Business Analytics: Cost, Revenue, Profit, Correlation, and Breakeven

VerifiedAdded on 2023/06/04

|14

|3859

|315

Report

AI Summary

This business analytics report provides a detailed analysis of cost and revenue behavior, profit and loss calculations, and five-year projections for KB Ltd. It includes the development of a mathematical model for profit calculation, analysis of correlation between advertising expenditure and sales using the correlation coefficient and scatter diagrams, and calculation of breakeven points and margin of safety. The report also compares target profit with actual profit and analyzes the benefits and limitations of the breakeven model. The analysis utilizes business analytic techniques to provide insights into decision-making, data analysis, and statistical modeling, focusing on enhancing business performance through understanding cost functions and market dynamics.

Business Analytic

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

a) Developing a mathematical model using the given cost information................................3

b) Calculating the profit or loss using the given information.................................................4

c) Five year projection from January 2023 considering given adjustments...........................4

d) Analysing the cost and revenue behaviour of KB Ltd, before and after projections.........5

Question 2........................................................................................................................................6

a) Calculation of correlation coefficient and analysis of the results......................................6

b) Scatter diagram of data and analysing the pattern of relationship among two given variables

................................................................................................................................................7

c) Analysis of impact of advertising expenditure on sales, and other relevant marketing tactics

................................................................................................................................................8

Question 3........................................................................................................................................9

a) Calculation of breakeven point and margin of safety.........................................................9

b) Comparing the target profit with the actual one.................................................................9

c) Breakeven chart................................................................................................................10

d) Analysing the benefits and limitations of breakeven model............................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

a) Developing a mathematical model using the given cost information................................3

b) Calculating the profit or loss using the given information.................................................4

c) Five year projection from January 2023 considering given adjustments...........................4

d) Analysing the cost and revenue behaviour of KB Ltd, before and after projections.........5

Question 2........................................................................................................................................6

a) Calculation of correlation coefficient and analysis of the results......................................6

b) Scatter diagram of data and analysing the pattern of relationship among two given variables

................................................................................................................................................7

c) Analysis of impact of advertising expenditure on sales, and other relevant marketing tactics

................................................................................................................................................8

Question 3........................................................................................................................................9

a) Calculation of breakeven point and margin of safety.........................................................9

b) Comparing the target profit with the actual one.................................................................9

c) Breakeven chart................................................................................................................10

d) Analysing the benefits and limitations of breakeven model............................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Business analytics can be defined as a collection of restraints and methods for elucidating

business related problems utilising data analysis, quantitative techniques and other statistical

models. This involves repetitive and systematic examination of a company’s data focusing on

statistical analysis to drive decision making. Data-driven businesses are actively seeking ways to

treat their data as an asset of business and turning it in a competitive edge. The success of

business analytics rely upon the quality of data and skilled analysts who have an understanding

of technology and business, and a commitment to utilising data to generate understandings that

drive business decisions (Ariyarathna. and Peter, 2018). The report includes the brief analysis

and answers of the first three case studies in the given assessment. The questions includes the

analysis of costing and revenues behaviour, calculating profit or loss, correlation coefficient,

breakeven point and margin of safety, the costing projections, plotting scatter diagram, analysis

of the impact that comes due to expenses incurred on sales , the benefits and limitations of

breakeven model and much more.

MAIN BODY

Question 1

a) Development of a mathematical model by using the information regarding cost that has been

given

There is a mathematical model known as profit model which is a linear deterministic

algebraic model utilised implicitly by most of the cost accountants. It gives a framework for

modelling elements of cost like material, multi products, depreciation, etc. starting with profit

equals to sales subtracted by costs. It assist with a mutable theoretical foundation for spreadsheet

modellers. It allows modellers to run deterministic replications or “what if” type modelling to see

the effect of changes in price or quantity, or cost on profitability (Arora, 2018).

π = pq – (Fn + wq)

Where π stands for profit, p for sales price, Fn stands for fixed cost, w is variable per unit sold

and q stands for quantity sold.

Business analytics can be defined as a collection of restraints and methods for elucidating

business related problems utilising data analysis, quantitative techniques and other statistical

models. This involves repetitive and systematic examination of a company’s data focusing on

statistical analysis to drive decision making. Data-driven businesses are actively seeking ways to

treat their data as an asset of business and turning it in a competitive edge. The success of

business analytics rely upon the quality of data and skilled analysts who have an understanding

of technology and business, and a commitment to utilising data to generate understandings that

drive business decisions (Ariyarathna. and Peter, 2018). The report includes the brief analysis

and answers of the first three case studies in the given assessment. The questions includes the

analysis of costing and revenues behaviour, calculating profit or loss, correlation coefficient,

breakeven point and margin of safety, the costing projections, plotting scatter diagram, analysis

of the impact that comes due to expenses incurred on sales , the benefits and limitations of

breakeven model and much more.

MAIN BODY

Question 1

a) Development of a mathematical model by using the information regarding cost that has been

given

There is a mathematical model known as profit model which is a linear deterministic

algebraic model utilised implicitly by most of the cost accountants. It gives a framework for

modelling elements of cost like material, multi products, depreciation, etc. starting with profit

equals to sales subtracted by costs. It assist with a mutable theoretical foundation for spreadsheet

modellers. It allows modellers to run deterministic replications or “what if” type modelling to see

the effect of changes in price or quantity, or cost on profitability (Arora, 2018).

π = pq – (Fn + wq)

Where π stands for profit, p for sales price, Fn stands for fixed cost, w is variable per unit sold

and q stands for quantity sold.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

