Comprehensive Report on Business Finance: Costing and Budgeting

VerifiedAdded on 2023/06/12

|13

|2656

|252

Report

AI Summary

This business finance report provides a detailed analysis of breakeven points, standard costing systems, and variance analysis. It explores the importance of contribution in decision-making and prepares profitability statements using both absorption and marginal costing methods. The report also demonstrates the significance of standard costing and variance analysis in controlling costs and enhancing efficiency. Furthermore, it includes the preparation of various types of budgets, such as direct material, direct labor, variable overhead, and fixed overhead expenditure budgets, highlighting their role in guiding expenses and ensuring financial performance aligns with organizational goals. This comprehensive analysis offers valuable insights into effective financial management and resource allocation.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

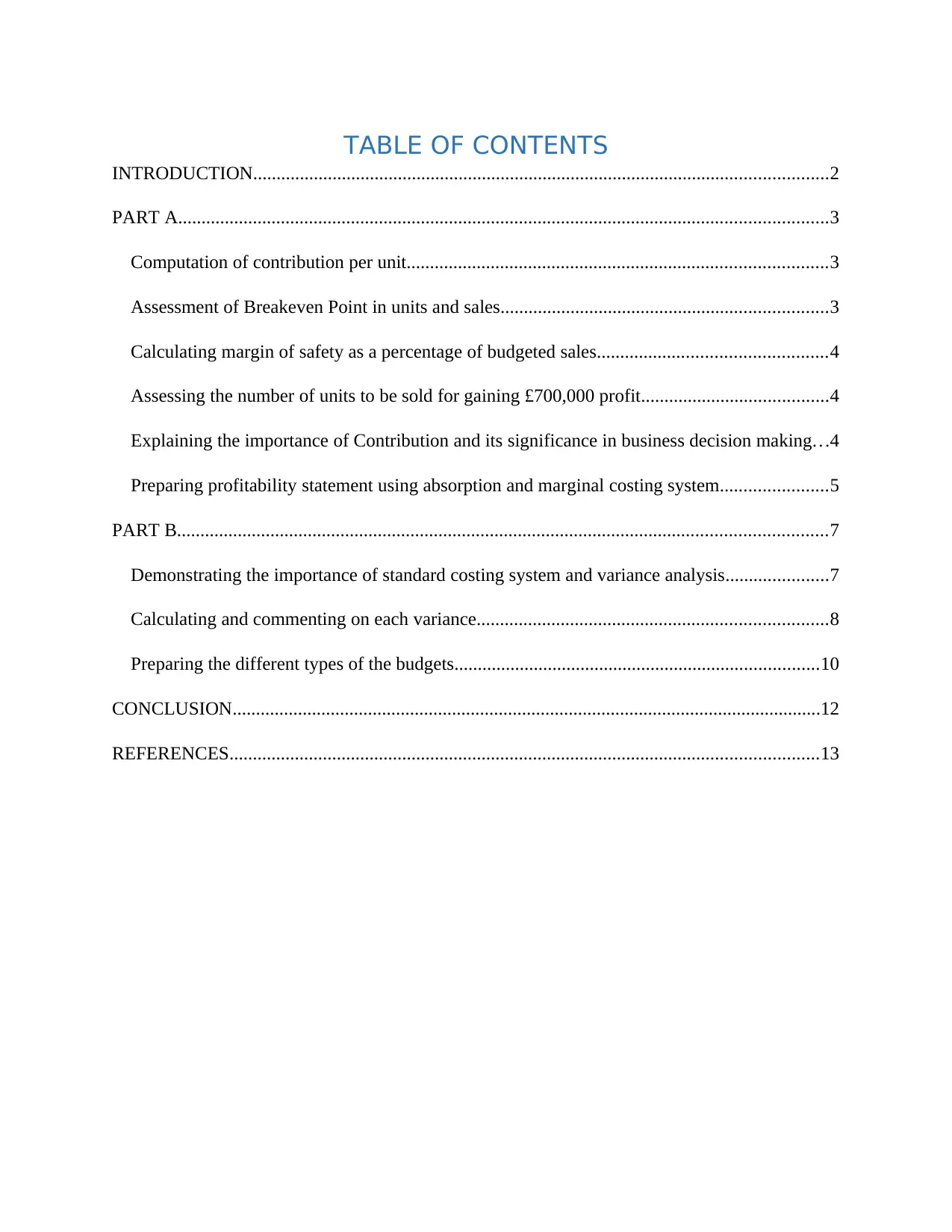

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................2

PART A...........................................................................................................................................3

Computation of contribution per unit..........................................................................................3

Assessment of Breakeven Point in units and sales......................................................................3

Calculating margin of safety as a percentage of budgeted sales.................................................4

Assessing the number of units to be sold for gaining £700,000 profit........................................4

Explaining the importance of Contribution and its significance in business decision making...4

Preparing profitability statement using absorption and marginal costing system.......................5

PART B...........................................................................................................................................7

Demonstrating the importance of standard costing system and variance analysis......................7

Calculating and commenting on each variance...........................................................................8

Preparing the different types of the budgets..............................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................2

PART A...........................................................................................................................................3

Computation of contribution per unit..........................................................................................3

Assessment of Breakeven Point in units and sales......................................................................3

Calculating margin of safety as a percentage of budgeted sales.................................................4

Assessing the number of units to be sold for gaining £700,000 profit........................................4

Explaining the importance of Contribution and its significance in business decision making...4

Preparing profitability statement using absorption and marginal costing system.......................5

PART B...........................................................................................................................................7

Demonstrating the importance of standard costing system and variance analysis......................7

Calculating and commenting on each variance...........................................................................8

Preparing the different types of the budgets..............................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

