LSME505 Business Finance: Costing, Budgeting & Investment Decisions

VerifiedAdded on 2023/06/11

|12

|2611

|161

Case Study

AI Summary

This business finance case study for Lobelia Ltd. analyzes costing methods, break-even points, margin of safety, and profit determination using marginal and absorption costing. It includes a memo to the financial manager and a reconciliation statement. The study further examines the importance of standard costing and variance analysis for Apparel Plc, calculating variances and preparing budgets for a target production of 10,000 units. The analysis covers direct material, direct labor, and overhead budgeting, providing a comprehensive overview of financial management techniques and their application in a business context. Desklib provides a platform for students to access similar solved assignments and past papers.

Business Finance CASE

STUDY 1

STUDY 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Calculating the contribution per unit...........................................................................................3

Calculating Break Even Point in units and sales volume............................................................3

Calculating Margin of Safety.......................................................................................................4

Calculation of the number of units to be sold for reaching desired profit of £700,000..............4

Memo for the Financial Manager................................................................................................4

Marginal and absorption costing methods of profit determination..............................................5

PART B............................................................................................................................................7

Importance of standard costing system and variance analysis.....................................................7

Calculating variances...................................................................................................................8

Preparation of budgets for the target of 10000 units...................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Calculating the contribution per unit...........................................................................................3

Calculating Break Even Point in units and sales volume............................................................3

Calculating Margin of Safety.......................................................................................................4

Calculation of the number of units to be sold for reaching desired profit of £700,000..............4

Memo for the Financial Manager................................................................................................4

Marginal and absorption costing methods of profit determination..............................................5

PART B............................................................................................................................................7

Importance of standard costing system and variance analysis.....................................................7

Calculating variances...................................................................................................................8

Preparation of budgets for the target of 10000 units...................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................11

INTRODUCTION

Business finance is that term of business world which is concerned with raising or

acquiring the required funds for the short and long term objective fulfillment of an organization.

The report, for Lobelia Ltd., will calculate contribution per unit along with break even units and

sales. The margin of safety and units requirement for production in order to earn desired profits

by Lobelia Ltd. will be highlighted. Further the will draft a memo to financial manager.

Calculation of profits as per marginal and absorption costing with the reconciliation of difference

in profits will be done. In addition differed variances will be find out and varied budgets will be

prepared for Apparel Plc.

PART A

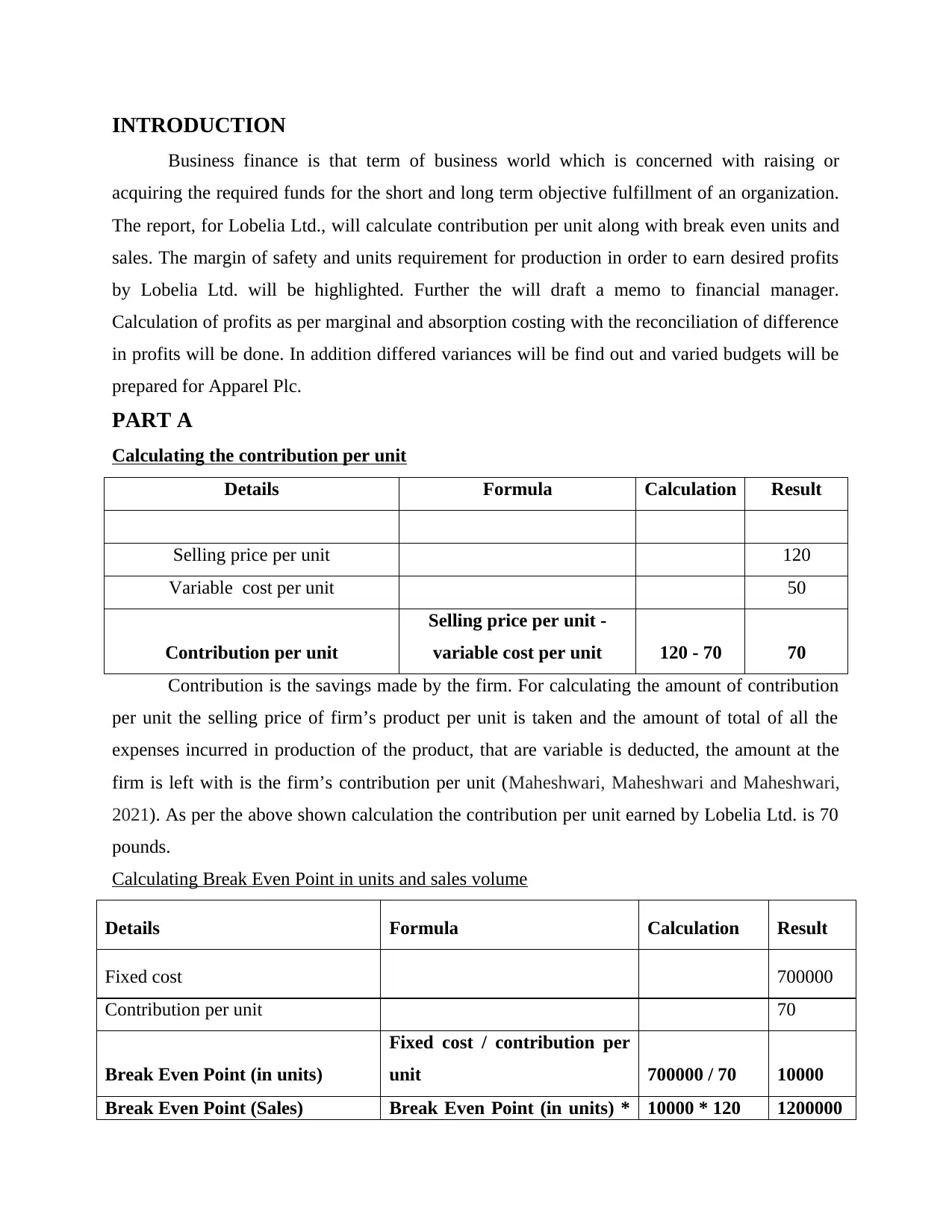

Calculating the contribution per unit

Details Formula Calculation Result

Selling price per unit 120

Variable cost per unit 50

Contribution per unit

Selling price per unit -

variable cost per unit 120 - 70 70

Contribution is the savings made by the firm. For calculating the amount of contribution

per unit the selling price of firm’s product per unit is taken and the amount of total of all the

expenses incurred in production of the product, that are variable is deducted, the amount at the

firm is left with is the firm’s contribution per unit (Maheshwari, Maheshwari and Maheshwari,

2021). As per the above shown calculation the contribution per unit earned by Lobelia Ltd. is 70

pounds.