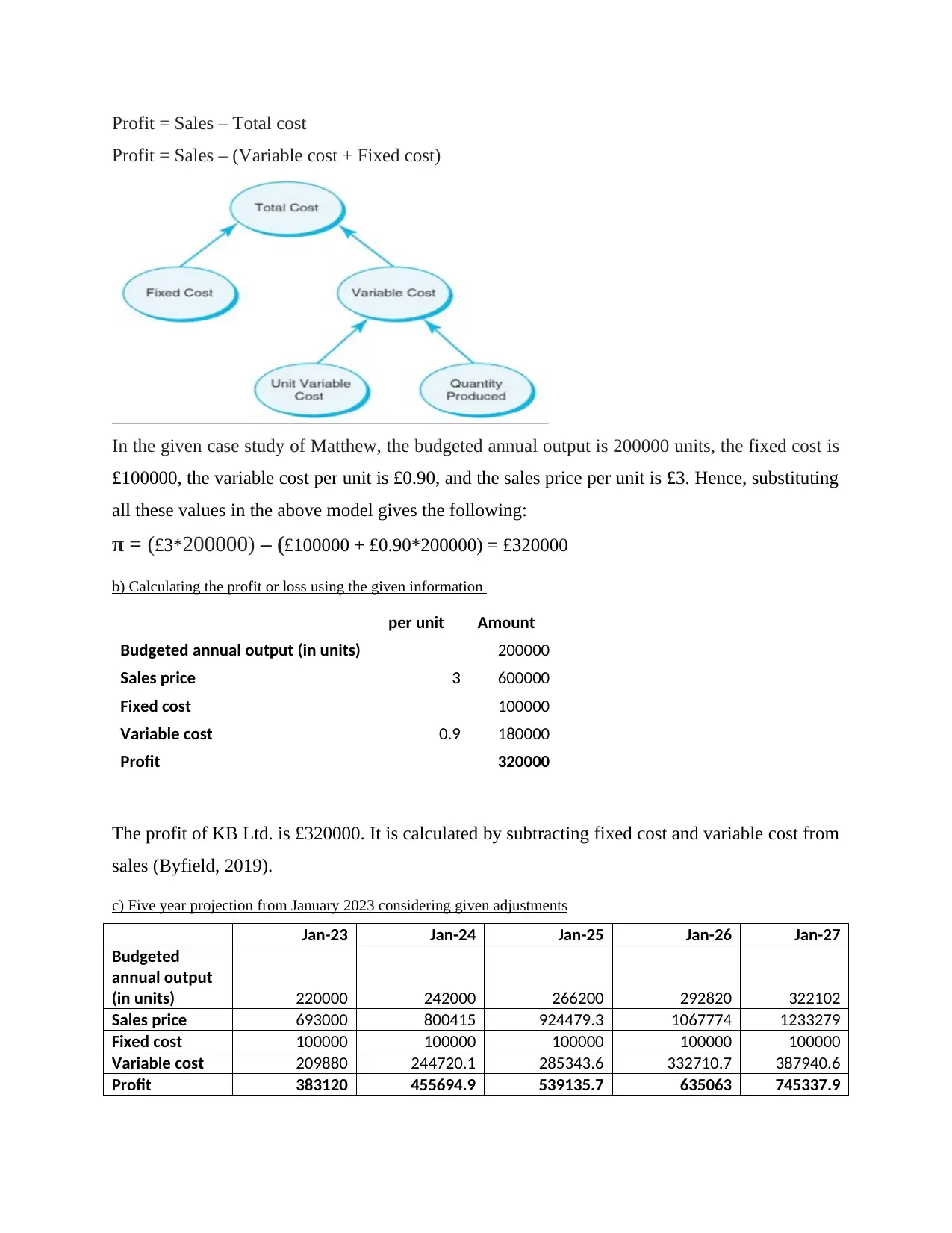

Profit = Sales – Total cost

Profit = Sales – (Variable cost + Fixed cost)

In the given case study of Matthew, the budgeted annual output is 200000 units, the fixed cost is

£100000, the variable cost per unit is £0.90, and the sales price per unit is £3. Hence, substituting

all these values in the above model gives the following:

π = (£3*200000) – (£100000 + £0.90*200000) = £320000

b) Calculating the profit or loss using the given information

per unit Amount

Budgeted annual output (in units) 200000

Sales price 3 600000

Fixed cost 100000

Variable cost 0.9 180000

Profit 320000

The profit of KB Ltd. is £320000. It is calculated by subtracting fixed cost and variable cost from

sales (Byfield, 2019).

