13708.76

18 1250 0.180 224.82 13933.58

19 1250 0.164 204.38 14137.97

20 1250 0.149 185.80 14323.77

Total 25750 8.51 11323.77 217216.82

Initial investment 3000

NPV 214216.82

Interpretation: in accordance with NPV values of both the projects with describes that in

project (A) the total cumulative cash flow was determined over the 10% of discounting factor

such as 101491.27. Therefore, the initial investment for this project is for 1000 which presents

the total NPV of these cash flow as 100491.27. In Project B the initial investment was for 3000

and the total cumulative CF was 217216.82 which present the NPV for 214216.82. Therefore, it

can be said that Project B will be fruitful for Galactic Empire.

IRR:

Project A

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

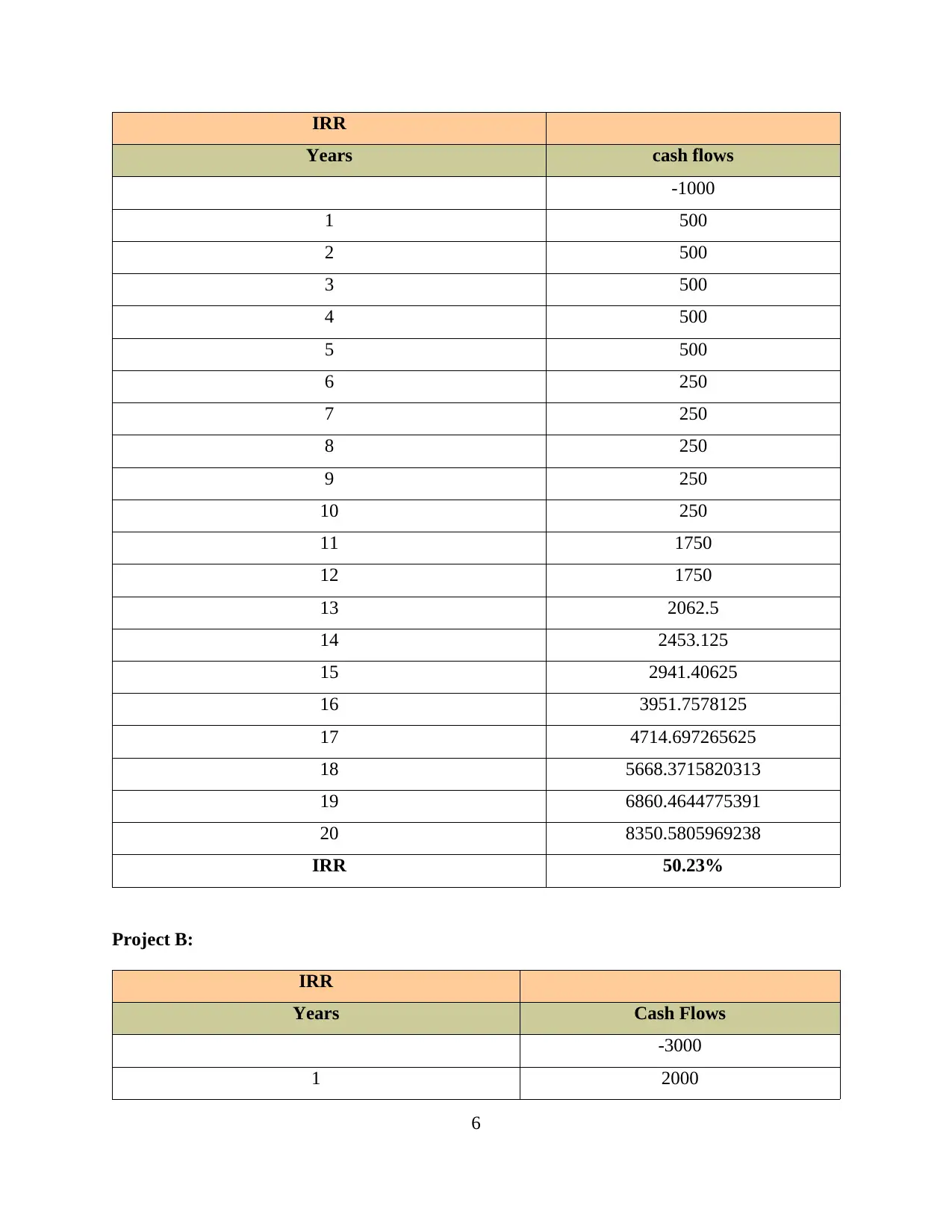

IRR

Years cash flows

-1000

1 500

2 500

3 500

4 500

5 500

6 250

7 250

8 250

9 250

10 250

11 1750

12 1750

13 2062.5

14 2453.125

15 2941.40625

16 3951.7578125

17 4714.697265625

18 5668.3715820313

19 6860.4644775391

20 8350.5805969238

IRR 50.23%

Project B:

IRR

Years Cash Flows

-3000

1 2000

6

Years cash flows

-1000

1 500

2 500

3 500

4 500

5 500

6 250

7 250

8 250

9 250

10 250

11 1750

12 1750

13 2062.5

14 2453.125

15 2941.40625

16 3951.7578125

17 4714.697265625

18 5668.3715820313

19 6860.4644775391

20 8350.5805969238

IRR 50.23%

Project B:

IRR

Years Cash Flows

-3000

1 2000

6

2 1250

3 1250

4 1250

5 1250

6 1250

7 1250

8 1250

9 1250

10 1250

11 1250

12 1250

13 1250

14 1250

15 1250

16 1250

17 1250

18 1250

19 1250

20 1250

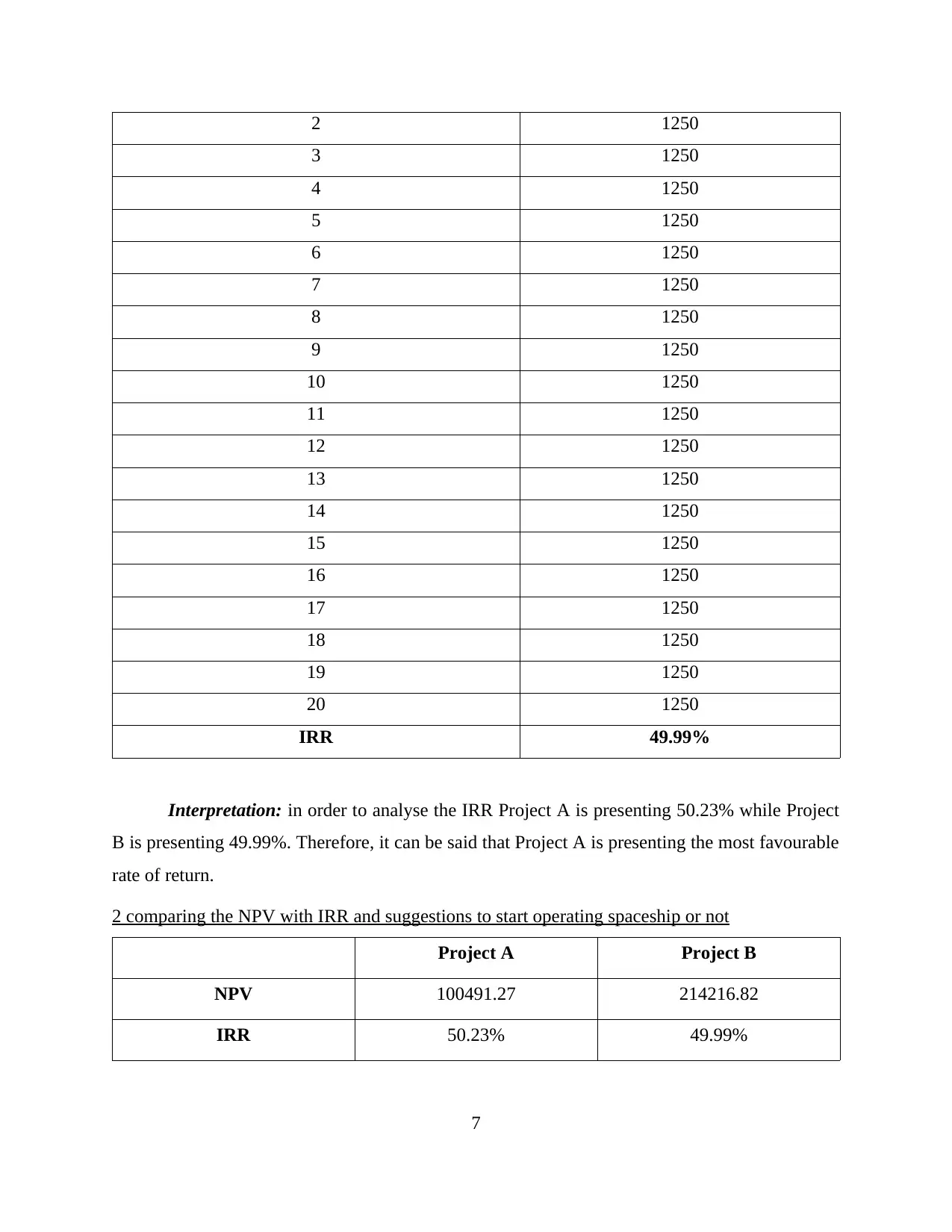

IRR 49.99%

Interpretation: in order to analyse the IRR Project A is presenting 50.23% while Project

B is presenting 49.99%. Therefore, it can be said that Project A is presenting the most favourable

rate of return.

