In this Problem Set we will discuss about Principles of Economics. The below description is the overview of that problem set.

Part A:

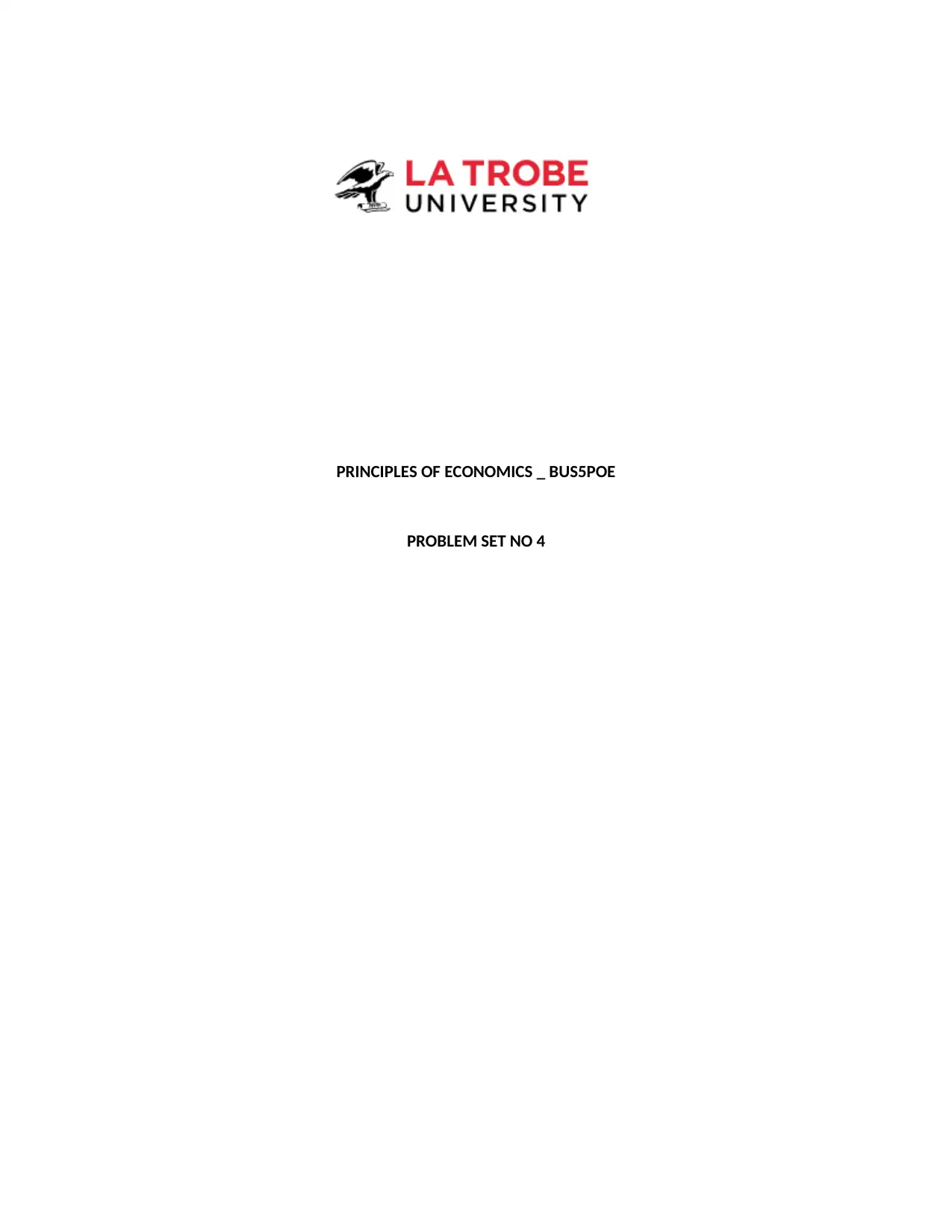

Decrease in the cost of creating computer chips causes the supply of computers to shift to the right, decreasing the equilibrium price and increasing the equilibrium quantity. The demand for typewriters decreases as they are replaced by computers.