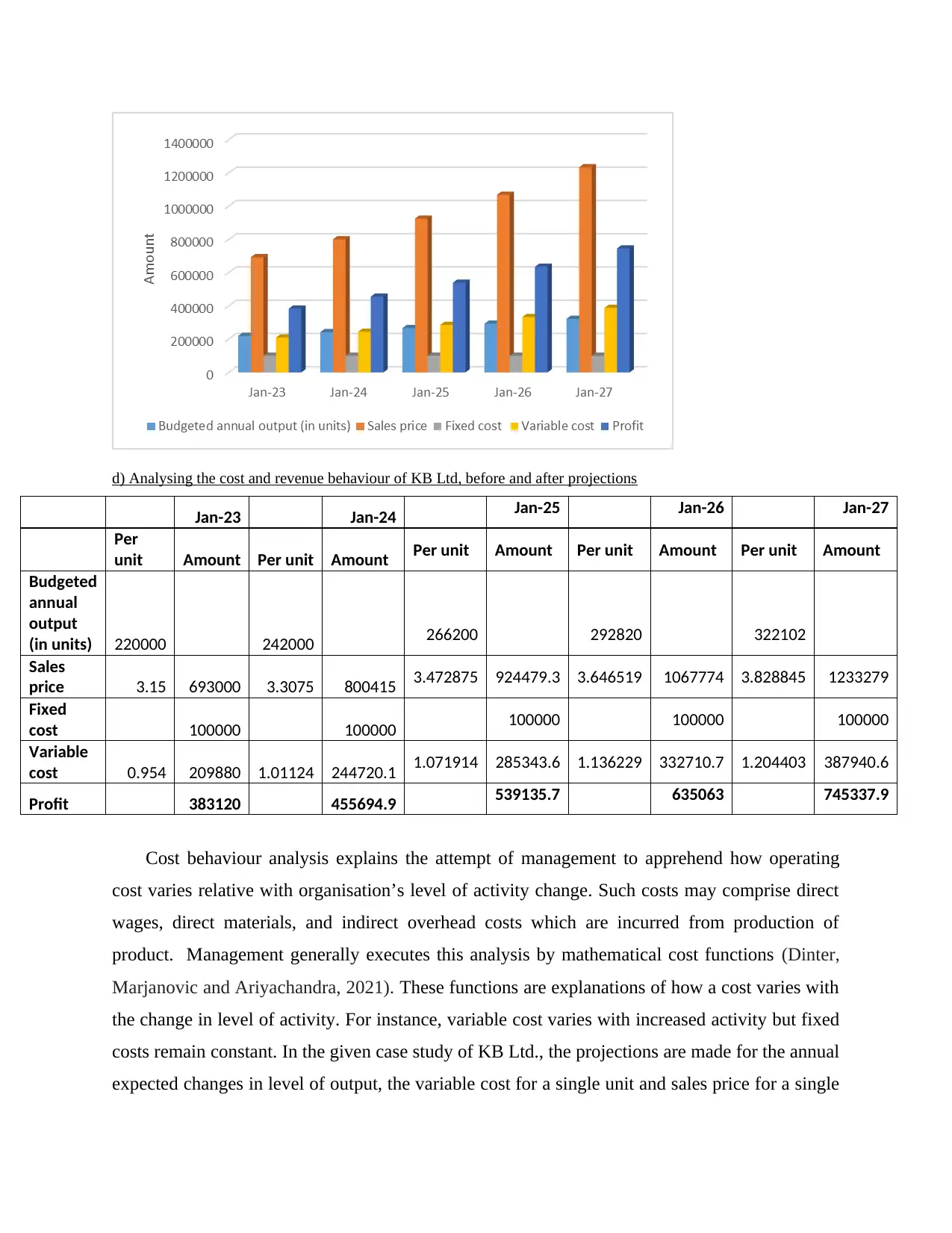

c) Five year projection from January 2023 considering given adjustments

Jan-23 Jan-24 Jan-25 Jan-26 Jan-27

Budgeted

annual output

(in units) 220000 242000 266200 292820 322102

Sales price 693000 800415 924479.3 1067774 1233279

Fixed cost 100000 100000 100000 100000 100000

Variable cost 209880 244720.1 285343.6 332710.7 387940.6

Profit 383120 455694.9 539135.7 635063 745337.9

Profit = Sales – (Variable cost + Fixed cost)

In the given case study of Matthew, the budgeted annual output is 200000 units, the fixed cost is

£100000, the variable cost per unit is £0.90, and the sales price per unit is £3. Hence, substituting

all these values in the above model gives the following:

π = (£3*200000) – (£100000 + £0.90*200000) = £320000

b) Calculating the profit or loss using the given information

per unit Amount

Budgeted annual output (in units) 200000

Sales price 3 600000

Fixed cost 100000

Variable cost 0.9 180000

Profit 320000

The profit of KB Ltd. is £320000. It is calculated by subtracting fixed cost and variable cost from

sales (Byfield, 2019).

c) Five year projection from January 2023 considering given adjustments

Jan-23 Jan-24 Jan-25 Jan-26 Jan-27

Budgeted

annual output

(in units) 220000 242000 266200 292820 322102

Sales price 693000 800415 924479.3 1067774 1233279

Fixed cost 100000 100000 100000 100000 100000

Variable cost 209880 244720.1 285343.6 332710.7 387940.6

Profit 383120 455694.9 539135.7 635063 745337.9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d) Analysing the cost and revenue behaviour of KB Ltd, before and after projections

Jan-23 Jan-24 Jan-25 Jan-26 Jan-27

Per

unit Amount Per unit Amount Per unit Amount Per unit Amount Per unit Amount

Budgeted

annual

output

(in units) 220000 242000 266200 292820 322102

Sales

price 3.15 693000 3.3075 800415 3.472875 924479.3 3.646519 1067774 3.828845 1233279

Fixed

cost 100000 100000 100000 100000 100000

Variable

cost 0.954 209880 1.01124 244720.1 1.071914 285343.6 1.136229 332710.7 1.204403 387940.6

Profit 383120 455694.9 539135.7 635063 745337.9

Cost behaviour analysis explains the attempt of management to apprehend how operating

cost varies relative with organisation’s level of activity change. Such costs may comprise direct

wages, direct materials, and indirect overhead costs which are incurred from production of

product. Management generally executes this analysis by mathematical cost functions (Dinter,

Marjanovic and Ariyachandra, 2021). These functions are explanations of how a cost varies with

the change in level of activity. For instance, variable cost varies with increased activity but fixed

costs remain constant. In the given case study of KB Ltd., the projections are made for the annual

expected changes in level of output, the variable cost for a single unit and sales price for a single

Jan-23 Jan-24 Jan-25 Jan-26 Jan-27

Per

unit Amount Per unit Amount Per unit Amount Per unit Amount Per unit Amount

Budgeted

annual

output

(in units) 220000 242000 266200 292820 322102

Sales

price 3.15 693000 3.3075 800415 3.472875 924479.3 3.646519 1067774 3.828845 1233279

Fixed

cost 100000 100000 100000 100000 100000

Variable

cost 0.954 209880 1.01124 244720.1 1.071914 285343.6 1.136229 332710.7 1.204403 387940.6

Profit 383120 455694.9 539135.7 635063 745337.9

Cost behaviour analysis explains the attempt of management to apprehend how operating

cost varies relative with organisation’s level of activity change. Such costs may comprise direct

wages, direct materials, and indirect overhead costs which are incurred from production of

product. Management generally executes this analysis by mathematical cost functions (Dinter,

Marjanovic and Ariyachandra, 2021). These functions are explanations of how a cost varies with

the change in level of activity. For instance, variable cost varies with increased activity but fixed

costs remain constant. In the given case study of KB Ltd., the projections are made for the annual

expected changes in level of output, the variable cost for a single unit and sales price for a single

unit. The variable cost and sales price are increasing every year but the fixed cost remains same

throughout the 5 years. The resultant is the increasing profit every year. The profit increased

from 383120 in 2023 to 745337.9 in 2027. The sales increased from 693000 in 2023 to 1233279

in 2027.