Calculating Break Even Point in units and sales volume

Details Formula Calculation Result

Fixed cost 700000

Contribution per unit 70

Break Even Point (in units)

Fixed cost / contribution per

unit 700000 / 70 10000

Break Even Point (Sales) Break Even Point (in units) * 10000 * 120 1200000

Business finance is that term of business world which is concerned with raising or

acquiring the required funds for the short and long term objective fulfillment of an organization.

The report, for Lobelia Ltd., will calculate contribution per unit along with break even units and

sales. The margin of safety and units requirement for production in order to earn desired profits

by Lobelia Ltd. will be highlighted. Further the will draft a memo to financial manager.

Calculation of profits as per marginal and absorption costing with the reconciliation of difference

in profits will be done. In addition differed variances will be find out and varied budgets will be

prepared for Apparel Plc.

PART A

Calculating the contribution per unit

Details Formula Calculation Result

Selling price per unit 120

Variable cost per unit 50

Contribution per unit

Selling price per unit -

variable cost per unit 120 - 70 70

Contribution is the savings made by the firm. For calculating the amount of contribution

per unit the selling price of firm’s product per unit is taken and the amount of total of all the

expenses incurred in production of the product, that are variable is deducted, the amount at the

firm is left with is the firm’s contribution per unit (Maheshwari, Maheshwari and Maheshwari,

2021). As per the above shown calculation the contribution per unit earned by Lobelia Ltd. is 70

pounds.

Calculating Break Even Point in units and sales volume

Details Formula Calculation Result

Fixed cost 700000

Contribution per unit 70

Break Even Point (in units)

Fixed cost / contribution per

unit 700000 / 70 10000

Break Even Point (Sales) Break Even Point (in units) * 10000 * 120 1200000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

selling price per unit

Break Even point for a firm can be calculated in the number of units or sales revenue.

Lobelia Ltd’s break even units are 10000 units and break even sales is 1200000 pounds. It means

that for reaching the situation of no profit and no loss the firm must sell 10000 units earning a

sales revenue of 1200000 pounds.

Calculating Margin of Safety

Details Formula Calculation Result

Margin of safety Budgeted sales – break even sales

4800000 -

1200000 3600000

Budgeted Sales Budgeted units * Selling price per unit 40000 * 120 4800000

Margin of safety as percentage of

budgeted sales (Marking of Safety/Budgeted Sales)*100

(3600000 /

4800000) *

100 75

Margin of safety like break even point can be calculated both in number of units and sales

revenue. Margin of safety is the excess of unit sold or sales revenue earned by the firm over its

break even sales or break even units (Vagner, 2020). The budgeted or targeted sales volume by

Lobelia Ltd is £4800000 aiming to achieve by selling 40000 units by firm at £120 per unit.And

the break even sales for the firm is 1200000. It means that the firm is planning to maintain a

margin of 75% as safety.

Calculation of the number of units to be sold for reaching desired profit of £700,000

Details Formula Calculation Result

Fixed Cost 700000

Desired profit 700000

Contribution per unit 70

Number of units required to sell

Fixed cost + desired profit

margin / contribution per

unit

(700000 +

700000) /

70 20000

Every firm targets to achieve a certain level of profit. This targeted profit is known as

desired profit by the company. Lobelia Ltd. desires to earn a profit of £700000. For reaching the

position in which the firm could earn the desired amount of profit it must sell 20000 units

provided that the contribution per unit is £70.

Break Even point for a firm can be calculated in the number of units or sales revenue.

Lobelia Ltd’s break even units are 10000 units and break even sales is 1200000 pounds. It means

that for reaching the situation of no profit and no loss the firm must sell 10000 units earning a

sales revenue of 1200000 pounds.

Calculating Margin of Safety

Details Formula Calculation Result

Margin of safety Budgeted sales – break even sales

4800000 -

1200000 3600000

Budgeted Sales Budgeted units * Selling price per unit 40000 * 120 4800000

Margin of safety as percentage of

budgeted sales (Marking of Safety/Budgeted Sales)*100

(3600000 /

4800000) *

100 75

Margin of safety like break even point can be calculated both in number of units and sales

revenue. Margin of safety is the excess of unit sold or sales revenue earned by the firm over its

break even sales or break even units (Vagner, 2020). The budgeted or targeted sales volume by

Lobelia Ltd is £4800000 aiming to achieve by selling 40000 units by firm at £120 per unit.And

the break even sales for the firm is 1200000. It means that the firm is planning to maintain a

margin of 75% as safety.

Calculation of the number of units to be sold for reaching desired profit of £700,000

Details Formula Calculation Result

Fixed Cost 700000

Desired profit 700000

Contribution per unit 70

Number of units required to sell

Fixed cost + desired profit

margin / contribution per

unit

(700000 +

700000) /

70 20000

Every firm targets to achieve a certain level of profit. This targeted profit is known as

desired profit by the company. Lobelia Ltd. desires to earn a profit of £700000. For reaching the

position in which the firm could earn the desired amount of profit it must sell 20000 units

provided that the contribution per unit is £70.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