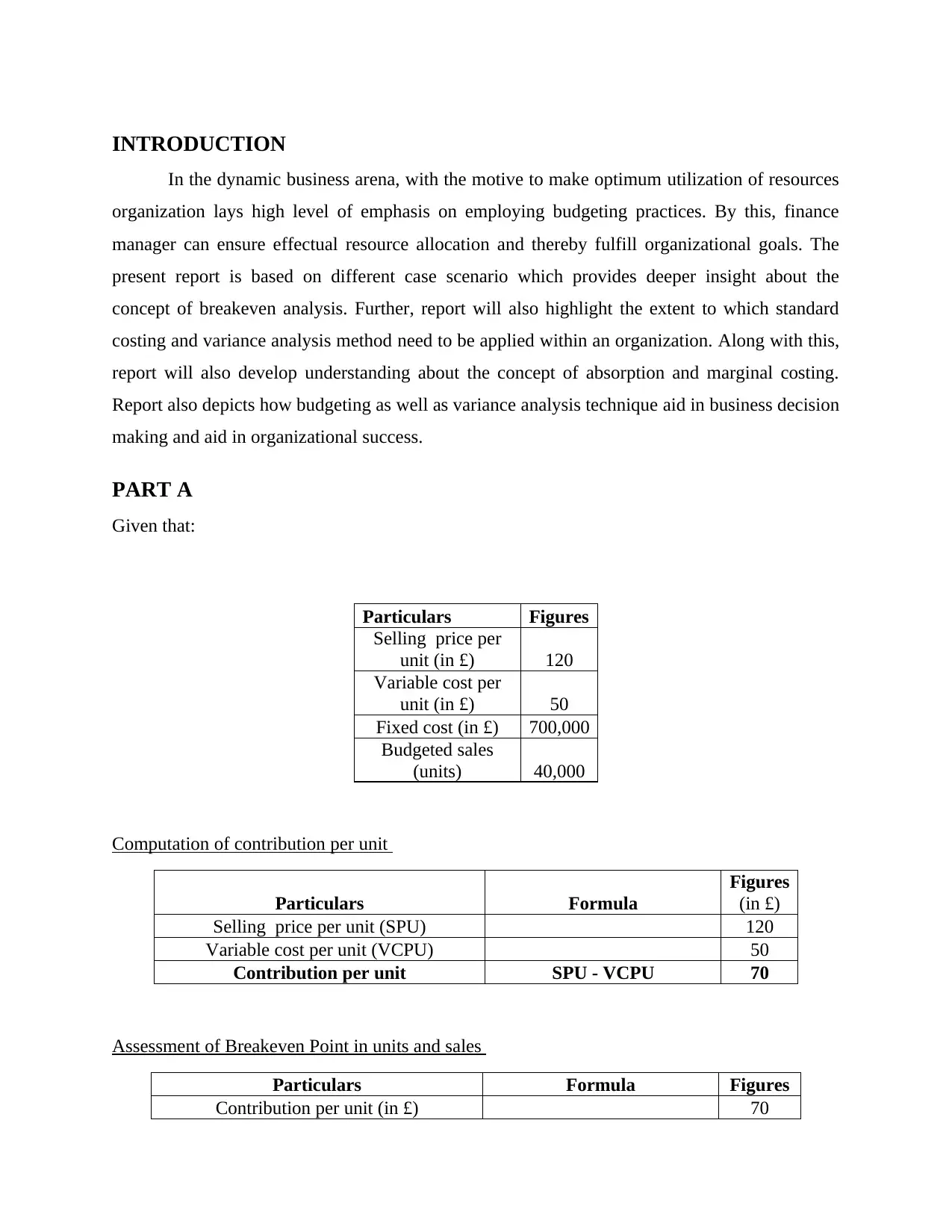

INTRODUCTION

In the dynamic business arena, with the motive to make optimum utilization of resources

organization lays high level of emphasis on employing budgeting practices. By this, finance

manager can ensure effectual resource allocation and thereby fulfill organizational goals. The

present report is based on different case scenario which provides deeper insight about the

concept of breakeven analysis. Further, report will also highlight the extent to which standard

costing and variance analysis method need to be applied within an organization. Along with this,

report will also develop understanding about the concept of absorption and marginal costing.

Report also depicts how budgeting as well as variance analysis technique aid in business decision

making and aid in organizational success.

PART A

Given that:

Particulars Figures

Selling price per

unit (in £) 120

Variable cost per

unit (in £) 50

Fixed cost (in £) 700,000

Budgeted sales

(units) 40,000

Computation of contribution per unit

Particulars Formula

Figures

(in £)

Selling price per unit (SPU) 120

Variable cost per unit (VCPU) 50

Contribution per unit SPU - VCPU 70

Assessment of Breakeven Point in units and sales

Particulars Formula Figures

Contribution per unit (in £) 70

In the dynamic business arena, with the motive to make optimum utilization of resources

organization lays high level of emphasis on employing budgeting practices. By this, finance

manager can ensure effectual resource allocation and thereby fulfill organizational goals. The

present report is based on different case scenario which provides deeper insight about the

concept of breakeven analysis. Further, report will also highlight the extent to which standard

costing and variance analysis method need to be applied within an organization. Along with this,

report will also develop understanding about the concept of absorption and marginal costing.

Report also depicts how budgeting as well as variance analysis technique aid in business decision

making and aid in organizational success.

PART A

Given that:

Particulars Figures

Selling price per

unit (in £) 120

Variable cost per

unit (in £) 50

Fixed cost (in £) 700,000

Budgeted sales

(units) 40,000

Computation of contribution per unit

Particulars Formula

Figures

(in £)