Question 2

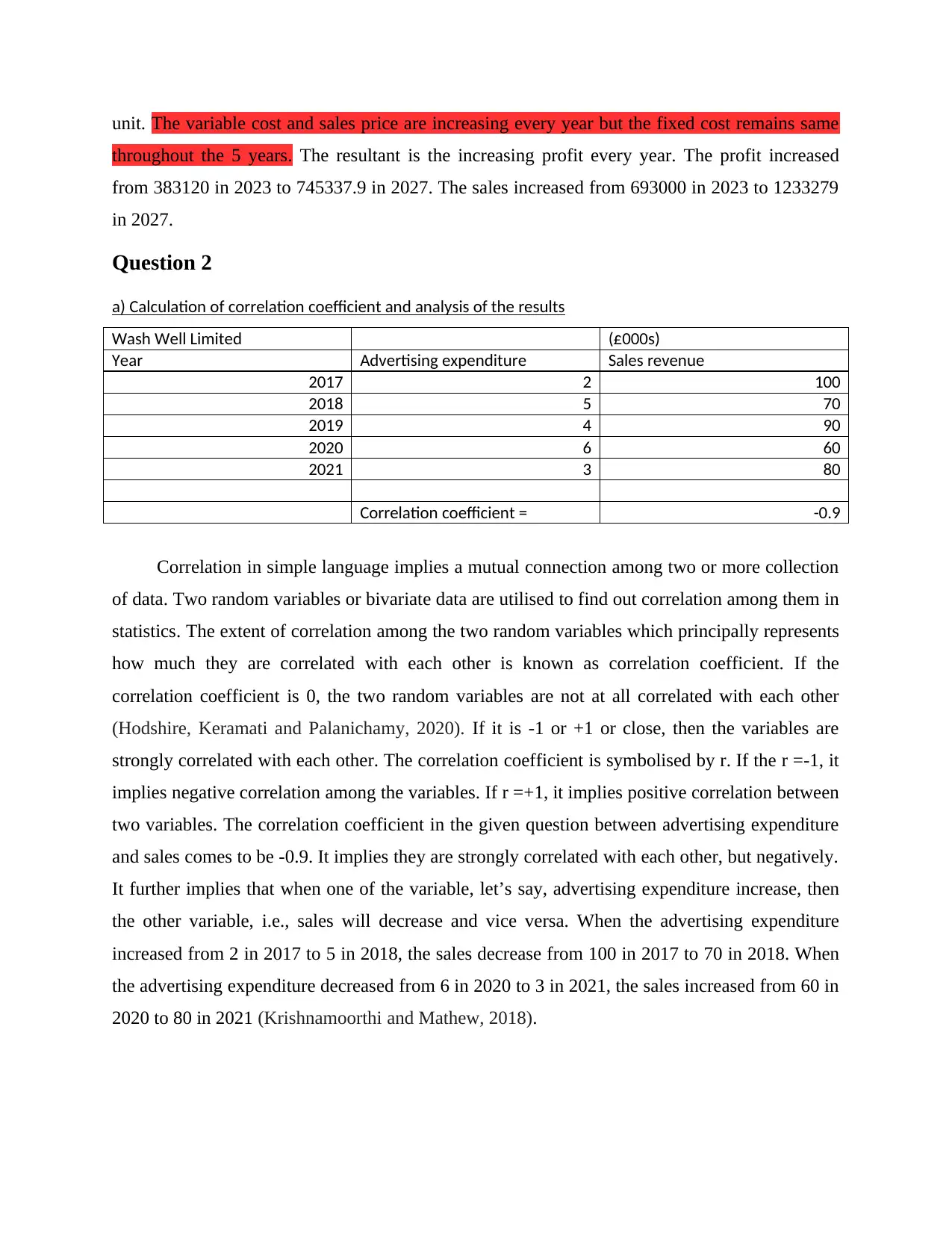

a) Calculation of correlation coefficient and analysis of the results

Wash Well Limited (£000s)

Year Advertising expenditure Sales revenue

2017 2 100

2018 5 70

2019 4 90

2020 6 60

2021 3 80

Correlation coefficient = -0.9

Correlation in simple language implies a mutual connection among two or more collection

of data. Two random variables or bivariate data are utilised to find out correlation among them in

statistics. The extent of correlation among the two random variables which principally represents

how much they are correlated with each other is known as correlation coefficient. If the

correlation coefficient is 0, the two random variables are not at all correlated with each other

(Hodshire, Keramati and Palanichamy, 2020). If it is -1 or +1 or close, then the variables are

strongly correlated with each other. The correlation coefficient is symbolised by r. If the r =-1, it

implies negative correlation among the variables. If r =+1, it implies positive correlation between

two variables. The correlation coefficient in the given question between advertising expenditure

and sales comes to be -0.9. It implies they are strongly correlated with each other, but negatively.

It further implies that when one of the variable, let’s say, advertising expenditure increase, then

the other variable, i.e., sales will decrease and vice versa. When the advertising expenditure

increased from 2 in 2017 to 5 in 2018, the sales decrease from 100 in 2017 to 70 in 2018. When

the advertising expenditure decreased from 6 in 2020 to 3 in 2021, the sales increased from 60 in

2020 to 80 in 2021 (Krishnamoorthi and Mathew, 2018).

throughout the 5 years. The resultant is the increasing profit every year. The profit increased

from 383120 in 2023 to 745337.9 in 2027. The sales increased from 693000 in 2023 to 1233279

in 2027.

Question 2

a) Calculation of correlation coefficient and analysis of the results

Wash Well Limited (£000s)

Year Advertising expenditure Sales revenue

2017 2 100

2018 5 70

2019 4 90

2020 6 60

2021 3 80

Correlation coefficient = -0.9

Correlation in simple language implies a mutual connection among two or more collection

of data. Two random variables or bivariate data are utilised to find out correlation among them in

statistics. The extent of correlation among the two random variables which principally represents

how much they are correlated with each other is known as correlation coefficient. If the

correlation coefficient is 0, the two random variables are not at all correlated with each other

(Hodshire, Keramati and Palanichamy, 2020). If it is -1 or +1 or close, then the variables are

strongly correlated with each other. The correlation coefficient is symbolised by r. If the r =-1, it

implies negative correlation among the variables. If r =+1, it implies positive correlation between

two variables. The correlation coefficient in the given question between advertising expenditure

and sales comes to be -0.9. It implies they are strongly correlated with each other, but negatively.

It further implies that when one of the variable, let’s say, advertising expenditure increase, then

the other variable, i.e., sales will decrease and vice versa. When the advertising expenditure

increased from 2 in 2017 to 5 in 2018, the sales decrease from 100 in 2017 to 70 in 2018. When

the advertising expenditure decreased from 6 in 2020 to 3 in 2021, the sales increased from 60 in

2020 to 80 in 2021 (Krishnamoorthi and Mathew, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