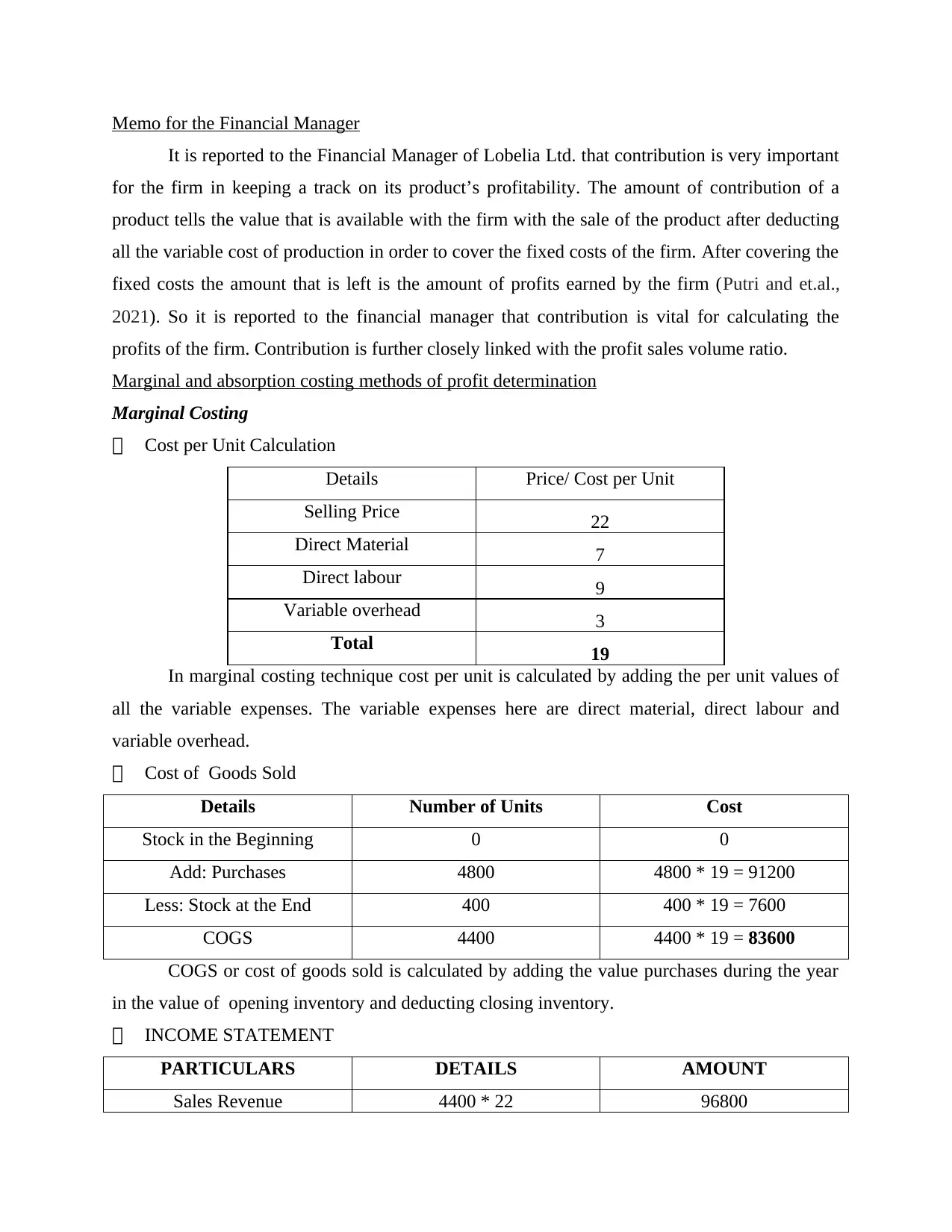

Memo for the Financial Manager

It is reported to the Financial Manager of Lobelia Ltd. that contribution is very important

for the firm in keeping a track on its product’s profitability. The amount of contribution of a

product tells the value that is available with the firm with the sale of the product after deducting

all the variable cost of production in order to cover the fixed costs of the firm. After covering the

fixed costs the amount that is left is the amount of profits earned by the firm (Putri and et.al.,

2021). So it is reported to the financial manager that contribution is vital for calculating the

profits of the firm. Contribution is further closely linked with the profit sales volume ratio.

Marginal and absorption costing methods of profit determination

Marginal Costing

Cost per Unit Calculation

Details Price/ Cost per Unit

Selling Price 22

Direct Material 7

Direct labour 9

Variable overhead 3

Total 19

In marginal costing technique cost per unit is calculated by adding the per unit values of

all the variable expenses. The variable expenses here are direct material, direct labour and

variable overhead.

Cost of Goods Sold

Details Number of Units Cost

Stock in the Beginning 0 0

Add: Purchases 4800 4800 * 19 = 91200

Less: Stock at the End 400 400 * 19 = 7600

COGS 4400 4400 * 19 = 83600

COGS or cost of goods sold is calculated by adding the value purchases during the year

in the value of opening inventory and deducting closing inventory.

INCOME STATEMENT

PARTICULARS DETAILS AMOUNT

Sales Revenue 4400 * 22 96800

It is reported to the Financial Manager of Lobelia Ltd. that contribution is very important

for the firm in keeping a track on its product’s profitability. The amount of contribution of a

product tells the value that is available with the firm with the sale of the product after deducting

all the variable cost of production in order to cover the fixed costs of the firm. After covering the

fixed costs the amount that is left is the amount of profits earned by the firm (Putri and et.al.,

2021). So it is reported to the financial manager that contribution is vital for calculating the

profits of the firm. Contribution is further closely linked with the profit sales volume ratio.

Marginal and absorption costing methods of profit determination

Marginal Costing

Cost per Unit Calculation

Details Price/ Cost per Unit

Selling Price 22

Direct Material 7

Direct labour 9

Variable overhead 3

Total 19

In marginal costing technique cost per unit is calculated by adding the per unit values of

all the variable expenses. The variable expenses here are direct material, direct labour and

variable overhead.

Cost of Goods Sold

Details Number of Units Cost

Stock in the Beginning 0 0

Add: Purchases 4800 4800 * 19 = 91200

Less: Stock at the End 400 400 * 19 = 7600

COGS 4400 4400 * 19 = 83600

COGS or cost of goods sold is calculated by adding the value purchases during the year

in the value of opening inventory and deducting closing inventory.

INCOME STATEMENT

PARTICULARS DETAILS AMOUNT

Sales Revenue 4400 * 22 96800

Less: COGS (83600) (83600)

Contribution (96800 - 83600) 13200

Less: Fixed Costs (9000) (9000)

Net Profit 4200

Income statement under marginal costing calculates the Net Profit amount by subtracting

the cost of goods sold and fixed costs from the sales revenue.

Absorption costing

Cost per Unit Calculation

Details Price/ Cost per Unit

Selling Price 22

Direct Material 7

Direct labour 9

Variable overhead 3

Fixed overhead 2

Total 21

Cost per unit under absorption costing is inclusive of all the per unit expenses incurred by

the firm whether variable or fixed.

Cost of Goods Sold

Details Number of Units Cost

Stock in the Beginning 0 0

Add: Purchases 4800 4800 * 21 = 100800

Less: Stock at the End 400 400 * 21 = 8400

COGS 4400 4400 * 21 = 92400

Cost of goods sold is calculated the same way as in marginal costing method the only

difference is in the value of per unit cost (Martinović, 2019). The difference is due to inclusion

of fixed overhead in cost per unit under absorption costing whereas the marginal costing

excludes the fixed overhead value and considers only the cost that is incurred additionally with

every additional unit produced by the firm,

INCOME STATEMENT

PARTICULARS DETAILS AMOUNT

Contribution (96800 - 83600) 13200

Less: Fixed Costs (9000) (9000)

Net Profit 4200

Income statement under marginal costing calculates the Net Profit amount by subtracting

the cost of goods sold and fixed costs from the sales revenue.

