BA4008QA Business Decision Making: Machinery Purchase Decision Report

VerifiedAdded on 2022/11/28

|9

|1554

|185

Report

AI Summary

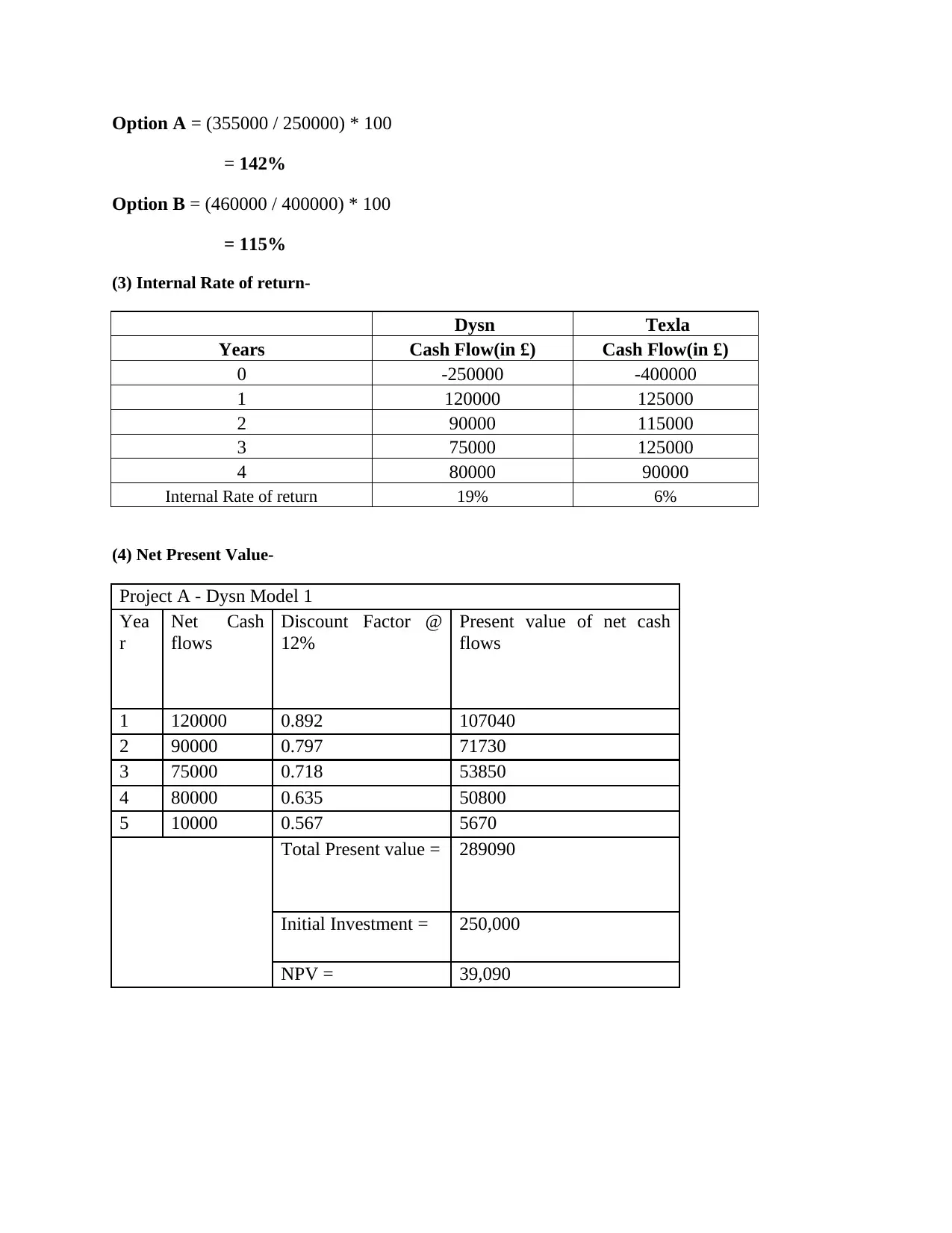

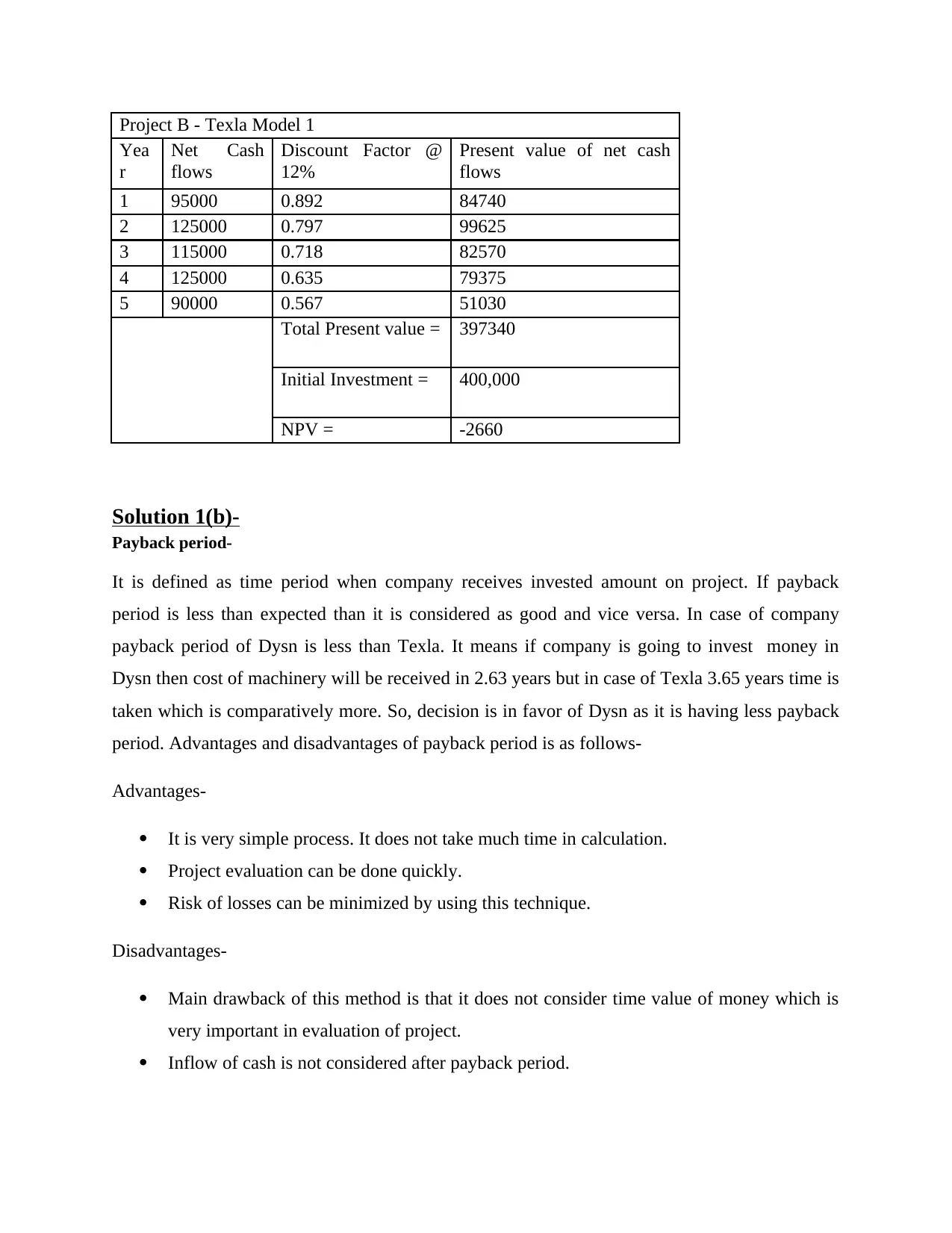

This report provides a comprehensive analysis of two machinery investment options, Dysn and Texla models, for Dolapo Plc. The analysis utilizes capital budgeting methods, including payback period, accounting rate of return (ARR), internal rate of return (IRR), and net present value (NPV), to assess the profitability and financial viability of each model. The report calculates and compares these metrics for both models, offering insights into the time required to recover the initial investment, the percentage return on investment, and the present value of future cash flows. Based on the findings, the report recommends the best choice for the company, supporting informed business decision-making regarding machinery purchase. The report also includes advantages and disadvantages of each method.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.