2 comparing the NPV with IRR and suggestions to start operating spaceship or not

Project A Project B

NPV 100491.27 214216.82

IRR 50.23% 49.99%

7

3 1250

4 1250

5 1250

6 1250

7 1250

8 1250

9 1250

10 1250

11 1250

12 1250

13 1250

14 1250

15 1250

16 1250

17 1250

18 1250

19 1250

20 1250

IRR 49.99%

Interpretation: in order to analyse the IRR Project A is presenting 50.23% while Project

B is presenting 49.99%. Therefore, it can be said that Project A is presenting the most favourable

rate of return.

2 comparing the NPV with IRR and suggestions to start operating spaceship or not

Project A Project B

NPV 100491.27 214216.82

IRR 50.23% 49.99%

7

In terms with comparing the NPV and IRR of both the Projects it can be said that Project

B is facilitation the most appropriate NPV such as 214216.82 while Project A is presenting the

most favourable rate of returns such as 50.23%. Therefore, it can be said that both the projects

will be beneficial for the business and they must start such Spaceship operations.

3 Determining the limitations of NPV and IRR as well as ranking the projects

To present the profitability of the projects for Galactic Empire there has been analysis

based on the various planning tools such as NPV, IRR as well as determine the net cash flow of

such projects (Simunaniemi, Saarela and Muhos, 2017). There will be various limitations of such

techniques are as :

NPV: This method is used to analyse or determine the preset value of the future cash

flows. Therefore, it will be helpful for the business in terms or identifying the present value on

which they can become able to analyse the profitability of such investment as well as make

necessary changes in their business operations (Potes and et.al., 2017). Therefore, this will be

fruitful techniques for the business in terms of making the adequate estimation as planning the

forecasted costs for industrial operations.

Limitations of NPV:

It does not consider size of project which will be problematic for organisation in terms of

performing the operations.

It will be very complicated and difficult to determine as well as estimate cash flows for

such operations or projects (Limitations of Net Present Value, 2010).

There will be difficulties while determining the costs factors for such projects.

Limitations of IRR:

The calculation of the internal rate of return relies on varied number of external factors

that are unpredictable (Kerzner, 2013).

It should be noted that on the surface, the evaluation seems easy however prediction of

cash flows hides the large assumptions.

The assumptions involved in the internal rate of return calculations covers a major aspect

of human subjectivity that further increases the errors and biases.

8

B is facilitation the most appropriate NPV such as 214216.82 while Project A is presenting the

most favourable rate of returns such as 50.23%. Therefore, it can be said that both the projects

will be beneficial for the business and they must start such Spaceship operations.

3 Determining the limitations of NPV and IRR as well as ranking the projects

To present the profitability of the projects for Galactic Empire there has been analysis

based on the various planning tools such as NPV, IRR as well as determine the net cash flow of

such projects (Simunaniemi, Saarela and Muhos, 2017). There will be various limitations of such

techniques are as :

NPV: This method is used to analyse or determine the preset value of the future cash

flows. Therefore, it will be helpful for the business in terms or identifying the present value on

which they can become able to analyse the profitability of such investment as well as make

necessary changes in their business operations (Potes and et.al., 2017). Therefore, this will be

fruitful techniques for the business in terms of making the adequate estimation as planning the

forecasted costs for industrial operations.

Limitations of NPV:

It does not consider size of project which will be problematic for organisation in terms of

performing the operations.

It will be very complicated and difficult to determine as well as estimate cash flows for

such operations or projects (Limitations of Net Present Value, 2010).

There will be difficulties while determining the costs factors for such projects.

Limitations of IRR:

The calculation of the internal rate of return relies on varied number of external factors

that are unpredictable (Kerzner, 2013).

It should be noted that on the surface, the evaluation seems easy however prediction of

cash flows hides the large assumptions.

The assumptions involved in the internal rate of return calculations covers a major aspect

of human subjectivity that further increases the errors and biases.