Absorption costing

Cost per Unit Calculation

Details Price/ Cost per Unit

Selling Price 22

Direct Material 7

Direct labour 9

Variable overhead 3

Fixed overhead 2

Total 21

Cost per unit under absorption costing is inclusive of all the per unit expenses incurred by

the firm whether variable or fixed.

Cost of Goods Sold

Details Number of Units Cost

Stock in the Beginning 0 0

Add: Purchases 4800 4800 * 21 = 100800

Less: Stock at the End 400 400 * 21 = 8400

COGS 4400 4400 * 21 = 92400

Cost of goods sold is calculated the same way as in marginal costing method the only

difference is in the value of per unit cost (Martinović, 2019). The difference is due to inclusion

of fixed overhead in cost per unit under absorption costing whereas the marginal costing

excludes the fixed overhead value and considers only the cost that is incurred additionally with

every additional unit produced by the firm,

INCOME STATEMENT

PARTICULARS DETAILS AMOUNT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

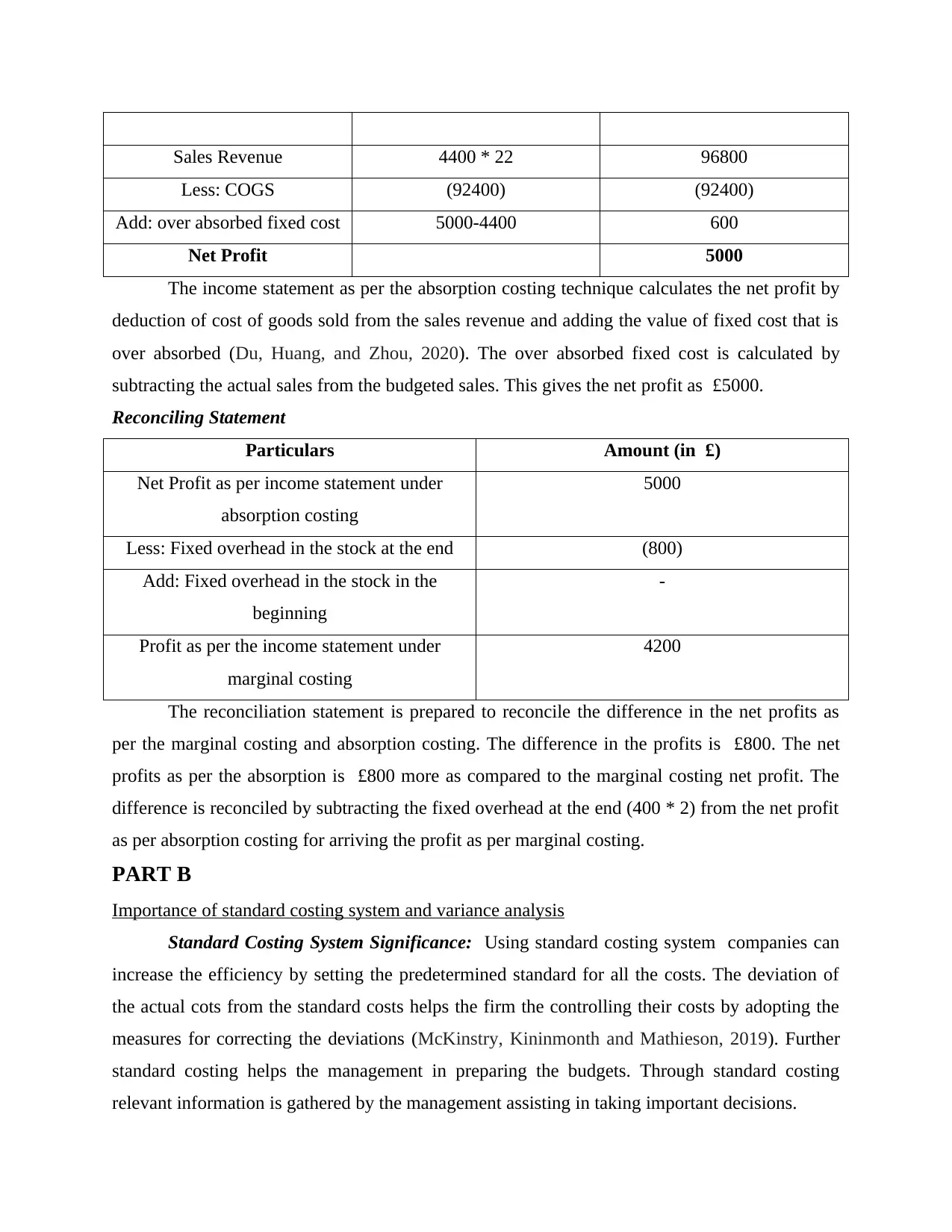

Sales Revenue 4400 * 22 96800

Less: COGS (92400) (92400)

Add: over absorbed fixed cost 5000-4400 600

Net Profit 5000

The income statement as per the absorption costing technique calculates the net profit by

deduction of cost of goods sold from the sales revenue and adding the value of fixed cost that is

over absorbed (Du, Huang, and Zhou, 2020). The over absorbed fixed cost is calculated by

subtracting the actual sales from the budgeted sales. This gives the net profit as £5000.

Reconciling Statement

Particulars Amount (in £)

Net Profit as per income statement under

absorption costing

5000

Less: Fixed overhead in the stock at the end (800)

Add: Fixed overhead in the stock in the

beginning

-

Profit as per the income statement under

marginal costing

4200

The reconciliation statement is prepared to reconcile the difference in the net profits as

per the marginal costing and absorption costing. The difference in the profits is £800. The net

profits as per the absorption is £800 more as compared to the marginal costing net profit. The

difference is reconciled by subtracting the fixed overhead at the end (400 * 2) from the net profit

as per absorption costing for arriving the profit as per marginal costing.

PART B

Importance of standard costing system and variance analysis

Standard Costing System Significance: Using standard costing system companies can

increase the efficiency by setting the predetermined standard for all the costs. The deviation of

the actual cots from the standard costs helps the firm the controlling their costs by adopting the

measures for correcting the deviations (McKinstry, Kininmonth and Mathieson, 2019). Further

standard costing helps the management in preparing the budgets. Through standard costing

relevant information is gathered by the management assisting in taking important decisions.

Less: COGS (92400) (92400)

Add: over absorbed fixed cost 5000-4400 600

Net Profit 5000

The income statement as per the absorption costing technique calculates the net profit by

deduction of cost of goods sold from the sales revenue and adding the value of fixed cost that is

over absorbed (Du, Huang, and Zhou, 2020). The over absorbed fixed cost is calculated by

subtracting the actual sales from the budgeted sales. This gives the net profit as £5000.