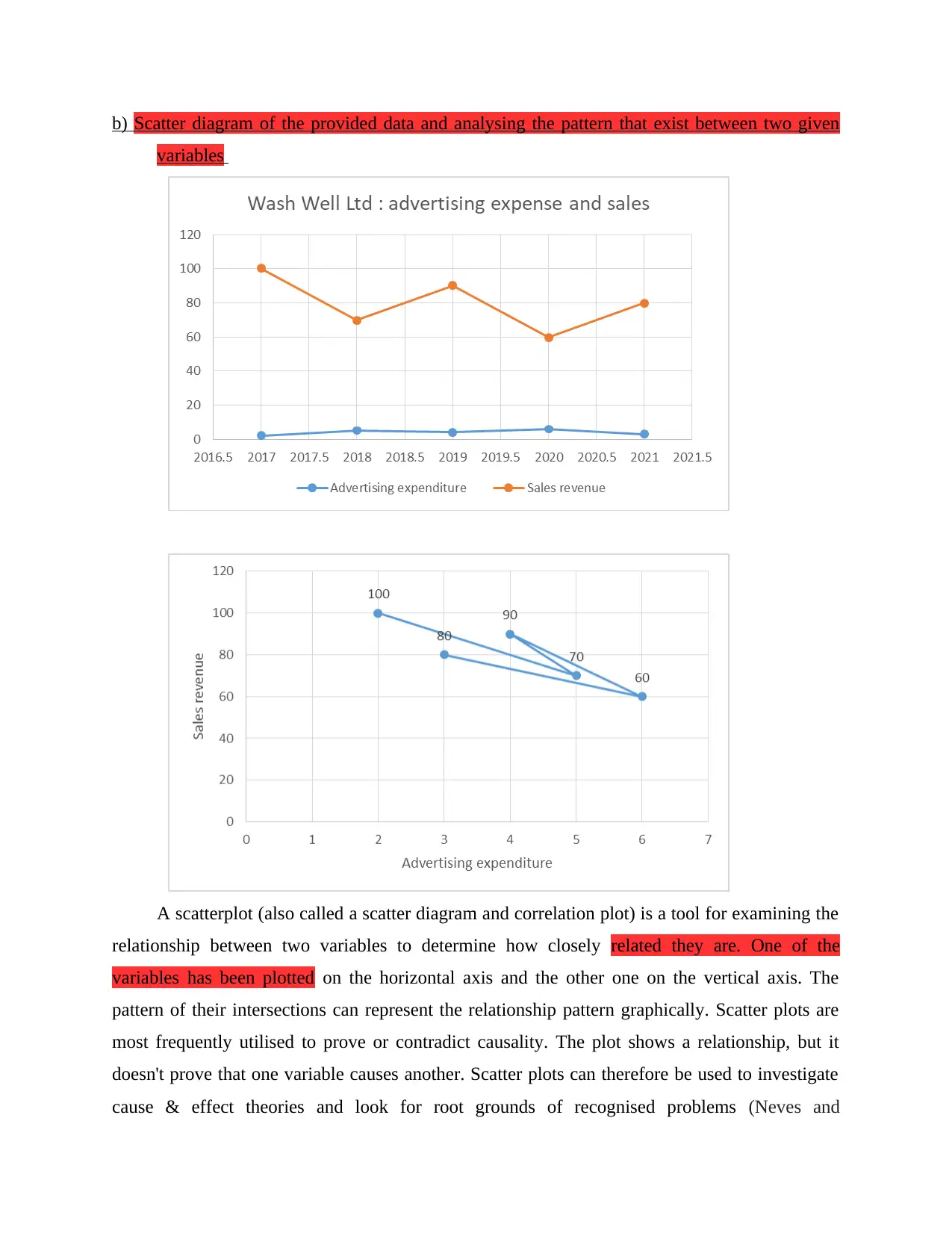

b) Scatter diagram of the provided data and analysing the pattern that exist between two given

variables

A scatterplot (also called a scatter diagram and correlation plot) is a tool for examining the

relationship between two variables to determine how closely related they are. One of the

variables has been plotted on the horizontal axis and the other one on the vertical axis. The

pattern of their intersections can represent the relationship pattern graphically. Scatter plots are

most frequently utilised to prove or contradict causality. The plot shows a relationship, but it

doesn't prove that one variable causes another. Scatter plots can therefore be used to investigate

cause & effect theories and look for root grounds of recognised problems (Neves and

variables

A scatterplot (also called a scatter diagram and correlation plot) is a tool for examining the

relationship between two variables to determine how closely related they are. One of the

variables has been plotted on the horizontal axis and the other one on the vertical axis. The

pattern of their intersections can represent the relationship pattern graphically. Scatter plots are

most frequently utilised to prove or contradict causality. The plot shows a relationship, but it

doesn't prove that one variable causes another. Scatter plots can therefore be used to investigate

cause & effect theories and look for root grounds of recognised problems (Neves and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bernardino, 2021). When plotted the points of the data, the closer they come to form a straight

line, the higher the correlation will be among the two variables, or it can also be said as the

stronger the relationship. If the plotted points of data create a straight line starting from near the

origin out to high y values, it is said to be in positive correlation. In the given case, the

advertising expenditure and sales scatter diagram is shown in the above chart. The lines are

moving downward representing the negative correlation among the two of them. And the lines

are coming closer to from a staright line, this shows the strong correltion among the two (Otola

and Grabowska, 2020).

c) Analysis of impact of advertising expenditure on sales, and other relevant marketing tactics

Although the two words are frequently used interchangeably, advertising and promotion

refer to distinct parts of a company's marketing strategy. Advertising is concerned with taking

action to increase brand awareness and create long period profitability, and promotions provide

instant revenue to an organisation by having a straight influence over price of goods and

services. Both can affect sales, but sales are directly related to the amount of money business

brings in.

Enhancing value: Advertising helps add value to the business and build the reputation. There are

two ways for this to happen. One is to buy advertising space in newspapers, magazines, and

social media or through editorial coverage. Editorial reporting is the goal of many small

enterprises ideally. It costs little and can have a lasting impact on a company's reputation.

Essentially, this is regarding getting publicity. Get in touch with local newspaper, community

organizations and clubs. Get involved in promoting community events or sponsor a team. These

are all ways to spread the name of company without expending money straight on advertising

(Paczkowski Pramanik and Uddin, 2021).

Reputation of Brand: Other than these conventional ways of increasing brand equity, businesses

should also pay attention to their brand reputation. A strong brand reputation has a direct impact

on sales as it gives customers confidence to purchase your products and services. Management

of reputation is regarding understanding the impact of client perceptions on a company's

prospects of revenue. The idea here is to control expectation of customer, reply rapidly to issues

and problems, and constantly conduct business in an ethical manner. The concern for reputation

should extend not only to all forms of marketing and advertising, but also to the approach to

customer service.

line, the higher the correlation will be among the two variables, or it can also be said as the

stronger the relationship. If the plotted points of data create a straight line starting from near the

origin out to high y values, it is said to be in positive correlation. In the given case, the

advertising expenditure and sales scatter diagram is shown in the above chart. The lines are

moving downward representing the negative correlation among the two of them. And the lines

are coming closer to from a staright line, this shows the strong correltion among the two (Otola

and Grabowska, 2020).

c) Analysis of impact of advertising expenditure on sales, and other relevant marketing tactics

Although the two words are frequently used interchangeably, advertising and promotion

refer to distinct parts of a company's marketing strategy. Advertising is concerned with taking

action to increase brand awareness and create long period profitability, and promotions provide

instant revenue to an organisation by having a straight influence over price of goods and

services. Both can affect sales, but sales are directly related to the amount of money business

brings in.

