Small Business Financial Statements Analysis

VerifiedAdded on 2020/06/03

|14

|2025

|203

AI Summary

This assignment presents the financial information of a small business, outlining its income statement, expenses, net profit, and balance sheet details. Students are tasked with analyzing these statements to understand the financial health and performance of the business.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BUSINESS CASE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INVESTOR’S REPORT..............................................................................................................................................................................1

Vision.......................................................................................................................................................................................................1

Mission.....................................................................................................................................................................................................1

Industry Trend and analysis.....................................................................................................................................................................1

Keys to success........................................................................................................................................................................................2

Financial Objectives.................................................................................................................................................................................2

Capital structure.......................................................................................................................................................................................2

Marginal costing statement......................................................................................................................................................................3

Cash flow statement.................................................................................................................................................................................3

Income Statement.....................................................................................................................................................................................4

Balance sheet............................................................................................................................................................................................4

REFERENCES............................................................................................................................................................................................6

APPENDIX..................................................................................................................................................................................................6

Marginal costing statement......................................................................................................................................................................6

Statement of cash flow.............................................................................................................................................................................7

Profitability statement..............................................................................................................................................................................8

INVESTOR’S REPORT..............................................................................................................................................................................1

Vision.......................................................................................................................................................................................................1

Mission.....................................................................................................................................................................................................1

Industry Trend and analysis.....................................................................................................................................................................1

Keys to success........................................................................................................................................................................................2

Financial Objectives.................................................................................................................................................................................2

Capital structure.......................................................................................................................................................................................2

Marginal costing statement......................................................................................................................................................................3

Cash flow statement.................................................................................................................................................................................3

Income Statement.....................................................................................................................................................................................4

Balance sheet............................................................................................................................................................................................4

REFERENCES............................................................................................................................................................................................6

APPENDIX..................................................................................................................................................................................................6

Marginal costing statement......................................................................................................................................................................6

Statement of cash flow.............................................................................................................................................................................7

Profitability statement..............................................................................................................................................................................8

Balance sheet..........................................................................................................................................................................................10

INVESTOR’S REPORT

To: Prospective Investors

From: Entrepreneur of New Footwear Business

10th August 2017

We are pleased to share our new footwear business plan, has planned to offer iconic, trendy, designer and innovative

footwear in vibrant colour and in all the sizes to kids, female and male of all the age group. Classic collection in different varieties,

brilliant designing ideas, greatest technologies, underfoot cushioning embedded with 3D printing & rapid prototyping will strongly

appeal to the audience.

Vision

Our long-term vision is to become the market leader in the British Footwear Industry by the end of 2030.

Mission

Our Mission is to be the heart of target audiences to build strong brand reputation through having a portfolio of highly loyal

consumers.

Industry Trend and analysis

British Footwear Industry reported annual revenue of £5 billion at an annual growth of 2.9% during 2012-2017 and

employed 51,013 people in the sector by 1,684 businesses. Looking to the impressive industrial progress and high growth of the top

key players such as C&J Clark Limited, Schuh Limited and Office Holding Limited happened because of boosting consumer

confidence, expansion through online operations, changing lifestyle and economic recovery as well (Footwear Retailers in the UK,

2015). Although footwear retailers are suffering issues from knock-down prices, emerging multinational retailers & stifled growth

in revenues, still, considering changing lifestyle, rising household income & growth opportunities, it has been decided to open a new

1

To: Prospective Investors

From: Entrepreneur of New Footwear Business

10th August 2017

We are pleased to share our new footwear business plan, has planned to offer iconic, trendy, designer and innovative

footwear in vibrant colour and in all the sizes to kids, female and male of all the age group. Classic collection in different varieties,

brilliant designing ideas, greatest technologies, underfoot cushioning embedded with 3D printing & rapid prototyping will strongly

appeal to the audience.

Vision

Our long-term vision is to become the market leader in the British Footwear Industry by the end of 2030.

Mission

Our Mission is to be the heart of target audiences to build strong brand reputation through having a portfolio of highly loyal

consumers.

Industry Trend and analysis

British Footwear Industry reported annual revenue of £5 billion at an annual growth of 2.9% during 2012-2017 and

employed 51,013 people in the sector by 1,684 businesses. Looking to the impressive industrial progress and high growth of the top

key players such as C&J Clark Limited, Schuh Limited and Office Holding Limited happened because of boosting consumer

confidence, expansion through online operations, changing lifestyle and economic recovery as well (Footwear Retailers in the UK,

2015). Although footwear retailers are suffering issues from knock-down prices, emerging multinational retailers & stifled growth

in revenues, still, considering changing lifestyle, rising household income & growth opportunities, it has been decided to open a new

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

footwear business in the UK market.

Keys to success

Market proximity

Supply of innovative, qualitative & designer footwear

Efficient supply chain

Instant online delivery

Use of high quality material to make highly comfortable shoes

Innovations to provide footwear in unique designs

For the financial projection, we have produced key financial statements and feel pleasure to share our plan with you so as to

build confidence in the newly designed business plan. It is necessary to construct projected statements such as profitability

statement and cash flow statement so that, investors, debtors and others can be informed with the expected financial results and

assists them in successful and right decisions (Revell, 2016). The report just brings your attention to several key highlights:

Financial Objectives

To grab target market segments by offering quality footwear to maximize revenues

To generate an attractive return of 10% or more on the total invested capital per year

To provide variety of designs in vibrant colours to gain a net yield of 8% or more p.a.