Reconciling Statement

Particulars Amount (in £)

Net Profit as per income statement under

absorption costing

5000

Less: Fixed overhead in the stock at the end (800)

Add: Fixed overhead in the stock in the

beginning

-

Profit as per the income statement under

marginal costing

4200

The reconciliation statement is prepared to reconcile the difference in the net profits as

per the marginal costing and absorption costing. The difference in the profits is £800. The net

profits as per the absorption is £800 more as compared to the marginal costing net profit. The

difference is reconciled by subtracting the fixed overhead at the end (400 * 2) from the net profit

as per absorption costing for arriving the profit as per marginal costing.

PART B

Importance of standard costing system and variance analysis

Standard Costing System Significance: Using standard costing system companies can

increase the efficiency by setting the predetermined standard for all the costs. The deviation of

the actual cots from the standard costs helps the firm the controlling their costs by adopting the

measures for correcting the deviations (McKinstry, Kininmonth and Mathieson, 2019). Further

standard costing helps the management in preparing the budgets. Through standard costing

relevant information is gathered by the management assisting in taking important decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

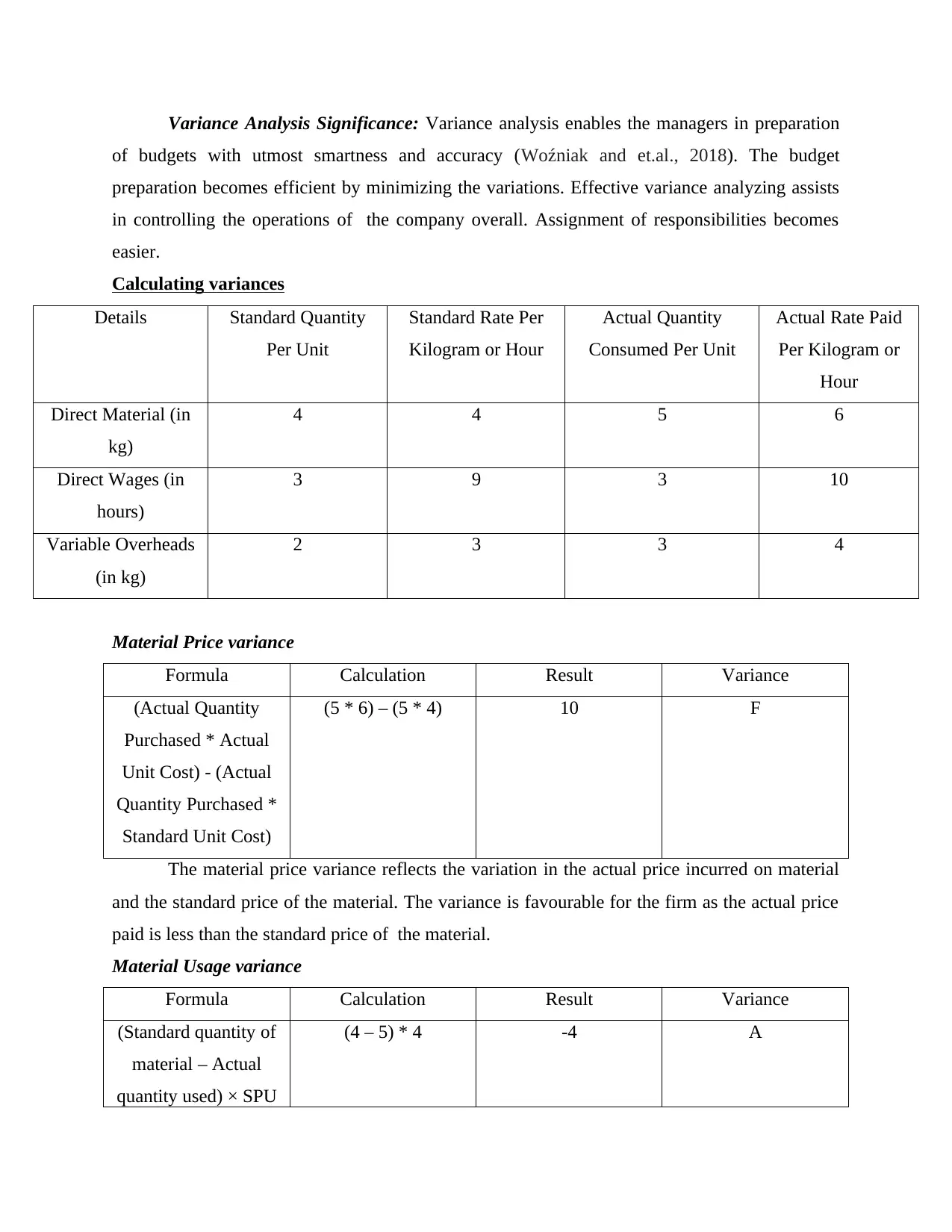

Variance Analysis Significance: Variance analysis enables the managers in preparation

of budgets with utmost smartness and accuracy (Woźniak and et.al., 2018). The budget

preparation becomes efficient by minimizing the variations. Effective variance analyzing assists

in controlling the operations of the company overall. Assignment of responsibilities becomes

easier.

Calculating variances

Details Standard Quantity

Per Unit

Standard Rate Per

Kilogram or Hour

Actual Quantity

Consumed Per Unit

Actual Rate Paid

Per Kilogram or

Hour

Direct Material (in

kg)

4 4 5 6

Direct Wages (in

hours)

3 9 3 10

Variable Overheads

(in kg)

2 3 3 4

Material Price variance

Formula Calculation Result Variance

(Actual Quantity

Purchased * Actual

Unit Cost) - (Actual

Quantity Purchased *

Standard Unit Cost)

(5 * 6) – (5 * 4) 10 F

The material price variance reflects the variation in the actual price incurred on material

and the standard price of the material. The variance is favourable for the firm as the actual price

paid is less than the standard price of the material.

Material Usage variance

Formula Calculation Result Variance

(Standard quantity of

material – Actual

quantity used) × SPU

(4 – 5) * 4 -4 A

of budgets with utmost smartness and accuracy (Woźniak and et.al., 2018). The budget

preparation becomes efficient by minimizing the variations. Effective variance analyzing assists

in controlling the operations of the company overall. Assignment of responsibilities becomes

easier.

Calculating variances

Details Standard Quantity

Per Unit

Standard Rate Per

Kilogram or Hour

Actual Quantity

Consumed Per Unit

Actual Rate Paid

Per Kilogram or

Hour

Direct Material (in

kg)

4 4 5 6

Direct Wages (in

hours)

3 9 3 10

Variable Overheads

(in kg)

2 3 3 4

Material Price variance

Formula Calculation Result Variance

(Actual Quantity

Purchased * Actual

Unit Cost) - (Actual

Quantity Purchased *

Standard Unit Cost)

(5 * 6) – (5 * 4) 10 F

The material price variance reflects the variation in the actual price incurred on material

and the standard price of the material. The variance is favourable for the firm as the actual price

paid is less than the standard price of the material.