Enhancing value: Advertising helps add value to the business and build the reputation. There are

two ways for this to happen. One is to buy advertising space in newspapers, magazines, and

social media or through editorial coverage. Editorial reporting is the goal of many small

enterprises ideally. It costs little and can have a lasting impact on a company's reputation.

Essentially, this is regarding getting publicity. Get in touch with local newspaper, community

organizations and clubs. Get involved in promoting community events or sponsor a team. These

are all ways to spread the name of company without expending money straight on advertising

(Paczkowski Pramanik and Uddin, 2021).

Reputation of Brand: Other than these conventional ways of increasing brand equity, businesses

should also pay attention to their brand reputation. A strong brand reputation has a direct impact

on sales as it gives customers confidence to purchase your products and services. Management

of reputation is regarding understanding the impact of client perceptions on a company's

prospects of revenue. The idea here is to control expectation of customer, reply rapidly to issues

and problems, and constantly conduct business in an ethical manner. The concern for reputation

should extend not only to all forms of marketing and advertising, but also to the approach to

customer service.

Sales promotion: Promotions are designed to directly increase sales. There are many ways to

drive sales, but they all have to do with providing value and incentives to consumers. For

instance, offering free trials of products and services, issuing coupons, offering discounts, and

running free product contests. All of these methods are aimed at getting customers to spend their

money (Sheikh and Goje, 2021).

Question 3

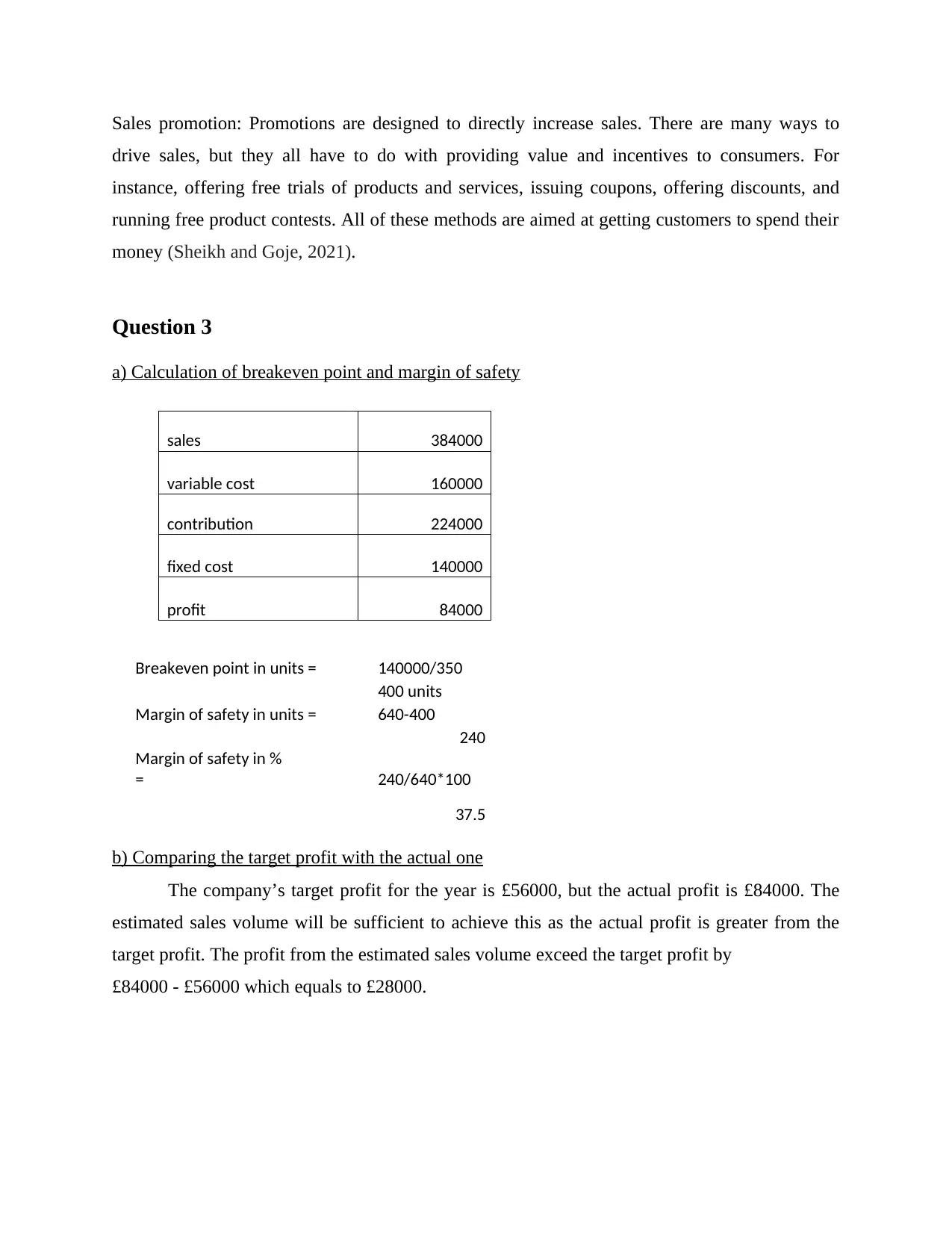

a) Calculation of breakeven point and margin of safety

b) Comparing the target profit with the actual one

The company’s target profit for the year is £56000, but the actual profit is £84000. The

estimated sales volume will be sufficient to achieve this as the actual profit is greater from the

target profit. The profit from the estimated sales volume exceed the target profit by

£84000 - £56000 which equals to £28000.

sales 384000

variable cost 160000

contribution 224000

fixed cost 140000

profit 84000

Breakeven point in units = 140000/350

400 units

Margin of safety in units = 640-400

240

Margin of safety in %

= 240/640*100

37.5

drive sales, but they all have to do with providing value and incentives to consumers. For

instance, offering free trials of products and services, issuing coupons, offering discounts, and

running free product contests. All of these methods are aimed at getting customers to spend their

money (Sheikh and Goje, 2021).