Selling price per unit (SPU) 120

Variable cost per unit (VCPU) 50

Contribution per unit SPU - VCPU 70

Assessment of Breakeven Point in units and sales

Particulars Formula Figures

Contribution per unit (in £) 70

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

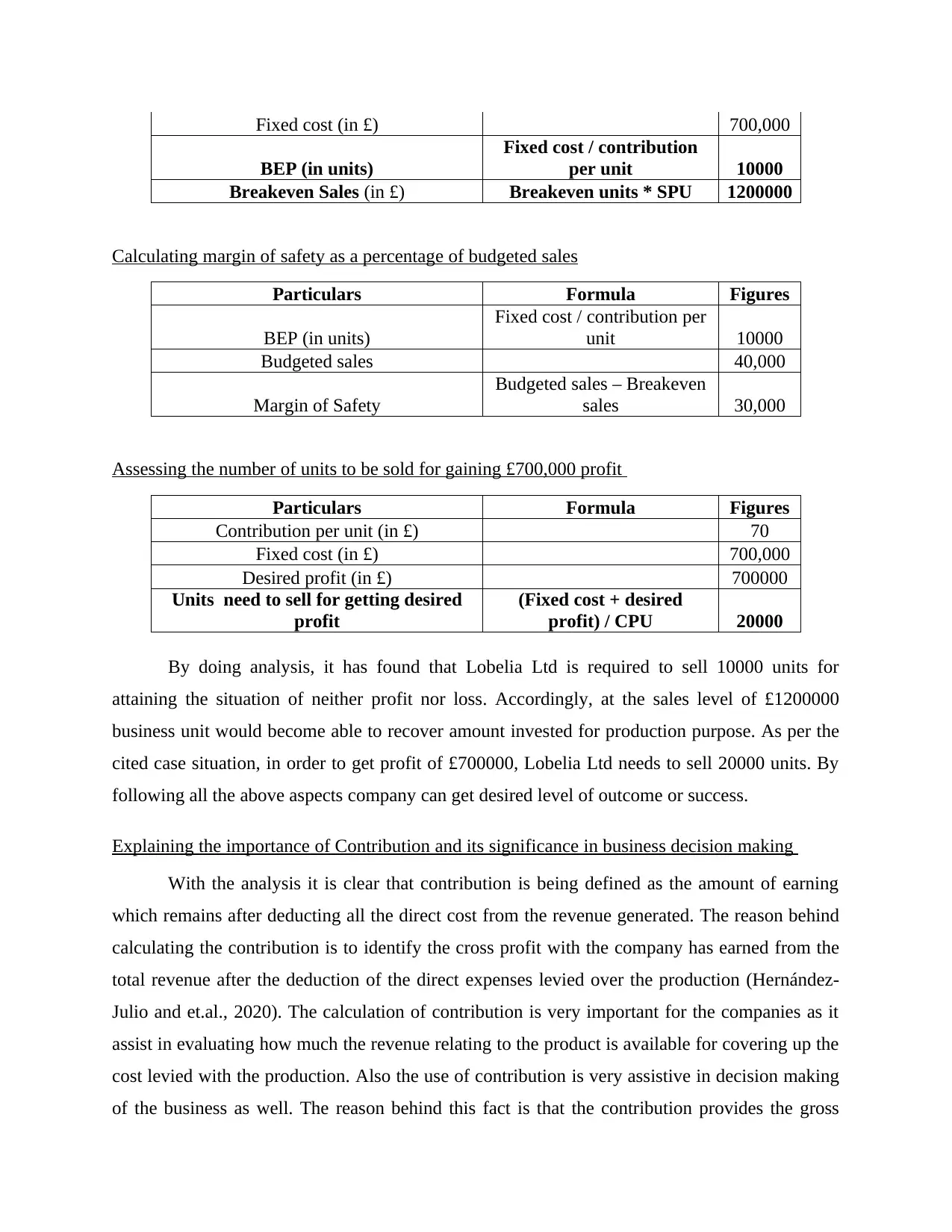

Fixed cost (in £) 700,000

BEP (in units)

Fixed cost / contribution

per unit 10000

Breakeven Sales (in £) Breakeven units * SPU 1200000

Calculating margin of safety as a percentage of budgeted sales

Particulars Formula Figures

BEP (in units)

Fixed cost / contribution per

unit 10000

Budgeted sales 40,000

Margin of Safety

Budgeted sales – Breakeven

sales 30,000

Assessing the number of units to be sold for gaining £700,000 profit

Particulars Formula Figures

Contribution per unit (in £) 70

Fixed cost (in £) 700,000

Desired profit (in £) 700000

Units need to sell for getting desired

profit

(Fixed cost + desired

profit) / CPU 20000

By doing analysis, it has found that Lobelia Ltd is required to sell 10000 units for

attaining the situation of neither profit nor loss. Accordingly, at the sales level of £1200000

business unit would become able to recover amount invested for production purpose. As per the

cited case situation, in order to get profit of £700000, Lobelia Ltd needs to sell 20000 units. By

following all the above aspects company can get desired level of outcome or success.

Explaining the importance of Contribution and its significance in business decision making

With the analysis it is clear that contribution is being defined as the amount of earning

which remains after deducting all the direct cost from the revenue generated. The reason behind

calculating the contribution is to identify the cross profit with the company has earned from the

total revenue after the deduction of the direct expenses levied over the production (Hernández-

Julio and et.al., 2020). The calculation of contribution is very important for the companies as it

assist in evaluating how much the revenue relating to the product is available for covering up the

cost levied with the production. Also the use of contribution is very assistive in decision making

of the business as well. The reason behind this fact is that the contribution provides the gross

BEP (in units)

Fixed cost / contribution

per unit 10000

Breakeven Sales (in £) Breakeven units * SPU 1200000

Calculating margin of safety as a percentage of budgeted sales

Particulars Formula Figures

BEP (in units)

Fixed cost / contribution per

unit 10000

Budgeted sales 40,000

Margin of Safety

Budgeted sales – Breakeven

sales 30,000

Assessing the number of units to be sold for gaining £700,000 profit

Particulars Formula Figures

Contribution per unit (in £) 70

Fixed cost (in £) 700,000

Desired profit (in £) 700000

Units need to sell for getting desired

profit

(Fixed cost + desired

profit) / CPU 20000

By doing analysis, it has found that Lobelia Ltd is required to sell 10000 units for

attaining the situation of neither profit nor loss. Accordingly, at the sales level of £1200000

business unit would become able to recover amount invested for production purpose. As per the

cited case situation, in order to get profit of £700000, Lobelia Ltd needs to sell 20000 units. By

following all the above aspects company can get desired level of outcome or success.

Explaining the importance of Contribution and its significance in business decision making

With the analysis it is clear that contribution is being defined as the amount of earning

which remains after deducting all the direct cost from the revenue generated. The reason behind

calculating the contribution is to identify the cross profit with the company has earned from the

total revenue after the deduction of the direct expenses levied over the production (Hernández-

Julio and et.al., 2020). The calculation of contribution is very important for the companies as it

assist in evaluating how much the revenue relating to the product is available for covering up the

cost levied with the production. Also the use of contribution is very assistive in decision making

of the business as well. The reason behind this fact is that the contribution provides the gross