To invest in advertisement & promotional campaign for maximizing brand value

To meet our commitments towards fund providers through excellent financial management

Capital structure

The proposed footwear business plan required a total investment of 130,000GBP which will be fully financed through owner’s

equity without any long-term debt because it is too risky for a new start-up.

2

Keys to success

Market proximity

Supply of innovative, qualitative & designer footwear

Efficient supply chain

Instant online delivery

Use of high quality material to make highly comfortable shoes

Innovations to provide footwear in unique designs

For the financial projection, we have produced key financial statements and feel pleasure to share our plan with you so as to

build confidence in the newly designed business plan. It is necessary to construct projected statements such as profitability

statement and cash flow statement so that, investors, debtors and others can be informed with the expected financial results and

assists them in successful and right decisions (Revell, 2016). The report just brings your attention to several key highlights:

Financial Objectives

To grab target market segments by offering quality footwear to maximize revenues

To generate an attractive return of 10% or more on the total invested capital per year

To provide variety of designs in vibrant colours to gain a net yield of 8% or more p.a.

To invest in advertisement & promotional campaign for maximizing brand value

To meet our commitments towards fund providers through excellent financial management

Capital structure

The proposed footwear business plan required a total investment of 130,000GBP which will be fully financed through owner’s

equity without any long-term debt because it is too risky for a new start-up.

2

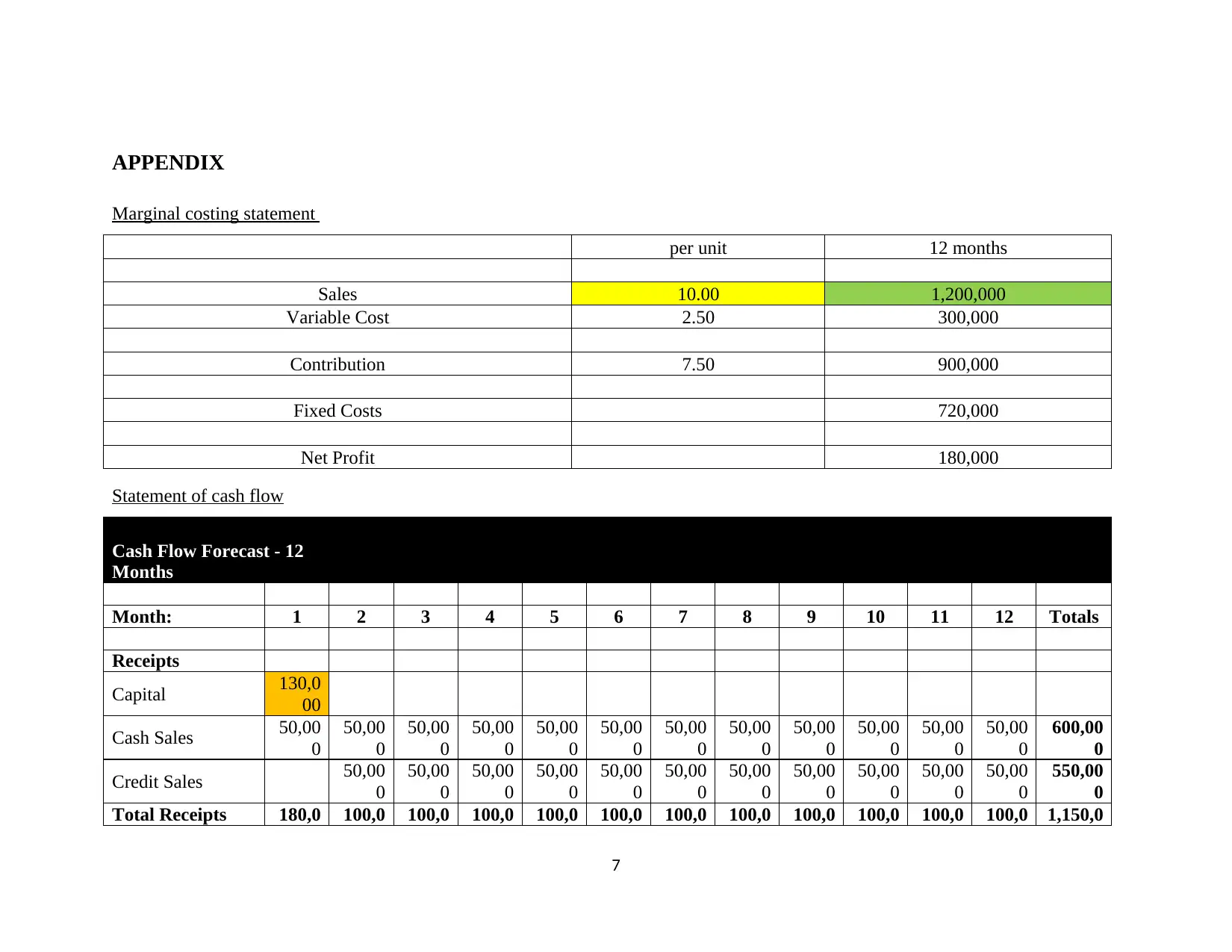

Marginal costing statement

The cost of producing one additional unit is called marginal cost hence, it considers only the variable cost and do not pay

attention to the fixed cost of production because it does not changes with the change in output (Sabri and et.al., 2015).