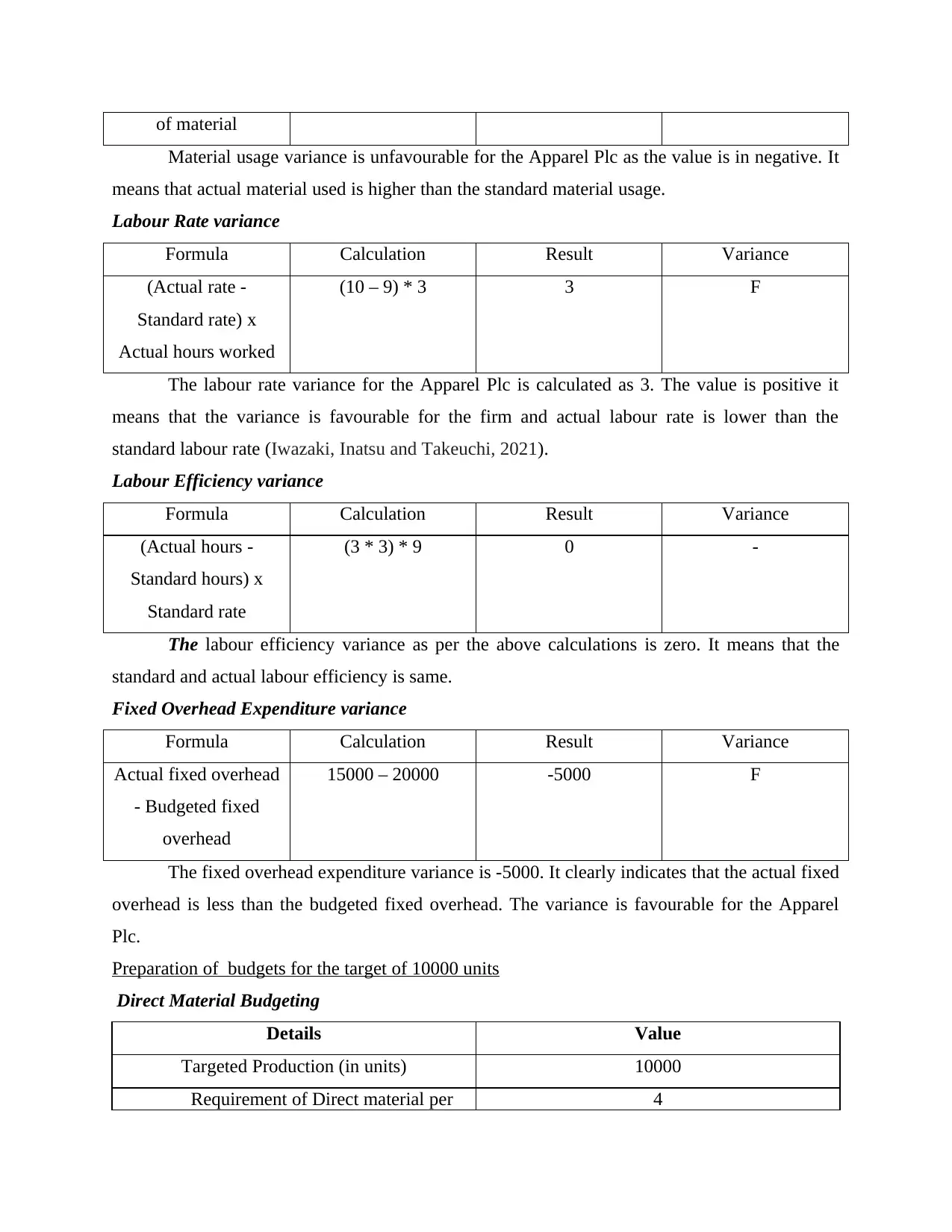

Material Usage variance

Formula Calculation Result Variance

(Standard quantity of

material – Actual

quantity used) × SPU

(4 – 5) * 4 -4 A

of material

Material usage variance is unfavourable for the Apparel Plc as the value is in negative. It

means that actual material used is higher than the standard material usage.

Labour Rate variance

Formula Calculation Result Variance

(Actual rate -

Standard rate) x

Actual hours worked

(10 – 9) * 3 3 F

The labour rate variance for the Apparel Plc is calculated as 3. The value is positive it

means that the variance is favourable for the firm and actual labour rate is lower than the

standard labour rate (Iwazaki, Inatsu and Takeuchi, 2021).

Labour Efficiency variance

Formula Calculation Result Variance

(Actual hours -

Standard hours) x

Standard rate

(3 * 3) * 9 0 -

The labour efficiency variance as per the above calculations is zero. It means that the

standard and actual labour efficiency is same.

Fixed Overhead Expenditure variance

Formula Calculation Result Variance

Actual fixed overhead

- Budgeted fixed

overhead

15000 – 20000 -5000 F

The fixed overhead expenditure variance is -5000. It clearly indicates that the actual fixed

overhead is less than the budgeted fixed overhead. The variance is favourable for the Apparel

Plc.