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

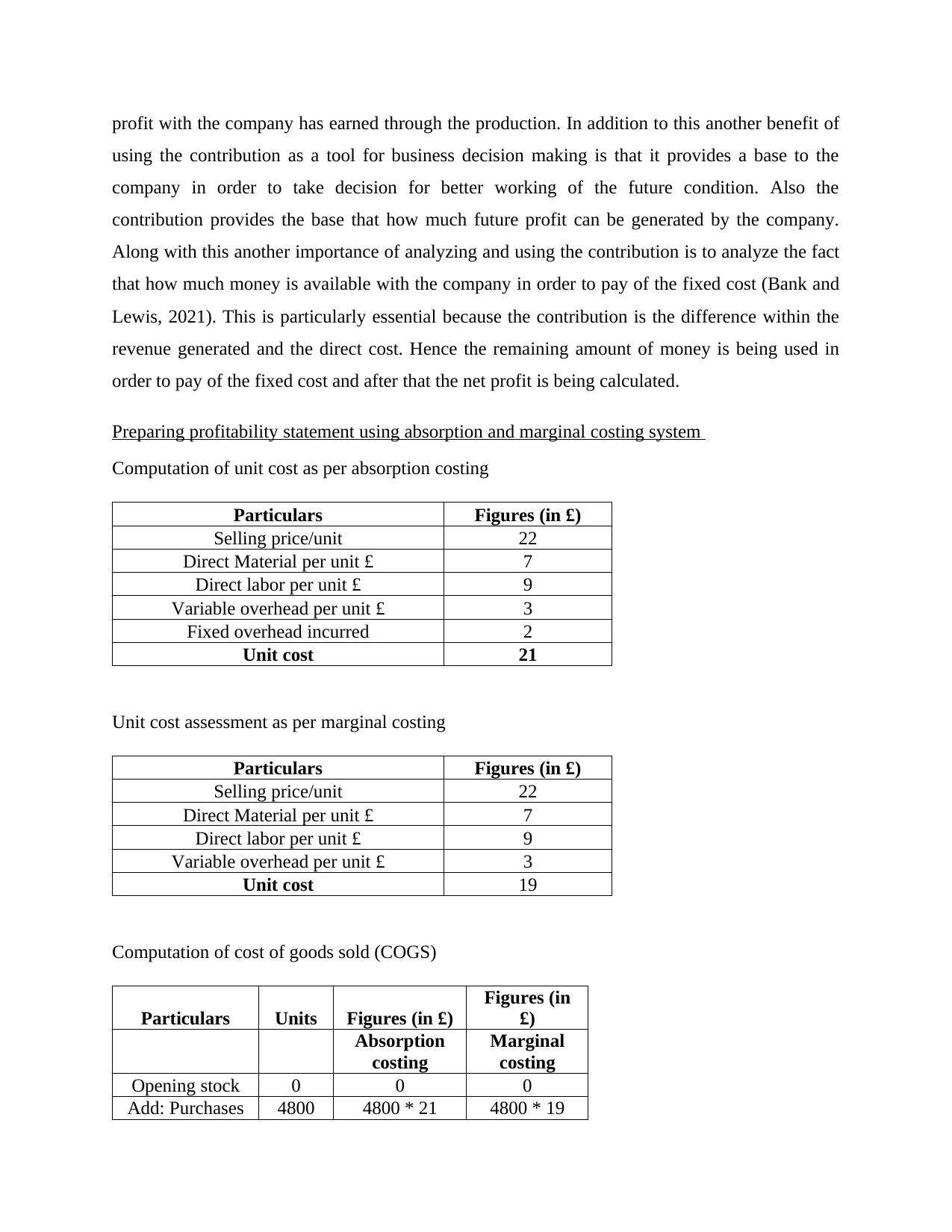

profit with the company has earned through the production. In addition to this another benefit of

using the contribution as a tool for business decision making is that it provides a base to the

company in order to take decision for better working of the future condition. Also the

contribution provides the base that how much future profit can be generated by the company.

Along with this another importance of analyzing and using the contribution is to analyze the fact

that how much money is available with the company in order to pay of the fixed cost (Bank and

Lewis, 2021). This is particularly essential because the contribution is the difference within the

revenue generated and the direct cost. Hence the remaining amount of money is being used in

order to pay of the fixed cost and after that the net profit is being calculated.

Preparing profitability statement using absorption and marginal costing system

Computation of unit cost as per absorption costing

Particulars Figures (in £)

Selling price/unit 22

Direct Material per unit £ 7

Direct labor per unit £ 9

Variable overhead per unit £ 3

Fixed overhead incurred 2

Unit cost 21

Unit cost assessment as per marginal costing

Particulars Figures (in £)

Selling price/unit 22

Direct Material per unit £ 7

Direct labor per unit £ 9

Variable overhead per unit £ 3

Unit cost 19

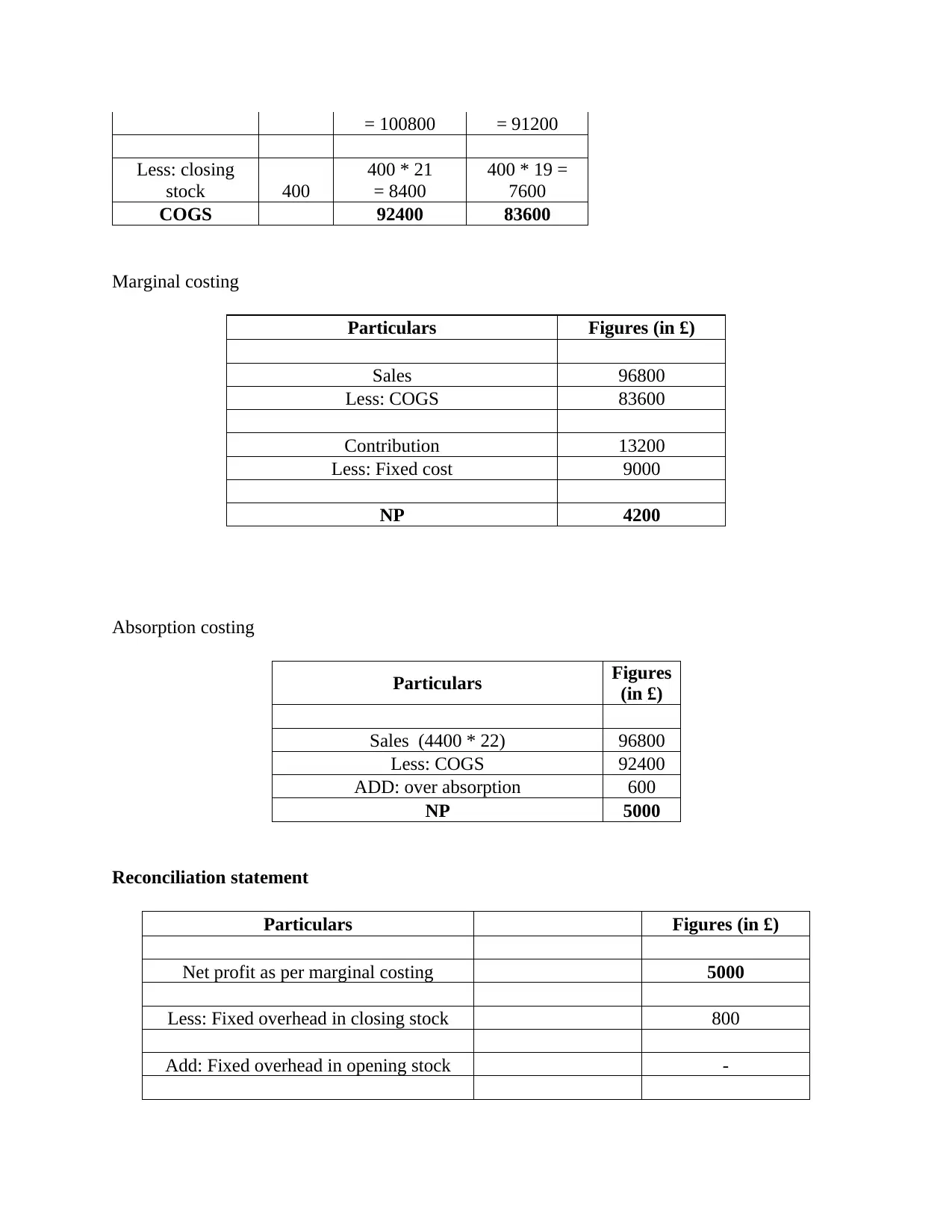

Computation of cost of goods sold (COGS)

Particulars Units Figures (in £)

Figures (in

£)

Absorption

costing

Marginal

costing

Opening stock 0 0 0

Add: Purchases 4800 4800 * 21 4800 * 19

using the contribution as a tool for business decision making is that it provides a base to the

company in order to take decision for better working of the future condition. Also the

contribution provides the base that how much future profit can be generated by the company.

Along with this another importance of analyzing and using the contribution is to analyze the fact

that how much money is available with the company in order to pay of the fixed cost (Bank and

Lewis, 2021). This is particularly essential because the contribution is the difference within the

revenue generated and the direct cost. Hence the remaining amount of money is being used in

order to pay of the fixed cost and after that the net profit is being calculated.