Question 3

a) Calculation of breakeven point and margin of safety

b) Comparing the target profit with the actual one

The company’s target profit for the year is £56000, but the actual profit is £84000. The

estimated sales volume will be sufficient to achieve this as the actual profit is greater from the

target profit. The profit from the estimated sales volume exceed the target profit by

£84000 - £56000 which equals to £28000.

sales 384000

variable cost 160000

contribution 224000

fixed cost 140000

profit 84000

Breakeven point in units = 140000/350

400 units

Margin of safety in units = 640-400

240

Margin of safety in %

= 240/640*100

37.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

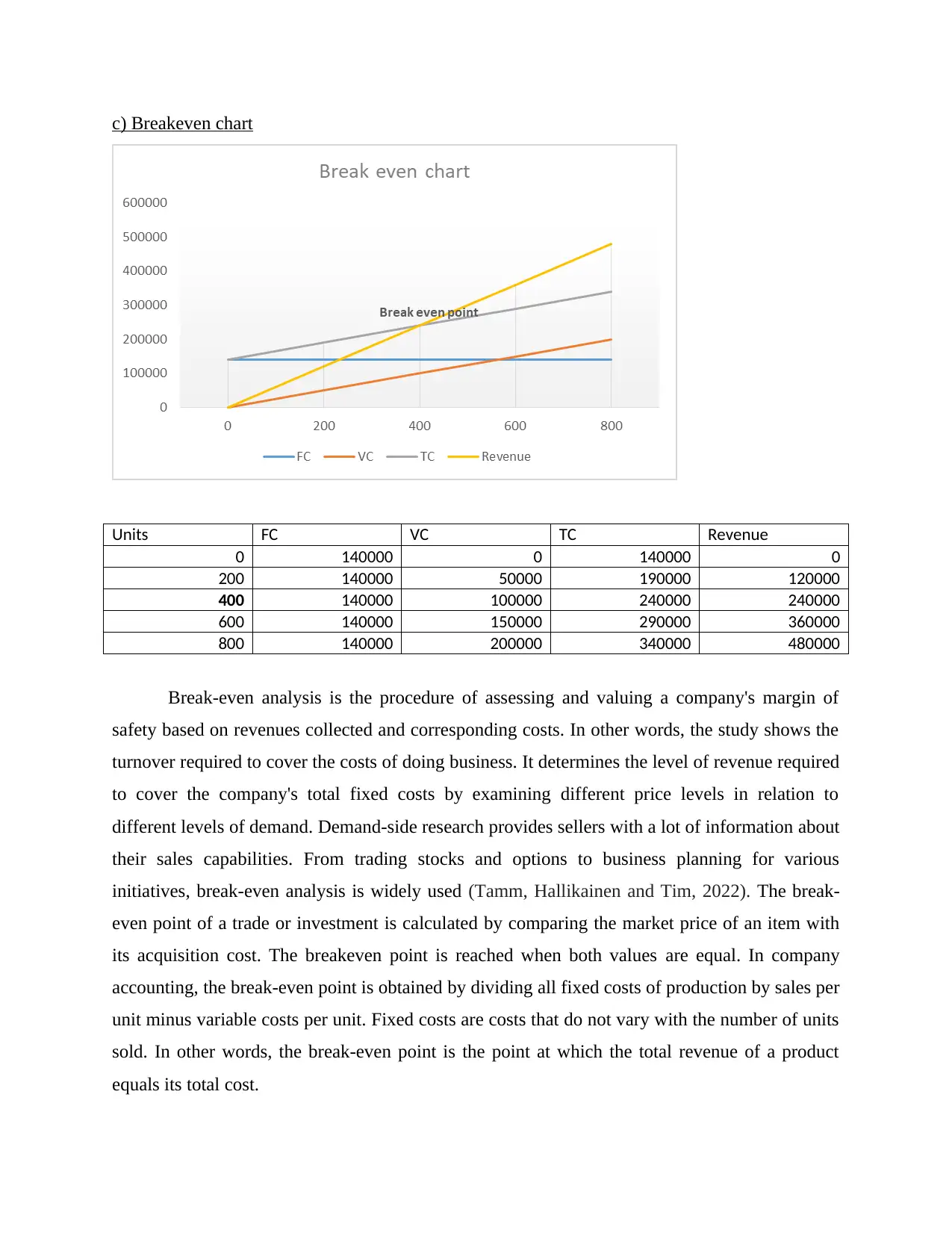

c) Breakeven chart

Units FC VC TC Revenue

0 140000 0 140000 0

200 140000 50000 190000 120000

400 140000 100000 240000 240000

600 140000 150000 290000 360000

800 140000 200000 340000 480000

Break-even analysis is the procedure of assessing and valuing a company's margin of

safety based on revenues collected and corresponding costs. In other words, the study shows the

turnover required to cover the costs of doing business. It determines the level of revenue required

to cover the company's total fixed costs by examining different price levels in relation to

different levels of demand. Demand-side research provides sellers with a lot of information about

their sales capabilities. From trading stocks and options to business planning for various

initiatives, break-even analysis is widely used (Tamm, Hallikainen and Tim, 2022). The break-

even point of a trade or investment is calculated by comparing the market price of an item with

its acquisition cost. The breakeven point is reached when both values are equal. In company

accounting, the break-even point is obtained by dividing all fixed costs of production by sales per

unit minus variable costs per unit. Fixed costs are costs that do not vary with the number of units

sold. In other words, the break-even point is the point at which the total revenue of a product

equals its total cost.

Units FC VC TC Revenue

0 140000 0 140000 0

200 140000 50000 190000 120000

400 140000 100000 240000 240000

600 140000 150000 290000 360000

800 140000 200000 340000 480000

Break-even analysis is the procedure of assessing and valuing a company's margin of

safety based on revenues collected and corresponding costs. In other words, the study shows the

turnover required to cover the costs of doing business. It determines the level of revenue required

to cover the company's total fixed costs by examining different price levels in relation to

different levels of demand. Demand-side research provides sellers with a lot of information about

their sales capabilities. From trading stocks and options to business planning for various

initiatives, break-even analysis is widely used (Tamm, Hallikainen and Tim, 2022). The break-

even point of a trade or investment is calculated by comparing the market price of an item with

its acquisition cost. The breakeven point is reached when both values are equal. In company

accounting, the break-even point is obtained by dividing all fixed costs of production by sales per

unit minus variable costs per unit. Fixed costs are costs that do not vary with the number of units

sold. In other words, the break-even point is the point at which the total revenue of a product

equals its total cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Break-even point (unit) = fixed cost ÷ (sales per unit – variable cost per unit).

d) Analysing the benefits and limitations of breakeven model

Benefits of break-even analysis

Pricing: The Break-Even analysis is identified as an extremely crucial for businesses and

has many benefits. This tells how many items are needed to sell to incur profit or

revenue. Determining if the product is worth selling or if it is too risky to sell. It shows

the amount of money which the organization makes at each stage of production.