Total demand for the footwear in the UK market has been expected to 120,000 at total sales revenues of £1,200,000.

From the constructed MC statement, it is really pleasurable to share that we have projected @ 2.5% per unit variable cost

at a selling price of £10/unit resulted in per unit contribution of £7.50 totalled to £300,000.

Expected total fixed cost has been estimated to 720,000 which give us an attractive return of £180,000 to the planned

footwear business.

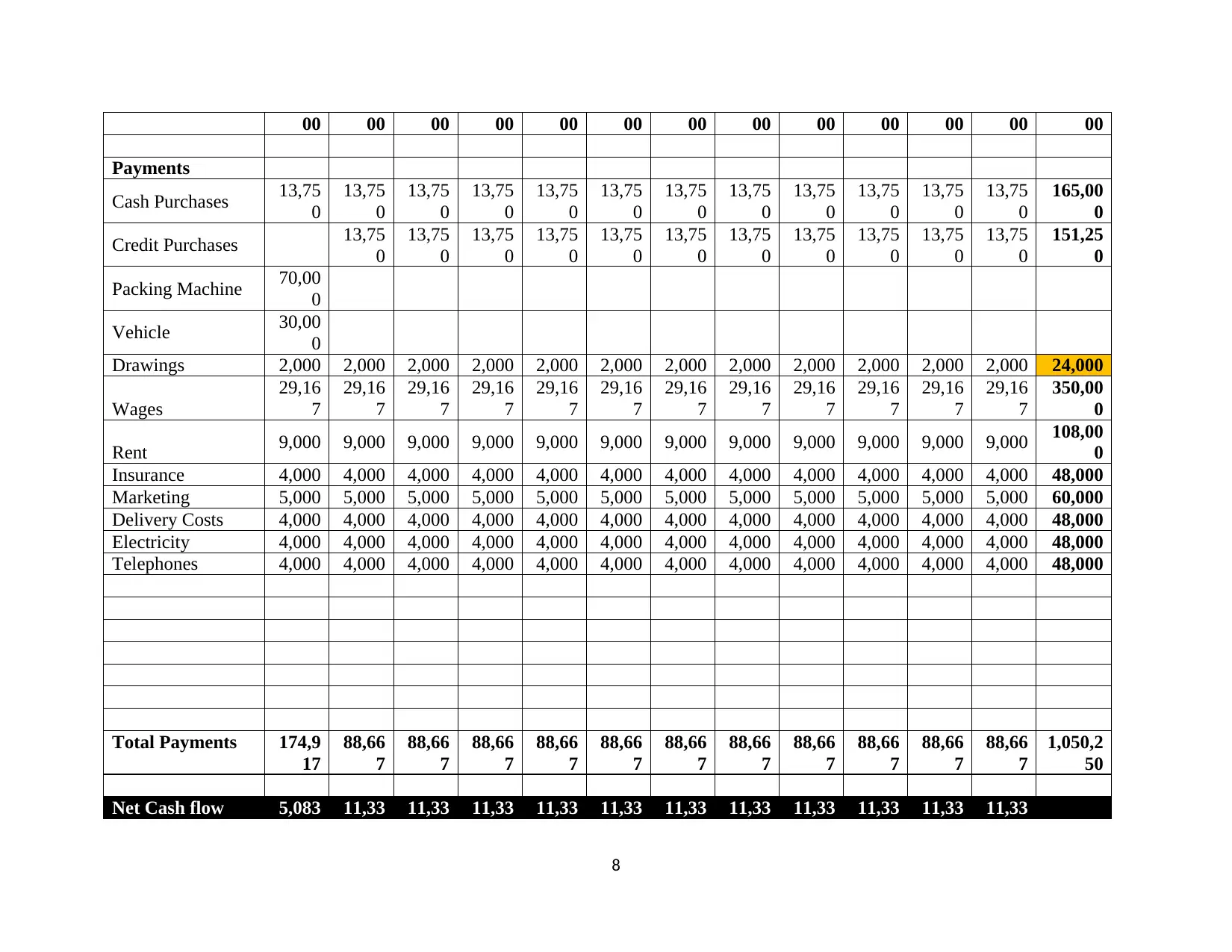

Cash flow statement

Cash Flow Statement is a summarized statement that accumulates all the cash inflow and outflow regarding operational,

financing and investing activities and provides usable statistics to examine surplus or shortfall of cash available in the business

(Revell, 2016).