Preparing profitability statement using absorption and marginal costing system

Computation of unit cost as per absorption costing

Particulars Figures (in £)

Selling price/unit 22

Direct Material per unit £ 7

Direct labor per unit £ 9

Variable overhead per unit £ 3

Fixed overhead incurred 2

Unit cost 21

Unit cost assessment as per marginal costing

Particulars Figures (in £)

Selling price/unit 22

Direct Material per unit £ 7

Direct labor per unit £ 9

Variable overhead per unit £ 3

Unit cost 19

Computation of cost of goods sold (COGS)

Particulars Units Figures (in £)

Figures (in

£)

Absorption

costing

Marginal

costing

Opening stock 0 0 0

Add: Purchases 4800 4800 * 21 4800 * 19

= 100800 = 91200

Less: closing

stock 400

400 * 21

= 8400

400 * 19 =

7600

COGS 92400 83600

Marginal costing

Particulars Figures (in £)

Sales 96800

Less: COGS 83600

Contribution 13200

Less: Fixed cost 9000

NP 4200

Absorption costing

Particulars Figures

(in £)

Sales (4400 * 22) 96800

Less: COGS 92400

ADD: over absorption 600

NP 5000

Reconciliation statement

Particulars Figures (in £)

Net profit as per marginal costing 5000

Less: Fixed overhead in closing stock 800

Add: Fixed overhead in opening stock -

Less: closing

stock 400

400 * 21

= 8400

400 * 19 =

7600

COGS 92400 83600

Marginal costing

Particulars Figures (in £)

Sales 96800

Less: COGS 83600

Contribution 13200

Less: Fixed cost 9000

NP 4200

Absorption costing

Particulars Figures

(in £)

Sales (4400 * 22) 96800

Less: COGS 92400

ADD: over absorption 600

NP 5000

Reconciliation statement

Particulars Figures (in £)

Net profit as per marginal costing 5000

Less: Fixed overhead in closing stock 800

Add: Fixed overhead in opening stock -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit as per marginal costing 4200

PART B

Demonstrating the importance of standard costing system and variance analysis

Standard costing system

In accounting, standard costing system focuses on setting or determining standard cost

for material, labor and overhead. Apparel Ltd can exert control over cost by using standard

costing technique.

Significance

Efficiency level can be enhanced by Apparel Ltd through the means of standard costing

system. With the help of this system, management can make proper forecast about cost

pertaining to the future activities which in turns act as a control mechanism (Standard

costing, 2022).

Using standard costing system firm can also control cost related to material, labor etc

and thereby helps in making effective use of monetary resources in other productive

activities.

Variance analysis

This quantitative method of finance provides high level of assistance in finding

deviations that take place in company’s financial performance. Hence, by doing comparison of

budget output with the actual performance manager of Apparel Ltd can find out deficiencies in

monetary terms (Apollos, Stephen and Atunbi, 2018). With regards to Apparel Ltd significance

of variance analysis technique is as follows:

By using variance analysis tool manager can take prominent and future oriented

decisions about budgeting. The rationale behind this, it helps in assessing the level to

which existing budget is unrealistic. Referring this, manager of Apparel Ltd can set

suitable and realistic budget for the upcoming time period.

PART B

Demonstrating the importance of standard costing system and variance analysis

Standard costing system

In accounting, standard costing system focuses on setting or determining standard cost

for material, labor and overhead. Apparel Ltd can exert control over cost by using standard

costing technique.

Significance

Efficiency level can be enhanced by Apparel Ltd through the means of standard costing

system. With the help of this system, management can make proper forecast about cost

pertaining to the future activities which in turns act as a control mechanism (Standard

costing, 2022).

Using standard costing system firm can also control cost related to material, labor etc

and thereby helps in making effective use of monetary resources in other productive

activities.

Variance analysis

This quantitative method of finance provides high level of assistance in finding

deviations that take place in company’s financial performance. Hence, by doing comparison of

budget output with the actual performance manager of Apparel Ltd can find out deficiencies in

monetary terms (Apollos, Stephen and Atunbi, 2018). With regards to Apparel Ltd significance

of variance analysis technique is as follows:

By using variance analysis tool manager can take prominent and future oriented

decisions about budgeting. The rationale behind this, it helps in assessing the level to

which existing budget is unrealistic. Referring this, manager of Apparel Ltd can set

suitable and realistic budget for the upcoming time period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

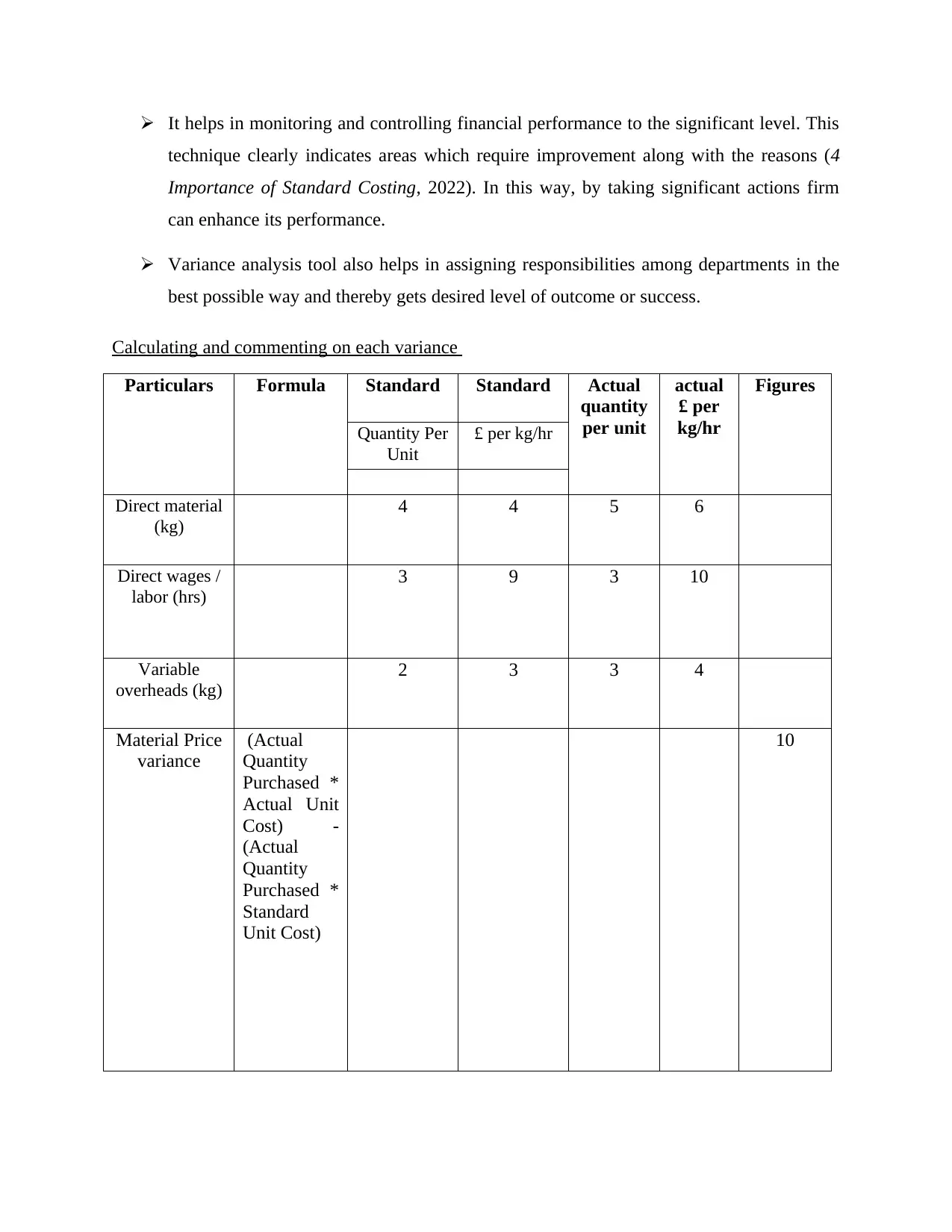

It helps in monitoring and controlling financial performance to the significant level. This

technique clearly indicates areas which require improvement along with the reasons (4

Importance of Standard Costing, 2022). In this way, by taking significant actions firm

can enhance its performance.