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

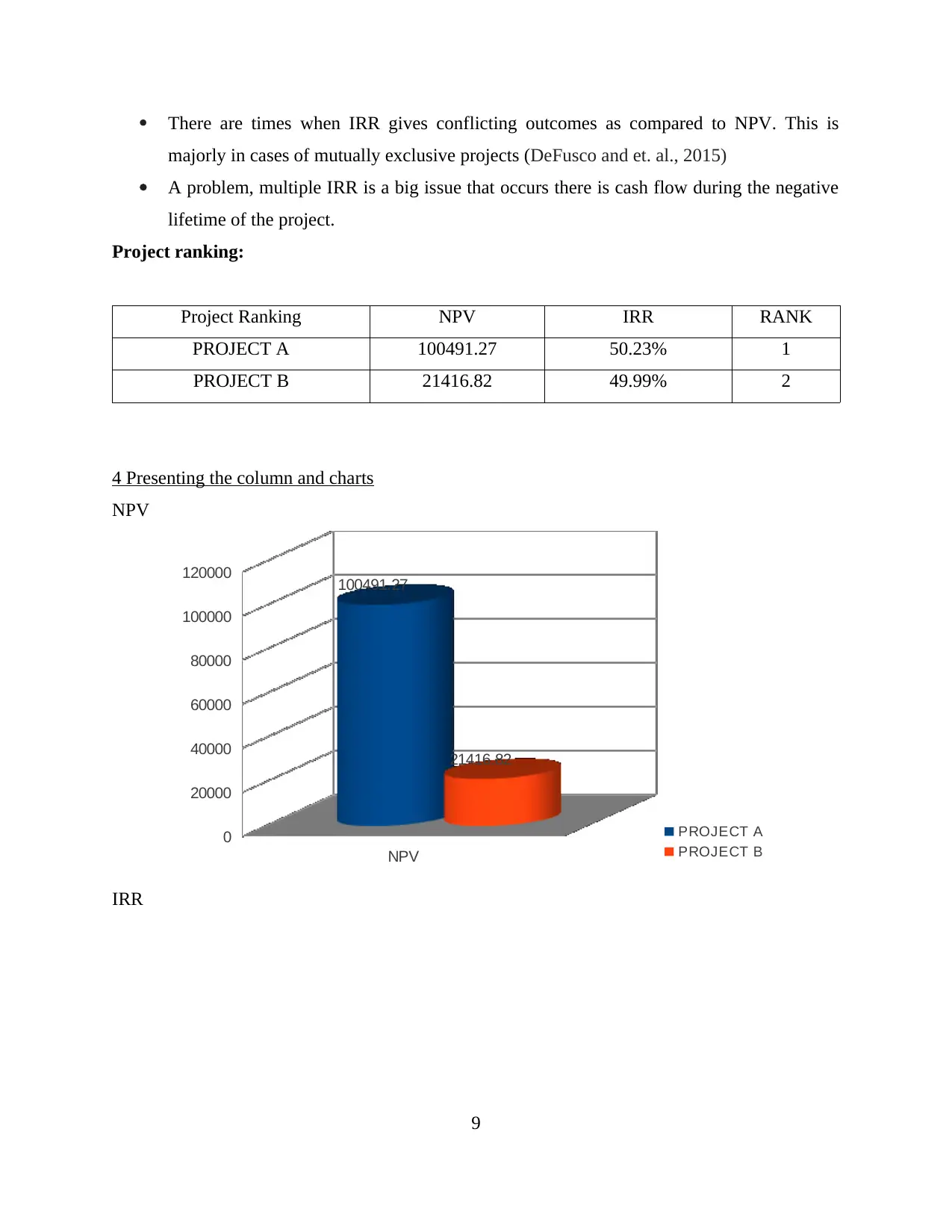

There are times when IRR gives conflicting outcomes as compared to NPV. This is

majorly in cases of mutually exclusive projects (DeFusco and et. al., 2015)

A problem, multiple IRR is a big issue that occurs there is cash flow during the negative

lifetime of the project.

Project ranking:

Project Ranking NPV IRR RANK

PROJECT A 100491.27 50.23% 1

PROJECT B 21416.82 49.99% 2

4 Presenting the column and charts

NPV

NPV

0

20000

40000

60000

80000

100000

120000 100491.27

21416.82

PROJECT A

PROJECT B

IRR

9

majorly in cases of mutually exclusive projects (DeFusco and et. al., 2015)

A problem, multiple IRR is a big issue that occurs there is cash flow during the negative

lifetime of the project.