It is decided to sell 50% goods on credit for 1 month and 50% on cash or prompt basis so as to generate immediate cash flow

from the consumers at the point of sale. On the other side, expenditures show a constant trend as it remains constant over the

projected period to £88,667.

Total revenue for the year is projected to be £1,150,000, out of these, £600,000 will be generated from the cash sales and rest

£550,000 from the credit sale. In order to manage cash funds, business decided to purchase 50% material on cash and 50%

from the supplier for one month credit duration (Kim and et.al., 2016).

Net Cash Flow (NCF) depicts a fixed trend by having surplus of £11,333 and due to the availability of beginning cash,

closing cash balance consistently shows an upward trend and in the end of 12th month, it is expected to grow up from £5,083

to £129,750 so as to have enough cash to meet financial commitments towards investors, suppliers and others.

3

The cost of producing one additional unit is called marginal cost hence, it considers only the variable cost and do not pay

attention to the fixed cost of production because it does not changes with the change in output (Sabri and et.al., 2015).

Total demand for the footwear in the UK market has been expected to 120,000 at total sales revenues of £1,200,000.

From the constructed MC statement, it is really pleasurable to share that we have projected @ 2.5% per unit variable cost

at a selling price of £10/unit resulted in per unit contribution of £7.50 totalled to £300,000.

Expected total fixed cost has been estimated to 720,000 which give us an attractive return of £180,000 to the planned

footwear business.

Cash flow statement

Cash Flow Statement is a summarized statement that accumulates all the cash inflow and outflow regarding operational,

financing and investing activities and provides usable statistics to examine surplus or shortfall of cash available in the business

(Revell, 2016).

It is decided to sell 50% goods on credit for 1 month and 50% on cash or prompt basis so as to generate immediate cash flow

from the consumers at the point of sale. On the other side, expenditures show a constant trend as it remains constant over the

projected period to £88,667.

Total revenue for the year is projected to be £1,150,000, out of these, £600,000 will be generated from the cash sales and rest

£550,000 from the credit sale. In order to manage cash funds, business decided to purchase 50% material on cash and 50%

from the supplier for one month credit duration (Kim and et.al., 2016).

Net Cash Flow (NCF) depicts a fixed trend by having surplus of £11,333 and due to the availability of beginning cash,

closing cash balance consistently shows an upward trend and in the end of 12th month, it is expected to grow up from £5,083

to £129,750 so as to have enough cash to meet financial commitments towards investors, suppliers and others.