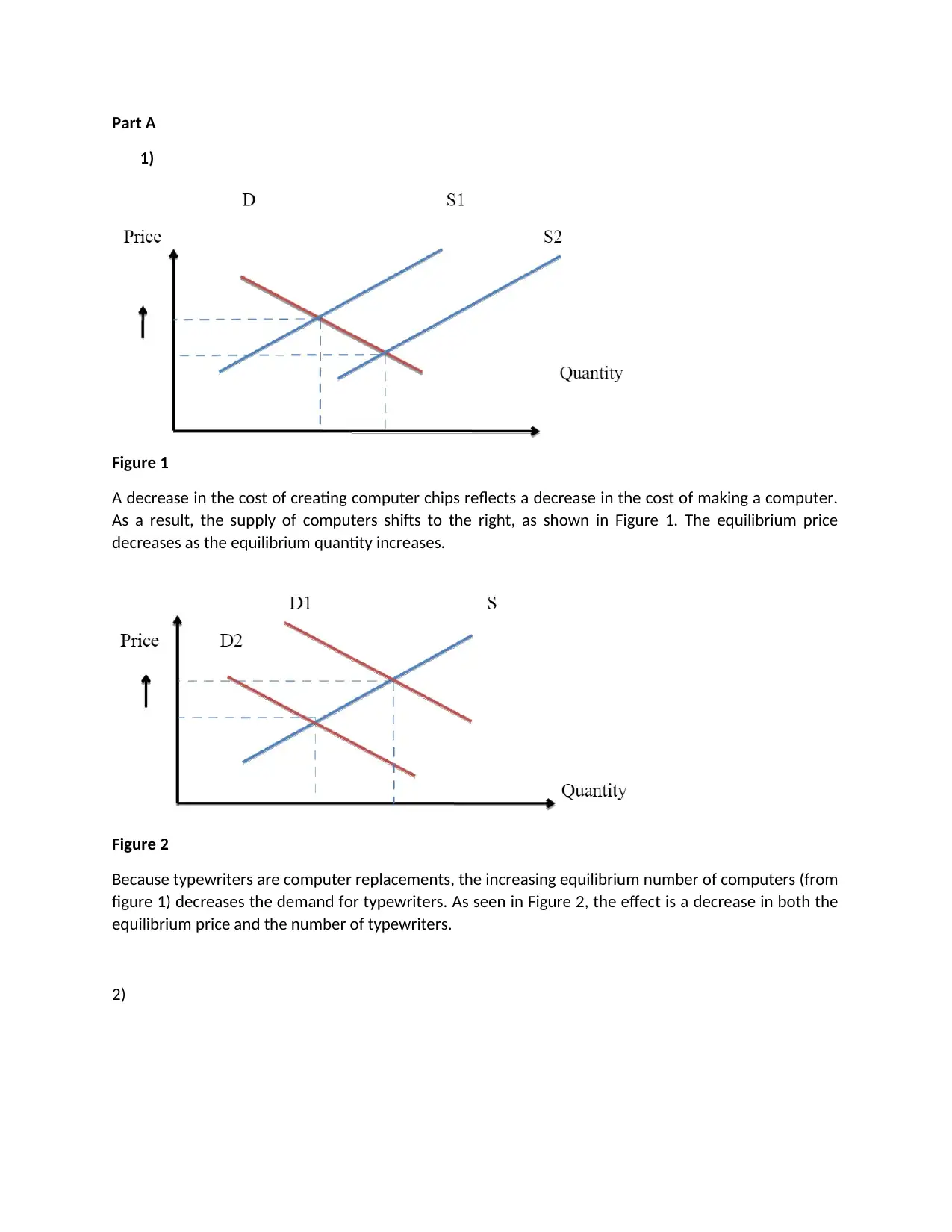

Increase in the price of mobile phones leads to an increase in the number of phones sold but decreases the demand for headphones (complementary goods), causing the equilibrium price and quantity of headphones to fall.