Preparation of budgets for the target of 10000 units

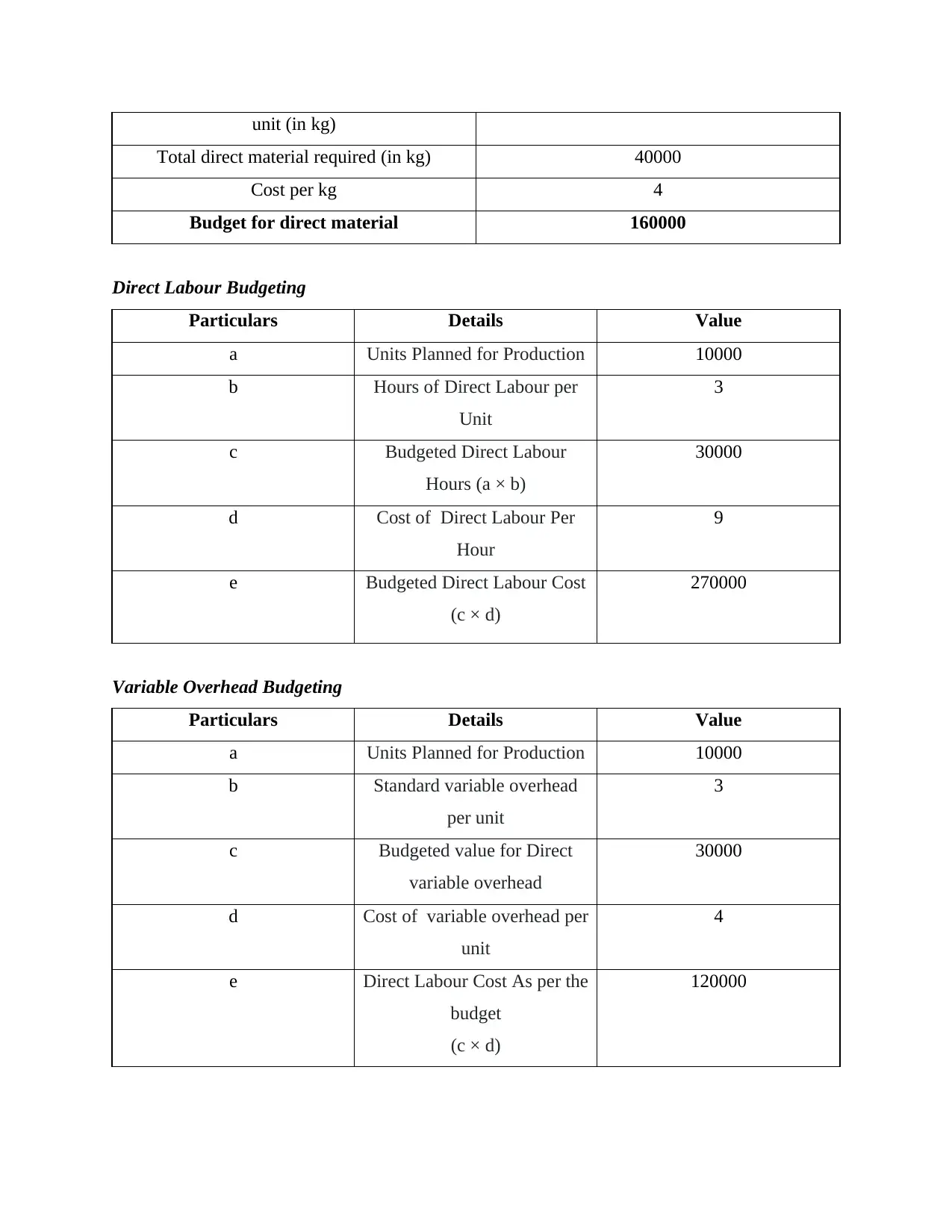

Direct Material Budgeting

Details Value

Targeted Production (in units) 10000

Requirement of Direct material per 4

Material usage variance is unfavourable for the Apparel Plc as the value is in negative. It

means that actual material used is higher than the standard material usage.

Labour Rate variance

Formula Calculation Result Variance

(Actual rate -

Standard rate) x

Actual hours worked

(10 – 9) * 3 3 F

The labour rate variance for the Apparel Plc is calculated as 3. The value is positive it

means that the variance is favourable for the firm and actual labour rate is lower than the

standard labour rate (Iwazaki, Inatsu and Takeuchi, 2021).

Labour Efficiency variance

Formula Calculation Result Variance

(Actual hours -

Standard hours) x

Standard rate

(3 * 3) * 9 0 -

The labour efficiency variance as per the above calculations is zero. It means that the

standard and actual labour efficiency is same.

Fixed Overhead Expenditure variance

Formula Calculation Result Variance

Actual fixed overhead

- Budgeted fixed

overhead

15000 – 20000 -5000 F

The fixed overhead expenditure variance is -5000. It clearly indicates that the actual fixed

overhead is less than the budgeted fixed overhead. The variance is favourable for the Apparel

Plc.

Preparation of budgets for the target of 10000 units

Direct Material Budgeting

Details Value

Targeted Production (in units) 10000

Requirement of Direct material per 4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

unit (in kg)

Total direct material required (in kg) 40000

Cost per kg 4

Budget for direct material 160000

Direct Labour Budgeting

Particulars Details Value

a Units Planned for Production 10000

b Hours of Direct Labour per

Unit

3

c Budgeted Direct Labour

Hours (a × b)

30000

d Cost of Direct Labour Per

Hour

9

e Budgeted Direct Labour Cost

(c × d)

270000

Variable Overhead Budgeting

Particulars Details Value

a Units Planned for Production 10000

b Standard variable overhead

per unit

3

c Budgeted value for Direct

variable overhead

30000

d Cost of variable overhead per

unit

4

e Direct Labour Cost As per the

budget

(c × d)

120000

Total direct material required (in kg) 40000

Cost per kg 4

Budget for direct material 160000

Direct Labour Budgeting

Particulars Details Value

a Units Planned for Production 10000

b Hours of Direct Labour per

Unit

3

c Budgeted Direct Labour

Hours (a × b)

30000

d Cost of Direct Labour Per

Hour

9

e Budgeted Direct Labour Cost

(c × d)

270000

Variable Overhead Budgeting

Particulars Details Value

a Units Planned for Production 10000

b Standard variable overhead

per unit

3

c Budgeted value for Direct

variable overhead

30000

d Cost of variable overhead per

unit

4

e Direct Labour Cost As per the

budget

(c × d)