3

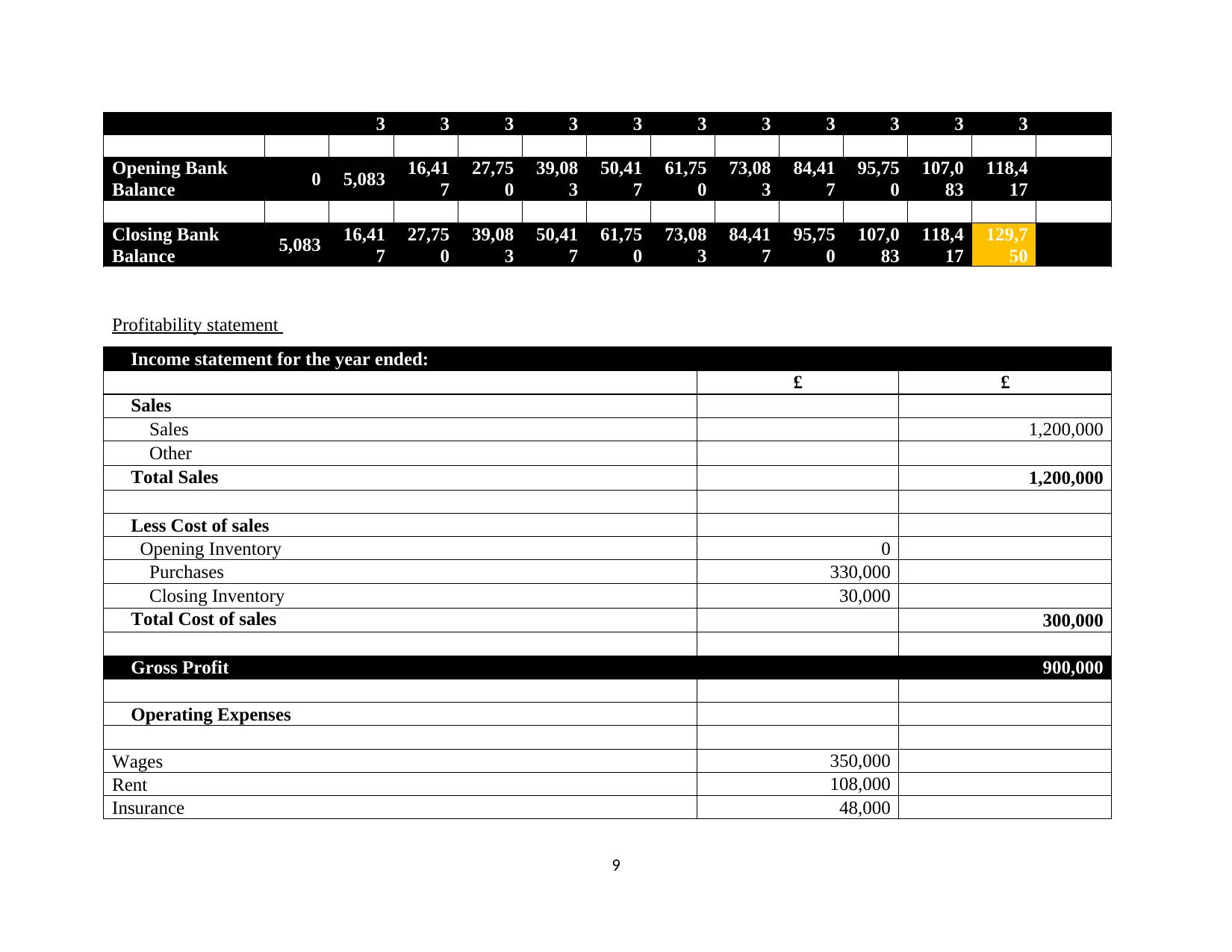

Income Statement

It provides useful information about total income and expenditure that is expected to be incurring in the first year of

operations and helps to determine net profit.

Annual demand for the designer, stylish and innovative footwear has been expected to 12,000 that will be offered at a selling

price of £10/unit with a total yearly turnover of £1,200,000.

As per the variable cost of 25%, the total cost of sales is reported to 300,000 that is 25% of projected sales at a gross profit of

£900,000.

Firm will incur an expected operational expenditure of £720,000 on wages, rent, insurance, marketing, delivery charges,

electricity, telephone and depreciation for the assets use. Operating cost percentage on sales is founded to be 60% which will

deliver a good return of £180,000 means 15% net profit margin on sales.

The assumptions can be justified considering UK footwear industry, rising household income, high spending on lifestyle and

industrial growth. Evidencing it, consumer spending reported a YOY growth of 7.6% and 8.4% including & excluding

inflation. In 2015, nation reported progressive growth of 17% through online sale whilst total footwear sales reached to

10.3GBP billion.