Variance analysis tool also helps in assigning responsibilities among departments in the

best possible way and thereby gets desired level of outcome or success.

Calculating and commenting on each variance

Particulars Formula Standard Standard Actual

quantity

per unit

actual

£ per

kg/hr

Figures

Quantity Per

Unit

£ per kg/hr

Direct material

(kg)

4 4 5 6

Direct wages /

labor (hrs)

3 9 3 10

Variable

overheads (kg)

2 3 3 4

Material Price

variance

(Actual

Quantity

Purchased *

Actual Unit

Cost) -

(Actual

Quantity

Purchased *

Standard

Unit Cost)

10

technique clearly indicates areas which require improvement along with the reasons (4

Importance of Standard Costing, 2022). In this way, by taking significant actions firm

can enhance its performance.

Variance analysis tool also helps in assigning responsibilities among departments in the

best possible way and thereby gets desired level of outcome or success.

Calculating and commenting on each variance

Particulars Formula Standard Standard Actual

quantity

per unit

actual

£ per

kg/hr

Figures

Quantity Per

Unit

£ per kg/hr

Direct material

(kg)

4 4 5 6

Direct wages /

labor (hrs)

3 9 3 10

Variable

overheads (kg)

2 3 3 4

Material Price

variance

(Actual

Quantity

Purchased *

Actual Unit

Cost) -

(Actual

Quantity

Purchased *

Standard

Unit Cost)

10

(Standard

quantity of

material –

Actual

quantity

used) × SPU

of material

-4

Material

Usage

variance

(Actual rate -

Standard

rate) x

Actual hours

worked

3

Labor Rate

variance

(Actual

hours -

Standard

hours) x

Standard rate

0

Labor

Efficiency

variance

Actual fixed

overhead -

Budgeted

fixed

overhead

-5000

Fixed

Overhead

Expenditure

variance

For the company to be successful it is very essential that proper variants analysis is being

undertaken for stop the variance analysis is a tool which August company in finding the

deviation within the budgeted and the actual performance. With the help of the material price

variance it is clear that the variance is favorable. This favorable variance implies that the actual

performance is better than the budgeted performance (Kraemer-Eis and et.al., 2019). Hence this

simply means that currently the company is performing well as expected. Further with help of

the material usage variants it is clear that the variance is adverse that is negative. This simply

quantity of

material –

Actual

quantity

used) × SPU

of material

-4

Material

Usage

variance

(Actual rate -

Standard

rate) x

Actual hours

worked

3

Labor Rate

variance

(Actual

hours -

Standard

hours) x

Standard rate

0

Labor

Efficiency

variance

Actual fixed

overhead -

Budgeted

fixed

overhead

-5000

Fixed

Overhead

Expenditure

variance

For the company to be successful it is very essential that proper variants analysis is being

undertaken for stop the variance analysis is a tool which August company in finding the

deviation within the budgeted and the actual performance. With the help of the material price

variance it is clear that the variance is favorable. This favorable variance implies that the actual

performance is better than the budgeted performance (Kraemer-Eis and et.al., 2019). Hence this

simply means that currently the company is performing well as expected. Further with help of

the material usage variants it is clear that the variance is adverse that is negative. This simply

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

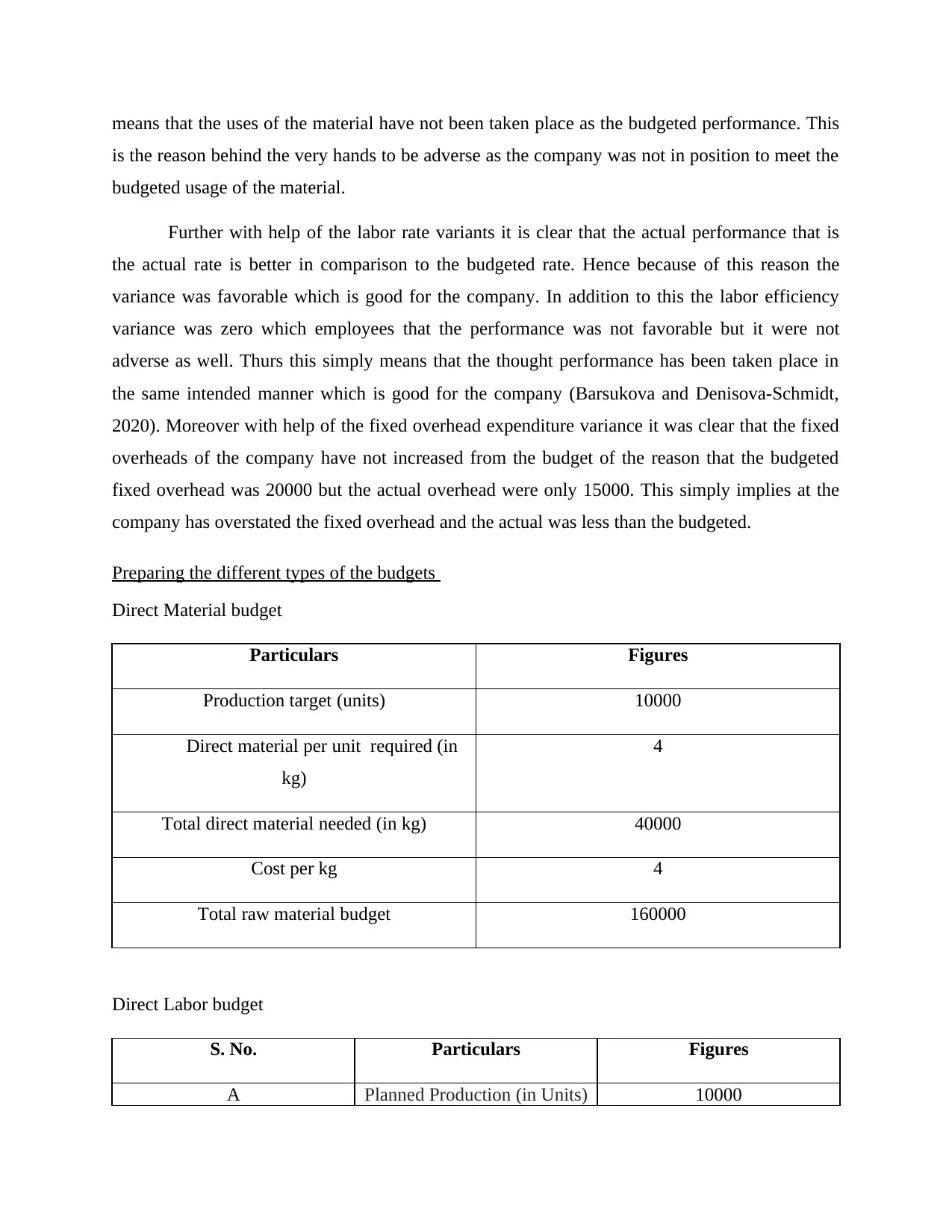

means that the uses of the material have not been taken place as the budgeted performance. This

is the reason behind the very hands to be adverse as the company was not in position to meet the

budgeted usage of the material.