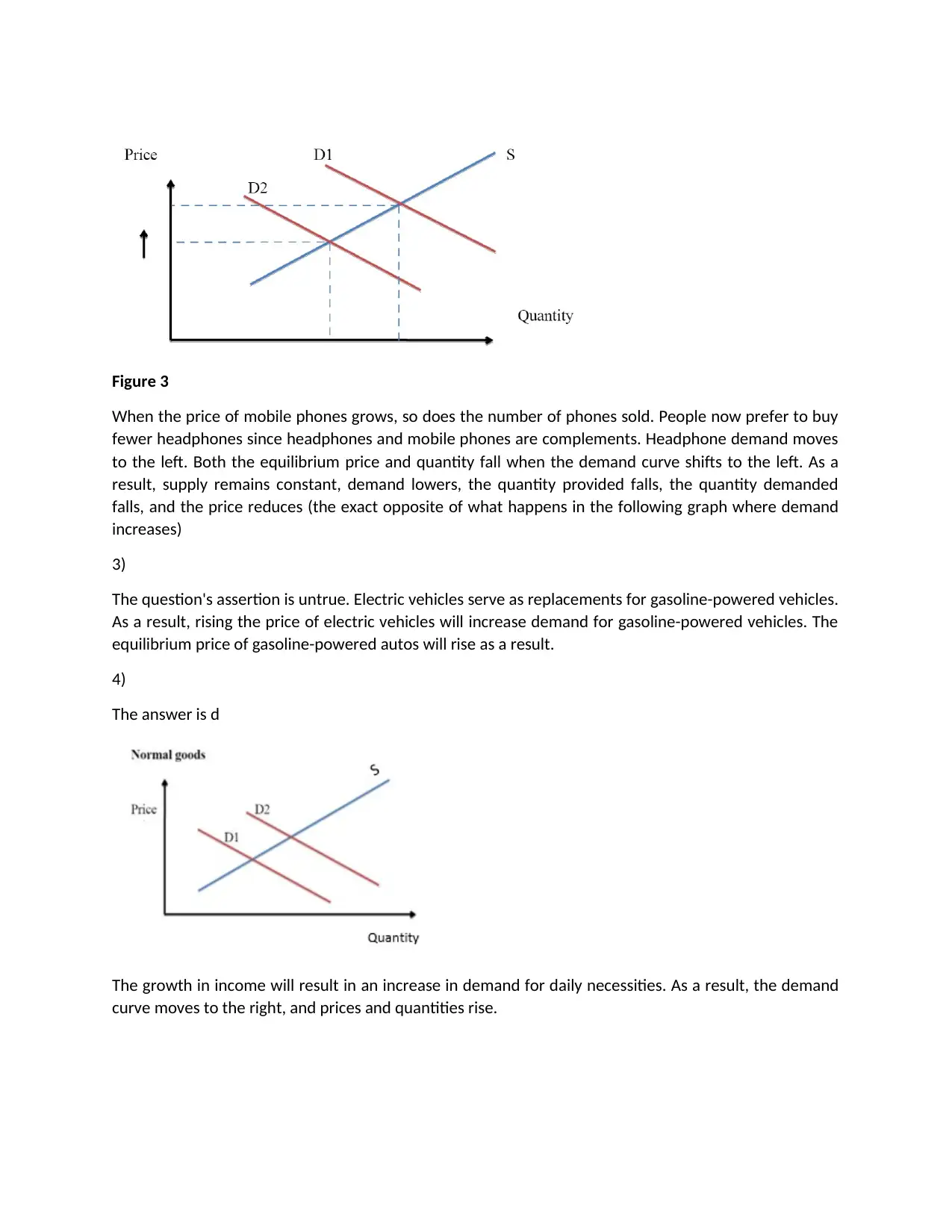

Raising the price of electric vehicles will increase the demand for gasoline-powered vehicles, causing the equilibrium price of gasoline-powered autos to rise.