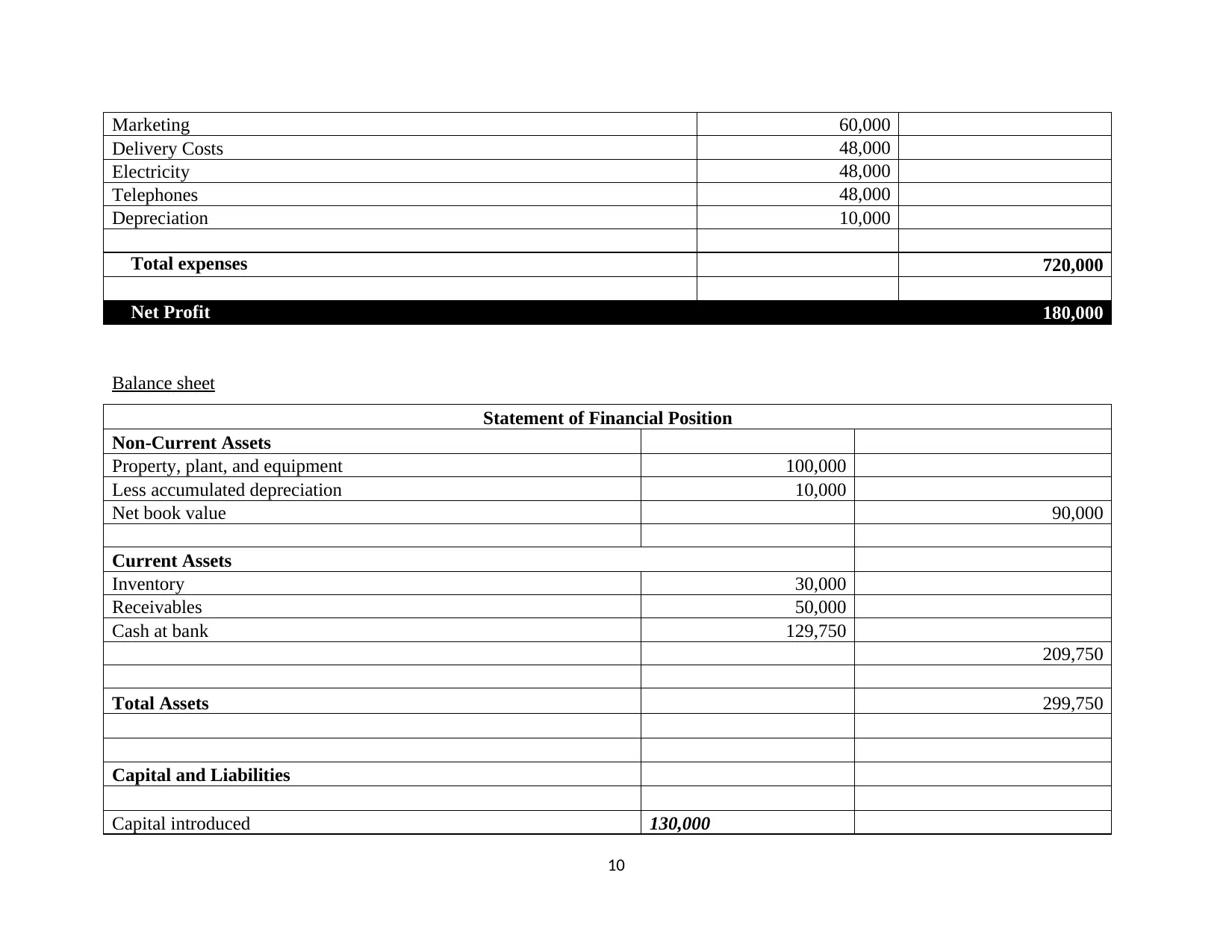

Balance sheet

It detailed out the balance of assets and liabilities which shows financial status of an entity.

We have decided to collect £130,000 by owner’s investment to finance investment worth £100,000 in property, plant and

equipment. SOCF clearly indicates that £70,000 will be invested in packing machine and rest £30,000 to purchase a vehicle.

It has been depreciated following straight line method (SLM) for the projected life over 10 years. Remaining £30,000 is

decided to invest in merchandising inventory items for the sale (Shibata and Nishihara, 2015).

As decided to offer 50% goods on cash and 50% on credit, at the end of the year, firm will have a trade receivable of

4

It provides useful information about total income and expenditure that is expected to be incurring in the first year of

operations and helps to determine net profit.

Annual demand for the designer, stylish and innovative footwear has been expected to 12,000 that will be offered at a selling

price of £10/unit with a total yearly turnover of £1,200,000.

As per the variable cost of 25%, the total cost of sales is reported to 300,000 that is 25% of projected sales at a gross profit of

£900,000.

Firm will incur an expected operational expenditure of £720,000 on wages, rent, insurance, marketing, delivery charges,

electricity, telephone and depreciation for the assets use. Operating cost percentage on sales is founded to be 60% which will

deliver a good return of £180,000 means 15% net profit margin on sales.

The assumptions can be justified considering UK footwear industry, rising household income, high spending on lifestyle and

industrial growth. Evidencing it, consumer spending reported a YOY growth of 7.6% and 8.4% including & excluding

inflation. In 2015, nation reported progressive growth of 17% through online sale whilst total footwear sales reached to

10.3GBP billion.

Balance sheet

It detailed out the balance of assets and liabilities which shows financial status of an entity.

We have decided to collect £130,000 by owner’s investment to finance investment worth £100,000 in property, plant and

equipment. SOCF clearly indicates that £70,000 will be invested in packing machine and rest £30,000 to purchase a vehicle.

It has been depreciated following straight line method (SLM) for the projected life over 10 years. Remaining £30,000 is

decided to invest in merchandising inventory items for the sale (Shibata and Nishihara, 2015).

As decided to offer 50% goods on cash and 50% on credit, at the end of the year, firm will have a trade receivable of