Further with help of the labor rate variants it is clear that the actual performance that is

the actual rate is better in comparison to the budgeted rate. Hence because of this reason the

variance was favorable which is good for the company. In addition to this the labor efficiency

variance was zero which employees that the performance was not favorable but it were not

adverse as well. Thurs this simply means that the thought performance has been taken place in

the same intended manner which is good for the company (Barsukova and Denisova-Schmidt,

2020). Moreover with help of the fixed overhead expenditure variance it was clear that the fixed

overheads of the company have not increased from the budget of the reason that the budgeted

fixed overhead was 20000 but the actual overhead were only 15000. This simply implies at the

company has overstated the fixed overhead and the actual was less than the budgeted.

Preparing the different types of the budgets

Direct Material budget

Particulars Figures

Production target (units) 10000

Direct material per unit required (in

kg)

4

Total direct material needed (in kg) 40000

Cost per kg 4

Total raw material budget 160000

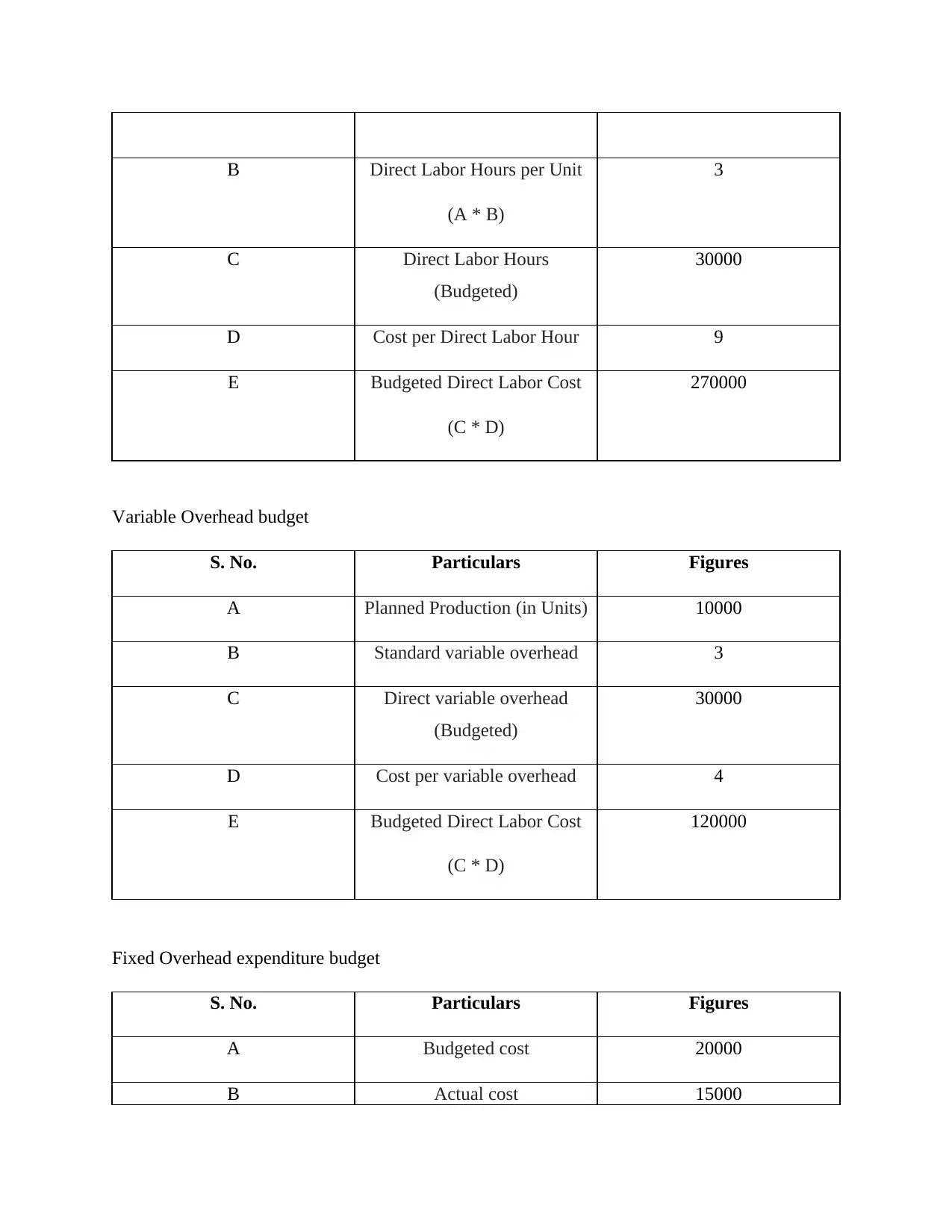

Direct Labor budget

S. No. Particulars Figures

A Planned Production (in Units) 10000

is the reason behind the very hands to be adverse as the company was not in position to meet the

budgeted usage of the material.

Further with help of the labor rate variants it is clear that the actual performance that is

the actual rate is better in comparison to the budgeted rate. Hence because of this reason the

variance was favorable which is good for the company. In addition to this the labor efficiency

variance was zero which employees that the performance was not favorable but it were not

adverse as well. Thurs this simply means that the thought performance has been taken place in

the same intended manner which is good for the company (Barsukova and Denisova-Schmidt,

2020). Moreover with help of the fixed overhead expenditure variance it was clear that the fixed

overheads of the company have not increased from the budget of the reason that the budgeted

fixed overhead was 20000 but the actual overhead were only 15000. This simply implies at the

company has overstated the fixed overhead and the actual was less than the budgeted.