Project ranking:

Project Ranking NPV IRR RANK

PROJECT A 100491.27 50.23% 1

PROJECT B 21416.82 49.99% 2

4 Presenting the column and charts

NPV

NPV

0

20000

40000

60000

80000

100000

120000 100491.27

21416.82

PROJECT A

PROJECT B

IRR

9

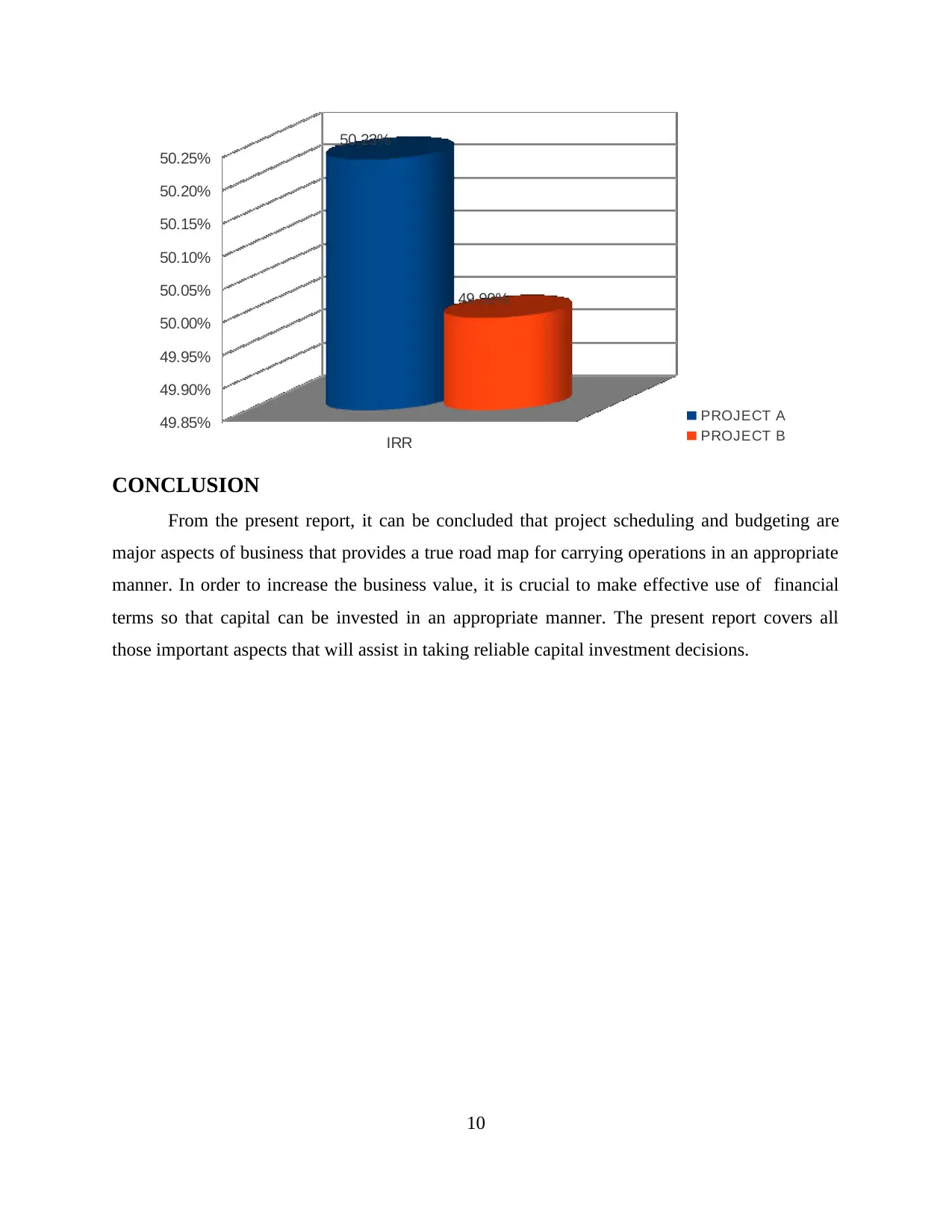

IRR

49.85%

49.90%

49.95%

50.00%

50.05%

50.10%

50.15%

50.20%

50.25%

50.23%

49.99%

PROJECT A

PROJECT B

CONCLUSION

From the present report, it can be concluded that project scheduling and budgeting are

major aspects of business that provides a true road map for carrying operations in an appropriate

manner. In order to increase the business value, it is crucial to make effective use of financial

terms so that capital can be invested in an appropriate manner. The present report covers all

those important aspects that will assist in taking reliable capital investment decisions.

10

49.85%

49.90%

49.95%

50.00%

50.05%

50.10%

50.15%

50.20%

50.25%

50.23%

49.99%

PROJECT A

PROJECT B

CONCLUSION

From the present report, it can be concluded that project scheduling and budgeting are

major aspects of business that provides a true road map for carrying operations in an appropriate

manner. In order to increase the business value, it is crucial to make effective use of financial

terms so that capital can be invested in an appropriate manner. The present report covers all

those important aspects that will assist in taking reliable capital investment decisions.

10

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.