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

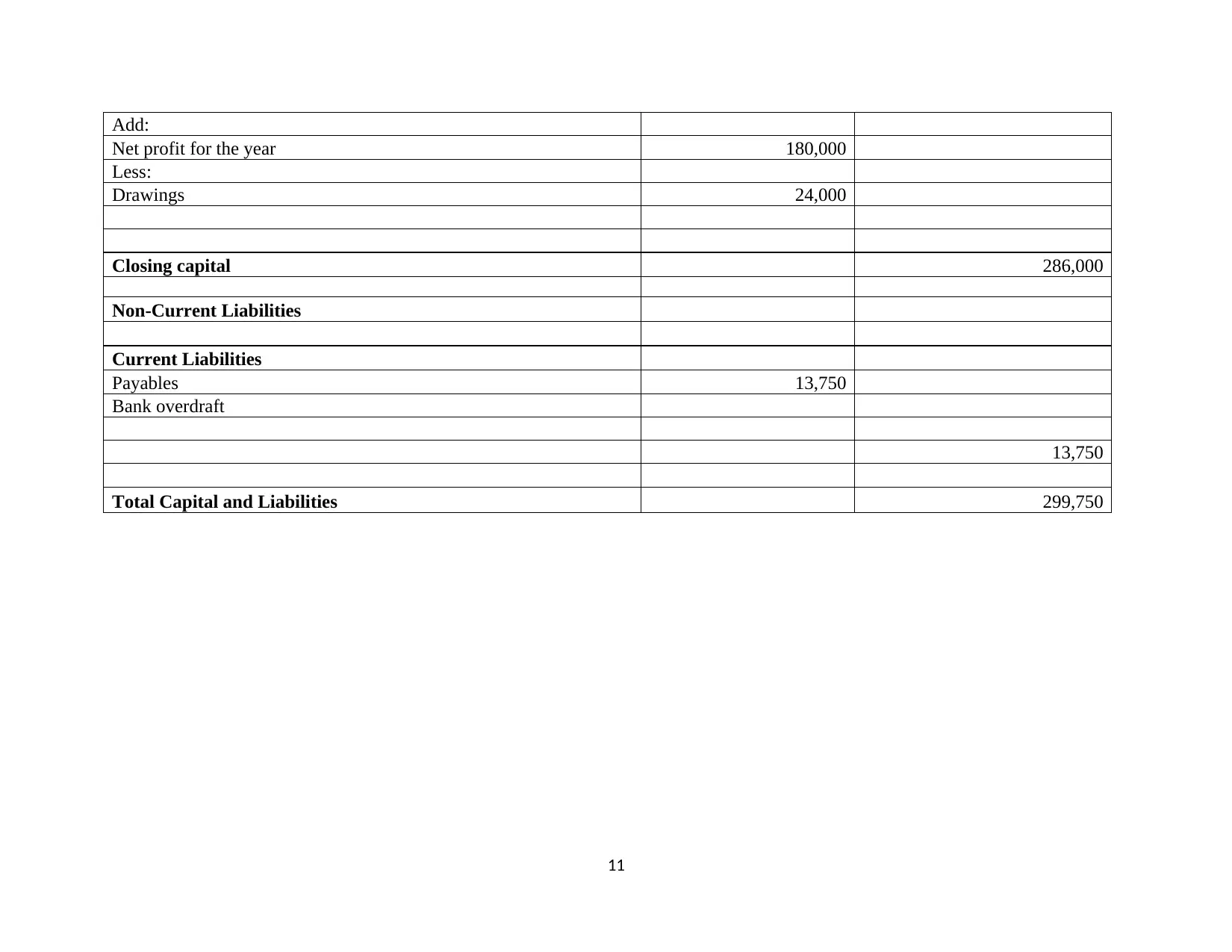

£50,000. Similarly, as suppliers have offered 1-month credit to us, therefore, we have a current liability in the form of trade

payable worth £13,750.

The closing cash balance of SOCF will be the most liquid assets available worth £129,750 shows good liquidity (Finkler and

et.al., 2016).

The projected net return of £180,000 is added to owner’s capital whilst drawing worth £24,000 reported in the SOCF has

been subtracted which bring closing capital to £286,000.

For further financial information, please look at the copy of Marginal costing statement, profitability statement, Statement of Cash

Flow and balance sheet attached in Appendix.

5

payable worth £13,750.

The closing cash balance of SOCF will be the most liquid assets available worth £129,750 shows good liquidity (Finkler and

et.al., 2016).

The projected net return of £180,000 is added to owner’s capital whilst drawing worth £24,000 reported in the SOCF has

been subtracted which bring closing capital to £286,000.

For further financial information, please look at the copy of Marginal costing statement, profitability statement, Statement of Cash

Flow and balance sheet attached in Appendix.

5

REFERENCES

Books and Journals

Shibata, T. and Nishihara, M., 2015. Investment timing, debt structure, and financing constraints. European Journal of Operational

Research. 241(2). pp. 513-526.

Revell, J., 2016. The recent evolution of financial systems. Springer.

Sabri, M. F. and et.al., 2015. Financial literacy, financial Management practices, and retirement confidence among Women working in

government Agencies: A mediation model. The Journal of Developing Areas. 49(6). pp. 405-412.

Kim, J.B. and et.al., 2016. Financial statement comparability and expected crash risk. Journal of Accounting and Economics. 61(2).

pp. 294-312.

Finkler, S. A. and et.al., 2016. Financial management for public, health, and not-for-profit organizations. CQ Press.

Online

Footwear Retailers in the UK. 2015. [Online]. Available through: https://www.ibisworld.co.uk/market-research/footwear-

retailers.html. [Accessed on 11th August 2017].

6

Books and Journals

Shibata, T. and Nishihara, M., 2015. Investment timing, debt structure, and financing constraints. European Journal of Operational

Research. 241(2). pp. 513-526.

Revell, J., 2016. The recent evolution of financial systems. Springer.

Sabri, M. F. and et.al., 2015. Financial literacy, financial Management practices, and retirement confidence among Women working in

government Agencies: A mediation model. The Journal of Developing Areas. 49(6). pp. 405-412.

Kim, J.B. and et.al., 2016. Financial statement comparability and expected crash risk. Journal of Accounting and Economics. 61(2).

pp. 294-312.

Finkler, S. A. and et.al., 2016. Financial management for public, health, and not-for-profit organizations. CQ Press.

Online

Footwear Retailers in the UK. 2015. [Online]. Available through: https://www.ibisworld.co.uk/market-research/footwear-

retailers.html. [Accessed on 11th August 2017].