Preparing the different types of the budgets

Direct Material budget

Particulars Figures

Production target (units) 10000

Direct material per unit required (in

kg)

4

Total direct material needed (in kg) 40000

Cost per kg 4

Total raw material budget 160000

Direct Labor budget

S. No. Particulars Figures

A Planned Production (in Units) 10000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

B Direct Labor Hours per Unit

(A * B)

3

C Direct Labor Hours

(Budgeted)

30000

D Cost per Direct Labor Hour 9

E Budgeted Direct Labor Cost

(C * D)

270000

Variable Overhead budget

S. No. Particulars Figures

A Planned Production (in Units) 10000

B Standard variable overhead 3

C Direct variable overhead

(Budgeted)

30000

D Cost per variable overhead 4

E Budgeted Direct Labor Cost

(C * D)

120000

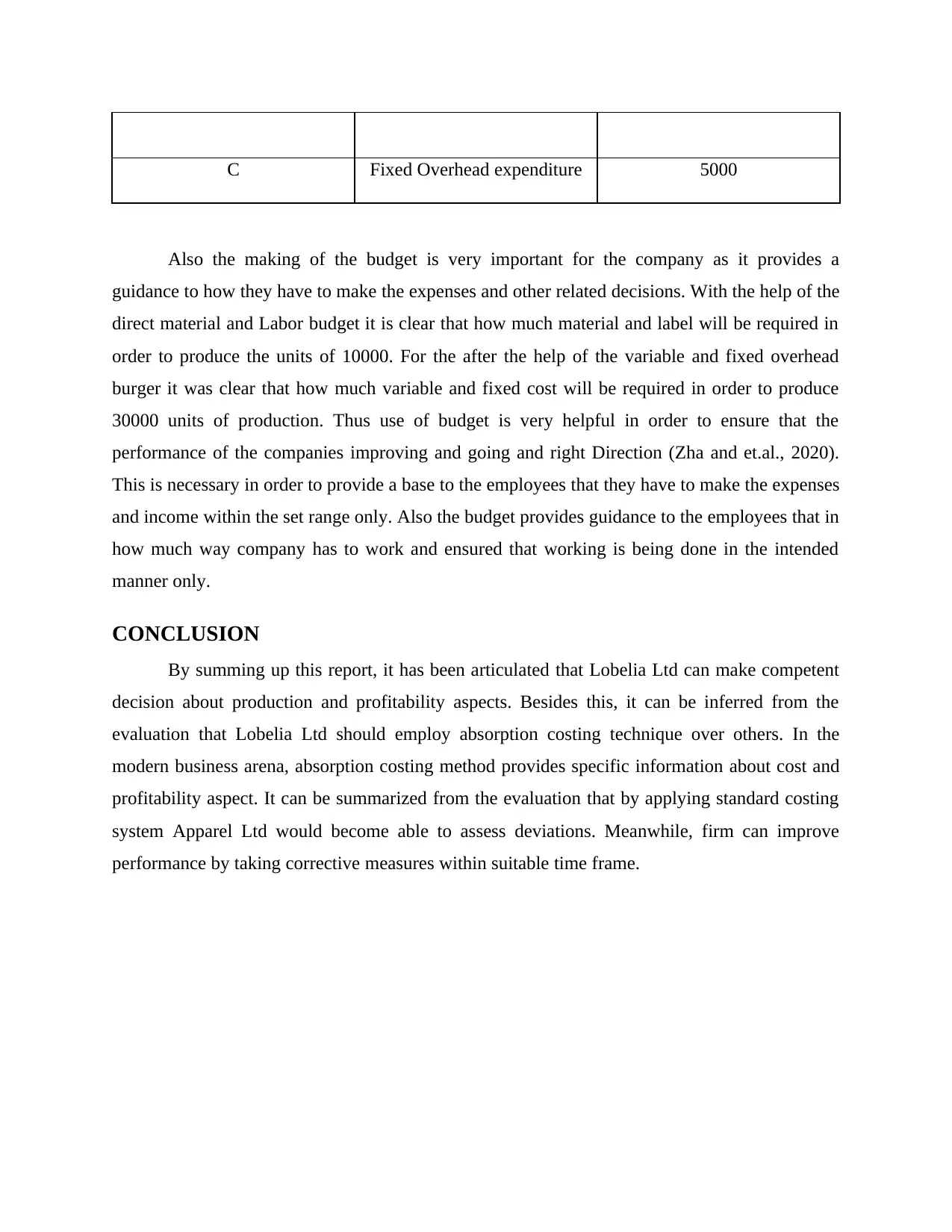

Fixed Overhead expenditure budget

S. No. Particulars Figures

A Budgeted cost 20000

B Actual cost 15000

(A * B)

3

C Direct Labor Hours

(Budgeted)

30000

D Cost per Direct Labor Hour 9

E Budgeted Direct Labor Cost

(C * D)

270000

Variable Overhead budget

S. No. Particulars Figures

A Planned Production (in Units) 10000

B Standard variable overhead 3

C Direct variable overhead

(Budgeted)

30000

D Cost per variable overhead 4

E Budgeted Direct Labor Cost

(C * D)

120000

Fixed Overhead expenditure budget

S. No. Particulars Figures

A Budgeted cost 20000

B Actual cost 15000

C Fixed Overhead expenditure 5000

Also the making of the budget is very important for the company as it provides a

guidance to how they have to make the expenses and other related decisions. With the help of the

direct material and Labor budget it is clear that how much material and label will be required in

order to produce the units of 10000. For the after the help of the variable and fixed overhead

burger it was clear that how much variable and fixed cost will be required in order to produce

30000 units of production. Thus use of budget is very helpful in order to ensure that the

performance of the companies improving and going and right Direction (Zha and et.al., 2020).

This is necessary in order to provide a base to the employees that they have to make the expenses

and income within the set range only. Also the budget provides guidance to the employees that in

how much way company has to work and ensured that working is being done in the intended

manner only.

CONCLUSION

By summing up this report, it has been articulated that Lobelia Ltd can make competent

decision about production and profitability aspects. Besides this, it can be inferred from the

evaluation that Lobelia Ltd should employ absorption costing technique over others. In the

modern business arena, absorption costing method provides specific information about cost and

profitability aspect. It can be summarized from the evaluation that by applying standard costing

system Apparel Ltd would become able to assess deviations. Meanwhile, firm can improve

performance by taking corrective measures within suitable time frame.

Also the making of the budget is very important for the company as it provides a

guidance to how they have to make the expenses and other related decisions. With the help of the

direct material and Labor budget it is clear that how much material and label will be required in

order to produce the units of 10000. For the after the help of the variable and fixed overhead

burger it was clear that how much variable and fixed cost will be required in order to produce

30000 units of production. Thus use of budget is very helpful in order to ensure that the

performance of the companies improving and going and right Direction (Zha and et.al., 2020).

This is necessary in order to provide a base to the employees that they have to make the expenses

and income within the set range only. Also the budget provides guidance to the employees that in

how much way company has to work and ensured that working is being done in the intended

manner only.

CONCLUSION

By summing up this report, it has been articulated that Lobelia Ltd can make competent

decision about production and profitability aspects. Besides this, it can be inferred from the

evaluation that Lobelia Ltd should employ absorption costing technique over others. In the

modern business arena, absorption costing method provides specific information about cost and

profitability aspect. It can be summarized from the evaluation that by applying standard costing

system Apparel Ltd would become able to assess deviations. Meanwhile, firm can improve

performance by taking corrective measures within suitable time frame.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.