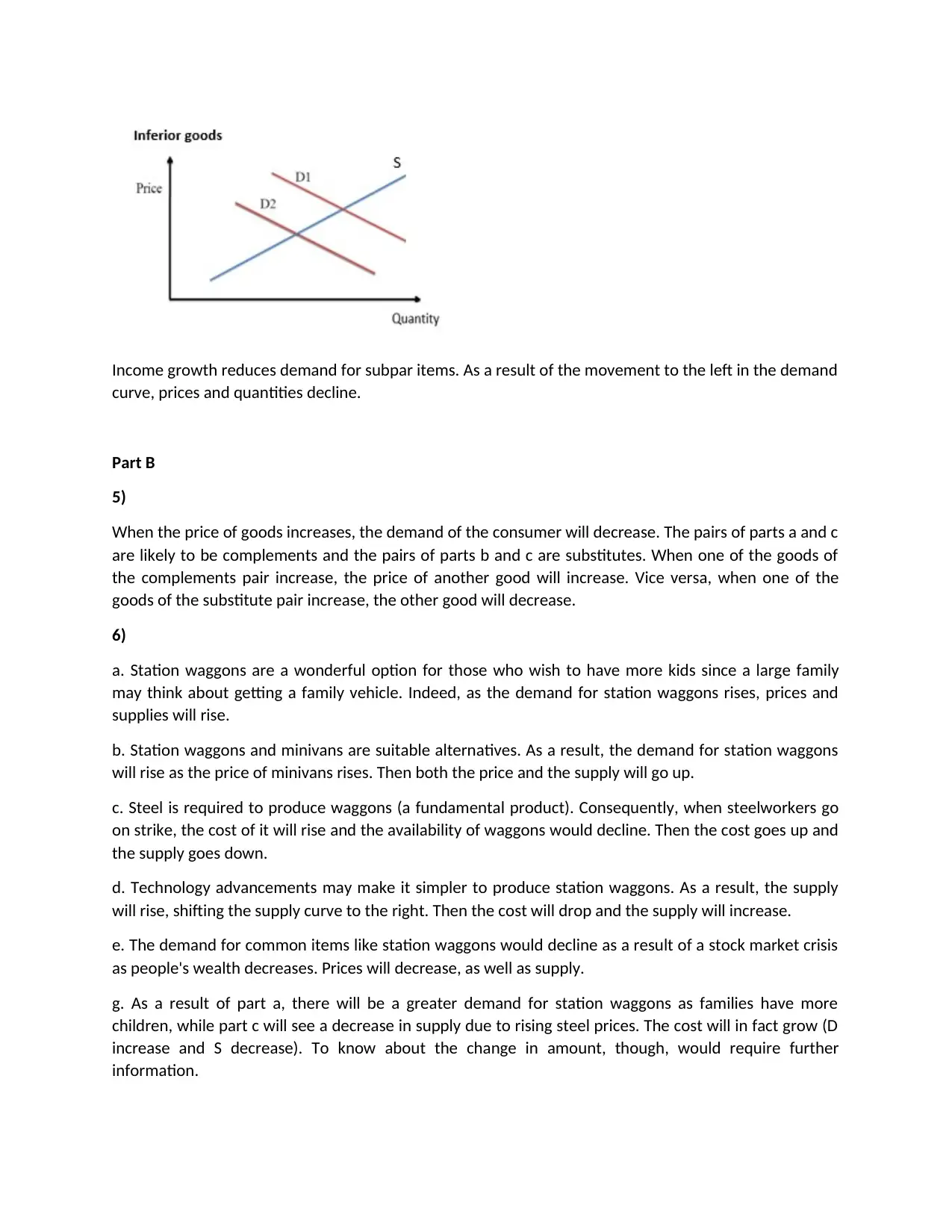

Growth in income leads to an increase in demand for daily necessities and a decrease in demand for subpar items.