120000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

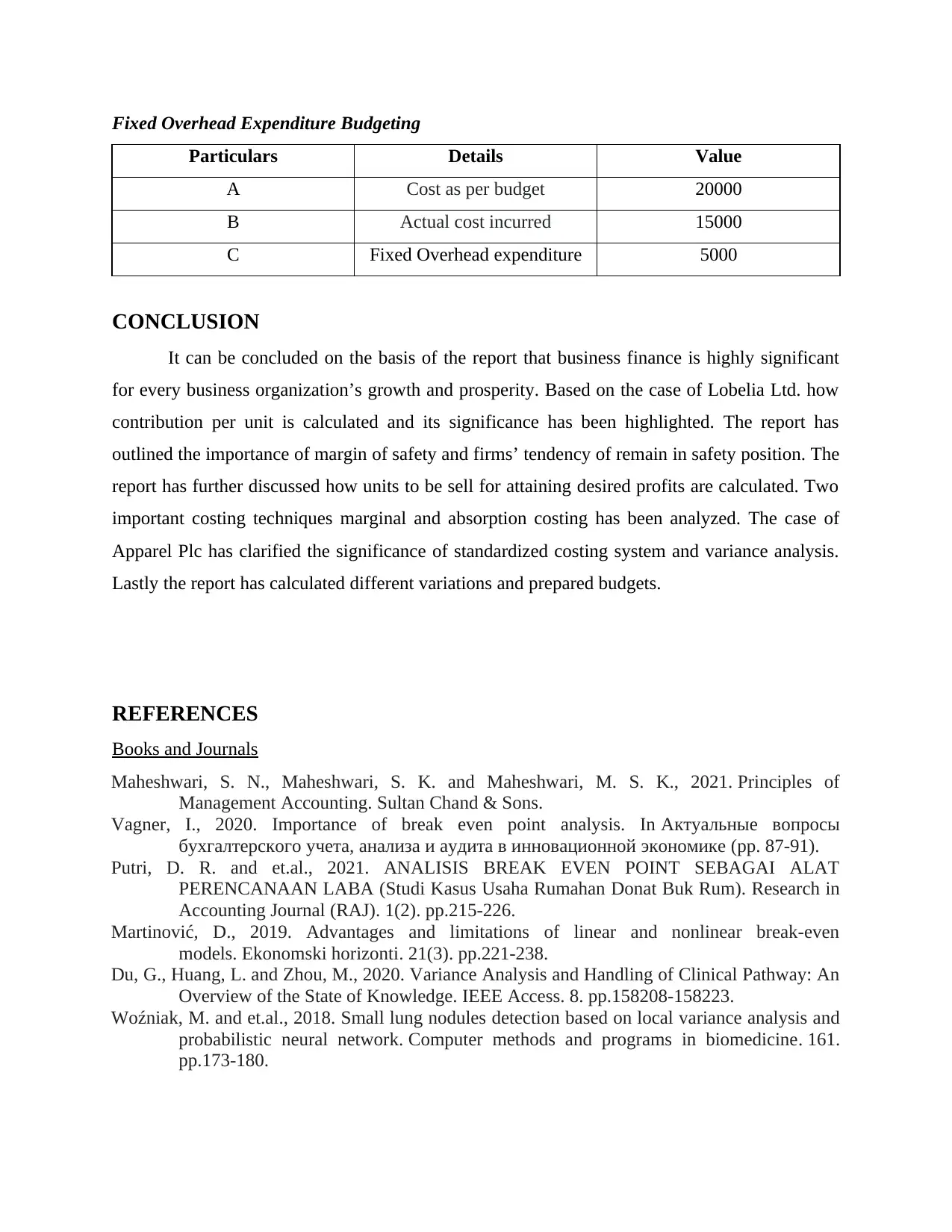

Fixed Overhead Expenditure Budgeting

Particulars Details Value

A Cost as per budget 20000

B Actual cost incurred 15000

C Fixed Overhead expenditure 5000

CONCLUSION

It can be concluded on the basis of the report that business finance is highly significant

for every business organization’s growth and prosperity. Based on the case of Lobelia Ltd. how

contribution per unit is calculated and its significance has been highlighted. The report has

outlined the importance of margin of safety and firms’ tendency of remain in safety position. The

report has further discussed how units to be sell for attaining desired profits are calculated. Two

important costing techniques marginal and absorption costing has been analyzed. The case of

Apparel Plc has clarified the significance of standardized costing system and variance analysis.

Lastly the report has calculated different variations and prepared budgets.

REFERENCES

Books and Journals

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Vagner, I., 2020. Importance of break even point analysis. In Актуальные вопросы

бухгалтерского учета, анализа и аудита в инновационной экономике (pp. 87-91).

Putri, D. R. and et.al., 2021. ANALISIS BREAK EVEN POINT SEBAGAI ALAT

PERENCANAAN LABA (Studi Kasus Usaha Rumahan Donat Buk Rum). Research in

Accounting Journal (RAJ). 1(2). pp.215-226.

Martinović, D., 2019. Advantages and limitations of linear and nonlinear break-even

models. Ekonomski horizonti. 21(3). pp.221-238.

Du, G., Huang, L. and Zhou, M., 2020. Variance Analysis and Handling of Clinical Pathway: An

Overview of the State of Knowledge. IEEE Access. 8. pp.158208-158223.

Woźniak, M. and et.al., 2018. Small lung nodules detection based on local variance analysis and

probabilistic neural network. Computer methods and programs in biomedicine. 161.

pp.173-180.

Particulars Details Value

A Cost as per budget 20000

B Actual cost incurred 15000

C Fixed Overhead expenditure 5000

CONCLUSION

It can be concluded on the basis of the report that business finance is highly significant

for every business organization’s growth and prosperity. Based on the case of Lobelia Ltd. how

contribution per unit is calculated and its significance has been highlighted. The report has

outlined the importance of margin of safety and firms’ tendency of remain in safety position. The

report has further discussed how units to be sell for attaining desired profits are calculated. Two

important costing techniques marginal and absorption costing has been analyzed. The case of

Apparel Plc has clarified the significance of standardized costing system and variance analysis.

Lastly the report has calculated different variations and prepared budgets.

REFERENCES

Books and Journals

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Vagner, I., 2020. Importance of break even point analysis. In Актуальные вопросы

бухгалтерского учета, анализа и аудита в инновационной экономике (pp. 87-91).

Putri, D. R. and et.al., 2021. ANALISIS BREAK EVEN POINT SEBAGAI ALAT

PERENCANAAN LABA (Studi Kasus Usaha Rumahan Donat Buk Rum). Research in

Accounting Journal (RAJ). 1(2). pp.215-226.

Martinović, D., 2019. Advantages and limitations of linear and nonlinear break-even

models. Ekonomski horizonti. 21(3). pp.221-238.

Du, G., Huang, L. and Zhou, M., 2020. Variance Analysis and Handling of Clinical Pathway: An

Overview of the State of Knowledge. IEEE Access. 8. pp.158208-158223.

Woźniak, M. and et.al., 2018. Small lung nodules detection based on local variance analysis and

probabilistic neural network. Computer methods and programs in biomedicine. 161.

pp.173-180.

Iwazaki, S., Inatsu, Y. and Takeuchi, I., 2021, March. Mean-variance analysis in Bayesian

optimization under uncertainty. In International Conference on Artificial Intelligence

and Statistics (pp. 973-981). PMLR.

McKinstry, S., Kininmonth, K. and Mathieson, K., 2019. The introduction and operation of

standard costing at J&P Coats Ltd., 1925–1961: an institutional

interpretation. Accounting History Review. 29(3). pp.369-389.

optimization under uncertainty. In International Conference on Artificial Intelligence

and Statistics (pp. 973-981). PMLR.

McKinstry, S., Kininmonth, K. and Mathieson, K., 2019. The introduction and operation of

standard costing at J&P Coats Ltd., 1925–1961: an institutional

interpretation. Accounting History Review. 29(3). pp.369-389.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.