Funding: In case of the funding, the adoption of break-even analysis is generally a crucial

aspect of the organizational strategy. If there is a need to raise capital for company or

start up, will definitely require a break-even analysis. Additionally, an insignificant

break-even point makes it more comfortable to take on additional debt and financing

(Torres, Sidorova and Jones, 2018).

Setting Sales Goals: A break-even analysis can also be identified as a significant method

accurate revenue bench mark for the team. Having exact amounts and time periods in

mind usually makes it easier to determine sales targets.

Reduce risk: Some business concepts are not meant to be followed. A break-even

analysis can assist reduce risk by keeping business away from that investments and

product lines that are less likely to succeed.

Rely on accurate data: Costs may be categorized as both fixed and variable costs. This

can complicate calculations and should almost certainly be put in one of the two.

Accurate breakeven points require correct data.

Competitors are ignored: As a newcomer, one influence the competition and vice versa.

They may change their prices, which may affect demand for their goods and force them

to adjust their prices. Prices are likely to rise. Finally, break-even analysis provides

reliable knowledge of the prerequisites for success. But that's not the only research one

should do before starting or changing a company.

Pay a fixed cost: Most people think of price as how much it costs to make a product.

These are known as variable costs. Fixed costs such as insurance and web development

still need to be paid. This can be achieved by doing a break-even analysis.

d) Analysing the benefits and limitations of breakeven model

Benefits of break-even analysis

Pricing: The Break-Even analysis is identified as an extremely crucial for businesses and

has many benefits. This tells how many items are needed to sell to incur profit or

revenue. Determining if the product is worth selling or if it is too risky to sell. It shows

the amount of money which the organization makes at each stage of production.

Funding: In case of the funding, the adoption of break-even analysis is generally a crucial

aspect of the organizational strategy. If there is a need to raise capital for company or

start up, will definitely require a break-even analysis. Additionally, an insignificant

break-even point makes it more comfortable to take on additional debt and financing

(Torres, Sidorova and Jones, 2018).

Setting Sales Goals: A break-even analysis can also be identified as a significant method

accurate revenue bench mark for the team. Having exact amounts and time periods in

mind usually makes it easier to determine sales targets.

Reduce risk: Some business concepts are not meant to be followed. A break-even

analysis can assist reduce risk by keeping business away from that investments and

product lines that are less likely to succeed.

Rely on accurate data: Costs may be categorized as both fixed and variable costs. This

can complicate calculations and should almost certainly be put in one of the two.

Accurate breakeven points require correct data.

Competitors are ignored: As a newcomer, one influence the competition and vice versa.

They may change their prices, which may affect demand for their goods and force them

to adjust their prices. Prices are likely to rise. Finally, break-even analysis provides

reliable knowledge of the prerequisites for success. But that's not the only research one

should do before starting or changing a company.

Pay a fixed cost: Most people think of price as how much it costs to make a product.

These are known as variable costs. Fixed costs such as insurance and web development

still need to be paid. This can be achieved by doing a break-even analysis.

Make better decisions: Entrepreneurs often make decisions based on emotion. If they are

excited about a new venture, they will pursue it. Knowing feelings is necessary, but not

enough. Successful entrepreneurs make decisions based on facts. Making decisions is

much easier when one put in the effort and have meaningful data.

Limitations of Breakeven Analysis

Break-even analysis is based on the assumption that all costs and expenses can be clearly

divided into fixed and variable components. However, in practice, it can be difficult to

clearly distinguish between fixed and variable costs.

Assuming a constant selling price leads to a straight line of sales, which may or may not

be exact. The selling price of a product is determined by various factors such as market

supply and demand, competition, etc., and is rarely held constant.

It assumes that the quantity produced and sold are the same, and that the starting and

ending stocks of the finished goods remain the same. But in reality it is not.

The amount of capital used by the company is not considered in the break-even analysis.

In fact, the amount of capital used is a key factor in a company's profitability.

It has proven unsuitable in industries such as shipbuilding. If fixed costs are not taken

into account when evaluating work in progress, losses can occur each year until the

contract is terminated. This can lead to income tax issues.

Firms may choose to over order at a lower price and ignore factory capacity based on the

concept of marginal cost. This may require additional labour and capacity expansion,

both of which can increase production costs and cause changes in fixed costs. Companies

often lose money.

Fixed costs are assumed to be constant at all activity levels. Note that fixed costs tend to

vary with level of activity.

Assume that variable costs are proportional to production volume. In practice, it moves

relative to production, though not always in exact proportions (Wickramasinghe and

Schaffer, 2018).

Sales revenue and variable costs do not grow in line with output. They are less

proportional than they should be at higher output levels. This is due to transaction

discounts, bulk buying savings, concessions on bulk sales, etc.

excited about a new venture, they will pursue it. Knowing feelings is necessary, but not

enough. Successful entrepreneurs make decisions based on facts. Making decisions is

much easier when one put in the effort and have meaningful data.

Limitations of Breakeven Analysis

Break-even analysis is based on the assumption that all costs and expenses can be clearly

divided into fixed and variable components. However, in practice, it can be difficult to

clearly distinguish between fixed and variable costs.

Assuming a constant selling price leads to a straight line of sales, which may or may not

be exact. The selling price of a product is determined by various factors such as market

supply and demand, competition, etc., and is rarely held constant.

It assumes that the quantity produced and sold are the same, and that the starting and

ending stocks of the finished goods remain the same. But in reality it is not.

The amount of capital used by the company is not considered in the break-even analysis.

In fact, the amount of capital used is a key factor in a company's profitability.

It has proven unsuitable in industries such as shipbuilding. If fixed costs are not taken

into account when evaluating work in progress, losses can occur each year until the

contract is terminated. This can lead to income tax issues.

Firms may choose to over order at a lower price and ignore factory capacity based on the

concept of marginal cost. This may require additional labour and capacity expansion,

both of which can increase production costs and cause changes in fixed costs. Companies

often lose money.

Fixed costs are assumed to be constant at all activity levels. Note that fixed costs tend to

vary with level of activity.

Assume that variable costs are proportional to production volume. In practice, it moves

relative to production, though not always in exact proportions (Wickramasinghe and

Schaffer, 2018).

Sales revenue and variable costs do not grow in line with output. They are less

proportional than they should be at higher output levels. This is due to transaction

discounts, bulk buying savings, concessions on bulk sales, etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.