Part B:

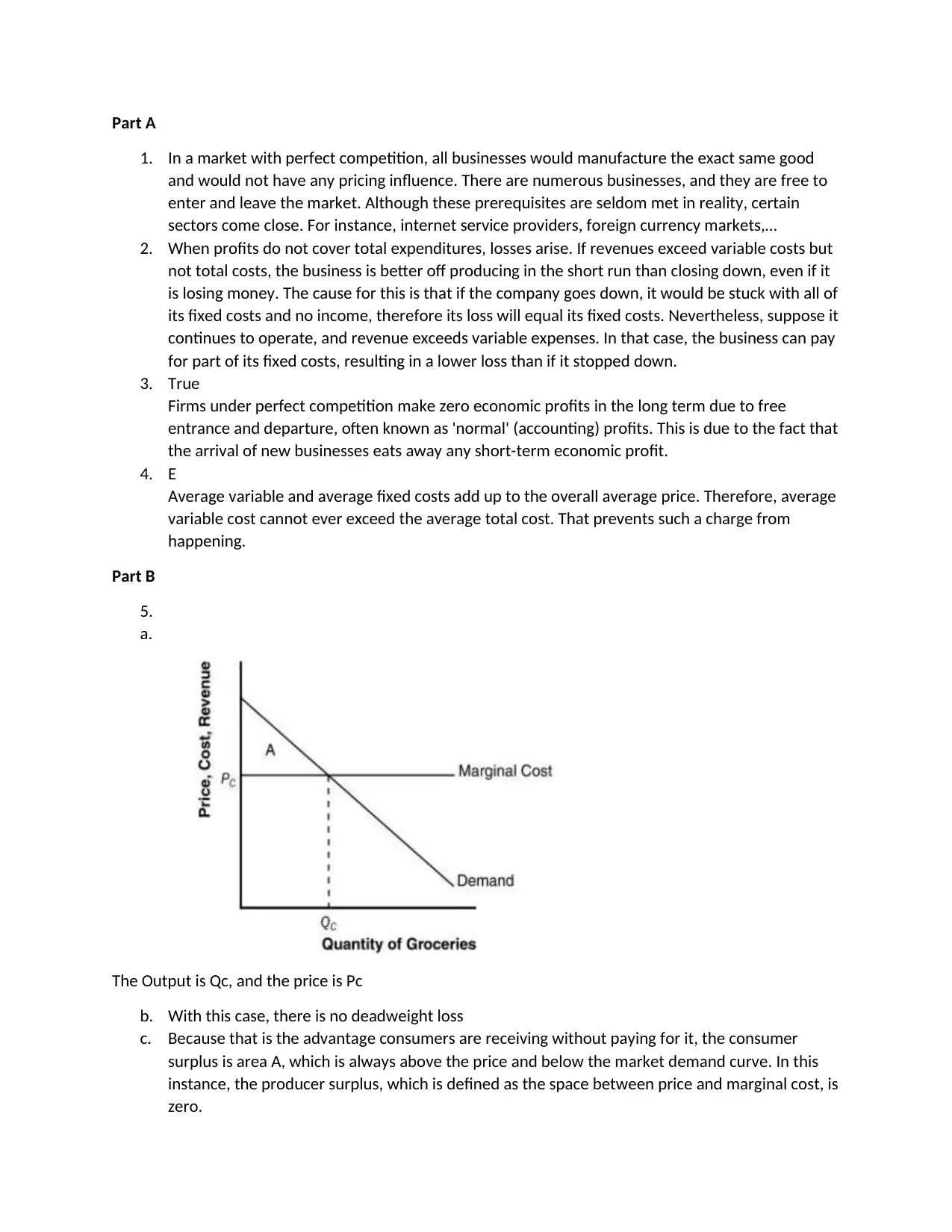

In a market with perfect competition, businesses produce the same goods and have no pricing power.

Losses occur when profits do not cover total costs. If revenues exceed variable costs but not total costs, businesses may still produce in the short run to avoid losses.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)