6

APPENDIX

Marginal costing statement

per unit 12 months

Sales 10.00 1,200,000

Variable Cost 2.50 300,000

Contribution 7.50 900,000

Fixed Costs 720,000

Net Profit 180,000

Statement of cash flow

Cash Flow Forecast - 12

Months

Month: 1 2 3 4 5 6 7 8 9 10 11 12 Totals

Receipts

Capital 130,0

00

Cash Sales 50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

600,00

0

Credit Sales 50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

550,00

0

Total Receipts 180,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 1,150,0

7

Marginal costing statement

per unit 12 months

Sales 10.00 1,200,000

Variable Cost 2.50 300,000

Contribution 7.50 900,000

Fixed Costs 720,000

Net Profit 180,000

Statement of cash flow

Cash Flow Forecast - 12

Months

Month: 1 2 3 4 5 6 7 8 9 10 11 12 Totals

Receipts

Capital 130,0

00

Cash Sales 50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

600,00

0

Credit Sales 50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

50,00

0

550,00

0

Total Receipts 180,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 1,150,0

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

00 00 00 00 00 00 00 00 00 00 00 00 00

Payments

Cash Purchases 13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

165,00

0

Credit Purchases 13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

151,25

0

Packing Machine 70,00

0

Vehicle 30,00

0

Drawings 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000

Wages

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

350,00

0

Rent 9,000 9,000 9,000 9,000 9,000 9,000 9,000 9,000 9,000 9,000 9,000 9,000 108,00

0

Insurance 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000

Marketing 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000

Delivery Costs 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000

Electricity 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000

Telephones 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000

Total Payments 174,9

17

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

1,050,2

50

Net Cash flow 5,083 11,33 11,33 11,33 11,33 11,33 11,33 11,33 11,33 11,33 11,33 11,33

8

Payments

Cash Purchases 13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

165,00

0

Credit Purchases 13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

13,75

0

151,25

0

Packing Machine 70,00

0

Vehicle 30,00

0

Drawings 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000

Wages

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

29,16

7

350,00

0

Rent 9,000 9,000 9,000 9,000 9,000 9,000 9,000 9,000 9,000 9,000 9,000 9,000 108,00

0

Insurance 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000

Marketing 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000

Delivery Costs 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000

Electricity 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000

Telephones 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000

Total Payments 174,9

17

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

88,66

7

1,050,2

50

Net Cash flow 5,083 11,33 11,33 11,33 11,33 11,33 11,33 11,33 11,33 11,33 11,33 11,33

8

3 3 3 3 3 3 3 3 3 3 3

Opening Bank

Balance 0 5,083 16,41

7

27,75

0

39,08

3

50,41

7

61,75

0

73,08

3

84,41

7

95,75

0

107,0

83

118,4

17

Closing Bank

Balance 5,083 16,41

7

27,75

0

39,08

3

50,41

7

61,75

0

73,08

3

84,41

7

95,75

0

107,0

83

118,4

17

129,7

50

Profitability statement

Income statement for the year ended:

£ £

Sales

Sales 1,200,000

Other

Total Sales 1,200,000

Less Cost of sales

Opening Inventory 0

Purchases 330,000

Closing Inventory 30,000

Total Cost of sales 300,000

Gross Profit 900,000

Operating Expenses

Wages 350,000

Rent 108,000

Insurance 48,000

9

Opening Bank

Balance 0 5,083 16,41

7

27,75

0

39,08

3

50,41

7

61,75

0

73,08

3

84,41

7

95,75

0

107,0

83

118,4

17

Closing Bank

Balance 5,083 16,41

7

27,75

0

39,08

3

50,41

7

61,75

0

73,08

3

84,41

7

95,75

0

107,0

83

118,4

17

129,7

50

Profitability statement

Income statement for the year ended:

£ £

Sales

Sales 1,200,000

Other

Total Sales 1,200,000

Less Cost of sales

Opening Inventory 0

Purchases 330,000

Closing Inventory 30,000

Total Cost of sales 300,000

Gross Profit 900,000

Operating Expenses

Wages 350,000

Rent 108,000

Insurance 48,000

9

Marketing 60,000

Delivery Costs 48,000

Electricity 48,000

Telephones 48,000

Depreciation 10,000

Total expenses 720,000

Net Profit 180,000

Balance sheet

Statement of Financial Position

Non-Current Assets

Property, plant, and equipment 100,000

Less accumulated depreciation 10,000

Net book value 90,000

Current Assets

Inventory 30,000

Receivables 50,000

Cash at bank 129,750

209,750

Total Assets 299,750

Capital and Liabilities

Capital introduced 130,000

10

Delivery Costs 48,000

Electricity 48,000

Telephones 48,000

Depreciation 10,000

Total expenses 720,000

Net Profit 180,000

Balance sheet

Statement of Financial Position

Non-Current Assets

Property, plant, and equipment 100,000

Less accumulated depreciation 10,000

Net book value 90,000

Current Assets

Inventory 30,000

Receivables 50,000

Cash at bank 129,750

209,750

Total Assets 299,750

Capital and Liabilities

Capital introduced 130,000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Add:

Net profit for the year 180,000

Less:

Drawings 24,000

Closing capital 286,000

Non-Current Liabilities

Current Liabilities

Payables 13,750

Bank overdraft

13,750

Total Capital and Liabilities 299,750

11

Net profit for the year 180,000

Less:

Drawings 24,000

Closing capital 286,000

Non-Current Liabilities

Current Liabilities

Payables 13,750

Bank overdraft

13,750

Total Capital and Liabilities 299,750

11

1 out of 14

Related Documents

![[SOLVED] Projected Statements and Financial Ratios](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fwu%2Fe9fde74d86d549c2a5887755687e52c6.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.